Hotel And Hospitality Management Software Market Size and Share

Market Overview

| Study Period | 2025 - 2030 |

|---|---|

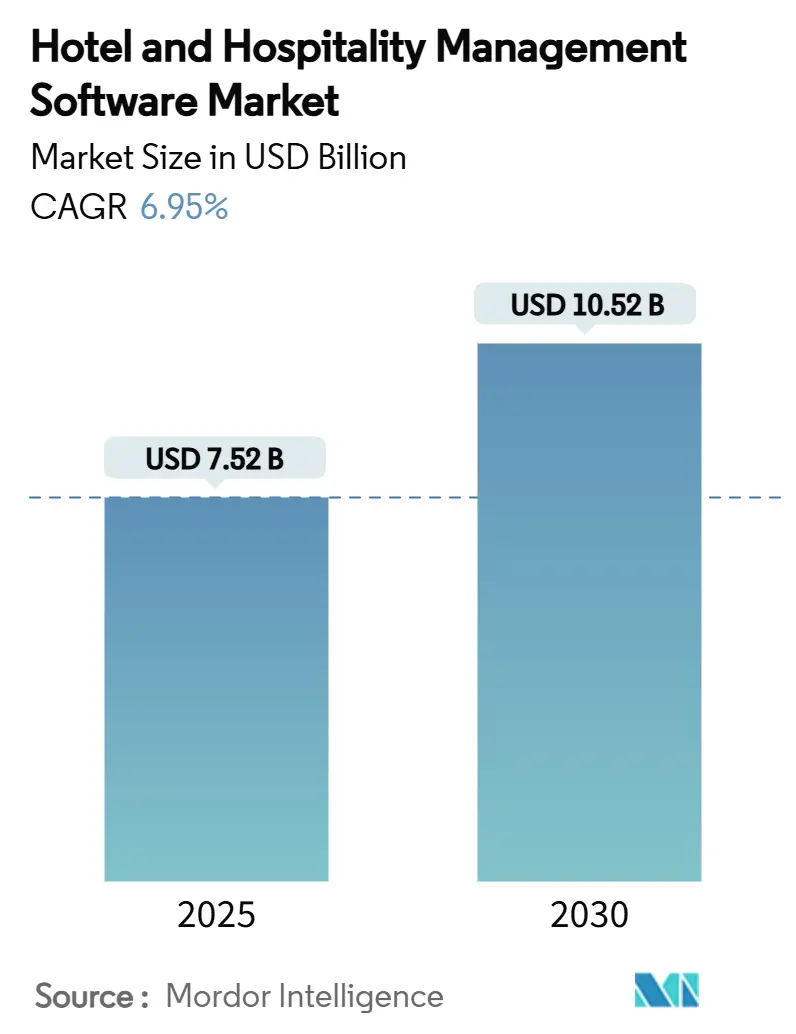

| Market Size (2025) | USD 7.52 Billion |

| Market Size (2030) | USD 10.52 Billion |

| Growth Rate (2025 - 2030) | 6.95% CAGR |

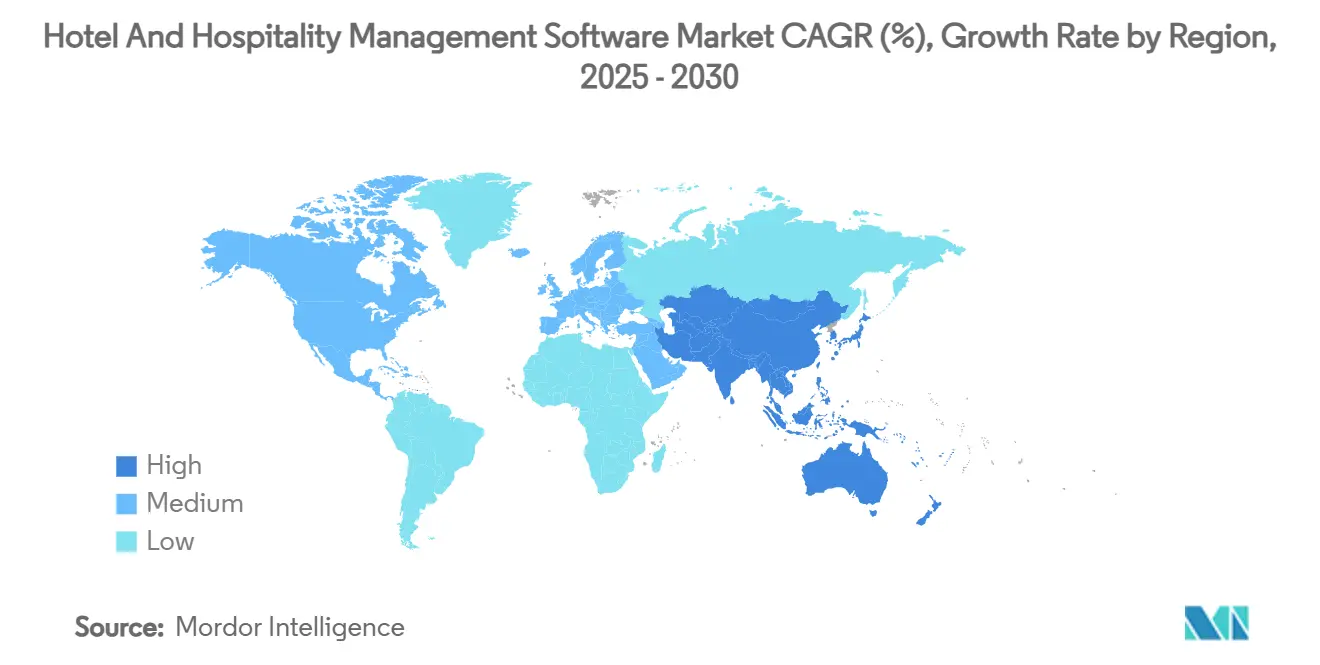

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hotel And Hospitality Management Software Market Analysis by Mordor Intelligence

The hotel and hospitality management software market recorded a market size of USD 7.52 billion in 2025 and is forecast to reach USD 10.52 billion by 2030, advancing at a 6.95% CAGR over the period. Hotels are prioritizing cloud-native platforms to relieve mounting cost pressure as labor expenses rose USD 9 per room in 2024 while overall operating costs outpaced revenue growth.[1]STR, “Hotel F&B Driving Labor Cost Growth in 2024,” str.com Mandatory digital invoicing rules in Europe, beginning with Germany’s January 2025 launch, add fresh urgency because legacy architectures already absorb 60-80% of IT budgets.[2]Johannes Vocke, “Adapting to Germany's E-Invoicing Compliance,” hospitalitynet.org Large enterprise migrations-Hyatt’s move to Oracle Opera Cloud for 1,000+ properties and Marriott’s deployment across premium brands-prove the strategic value of platform modernisation and underpin demand momentum. At the same time, independent hotels gain affordable access to enterprise-grade solutions, driving competitive intensity across all property sizes.

Key Report Takeaways

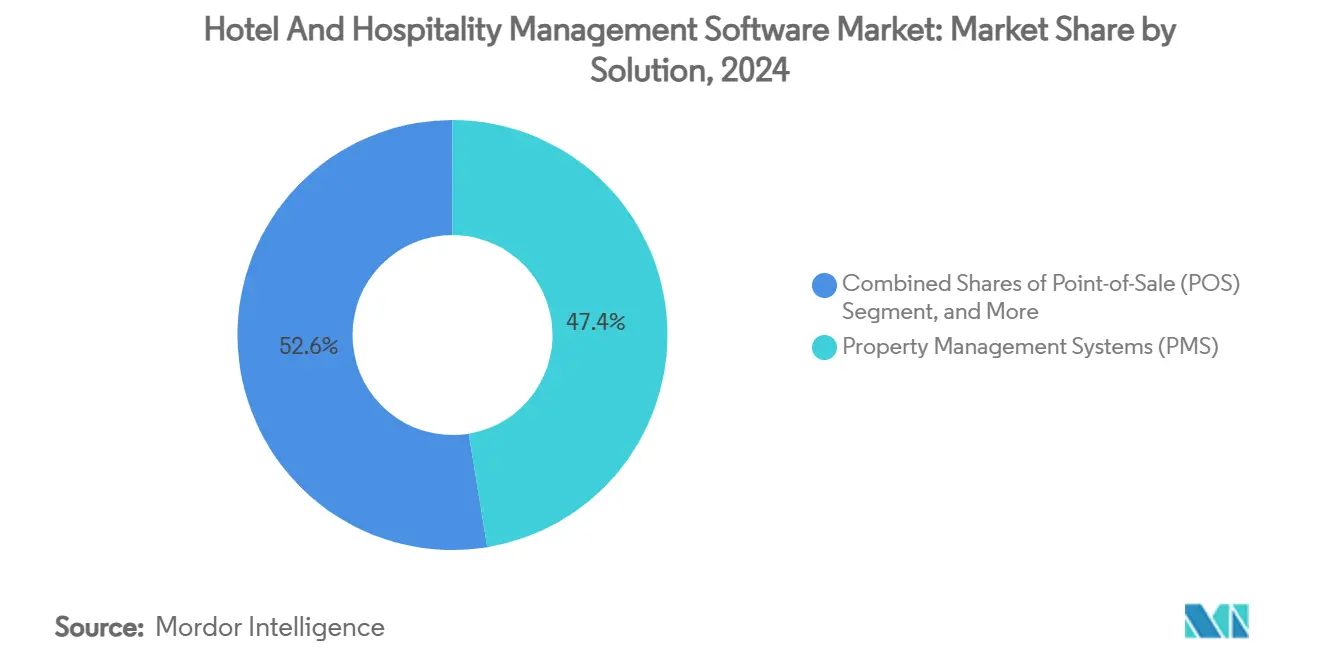

- By solution, Property Management Systems led with 47.41% of the hotel and hospitality management software market share in 2024; Revenue Management is forecast to grow fastest at an 8.34% CAGR through 2030.

- By deployment, cloud-based models accounted for 61.92% of the hotel and hospitality management software market size in 2024 and are projected to expand at a 9.17% CAGR to 2030.

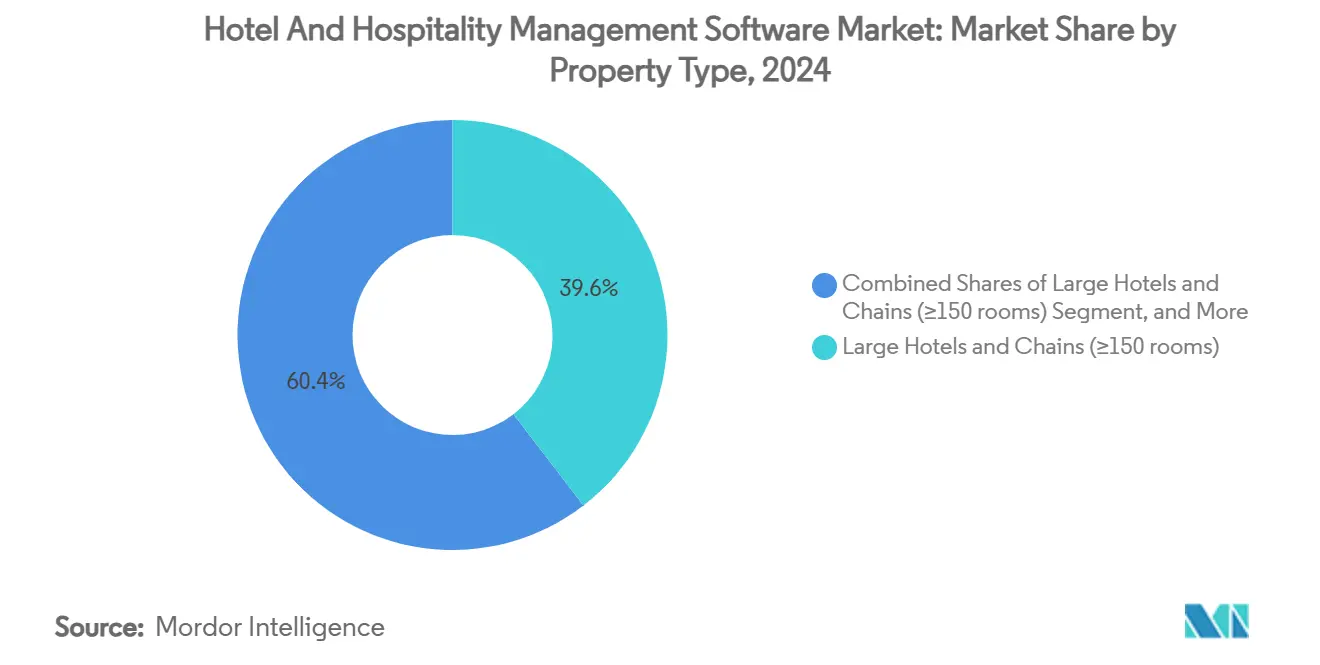

- By property type, Large Hotels & Chains held 39.58% share of the hotel and hospitality management software market size in 2024, while Serviced Apartments and Vacation Rentals are set to climb at a 10.47% CAGR to 2030.

- By end user, Hotel Chains retained 35.97% share, yet Independent Hotels are expected to advance at an 11.81% CAGR through 2030 within the hotel and hospitality management software market size.

- By geography, North America dominated with 31.64% share in 2024; Asia-Pacific is forecast to post the fastest 10.07% CAGR through 2030.

Global Hotel And Hospitality Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift toward cloud-native PMS platforms | +1.8% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Accelerating adoption of contact-less guest journey tools | +1.2% | Global, with Asia-Pacific showing highest growth | Short term (≤ 2 years) |

| Growth in mid-scale hotel construction pipelines | +0.9% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Mandatory digital invoicing and e-visitor regulations in Europe | +0.7% | Europe, with spillover to other regulated markets | Short term (≤ 2 years) |

| Rise of AI-driven dynamic pricing engines | +1.1% | Global, with independent hotels showing rapid adoption | Medium term (2-4 years) |

| Ecosystem push from OTAs and GDS APIs lowering integration cost | +0.8% | Global, particularly benefiting smaller properties | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid shift toward cloud-native PMS platforms

Thirty percent of 2025 hotel IT budgets are now earmarked for new cloud Property Management Systems, freeing resources previously locked in maintaining aging software. Hyatt reported 34% less downtime and 50% fewer service-desk tickets after moving 1,000+ properties to Oracle Opera Cloud, underscoring the operating gains available at scale. Choice Hotels completed the hospitality sector’s first full data-center exit by decommissioning 3,729 servers and relocating every workload to AWS, cementing the enterprise case for cloud migration. These examples show how modern architectures integrate real-time data flows across revenue, guest-experience, and back-office modules. The performance uplift creates an attractive runway for vendors positioned with API-first, multitenant platforms.

Accelerating adoption of contact-less guest journey tools

Contact-less technologies moved from pandemic necessity to revenue lever as 71% of business travelers prefer online check-in and participating hotels report 25% higher guest satisfaction. Digital keys already approach 70% penetration in upscale properties, cutting front-desk labor while raising convenience.[3]SALTO Systems, “The Rise of Mobile Keys in Hospitality,” bdcnetwork.com Upselling engines embedded in mobile pre-arrival flows deliver 35.7% conversion rates, illustrating ancillary-revenue potential. Properties deploying full contact-less suites see 76% of guests more likely to return, translating adoption into measurable loyalty uplift. Facial recognition pilots and biometric ID promise even faster interactions, though European eIDAS II rules require stringent privacy controls.

Growth in mid-scale hotel construction pipelines

Developers are concentrating on mid-scale formats that balance affordability with tech-enabled consistency. Asia-Pacific leads, supported by China’s 86.91 million hotels and 2.888 million rooms, which create sizeable demand pools for cloud-ready systems. Newbuild properties skip legacy constraints and open with integrated stacks that automate housekeeping, maintenance, and guest messaging from day one. Vendors specialising in rapid onboarding and lightweight pricing models gain first-mover advantage as investors insist on scalable but cost-efficient backbones.

Mandatory digital invoicing and e-visitor regulations in Europe

Germany’s e-invoicing mandate took effect January 2025, obliging hotels to generate ZUGFeRD or XRechnung documents, while Spain now requires real-time visitor data uploads to the interior ministry. Add the European Accessibility Act’s June 2025 deadline for digital interfaces and the compliance burden becomes impossible without modern, standards-based software. Providers embedding turnkey compliance thus secure competitive edges as multinational chains standardise on a single global platform capable of meeting Europe’s rules and future extensions elsewhere.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy data-migration complexity in full-service chains | -1.4% | Global, particularly North America and Europe | Medium term (2-4 years) |

| High churn among small independent properties | -0.8% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Data-privacy compliance costs (GDPR, CPRA, PDPA) | -0.6% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Fragmented on-prem hardware in emerging economies | -0.5% | Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy data-migration complexity in full-service chains

Decades of customisations mean converting an enterprise PMS can take 12-18 months, with feared service interruptions at cutover. Wyndham trimmed expected downtime by 34% while migrating 550 hotels in one month, yet such successes require specialised tooling and experienced partners. Duplicate guest profiles and bespoke interfaces further complicate projects, prompting some brands to stagger rollouts. Even so, once legacy debt is retired, maintenance drops sharply, freeing capital for innovation.

High churn among small independent properties

The 2025 European Accommodation Barometer notes 61% of establishments cite high upfront costs and 58% flag integration complexity as technology barriers, leading to elevated contract turnover. Ownership changes amplify risk in emerging markets where financing is fragile. Subscription-based, modular suites that go live in days rather than months mitigate churn by aligning cost with revenue seasonality, but vendors must still balance acquisition expense against shorter average customer life.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: PMS Dominance Faces Revenue Management Disruption

Property Management Systems held 47.41% of hotel and hospitality management software market share in 2024, confirming their role as operational hubs. However, Revenue Management applications are advancing at an 8.34% CAGR through 2030, reflecting management’s pivot from cost control towards profit optimisation. Many vendors now bundle AI pricing engines into PMS suites, blurring category lines but enlarging the hotel and hospitality management software market.

Channel Management, Booking Engines, and Guest Experience modules follow PMS upgrades, since integrated data flow maximises direct booking conversion and personalised offers. Case studies like Kabannas’ 92% chatbot query resolution and 35.7% upsell conversion underline tangible ROI. As integrations standardise, point-solutions risk displacement by broader platforms, compelling specialists to innovate or partner to stay relevant.

By Deployment: Cloud Migration Accelerates Across All Segments

Cloud deployments represented 61.92% of hotel and hospitality management software market size in 2024 and are projected to grow 9.17% annually. Choice Hotels’ removal of 3,729 servers exemplifies capital redeployment potential when infrastructure moves to IaaS. Vendors monetise through subscription arrangements that align revenue with value delivered, while customers appreciate automatic updates and built-in redundancy.

On-premise persists where data-sovereignty or patchy connectivity dictate local hosting, though even these hotels experiment with hybrid models that replicate data to the cloud. Oracle’s 27% cloud-services revenue growth validates market appetite for multitenant architectures. As hotel boards demand resilience and speed, cloud penetration will continue widening across geographies and property classes.

By Property Type: Serviced Apartments Disrupt Traditional Hospitality Models

Large Hotels & Chains retained 39.58% share in 2024 thanks to brand resources and global loyalty programs. Yet Serviced Apartments and Vacation Rentals are expanding at a 10.47% CAGR, making them the hottest sub-segment within the hotel and hospitality management software market. Their hybrid operating model needs both transient guest tools and longer-stay lease features, prompting specialised vendors like Hostaway to emerge.

Resorts add complexity with multiple revenue centres per guest, from golf to spa, requiring tightly integrated reservations and POS. Meanwhile, small and mid-size hotels benefit from SaaS licensing that scales with room count, letting independents access modules once limited to chain budgets.

By End User: Independent Hotels Drive Technology Democratization

Hotel Chains still commanded 35.97% of hotel and hospitality management software market share in 2024, but Independent Hotels are on track for 11.81% CAGR growth. Cloudbeds reports 40% more direct bookings and 60% lower software spend for independent adopters, underscoring economic motivation.

Resorts and Spas demand guest-centric workflows that orchestrate rooms with wellness, while Cruises and Casinos add maritime and gaming regulations. Vendors that present configurable templates rather than rigid feature sets gain favour because diverse end users want to activate only relevant modules without code changes.

Geography Analysis

North America captured 31.64% of hotel and hospitality management software market share in 2024 due to entrenched enterprise systems and high per-property IT budgets. Replacement cycles now dominate as chains phase out on-premise stacks in favour of fully managed cloud services, securing predictable operating expenditure over capex peaks.

Asia-Pacific is forecast to post a 10.07% CAGR to 2030, the fastest globally, fuelled by China’s extensive hotel estate and ongoing new-build surge. Many properties there leapfrog legacy architectures, implementing modern suites from the outset and drawing vendors eager for greenfield scale. Southeast Asian governments also promote digital tourism platforms that embed standardized APIs, easing software vendor entry.

Europe sits between maturity and disruption. GDPR and January 2025 e-invoicing obligations force hotels to upgrade, creating spikes in demand despite softer economic indicators. Supplier selection increasingly hinges on proven compliance toolkits. South America and the Middle East & Africa remain largely underpenetrated but attractive over the long run as inbound travel rebounds and investors fund regional brand expansion. Connectivity and local language support remain primary hurdles vendors must address to convert pipeline in these regions.

Competitive Landscape

The hotel and hospitality management software market is moderately fragmented. Oracle, Agilysys, and Sabre maintain scale via extensive R&D, broad module portfolios, and enterprise contracts. Oracle reported USD 6.7 billion in hospitality-related cloud revenue for fiscal 2025, up 27%, signalling effective monetisation of its Opera Cloud road map. Sabre’s planned USD 1.1 billion divestiture of its Hospitality Solutions unit reshapes competitive positions and frees capital for its airline core.

Challengers like Mews and Cloudbeds grow quickly on usability, API openness, and rapid deployment. Mews secured USD 100 million from Vista Credit Partners to extend acquisition capacity, pointing to continued roll-up potential. AI capability arms-races intensify: Microsoft’s patent for a hotel-oriented virtual assistant shows tech giants’ interest in conversational interfaces.

Specialist niches also proliferate. BirchStreet leads procure-to-pay automation, while Duetto’s HotStats acquisition fuses revenue and profit analytics. Vendors differentiate through ecosystem partnerships-xnPOS linking to Stayntouch PMS, or Guestline embedding an AI Revenue Management System-to present one-stop solutions without rebuilding every module internally. M&A, strategic partnerships, and verticalised innovation will therefore stay central to competitive strategy over the forecast horizon.

Hotel And Hospitality Management Software Industry Leaders

Oracle Corporation

Sabre Corporation

Agilysys Inc.

Amadeus IT Group S.A.

Cloudbeds LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sabre agreed to sell its Hospitality Solutions business for USD 1.1 billion, streamlining focus on airline and travel marketplace services.

- April 2025: Duetto acquired HotStats to blend revenue management with profit benchmarking, aiming to deliver an end-to-end commercial platform.

- March 2025: IDS Next bought ShawMan Software, adding POS and spa modules that deepen its integrated suite for full-service hotels

- January 2025: Mews acquired Clarity Hospitality to strengthen presence in APAC and the UK upscale segment and accelerate cross-sell of its cloud PMS.

Global Hotel And Hospitality Management Software Market Report Scope

| Property Management Systems (PMS) |

| Point-of-Sale (POS) |

| Channel Management |

| Booking Engine |

| Guest Experience / CRM |

| Revenue Management |

| Other Solutions |

| Cloud-based |

| On-premise |

| Hybrid |

| Small and Mid-Size Hotels (≤150 rooms) |

| Large Hotels and Chains (≥150 rooms) |

| Resorts |

| Serviced Apartments and Vacation Rentals |

| Other Property Types |

| Independent Hotels |

| Hotel Chains |

| Resorts and Spas |

| Cruises and Casinos |

| Other End-users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Turkey | ||

| Saudi Arabia | ||

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Solution | Property Management Systems (PMS) | ||

| Point-of-Sale (POS) | |||

| Channel Management | |||

| Booking Engine | |||

| Guest Experience / CRM | |||

| Revenue Management | |||

| Other Solutions | |||

| By Deployment | Cloud-based | ||

| On-premise | |||

| Hybrid | |||

| By Property Type | Small and Mid-Size Hotels (≤150 rooms) | ||

| Large Hotels and Chains (≥150 rooms) | |||

| Resorts | |||

| Serviced Apartments and Vacation Rentals | |||

| Other Property Types | |||

| By End User | Independent Hotels | ||

| Hotel Chains | |||

| Resorts and Spas | |||

| Cruises and Casinos | |||

| Other End-users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Turkey | |||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the 2025 value of the hotel and hospitality management software market?

The market reached USD 7.52 billion in 2025.

Which solution commanded the largest share in 2024?

Property Management Systems led with 47.41% share.

How fast is the Asia-Pacific region growing?

Asia-Pacific is projected to register a 10.07% CAGR through 2030.

Why are independent hotels adopting software rapidly?

Cloud pricing models lower upfront costs, enabling independents to access enterprise-grade tools and boost direct bookings by 40%.

What regulatory change is influencing European adoption?

Germany’s January 2025 e-invoicing mandate is forcing hotels to upgrade to compliant digital platforms.

Which deployment model is expanding quickest?

Cloud-based deployments are forecast to grow 9.17% annually to 2030.

Page last updated on: