Baby Food Glass Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

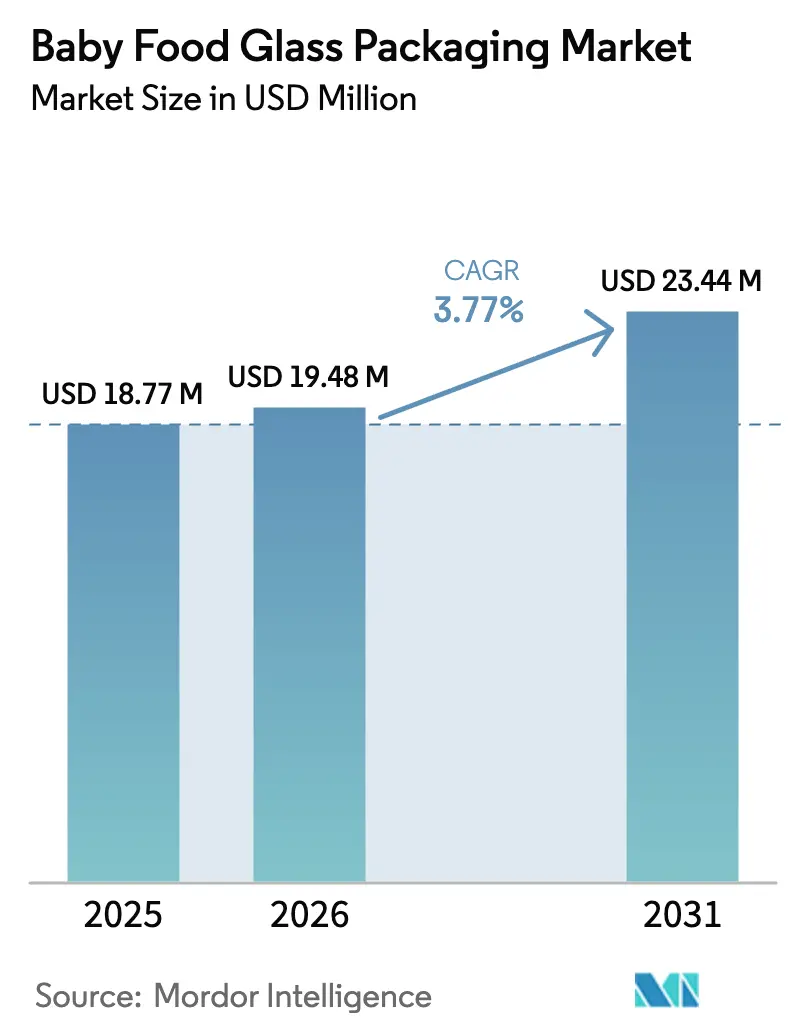

| Market Size (2026) | USD 19.48 Million |

| Market Size (2031) | USD 23.44 Million |

| Growth Rate (2026 - 2031) | 3.77% CAGR |

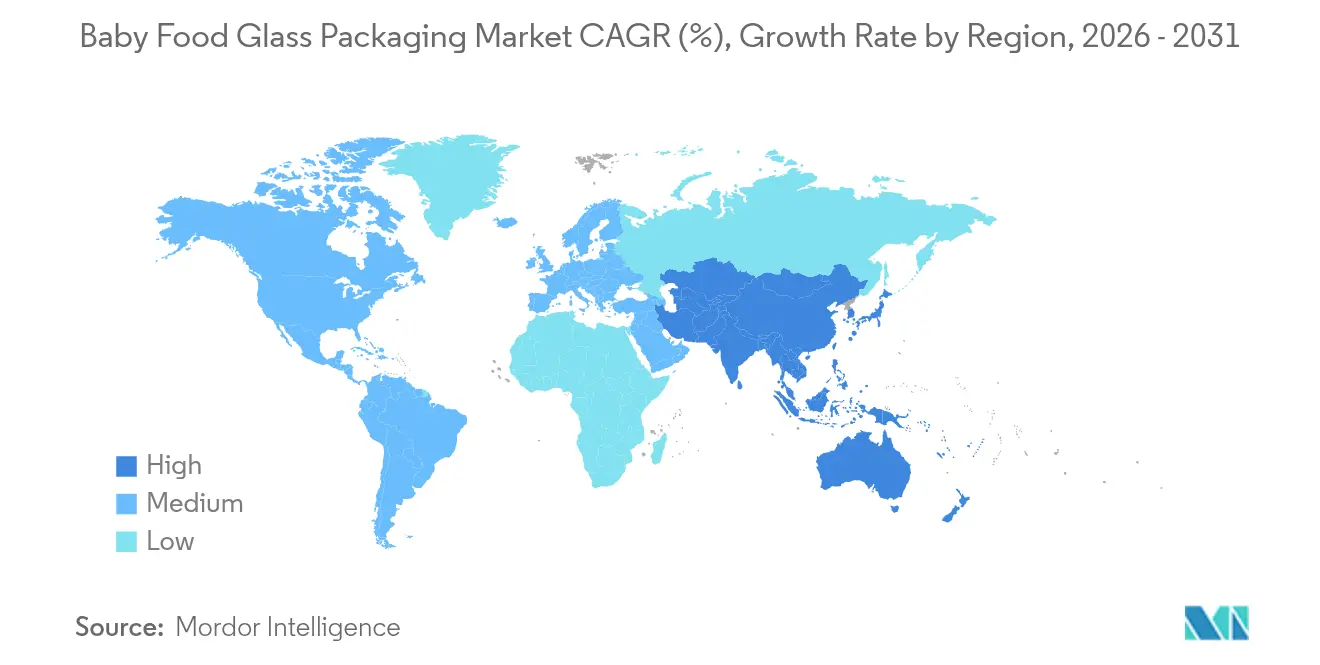

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Baby Food Glass Packaging Market Analysis by Mordor Intelligence

The baby food glass packaging market size was valued at USD 18.77 billion in 2025 and estimated to grow from USD 19.48 billion in 2026 to reach USD 23.44 billion by 2031, at a CAGR of 3.77% during the forecast period (2026-2031). Robust demand is propelled by parents’ growing preference for premium, chemical-free containers, regulators’ tighter limits on plastics in infant nutrition, and brand owners’ search for strong visual shelf appeal. Europe’s total ban on bisphenol A (BPA) in food-contact materials from January 2025 reinforces glass as the material of choice for sensitive formulations. At the same time, continuous investments in electric furnaces and recycled-content cullet have lowered the carbon footprint of glass production, aligning with circular-economy mandates. Yet rising energy prices, heavier logistics costs and capacity curtailments in North America temper short-term growth. Asia-Pacific offers the biggest upside as urban families in China and India shift from homemade meals to branded baby foods, often perceiving glass as a quality cue.

Key Report Takeaways

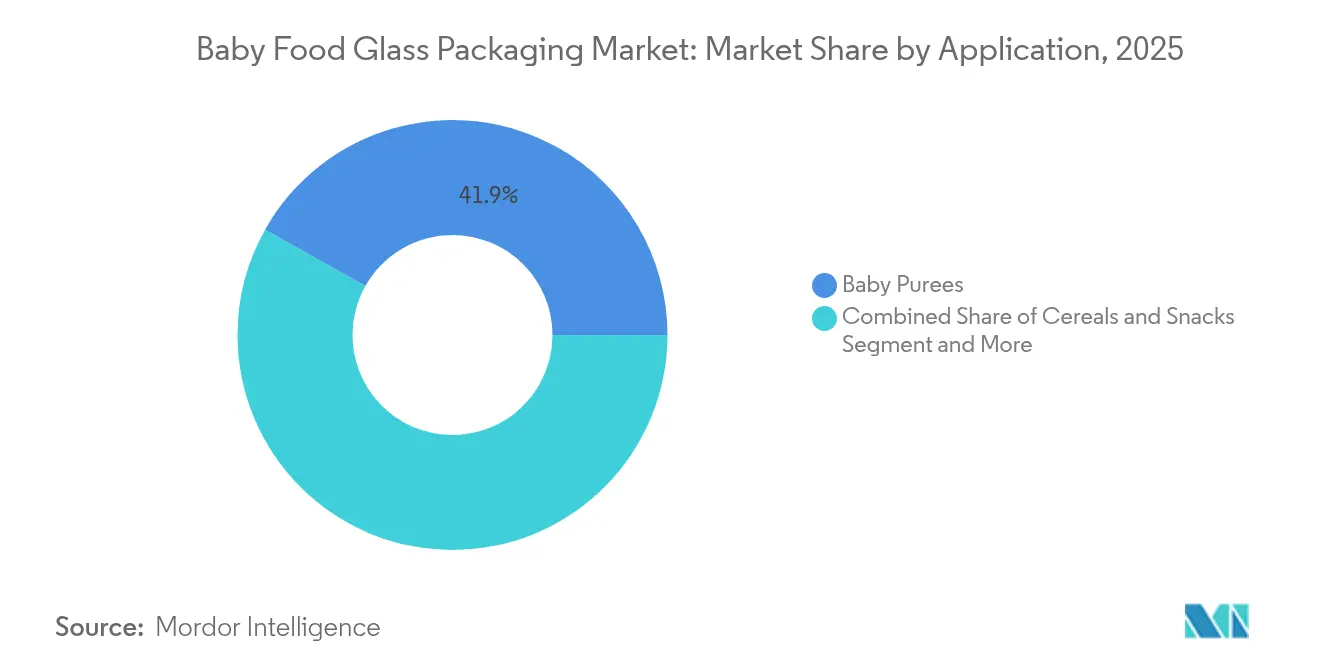

- By application, baby purees led with 41.85% of baby food glass packaging market share in 2025; drinks and juices are forecast to expand at a 5.04% CAGR to 2031.

- By container type, glass jars accounted for 58.15% share of the baby food glass packaging market size in 2025, while glass cups/portion pots are projected to grow at 4.65% CAGR through 2031.

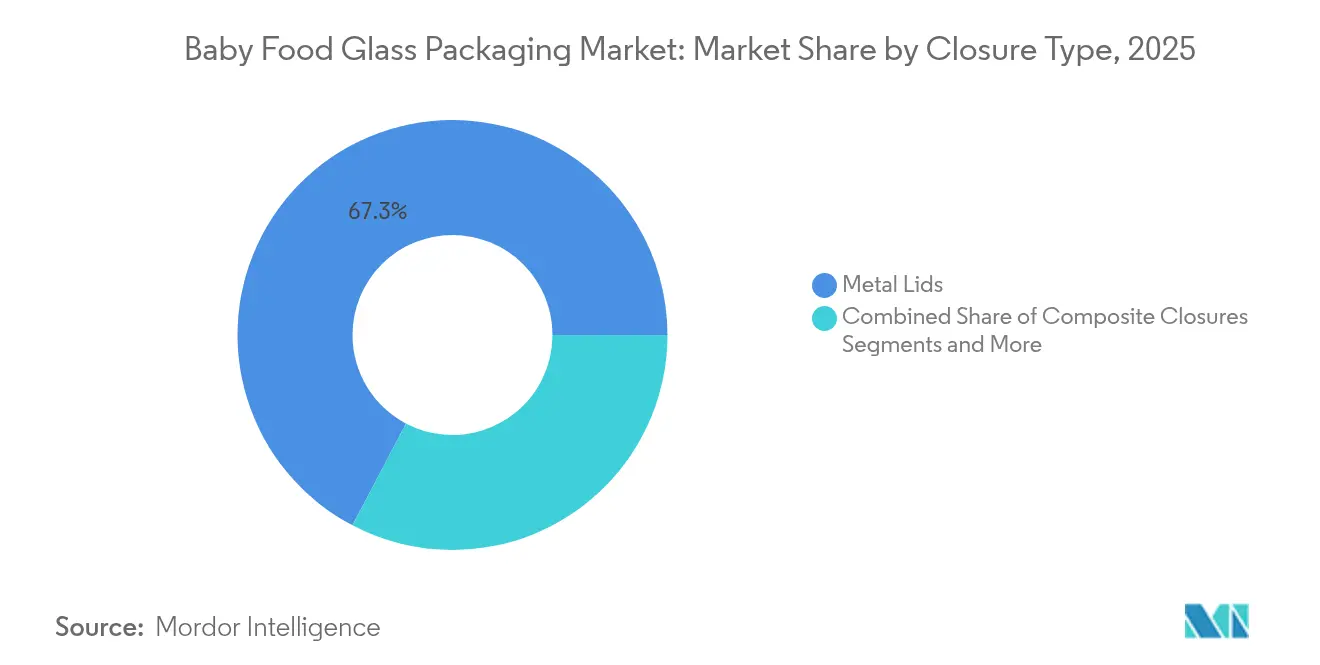

- By closure type, metal lids held 67.30% revenue share in 2025; composite closures record the fastest 5.82% CAGR during the forecast period.

- By distribution channel, offline retail commanded 83.40% of the baby food glass packaging market in 2025, whereas e-commerce and direct-to-consumer sales rise at 5.39% CAGR to 2031.

- By geography, Asia-Pacific captured 32.05% market share in 2025 and posts the highest 4.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Baby Food Glass Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for organic and natural baby foods | +1.2% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Parental preference for glass over plastics for health-safety perception | +0.8% | Developed markets worldwide | Long term (≥ 4 years) |

| Premiumization and brand differentiation through glass packaging | +0.6% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Government recycling and circular-economy mandates | +0.4% | Europe, North America, select Asia-Pacific | Long term (≥ 4 years) |

| Refill-in-store and container-deposit pilots | +0.3% | Europe, pilot programs in North America | Long term (≥ 4 years) |

| DTC baby-food start-ups needing temperature-stable tempered glass | +0.2% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for organic and natural baby foods

Organic baby food lines expand quickly because parents trust products free of synthetic additives. Brands position glass as the safest barrier to preserve nutrients and aromas. Gerber has already shifted its Organic range toward carbon-neutral glass jars to strengthen premium cues. The U.S. FDA emphasizes rigorous safety review of packaging intended for infant formula, a stance that naturally favors inert glass surfaces.[1]U.S. FDA, “Food Contact Substances for Infant Formula,” fda.gov Venture-backed disruptors follow suit; Once Upon a Farm earmarked USD 52 million to scale cold-pressed blends packed in integrity-focused formats. Momentum is now spreading to China’s metropolitan parents who willingly pay more for organic certification. These combined forces lift the baby food glass packaging market as organic SKUs multiply across aisles.

Parental preference for glass over plastics for health-safety perception

Consumer surveys show up to 70% of new parents trust glass jars more than any alternative for baby nutrition.[2]Glass Packaging Institute, “Consumer Research on Glass Safety,” gpi.orgConfidence jumped after the EU confirmed a complete BPA ban in early 2025. Brands and retailers underline this narrative; Mason Bottle actively markets “non-toxic glass feeding solutions” to millennial families. Health-driven sentiment lets manufacturers maintain a price premium while limiting promotions. Because such trust stems from intrinsic material properties rather than branding alone, the differential is hard for flexible pouches to erode, reinforcing a long-term demand tailwind.

Premiumization and brand differentiation through glass packaging

Glass adds perceived value through clarity, weight and sound cues. Beech-Nut’s prebiotic smoothies in transparent jars highlight natural ingredients, enabling higher shelf prices. In e-commerce, imagery of a gleaming jar communicates authenticity better than opaque pouches, improving click-through rates. Emerging clean-label brands such as Babylife Organics use embossed jar shapes and QR codes to elevate trust online. These branding benefits keep glass central in premium baby food launches despite costlier production.

Government recycling and circular-economy mandates

Legislators push all packaging to become fully recyclable by 2030 in the EU, a milestone glass already meets because it can be endlessly remelted without loss of quality. Similar rules in Canada, California and South Korea levy fees on material with low recycling rates, indirectly favoring glass. Producers respond by acquiring recyclers; Ardagh bought Svensk Glasåtervinning to guarantee furnace cullet supply. Mandates raise compliance costs for plastics while amplifying glass’s environmental credentials.

Restraint Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher cost and weight of glass versus plastics | -0.9% | Global, greatest in price-sensitive regions | Short term (≤ 2 years) |

| Glass supply-chain disruptions and furnace downtime risk | -0.6% | Areas with aging infrastructure | Medium term (2-4 years) |

| Rapid uptake of retortable pouches in emerging economies | -0.4% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Lightweight-packaging rules favoring plastic-glass laminates | -0.3% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher cost and weight of glass versus plastics

Melting sand, soda ash and limestone requires extreme temperatures, so glass plants face higher energy bills than polymer extruders. Glass containers weigh 4-6 times more than equivalent laminate pouches, inflating freight spend and carbon emissions per shipped calorie.[3]Drug Plastics & Glass, “Energy Inputs in Glass vs. Plastic,” drugplastics.com Price sensitivity in Southeast Asia pushes local brands toward spouted pouches that already command more than 30% of baby food packaging volume. Energy inflation lifted the U.S. glass industry Producer Price Index by 4.5% in 2024, squeezing converters’ margins. Unless fuel surcharges retreat, this disadvantage limits penetration outside premium SKUs.

Glass supply-chain disruptions and furnace downtime risk

A blast furnace must stay hot for 10-12 years between rebuilds, so unplanned outages remove large chunks of capacity very suddenly. Ardagh shuttered two additional U.S. plants in September 2024, immediately tightening North American supply. Vetropack’s Swiss shutdown in May 2024 had similar effects in Central Europe. Energy interruptions or labor shortages further endanger uptime, prompting brand owners to dual-source with plastics. The need for heavy capital (O-I reserved USD 150 million to modernize its Alloa site) stretches balance sheets and depresses rapid capacity additions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Purées dominate while beverages accelerate

In 2025, baby purées held 41.85% of the baby food glass packaging market size, reflecting their role as first weaning meals for infants. Stable demand comes from every region, and parents trust jars to guard color, aroma and micronutrients. Formulators also appreciate glass for hot-fill and retort tolerance, reducing preservatives. However, drinks and juices are rising fastest at a 5.04% CAGR to 2031. Thirst for cold-pressed fruit blends and probiotic smoothies drives this upswing, with transparent jars showcasing vibrant hues that resonate on social media. Beech-Nut’s prebiotic beverage line illustrates how glass underpins new liquid nutriment launches.

Beverage producers prize glass’s oxygen barrier to uphold fresh taste without additives, underpinning premium price tags. Meanwhile cereals and snacks keep steady momentum, supported by extended shelf life needs that glass fulfills. Specialized “others” such as therapeutic formulations fetch the highest unit prices thanks to stringent safety expectations. Across categories, portion control trends nudge brands toward smaller SKUs, subtly diversifying volume beyond the traditional 4-ounce jar. These shifts collectively reinforce the baby food glass packaging market even as broader infant nutrition formats expand.

By Container Type: Jars retain primacy despite portion innovation

Glass jars captured 58.15% of baby food glass packaging market share in 2025 as their versatility suits purées, cereals and snacks alike. Standard neck finishes integrate easily with high-speed metal-lug cappers, aiding cost control. Less dominant but faster-growing glass cups / portion pots clock a 4.65% CAGR by 2031, aligning with parents’ wish to minimize waste and simplify on-the-go feeding. Designs like WeeSprout’s graduated storage pots blend measurement precision with freezer-to-microwave resilience.

Nursing bottles remain a niche driven by premium positioning and safety narratives, especially among parents avoiding polycarbonate feeders. Developers now explore slim-wall jar geometries and internal embossing to shave weight while safeguarding strength. The momentum toward portion pots encourages glassmakers to invest in narrow-neck IS machines capable of multiple cavity configurations, keeping innovation vibrant inside this baby food glass packaging industry segment.

By Closure Type: Metal rules while composites surge

Metal lug lids owned 67.30% revenue share in 2025 thanks to proven hermeticity and cost efficiency. Rubberized compound systems endure high retort temperatures, guaranteeing shelf stability. Nevertheless composite closures show a brisk 5.82% CAGR as converters incorporate bio-based polymers, tamper-evident bands and resealable features. Top Cap’s dual-material easy-open ends exemplify the push toward functionality with lower plastic fractions.

Plastic caps satisfy certain bottle applications where flip-tops help dosing, yet sustainability scrutiny restrains broader take-up. Niche “green-and-others” groups such as cork-fiber hybrids remain experimental. Over the next five years, metallized finishes, laser scoring and tethered components are expected to lift perceived value, reinforcing the premium aura of glass-packed infant foods.

By Distribution Channel: Retail dominates despite digital lift

Brick-and-mortar outlets represented 83.40% of 2025 revenue because parents still value inspecting expiry dates and vacuum buttons before purchase. Supermarkets grant shelf visibility, and bundled promotions with diapers or formula foster impulse buys. Yet e-commerce and direct-to-consumer sales pace ahead at 5.39% CAGR, propelled by app-enabled convenience and subscription offerings. The growth invites redesign work so that jars survive parcel shocks without excess cushioning.

Brands such as Once Upon a Farm leverage online reach to launch mail-back recycling loops, bolstering circular narratives. As younger parents shift grocery budgets online, glass converters must solve weight and breakage challenges through lighter flint, reinforced corners or partitioned packs. Successful adaptation secures volumes while keeping the baby food glass packaging market relevant in digital storefronts.

Geography Analysis

Asia-Pacific held 32.05% of total value in 2025 and leads growth with a 4.44% CAGR to 2031. China’s imported baby food brands still account for 60% of local category spending despite rising domestic entrants, a sign that trust and packaging quality trump price among urban households. India mirrors this pattern as disposable incomes climb; glass jar SKUs gain presence on modern-trade shelves in Tier-I cities. Meanwhile Japan’s mature demographic sustains premium sales through innovation such as microwavable jars for rice porridge. Regional suppliers increasingly source post-consumer cullet to meet city recycling quotas, anchoring supply stability for the baby food glass packaging market.

North America and Europe post slower absolute growth yet remain essential premium bastions. The forthcoming EU rule that all packaging must be recyclable by 2030 coupled with its BPA ban cements glass as the lowest-risk option. U.S. consumer education from the Glass Packaging Institute supports brand messaging around purity and taste. Retailers emphasize plastic-free zones in baby aisles, amplifying share of wallet for glass even when pouch volumes expand in value lines.

Competitive Landscape

The baby food glass packaging market is moderately consolidated around multinationals like O-I Glass, Gerresheimer and Verallia. These firms operate large tank furnaces, leverage scale in cullet procurement and invest in decarbonization. O-I’s USD 150 million revamp of its Alloa plant includes hybrid electric melting, targeting a 20% energy cut. Verallia already launched a fully electric furnace that lowers CO₂ by 60% while keeping throughput constant. Such capex sustains entry barriers.

Flexible pouch specialists erode share on cost grounds, now topping 30% of the wider baby food packaging landscape. In response, glass majors pilot ultra-light jars and engravable QR lids to augment value. Acquisition activity targets recycling assets; Ardagh’s purchase of Svensk Glasåtervinning locks in feedstock for Nordic sites. Smaller regional players such as Beatson Clark serve craft and private-label niches, often customizing short-run embossing for boutique organic brands.

Start-ups in the direct-to-consumer space demand tempered borosilicate jars that cope with cold-pressure processing, opening pockets of premium growth for specialty glassmakers. Smart packaging, including NFC chips under metal caps to authenticate origin, appears in pilot runs with European organic producers. As regulatory scrutiny of single-use plastics tightens, incumbents with established furnace fleets and closed-loop cullet networks look well positioned to protect share within the baby food glass packaging market.

Baby Food Glass Packaging Industry Leaders

O-I Glass Inc.

Gerreshmier AG

Vetropack Holding Ltd

Glassware Depot

Ardagh Group S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Verallia reported Q1 volume recovery and confirmed its 60% CO₂-reduction electric furnace rollout.

- January 2025: Gerresheimer posted FY 2024 revenue of EUR 898.6 million (USD 988.5 million) for Primary Packaging Glass, guiding 3-5% organic growth in 2025.

- October 2024: Verallia completed a EUR 600 million (USD 660 million) bond to refinance debt while producing over 16 billion containers in 2023.

- October 2024: Once Upon a Farm upgraded packaging lines to 1.2 million units weekly with SOMIC automation.

Global Baby Food Glass Packaging Market Report Scope

Glass packaging is often preferred for baby food as it is impermeable and nonporous. Thus, there is no interaction between the glass packaging and the products to alter the taste of baby food. There is no unpleasant aftertaste as well. Glass has a near-zero rate of chemical reactions, which ensures that the products contained within a glass bottle maintain their potency, aroma, and taste.

The baby food glass packaging market is segmented by application (baby food and other applications) and geography (North America [United States and Canada], Europe [Germany, United Kingdom, France, Spain, and the Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific] Middle East & Africa, and Latin America). The study also includes the baby glass bottles market, segmented by geography: North America [United States and Canada], Europe [Germany, United Kingdom, France, Spain, and the Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific] and the Rest of world. The report offers the market size in terms of value USD for all the above segments.

| Baby Purees |

| Cereals and Snacks |

| Drinks and Juices |

| Others |

| Glass Jars |

| Glass Bottles (Nursing/Feeding) |

| Glass Cups / Portion Pots |

| Metal Lids |

| Composite Closures |

| Plastic Caps |

| Green and Others |

| Offline Retail |

| E-commerce and DTC |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia and New Zealand | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Application | Baby Purees | ||

| Cereals and Snacks | |||

| Drinks and Juices | |||

| Others | |||

| By Container Type | Glass Jars | ||

| Glass Bottles (Nursing/Feeding) | |||

| Glass Cups / Portion Pots | |||

| By Closure Type | Metal Lids | ||

| Composite Closures | |||

| Plastic Caps | |||

| Green and Others | |||

| By Distribution Channel | Offline Retail | ||

| E-commerce and DTC | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia and New Zealand | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the baby food glass packaging market?

The market stands at USD 19.48 billion in 2026 and is projected to reach USD 23.44 billion by 2031.

Which application segment holds the largest share?

Baby purées dominate with 41.85% market share, while drinks and juices grow fastest at a 5.04% CAGR.

Why is Asia-Pacific considered the growth engine for baby food glass packaging?

The region combines large birth cohorts, rising disposable incomes and growing trust in premium glass containers, resulting in a 4.44% forecast CAGR.

What is the main challenge facing glass packaging producers?

Higher production and freight costs, compounded by energy-intensive furnaces, create pricing pressure versus flexible pouches.

Page last updated on: