Bags Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 95.67 Billion |

| Market Size (2031) | USD 125.18 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

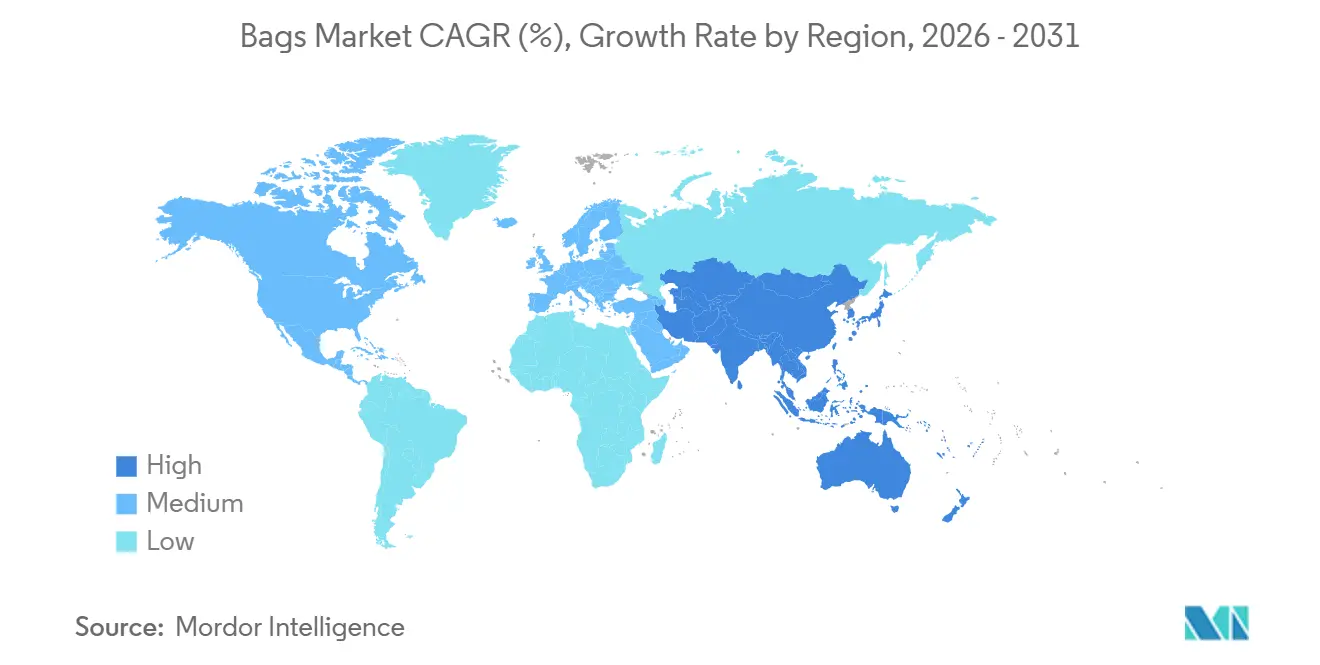

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

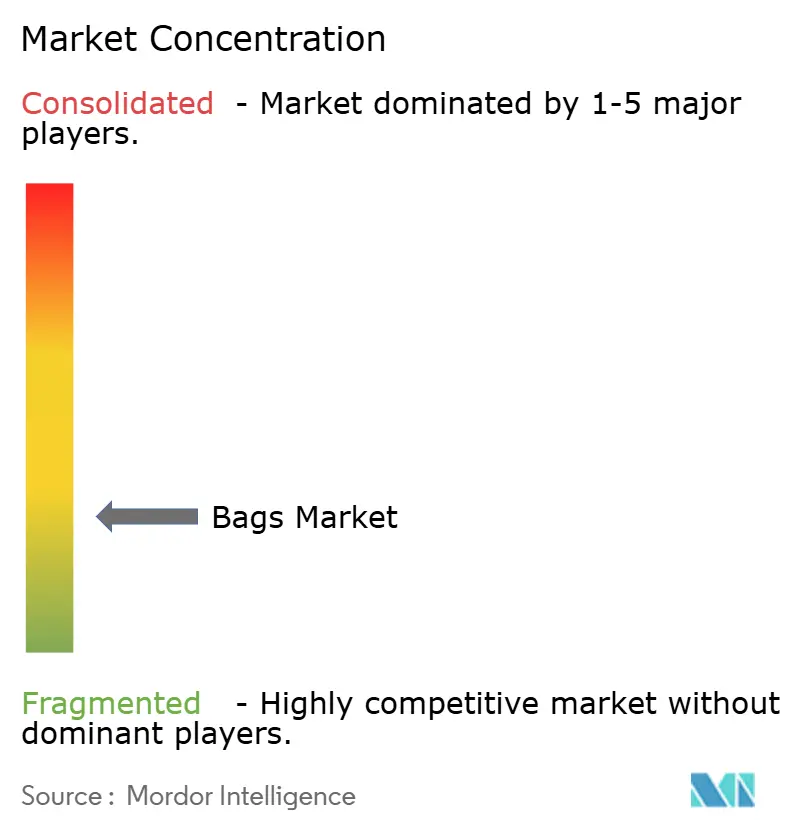

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bags Market Analysis by Mordor Intelligence

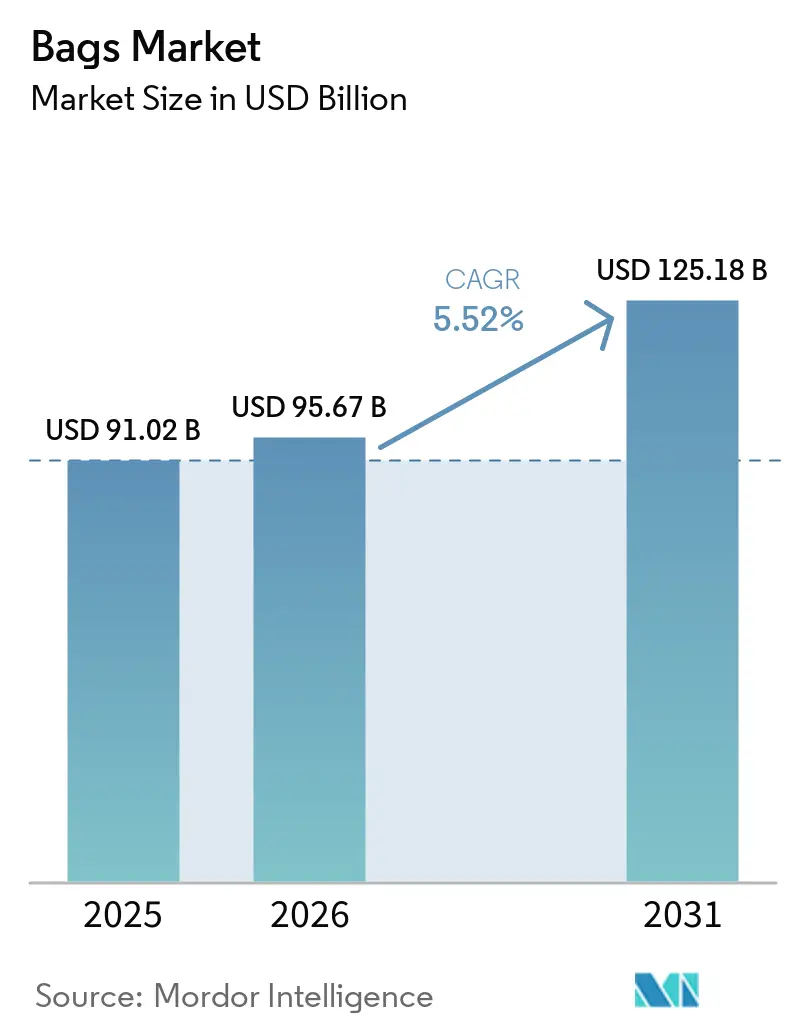

The bags market size is expected to grow from USD 91.02 billion in 2025 to USD 95.67 billion in 2026 and is forecast to reach USD 125.18 billion by 2031 at 5.52% CAGR over 2026-2031. The bags market is poised for steady growth over the forecast period, supported by rising consumer spending on fashion and lifestyle products, increasing urbanization, and the expanding influence of e-commerce platforms. Growing demand for travel bags, backpacks, handbags, and multifunctional luggage among both leisure and business travelers is further contributing to market expansion. Additionally, manufacturers are introducing innovative designs, lightweight materials, and sustainable products to attract environmentally conscious consumers. The increasing popularity of premium and branded bags, particularly in emerging economies, is strengthening revenue generation across the industry. Furthermore, the integration of smart features such as tracking systems, USB charging ports, and anti-theft technologies in luggage and backpacks is creating new growth opportunities.

Key Report Takeaways

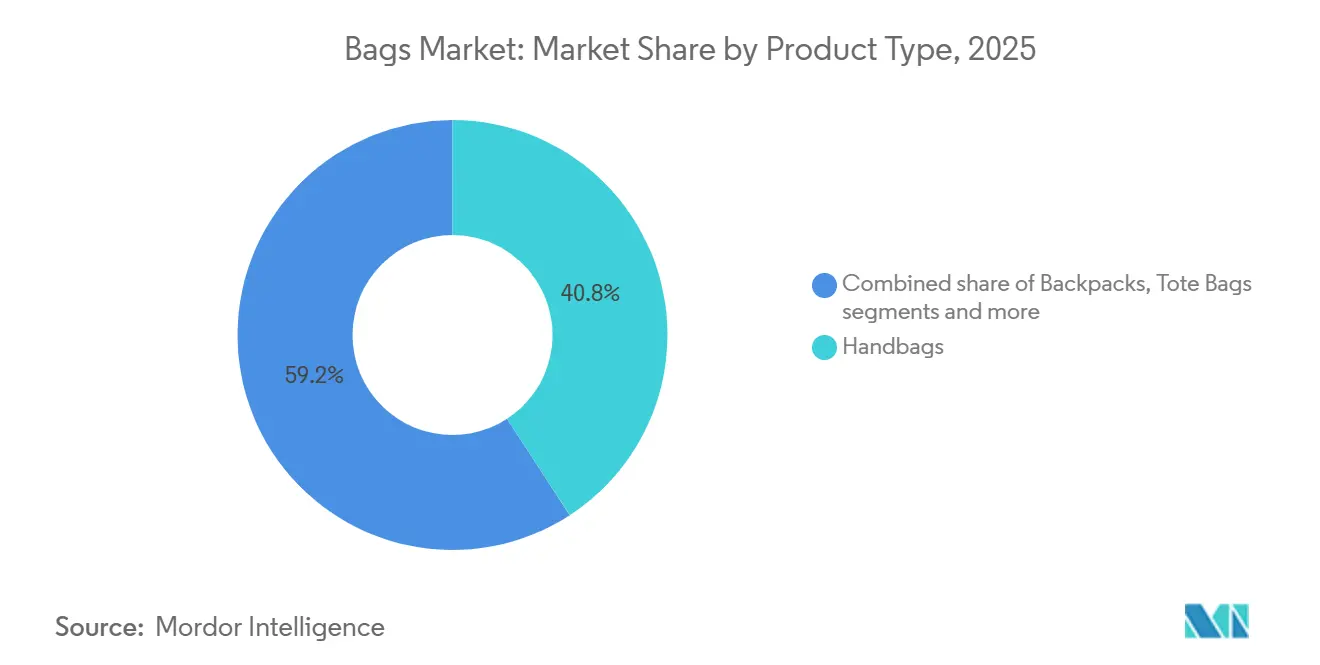

- By product type, handbags led with 40.81% of the bags market share in 2025, while luggage and travel bags recorded the fastest projected expansion at 6.49% CAGR through 2031.

- By category, mass accounted for 70.21% of the bags market size in 2025, while premium is forecast to grow the fastest at 6.65% through 2031.

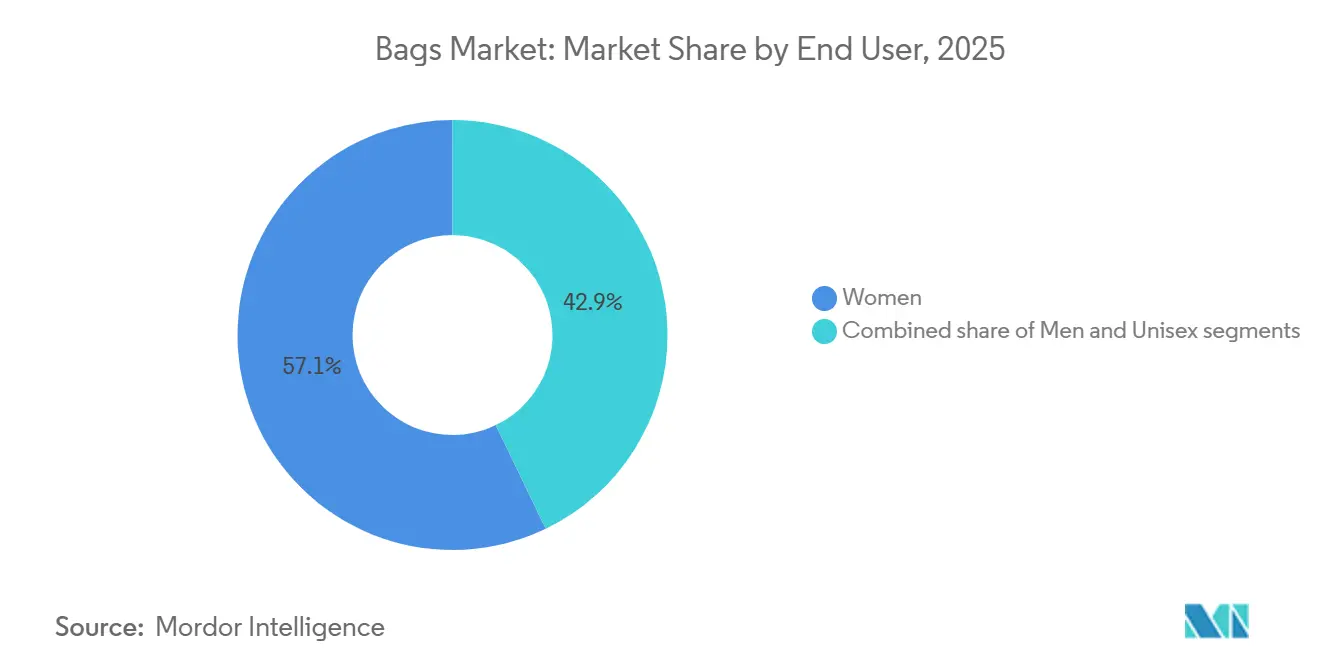

- By end user, women held 57.14% of global value in 2025, while unisex is expected to post the fastest growth at 7.16% through 2031.

- By distribution channel, offline stores represented 73.17% of value in 2025, while online stores are advancing at the highest CAGR of 7.71% through 2031.

- By geography, Asia-Pacific captured 33.27% of global value in 2025 and is also set to remain the fastest-growing regional segment at 6.76% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing international and domestic travel increasing demand for luggage and travel bags | +1.2% | Global, strongest in Asia-Pacific, South America, and Africa | Short term (≤ 2 years) |

| Rising fashion consciousness boosting sales of handbags and designer bags. | +1.0% | Global, led by Europe, North America, China, and India | Medium term (2-4 years) |

| Increasing participation in outdoor, sports, and adventure activities fueling specialty bag demand | +0.7% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Increasing urban workforce driving demand for backpacks, laptop bags, and office bags | +0.9% | Asia-Pacific core markets with spillover into the Middle East and Africa | Long term (≥ 4 years) |

| Rising preference for multifunctional and ergonomic bags for daily use | +0.5% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Growing consumer interest in sustainable and eco-friendly bag materials | +0.6% | Global, with stronger regulatory pressure in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing international and domestic travel increasing demand for luggage and travel bags

The continued expansion of both international and domestic tourism is creating strong demand for luggage, backpacks, duffel bags, and other travel-oriented bags. According to the United Nations Tourism Report, approximately 1.52 billion international tourist arrivals were recorded globally in 2025, nearly 60 million more than in 2024, reflecting sustained growth in global travel activity[1]Source: United Nations Tourism, International tourist arrivals up 4% in 2025 reflecting strong travel demand around the world", untourism.int. Rising business trips, leisure vacations, weekend getaways, and cross-border tourism are encouraging consumers to invest in durable, lightweight, and multifunctional travel bags. Airlines' increasing passenger volumes and the recovery of long-haul travel are further supporting purchases of premium luggage and cabin bags. In addition, the growing preference for organized travel accessories, including carry-on bags and travel backpacks, is expanding product demand across multiple price segments. This steady increase in travel frequency continues to strengthen sales opportunities for bag manufacturers worldwide.

Rising fashion consciousness boosting sales of handbags and designer bags.

Fashion-forward consumer preferences are significantly increasing demand for handbags, designer bags, and premium accessories across global markets. Bags are increasingly viewed as style statements that complement personal identity, driving consumers to purchase multiple products for different occasions, outfits, and lifestyles. The influence of social media platforms, celebrity endorsements, fashion influencers, and luxury branding has strengthened the appeal of branded and designer handbags, particularly among younger consumers. Frequent product launches featuring new colors, materials, and limited-edition collections encourage repeat purchases and brand engagement. Premiumization trends are also prompting consumers to spend more on high-quality and aesthetically appealing bags. In emerging economies, rising disposable incomes and growing exposure to global fashion trends are further expanding the customer base for fashionable bags.

Increasing participation in outdoor, sports, and adventure activities fueling specialty bag demand

The growing popularity of outdoor recreation, fitness activities, and adventure tourism is increasing demand for specialized bags designed for specific use cases. Consumers participating in hiking, trekking, camping, cycling, gym workouts, and water sports require durable, lightweight, and functional bags with enhanced storage and weather-resistant features. Rising interest in wellness-focused lifestyles and experiential travel is encouraging purchases of backpacks, duffel bags, hydration packs, and sports bags tailored to active pursuits. Manufacturers are responding with products that offer ergonomic designs, multiple compartments, anti-theft features, and improved comfort for extended use. The expansion of adventure tourism and organized sporting events is further supporting category growth. Additionally, increasing participation among younger consumers and women in outdoor activities is broadening the customer base for specialty bags.

Increasing urban workforce driving demand for backpacks, laptop bags, and office bags

The expansion of the urban workforce is contributing significantly to demand for backpacks, laptop bags, messenger bags, and office bags designed for daily professional use. As employment levels rise across both developed and emerging economies, more individuals require functional bags for carrying laptops, documents, and work essentials during their daily commute. For instance, according to the General Authority for Statistics, the number of employed people in Saudi Arabia increased from 14.76 million in 2022 to 17.70 million in 2024, reflecting substantial workforce growth[2]Source: General Authority for Statistics, “GASTAT publishes Labor Market Statistics for Q3 of 2025”, stats.gov.sa. This trend is increasing purchases of professional and business-oriented bags across corporate, government, and service sectors. The growing adoption of hybrid work models and mobile work environments is also encouraging demand for versatile, technology-friendly bags with dedicated compartments and security features.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit and imitation products affecting branded bag sales | -0.7% | Global, with higher exposure in online channels, Southeast Asia, and Eastern Europe | Short term (≤ 2 years) |

| Fluctuating prices of leather, synthetic fabrics, and other raw materials | -0.5% | Global, especially for producers sourcing from China, Vietnam, and India | Medium term (2-4 years) |

| Intense competition from local and unorganized manufacturers creating pricing pressure | -0.4% | Asia-Pacific, South America, and the Middle East and Africa | Medium term (2-4 years) |

| Economic uncertainties reducing consumer spending on non-essential bag purchases | -0.3% | North America, Europe, and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit and imitation products affecting branded bag sales

The widespread availability of counterfeit and imitation bags continues to pose a challenge for established brands across both luxury and mass-market segments. Fake products often replicate the appearance of premium handbags, backpacks, and luggage at significantly lower prices, attracting price-sensitive consumers and diverting sales from legitimate manufacturers. The growth of online marketplaces and informal distribution channels has made counterfeit products more accessible in many regions. This not only reduces revenue for branded companies but also weakens brand value and consumer trust when low-quality imitations are mistaken for authentic products. Luxury and designer bag manufacturers face particularly high exposure due to the strong demand for recognizable brands and logos. Additionally, companies incur substantial costs related to intellectual property protection, anti-counterfeiting measures, and legal enforcement.

Fluctuating prices of leather, synthetic fabrics, and other raw materials

Price volatility in key raw materials such as leather, synthetic fabrics, nylon, polyester, metal fittings, and zippers presents a significant challenge for bag manufacturers. Fluctuations in the costs of these materials are often influenced by changes in commodity prices, supply chain disruptions, transportation expenses, and currency exchange rates. Rising input costs can increase production expenses and reduce profit margins, particularly for companies operating in highly competitive and price-sensitive market segments. Manufacturers may face difficulties in passing higher costs on to consumers without affecting demand. The uncertainty associated with raw material pricing also complicates procurement planning and long-term contract negotiations. Additionally, premium bag producers that rely on high-quality leather are especially vulnerable to supply and pricing fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Luggage Surge Reshapes Mix Despite Handbags' Structural Lead

Handbags emerged as the largest product segment in the bags market, accounting for 40.81% of total market share in 2025. The segment benefits from its broad consumer appeal, serving both functional and fashion-oriented needs across diverse demographic groups. Demand remains strong due to frequent product purchases driven by changing fashion trends, seasonal collections, and brand-driven consumer preferences. Premium, luxury, and affordable handbag categories collectively contribute to the segment’s dominant position, allowing manufacturers to target multiple income groups. The growing influence of social media, celebrity endorsements, and fashion-conscious consumers continues to support sales worldwide.

Luggage and travel bags are projected to be the fastest-growing segment of the bags market, registering a CAGR of 6.49% through 2031. Growth is being driven by the continued recovery and expansion of global tourism, business travel, and cross-border mobility. Rising disposable incomes and increasing consumer willingness to spend on travel-related products are encouraging demand for durable and feature-rich luggage solutions. Manufacturers are introducing lightweight materials, smart tracking capabilities, enhanced security features, and ergonomic designs to meet evolving traveler requirements. The rapid growth of domestic and international travel in emerging economies is also creating new opportunities for market participants.

By Category: Premium Accelerates as Mass Maintains Volume Supremacy

The mass category dominated the bags market in 2025, accounting for 70.21% of total market revenue. Its leading position is supported by a broad consumer base seeking affordable, functional, and versatile bag products for everyday use. Mass-market bags are widely available across supermarkets, department stores, specialty retailers, and online platforms, ensuring strong market penetration across urban and rural regions. The segment benefits from consistent demand for school bags, backpacks, tote bags, casual handbags, and travel bags that cater to practical consumer needs. Competitive pricing, extensive product variety, and frequent product refreshes enable manufacturers to attract a wide range of customers.

The premium category is expected to register the fastest growth in the bags market, expanding at a CAGR of 6.65% through 2031. Growth is being driven by increasing consumer preference for high-quality materials, superior craftsmanship, and distinctive brand identity. Rising disposable incomes, particularly in emerging markets, are enabling more consumers to purchase premium handbags, luggage, and lifestyle accessories. Luxury and premium brands are also benefiting from growing digital engagement, direct-to-consumer sales channels, and expanding retail presence in high-growth regions. Sustainability initiatives, limited-edition collections, and product personalization are further enhancing the appeal of premium offerings among affluent and aspirational consumers.

By End User: Unisex Gains Ground as Women Retain Market Leadership

Women represented the largest end-user segment in the bags market, accounting for 57.14% of global market value in 2025. The segment's dominance is driven by strong demand across multiple product categories, including handbags, totes, shoulder bags, clutches, backpacks, and luxury fashion accessories. Fashion trends, seasonal product launches, and frequent purchasing behavior continue to support consistent sales among female consumers. Premium and luxury brands particularly benefit from the high level of engagement and brand loyalty observed within this customer group. In addition, increasing workforce participation, rising disposable incomes, and growing fashion consciousness among women have expanded spending on both functional and style-oriented bags.

The unisex segment is projected to be the fastest-growing end-user category, registering a CAGR of 7.16% through 2031. Growth is being fueled by changing consumer preferences toward versatile, gender-neutral, and multifunctional bag designs that can be used across different lifestyles and occasions. Increasing demand for backpacks, travel bags, laptop bags, and casual everyday carry products is contributing significantly to segment expansion. Brands are increasingly adopting inclusive marketing strategies and developing products that appeal to a broader consumer base rather than targeting specific genders. The rise of minimalist fashion trends and practical design preferences has also strengthened demand for unisex bag offerings.

By Distribution Channel: Digital Commerce Rewires Purchase Journeys but Offline Retains Majority

Offline stores remained the dominant distribution channel in the bags market, accounting for 73.17% of total market value in 2025. The segment benefits from consumers' preference to physically examine products before purchase, particularly for bags where material quality, durability, size, and design are important purchasing considerations. Department stores, specialty fashion retailers, brand-exclusive outlets, and luggage stores continue to play a crucial role in product sales across both premium and mass-market categories. In-store shopping also provides immediate product availability and personalized customer assistance, enhancing the overall buying experience. Luxury and premium bag brands especially rely on physical retail locations to strengthen brand perception and deliver exclusive customer experiences.

Online stores are projected to be the fastest-growing distribution channel in the bags market, expanding at a CAGR of 7.71% through 2031. The growth of e-commerce platforms, increasing internet penetration, and widespread smartphone adoption are driving greater online purchases of bags across global markets. Consumers are increasingly attracted to the convenience of browsing extensive product selections, comparing prices, and accessing customer reviews from any location. Online channels also allow brands to reach broader audiences through direct-to-consumer strategies, digital marketing campaigns, and personalized shopping experiences. The availability of secure payment options, flexible return policies, and faster delivery services has further strengthened consumer confidence in online shopping.

Geography Analysis

Asia-Pacific accounted for 33.27% of the global bags market value in 2025, making it the largest regional market, and is projected to remain the fastest-growing region with a CAGR of 6.76% through 2031. Growth is supported by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing consumer spending on fashion, travel, and lifestyle products. 54% of the global urban population, more than 2.2 billion people, live in Asia. By 2050, the urban population in Asia is expected to grow by 50% - an additional 1.2 billion people[3]Source: UN-Habitat, “Asia and the Pacific Region”, unhabitat.org. Countries such as China, India, Japan, and South Korea continue to drive demand for handbags, backpacks, luggage, and premium accessories. The region also benefits from a strong manufacturing base, extensive retail networks, and the rapid expansion of e-commerce platforms.

North America and Europe represent mature but highly valuable markets characterized by strong demand for premium, luxury, and travel-oriented bags. In North America, consumer preference for branded products, frequent travel activity, and high spending power support steady market expansion. The United States remains a key contributor, driven by demand for fashion handbags, business bags, and innovative luggage solutions. In Europe, established luxury fashion houses, strong tourism activity, and a well-developed retail infrastructure continue to support market performance. Sustainability trends and demand for eco-friendly materials are also influencing purchasing decisions across both regions, encouraging manufacturers to invest in sustainable product lines and circular economy initiatives.

South America, the Middle East, and Africa are emerging markets that offer significant long-term growth opportunities for the bags industry. Rising urban populations, improving economic conditions, and increasing exposure to global fashion trends are driving demand across these regions. In South America, growing middle-class consumption and expanding online retail channels are supporting sales of affordable and mid-range bags. The Middle East benefits from strong luxury goods demand, particularly in the Gulf countries, where premium brands continue to expand their presence. Meanwhile, Africa is witnessing gradual market development supported by increasing retail penetration, improving consumer purchasing power, and growing demand for functional and affordable bag products across major urban centers.

Competitive Landscape

The bags market exhibits a fragmented competitive structure, characterized by the presence of luxury conglomerates, specialist luggage manufacturers, and numerous regional and private-label brands. Leading luxury groups such as LVMH, Kering, Hermès, Tapestry, and Capri Holdings maintain a strong position in the premium segment through established brand equity, exclusive product offerings, and robust pricing strategies. Their ability to leverage global retail networks, marketing investments, and customer loyalty enables them to capture a significant share of the value generated within the high-end bags category. As a result, competition in the premium market is driven more by brand perception and craftsmanship than by price.

Specialist luggage companies play a critical role in shaping competition within travel-oriented segments of the bags market. Companies such as Samsonite and Rimowa have built strong market positions by focusing on product durability, innovative materials, lightweight construction, and advanced travel features. Unlike fashion-focused brands, these players compete primarily on functionality, performance, and reliability, which are key purchasing criteria for frequent travelers. Their continued investment in product development and premium travel solutions has strengthened their competitive standing in both mature and emerging markets.

At the mass-market level, competition remains highly intense due to the large number of regional manufacturers, local brands, and private-label operators. These companies benefit from flexible production capabilities, localized product designs, and competitive pricing strategies that allow them to respond quickly to changing consumer preferences. The presence of numerous players across different price points prevents excessive market concentration and creates a dynamic competitive environment. Consequently, success in the bags market depends heavily on segment specialization, distribution reach, brand positioning, and the ability to meet evolving consumer demands across diverse product categories.

Bags Industry Leaders

-

Samsonite International S.A.

-

Tapestry, Inc.

-

Kering SA

-

LVMH Moët Hennessy Louis Vuitton SE

-

Hermès International SCA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: British travel luggage brand Antler expanded its retail footprint by opening a flagship store on Regent Street in London. The two-floor store marks the company’s first standalone UK flagship location under its current ownership and forms part of its broader global retail expansion strategy. The development strengthens Antler’s direct-to-consumer presence and improves brand visibility in a key international shopping destination.

- March 2026: Peak Design expanded its Travel Line portfolio by introducing four new travel bags: the Travel Backpack 2-in-1, Travel Backpack 20L, Travel Weekender 25L, and Travel Crossbody 3L. The company targeted travelers, commuters, and photography enthusiasts seeking versatile and lightweight carrying solutions. The expansion strengthens Peak Design’s position in the premium travel bag segment and reflects rising demand for multifunctional travel products.

- February 2026: Skybags, a leading luggage and backpack brand under VIP Industries Limited, entered into a strategic partnership with Chennai Super Kings (CSK) as the team’s Official Luggage Partner for the 2026 season. As part of the collaboration, the company launched an exclusive range of officially licensed CSK-branded luggage and backpacks. The initiative marked Skybags’ entry into sports-focused brand collaborations and expanded its reach among young and travel-oriented consumers.

Global Bags Market Report Scope

The bags market comprises the manufacturing, distribution, and sale of products designed to carry, store, organize, and transport personal belongings, travel essentials, professional items, and other goods. The bags market is segmented by product type, category, end user, distribution channel, and geography. Based on product type, the market is segmented into backpacks, handbags, luggage, travel bags, tote bags, duffel bags, and other product types. Based on category, the market is segmented into mass and premium. Based on end user, the market is segmented into men, women, and unisex. Based on the distribution channel, the market is segmented into offline stores and online stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East, and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD).

| Backpacks |

| Handbags |

| Luggage and Travel Bags |

| Tote Bags |

| Duffel Bags |

| Other Product Types |

| Mass |

| Premium |

| Men |

| Women |

| Unisex |

| Offline Stores |

| Online Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Belgium | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Backpacks | |

| Handbags | ||

| Luggage and Travel Bags | ||

| Tote Bags | ||

| Duffel Bags | ||

| Other Product Types | ||

| By Category | Mass | |

| Premium | ||

| By End User | Men | |

| Women | ||

| Unisex | ||

| By Distribution Channel | Offline Stores | |

| Online Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for global bags demand through 2031?

The bags market is projected to rise from USD 95.67 billion in 2026 to USD 125.18 billion by 2031 at a 5.52% CAGR, supported by travel recovery, urban demand, and steady premium brand investment.

Which product category contributes the most value today?

Handbags held 40.81% of 2025 value, making them the largest product type because they combine everyday use with strong fashion relevance.

Which product type is growing the fastest over the forecast period?

Luggage and travel bags are forecast to grow at 6.49% CAGR through 2031, largely due to stronger travel activity and higher replacement demand.

Why do offline stores still matter when online sales are rising?

Offline stores still accounted for 73.17% of 2025 value because many buyers prefer to inspect size, material, and finish in person before purchase.

What are the biggest risks affecting branded bag makers?

Counterfeits and raw material inflation remain the main risks, because they weaken brand trust, raise compliance needs, and pressure margins across both mass and premium ranges.

Page last updated on: