Europe Luggage Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.69 Billion |

| Market Size (2026) | USD 13.23 Billion |

| Market Size (2031) | USD 16.82 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

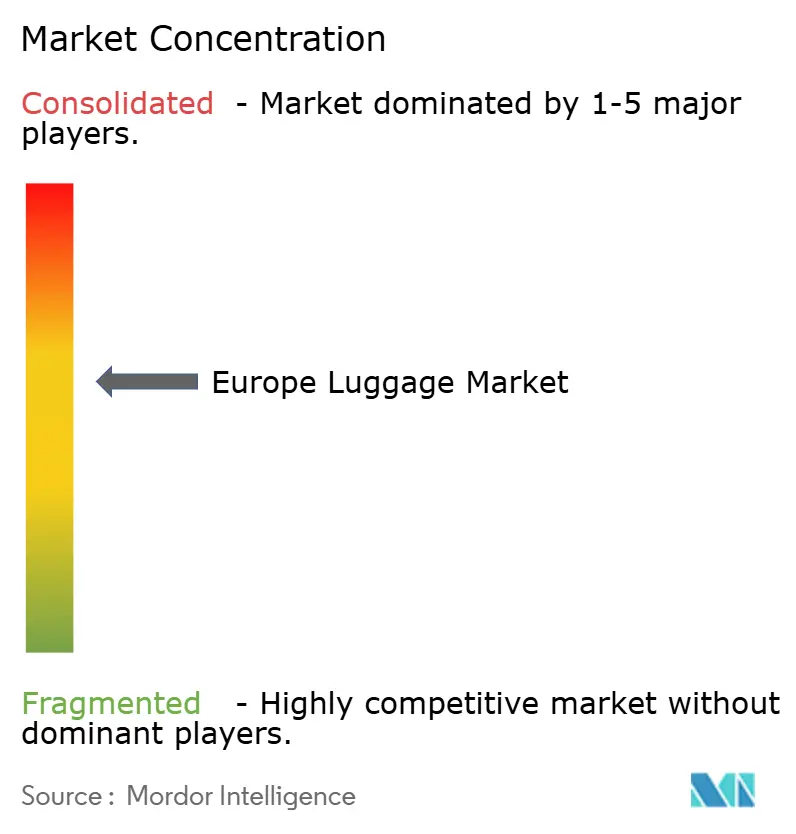

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Luggage Market Analysis by Mordor Intelligence

The Europe luggage market was valued at USD 12.69 billion in 2025 and is estimated at USD 13.23 billion in 2026, projected to reach USD 16.82 billion by 2031, growing at a CAGR of 4.92% during 2026–2031. The market is driven by steady growth in regional and international travel, increasing consumer preference for premium and durable luggage, and ongoing innovation in lightweight materials, smart travel features, and ergonomic product designs. The market is also supported by the growing adoption of sustainable manufacturing practices, with companies increasingly incorporating recycled fabrics, recycled polycarbonate, and environmentally responsible production processes into their product portfolios. The expansion of omnichannel retail and direct-to-consumer sales platforms has improved product accessibility while enabling brands to offer broader product assortments, premium collections, and personalized offerings.

Key Report Takeaways

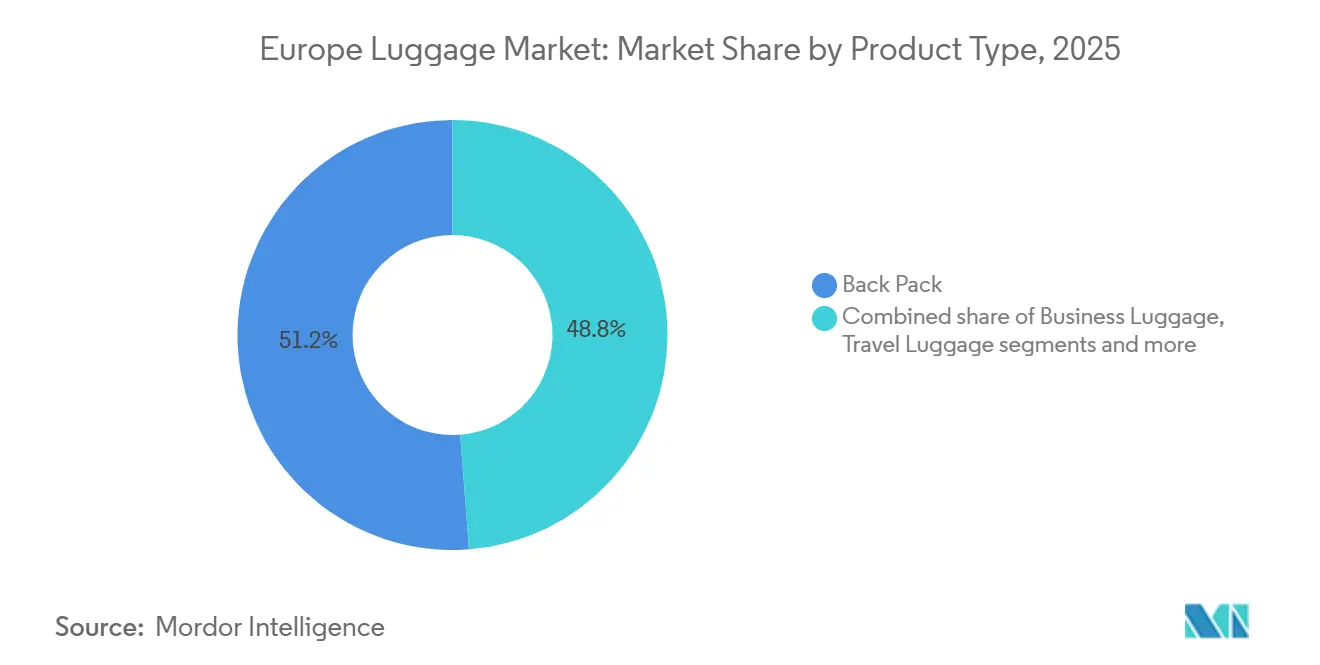

- By product type, backpacks led with 51.23% revenue share in 2025, while travel luggage is forecast to expand at a 5.58% CAGR through 2031.

- By material, soft case held 76.43% share in 2025, while hard case is projected to grow at a 6.54% CAGR through 2031.

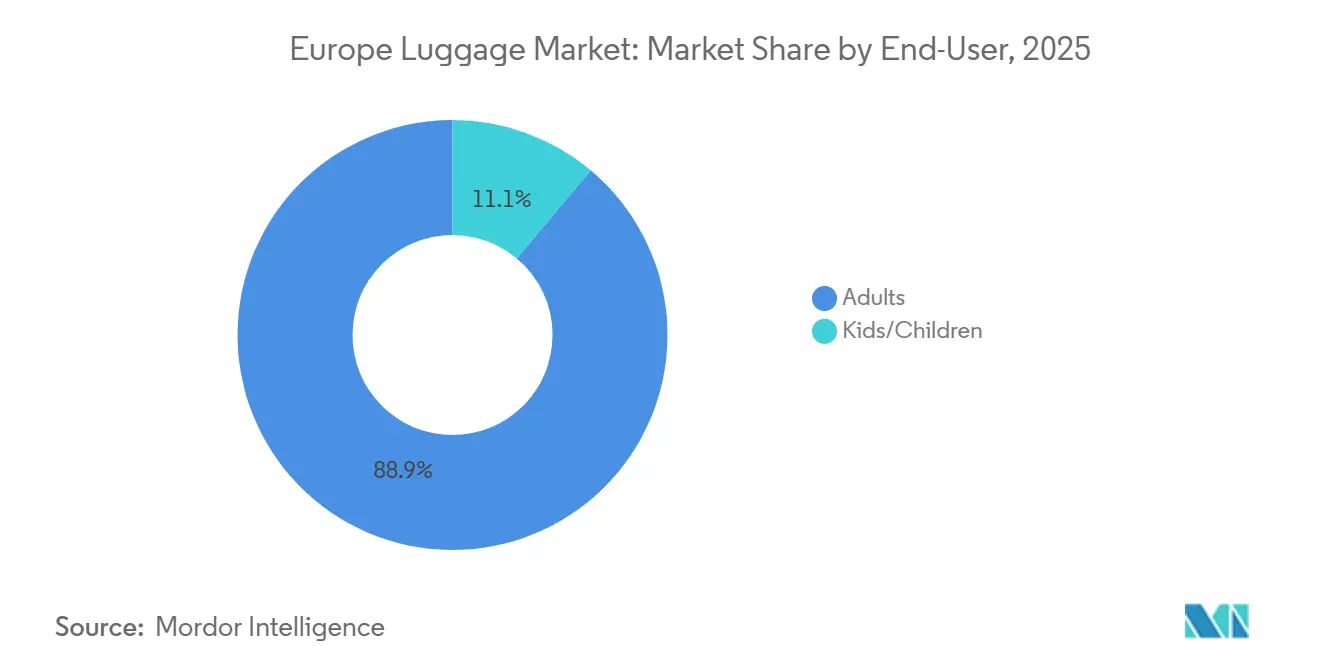

- By end-user, adults accounted for 88.89% share in 2025, while kids and children are advancing at a 6.81% CAGR through 2031.

- By distribution channel, specialty stores accounted for 42.32% share of the Europe luggage market size in 2025, while online retail is advancing at a 7.21% CAGR through 2031.

- By geography, Germany held 22.24% of the Europe luggage market share in 2025, while Poland is forecast to expand at a 6.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Luggage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing outbound and intra-European travel activity | +1.4% | Pan-European; strongest in Germany, France, Spain, Italy | Short term (≤ 2 years) |

| Accelerating adoption of smart luggage technologies | +0.6% | Western Europe core: Germany, United Kingdom, Netherlands, France | Medium term (2–4 years) |

| Strengthening demand for sustainable and recycled-material luggage | +0.5% | Pan-Europe; led by Germany, Netherlands, and Nordic markets | Long term (≥ 4 years) |

| Expanding participation in outdoor recreation and sports | +0.7% | Nordic countries, Germany, Austria, France (Alps corridor) | Medium term (2–4 years) |

| Increasing influence of fashion and premium design trends | +0.8% | Italy, France, Germany, Spain; spill-over to Benelux | Long term (≥ 4 years) |

| Rising business travel and hybrid work-related mobility | +0.6% | Germany, United Kingdom, France, Netherlands (major corporate hubs) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing outbound and intra-European travel activity

The steady expansion of outbound and intra-European travel directly supports demand for new and replacement luggage. Higher volumes of leisure, business, and short-duration trips are encouraging consumers to purchase luggage that is lightweight, durable, and suited to different travel requirements. Frequent travel also accelerates product wear and tear, resulting in shorter replacement cycles and greater demand for upgraded luggage with improved mobility, storage efficiency, and security. Evolving travel patterns have also increased consumer preference for specialized luggage formats designed for varying trip durations and transport modes. According to Eurostat, tourist accommodation establishments across the European Union recorded nearly 3.1 billion overnight stays in 2024, representing a 2.2% increase compared with the previous year, highlighting the continued strength of regional travel activity that supports sustained growth in the Europe luggage market [1]Source: Eurostat, "Another record year for EU tourism in 2025", ec.europa.eu.

Accelerating adoption of smart luggage technologies

The adoption of smart luggage technologies is accelerating as consumers increasingly seek travel products that offer enhanced security, convenience, and connectivity. Manufacturers are integrating advanced features such as GPS tracking, Bluetooth-enabled location services, TSA-approved smart locking systems, USB charging ports, digital weighing systems, and app-based monitoring to improve the overall travel experience. These features help reduce the risk of lost baggage, simplify luggage management, and provide greater peace of mind for travelers. The growing emphasis on connected travel solutions is also encouraging consumers to upgrade from conventional luggage to technology-enabled alternatives with premium functionality. For instance, Safari offers the Trackr GPS Enabled Black Trolley Bag, featuring a BoAt smart tracking tag, TSA lock, dual-spinner wheels, and an organized interior with a dedicated wet pouch, reflecting the industry's increasing focus on integrating smart technologies into modern luggage solutions.

Strengthening demand for sustainable and recycled-material luggage

Growing demand for sustainable and recycled-material luggage is prompting manufacturers to redesign products using environmentally responsible materials and circular manufacturing practices. Consumers are increasingly prioritizing luggage that combines durability with reduced environmental impact, driving adoption of recycled polyester fabrics, recycled polycarbonate shells, water-based coatings, bio-based materials, and repairable product designs. In response, manufacturers are investing in eco-friendly production processes, reducing packaging waste, and incorporating recycled components without compromising product performance or aesthetics. Sustainability has also become an important factor in product differentiation, prompting brands to expand environmentally conscious product portfolios and strengthen long-term competitiveness.

Expanding participation in outdoor recreation and sports

Growing participation in outdoor recreation and sports is creating sustained demand for specialized luggage designed to carry sports equipment, outdoor gear, and adventure travel essentials. Consumers are increasingly seeking durable, lightweight, and high-capacity luggage with reinforced construction, weather-resistant materials, and organized storage compartments. This trend is encouraging manufacturers to introduce purpose-built travel solutions with enhanced durability, easy mobility, and versatile packing configurations for recreational use. The growing popularity of recreational activities is also contributing to more frequent replacement purchases as consumers invest in luggage tailored to different travel and outdoor requirements. According to Sport England, around 2.3 million people in England participated in leisure activities and games in 2024, reflecting rising engagement in active lifestyles that continues to support demand for functional and performance-oriented luggage across Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising threat of counterfeit and unbranded luggage products | -0.3% | Italy, Spain, France, Poland, Netherlands (primary seizure countries) | Short term (≤ 2 years) |

| Stringent environmental regulations on synthetic materials | -0.2% | Pan-Europe; compliance burden concentrated in Germany and France | Medium term (2–4 years) |

| Volatility in raw material prices | -0.1% | Global supply-chain impact; Europe manufacturers exposed | Short term (≤ 2 years) |

| Seasonal fluctuations in travel demand | -0.1% | Southern Europe (Spain, Italy) seasonally pronounced | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising threat of counterfeit and unbranded luggage products

The growing availability of counterfeit and unbranded luggage products is restraining the growth of the Europe luggage market by eroding consumer confidence and intensifying competition for established manufacturers. Counterfeit products often imitate premium designs at significantly lower prices while compromising on material quality, durability, and safety standards, making it difficult for branded companies to differentiate their offerings. The widespread circulation of counterfeit luggage also weakens brand equity, reduces legitimate sales, and discourages investment in product innovation and premium positioning. In addition, counterfeit products can negatively affect consumer perceptions of genuine brands when inferior-quality imitations fail to meet performance expectations. According to the European Union Intellectual Property Office (EUIPO), EU authorities intercepted approximately 112 million counterfeit goods in 2024, highlighting the persistent challenge posed by counterfeit products across consumer goods industries, including luggage [2]Source: European Union Intellectual Property Office (EUIPO), "European Union detains 112 million counterfeit items worth €3.8 billion in 2024", euipo.europa.eu.

Stringent environmental regulations on synthetic materials

Stringent environmental regulations on synthetic materials are restraining the Europe luggage market by increasing compliance requirements for manufacturers that rely on conventional plastics, synthetic fabrics, and chemical-based coatings. Manufacturers are required to reformulate materials, adopt safer chemical alternatives, improve product recyclability, and comply with evolving sustainability standards, resulting in longer product development cycles and higher certification and testing costs. The transition toward recycled and low-impact materials also requires significant investment in manufacturing processes, supplier qualification, and material validation to maintain product durability and performance. These regulatory obligations increase operational complexity, can delay the commercialization of new luggage products, and raise overall production costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Travel Luggage Gains Ground While Backpacks Anchor Volume

Backpacks accounted for a 51.23% revenue share in 2025, supported by their dual utility across daily use and short-duration travel, making them one of the most versatile luggage formats. Their dominance reflects shifting consumer preferences toward lightweight, compact, and multifunctional travel solutions that offer convenience and comfort. Advancements in ergonomic design, organized storage systems, anti-theft features, RFID-protected compartments, integrated USB charging ports, and weather-resistant materials have enhanced product functionality and user experience. Manufacturers are also introducing premium finishes, sustainable recycled fabrics, and modular designs to meet consumer demand for durability, style, and environmental responsibility.

Travel luggage is projected to register the fastest CAGR of 5.58% during 2026–2031, driven by evolving consumer preferences toward purpose-built, durable, and convenience-oriented luggage solutions. Consumers are increasingly seeking products that combine lightweight construction, high storage efficiency, enhanced maneuverability, and advanced security features to support diverse travel needs. Product innovation in hard-shell materials, expandable storage, silent spinner wheels, TSA-approved locking systems, and impact-resistant designs is improving product performance and extending product lifespan. Growing consumer preference for premium luggage with modern aesthetics, sustainable materials, and smart organizational features is driving replacement purchases and value-added upgrades.

By Material: Soft Case Dominates, Hard Case Accelerates on Premiumisation

Soft case products held a 76.43% share of the Europe luggage market in 2025, driven by their flexibility, compressibility, and practical storage advantages. Their ability to accommodate irregularly shaped items and maximize packing capacity makes them well-suited for travelers who need adaptable luggage. Multiple external pockets, expandable compartments, and easy-access storage improve packing efficiency and convenience, while lighter construction enhances portability during transit. The availability of diverse sizes, styles, and price points has broadened consumer adoption across different travel occasions. Ongoing improvements in high-strength woven fabrics, water-repellent coatings, abrasion resistance, and reinforced stitching have enhanced durability, supporting the continued dominance of soft case luggage in the market.

Hard case luggage is projected to register the fastest CAGR of 6.54% during 2026–2031, supported by growing consumer preference for luggage that offers structural protection and long-term durability. Consumers increasingly value rigid-shell construction for its ability to protect fragile and high-value items against impact, pressure, and rough handling. Advancements in polycarbonate composites, lightweight shells, scratch-resistant finishes, and reinforced frame engineering are improving performance and product longevity without significantly increasing weight. Premium aesthetics, minimalist designs, and improved manufacturing technologies are further strengthening consumer appeal, while innovations in shell construction and surface finishes continue to position hard case luggage as a preferred choice for quality-focused buyers.

By End-User: Kids Segment Emerges as the Fastest Growth Vector

Adults accounted for 88.89% of the Europe luggage market revenue in 2025, reflecting the broad diversity of luggage requirements across professional, leisure, and lifestyle-driven travel needs. The segment benefits from continuous demand for products designed to accommodate varying trip durations, storage capacities, and functional requirements, while offering durability and carrying comfort. Premium product positioning, evolving design aesthetics, and the availability of specialized luggage formats have encouraged consumers to invest in purpose-specific travel gear rather than relying on a single luggage type. The introduction of advanced organizational features, ergonomic handling systems, lightweight construction, and premium finishes has further elevated product value, supporting sustained market leadership.

The kids/children segment is projected to register the fastest CAGR of 6.81% during 2026–2031, supported by rising demand for age-appropriate luggage that combines functionality with engaging design. Manufacturers are increasingly introducing compact, lightweight products with child-friendly dimensions, easy-rolling mechanisms, adjustable handles, and enhanced safety features to improve usability during travel. Strong emphasis on licensed characters, vibrant colors, interactive designs, and durable construction has expanded product appeal while encouraging premium purchases. Continuous innovation in ergonomic design, scratch-resistant materials, and easy-to-clean surfaces is further strengthening the value proposition, enabling the segment to achieve robust growth over the forecast period.

By Distribution Channel: Specialty Stores Lead Volume; Online Rewrites the Growth Trajectory

Specialty stores held a 42.32% share of the Europe luggage market in 2025, supported by consumers' preference for in-person product evaluation before purchase. Luggage is a high-involvement product where buyers often assess factors such as size, weight, maneuverability, storage capacity, material quality, wheel performance, and handle ergonomics before making a purchase decision. Dedicated retail outlets offer a broader assortment of luggage categories, premium collections, and expert product guidance, enabling consumers to compare features and identify products that best match their travel requirements. Immediate product availability, after-sales assistance, repair services, and personalized recommendations further strengthen consumer confidence, reinforcing the channel's dominant position in the market.

Online retail is projected to register the fastest CAGR of 7.21% during 2026–2031, driven by the rapid digitalization of shopping experiences and continuous improvements in e-commerce capabilities. Advanced product visualization, detailed specifications, virtual comparisons, customer reviews, AI-powered recommendations, and flexible delivery and return options have significantly improved purchasing convenience. The availability of extensive product assortments, exclusive online launches, customization options, and transparent price comparisons enables consumers to evaluate multiple alternatives efficiently. Continuous investments in digital platforms, omnichannel fulfillment, and faster logistics are further improving the online purchasing experience, supporting the channel's growth throughout the forecast period.

Geography Analysis

Germany accounted for 22.24% of the Europe luggage market revenue in 2025, supported by strong consumer preference for premium, durable, and high-quality travel products. The market benefits from a mature retail ecosystem, widespread availability of premium luggage collections, and high replacement demand driven by evolving product design and innovation. Consumers place significant emphasis on craftsmanship, functionality, and long-term product reliability, sustaining demand for premium luggage. This preference is reflected in ownership trends, with IfD Allensbach reporting that around 2.3 million people in Germany owned valuable luggage pieces in 2025, compared with approximately 2.2 million in 2024, highlighting the country's strong inclination toward premium travel accessories [3]Source: IfD Allensbach, "Number of people in Germany owning valuable luggage", ifd-allensbach.de.

Poland is projected to register the fastest CAGR of 6.39% during 2026–2031, driven by the rapid modernization of its retail landscape and increasing availability of international and premium luggage brands. The market is benefiting from expanding e-commerce penetration, wider product assortments, and rising consumer preference for feature-rich and design-oriented luggage. Continuous investments in organized retail, digital commerce platforms, and omnichannel distribution are improving product accessibility and accelerating adoption of innovative luggage formats. Growing demand for lightweight, durable, and technologically enhanced travel products is expected to support sustained market expansion throughout the forecast period.

The United Kingdom, Spain, Italy, the Netherlands, and other European countries continue to contribute significantly to regional market development through strong product innovation, evolving consumer preferences, and an established premium travel goods ecosystem. Demand across these markets is supported by increasing adoption of sustainable materials, smart luggage technologies, and premium design aesthetics that encourage product upgrades and replacement purchases. Retailers and manufacturers continue to expand product portfolios with lightweight materials, enhanced security features, and multifunctional designs, while omnichannel retail strategies improve product reach and customer engagement. The continued emphasis on quality, innovation, and differentiated product offerings is reinforcing the overall growth trajectory of the Europe luggage market.

Competitive Landscape

The Europe luggage market is moderately consolidated in the premium segment and fragmented across the mid-range and value segments, with competition centered on product innovation, brand positioning, material technology, and omnichannel distribution capabilities. Leading participants, including Samsonite International S.A., Delsey S.A., VF Corporation, LVMH Moët Hennessy Louis Vuitton, and Travelpro Products, Inc., compete by continuously expanding premium product portfolios, integrating advanced materials, and enhancing product durability and functionality. Samsonite International S.A. maintains the broadest distribution footprint among leading luggage manufacturers, operating 1,150 company-operated retail stores globally as of December 2025.

Rather than competing primarily on price, manufacturers are focusing on differentiated product design, lightweight construction, premium aesthetics, and value-added features to strengthen brand loyalty and maintain competitive positioning. Market participants are increasingly strengthening their competitive positions through direct-to-consumer channels, exclusive retail partnerships, and omnichannel strategies that provide consistent consumer experiences across physical and digital platforms. Companies are also investing in premium retail concepts, product customization, after-sales services, and digital engagement initiatives to improve customer retention and enhance brand visibility across Europe.

Competition is increasingly being shaped by materials innovation and intellectual property development, with manufacturers investing in next-generation luggage technologies that enhance durability, security, and user convenience. Patent activity surrounding smart-locking systems, lightweight composite materials, impact-resistant shell technologies, modular luggage architectures, and advanced wheel and handle mechanisms is intensifying, reflecting the industry's focus on technological differentiation. Sustainability has also become a key competitive factor, driving innovation in recycled materials, low-impact manufacturing processes, repairable product designs, and circular product development strategies that strengthen long-term market competitiveness.

Europe Luggage Industry Leaders

-

Samsonite International S.A.

-

Delsey S.A.

-

VF Corporation

-

LVMH Moët Hennessy Louis Vuitton

-

Travelpro Products, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Rimowa unveiled two new seasonal colorways – Orange and Magenta – across its Essential suitcase collection and Groove leather bag range. These additions offer a fresh take on luxury travel accessories.

- April 2026: Air France, in collaboration with DELSEY PARIS, unveiled a new range of baggage and travel accessories called 'Elegance'. Designed as a signature collection embodying the French art of travel, it brings together the expertise and craftsmanship of both brands to serve travelers across all journeys.

- July 2025: Victorinox launched the Altmont Modern collection, which delivers versatile travel essentials suitable for both business commutes and personal travel. Each bag features a gender-neutral and functional design. Backpacks and daypacks include a removable laptop sleeve compatible with 15.6-inch devices.

Europe Luggage Market Report Scope

Luggage refers to the suitcases, bags, and containers used to carry personal belongings when traveling. The Europe luggage market is segmented by product type, material, end-user, distribution channel, and geography. Based on product type, the market is segmented into travel luggage, business luggage, sports luggage, and backpacks. Based on material, the market is segmented into hard case and soft case. Based on end-user, the market is segmented into adults and kids/children. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into Germany, the United Kingdom, Italy, France, Spain, the Netherlands, Poland, Belgium, Sweden, and the Rest of Europe. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Travel Luggage |

| Business Luggage |

| Sports Luggage |

| Back Pack |

| Hard Case |

| Soft Case |

| Adults |

| Kids/Children |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Travel Luggage |

| Business Luggage | |

| Sports Luggage | |

| Back Pack | |

| By Material | Hard Case |

| Soft Case | |

| By End-User | Adults |

| Kids/Children | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the expected size of the Europe luggage space by 2031?

It is forecast to reach USD 16.82 billion by 2031, rising from USD 13.23 billion in 2026 at a 4.9% CAGR.

Which product category leads demand across Europe?

Backpacks led in 2025 with 51.23% revenue share, supported by commuting, campus use, and short-trip utility.

Which sales channel is growing the fastest?

Online retail is the fastest-growing channel, with a projected 7.21% CAGR through 2031, while specialty stores still led with 42.32% share in 2025.

Which country currently leads regional demand?

Germany led with 22.24% share in 2025, supported by the largest travel base in the EU and steady branded luggage demand.

Page last updated on: