Bags And Containers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 54.68 Billion |

| Market Size (2031) | USD 74.32 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bags And Containers Market Analysis by Mordor Intelligence

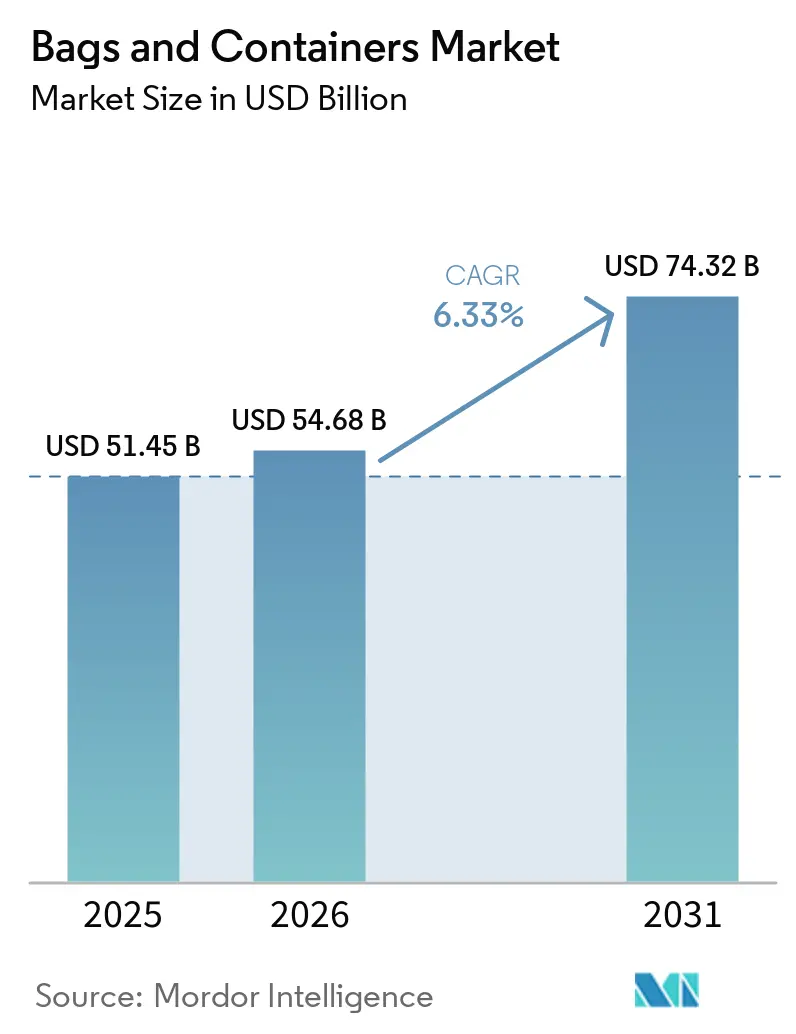

The bags and containers market size is expected to grow from USD 51.45 billion in 2025 to USD 54.68 billion in 2026 and is forecast to reach USD 74.32 billion by 2031 at 6.33% CAGR over 2026-2031. The bags and containers market is supported by demand from e-commerce logistics, food safety needs, and industrial bulk handling, which are changing the packaging formats needed in daily use. Post-pandemic supply chain resets have pushed converters toward broader format portfolios that can serve direct-to-consumer shipments and large industrial distribution from the same asset base. The bags and containers market is also gaining support from pharmaceutical pipeline expansion and from the shift toward recyclable and reusable formats across both bags and containers. Digital labeling rules are adding a new layer of technical complexity because print area, code placement, and material surface quality now matter more on smaller formats. Competitive activity remains active as large players pursue M&A and regional specialists focus on material upgrades, while resin cost pressure and stricter packaging rules remain the main risks during the forecast period.

Key Report Takeaways

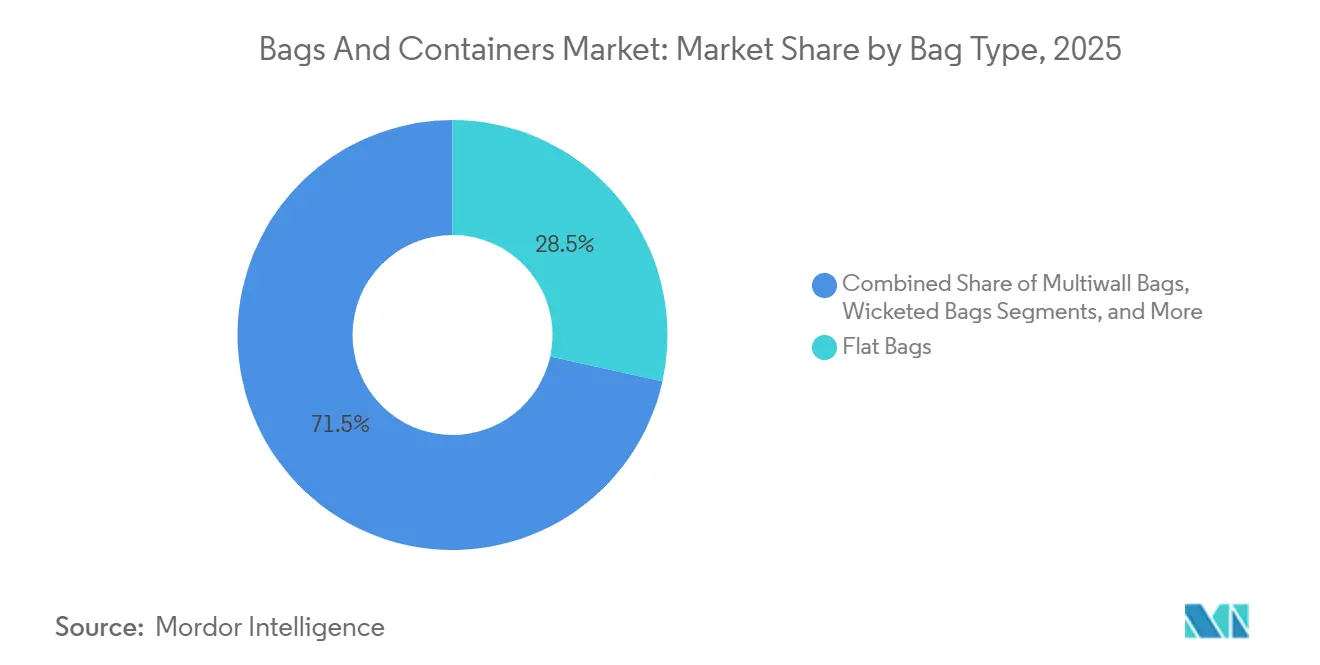

- By bag type, flat bags held 28.46% of the bags and containers market in 2025.

- By container type, the bags and containers market for intermediate bulk containers is expected to grow at a 7.35% CAGR through 2031.

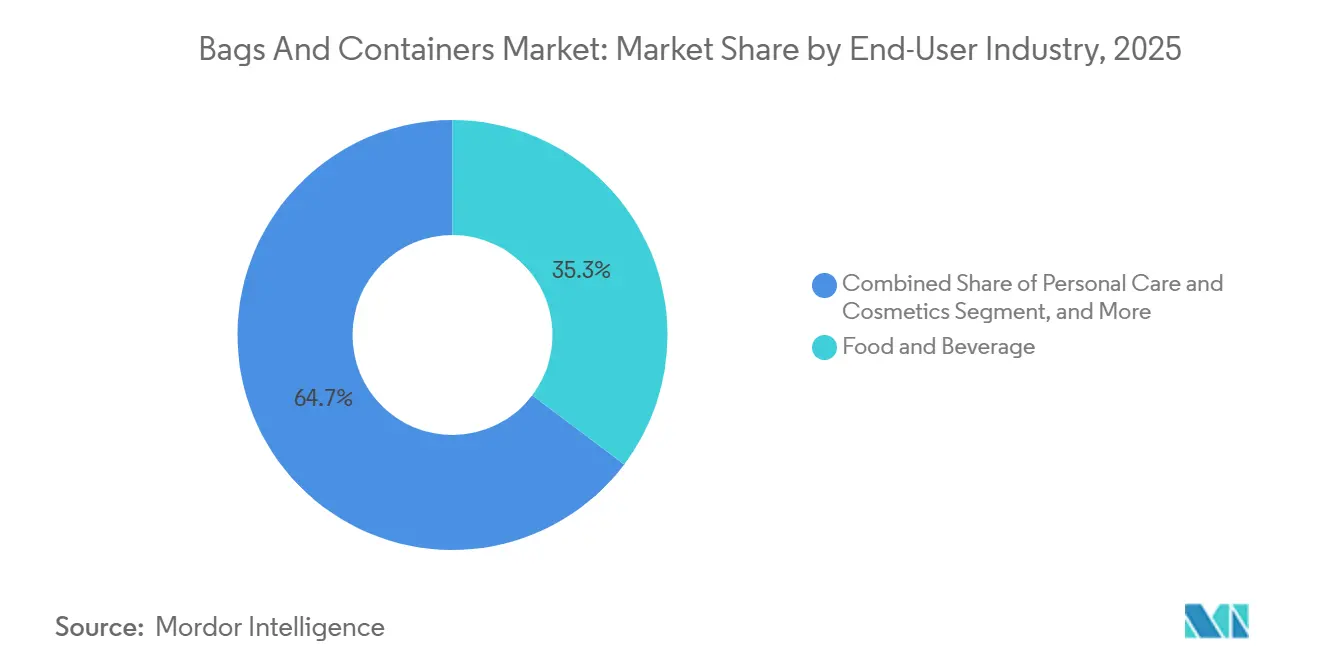

- By end-user industry, the food and beverage industry held 35.28% of the bags and containers market in 2025.

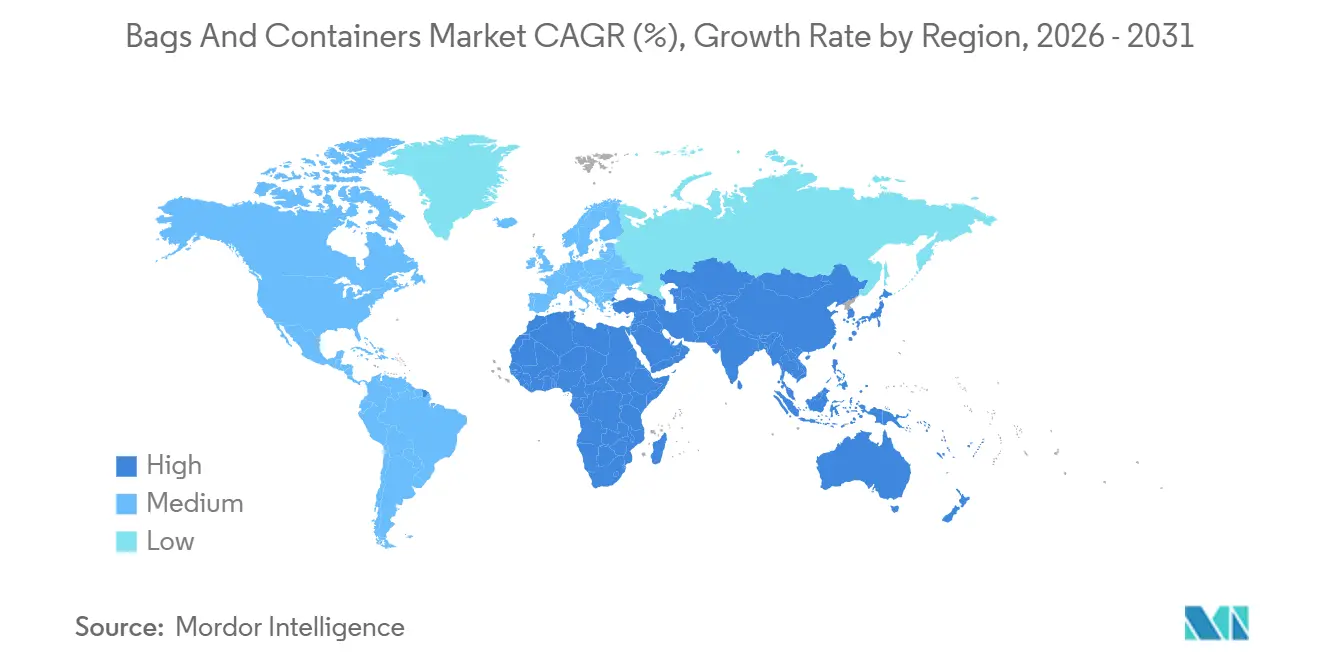

- By geography, the bags and containers market for Asia-Pacific is projected to expand at a 7.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bags And Containers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Fulfillment Driving Demand for Lightweight Protective Packs | +1.5% | North America, Asia-Pacific, Europe | Short term (≤ 2 years) |

| Sustainability Targets Accelerating Recyclable and Reusable Format Adoption | +1.3% | Europe, North America, Global | Medium term (2-4 years) |

| Packaged Food and Delivery Growth Expanding High-Throughput Packaging Volumes | +1.1% | Global, Asia-Pacific core | Short term (≤ 2 years) |

| Healthcare and Pharma Quality Needs Supporting Barrier and Tamper-Evident Formats | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Packaging Data Carriers Becoming Essential Under Traceability and Digital Labeling Rules | +0.6% | Europe, North America, Global | Medium term (2-4 years) |

| Reuse Infrastructure Investments Creating Demand for Returnable Transport Packaging | +0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfillment Driving Demand for Lightweight Protective Packs

E-commerce remains the clearest near-term growth engine for the bags and containers market, as each parcel typically requires its own protective packaging. Direct-to-consumer shipping uses more unit-level packaging than palletized retail movement, which raises demand for mailing bags, padded mailers, and related lightweight protective packs. This shift is also changing capital spending decisions, as converters place more emphasis on automated flexible filling, sealing, and printing lines. The bags and containers market is therefore seeing a gradual move away from purely commodity production toward more application-specific flexible packaging capacity. Mondi opened its new paper bags plant in Pittsburgh in April 2026, with annual ramp-up capacity targeted at 300 million paper bags and a focus on e-commerce, food, feed, and industrial end uses. That type of investment shows that parcel shipping is not only adding volume to the bags-and-containers market but also raising the value of automation and print capabilities.

Sustainability Targets Accelerating Recyclable and Reusable Format Adoption

Sustainability commitments are now shaping packaging selection more directly across the bags and containers market. Amcor reported in FY25 that 72% of its packaging production by weight was designed for recyclability, including 96% of its rigid packaging portfolio and 49% of its flexible packaging portfolio, while it also met its global 10% post-consumer recycled plastic target of 218,000 metric tons.[1]Amcor plc, “Amcor FY25 Sustainability Report Showcases Progress, Leadership and Innovation,” Amcor, amcor.com The Ellen MacArthur Foundation stated that businesses representing 20% of the plastic packaging market recommitted to 2030 targets under the New Plastics Economy Global Commitment, which shows that demand signals are moving through brand procurement plans into converter investment cycles. A practical effect is now visible in format choice: mono-material flexible structures help meet recyclability goals but can also narrow performance options in some applications. That is one reason rigid containers continue to hold strong positions in areas where recycling systems are more established and material recovery is easier to scale. IFCO said in its 2025 ESG reporting that reusable packaging containers delivered measurable reductions in CO₂ emissions and food waste across fresh grocery supply chains, which supports the commercial case for pooled and returnable systems in the bags and containers market.

Packaged Food and Delivery Growth Expanding High-Throughput Packaging Volumes

Food and beverage remained the largest end-user base in 2025, and that scale continues to support the bags and containers market across retail food, delivery, and institutional channels. Growth in the ready-to-eat and ready-to-cook categories is driving demand for formats that combine barrier protection, shelf-life support, and compatibility with automated filling lines. Quick-commerce is adding another layer because packaging now needs to perform across ambient, chilled, and frozen conditions within faster delivery cycles. That pushes suppliers and filling equipment partners toward tighter coordination on substrate properties, sealing performance, and machine tolerance ranges. Amcor advanced a fiber-tray packaging collaboration with Metsä Group and G. Mondini in April 2026, showcasing an integrated tray system that combines molded fiber trays, barrier liners, and top web films to reduce plastic use in protein and chilled ready-meal applications. Developments like this show that the bags and containers market is growing not only through higher packaged food volumes, but also through a steady rise in format complexity.

Healthcare and Pharma Quality Needs Supporting Barrier and Tamper-Evident Formats

Healthcare is becoming one of the strongest quality-driven demand pools in the bags and containers market. Biologics, biosimilars, and advanced therapies require sterile barriers, strong moisture control, and reliable tamper-evident performance, which raises the technical threshold for both bags and rigid formats. A 2025 review in AAPS PharmSciTech highlighted the growing use of advanced barrier materials and coatings in pharmaceutical packaging, including structures designed for greater protection under demanding storage and sterilization conditions. Amcor opened an advanced healthcare packaging coating facility in Subang Jaya, Malaysia, in April 2026, investing more than USD 35 million and deploying air-knife coating technology for sterile medical device packaging. The bags and containers market is also being affected by traceability requirements, as smaller healthcare formats must now carry more coding and identification without compromising readability or package performance. This is raising demand for better print surfaces, more precise converting, and stricter validation across healthcare packaging programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resin, Pulp, and Metal Cost Volatility Pressuring Margins | -1.7% | Global, North America, Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Tightening Packaging Waste and Single-Use Plastic Rules Raising Compliance Costs | -1.3% | Europe core, North America state level | Medium term (2-4 years) |

| PFAS and Substance Restrictions Disrupting Barrier Material Choices | -0.8% | North America, Europe | Short term (≤ 2 years) |

| Food-Grade PCR Shortages Limiting Recycled-Content Claims and Scale-Up | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Resin, Pulp, and Metal Cost Volatility Pressuring Margins

Raw material volatility remains the most direct earnings restraint on the bags and containers market in 2026. Flexible packaging converters continue to face swings in resin costs, while paper-based formats depend on separate pulp and recovered fiber dynamics. On the rigid side, metal packaging producers are still grappling with higher aluminum and steel costs that can distort revenue trends even when physical volumes remain stable. Amcor lowered its FY26 free cash flow guidance to USD 1.5-1.6 billion, partly because it held higher-cost inventory to protect supply continuity, underscoring how input risk is affecting working capital decisions. Silgan said its Q1 2026 Metal Containers net sales rose by USD 96.5 million year over year, driven mainly by contractual pass-through of higher raw material costs. The bags and containers market can usually pass through part of these costs, but the timing gap still puts pressure on margins and customer contracts.

Tightening Packaging Waste and Single-Use Plastic Rules Raising Compliance Costs

Regulatory pressure is adding cost and complexity to the bags and containers market, especially in Europe and in parts of North America. The EU Packaging and Packaging Waste Regulation is pushing converters to revisit recyclability design, material choices, documentation, and chemical compliance before key provisions take effect from August 12, 2026. These changes weigh more heavily on smaller converters because they have less room to absorb testing costs, reformulation work, and customer-specific documentation requests. The effect is not limited to Europe, because companies serving multiple regions must manage different recycled-content timelines and chemical rules simultaneously. Amcor’s 2026 fiber packaging collaboration with Metsä Group and G. Mondini reflects how suppliers are already moving toward alternative structures that can reduce plastic content and support compliance-oriented format redesign. The bags and containers market, therefore, faces a regulatory cost burden even when demand remains healthy, because compliance work now shapes product development, procurement, and customer qualification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bag Type: E-Commerce Lifts Mailing Bags While Flat Bags Keep Their Scale

Flat bags held 28.46% of the bag-type segment in 2025, giving them the largest share in this part of the bags and containers market. Their role stayed strong in retail pre-packing, food service, and institutional use, where low cost and simple machine handling mattered more than advanced protection. Wicketed bags kept a stable place in bakery, produce, and poultry lines because pre-opened stacks support high-speed automated filling. Multiwall bags and woven sacks also remained important for industrial and agricultural loads, where puncture resistance, moisture protection, and payload economics guide purchasing decisions.

Mailing bags are projected to grow at a 6.84% CAGR through 2031, making them the fastest-growing sub-segment in the bags and containers market within bag formats. Growth is tied to parcel expansion and to the replacement of corrugated boxes in some direct-to-consumer applications where weight and shipping efficiency matter. Mondi’s Pittsburgh plant, opened in April 2026, was built around this demand pattern and adds highly automated paper bag capacity with advanced printing capabilities. The bag side of the bags and containers industry is also facing more reformulation work because coated mailing bag formats used near food channels must adapt to stricter material rules and to the growing need for readable variable data and scannable codes.

By Container Type: IBCs Grow Fast While Consumer Rigid Containers Hold the Core

Consumer rigid containers held 52.67% of the container-type segment in 2025, making them the largest product group in this section of the bags and containers market. Their position is anchored in food, personal care, and over-the-counter pharmaceutical applications where shelf presence, user interaction, tamper evidence, and compliance remain central. Amcor reported that 96% of its rigid packaging portfolio was designed for recyclability by the end of FY25, underscoring the extent to which major suppliers have invested in recycling-compatible rigid formats. Bulk drums and pails also maintained stable demand in industrial and food-ingredient distribution, where specification changes occur slowly and handling requirements remain strict.

IBCs are projected to expand at a 7.35% CAGR through 2031, the fastest pace among container sub-segments in the bags and containers market size. Their appeal comes from lower handling costs, easier palletized movement, and stronger reuse economics than many legacy bulk formats. Silgan’s Q1 2026 results showed that mix shifts can create divergence within rigid packaging categories, with strong pet food demand partly offset by lower fruit and vegetable volumes following pre-buy activity in late 2025.[2]Silgan Holdings Inc., “Silgan Announces First Quarter 2026 Results,” Business Wire, businesswire.com This part of the bags and containers industry is also benefiting from service models, as large operators can recondition and recirculate IBCs in ways that smaller regional suppliers struggle to match.

By End-User Industry: Healthcare Leads Growth While Food and Beverage Provides the Base

Food and beverage accounted for 35.28% of the total market in 2025, giving it the largest share of the bags and containers market by end-user industry. That position reflects steady demand for flexible bags in dry goods and food service, as well as for rigid containers for liquids, sauces, and personal consumption formats. Industrial demand also remained resilient, as chemicals, agrochemicals, and construction materials require a recurring supply of woven sacks, multiwall bags, IBCs, and drums. Personal care and consumer goods added another layer of growth as brands sought refillable or more transit-ready formats without sacrificing shelf quality.

Healthcare is projected to record the fastest CAGR at 7.53% through 2031, making it the strongest growth engine in the bags and containers market across end users. The growth profile is tied to biologics, specialty drugs, and sterile barrier upgrades that require tighter control of moisture, oxygen, and contamination. A 2025 scientific review in AAPS PharmSciTech described how advanced pharmaceutical packaging is moving toward more specialized barrier materials and coating systems for higher protection needs. Amcor’s Malaysia healthcare coating facility, opened in April 2026, provides a clear industrial example of this trend, adding regional capacity for sterile medical device packaging as Southeast Asian pharmaceutical manufacturing expands.

Geography Analysis

North America accounted for 39.14% of global revenue in 2025, making it the largest regional share in the bags and containers market. Its lead rests on mature e-commerce infrastructure, high use of rigid containers in food and consumer goods, and a compliance environment shaped by FDA oversight and state-level packaging rules. The region also benefits from deep converter networks and a broad installed base of automated filling, sealing, and labeling systems. In flexible packaging, North America remains a major arena for consolidation and footprint expansion. ProAmpac completed its acquisition of TC Transcontinental Packaging in March 2026 for approximately USD 1.51 billion, which materially extended its North American flexible packaging reach.

Asia-Pacific is projected to expand at a 7.16% CAGR through 2031, which makes it the fastest-growing regional cluster in the bags and containers market size. Urbanization, rising disposable income, e-commerce penetration, and industrial expansion are all adding volume across both consumer and bulk formats. Mondi announced a joint venture with PT Indocement Tunggal Prakarsa in Indonesia in 2026, expected to add more than 200 million paper bags to its global production footprint, underscoring Southeast Asia's growing importance in converter capacity planning.[3]Mondi plc, “Mondi Expands Paper Bags Business in Southeast Asia Through New Joint Venture,” Mondi, mondigroup.com Amcor’s April 2026 healthcare packaging investment in Malaysia also points to rising regional demand for higher-specification medical and pharmaceutical packaging substrates.

Europe faces slower underlying volume conditions because packaging reduction rules and compliance costs are weighing on parts of the market, even as sustainability-led premiumization creates value opportunities. South America is seeing growing demand for flexible bags in food, retail, and agricultural export chains, with woven sacks and multiwall bags supported by grains, soy, and minerals flows. The Middle East and Africa is investing in local packaging capacity as food security goals and industrial diversification programs raise demand for multiwall bags, IBCs, and bulk drums. Across all three regions, the bags and containers market is becoming more specification-driven, which favors suppliers that can pair regulatory readiness with format flexibility.

Competitive Landscape

The bags and containers market remains moderately to highly fragmented below the top tier, even though a small group of global integrated converters holds meaningful scale. Large players are using M&A to widen product reach, improve procurement leverage, and strengthen regional manufacturing networks. ProAmpac’s March 2026 acquisition of TC Transcontinental Packaging for approximately USD 1.51 billion added a business that generated approximately USD 1.2 billion in revenue in the 12 months ended July 27, 2025, making it one of the clearest recent consolidation moves in the flexible packaging space.[4]ProAmpac Intermediate Inc., “ProAmpac Completes Acquisition of TC Transcontinental Packaging,” Business Wire, businesswire.com Sealed Air also changed hands in 2026 after receiving all regulatory approvals in March and closing its acquisition by funds affiliated with CD&R in April, following net sales of USD 5.4 billion in 2025 across food, e-commerce, logistics, medical and life science, and industrial packaging. These moves show that scale still matters in the bags and containers market, especially when customers want broad format coverage and dependable sourcing across regions.

At the same time, competition is no longer based only on capacity or footprint. Amcor launched its Lift-Off Rigids challenge in May 2026 to screen startup solutions for rigid packaging and adjacent hybrid systems, demonstrating how major companies are using open innovation to pull new ideas into established commercial platforms. Mondi’s Pittsburgh paper bags plant and its Indonesia joint venture show a parallel strategy built around automation, regional proximity, and targeted end-market growth. In practice, the bags and containers market is rewarding companies that can combine material science, application engineering, and responsive manufacturing in the same offer.

Another active front is returnable transport packaging, where hardware is increasingly tied to service and data management. IFCO’s 2025 ESG reporting showed that reusable packaging systems are delivering measurable environmental benefits in fresh grocery flows, which helps explain why pooled and circular models are moving beyond pilot scale. This direction raises the bar for smaller competitors because successful reuse systems need asset tracking, cleaning standards, reverse logistics, and customer coordination. As a result, the bags and containers market is seeing a wider separation between large operators with service depth and smaller converters focused on narrower product niches.

Bags And Containers Industry Leaders

Amcor plc

Mondi plc

Sealed Air Corporation

Huhtamäki Oyj

Smurfit Westrock plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Amcor opened an advanced healthcare packaging coating facility in Subang Jaya, Selangor, Malaysia, representing an investment of over USD 35 million. The facility introduces air-knife coating technology for sterile medical device packaging and was facilitated by the Malaysian Investment Development Authority, strengthening regional supply chain resilience for Southeast Asian pharmaceutical manufacturers.

- April 2026: Mondi opened its new paper bags manufacturing plant in Pittsburgh, Pennsylvania, consolidating production from 2 legacy US sites. The plant integrates highly automated production lines and advanced printing capabilities, targeting an annual capacity of 300 million paper bags after ramp-up, with approximately 170 employees expected by end-2026.

- March 2026: ProAmpac completed the acquisition of TC Transcontinental Packaging from TC Transcontinental for approximately USD 1.51 billion, with TC Transcontinental Packaging generating approximately USD 1.2 billion in revenue during the 12 months ended July 27, 2025.

- March 2026: Sealed Air received all regulatory approvals required to complete its acquisition by funds affiliated with CD&R (Clayton, Dubilier and Rice), with the transaction closing in April 2026. Sealed Air generated USD 5.4 billion in net sales in 2025, operating across food, e-commerce, logistics, medical and life science, and industrial packaging segments.

Global Bags And Containers Market Report Scope

The scope of the report covers the analysis of the global bags and containers market, including production, distribution, and consumption of various types of bags and containers. Bags are flexible packaging solutions made from materials such as plastic, paper, or fabric, while containers are rigid or semi-rigid packaging used for storage and transportation. The study examines market trends, growth drivers, challenges, and opportunities, providing insights into the competitive landscape and key market players.

The Bags and Containers Market is Segmented by Bag Type (Flat Bags, Wicketed Bags, Mailing Bags, Multiwall Bags, and Woven Sacks), Container Type (Consumer Rigid Containers, Bulk Drums and Pails, and Intermediate Bulk Containers), End-User Industry (Food and Beverage, Healthcare, Personal Care and Cosmetics, Industrial, Consumer Goods and Retail, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Flat Bags |

| Wicketed Bags |

| Mailing Bags |

| Multiwall Bags |

| Woven Sacks |

| Consumer Rigid Containers |

| Bulk Drums and Pails |

| Intermediate Bulk Containers |

| Food and Beverage |

| Healthcare |

| Personal Care and Cosmetics |

| Industrial |

| Consumer Goods and Retail |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Bag Type | Flat Bags | ||

| Wicketed Bags | |||

| Mailing Bags | |||

| Multiwall Bags | |||

| Woven Sacks | |||

| By Container Type | Consumer Rigid Containers | ||

| Bulk Drums and Pails | |||

| Intermediate Bulk Containers | |||

| By End-User Industry | Food and Beverage | ||

| Healthcare | |||

| Personal Care and Cosmetics | |||

| Industrial | |||

| Consumer Goods and Retail | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the bags and containers market?

The bags and containers market was valued at USD 51.45 billion in 2025, stands at USD 54.68 billion in 2026, and is forecast to reach USD 74.32 billion by 2031 at a CAGR of 6.33%.

Which product area holds the largest share in this space?

On the bag side, flat bags held 28.46% of the segment in 2025. On the container side, consumer rigid containers led with 52.67% in 2025.

Which end-user group is expanding the fastest?

Healthcare is the fastest-growing end-user segment, with a projected CAGR of 7.53% through 2031, driven by biologics, specialty drugs, and sterile barrier upgrades.

Which region leads global demand, and which one grows the fastest?

North America held 39.14% of global revenue in 2025, while Asia-Pacific is projected to grow the fastest at a 7.16% CAGR through 2031.

Why are mailing bags and IBCs gaining traction?

Mailing bags are growing with e-commerce parcel volumes and lighter direct-to-consumer shipping needs. IBCs are benefiting from lower handling costs, reuse advantages, and growing bulk chemical and food ingredient logistics.

What are the main risks affecting supplier margins and strategy?

Raw material cost swings, tighter packaging waste rules, and stricter material compliance requirements are raising costs and pushing companies toward reformulation, automation, and scale-driven consolidation.

Page last updated on: