Batter And Breader Premixes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

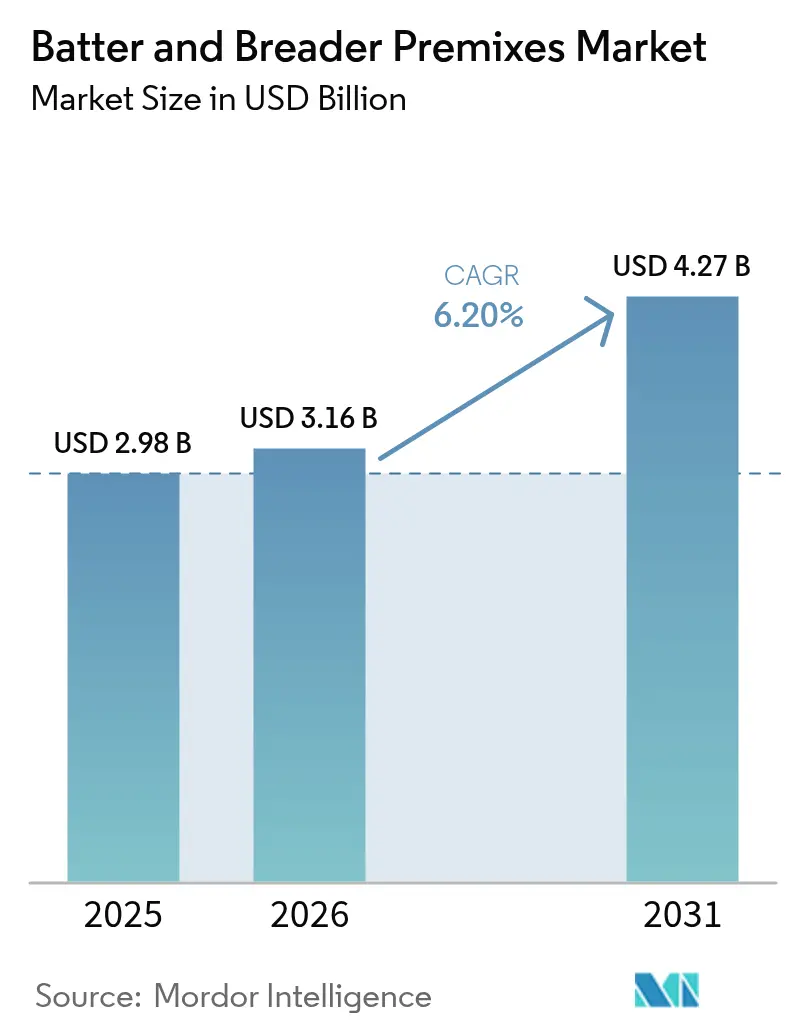

| Market Size (2026) | USD 3.16 Billion |

| Market Size (2031) | USD 4.27 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

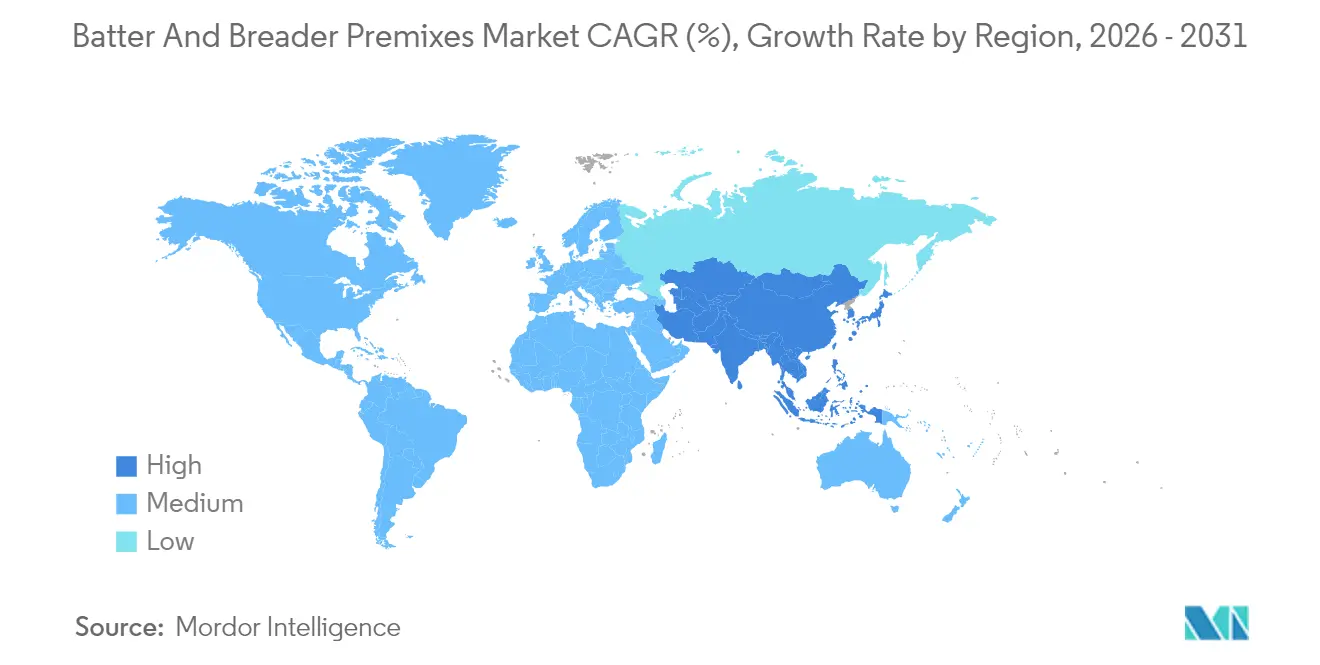

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Batter And Breader Premixes Market Analysis by Mordor Intelligence

The batter and breader premixes market size is expected to grow from USD 2.98 billion in 2025 to USD 3.16 billion in 2026 and is forecast to reach USD 4.27 billion by 2031 at 6.20% CAGR over 2026-2031. The significant expansion of quick-service restaurant menus globally has intensified the demand for high-performance coating formulations that maintain consistent texture and appearance during large-scale food production operations. The substantial growth in frozen and ready-to-cook meal segments has prompted suppliers to develop advanced starch-based systems that effectively maintain crispness after reheating while demonstrating resilience through multiple freeze-thaw cycles. The increasing disposable income levels in emerging economies have facilitated the introduction of premium coating formulations that deliver superior adhesion properties alongside enhanced taste, texture, and visual appeal. In response to market volatility, manufacturers are implementing comprehensive vertical integration strategies and establishing long-term commodity hedging mechanisms to effectively manage wheat price fluctuations and preserve operating margins across their production cycles.

Key Report Takeaways

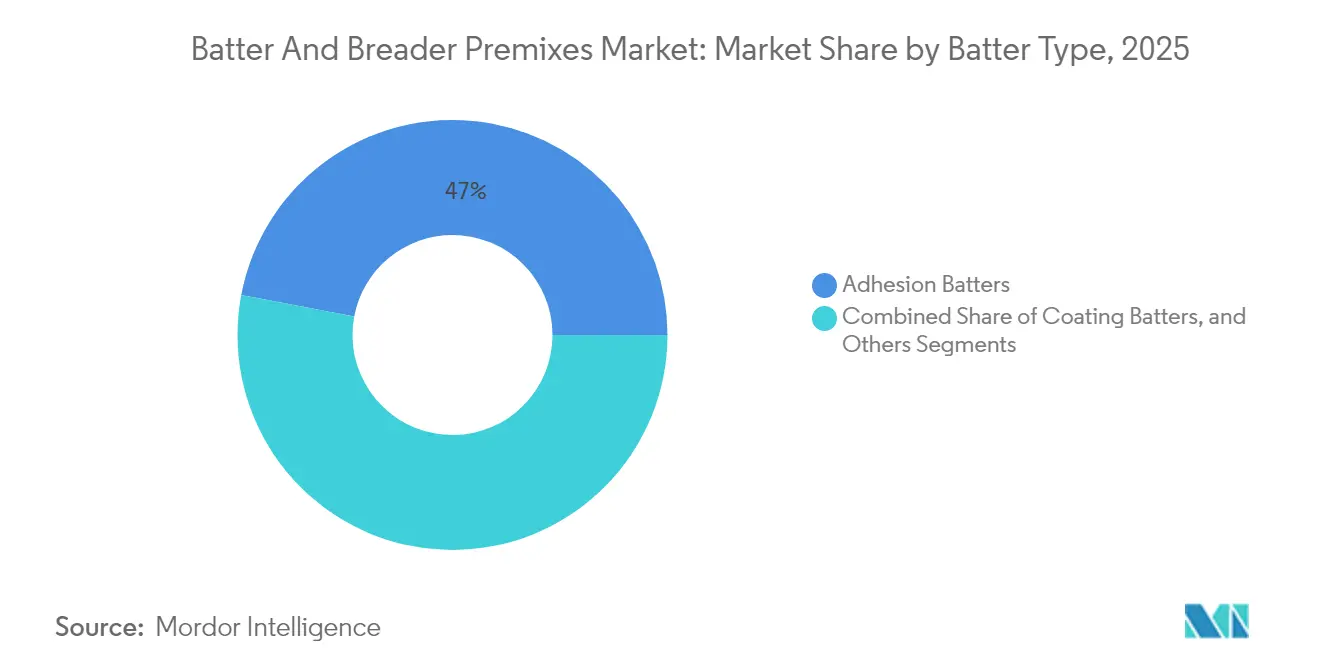

- By batter type, adhesion batters held 47.02% revenue share of the batter and breader premixes market in 2025, while coating batters are projected to register the fastest 7.42% CAGR through 2031.

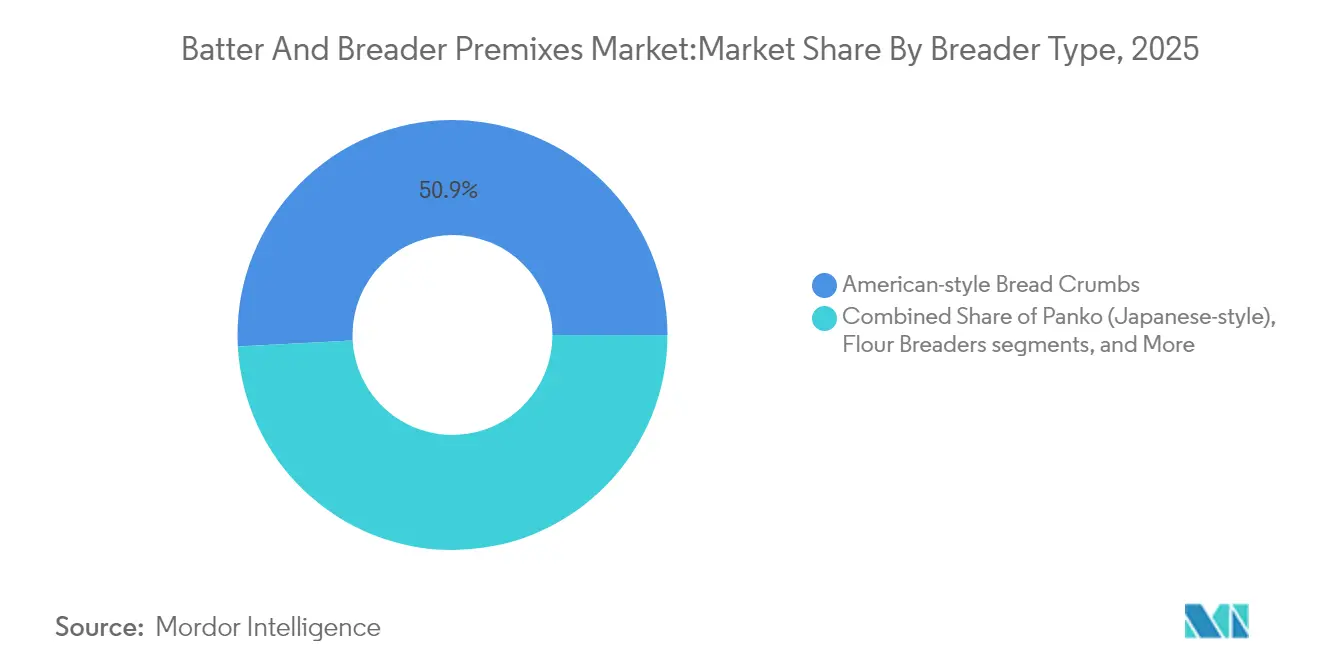

- By breader type, American-style crumbs led with 50.86% revenue share in 2025; Japanese Panko crumbs are expected to expand at a 9.08% CAGR to 2031.

- By application, processed meat and seafood accounted for 48.44% revenue share of the batter and breader premixes market in 2025; savory snacks are forecast to grow at a 6.32% CAGR between 2026 and 2031.

- By geography, North America dominated with a 36.16% share in 2025, whereas Asia-Pacific is set to post the highest 8.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Batter And Breader Premixes Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenience, frozen, and ready-to-cook meals | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion of quick-service restaurants (QSRs) and food-service chains | +1.2% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Rising consumption of processed meat and seafood products | +0.9% | Global, particularly strong in North America & APAC | Medium term (2-4 years) |

| Growth in global snacking culture and popularity of finger foods | +0.7% | Global, led by urban centers in developed markets | Short term (≤ 2 years) |

| Increasing consumer preference for enhanced taste and texture in coated foods | +0.6% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Rise in demand for specialty coating systems for plant-based protein products | +0.5% | North America & Europe, early adoption in urban APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Convenience, Frozen, and Ready-to-Cook Meals

The growth of convenience foods has led manufacturers to adjust coating systems to maintain quality during freeze-thaw cycles and ensure good texture after reheating. Conagra's Future of Frozen Food 2025 report states that the U.S. frozen food market has grown to USD 91.3 billion, with rising demand for air fryer-compatible products requiring specific coating methods. This shift has driven the creation of modified starch-based coating systems that prevent moisture loss and keep food crisp during frozen storage. The FDA's approval of food starch-modified formulations for batter applications provides the regulatory framework for manufacturers to improve texture retention [1]Organisation for Economic Co-operation and Development, "Household disposable income" oecd.org. Current coating technologies use nano-emulsion systems and composite materials to enhance barrier properties, meeting consumer expectations for high-quality frozen food. These advancements help coating manufacturers benefit from consumers' willingness to pay more for premium convenience foods.

Expansion of Quick-Service Restaurants (QSRs) and Food-Service Chains

Quick-service restaurant (QSR) chains are increasingly adopting coating systems that ensure consistent food preparation across different markets and workforce skill levels. This trend has increased the demand for premixed coatings that provide uniform results despite variations in local preparation methods. US Foods' 2024 product line includes Taiwanese-style salt and pepper popcorn chicken with a light coating and par-fried preparation, which reduces preparation time by 40% while maintaining menu flexibility. QSRs are implementing coating systems that combine multiple functions - adhesion, texture, flavor enhancement, and appearance - in a single application step. As QSR chains expand into new markets, they require coating systems that balance local flavor preferences with brand consistency. Recent patents in coating formulations indicate the industry's focus on developing adaptable systems that maintain operational efficiency across markets with varying labor costs and workforce capabilities.

Rising Consumption of Processed Meat and Seafood Products

The processed meat industry has shifted toward premium products, increasing the demand for coating systems that enhance taste and texture while ensuring meat preservation. FDA regulations require frozen breaded shrimp to contain at least 65% shrimp content, which has led manufacturers to develop coating systems that optimize product value within regulatory limits. These regulations have driven innovations in coating efficiency, as manufacturers aim to achieve maximum sensory benefits with minimal coating usage. Manufacturers face the technical challenge of developing coating systems that perform consistently across various protein bases, including conventional meat, fish, and plant-based alternatives. Modern coating formulations incorporate functional proteins, such as zein and modified wheat proteins, to improve binding capabilities and nutritional content while meeting clean-label demands.

Growth in Global Snacking Culture and Popularity of Finger Foods

Changes in snacking preferences have transformed coating system requirements, with emphasis on convenience, cleanliness during consumption, and aesthetic appeal. Mini portions show consistent year-over-year growth, as reported by Conagra, reflecting consumers' shift toward smaller, more frequent meals that include coated finger foods. This consumer behavior has prompted the development of coating systems specifically engineered for handheld foods, featuring enhanced coating adhesion and regulated oil migration during storage. Visual appearance has become essential, driving manufacturers to create coating systems that maintain uniform color and texture under different lighting conditions. Technological developments focus on coating systems that provide stronger flavor profiles and superior mouthfeel in smaller portions to meet consumer expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw-material prices | -0.8% | Global, particularly acute in regions dependent on wheat imports | Short term (≤ 2 years) |

| Price sensitivity among mass food-service operators | -0.6% | Emerging markets and cost-focused segments globally | Medium term (2-4 years) |

| Stringent regulatory standards on food additives and labeling | -0.4% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| Consumer concerns over artificial ingredients and preservatives in premixes | -0.3% | Developed markets, urban centers in emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw-Material Prices

Raw material price volatility affects the coating supply chain, as wheat flour price fluctuations impact product margins and customer relationships. Coating manufacturers have responded by developing new formulations that incorporate alternative starches and protein sources to reduce wheat flour dependency. Global commodity market factors, including weather conditions, trade policies, and currency fluctuations, create variable cost structures that affect long-term customer agreements. Ingredion's 2024 financial results demonstrated this impact, with favorable pricing in multi-year contracts driving 74% operating income growth in their Food and Industrial Ingredients segment. Companies manage price risk through procurement strategies that include derivative instruments and diversified supply sources. Research and development efforts focus on creating flexible coating systems that enable ingredient substitutions while maintaining product performance.

Price Sensitivity Among Mass Food-Service Operators

The foodservice industry's margin pressures have created a market segmentation between premium and economy coating systems. Quick-service restaurants require coatings that enhance protein quality perception while maintaining cost efficiency. Manufacturers have responded by developing formulations that deliver consistent results across different protein qualities. The industry has incorporated functional ingredients, including modified starches and protein concentrates, in coating systems to improve yield and reduce waste, lowering per-serving costs. Coating systems must also offer simple application methods and consistent results to reduce training needs and operational complexity. In response to operational cost concerns and consumer health preferences, manufacturers have developed coating systems optimized for air frying applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breader Type: American-Style Dominance Faces Asian Innovation Challenge

American-style bread crumbs held a 50.86% market share in 2025, supported by established supply chains and widespread adoption in major food service markets. Panko Japanese-style breaders are growing at 9.08% CAGR through 2031, driven by consumer demand for their lighter, crispier texture. This growth indicates changing consumer preferences, with texture becoming a significant factor in coated food products. Manufacturing advancements have enabled the mass production of Panko while preserving its characteristic airy structure that provides superior crispness and controlled oil absorption.

Flour breaders serve a specific purpose in applications that require thin coatings, particularly in products where the protein component needs to remain prominent. The premium segment comprises specialty and seasoned breadcrumbs, which incorporate herbs, spices, and functional ingredients to enhance both flavor and appearance. The market is segmented between basic commodity applications and premium products that emphasize sensory attributes.

By Application: Processed Proteins Drive Volume While Snacks Capture Growth

Processed meat and seafood products dominate the coating systems market with a 48.44% share in 2025. These systems enhance product value and extend shelf life for protein products. The segment's prominence results from coating systems' effectiveness in improving yield, minimizing cooking losses, and delivering consistent sensory attributes across varying protein qualities. Savory snacks represent the fastest-growing application segment, with a projected CAGR of 6.32% through 2031. This growth reflects the expansion of snacking culture and increased demand for portable, clean-consumption formats enabled by coating systems. The market shows a shift from traditional meal applications toward frequent, smaller consumption occasions favoring coated snack foods.

Coating systems in frozen and ready-to-eat meals maintain structural integrity during freeze-thaw cycles and ensure optimal texture after reheating. Research by Conagra indicates that air fryer compatibility drives growth in frozen foods, leading to the development of specific coating systems for air fryer preparation. In bakery products, coatings function as moisture barriers and enhance texture, while in plant-based proteins, they provide specialized formulations for desired sensory attributes. These applications showcase how coating systems deliver multiple benefits, including product protection, texture enhancement, flavor delivery, and visual appeal across various food categories.

By Batter Type: Adhesion Systems Lead Market Foundation

Adhesion batters held a 47.02% market share in 2025, demonstrating their essential role in maintaining coating integrity across various protein substrates and cooking methods. These systems prevent coating separation during processing, storage, and consumption, making them essential for large-scale food manufacturing operations. Coating batters, while currently holding a smaller market share, are projected to grow at 7.42% CAGR through 2031. This growth is driven by increasing consumer demand for enhanced texture and visual appeal in coated foods, indicating a shift toward premium product positioning.

Recent developments in adhesion batter formulations focus on maintaining binding effectiveness across varying moisture conditions and protein types, particularly in plant-based protein applications. These formulations include modified starch systems that work effectively with both animal proteins and plant-based alternatives. The remaining batter types present opportunities in specialized applications, including gluten-free and clean-label systems for specific dietary needs. This evolution aligns with food industry trends toward customization, where manufacturers balance functional performance with natural ingredients and improved sensory attributes.

Geography Analysis

North America dominated the batter and breader premixes market with a 36.16% share in 2025. This leadership position stems from extensive quick-service restaurant networks, efficient cold-chain logistics, and established FDA regulatory frameworks. The market benefits from direct integration between coating suppliers and protein processors through long-term contracts, ensuring predictable demand. The region's focus on standardized premixes enables consistent performance across corporate and franchise operations, maintaining regular replacement cycles.

Asia-Pacific is expected to grow at 8.18% CAGR through 2031. The growth is driven by increasing disposable income and expansion of cloud kitchens across China, India, and Southeast Asia, generating high-volume purchases of batters that combine Western textures with regional flavors. Japanese Panko manufacturing expertise is expanding across the region through licensing agreements and joint ventures. The development of cold-chain infrastructure by governments is creating new distribution channels for specialized coatings as frozen food adoption increases.

Europe maintains steady growth, influenced by strict clean-label regulations requiring natural ingredients and colors. Manufacturers gain market advantage by emphasizing sustainable grain sourcing and reduced environmental impact in production. Latin America and the Middle East and Africa show growth potential, though price remains a key factor. Suppliers combining technical support with product offerings are establishing relationships with early adopters, preparing for increased adoption as cold-storage infrastructure develops.

Competitive Landscape

The batter and breader premixes market maintains a moderately fragmented structure, with major companies integrating ingredient expertise and supply chain management. Key manufacturers, such as McCormick and Company Inc., Archer Daniels Midland Co., and Bunge Ltd., are not only broadening their foothold in emerging markets but are also acquiring specialty starch manufacturing capabilities and crafting formulations that align with plant-based proteins.

McCormick and Company Inc. asserts its dominance through its Flavor Solutions division, which recorded a 14% operating-income surge in 2024. This uptick is attributed to McCormick's strategic melding of coating systems with seasoning products, offering food manufacturers a holistic flavor solution. Newly Weds Foods Inc. bolsters its market stance with regional innovation centers tailored to test breading applications on local protein varieties. This approach not only shortens product development timelines but also guarantees solutions tailored to specific markets.

Mid-sized manufacturers have established strong market positions by focusing on specialized segments, particularly in allergen-free batters and ancient grain-based breadings. This specialization has enabled them to capture significant market share in natural and organic product categories. The market's evolution is further characterized by the introduction of subscription-based formulation services, offering manufacturers continuous optimization support.

Batter And Breader Premixes Industry Leaders

-

McCormick and Company Inc.

-

Newly Weds Foods Inc.

-

Archer Daniels Midland Co.

-

Bunge Ltd.

-

Solina

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Solina acquired a majority stake in Bowman Ingredients Thailand to expand its Asian market presence. Bowman Ingredients Thailand, which specializes in food industry coating solutions, provides customized products to regional and international customers.

- April 2025: Ingredion Incorporated invested more than USD 100 million to expand its Indianapolis facility to increase the production capacity of texture and coating solutions.

- February 2024: Bunge Ltd. acquired Viterra, a privately held global trader of grain, oilseeds, and meal, for USD 8.2 billion. This acquisition strengthens Bunge's raw material procurement capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Batter and breader premixes are dry, shelf-stable blends of flours, starches, spices, and functional additives that coat meat, seafood, poultry, vegetables, or snacks before frying or baking, with all values captured at manufacturer selling price in nominal USD. According to Mordor Intelligence, only factory-produced premixes sold in bulk or retail packs are counted; in-house blends prepared inside restaurants or processors fall outside the value pool.

Scope exclusion: Wet tempura slurries mixed on-site and flavored marinades that double as coatings are not included.

Segmentation Overview

-

By Batter Type

- Adhesion Batters

- Coating Batters

- Other Batter Types

-

By Breader Type

- American-style Bread Crumbs

- Panko (Japanese-style)

- Flour Breaders

- Specialty and Seasoned Crumbs

- Other Breader Types

-

By Application

- Frozen and Ready-to-Eat Meals

- Savory Snacks

- Processed Meat and Seafood Products

- Other Food Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed premix formulators, contract coaters, quick-service menu developers, and grocery buyers across North America, Europe, and Asia-Pacific. These discussions verified average usage rates per kilogram of protein, regional price pass-through, and the speed at which gluten-free variants penetrate retail shelves, closing gaps left by desk work.

Desk Research

We began by mapping production and trade flows through public sources such as UN Comtrade shipment codes, the USDA's Livestock and Poultry Outlook, Eurostat PRODCOM food mixes, and the FAO Food Balance Sheets, which illustrate protein volumes that drive coating demand. Supplementary insights were drawn from industry magazines like Meat & Poultry and Snack Food & Wholesale Bakery, plus company 10-Ks posted on EDGAR. Paid databases, D&B Hoovers for revenue splits and Dow Jones Factiva for deal news, helped us size leading suppliers. This list is illustrative; many additional references informed data collection and validation.

Market-Sizing & Forecasting

A top-down reconstruction starts with edible animal protein output and frozen snack tonnage, which are then multiplied by benchmark coating uptake ratios. Results are cross-checked with a bottom-up roll-up of sampled supplier sales drawn from financial filings and channel checks, and adjusted where disparities exceed 5 percent. Key variables include protein production growth, quick-service restaurant transactions, premix average selling prices, packaged frozen meal penetration, coating thickness norms, and corn-plus-wheat cost indices. A multivariate regression projects each driver through 2030, while scenario analysis tests shocks such as tariff hikes on starch. Gaps in bottom-up data are bridged using regional ASP proxies agreed upon during expert calls.

Data Validation & Update Cycle

Outputs pass three tiers of review: automated variance scans, peer analyst back-checks, and a sector lead sign-off. Reports refresh once a year; interim updates are triggered by material price or trade shifts, after which a fresh validation run is completed before client release.

Why Mordor's Batter And Breader Premixes Baseline earns trust

Published market values differ because firms pick varied scopes, base years, and price assumptions. Our disciplined approach, anchored to clearly stated protein volumes and verified ASPs, reduces hidden biases.

Key gap drivers include: some publishers bundle wet batters and flavor marinades; others freeze prices to one year or omit e-commerce retail packs; a few rely solely on secondary desk sources without primary validation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.98 B (2025) | Mordor Intelligence | - |

| USD 3.76 B (2023) | Global Consultancy A | Includes wet coatings and seasoning marinades; older base year; limited primary checks |

| USD 2.71 B (2024) | Research Publisher B | Covers only North America and Europe; keeps prices constant at 2021 levels |

| USD 2.73 B (2023) | Industry Association C | Excludes online retail packs; derives value from shipment tonnage without ASP triangulation |

The comparison shows how Mordor's clearly bounded scope, annual refresh cadence, and blended top-down/bottom-up modeling deliver a balanced baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

How big is the Batter And Breader Premixes Market?

The Batter And Breader Premixes Market size is estimated at USD 3.16 billion in 2026 and grow at a CAGR of 6.20% to reach USD 4.27 billion by 2031.

What is the current Batter And Breader Premixes Market size?

In 2026, the Batter And Breader Premixes Market size is estimated at USD 3.16 billion.

Who are the key players in Batter And Breader Premixes Market?

Newly Weds Foods, McCormick & Company, Inc., Bunge Ltd., Archer Daniels Midland Co., and Solina are the major companies operating in the Batter And Breader Premixes Market.

Which is the fastest growing region in Batter And Breader Premixes Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Batter And Breader Premixes Market?

In 2025, the North America accounts for the largest market share in Batter And Breader Premixes Market.

What years does this Batter And Breader Premixes Market cover, and what is the market CAGR for forecast period (2026-2031)?

The Batter And Breader Premixes Market is estimated to register a CAGR of 6.20% during 2026-2031. The report covers the Batter And Breader Premixes Market size for historical years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Batter And Breader Premixes Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: