Market Overview

| Study Period | 2020 - 2031 |

|---|---|

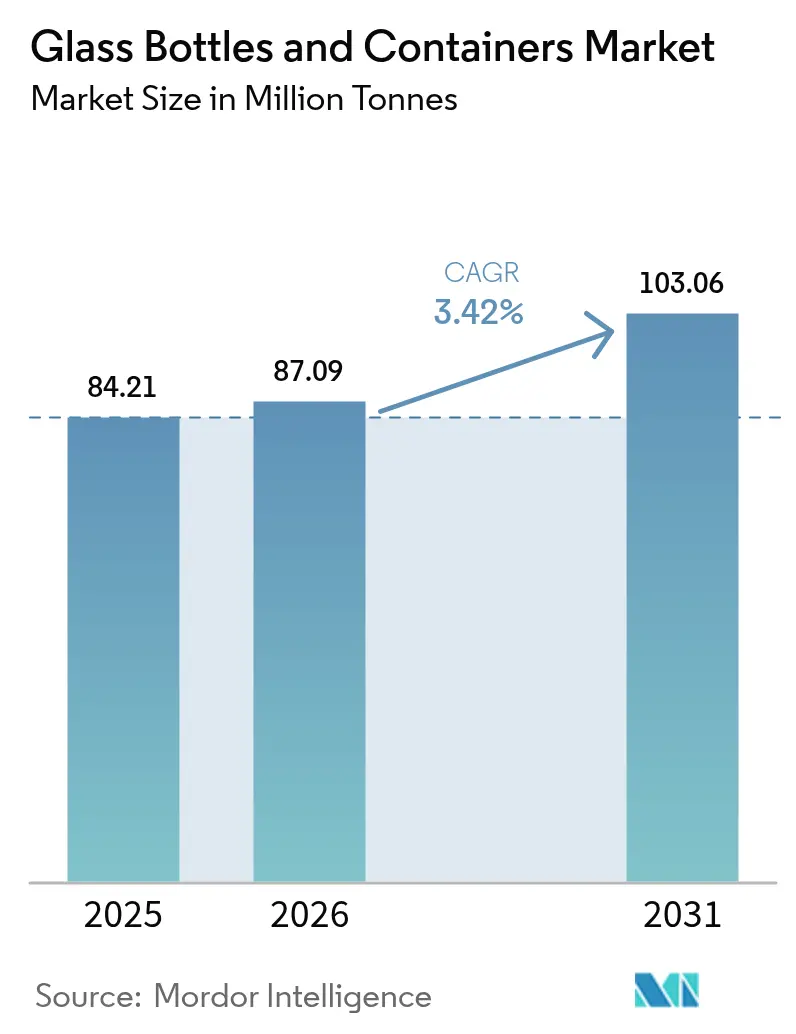

| Market Volume (2026) | 87.09 Million tonnes |

| Market Volume (2031) | 103.06 Million tonnes |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

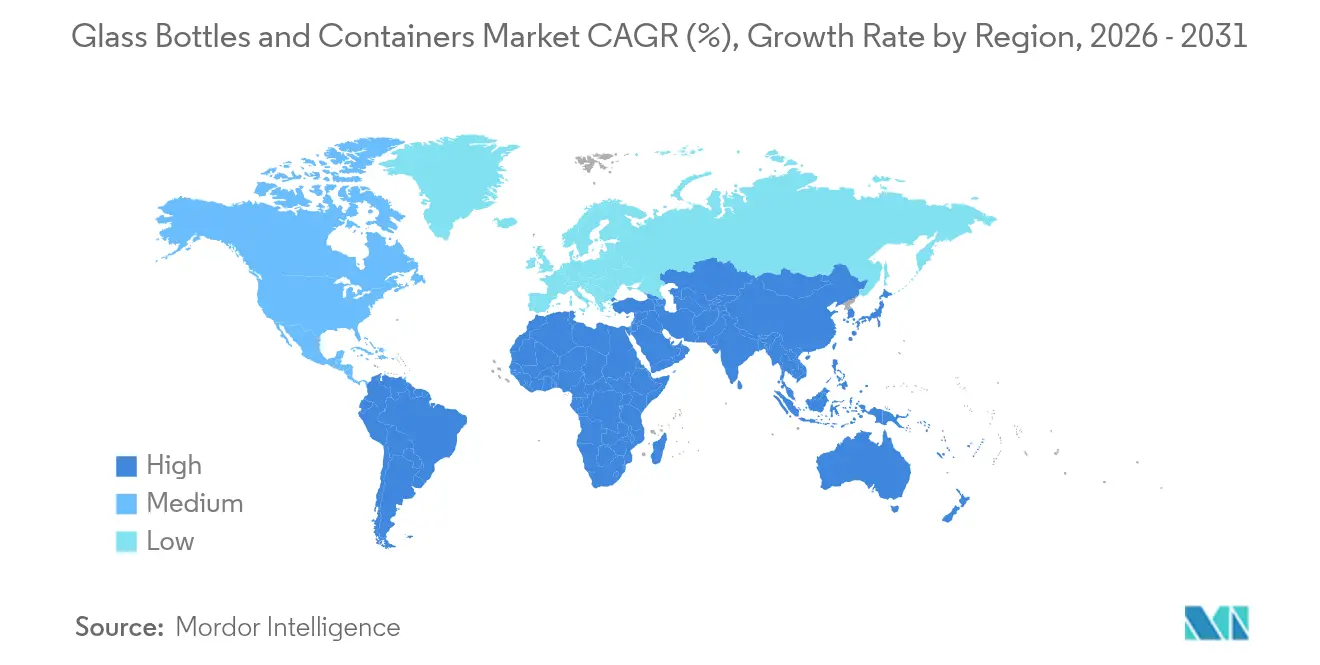

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glass Bottles And Containers Market Analysis by Mordor Intelligence

The Glass Bottles and Containers market size is expected to grow from 84.21 million tonnes in 2025 to 87.09 million tonnes in 2026 and is forecast to reach 103.06 million tonnes by 2031 at 3.42% CAGR over 2026-2031. Heightened regulatory pressure on single-use plastics, premiumization in beauty and spirits, and pharmaceutical fill-finish expansion are steering steady gains despite energy-price headwinds. California’s 65% plastic-reduction mandate and France’s polystyrene ban have already swung demand toward infinitely recyclable glass.[1]California Legislative Information, “Senate Bill No. 54,” leginfo.legislature.ca.govHybrid furnaces, oxy-fuel combustion, and high-cullet recipes are mitigating cost exposure, while lightweighting breakthroughs such as Vidrala’s 260-gram 75 cl bottle trim material intensity without sacrificing shelf appeal. Producers also leverage color differentiation, especially amber, to protect light-sensitive drugs and craft beverages, reinforcing value over lighter substitutes.

Key Report Takeaways

- By end-user, beverages captured 64.02% of the glass bottles and containers market share in 2025.

- By color, the glass bottles and containers for amber glass are projected to grow at a 3.79% CAGR between 2026-2031.

- By geography, North America captured 55.18% of the glass bottles and containers market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glass Bottles And Containers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic bans drive shift to recyclable glass packaging | +0.8% | California, France, EU | Medium term (2–4 years) |

| Prestige beauty “glassification” trend lifts jar and bottle volumes | +0.6% | North America and Europe | Long term (≥ 4 years) |

| Pharma fill-finish expansion boosts demand for glass vials | +0.5% | APAC, global | Long term (≥ 4 years) |

| Craft alcohol boom spurs custom container demand | +0.4% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Plastic Bans Drive Shift to Recyclable Glass Packaging

California’s SB 54 mandates a 65% cut in single-use plastic packaging by 2032, while France has barred expanded polystyrene food containers from January 2025, propelling brand owners to switch to glass. The European Union’s pending bisphenol-A restrictions further reinforce conversion in food contact segments. Because glass maintains an endless closed loop and established curb-side collection, converters are capturing new volumes even as they absorb retooling costs. The ripple effect is evident in beverage and condiment lines moving back to glass at big-box retailers. Though cullet supply tightens temporarily, hybrid furnaces and lightweighting partially offset margin compression, paving a sustained uplift through the forecast horizon.

Prestige Beauty “Glassification” Trend Lifts Jar and Bottle Volumes

Luxury skincare and fragrance brands increasingly adopt glass to signal premium quality and environmental stewardship. Verallia’s 100% post-consumer-recycled (PCR) Vista bottles cut energy use by 40% versus virgin production, proving that circularity can coexist with high-end aesthetics.[2]Packaging Europe, “Verallia unveils bottle made from 100% PCR glass,” packagingeurope.comEmbossing, color gradations, and refillable designs amplify shelf differentiation and justify higher price points. Since packaging cost is a small share of retail value in beauty, brands absorb higher unit costs more easily than mass-market beverages. The trend scales globally but is most pronounced in North America and Western Europe, reinforcing long-tail demand for custom molds and short production runs.

Pharma Fill-Finish Expansion Boosts Demand for Glass Vials

Surging biologics pipelines and injectable therapies such as GLP-1 drugs require chemically inert vials that prevent interaction and delamination. Gerresheimer derived EUR 898.6 million (USD 1.02 billion) in primary packaging glass revenue in 2024 and doubled down with its Bormioli Pharma acquisition, illustrating strategic consolidation around pharma glass. Asia Pacific’s contract-manufacturing boom compounds volume needs, while the FDA and EMA continue to specify Type I borosilicate for sensitive formulations. High-margin, specification-driven vials insulate producers from commodity pricing cycles and anchor capacity investments for the long term.

Craft Alcohol Boom Spurs Custom Glass Container Demand

Craft distilleries produced 13.5 million cases in 2024, pursuing ornate bottle shapes that elevate brand storytelling. Similar momentum in the United Kingdom, where the number of licensed distilleries widened 42.8% from pre-COVID levels, underscores a flourishing niche for bespoke glass. Small-batch spirits command price premiums that absorb container cost inflation, incentivizing manufacturers to offer low-minimum-order, high-decoration services. The trend also spills into ready-to-drink cocktails and low-alcohol variants, broadening addressable demand for custom designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy price volatility threatens furnace economics | -0.9% | Europe, global | Short term (≤ 2 years) |

| rPET bottle adoption undercuts glass in logistics-sensitive channels | -0.7% | Global beverage logistics | Medium term (2–4 years) |

| Weak Cullet Collection Infrastructure Limits Recycled Content | -0.4% | Developing markets, rural areas globally | Long term (≥ 4 years) |

| Breakage Losses in Long-Haul Shipping Discourage Glass Use | -0.3% | Global trade routes, emerging markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Energy Price Volatility Threatens Furnace Economics

Electricity prices in the United Kingdom spiked to record levels in 2024, compelling glassmakers to idle lines during peak tariffs. Energy constitutes roughly 18% of production costs, so volatility can erase margins faster than price adjustments reach the market. Carbon-pricing schemes further penalize fossil-fuel consumption, intensifying capital commitments toward hybrid furnaces and on-site renewables. In contrast, O-I Glass secured USD 125 million in federal funding for decarbonization, but smaller regional plants face liquidity strains, potentially curbing short-term supply.

rPET Bottle Adoption Undercuts Glass in Logistics-Sensitive Channels

Lightweight rPET bottles weigh nearly 90% less than comparable glass, yielding freight savings that make a decisive difference for low-margin, long-haul beverage SKUs. Breakage rates of 2-3% in glass shipments amplify the cost gap. As recycling rates climb and bottle-to-bottle loops mature, sustainability objections erode, especially for private-label soft drinks where aesthetics carry less weight. Glass retains an edge in premium tiers, but the value segment’s tilt toward rPET will restrain container glass packaging market growth in high-volume channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Anchor Market Despite Cosmetics Surge

Beverages commanded 64.63% of the container glass packaging market in 2024, but growth has begun to plateau as major breweries trial lightweight rPET for economy lines. In contrast, cosmetics and personal care, though on a smaller base, are set to post the fastest 4.24% CAGR as brands use glass to signal luxury and sustainability. The container glass packaging market size for cosmetics jars is projected to widen materially by 2030 as refill stations and PCR glass creations gain ground. Food, condiments, and preserves maintain a stable share thanks to shelf-life advantages, while pharmaceutical demand continues to expand on the back of biologics.

The cosmetics advance springs from consumer willingness to pay a premium for beautiful, tactile jars and bottles. Custom shapes, pastel tints, and heavy bases espouse the sensorial narrative that glass uniquely delivers. Moreover, zero-plastic brand pledges, amplified by social-media influencers, accelerate brand conversions in key Western markets. Although drinks still dominate absolute tonnage, value growth is migrating toward higher-margin beauty and health categories, diversifying revenue streams for producers.

By Color: Amber Gains Ground Through Pharma and Craft Applications

Flint maintained a 58.28% share of the container glass packaging market size in 2024, owing to its broad utility across beverages and foods. Nonetheless, amber glass-favored for its ultraviolet-blocking feature-will outpace at a 3.83% CAGR through 2030 as pharma vials and craft drinks proliferate. The container glass packaging market share for amber beer bottles in Europe is already climbing in tandem with independent breweries that prize product stability and rustic aesthetics.

Growth in amber owes much to pharmaceutical regulatory guidance that specifies light protection for biologics, boosting procurement contracts for Type I amber borosilicate. Craft distillers also gravitate toward darker hues to convey heritage themes. Green and specialty colors persist as niche domains, notably in wine and limited-edition spirits, where marketing narratives trump functional considerations.

Geography Analysis

North America captured 55.18% of the container glass packaging market in 2025, leveraging mature curbside collection and corporate sustainability goals that encourage high-cullet recipes. The Glass Packaging Institute’s roadmap to reach a 50% recycling rate by 2030 underpins the long-term feedstock base. Yet energy-price swings and growing rPET penetration in value beverages temper volume gains, shifting strategic emphasis toward premium spirits and beauty care.

Europe trails but benefits from the EU’s 80.8% recycling rate, which secures cullet and lowers furnace energy demand. Ardagh and Verallia are investing in electric-boost and hydrogen-ready furnaces to hedge carbon-pricing exposure while maintaining output. However, power-price stress and environmental levies suppress near-term margins, sparking collaboration on shared renewable micro-grids and cross-border cullet trade.

Asia Pacific is the fastest-growing region, expanding 4.76% CAGR through 2031 and rapidly closing the gap in the container glass packaging market. India and China build greenfield pharmaceutical plants that require sterile vials, while South Korea and Japan import premium cosmetic glass for luxury skincare. O-I Glass’s USD 120 million upgrade in Zipaquirá, Colombia, signals how producers replicate best-in-class technology in emerging regions to capture demand while aligning with ESG mandates. Limited cullet infrastructure in parts of Southeast Asia constrains recycled content, creating cost penalties versus Western peers; nevertheless, rising incomes and regulatory push for circularity promise robust long-term demand.

Competitive Landscape

The container glass packaging market remains moderately consolidated. O-I Glass, Verallia, and Ardagh collectively shipped just over 55% of global volumes in 2024, wielding scale advantages in procurement, furnace technology, and distribution. O-I Glass’s MAGMA modular furnace, now topping off in Kentucky, exemplifies capital-light expansion that trims changeover downtime and improves glass quality. Verallia focuses on PCR breakthroughs, while Ardagh pilots hydrogen-assisted melting.

Medium-sized regional specialists vie on custom molds, agile batch sizes, and service proximity, addressing craft beverage and beauty segments that the majors sometimes overlook. Vidrala’s record-light 260-gram bottle showcases value creation through engineering-diminishing glass-to-product weight ratio, lowering logistics emissions, and courting environmentally conscious brands.

M&A stays active: Gerresheimer’s December 2024 acquisition of Bormioli Pharma bolsters its molded-glass unit and strengthens a pharma-heavy portfolio. Joint ventures emerge in Latin America and Africa, where greenfield capital needs are high, but political risk is equally elevated. Despite moderate concentration, high furnace costs form a barrier to entry that keeps new competitors at bay unless they secure government or customer co-funding.

Glass Bottles And Containers Industry Leaders

O-I Glass, Inc.

Ardagh Group S.A.

Gerresheimer AG

Vidrala S.A.

Verallia S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Verallia launched Vista bottles made entirely from post-consumer cullet, claiming 40% energy savings versus virgin production, and targeting premium beauty and spirits applications.

- August 2025: Vidrala introduced the 260G bottle, the world’s lightest 75 cl glass bottle at 260 g, spotlighting material-efficiency gains.

- June 2025: Gerresheimer reported EUR 898.6 million (USD 1.02 billion) in 2024 primary packaging glass revenue and guided 8-10% organic CAGR, underpinned by pharma demand.

- June 2025: O-I Glass secured USD 125 million from the U.S. Department of Energy for hybrid-furnace decarbonization.

Global Glass Bottles And Containers Market Report Scope

Glass containers market tracks the demand of glass packaging containers and bottles across the end-users industries including beverage, food, pharmaceutical, cosmetics and others. Glass containers are majorly used in the alcoholic and non-alcoholic beverage industry due to their ability to maintain chemical inertness and sterility and non-permeability.

The container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors) and by geography (North America [United States and Canada], Europe [France, Germany, Italy, United Kingdom, Spain, Poland, Russia, Denmark, Sweden, Belgium, Czech Republic, Netherlands, Ukraine, Austria, Hungary and Rest of Europe], Asia-Pacific [China, India, Japan, Thailand, New Zealand and Australia, South Korea, Indonesia, Vietnam, and Rest of Asia -Pacific], Middle East and Africa [United Arab Emirates, Saudi Arabia, Egypt, Kuwait, South Africa, Nigeria, Morocco, and Rest of Middle East and Africa] and Latin America [Brazil, Mexico, Colombia, Chile, Argentina, Uruguay, Ecuador and Rest of Latin America]). The market sizes and forecasts are provided in terms of consumption volume (tonnes) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the container glass packaging market?

The sector reached 87.09 million tonnes in 2026 and is forecast to hit 103.06 million tonnes by 2031.

How fast is Asia Pacific demand for container glass rising?

Volume in Asia Pacific is expected to grow at a 4.76% CAGR between 2026-2031 on the back of pharma and beauty applications.

Which end-user segment shows the strongest growth?

Cosmetics and personal care leads with an anticipated 4.18% CAGR through 2031 thanks to luxury-branding and sustainability trends.

How are energy costs influencing glass manufacturing?

Volatile electricity and gas prices, especially in Europe, squeeze margins and hasten adoption of hybrid and oxy-fuel furnaces.

What innovation is helping reduce glass weight?

Vidrala’s 260-gram 75 cl bottle exemplifies lightweighting that cuts materials and freight emissions.

Who are the top players in the market?

O-I Glass, Verallia, and Ardagh together account for just over 55% of global shipments, reflecting moderate consolidation.

Page last updated on: