Travel Bag Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 19.5 Billion |

| Market Size (2031) | USD 27.03 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

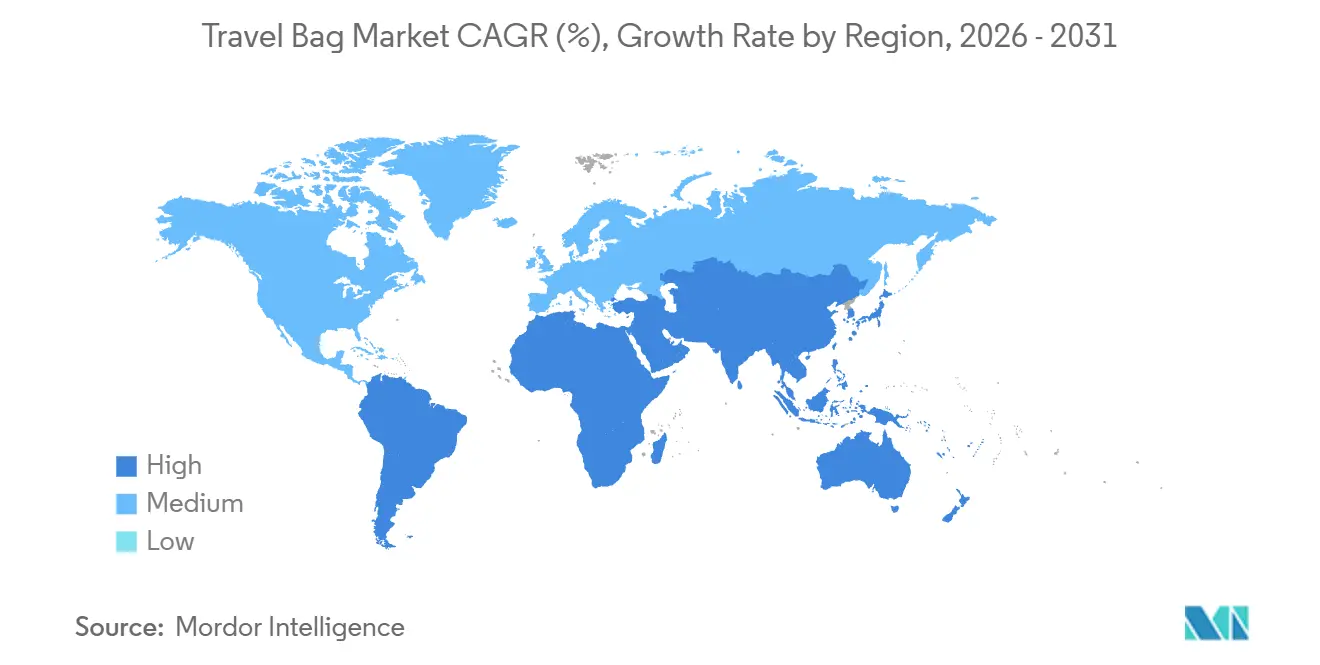

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Travel Bag Market Analysis by Mordor Intelligence

The travel bag market size is projected to expand from USD 18.27 billion in 2025 and USD 19.50 billion in 2026 to USD 27.03 billion by 2031, registering a CAGR of 6.75% between 2026 and 2031. Consistent recovery in global tourism, stricter airline cabin-baggage rules, and sustainability preferences are reshaping product design, channel strategy, and regional growth prospects. Polycarbonate weight-reduction breakthroughs, direct-to-consumer positioning, and carbon-neutral lines reinforce premiumization, while unorganized players and petrochemical volatility pressure margins. Private-equity acquisitions, airline–brand collaborations, and smart-luggage features illustrate an increasingly strategic competitive landscape for the travel bag market.

Key Report Takeaways

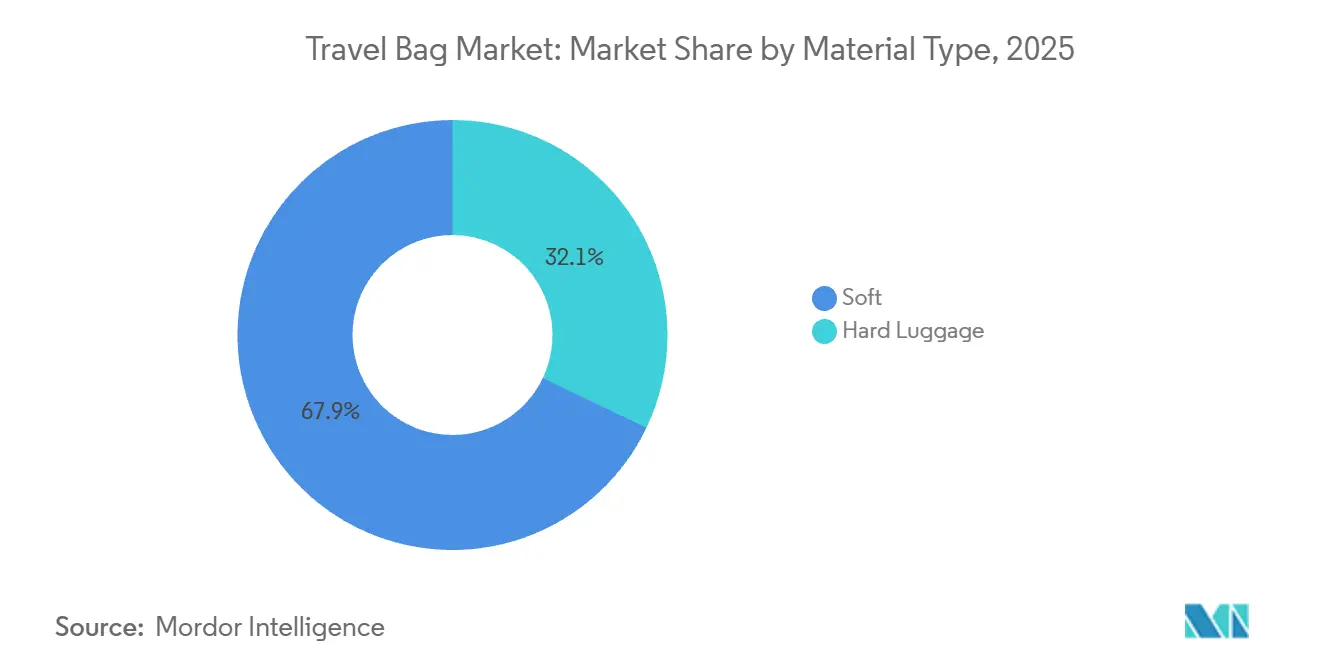

- By material type, soft-sided bags dominated with 67.90% revenue share in 2025, while hard-shell variants are forecast to register the fastest 7.02% CAGR through 2031.

- By end user, adults accounted for 91.87% of 2025 demand, whereas the kids segment is projected to expand at a 7.5% CAGR to 2031.

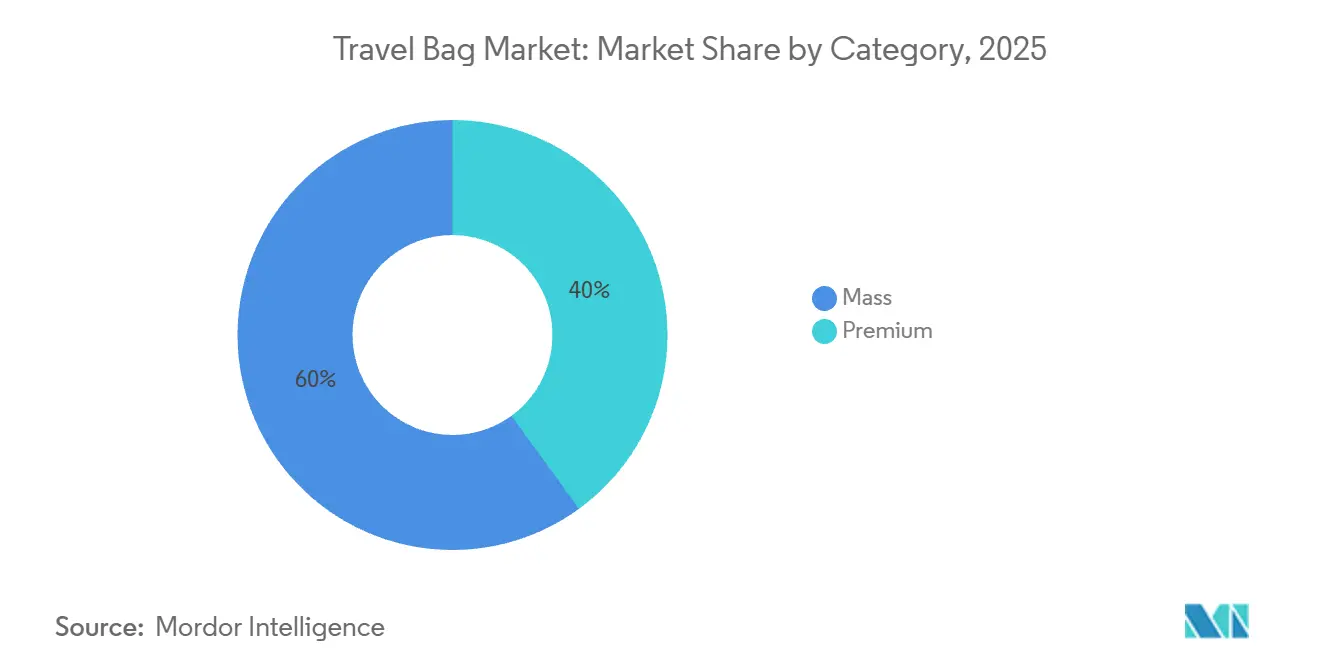

- By category, the mass segment captured 60.02% of 2025 revenue, but premium offerings are expected to grow at an 8.92% CAGR over 2026-2031.

- By distribution channel, offline retail stores held 66.82% of 2025 sales, yet online channels are poised for a 7.99% CAGR through 2031.

- By geography, North America led with 41.98% of 2025 revenue, while the Middle East and Africa region is set to post the highest 8.23% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Travel Bag Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adventure and experiential travel trends | +1.2% | Global, with peak growth in Asia-Pacific, Middle East, and South America | Medium term (2-4 years) |

| Low-cost carrier expansion stimulating lightweight carry-on sales | +0.9% | Europe, Asia-Pacific core, spill-over to Middle East and North Africa | Short term (≤ 2 years) |

| Rapid e-commerce cross-border shipping of baggage and packaging solutions | +0.8% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Rising global tourism and travel frequency | +1.5% | Global, led by Middle East, Africa, and Asia-Pacific | Long term (≥ 4 years) |

| Technological innovations and smart features | +0.7% | North America, Europe, affluent Asia-Pacific markets | Medium term (2-4 years) |

| Carbon-neutral luggage lines capturing sustainability-led consumer switch | +1.0% | North America, Western Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adventure and Experiential Travel Trends

As travelers increasingly prioritize gear that can endure rugged environments, luggage design is shifting towards durability and modularity, moving away from traditional hard-shell aesthetics. From 2020 to 2025, the global adventure travel sector experienced a robust annual growth rate of 15%, outpacing the leisure travel segment[1]Source: Adventure Travel Trade Association, "Unlocking the potential of outdoor and active travel to change the world", adventuretravel.biz. Notably, millennials and Gen Z made up a significant 62% of these bookings. In response to this demographic trend, brands are introducing hybrid products. For instance, Osprey's Transporter series melds the flexibility of soft-shells with the protective zones of hard-shells, even incorporating backpack harness systems into wheeled luggage for versatile journeys. Reflecting this shift, Samsonite revealed that a notable 40% of its 2024 sales stemmed from products made with recycled materials, catering to adventure travelers who prioritize sustainability alongside performance. Furthermore, there's a rising demand for smaller bags that comply with carry-on restrictions. This trend aligns with adventure travelers' preference for budget airlines, allowing them to invest more in experiences rather than incurring checked-baggage fees.

Low-Cost Carrier Expansion Stimulating Lightweight Carry-On Sales

In 2025, low-cost carriers tightened cabin-bag policies, with 42% of passengers paying an average gate fee of EUR 47 (USD 51) for oversized carry-ons, up from 38% in 2024, according to the European Consumer Organisation. Ryanair restricted free cabin bags to 40 cm × 20 cm × 25 cm unless priority boarding was purchased, while Spirit and Frontier in the U.S. reduced personal-item sizes to 45 cm × 35 cm × 20 cm. These changes pushed manufacturers to create compact designs maximizing internal space. Travelers are shifting from 55 cm spinners to lighter 50 cm and 48 cm models, offering 30-35 liters of capacity with features like compression panels and expandable compartments. In April 2026, Delsey Paris launched its "Elegance" collection with Air France, featuring IATA-compliant cabin suitcases priced from EUR 249 (USD 270) and lined with 100% recycled polyester. This targets the 68% of European travelers who check luggage dimensions online before buying. The rise of low-cost carriers is also boosting demand for hard-shell carry-ons, as polycarbonate models better withstand overhead-bin compression, reducing warranty claims and improving brand reputation.

Rapid E-Commerce Cross-Border Shipping of Baggage and Packaging Solutions

Cross-border e-commerce is changing how luggage is distributed by helping brands avoid traditional retail markups and connect with cost-conscious consumers in emerging markets. In 2025, FedEx shared an example of a European luggage manufacturer that reduced shipping costs by 40% and increased export volumes by 20% using its International Connect Plus service. This service consolidates small parcels at regional hubs before delivering them to the final destination, making the process more efficient. This model works particularly well for direct-to-consumer (DTC) brands like Monos. Monos ships products directly from Chinese contract manufacturers to customers in North America and Europe, reducing delivery times to 7-10 days compared to the 30-45 days required for container shipments to retail warehouses. However, cross-border sellers face challenges such as customs delays caused by errors in HS code classification and the need for packaging that complies with local regulations. For example, the EU's Single-Use Plastics Directive bans certain foam inserts, requiring sellers to use alternative materials.

Rising Global Tourism and Travel Frequency

Global tourism is recovering faster than expected, with international arrivals projected to reach 1.52 billion by 2025, just 2% below the 2019 peak. Tourism revenues have already exceeded pre-pandemic levels, reaching USD 1.9 trillion, an 8% increase driven by higher spending per trip. Business travel in 2025 has shown strong growth, increasing by 55% in Saudi Arabia and 23% across the Middle East. This growth is largely due to the return of corporate events and government-backed conferences aimed at supporting economic diversification initiatives[2]Source: Saudi Tourism Authority, “Tourism Statistics 2025,” saudi tourism.sa. Frequent travelers are now replacing their luggage more frequently, with the replacement cycle shortening to 3.5 years from 5 years before the pandemic, as per industry surveys. Premium luggage brands are gaining from this trend, as travelers who fly more than six times a year are 2.3 times more likely to purchase luggage priced above USD 300. These buyers prioritize features such as TSA-approved locks, USB charging ports, and lifetime warranties, which justify the higher price. According to IATA data, air passenger demand grew by 5.3% in 2025, with the Asia-Pacific region leading at 7.8% growth and Africa following with a 9.4% increase. This trend reflects the growing participation of middle-class consumers in emerging markets, many of whom are entering the replacement-purchase cycle for the first time.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dominance of unorganized low-end players | -0.6% | Asia-Pacific, Middle East, Africa, South America | Long term (≥ 4 years) |

| Counterfeit branded bags diluting premium price realization | -0.5% | Global, concentrated in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Volatile petrochemical prices inflating ABS/PC resin costs | -0.7% | Global, acute in Asia-Pacific and Europe manufacturing hubs | Short term (≤ 2 years) |

| Regulatory pressures on materials and safety | -0.4% | North America, Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dominance of Unorganized Low-End Players

Unorganized manufacturers dominate price-sensitive markets like India, Indonesia, and Nigeria, controlling 40-50% of unit volumes by offering products 30-50% cheaper than branded players through informal distribution and low quality-control costs. In fiscal 2024, VIP Industries held over 50% of India's branded luggage market, but its revenue in calendar 2024 fell 18% year-on-year to USD 210 million due to competition from unorganized players selling soft-shell bags at Rs 800-1,200 (USD 10-14), compared to VIP's Rs 2,500-4,000 (USD 30-48) models. These unorganized players rarely invest in R&D or sustainable materials, creating a two-tier market where urban consumers pay premiums for warranties and design, while rural buyers opt for cheaper, short-lived products. VIP's 32% stake sale to a Multiples Equity-led consortium for Rs 1,437.78 crore (USD 173 million) in August 2025 signals confidence in market formalization, driven by stricter e-commerce quality standards and improved tax compliance.

Counterfeit branded bags diluting premium price realization

Counterfeit luggage weakens brand equity and pricing power. The OECD reports global counterfeit trade at USD 467 billion annually, over 2% of world imports, with luxury handbags and leather goods among the top five counterfeit categories. In 2024, U.S. Customs and Border Protection (CBP) seized USD 5 billion worth of counterfeit goods, including "superfakes" priced at USD 1,000-1,500 but mimicking USD 10,000 designer luggage with nearly identical materials and branding[3]Source: U.S. Customs and Border Protection, “Trade and Travel Data,” cbp.gov. In March 2025, CBP in Wilmington, Ohio, intercepted counterfeit Gucci and Louis Vuitton luggage worth USD 151,000, while Louisville seized USD 18.6 million in fake luxury goods in one operation, highlighting the scale of smuggling. Boston Consulting Group suggests using Digital Product Passports (DPPs) and blockchain authentication to fight counterfeits, but costs of USD 2-5 per unit hinder adoption, especially in mass markets. This issue is severe in Asia-Pacific and the Middle East, where counterfeit rates in some price tiers exceed 20%. Legitimate brands are forced to invest in consumer education and enforcement, diverting resources from innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polycarbonate Innovations Drive Hard-Shell Acceleration

In 2025, soft-sided luggage dominated 67.90% of global market revenue due to its affordability, expandability, and lightweight design. Priced at USD 40–80, nylon and polyester duffels are far cheaper than hard-shell options costing USD 120–250, making them popular in cost-sensitive regions like India, Southeast Asia, and Latin America. These bags offer 15–20% extra capacity using external straps, making them ideal for long trips with varying packing needs. Additionally, low-cost carriers’ baggage restrictions favor soft-sided carry-ons, as collapsible duffels fit under seats and help travelers avoid gate-check fees, which 42% of European passengers paid in 2025, averaging EUR 47. However, the EU's REACH directive, which limits phthalates in PVC linings, has pushed manufacturers toward costlier thermoplastic polyurethane alternatives, increasing production costs by 12–18% and reducing profit margins.

Hard-shell luggage is expected to grow at a 7.02% CAGR through 2031, outpacing the overall market. Polycarbonate innovations have reduced weight by 20–30% since 2015 while maintaining durability, making them ideal for checked baggage in cold cargo holds. Covestro’s Makrolon polycarbonate enables thinner shell walls, cutting material costs by 15–20% and meeting airline weight limits for bags under 23 kg. Samsonite’s Curv material, a self-reinforcing polypropylene, provides superior impact absorption. In 2025, Samsonite expanded its Nashik, India plant to produce 700,000 units monthly, with 60% focused on polycarbonate carry-ons. Recycled-content mandates are also driving hard-shell demand. Covestro’s Shanghai facility produces 25,000 tonnes of post-consumer polycarbonate annually, allowing brands to market eco-friendly products with 20–35% price premiums in Western Europe and North America, where 68% of consumers consider environmental impact before purchasing premium luggage. Online shoppers prefer hard-shell luggage for better shipping protection, reducing damage-related returns by 12–18%, while in-store buyers favor soft-sided bags for their flexibility and compressibility.

By End User: Adult Segment Drives Volume While Kids Market Accelerates

In 2025, adults made up 91.87% of end-user demand for luggage, primarily using it as a practical tool for both business and leisure travel. Frequent flyers, who take four or more international trips each year, typically replace their luggage every 3 to 5 years, while occasional travelers do so every 5 to 7 years. Although they constitute only 18% of global passengers, frequent flyers account for a significant 38% of premium luggage purchases. They tend to favor modular ecosystems—like carry-ons, checked bags, and garment sleeves—from a single brand, ensuring both stackability and a cohesive look. Business travelers, justifying price points between USD 200 and USD 400, seek organizational features in their luggage. These include laptop compartments with shock-absorbing foam, garment folders to reduce wrinkles, and USB charging ports integrated into telescoping handles.

Driven by partnerships with Disney, Marvel, and Pixar, the kids' luggage segment is set to grow at a 7.5% CAGR through 2031. These collaborations elevate luggage from mere travel items to coveted products, with retail prices ranging from USD 79 to USD 109. For instance, the Disney Store's Minnie Mouse rolling suitcase is priced at USD 79, while hard-shell models from Samsonite, licensed under Disney's Frozen and Toy Story, retail between USD 89 and USD 129. Such licensing allows these brands to command a 30% to 40% premium over generic kids' luggage, which typically retails between USD 49 and USD 69. The segment enjoys a protective edge against unorganized manufacturers due to regulatory barriers. The U.S. Consumer Product Safety Commission's 16 CFR Part 1500 imposes strict mandates on children's products, including lead-content limits, phthalate restrictions, and small-parts testing. These compliance measures add an estimated USD 5 to USD 10 per unit in costs. Targeting eco-conscious parents, Fūl offers PVC-free kids' luggage priced between USD 59 and USD 79. This niche, emphasizing phthalate-free materials, saw an 18% year-on-year growth in 2025, driven by heightened awareness of chemical safety in children's products.

By Category: Premium Segment Outpaces Mass Market Growth

In 2025, mass-market luggage contributed 60.02% to global revenue, driven by prices between USD 50 and USD 150. These products appeal to consumers in emerging markets seeking replacements and budget-conscious buyers in developed markets, prioritizing functionality over brand prestige. Brands like Samsonite, VIP Industries, and Delsey partner with retailers such as Walmart, Target, and Carrefour to capture seasonal purchases during back-to-school and holiday periods. Mass-market sales are concentrated in Asia-Pacific, Latin America, and Africa, where 70% of revenue comes from consumers replacing luggage every 18-24 months, focusing on affordability over features like lifetime warranties or eco-friendly production. In North America, Black Friday and Cyber Monday discounts of 20-40% drive 35% of annual sales, creating inventory challenges that require manufacturers to maintain 8-12 weeks of safety stock.

Premium luggage is projected to grow at a CAGR of 8.92% through 2031, led by direct-to-consumer brands like Monos, Away, and July. These brands avoid wholesale markups and invest in features like lifetime warranties, sustainable materials, and unique designs to attract affluent millennials. Monos grew its revenue from USD 8 million in 2020 to over USD 150 million in 2024 by selling directly through its website and five U.S. stores in Boston, Los Angeles, Chicago, New York, and Washington D.C., avoiding 40-50% wholesale discounts. Beis reported over USD 40 million in sales in November 2023 and expects 145% growth in 2024, driven by Instagram influencer partnerships costing USD 40-70 per customer acquisition, compared to USD 15-25 for Amazon sellers using organic search. Sustainability is a key focus for premium brands. Paravel’s Aviator line uses recycled plastic bottles and carbon-neutral shipping, while Horizn Studios’ Circle One collection uses BioX plant-based materials, cutting carbon emissions by 30% compared to virgin polycarbonate. These efforts align with 68% of consumers who consider environmental impact when buying premium luggage.

By Distribution Channel: Digital Transformation Accelerates Online Growth

In 2025, offline stores dominated the travel bags market, capturing 66.82% of total revenues. Shoppers prioritize the chance to physically assess product features, like wheel glide smoothness, handle sturdiness, and interior organization, before making significant purchases. Department stores elevate the in-store experience, using interactive displays and RFID-enabled mirrors. These mirrors not only offer packing tutorials but also showcase physical samples, seamlessly merging physical and digital engagement. Additionally, retailers have set up repair drop-off desks, turning routine store visits into opportunities to foster brand loyalty and promote extended product use. Such tactile and service-oriented advantages solidify offline stores' status as pivotal revenue drivers in the travel bags market. Ultimately, offline retail remains crucial for experiential shopping, bolstering consumer confidence in high-ticket bag investments.

On the other hand, online platforms are the market's fastest-growing segment, boasting an 7.99% CAGR. They revolutionize product discovery, evaluation, and post-sale service. With advanced search filters, busy professionals can swiftly compare features, like liter capacity, airline compliance, and smart functionalities—across numerous SKUs in mere minutes. Drop-shipping from bonded warehouses not only slashes import duties but also broadens color options, enhancing both selection and affordability. Social commerce leaps with livestream demonstrations, where influencers conduct real-time stress tests, turning viewer curiosity into instant purchases. Enhanced return logistics now utilize reusable shipping boxes, which conveniently double as home storage solutions, amplifying perceived sustainability. Brands that harness this omnichannel approach effectively blend offline experiential perks with online convenience, broadening their market reach.

Geography Analysis

In 2025, North America accounted for 41.98% of global revenue, supported by the U.S.'s advanced travel infrastructure and high luggage ownership. However, growth is slowing as consumers prioritize durable products and extend replacement cycles. U.S. sales were flat from January to June 2025 after a 6% decline in 2023-2024, reflecting market saturation in urban areas. Canada and Mexico added volume through cross-border tourism and e-commerce, though tariff uncertainties under USMCA renegotiations created pricing challenges for manufacturers relying on Chinese components. Direct-to-consumer brands like Monos (Toronto), Away (New York), and July (San Francisco) capitalized on access to venture capital and affluent consumers, offering premium carry-ons priced at USD 250 to USD 400. North America leads in smart luggage adoption, with 28% of travelers showing interest in GPS-enabled cases, though restrictions on non-removable lithium batteries limit broader adoption.

The Middle East and Africa are expected to grow the fastest, with an 8.23% CAGR through 2031. Saudi Arabia's travel and tourism GDP reached USD 178 billion in 2025, up 7.4% year-on-year, with international arrivals 39% higher than 2019 levels. Vision 2030 projects like NEOM and Red Sea resorts boosted business travel by 55%, while religious tourism to Mecca and Medina sustained demand for durable luggage. The UAE recorded an 8.2% rise in visitor spending, driven by Dubai's role as a global transit hub and Abu Dhabi's cultural investments. Africa saw 81 million arrivals in 2025, an 8% increase, with North Africa leading at 11% growth. Egypt experienced a 20% rise to 19 million visitors, supported by proximity to Europe and favorable currency rates. However, unorganized manufacturers dominate 60-70% of the luggage market in Nigeria, Kenya, and South Africa, limiting international brands' pricing power.

Asia-Pacific, Europe, and South America showed varied trends. China's domestic travel rebounded to 6.2 billion trips in 2025, but luggage sales grew only 3% as consumers focused on experiences over goods. India became Samsonite's largest manufacturing hub, with its Nashik plant exporting 10% of output to Southeast Asia and the Middle East. VIP Industries, holding over 50% market share, faces competition from private-equity-backed consolidations. In Europe, stricter baggage rules by Ryanair and easyJet led 42% of passengers to pay gate fees averaging EUR 47, driving demand for compliant carry-ons. South America's growth remained modest due to currency volatility and tariffs. Brazil's 35% duty on non-Mercosur luggage raised prices by 50-70%, encouraging local assembly by VIP Industries and Safari, though quality gaps persist compared to imports.

Competitive Landscape

The travel bags market is moderately consolidated, with Samsonite leading the way and holding a significant global share. Samsonite's strong position is supported by its portfolio of well-known brands, including American Tourister, Tumi, and Gregory. In 2024, the company reported a gross margin of 60.2%, reflecting its effective pricing strategies and efficient sourcing. However, new players are entering the market, using platforms like Kickstarter and Instagram to introduce minimalist, direct-to-consumer luggage that challenges traditional retail pricing. In response, established companies are acquiring niche brands or launching sub-brands designed to appeal to tech-savvy and digital-first consumers.

Key strategies in the market now focus on sustainability, smart technology, and omnichannel approaches. TUMI has pledged to use 100% renewable energy by 2025 and is introducing products with carbon labeling. Similarly, Horizn Studios is innovating with plant-based flax shells for its luggage. Advanced features like RFID chips, Bluetooth-enabled locks, and Apple Find My compatibility are becoming standard in premium product lines, transforming smart technology from a luxury feature into a necessity.

Collaborations are emerging as a major trend, with luggage manufacturers partnering with airlines and fintech companies. Some brands are adding value by bundling services such as lost-bag insurance and airport lounge access, creating new revenue streams from post-purchase services. Others are integrating NFC tags to simplify bag-drop processes, aligning with the broader trend of airport digitalization. These developments are reshaping the competitive landscape, with a growing focus on combining traditional products with service ecosystems, which is expected to influence future market shares in the travel bags industry.

Travel Bag Industry Leaders

-

Samsonite International S.A

-

VIP Industries Ltd.

-

VF Corporation

-

Delsey Paris

-

LVMH (Moët Hennessy Louis Vuitton)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Black Voyage unveiled its latest luggage: the 28 AirTrunk Suitcase, equipped with Vortex Vacuum-Seal Compression Technology. Crafted from aerospace-grade materials, this suitcase is tailored for elite travelers, offering durability, lightweight design, and advanced compression features that revolutionize the way users pack and travel.

- July 2025: Urban Jungle is broadening its footprint by debuting offline stores, showcasing a range of travel bags. These stores aim to provide customers with a hands-on experience, allowing them to explore the brand's diverse product offerings and make informed purchasing decisions.

- May 2025: CASETiFY introduced its 29 Bounce Check-in Trunk Suitcase, blending premium engineering with a signature flair. Available in various colors, fonts, and exclusive customizable prints, the suitcase empowers travelers to pack freely and embark with assurance. The product is designed to combine functionality with style, catering to the needs of modern travelers who value both practicality and personalization.

- February 2025: Indian brand Uppercase made its U.S. debut, launching the 'Rock' and 'Vector' suitcases. These products merge aesthetics with modern travel needs, offering features such as robust build quality, sleek designs, and practical compartments to enhance the travel experience for consumers in the United States.

Global Travel Bag Market Report Scope

| Hard |

| Soft |

| Adults |

| Kids |

| Mass |

| Premium |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Material Type | Hard | |

| Soft | ||

| By End User | Adults | |

| Kids | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the travel bag market be by 2031?

The travel bag market size is forecast to reach USD 27.03 billion by 2031, expanding at a 6.75% CAGR over 2026-2031.

Which material segment is growing fastest?

Hard-shell polycarbonate luggage is projected to post a 7.02% CAGR through 2031 as weight-saving resins gain favor.

Which region will lead growth?

The Middle East and Africa is expected to register the highest regional CAGR of 8.23% due to Saudi Arabia’s tourism boom

What is driving premium segment expansion?

Direct-to-consumer brands offering lifetime warranties and carbon-neutral lines are growing the premium slice at an 8.92% CAGR through 2031.

Page last updated on: