Ball Sports Luggage Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

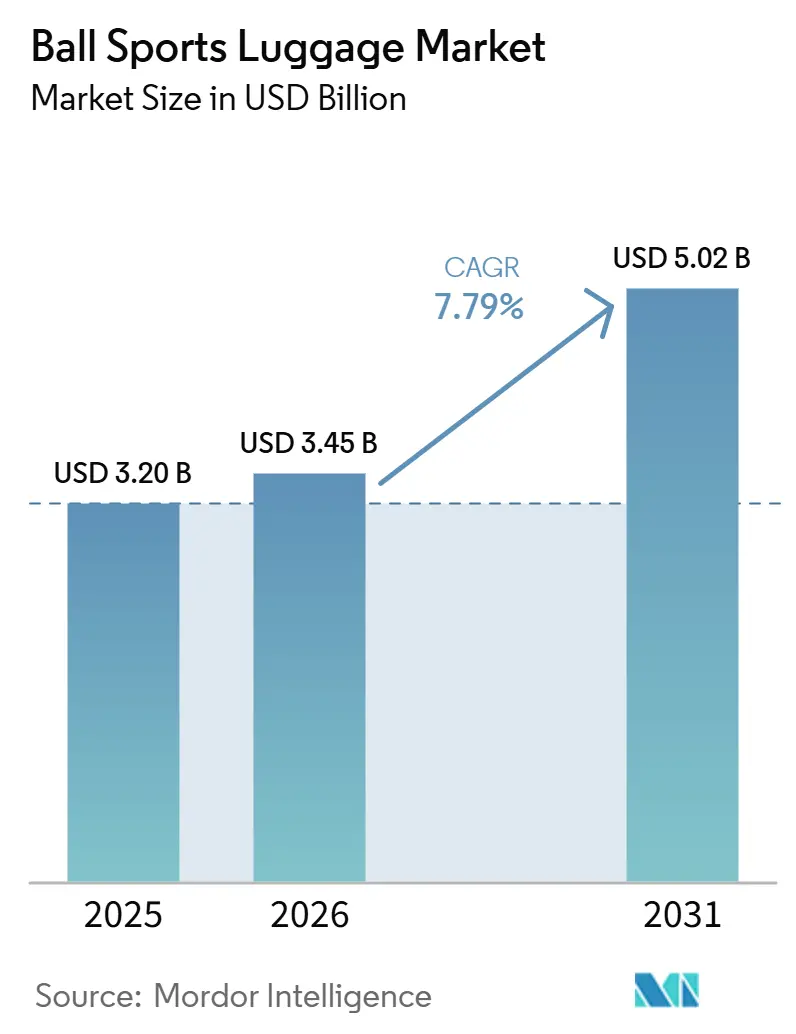

| Market Size (2026) | USD 3.45 Billion |

| Market Size (2031) | USD 5.02 Billion |

| Growth Rate (2026 - 2031) | 7.79% CAGR |

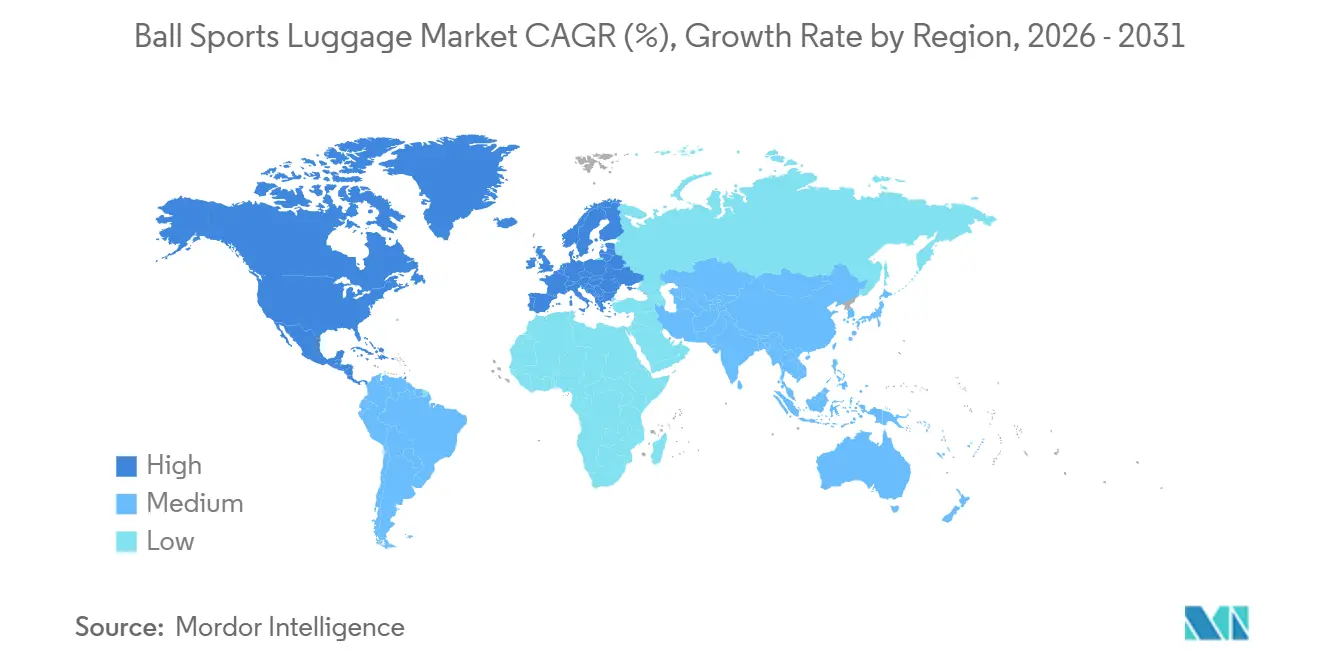

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ball Sports Luggage Market Analysis by Mordor Intelligence

The ball sports luggage market size is expected to grow from USD 3.20 billion in 2025 to USD 3.45 billion in 2026 and is forecast to reach USD 5.02 billion by 2031 at 7.79% CAGR over 2026-2031. Parents in North America are increasingly investing in their children's sports activities, spending significantly more each year compared to the previous year. This rise in spending highlights a growing demand for durable multi-sport luggage, especially as families frequently travel for sports. In the Asia-Pacific region, growth is even more pronounced. The expansion is driven by the rapid development of soccer academies in China, the growing popularity of cricket in India, and substantial investments from sovereign wealth funds into regional sports projects, which are boosting the need for equipment transportation. Brands are differentiating themselves by adopting recycled fabrics and finishes free of per- and polyfluoroalkyl substances (PFAS), aligning with upcoming chemical regulations in France and mandates in California. Additionally, online and omnichannel sales strategies are transforming the retail experience by significantly reducing delivery times. This approach is particularly appealing to mobile-first consumers, who now account for a majority of site traffic at leading retailers in the United States. As women's leagues gain commercial momentum and there is a shift toward premium, sustainable materials, the organized sports landscape continues to evolve.

Key Report Takeaways

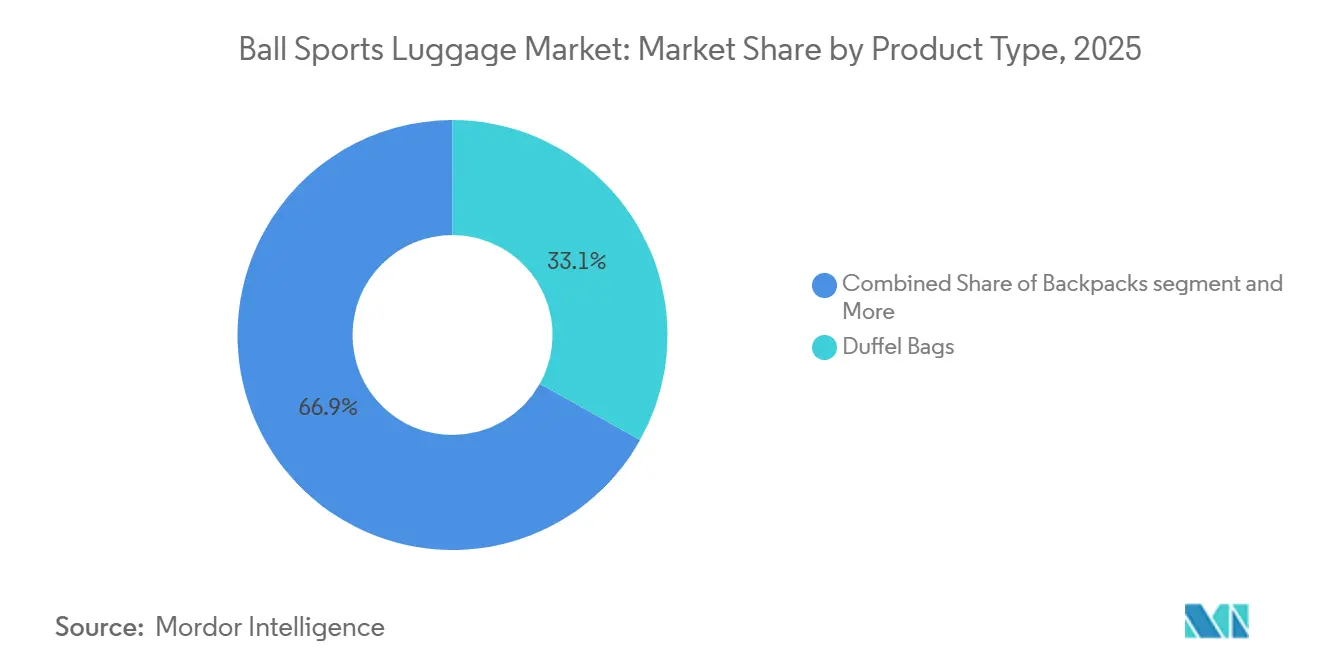

- By product type, duffel bags led with 33.12% of ball sports luggage market share in 2025, while backpacks recorded the fastest 8.81% CAGR through 2031.

- By sport, soccer/football accounted for 36.33% share of the ball sports luggage market size in 2025; cricket bags are advancing at an 8.63% CAGR over the same horizon.

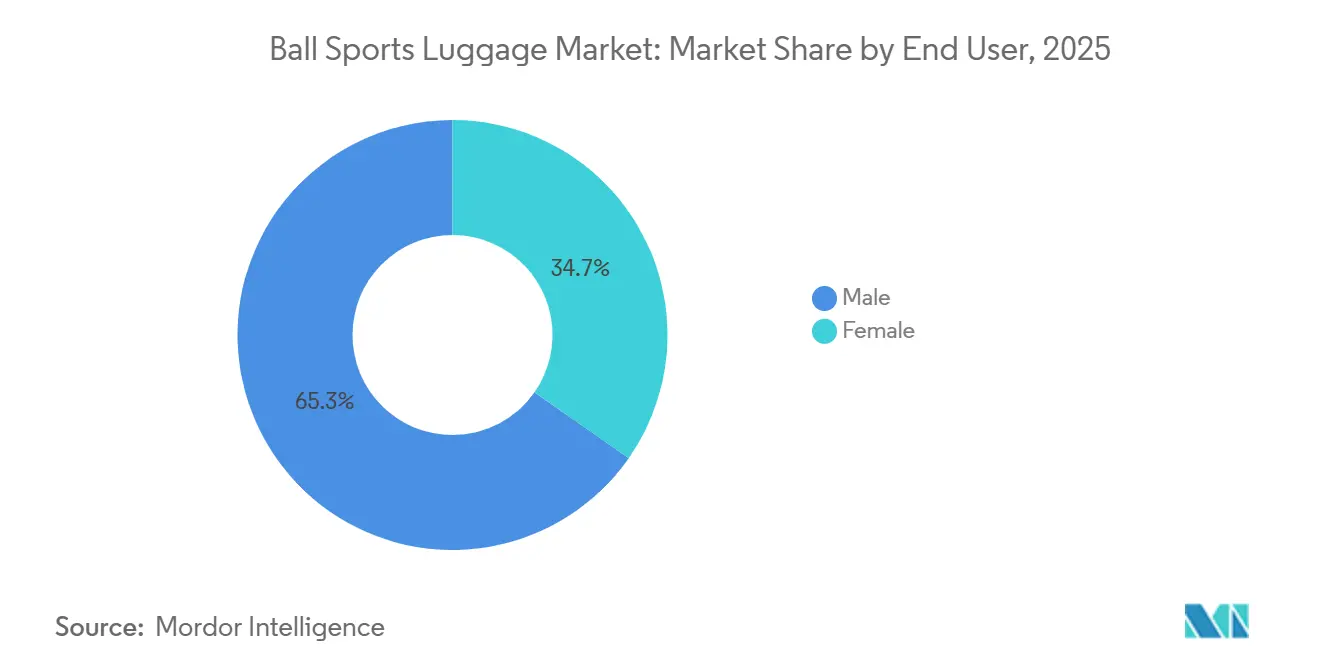

- By end user, male consumers commanded 70.13% of 2025 revenue, whereas female-targeted products are expanding at an 8.42% CAGR as women’s sports commercialize.

- By category, mass offerings represented 62.71% of 2025 value, yet premium lines are growing at an 8.97% CAGR on the back of recycled content and tech features.

- By distribution channel, sports specialty stores held 34.82% share in 2025; online retail is scaling at a 9.86% CAGR as brands perfect ship-from-store fulfillment.

- By geography, North America contributed 32.66% of 2025 revenue, but Asia-Pacific is growing the quickest at 9.07% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ball Sports Luggage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing interest in outdoor and recreational sports | +1.5% | Global, with strongest gains in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Expansion of the travel and tourism industry | +1.3% | Global, concentrated in North America, Europe, Middle East | Short term (≤ 2 years) |

| Rising focus on sustainability and use of recycled materials | +1.1% | Europe and North America lead; Asia-Pacific adoption accelerating | Long term (≥ 4 years) |

| Growing demand for durable and high-performance bags | +1.4% | Global, premium segments in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Enhanced online presence and digital strategies by brands | +1.6% | Global, highest penetration in North America and Europe | Short term (≤ 2 years) |

| Rising popularity of athleisure and multi-functional bags | +1.2% | North America, Europe, urban Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing interest in outdoor and recreational sports

Driven by increasing youth sports participation, the global youth sports market is expected to witness significant growth over the coming years. At the same time, parental spending on youth sports has seen a notable rise in recent years. This increase in spending is linked to more frequent tournament travels, involvement in multiple sports, and earlier brand engagements, particularly through Name, Image, and Likeness (NIL) deals, which are now active in more than 40 states across the United States [1]Source: The Florida Senate, “Bill Analysis and Fiscal Impact Statement,” flsenate.gov. In the Middle East, substantial infrastructure investments are enhancing sports participation. For example, Saudi Arabia has established hundreds of women's sports centers, enrolled a large number of girls in school football leagues, and significantly increased participation in the Riyadh Marathon [2]Source: Saudi Government, “Riyadh Marathon,” my.gov.sa. In India, cricket's growing popularity, especially following the launch of the Women's Premier League, has driven higher spending on gear and created demand for specialized equipment carriers. As youth leagues expand and women's sports gain greater commercialization, there is a clear shift in demand from generic gym bags to sport-specific designs. These new designs include features such as reinforced compartments, ventilated sections, and modular dividers, addressing the evolving needs of athletes.

Expansion of the travel and tourism industry

Sports tourism is capitalizing on event-driven travel. Qatar's FIFA World Cup in 2022 attracted a substantial number of visitors, generating significant revenue from tourism and broadcasting. Meanwhile, with Saudi Arabia securing the hosting rights for the FIFA World Cup in 2034 and the United Arab Emirates rolling out a series of events including Formula 1, Ultimate Fighting Championship, and tennis, the demand for travel bags is on the rise [3]Source: International Trade Administration, “Saudi Arabia Logistics Transformation for 2034 FIFA World Cup,” trade.gov. These events have spurred a consistent demand for wheeled duffels and carry-on-compliant bags, designed to meet airline size restrictions and safeguard gear. In December 2025, Nike introduced a hard-shell suitcase collection, priced at a premium and set for spring 2026 availability, aiming to blend sports identity with travel practicality. Families, traveling frequently during the season for youth tournaments in baseball, soccer, and basketball, are now favoring bags equipped with reinforced bottoms, dirt-resistant zippers, and dedicated cleat compartments. As youth tournaments shift from domestic venues to international stages, especially in Europe and the Asia-Pacific, there is a growing preference for Transportation Security Administration-compliant designs and lightweight materials, helping families avoid checked-baggage fees.

Rising focus on sustainability and use of recycled materials

As regulatory pressures mount and consumer preferences shift, the push for recycled content intensifies. However, the cost of recycled materials remains a significant hurdle. For instance, recycled nylon is priced significantly higher than its virgin polyester counterpart. Moreover, bio-based materials, such as Bio-Dyneema, come with an even steeper price tag. In a nod to this trend, Norda unveiled the inaugural bio-based Dyneema duffel in June 2024. Similarly, Osprey's Transporter family rolled out a fully recycled NanoTough fabric in spring 2025. Both brands are targeting outdoor enthusiasts, who are reportedly willing to pay a premium for verified sustainability. In France, a regulatory exemption allows products with a minimum of post-consumer recycled material to bypass certain restrictions, as long as per- and polyfluoroalkyl substances (PFAS) residues are in line with the recycled content. This move offers a compliance avenue for brands that can trace their supply chain. Yet, there's a catch: while PFAS-free water repellents are a step towards sustainability, they often lag in durability and stain resistance. This gap necessitates brands to invest in consumer education, emphasizing care and reapplication. Furthermore, standards like Bluesign-certified inputs and OEKO-TEX (International Association for Research and Testing in the Field of Textile and Leather Ecology) are becoming essential for distribution in Europe and North America. Retailers are now demanding third-party verification as a prerequisite for listing new stock-keeping units (SKUs).

Growing demand for durable and high-performance bags

As consumers increasingly demand bags that can endure multiple seasons of use, extreme weather, and the rigors of tournament travel, performance expectations are on the rise. Wilson's Roland-Garros 2025 Collection, equipped with Thermoguard technology, safeguards racquet string tension from temperature shifts, tackling a key concern for competitive players at outdoor tournaments. Babolat's Pure Aero Pack, retailing at a premium price, boasts water-repellent coatings and insulated compartments, ensuring gear integrity in diverse climates. Material innovation plays a pivotal role: Kitworks employs a thermoplastic polyurethane-laminated ripstop, while Deuter opts for a thermoplastic polyurethane-coated polyester, both enhancing abrasion resistance and extending product lifecycles. This durability justifies their premium pricing by reducing the need for replacements. Families involved in youth sports, traveling frequently each season, emphasize features like reinforced bottoms, heavy-duty zippers, and dirt-resistant fabrics. These elements are crucial for withstanding muddy fields and wet dugouts, as showcased by Rawlings' molded-bottom ball bags, a testament to durability-first design. The push for durability is also influencing warranty offerings. Nike's hard-shell suitcase collection, backed by lifetime warranties, underscores the brand's confidence in its material quality and manufacturing precision.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated production costs for advanced bags | -1.2% | Global, most acute in Europe and North America | Short term (≤ 2 years) |

| Disruptions in the supply chain | -0.9% | Global, concentrated in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Volatility in raw material prices | -1.0% | Global, petrochemical-dependent regions most exposed | Short term (≤ 2 years) |

| Short Product Life Cycles Due to Fashion Trends | -0.5% | North America and Europe primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated production costs for advanced bags

As of March 2026, polyester prices have increased significantly, and nylon has also experienced a notable rise. These hikes are largely attributed to fluctuations in petrochemical markets and energy surcharges, which have also seen an upward trend. Recycled nylon, a key player in sustainability efforts, commands a premium, costing substantially more than its virgin counterpart. Furthermore, bio-based alternatives such as ECONYL and Bio-Dyneema come with added premiums. Brands find it challenging to transfer these costs to consumers who are sensitive to pricing, especially in the mass market. Logistics have also felt the pinch, with costs rising due to increasing container rates and fuel surcharges. This surge has particularly hurt brands without the scale to negotiate discounts with freight forwarders. Compliance with per- and polyfluoroalkyl substances (PFAS) regulations is adding another layer of expense. Testing under European Norm 17681-1:2025, which identifies polymer-embedded PFAS through a combination of methanol extraction and alkaline hydrolysis, can set brands back significantly per sample, depending on the range of analytes. To ensure consistency across batches, brands are compelled to test various colorways and material combinations. In France, the mandated fluorine threshold is set at a very low level. This regulation pushes brands to rethink their water-repellent treatments, often leading to extensive research and development investments spanning multiple years. Such reformulations can also mean compromising on performance features that consumers typically expect, especially in outdoor and sports products.

Disruptions in the supply chain

Asia-Pacific's manufacturing concentration leaves it vulnerable to regional disruptions. China dominates global textile production, while Vietnam, Bangladesh, and Indonesia emerge as key players in bag assembly. The supply chains for recycled materials are fragmented. Collection rates for post-consumer polyethylene terephthalate (PET) and nylon differ by region, and contamination levels impact the usable yield. This inconsistency forces brands to hold buffer inventories, tying up essential working capital. The push for per- and polyfluoroalkyl substances (PFAS) reformulation is reshaping supplier dynamics. Mills are racing to procure PFAS-free durable water repellent (DWR) finishes and cleaning agents, often facing significant cost premiums and extended lead times. Meanwhile, brands without robust chemical management systems grapple with production delays and inconsistent quality. Container rate fluctuations, with surcharges rising significantly, are tightening delivery schedules. Brands now face a dilemma: pay for air freight premiums or risk missing out on product launches aligned with seasonal sports events. Relying on single sources for specialized materials such as Thermoguard insulation or bio-based Dyneema puts brands at risk. When suppliers encounter capacity or quality challenges, it can lead to inventory shortages. This is especially critical for limited-edition colorways and merchandise linked to tournament schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Backpacks Gain as Hybrid Designs Blur Use Cases

Backpacks are expected to grow at an annual rate of 8.81% during 2026 to 2031, exceeding the overall market growth rate of 7.79%. This growth is attributed to the rising demand for multi-functional designs that accommodate consumers transitioning between gym, office, and weekend travel. For example, Under Armour's No Weigh Backpack, introduced in May 2025 at USD 185, offers an expandable capacity of 28 to 35 liters and Under Armour Suspension straps. This product highlights the shift toward premium, technology-enabled designs that include features such as integrated laptop sleeves and charging pockets.

In 2025, duffel bags contributed 33.12% of the total revenue, primarily driven by team sports that require transporting bulk gear. However, growth in this category is slowing as wheeled duffel and trolley bags gain popularity among tournament travelers who prioritize ease of mobility at airports. These products are benefiting from the increasing trend of sports tourism, with examples like Patagonia's 100-liter wheeled duffel priced at USD 435 and Nike's hard-shell suitcase collection starting at USD 260. These options appeal to consumers who value durability and brand identity over generic luggage alternatives.

By Sport: Cricket Bags Surge as Women's Leagues Drive Equipment Upgrades

Cricket bags are expected to grow at an annual rate of 8.63% during 2026-2031, representing the fastest growth among sports segments. This growth is primarily driven by the establishment of India's Women's Premier League and the development of youth cricket infrastructure across the Asia-Pacific region. India's cricket gear market has also experienced notable expansion, with increased budgets for women's cricket equipment as franchises invest in professional-grade gear to support the sport's growth.

Soccer and football bags accounted for 36.33% of revenue in 2025, highlighting the global popularity of the sport and its high participation rates. However, growth in this segment is slowing in mature European markets, where market penetration is approaching saturation. Basketball bags are benefiting from the global expansion of the National Basketball Association (NBA) and Women's National Basketball Association (WNBA). These bags often include rectangular team duffels with ventilated compartments and sublimation printing that matches team uniforms, catering to the needs of players and teams.

By End User: Female Segment Accelerates as Women's Sports Revenue Triples

The market for female-targeted bags is projected to grow at an annual rate of 8.42% during 2026 to 2031, driven by the increasing revenue from women's sports, with notable projections for 2025. Male consumers accounted for 70.13% of the revenue in 2025. Rising participation rates in team sports are contributing to larger average purchase sizes. The gender gap in sports is narrowing as women's leagues gain professionalism and media coverage. The market for women's sports backpacks is expected to witness significant growth, supported by a strong compound annual growth rate (CAGR). This trend reflects a broader adoption of athletic leisurewear (athleisure), extending beyond competitive sports.

In Saudi Arabia, the development of women's sports infrastructure, including the establishment of numerous sports centers and the enrollment of many girls in school football leagues, is driving demand in a previously underserved market. Since 2021, there has been a notable increase in professional female players, a rise in sports clubs, and significant growth in national teams. Similarly, in India, the Women's Premier League (WPL) has led to a substantial increase in budgets for cricket equipment. Female athletes are now seeking bags with lighter materials, organized compartments for protective gear, and stylish designs that transition seamlessly from the field to everyday use.

By Category: Premium Segment Expands as Sustainability and Tech Command Margins

The premium bags market is expected to grow at an annual rate of 8.97% during 2026-2031, outpacing the growth of the mass segment. This growth is driven by consumer preferences for features such as recycled materials, temperature-controlled compartments, and technology integration, rather than focusing solely on price. In 2025, mass-market products accounted for 62.71% of revenue. Brands catering to youth leagues and recreational players generally emphasize functional designs at affordable price points. However, rising raw material costs are pressuring these brands to either scale back on product features or accept reduced profit margins.

Under Armour introduced its No Weigh Duffle Backpack in December 2025, positioning it as a premium product with expandable capacity. Similarly, PUMA launched a collaboration backpack with LaMelo Ball, highlighting a premium positioning strategy. Both brands rely on athlete endorsements and performance-focused narratives to justify their higher price points. Nike, on the other hand, introduced its hard-shell suitcase collection in spring 2026, targeting affluent consumers who view sports luggage as an extension of their personal brand. These products include features such as polycarbonate shells, Transportation Security Administration (TSA)-approved locks, and lifetime warranties, appealing to this consumer segment. Osprey launched its Transporter series in spring 2025, utilizing fully recycled NanoTough fabric and treatments free from per- and polyfluoroalkyl substances. This strategy enables Osprey to command a premium price over standard duffels, catering to environmentally conscious consumers who seek sustainability verified through third-party certifications.

By Distribution Channel: Online Retail Surges as Omnichannel Fulfillment Scales

Online retail is projected to grow at an annual rate of 9.86% between 2026 and 2031, making it the fastest-growing distribution channel. This growth is driven by brands adopting ship-from-store fulfillment and mobile-optimized checkout processes to attract digital-native consumers. Sports specialty stores accounted for 34.82% of revenue in 2025. Leading players include Academy Sports, which operates a large number of stores and plans significant expansion by 2027, and Dick's Sporting Goods, which runs numerous locations, including several House of Sport experiential formats. In the third quarter of 2026, Academy Sports reported notable growth in e-commerce, achieving strong quarterly revenue alongside an overall revenue increase. Similarly, Dick's Sporting Goods, which fulfills most online orders from physical stores, has reduced delivery times to just a few days while lowering inventory holding costs.

Intersport, employing a comparable omnichannel strategy, also reported substantial growth in online revenue. These developments demonstrate that physical retail and e-commerce can complement each other effectively when integrated properly. Supermarkets and hypermarkets, which cater to price-sensitive consumers seeking affordable duffels and backpacks, are losing market share. They face challenges in competing with the broader product assortments and specialized staff expertise offered by specialty stores and branded direct-to-consumer platforms.

Geography Analysis

North America accounted for 32.66% of the projected 2025 revenue, making it the leading segment. In 2024, parental spending on youth sports increased significantly, driven by the growing frequency of tournament travel and multi-sport enrollments. Academy Sports, which operates hundreds of stores, plans to expand its footprint by adding numerous new locations by 2027, aiming for a substantial revenue target. Similarly, Dick's Sporting Goods is introducing dozens of 'House of Sport' experiential formats by 2027, combining retail with training and event hosting. E-commerce has gained significant traction, contributing notably to sales at both Dick's and Academy. Academy reported strong online growth in the third quarter of 2026. However, low mobile conversion rates remain a challenge, prompting brands to implement innovations such as one-click payments and augmented reality product visualizations. In the United States, consumers increasingly prioritize premium features like temperature-controlled compartments, recycled materials, and technology integration. In contrast, Canada and Mexico exhibit greater price sensitivity, with mass-market products dominating outside major metropolitan areas. While growth in established sports like baseball and basketball is slowing due to market saturation, the rapid rise of pickleball among middle-aged adults is creating a new bag category characterized by modest volumes but higher unit prices.

The Asia-Pacific region is expanding at an annual growth rate of 9.07% during 2026-2031, making it the fastest-growing segment. China's expansion of soccer academies, India's investments in cricket infrastructure, and significant investments by Middle Eastern sovereign wealth funds are driving this growth. Saudi Arabia is targeting substantial growth in domestic sports revenue by the end of the decade. India's cricket gear market, valued at millions in 2025, is expected to grow significantly by 2034, supported by increased budgets for women's cricket equipment following the launch of the Women's Premier League. Saudi Arabia has made notable progress in women's sports, establishing hundreds of centers, enrolling a significant number of girls in football leagues, and increasing participation in the Riyadh Marathon in 2024. Since 2021, there has been a substantial rise in professional female players, clubs, and national teams. Meanwhile, Japan and Australia, with their well-established markets, prefer premium, durable products. In contrast, Southeast Asia, supported by a growing middle class and infrastructure investments in countries like Indonesia, Thailand, and Singapore, is witnessing increasing demand for mass-market offerings.

Europe maintains steady growth, driven by soccer's dominance and established retail infrastructure. However, Per- and Polyfluoroalkyl Substances (PFAS) regulations are prompting reformulation and increasing compliance costs. France's Decree No. 2025-1376, effective January 1, 2026, limits individual PFAS to 25 parts per billion and total PFAS, including polymers, to 50 parts per million, with a 12-month clearance period for products manufactured before the deadline. The European Union's EN 17681-1:2025 testing standard, published on April 30, 2025, introduces alkaline hydrolysis to detect polymer-embedded PFAS. This has increased testing costs to USD 500-1,500 per sample and revealed previously hidden fluorine in water-repellent treatments. Germany, the United Kingdom, France, Italy, and Spain lead in sustainability adoption, with consumers willing to pay 15-25% premiums for recycled materials and third-party certifications like Bluesign and OEKO-TEX. However, mass-market brands face challenges in passing on cost increases without losing market share to Decathlon's vertically integrated private labels. South America exhibits moderate growth, with Brazil and Argentina driving demand for soccer bags, while Colombia and Chile show rising interest in outdoor and adventure sports. The Middle East and Africa benefit from sovereign investments in Saudi Arabia, the United Arab Emirates (UAE), South Africa, and Nigeria. However, infrastructure gaps and lower per-capita income constrain premium segment penetration outside major cities.

Competitive Landscape

The Ball Sports Luggage Market shows a moderate level of concentration, with a combination of global companies such as Nike, Adidas, Under Armour, and PUMA, along with regional competitors like Decathlon, Babolat, Wilson, and Osprey. Additionally, new players in the direct-to-consumer segment are utilizing influencer partnerships and creator-led commerce to establish their presence. A significant development in the market was ANTA's acquisition of a major stake in PUMA in January 2026, reflecting a trend toward consolidation and a strategic focus on the Asian market. Key partnerships, such as Pennsylvania State University's decade-long agreement with Adidas starting in July 2026 and Under Armour's extended collaboration with the University of Wisconsin in November 2025, both spanning ten years, highlight the importance of collegiate licensing in increasing brand visibility and driving merchandise sales.

Brands are increasingly focusing on sustainability as a key differentiator. Examples include Osprey's fully recycled NanoTough fabric, Norda's bio-based Dyneema duffel, and Kitworks' fully recycled thermoplastic polyurethane laminated ripstop. These sustainable materials often come at a higher cost compared to traditional options. However, challenges remain, such as the high price of recycled nylon, which is significantly more expensive than virgin nylon, thereby affecting profit margins and slowing its adoption in the mass market.

There is growing potential in designs specifically tailored for women, driven by the significant growth in women's sports revenue in recent years. Projections indicate that the women's sports backpack market could reach a substantial valuation by 2033. Despite this growth, product offerings remain largely male-focused, often overlooking women's preferences for lighter materials, organized compartments, and stylish designs. Emerging disruptors are addressing these gaps while leveraging omnichannel fulfillment and creator partnerships. For example, Academy Sports reported a notable increase in e-commerce sales during the third quarter of 2026, primarily due to fulfilling a significant portion of online orders directly from their stores.

Ball Sports Luggage Industry Leaders

Adidas AG

Nike Inc.

Puma SE

Wilson Sporting Goods Co.

Decathlon S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Crankshooter Lacrosse introduced a ball bag in 2025, featuring 1680D Poly Material for enhanced durability, an upright and steady plastic base with drain holes, high-visibility orange straps, a steel swivel base, and reinforced box stitching with rivets for heavy-duty use. The bag is designed to accommodate up to 75 lacrosse balls, making it suitable for team use.

- February 2025: Elite Sports introduced the Roller BP Big Ball Bag as part of its 2025 series. This roller bag is designed for high-capacity storage, targeting teams and clubs. It features reinforced wheels to handle heavy loads and offers convenient mobility for use on fields or during tournaments.

- January 2025: Genesis Sport introduced the 3-ball modular roller bowling bag, designed to be lighter and more compact than traditional 3-ball rollers. It features a low center of gravity, deep bolstering to minimize ball movement, and six external anchors for attaching modular add-ons, such as shoe or accessory bags, offering customization options to meet the needs of competitive bowlers.

- January 2025: Select Sport introduced a new collection of sports bags, comprising an updated range of multi-sport ball bags. These products feature enhanced durability, ergonomic designs, and sport-specific compartments tailored for soccer, basketball, and other ball sports, aligning with recent trends in the European market.

Global Ball Sports Luggage Market Report Scope

The ball sports luggage market encompasses products designed specifically for sports activities, distinguished from general travel bags by features such as dedicated ball compartments, space for footwear and apparel, multiple storage pockets, ventilation, durable construction, and mobility elements like shoulder straps, handles, or wheels. The market is segmented by product type, including duffel bags, backpacks, wheeled duffel/trolley bags, ball carriers & tubes, and hybrid convertible packs; by sport, covering soccer/football, basketball, baseball/softball, cricket, tennis, volleyball, and others; by end user, categorized into male and female; by category, divided into mass and premium; by distribution channel, including supermarkets/hypermarkets, sports specialty stores, online retail stores, and other distribution channels; and by geography, spanning North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

| Duffel Bags |

| Backpacks |

| Wheeled Duffel/Trolley Bags |

| Ball Carriers & Tubes |

| Hybrid Convertible Packs |

| Soccer/Football |

| Basketball |

| Baseball/Softball |

| Cricket |

| Tennis |

| Volleyball |

| Others |

| Male |

| Female |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Sports Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Duffel Bags | |

| Backpacks | ||

| Wheeled Duffel/Trolley Bags | ||

| Ball Carriers & Tubes | ||

| Hybrid Convertible Packs | ||

| By Sport | Soccer/Football | |

| Basketball | ||

| Baseball/Softball | ||

| Cricket | ||

| Tennis | ||

| Volleyball | ||

| Others | ||

| By End User | Male | |

| Female | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Sports Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global spending on ball-game gear carriers be by 2031?

The Ball sports luggage market is projected to reach USD 5.02 billion by 2031, advancing at 7.79% CAGR from 2026.

Which product type is expanding the fastest?

Backpacks lead growth at an 8.81% CAGR, reflecting consumer demand for hybrid designs that shift from gym to office travel.

Why is Asia-Pacific considered the key growth engine?

China’s soccer academies, India’s cricket boom, and Gulf investment generate a 9.07% regional CAGR, the highest worldwide.

How will PFAS regulations affect suppliers?

France’s 50 ppm fluorine ceiling and California’s AB 1817 ban oblige brands to reformulate water repellents or risk delisting after 2026.

What share do online channels command, and where are they heading?

Online sales represented roughly 15-25% of 2025 U.S. turnover and are rising at 9.86% CAGR as ship-from-store models cut delivery to two days.

Page last updated on: