Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

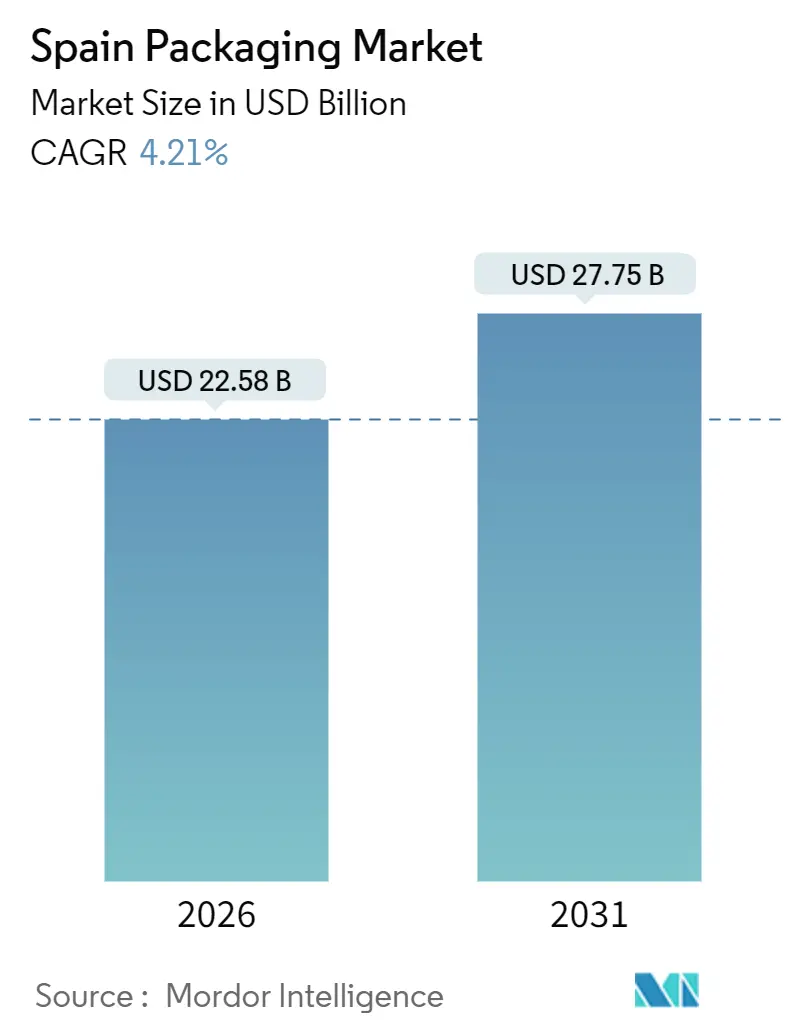

| Market Size (2026) | USD 22.58 Billion |

| Market Size (2031) | USD 27.75 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

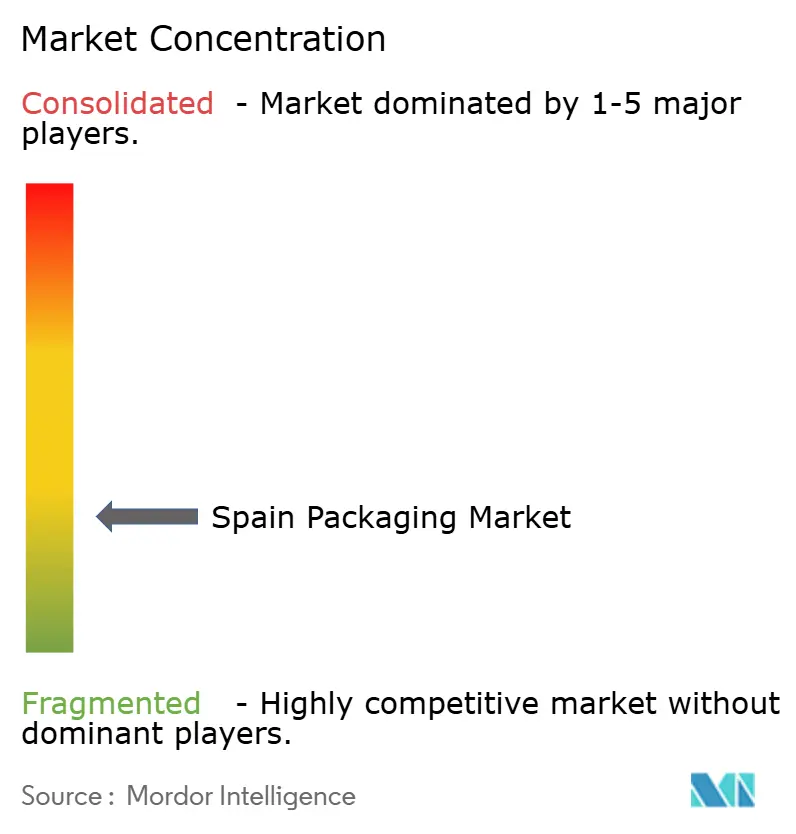

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Packaging Market Analysis by Mordor Intelligence

The Spain packaging market size reached USD 22.58 billion in 2026 and is projected to climb to USD 27.75 billion by 2031, translating into a 4.21% CAGR over the forecast period. This steady pace masks a structural pivot as converters adjust to Royal Decree 1055/2022, the EUR 0.45-per-kilogram plastic-packaging tax, and a sharp pull from food exports and e-commerce deliveries. Food shipments delivered a EUR 12.054 billion trade surplus in the first seven months of 2025, and online parcel flows hit 1.303 billion in 2024, up 8.6% year on year, reinforcing demand for corrugated boxes, flexible films, and protective formats. Brand owners now accelerate trials of recyclable paper, mono-material laminates, and lightweight bottles to blunt tax exposure and meet EU Regulation 2025/40 recyclability deadlines. Meanwhile, 93.8 million international visitors in 2024 revived single-use food-service articles, and converters are investing in automation to offset volatile pulp and resin costs. Collectively, these shifts position the Spain packaging market for measured yet higher-quality growth built on circular-economy principles.

Key Report Takeaways

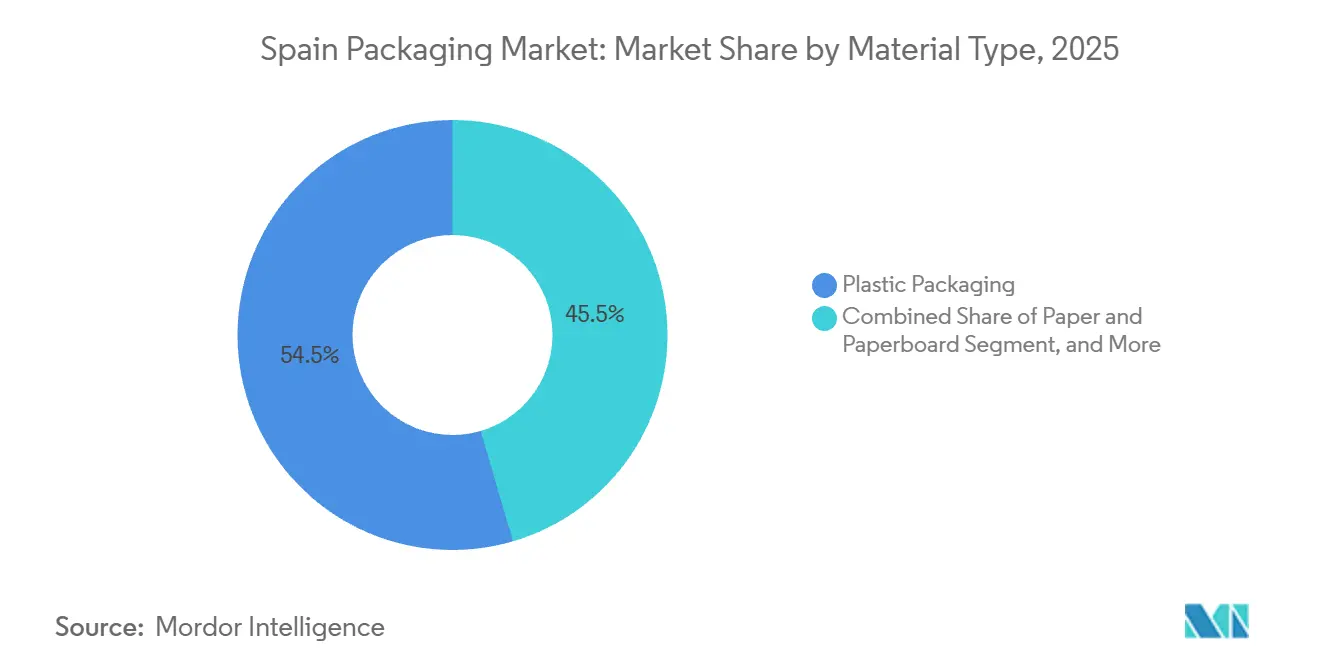

- By material, plastic packaging led with 54.54% Spain packaging market share in 2025, while paper and paperboard is forecast to expand at a 5.32% CAGR to 2031.

- By product type, flexible plastics captured 36.92% of the Spain packaging market in 2025; single-use paper items are on track for a 6.46% CAGR through 2031.

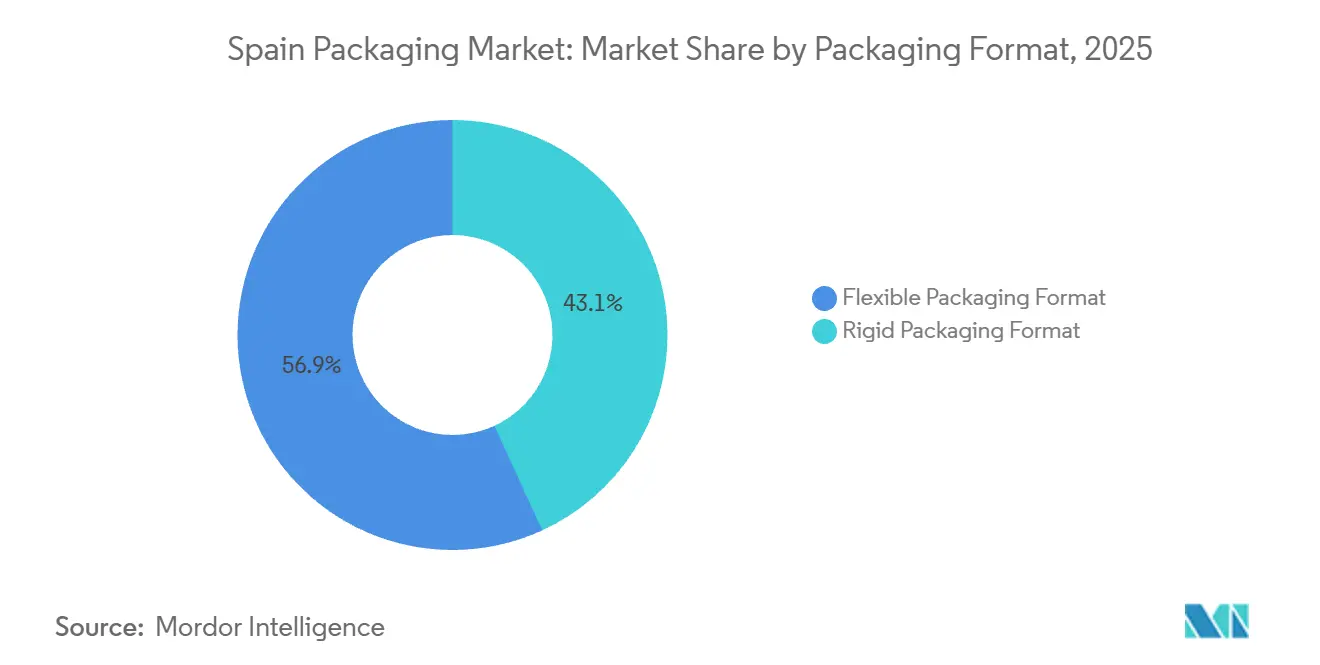

- By format, flexible configurations accounted for 56.86% of Spain packaging market size in 2025 and are projected to rise at a 5.75% CAGR, outpacing rigid formats.

- By end-user, food applications dominated with 27.78% share of Spain packaging market size in 2025, whereas personal care and cosmetics is expected to post the fastest 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Growth of Spain's Processed Food Exports | +1.2% | Cataluña, Andalucía, Comunidad Valenciana | Medium term (2–4 years) |

| Surge in E-commerce Parcel Volumes Requiring Protective Packaging | +0.9% | Madrid, Barcelona, Valencia metropolitan areas | Short term (≤ 2 years) |

| Tourism Rebound Elevating On-the-Go Packaging Demand | +0.7% | Cataluña, Illes Balears, Andalucía, Canarias | Short term (≤ 2 years) |

| Mandatory Recyclability Targets Under Royal Decree 1055/2022 | +0.8% | National | Medium term (2–4 years) |

| Automation Investments in Catalan Packaging Hubs | +0.3% | Cataluña, Aragón, País Vasco | Long term (≥ 4 years) |

| Digital Product Passport Pilots Boosting Smart Packaging Adoption | +0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Growth of Spain's Processed Food Exports

The agri-food sector delivered a EUR 12.054 billion trade surplus in the first seven months of 2025, equal to 18.65% of national merchandise exports, and that export pull locks in baseline demand for corrugated shippers, aseptic cartons, and vacuum-skin films. Olive oil, wine, and pork bound for EU and Asian markets must comply with ISPM 15 wood-packaging rules, pushing adoption of certified pallets and heat-treated corrugated sheets.[1]Food and Agriculture Organization, “ISPM 15 Phytosanitary Standards for Wood Packaging,” fao.org Smurfit Kappa’s EUR 54 million (USD 64.6 million) bag-in-box plant in Alicante adds capacity tuned to bulk wine flows.[2]Smurfit Kappa, “Bag-in-Box Plant Alicante,” smurfitkappa.com Because exports shield mills from slow domestic retail, converters are upgrading to lightweight high-strength linerboard that trims freight costs per pallet. As a result, the Spain packaging market benefits from a resilient, currency-diversified demand base even when consumer spending eases.

Surge in E-commerce Parcel Volumes Requiring Protective Packaging

Parcel traffic reached 1.303 billion in 2024 and should add another 5.4% in 2025, intensifying needs for corrugated mailers, air-cushion films, and tamper-evident seals. Amazon and Inditex fulfillment hubs around Madrid and Barcelona press suppliers for next-day lead times, which is accelerating automation upgrades among regional box plants. Mondi’s recyclable paper-padded mailer, rolled out by Amazon Europe, illustrates how lightweight paper solutions can replace plastic bubble wrap without sacrificing drop resistance.[3]Mondi Group, “Amazon Paper-Padded Mailer,” mondigroup.com The e-commerce boom funnels incremental volume into the Spain packaging market while rewarding converters that integrate digital printing, late-stage customization, and return-ready formats.

Tourism Rebound Elevating On-the-Go Packaging Demand

International arrivals rose to 93.8 million in 2024, and travelers spent EUR 118.61 billion (USD 142 billion) through October 2025, reviving single-serve PET, aluminum cans, and paper cups at airports and coastal resorts. Vidrala responded with the 360-gram Bordelesa Nova Lite wine bottle, shaving transport emissions by 4% year on year. Quick-service restaurants in beach corridors are shifting from polystyrene to molded-fiber clamshells to align with the Single-Use Plastics Directive. High-profile collection campaigns by Ecovidrio and Ecoembes during peak tourist months reinforce recycling habits and the circular credentials of the Spain packaging market.

Mandatory Recyclability Targets Under Royal Decree 1055/2022

The decree took effect in 2023 and extends producer responsibility fees to commercial streams from January 2025, while raising the household recycling target to 70% by 2030. Ecoembes already managed 1.56 million tonnes of household packaging in 2024, posting a 76.3% recovery rate. Supermarkets qualify for zero fees when 85% of packaging is privately managed, nudging retailers toward in-house reverse logistics, as shown by Mercadona’s acquisition of Logifruit in December 2025. Converters must therefore design mono-material packs and switch to water-based inks that pass sorting tests, encouraging capital spending yet also driving higher-value orders throughout the Spain packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-Driven Raw Material Price Volatility | -0.6% | National | Short term (≤ 2 years) |

| Compliance Costs from Plastic Packaging Tax (EUR 0.45/kg) | -0.4% | National | Medium term (2–4 years) |

| Limited Availability of Food-Grade rPET and rPP | -0.5% | National, linked to EU recycling infrastructure | Medium term (2–4 years) |

| Competition from Imported Low-Cost Packaging | -0.3% | National, pressure on commodity grades | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Raw Material Price Volatility

The producer price index for pulp, paper, and paperboard remained 8.5% above pre-pandemic levels in October 2025, and plastic resin swung from EUR 528 (USD 632) per tonne in mid-2022 to EUR 323 (USD 387) per tonne a year later, before stabilizing near EUR 400 (USD 479) per tonne. Such turbulence undermines long-term supply contracts and pushes small converters with limited hedging tools into cash-flow stress. Energy remains another wild card, despite biomass boiler projects at International Paper’s Madrid mill designed to cut CO₂ by 50%. Persistent raw-material volatility therefore subtracts momentum from the Spain packaging market even as demand grows.

Limited Availability of Food-Grade rPET and rPP

Spain has roughly 2 million tonnes of plastic recycling capacity, yet EFSA approvals for food-contact rPET remain scarce, and about 300,000 tonnes of capacity shut down across the EU in 2024 due to low virgin resin prices. Beverage brands that have pledged 50% recycled content are importing pellets from Germany and the Netherlands, adding freight costs and carbon emissions. The plastic-packaging tax grants relief only if packs hit 25% recycled content, creating a compliance cliff for converters who cannot secure supply. Shortfalls in food-grade recyclate thus act as a material brake on the circular transition of the Spanish packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Paper Gains Ground as Tax Economics Shift

Plastic packaging held 54.54% of the Spain packaging market in 2025, spanning flexible films, bottles, and closures. Paper and paperboard are forecast to post the fastest 5.32% CAGR through 2031 as brand owners seek tax relief and prepare for EU recyclability rules. The Spain packaging market size for paper grades benefits from investments such as Mondi’s EUR 30 million (USD 36 million) Zaragoza upgrade that adds recyclable barrier papers. Metal retains a niche in canned foods and beverages thanks to infinite recyclability, while container glass rides premium wine and spirits demand, supported by Vidrala’s 49% cullet rate. Polyethylene and polypropylene continue as workhorses for liners and microwaveable trays, though lightweight designs mitigate tax exposure. Polyvinyl chloride and polystyrene slide under regulatory pressure, replaced by molded fiber and PET alternatives.

Converters poured EUR 288 million (USD 345 million) into Spanish paper mills in 2023, with a quarter earmarked for innovation that lowers basis weights and boosts recycled content. Smurfit WestRock’s Navarra machine rebuild will widen kraftliner grammage flexibility, reducing energy per tonne. Metal-can suppliers pursue lightweight ends and tethered tabs, mirroring PET tethered closures that comply with the Single-Use Plastics Directive. Overall, tax incentives and circular commitments slot paper firmly into the Spain packaging market growth engine, even as plastics maintain scale.

By Product Type: Flexible Plastics Dominate, Paper Serviceware Accelerates

Flexible plastics captured 36.92% of the Spain packaging market share in 2025 through snack pouches, frozen-food films, and pharmaceutical laminates. Yet single-use paper cups, bowls, and wraps are expected to expand at a 6.46% CAGR on the back of quick-service restaurants and revived tourism. Corrugated boxes still command volume leadership; Spain produced 6.049 million tonnes of paper and cardboard in 2023, two-thirds of which fed the packaging chain. Folding cartons cater to cosmetics and confectionery; Quadpack invested EUR 2 million (USD 2.4 million) in injection capacity for PMMA jars that elevate shelf appeal.

Rigid plastics, dominated by PET bottles and polypropylene closures, pivot toward lightweighting and tethered caps to satisfy both taxation and EU directives. PET preform makers such as Plastipak supply local fillers, while Coveris rolls out easily separable paper-plastic laminates. Aluminum beverage cans, supplied by Ball and Crown, grow on the back of craft beer and energy drinks, taking advantage of their 100% recyclability. Glass remains entrenched in premium wine, with Vidrala’s new color palette offering differentiation. Net, flexible plastics maintain primacy in Spain packaging market volume, but paper serviceware now leads relative growth.

By Packaging Format: Flexibles Outpace Rigids under Weight-Based Tax

Flexible formats accounted for 56.86% of the Spanish packaging market in 2025 and are forecast to grow at a 5.75% CAGR to 2031. Stand-up pouches, flow-wrap films, and vacuum-skin packs use up to 70% less material than rigid jars, magnifying the savings when the plastic-packaging tax is levied by weight. Mondi’s BarrierPack Recyclable illustrates how a paper-aluminum laminate can meet oxygen and moisture specs without a polyethylene layer. E-commerce adds further pull, as Amazon adopts paper-padded mailers that ship flat and reduce void fill.

Rigid formats still dominate beverages, cosmetics, and premium foods. Coca-Cola European Partners trimmed PET bottle weight by 15% between 2020 and 2024, and Vidrala matched with the 360-gram Nova Lite wine bottle. Refill models also lift rigid demand; Mercadona’s integration of Logifruit crates keeps containers in closed loops for multiple trips. In balance, flexible packaging will carry the growth baton, but rigid innovations ensure continued relevance in the Spain packaging market.

By End-User: Food Leads, Beauty Sets the Pace

Food contributed 27.78% of the Spain packaging market in 2025, anchored by export-oriented olive oil, wine, and pork that require corrugated, aseptic, and vacuum-skin solutions. Supermarket private-label expansion lets large retailers negotiate volume discounts, and reusable crate fleets cut costs per trip. Quick-service outlets, boosted by tourism, swap polystyrene for compostable or PET serviceware, supporting paper hubs such as Drylock’s EUR 113 million (USD 135 million) biosustainable complex in Segovia.

Personal care and cosmetics is projected as the fastest 6.18% CAGR segment. Barcelona-based Quadpack rolls out FSC-certified Woodacity caps and refillable compacts that meet luxury brands’ sustainability playbooks. Beverage packaging follows, covering PET, aluminum, glass, and cartons. Industrial and chemical users deploy drums and IBCs, while agriculture leans on stretch films and returnable produce crates linked to IFCO’s IoT-enabled pooling network. This mixed end-user matrix ensures steady core volume for the Spain packaging market while enabling high-margin niches in premium beauty.

Geography Analysis

Cataluña tops Spain packaging market demand, riding a blend of food exports, cosmetics production, and 19.3% of 2024 tourist arrivals. Saica’s EUR 100 million (USD 120 million) corrugated plant in Barcelona and Nestlé’s EUR 15 million (USD 18 million) sustainable lines in Girona exemplify capacity bets on regional growth. Madrid functions as the e-commerce nerve center; International Paper’s biomass boiler at Fuenlabrada underscores a push to lower grid exposure. Andalucía funnels olive oil and citrus through export corridors, underpinning corrugated flows, while the País Vasco hosts Vidrala’s flagship glass plant, supplying Rioja wineries.

Aragón benefits from Mondi’s EUR 30 million investment in Zaragoza, aimed at recyclable paper. Illes Balears and Canarias see seasonal peaks in single-serve beverage sales, supported by Ecovidrio’s EUR 743 million (USD 889 million) island container rollout to reach 80% glass recycling by 2030.

Comunidad Valenciana balances citrus exports and ceramic-tile protective packaging, while Castilla y León’s automotive clusters lift demand for returnable racks. Harmonization under Royal Decree 1055/2022 should smooth regional fee disparities, but municipalities with fragmented waste systems still face higher compliance costs.

Competitive Landscape

Multinationals such as Smurfit WestRock, Mondi, Amcor, and International Paper compete with regional champions Saica, Vidrala, and Hinojosa, giving the Spain packaging market a moderately fragmented structure. Smurfit WestRock posted Q3 2025 net sales of USD 8.003 billion and is modernizing Navarra paper machine 3 for a Q1 2026 start-up.

International Paper vaulted into the top tier after buying DS Smith, though EU regulators forced a divestiture of a Bilbao plant to PALM Group. Retailer vertical integration is rising, Mercadona bought Logifruit and its 1,600-employee crate pool to internalize reverse logistics.

Technology also differentiates. IFCO’s Barcelona digital hub embeds IoT sensors and AI routing to extend crate life. Ecoembes invests EUR 192.5 million (USD 230.4 million) per year into AI sorting and digital watermarks to lift recovery rates. Smaller converters feeling the tax and compliance squeeze are prime targets; Nefab’s April 2025 purchase of Embalajes Echeberría and Iflex’s EUR 1.6 million (USD 1.9 million) capital raise illustrate consolidation and fresh capacity plays. The net result is a landscape where scale, recycling capability, and digital upgrades dictate competitive success.

Spain Packaging Industry Leaders

Amcor PLC

International Paper Company

Crown Holdings Inc.

Coveris Holdings SA

Quadpack Industries SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Voith confirmed that modernization of paper machine 3 at Smurfit WestRock’s Navarra mill remains on track for Q1 2026 commissioning.

- November 2025: Copack Envases Activos broke ground on a flexible-packaging plant in Murcia to expand active and intelligent packaging capacity.

- July 2025: Iflex Flexible Packaging secured EUR 1.6 million in new equity to fund land purchase and an Olympia laminator, lifting first-half 2025 sales to EUR 7.75 million.

- April 2025: Nefab acquired Embalajes Echeberría to deepen its Spanish logistics-packaging footprint.

Spain Packaging Market Report Scope

The study tracks the market from the demand perspective and the revenue derived from the sales of packaging solutions made of plastic, paper, glass, and metal. The study also tracks the effects of regulations and market drivers, as well as factors challenging market growth.

The Spain Packaging Market Report is Segmented by Material Type (Paper and Paperboard, Plastic, Metal, and Container Glass), Product Type (Paper and Paperboard Products, Plastic Products, Metal Products, and Container Glass Products), Packaging Format (Rigid, and Flexible), and End-User (Food, Beverage, Pharmaceuticals and Medical, Personal Care and Cosmetics, Industrial and Chemical, Agriculture, Automotive, and Other End-users). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Paper and Paperboard | |

| Plastic | Polyethylene Polypropylene (PP) |

| High-density Polyethylene (HDPE) and Low-density Polyethylene (LDPE) | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride (PVC) | |

| Polystyrene (PS) | |

| Other Plastics | |

| Metal | |

| Container Glass |

By Product Type

| Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | ||

| Single-use Paper Products | ||

| Other Paper and Paperboard Product Types | ||

| Plastic Product Type | Rigid Plastics | Bottles and Jars |

| Caps and Closures | ||

| Bulk-Grade Products | ||

| Other Rigid Plastics | ||

| Flexible Plastics | Pouches | |

| Bags | ||

| Films and Wraps | ||

| Other Flexible Plastics | ||

| Metal Product Type | Cans | |

| Aerosol Containers | ||

| Caps and Closures | ||

| Other Metal Product Types | ||

| Container Glass Product Type | Bottles | |

| Jars | ||

By Packaging Format

| Rigid Packaging Format |

| Flexible Packaging Format |

By End-user

| Food |

| Beverage |

| Pharmaceuticals and Medical |

| Personal Care and Cosmetics |

| Industrial and Chemical |

| Agriculture |

| Automotive |

| Other End-users |

| By Material Type | Paper and Paperboard | ||

| Plastic | Polyethylene Polypropylene (PP) | ||

| High-density Polyethylene (HDPE) and Low-density Polyethylene (LDPE) | |||

| Polyethylene Terephthalate (PET) | |||

| Polyvinyl Chloride (PVC) | |||

| Polystyrene (PS) | |||

| Other Plastics | |||

| Metal | |||

| Container Glass | |||

| By Product Type | Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | |||

| Single-use Paper Products | |||

| Other Paper and Paperboard Product Types | |||

| Plastic Product Type | Rigid Plastics | Bottles and Jars | |

| Caps and Closures | |||

| Bulk-Grade Products | |||

| Other Rigid Plastics | |||

| Flexible Plastics | Pouches | ||

| Bags | |||

| Films and Wraps | |||

| Other Flexible Plastics | |||

| Metal Product Type | Cans | ||

| Aerosol Containers | |||

| Caps and Closures | |||

| Other Metal Product Types | |||

| Container Glass Product Type | Bottles | ||

| Jars | |||

| By Packaging Format | Rigid Packaging Format | ||

| Flexible Packaging Format | |||

| By End-user | Food | ||

| Beverage | |||

| Pharmaceuticals and Medical | |||

| Personal Care and Cosmetics | |||

| Industrial and Chemical | |||

| Agriculture | |||

| Automotive | |||

| Other End-users | |||

Key Questions Answered in the Report

What is the current value of the Spain packaging market and its expected growth?

The Spain packaging market size reached USD 22.58 billion in 2026 and is forecast to reach USD 27.75 billion by 2031, implying a 4.21% CAGR.

Which material category is growing fastest in Spanish packaging?

Paper and paperboard are projected to expand at a 5.32% CAGR through 2031 as brands substitute toward recyclable substrates.

How is the plastic-packaging tax affecting converter strategies?

The EUR 0.45 per kilogram tax on non-recycled plastic accelerates lightweighting, mono-material design, and a shift to paper-based alternatives.

Which end-user segment will post the highest growth?

Personal care and cosmetics packaging is forecast to advance at a 6.18% CAGR thanks to premiumization and refillable beauty formats.

What geographic region contributes the most packaging demand?

Cataluña leads demand on the back of export-oriented food processors, cosmetics manufacturing, and high tourist arrivals.

Are multinational or regional firms dominant in Spain?

The market is moderately fragmented, with multinationals like Smurfit WestRock and Mondi holding scale advantages but regional leaders such as Saica and Vidrala retaining strong local positions.

Page last updated on: