Gluten-Free Bakery Premixes Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

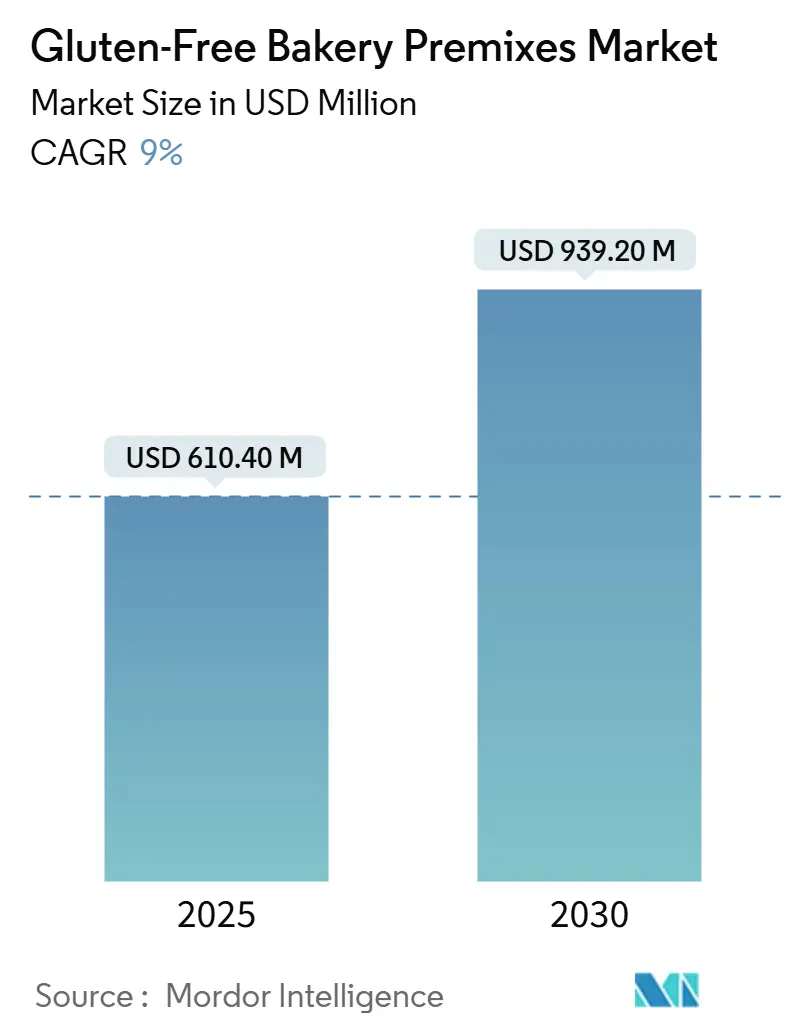

| Market Size (2025) | USD 610.40 Million |

| Market Size (2030) | USD 939.20 Million |

| Growth Rate (2025 - 2030) | 9.00% CAGR |

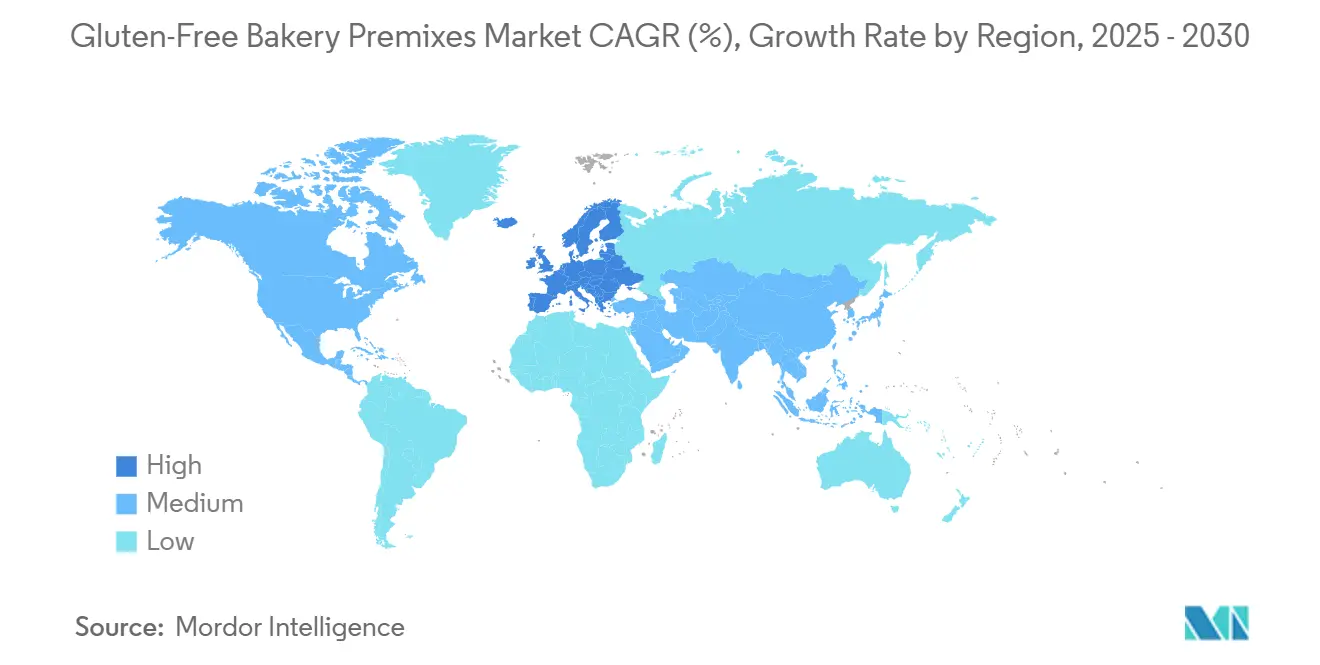

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

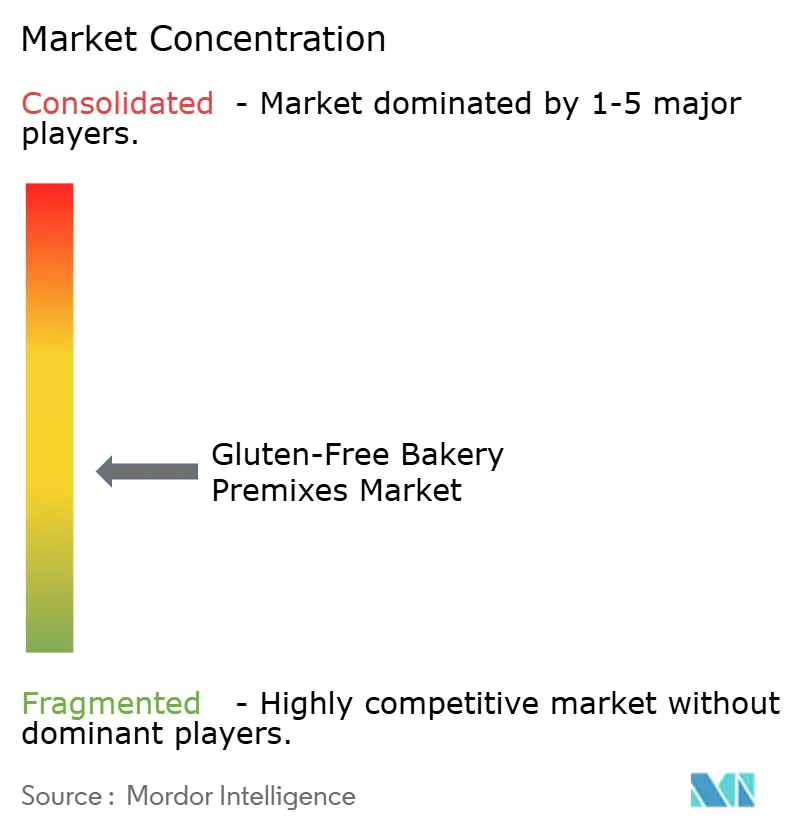

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gluten-Free Bakery Premixes Market Analysis by Mordor Intelligence

The gluten-free bakery premixes market size stands at USD 610.40 million in 2025 and is forecast to expand at a 9% CAGR, reaching USD 939.20 million by 2030. Momentum reflects the passage from a niche gluten-free bakery premixes market to a mainstream staple as diagnosis of celiac disease rises and lifestyle adoption accelerates. Bread premixes hold center stage while pancake and waffle premixes gain pace, helped by texture-enhancing enzymes that reduce the sensory gap with conventional products. Europe leads in value terms, yet Asia-Pacific posts the quickest growth, underscoring different maturity curves and regulatory environments. Digital commerce, stricter labeling laws, and the incorporation of functional ancient grains jointly keep the gluten-free bakery premixes market on a steady upward trajectory.

Key Report Takeaways

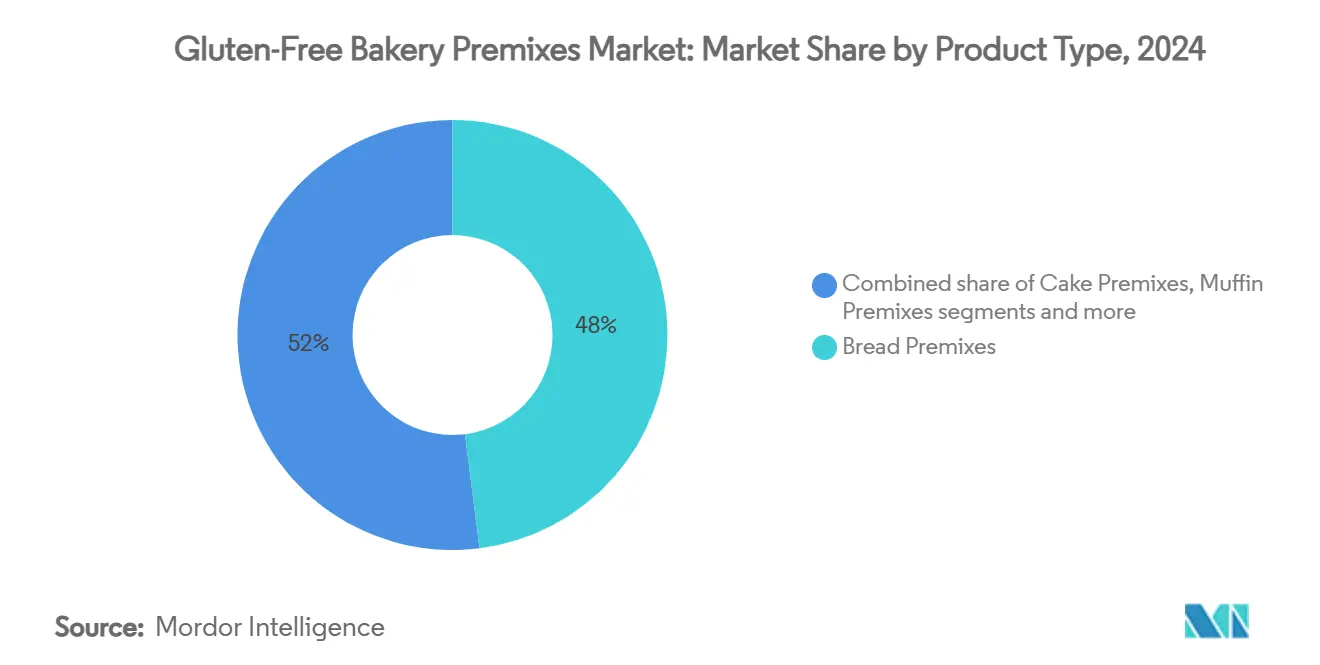

- By product type, bread premixes led with 48% of gluten-free bakery premixes market share in 2024; pancake & waffle premixes are projected to expand at a 10.40% CAGR to 2030.

- By ingredient base, rice-based premixes commanded 34% share of the gluten-free bakery premixes market size in 2024, while multigrain & ancient-grain blends are forecast to grow at 12.20% CAGR between 2025-2030.

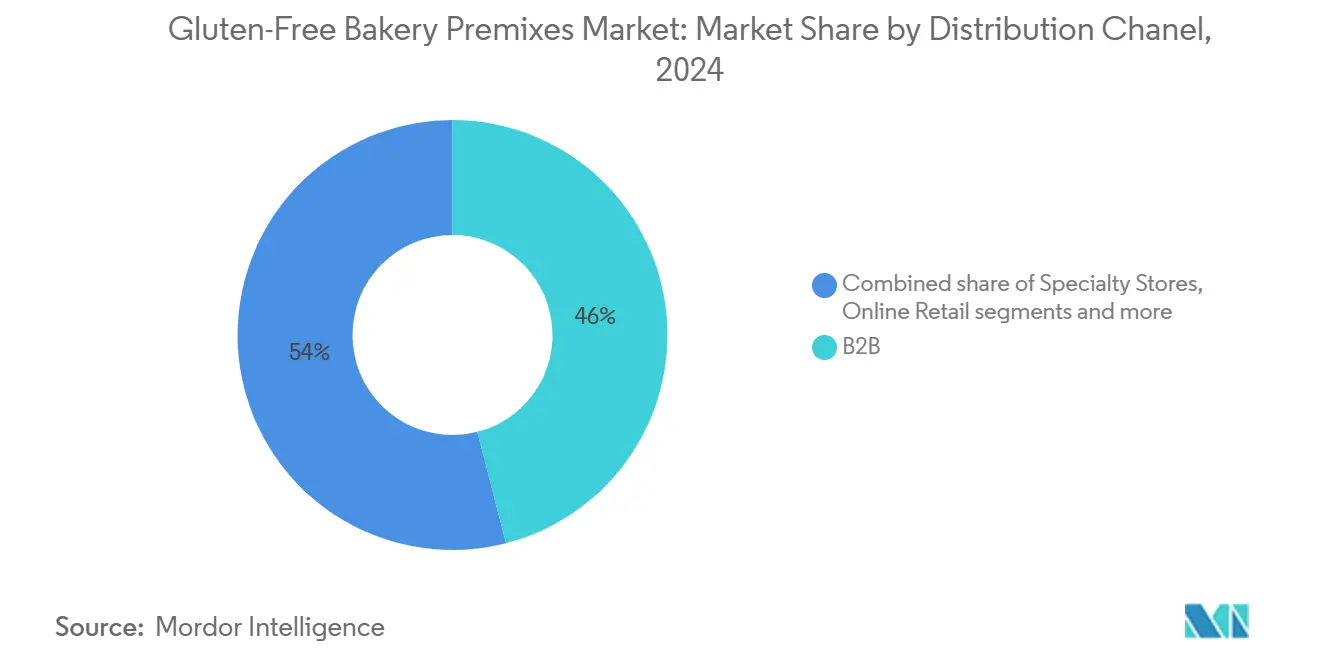

- By distribution channel, B2B sales held 46% of the gluten-free bakery premixes market in 2024; online retail is advancing at a 13.10% CAGR through 2030.

- By end-user, industrial/commercial bakeries accounted for 42% share of the gluten-free bakery premixes market size in 2024, whereas household/retail usage is projected to rise at 11.20% CAGR.

- By geography, Europe captured 32% revenue share in 2024; Asia-Pacific is forecast to post a 10.80% CAGR to 2030.

Global Gluten-Free Bakery Premixes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Gluten Sensitivity and Celiac Disease | +3.2% | Global, with higher impact in North America and Europe | Long term (≥ 5 years) |

| Growing Demand for Gluten-Free Options in Bakery Retail | +2.4% | North America and Europe, Urban centers in Asia-Pacific | Medium term (3-4 years) |

| Expansion of Specialty and Online Retail Channels | +1.8% | Global, with higher penetration in developed markets | Medium term (3-4 years) |

| Innovation in Texture and Taste of Gluten-Free Products | +1.1% | Global, with innovation centers in North America and Europe | Short term (≤ 2 years) |

| Increasing Demand for Ready-to-Eat Products | +1.5% | Global, with higher impact in urban centers | Medium term (3-4 years) |

| Clean Label and Organic Trends | +1.2% | North America and Europe, spreading to Asia-Pacific urban markets | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Gluten Sensitivity and Celiac Disease

The increasing diagnosis of celiac disease is fundamentally reshaping the gluten-free premixes market. According to the Beyond Celiac Reports, approximately 1 in 133 Americans, or about 1% of the population, has celiac disease [1]Beyond Celiac, "Celiac Disease: Fast Facts", www.beyondceliac.org. Furthermore, the organization highlights that an estimated 18 million Americans have non-celiac gluten sensitivity, which is six times the number of individuals diagnosed with celiac disease. This growing consumer base is driving the demand for gluten-free bakery products, including premixes. Governments and health organizations are increasingly focusing on raising awareness about gluten-related disorders. For instance, the U.S. Food and Drug Administration (FDA) has established guidelines for gluten-free labeling, ensuring transparency and trust among consumers [2]U.S. Food and Drug Administration, "Gluten-Free Labeling of Foods", www.fda.gov. Additionally, advancements in diagnostic tools and increased healthcare access have contributed to higher diagnosis rates, further fueling market growth. These factors are expected to sustain the expansion of the gluten-free bakery premixes market during the forecast period.

Growing Demand for Gluten-Free Options in Bakery Retail

The growing demand for gluten-free options is a significant driver in the gluten-free bakery premixes market. Rising health awareness and the increasing prevalence of gluten-related disorders, such as celiac disease and gluten intolerance, are fueling this trend. Government initiatives and regulations supporting gluten-free labeling standards are further propelling market growth. For instance, the U.S. Food and Drug Administration (FDA) has established specific guidelines for labeling gluten-free products, ensuring transparency and boosting consumer confidence. This regulatory framework has encouraged manufacturers to innovate and expand their gluten-free product portfolios, including bakery premixes. Moreover, the increasing availability of gluten-free bakery premixes in retail channels, coupled with advancements in product formulations to enhance taste and texture, is expected to drive market growth during the forecast period.

Expansion of Specialty and Online Retail Channels

Specialty and online retail channels are expanding, driving the growth of the gluten-free bakery premixes market. The increasing consumer preference for gluten-free products has led to a surge in demand across these channels. The convenience offered by online platforms, coupled with the availability of a wide range of specialty gluten-free bakery premixes, is further propelling market expansion. According to the European Commission, the implementation of regulations such as Regulation (EU) No 828/2014, which standardizes gluten-free labeling, has significantly contributed to the growth of gluten-free products in the region [3]European Commission, "Gluten-free food", www.food.ec.europa.eu. Similarly, in the United States, the Food and Drug Administration (FDA) has established guidelines for gluten-free labeling, ensuring transparency and boosting consumer confidence. These regulatory measures are encouraging manufacturers to innovate and cater to the growing demand for gluten-free bakery premixes.

Innovation in Texture and Taste of Gluten-Free Products

The gluten-free bakery premixes market is witnessing significant growth, driven by continuous innovations aimed at improving the texture and taste of gluten-free products. Manufacturers are focusing on developing formulations that closely mimic the sensory attributes of traditional baked goods, addressing consumer demand for high-quality gluten-free alternatives. The market has been expanding due to increasing awareness of gluten intolerance and celiac disease, alongside a growing preference for healthier food options. Government initiatives promoting the availability of gluten-free products and the rising number of certifications for gluten-free labeling are further supporting market growth. For instance, several countries have introduced regulations to ensure the authenticity of gluten-free claims, enhancing consumer trust and driving product adoption. These advancements are expected to play a pivotal role in shaping the market during the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Cost Compared to Conventional Premixes | -1.3% | Global, with higher impact in price-sensitive markets | Medium term (3-4 years) |

| Limited Shelf Life of Natural, Gluten-Free Premixes | -0.8% | Global, greater impact in regions with underdeveloped cold chains | Short term (≤ 2 years) |

| Limited Availability of Raw Materials | -0.9% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Medium term (3-4 years) |

| Health Concerns with Gluten-Free Diets | -0.6% | North America and Europe, educated consumer segments | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Higher Cost Compared to Conventional Premixes

The persistent price premium of gluten-free bakery premixes remains a significant market constraint, limiting adoption particularly in price-sensitive segments and emerging economies. Production economics fundamentally disadvantage gluten-free formulations, as they typically require more expensive alternative flours, additional functional ingredients to replicate gluten's properties, and dedicated manufacturing facilities to prevent cross-contamination. According to industry reports, the cost of gluten-free flours, such as almond or coconut flour, is approximately 2-3 times higher than traditional wheat flour. Additionally, the need for specialized equipment and stringent quality control measures further escalates production costs. For instance, the European Commission has highlighted that gluten-free product manufacturing often involves higher operational expenses due to compliance with strict food safety regulations. These factors collectively contribute to the higher retail prices of gluten-free bakery premixes, making them less accessible to a broader consumer base.

Limited Shelf Life of Natural, Gluten-Free Premixes

The limited shelf life of natural, gluten-free premixes acts as a significant restraint in the gluten-free bakery premixes market. These premixes, often made without artificial preservatives, are prone to spoilage and quality degradation over time. This challenge is particularly critical for manufacturers and retailers aiming to maintain product quality during storage and distribution. Natural premixes typically have a shelf life ranging from 6 to 12 months, depending on storage conditions and packaging. This limitation increases the logistical complexities and costs associated with inventory management. Furthermore, regulatory bodies, such as the Food and Drug Administration (FDA), emphasize the importance of accurate labeling and adherence to food safety standards, which further impacts the production and distribution processes. The need for innovative preservation techniques and advanced packaging solutions is becoming increasingly vital to address these challenges and extend the shelf life of gluten-free premixes without compromising their natural composition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bread Premixes Lead Despite Diversification

In 2024, bread premixes commanded a dominant 48% share of the gluten-free bakery premixes market, buoyed by daily consumption trends and innovations in dough rheology. The market for gluten-free bread premixes is set to enjoy robust double-digit value growth, thanks to enzymatic systems producing softer crumbs and taller loaves. These advancements cater to the increasing demand for gluten-free bread, driven by health-conscious consumers and those with dietary restrictions. Bread premixes continue to play a pivotal role in the gluten-free bakery segment, offering convenience, consistent quality, and the ability to replicate traditional bread textures and flavors. Additionally, the growing adoption of gluten-free diets across various demographics further supports the expansion of this segment.

Riding the wave of breakfast and snacking moments, pancake and waffle premixes are on track to achieve a 10.40% CAGR through 2030. Quinoa-based formulations not only enhance micronutrient density but also ensure a fluffy texture, meeting consumer preferences for healthier and indulgent options. These premixes align with the growing trend of quick and easy meal solutions, making them a popular choice for busy lifestyles. The versatility of pancake and waffle premixes further supports their growth, as they cater to diverse culinary applications and occasions. With increasing consumer interest in gluten-free breakfast options, these premixes are gaining traction in both retail and foodservice channels, offering a balance of nutrition and convenience.

By End-User: Industrial Efficiency Meets Retail Convenience

In 2024, industrial bakeries commanded a dominant 42% share of the gluten-free bakery premixes market, leveraging scale economics and stringent process controls. With centralized quality assurance, these bakeries produce contaminant-free outputs, earning the trust of grocery chains. The ability to maintain consistent quality and meet large-scale demand has positioned industrial bakeries as key players in the market, catering to both retail and wholesale requirements. Their established infrastructure and adherence to strict standards ensure reliability and efficiency in production, further solidifying their market presence. Additionally, industrial bakeries benefit from advanced machinery and automation, enabling them to produce a wide variety of gluten-free products while maintaining cost efficiency.

On the other hand, household adoption of gluten-free bakery premixes has witnessed significant growth, driven by a surge in home baking trends that gained momentum during the pandemic. This segment is growing at an impressive 11.20% CAGR as more consumers explore gluten-free baking at home. E-commerce platforms have played a pivotal role in this growth by offering convenient access to premix kits. These kits often include clear instructions, making them user-friendly for first-time bakers and encouraging experimentation among households. The availability of diverse product options, including organic and allergen-free variants, has further fueled interest in this segment.

By Distribution Channel: Digital Transformation Accelerates Access

In 2024, B2B sales in the Gluten-Free Bakery Premixes market accounted for 46% of the turnover, driven by direct shipments to bakeries and food manufacturers. These businesses rely on gluten-free premixes to streamline production processes and meet the growing consumer demand for gluten-free baked goods. The B2B segment benefits from long-term contracts and bulk purchasing, which ensure consistent supply and cost efficiency for manufacturers and bakeries. Additionally, the rising awareness of gluten-related health issues has prompted bakeries and food manufacturers to expand their gluten-free product portfolios, further driving demand in this segment.

Meanwhile, online retail in the market is advancing at a robust 13.10% CAGR, emerging as a key growth driver. Interactive e-commerce platforms combine product catalogs with engaging recipe content, creating a unique shopping experience for consumers. These platforms foster brand loyalty by building communities around gluten-free baking, encouraging repeat purchases. The convenience of online shopping, coupled with the availability of detailed product information and customer reviews, has significantly boosted the adoption of gluten-free bakery premixes among individual consumers and small-scale bakers. Furthermore, the increasing penetration of smartphones and internet connectivity has expanded the reach of online retail, making gluten-free premixes accessible to a broader audience.

By Ingredient Base: Ancient Grains Disrupt Rice Dominance

In 2024, rice-based premixes accounted for a 34% market share in the gluten-free bakery premixes market. Their popularity stems from their mild flavor, which appeals to a wide range of consumers, and their broad availability, making them a staple choice for manufacturers. These premixes are particularly favored for their versatility in creating gluten-free baked goods, such as bread, cakes, and cookies, catering to the growing demand for gluten-free options among health-conscious consumers and those with dietary restrictions. Additionally, rice-based premixes are often perceived as a cost-effective option for manufacturers, further contributing to their widespread adoption in the market.

Meanwhile, multigrain and ancient-grain blends are forecast to lead the market growth with a projected CAGR of 12.20% during the forecast period. These blends are gaining traction due to their ability to enhance the nutritional profile of gluten-free baked goods by boosting fiber and mineral intake. Consumers are increasingly drawn to these formulations for their health benefits, as they incorporate nutrient-rich grains like quinoa, amaranth, and millet. This trend aligns with the rising preference for functional and wholesome food products, driving the adoption of multigrain and ancient-grain premixes in the gluten-free bakery segment. Furthermore, these blends cater to the growing consumer interest in diverse and innovative flavors, making them a preferred choice for premium and health-focused bakery products.

Geography Analysis

In 2024, Europe commands a 32% market share in the gluten-free bakery premixes market, driven by advanced regulatory frameworks, high celiac disease diagnosis rates, and sophisticated consumer preferences. The region's dominance is further supported by a well-established ecosystem of specialty retailers and foodservice establishments catering to gluten-free consumers. Key markets such as the United Kingdom, Germany, and Italy play a pivotal role in maintaining this leadership, with a strong focus on innovation, product availability, and consumer education. The increasing adoption of gluten-free diets, even among non-celiac individuals, further strengthens the market in this region, as consumers prioritize health and wellness.

Asia-Pacific emerges as the fastest-growing region in the gluten-free bakery premixes market, with a projected CAGR of 10.80% from 2025-2030. This growth is attributed to increasing diagnosis rates of gluten-related disorders, rising health consciousness, and the rapid expansion of retail infrastructure. Urban centers in countries like China, Japan, and India are at the forefront of this growth, driven by changing dietary habits, increasing disposable incomes, and a notable rise in wheat consumption. These factors are contributing to a higher prevalence of gluten-related health issues, thereby boosting demand for gluten-free bakery premixes. Additionally, the growing influence of Western dietary trends and the expansion of e-commerce platforms are making gluten-free products more accessible to consumers in the region.

North America represents a mature yet steadily growing market for gluten-free bakery premixes. The region benefits from high consumer awareness and a well-developed retail infrastructure, which ensures widespread availability of gluten-free products. Additionally, the FDA's stringent standards for gluten-free labeling enhance consumer confidence and trust in the products. This regulatory support, combined with a growing focus on health and wellness, continues to drive the market forward in the United States and Canada. The increasing prevalence of gluten intolerance and celiac disease, coupled with a rising trend of adopting gluten-free diets for lifestyle reasons, further propels market growth. Moreover, the presence of key market players and their efforts in product innovation and marketing contribute to the sustained expansion of the gluten-free bakery premixes market in the region.

Competitive Landscape

The Global Gluten-free Bakery Premixes Market, with a concentration score of 4 out of 10, reflects a moderately competitive landscape. This environment strikes a balance between the advantages enjoyed by established players and the opportunities available for new entrants. Established companies like Associated British Foods plc, Puratos Group, and Bakels Group leverage their integrated supply chains and extensive distribution networks to maintain their market positions. At the same time, they are heavily investing in research and development to cater to evolving consumer preferences, particularly the demand for clean labels and improved nutritional profiles. These efforts underscore the importance of innovation in sustaining competitiveness in this market.

Technological differentiation and vertical integration are emerging as key strategic priorities for companies operating in this market. By focusing on these areas, businesses aim to secure a reliable supply of specialized ingredients, which are critical for producing gluten-free bakery premixes. This approach not only enhances operational efficiency but also strengthens their ability to meet the growing demand for high-quality, gluten-free products. Additionally, companies are increasingly adopting strategies that combine organic growth through product innovation with inorganic growth via acquisitions, enabling them to expand their market presence and diversify their product portfolios.

Strategic acquisitions have played a significant role in shaping the competitive dynamics of the market. For instance, Associated British Foods has made notable acquisitions, including Omega Yeast Labs LLC, Mapo (an Italian manufacturer of premium frozen baked goods), and Romix, a specialist blender of baking ingredients. These acquisitions highlight the importance of expanding capabilities and securing access to specialized expertise in the gluten-free bakery premixes market. Such moves not only strengthen the acquiring companies' market positions but also enhance their ability to address the diverse needs of consumers in this growing market.

Gluten-Free Bakery Premixes Industry Leaders

-

Associated British Foods plc

-

Watson Inc,

-

Caremoli SPA

-

Puratos Group

-

Bakels Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Modern Mills Company unveiled plans to expand its wheat milling capacity by 1,250 metric tons per day by Q2 2025, introducing specialty flours including gluten-free options to address the growing demand from health-conscious consumers.

- June 2024: Corbion introduced Ultra Fresh® Premium 1650 GF enzyme product to enhance the quality and shelf life of gluten-free products, addressing key challenges in texture and shelf life issues, particularly in products like bread, tortillas, cookies, and pizza crusts.

- May 2024: Dawn Foods, launched two new products as part of its Total Cake Solutions concept. The first is the Dawn Yogurt Cake Mix, which delivers a tender and fluffy texture with a hint of yogurt flavor. This versatile mix can be used to make a variety of baked goods, from loaf cakes to muffins. The second product is the Dawn Exceptional Yuzu Compound, a flavoring paste that brings the unique taste of yuzu, a blend of lemon and grapefruit with herbal and floral notes, to bakers' recipes.

- March 2024: Pillsbury Baking, a leading name in the baking industry, has unveiled two new product lines. The first, the Creamy Cake Mix Line, introduces two flavors: Moist Supreme Creamy Almond and Moist Supreme Creamy Vanilla. These mixes promise a refined and creamy experience, with the almond variant delivering a subtly fruity sweetness, while the vanilla offers a rich, dreamy taste.

Global Gluten-Free Bakery Premixes Market Report Scope

Gluten-free bakery premixes are dry ingredient mixtures designed for baking gluten-free bread, cakes, cookies, and other baked goods.

The global gluten-free bakery premixes market is segmented by product type, end user, distribution channel, ingredient base and geography. By product type the market is segmented into bread premixes, cake premixes, muffin premixes, pancakes & waffle premixes, cookie & biscuit premixes and others. Based on end-user, the market is segmented into industrial/commercial, foodservice & household & retail. By distribution channel, the market is segmented into B2B, hypermarkets & supermarkets, speciality stores, offline stores and others. By ingredient base, the market is segmented into rice-based premixes, corn-based premixes, nut & seed based and multigrain & ancient grain blends. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, market sizing and forecast have been done based on value (USD million).

| Bread Premixes |

| Cake Premixes |

| Muffin Premixes |

| Pancake and Waffle Premixes |

| Cookie and Biscuit Premixes |

| Others |

| Industrial/Commercial |

| Foodservice and HoReCa |

| Household/Retail |

| B2B |

| Hypermarkets and Supermarkets |

| Specialty Stores |

| Online Retail |

| Others |

| Rice-Based Premixes |

| Corn-Based Premixes |

| Nut and Seed-Based |

| Multigrain and Ancient-Grain Blends |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Columbia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria' | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bread Premixes | |

| Cake Premixes | ||

| Muffin Premixes | ||

| Pancake and Waffle Premixes | ||

| Cookie and Biscuit Premixes | ||

| Others | ||

| By End-User | Industrial/Commercial | |

| Foodservice and HoReCa | ||

| Household/Retail | ||

| By Distribution Channel | B2B | |

| Hypermarkets and Supermarkets | ||

| Specialty Stores | ||

| Online Retail | ||

| Others | ||

| By Ingredient Base | Rice-Based Premixes | |

| Corn-Based Premixes | ||

| Nut and Seed-Based | ||

| Multigrain and Ancient-Grain Blends | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Columbia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria' | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the gluten-free bakery premixes market?

The gluten-free bakery premixes market size is valued at USD 610.40 million in 2025.

How fast will the market grow until 2030?

The market is forecast to advance at a 9% CAGR, reaching USD 939.20 million by 2030.

Which product category leads the market?

Bread premixes dominate with 48% gluten-free bakery premixes market share in 2024.

What region shows the strongest growth outlook?

Asia-Pacific is projected to expand at a 10.80% CAGR between 2025 and 2030.

Page last updated on: