Aviation Testing Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.58 Billion |

| Market Size (2030) | USD 4.21 Billion |

| Growth Rate (2025 - 2030) | 3.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Testing Services Market Analysis by Mordor Intelligence

The aviation testing services market size is valued at USD 3.58 billion in 2025 and is forecasted to reach USD 4.21 billion by 2030, advancing at a 3.28% CAGR. Persistent fleet renewal, the shift toward data-rich aircraft, and widening adoption of alternative propulsion together recalibrate demand for validation across structures, avionics, propulsion, and emerging flight platforms. Testing providers are investing in digital twins, artificial intelligence (AI)-driven analytics, and remote sensor networks to migrate from episodic inspections to continuous airworthiness verification. Regulatory tightening around software updates and cyber-hardening enlarges the serviceable market for security-centred test regimes. At the same time, hypersonic programs and hydrogen propulsion trials broaden the technical envelope that laboratories must accommodate. Competitive pressure intensifies as test-as-a-service offerings give smaller operators access to sophisticated rigs without committing fresh capital, accelerating market fragmentation and raising utilization of high-value facilities.

Key Report Takeaways

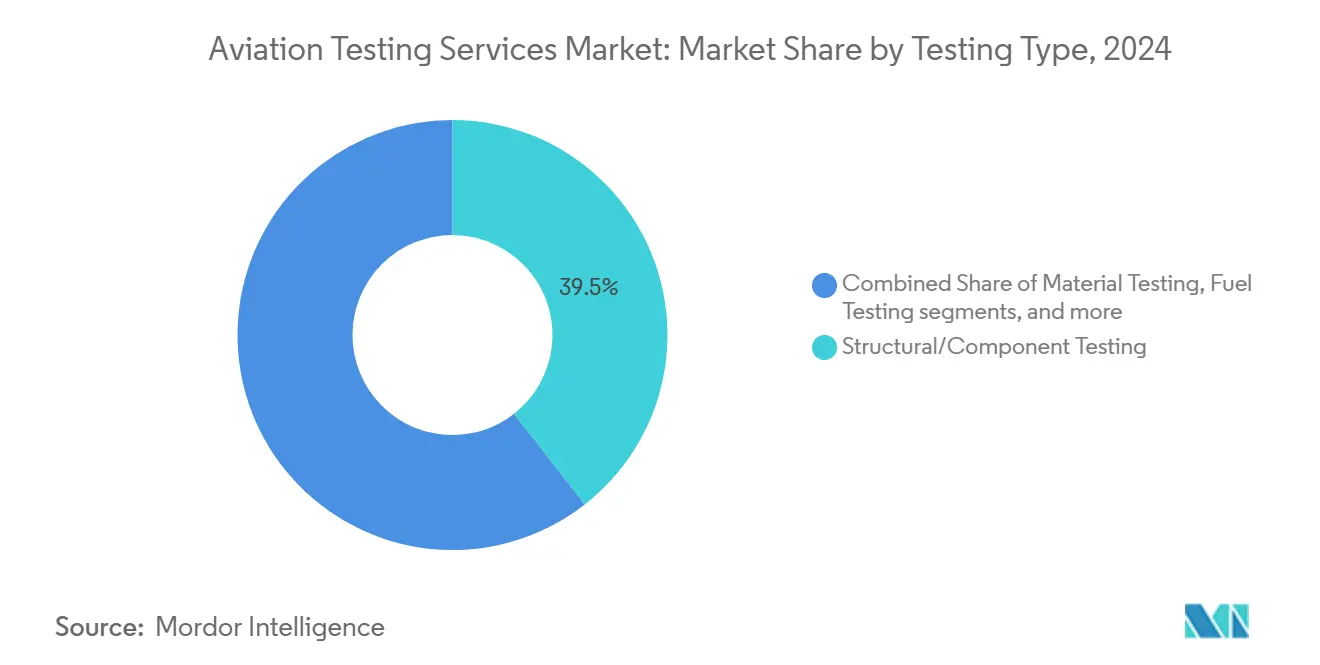

- By testing type, structural/component services captured 39.45% of the aviation testing services market share in 2024, whereas avionics and electronics testing is forecast to grow at a 4.29% CAGR through 2030.

- By platform, commercial aviation led with 64.25% revenue in 2024; unmanned aerial vehicles (UAVs) are projected to expand at a 6.5% CAGR to 2030.

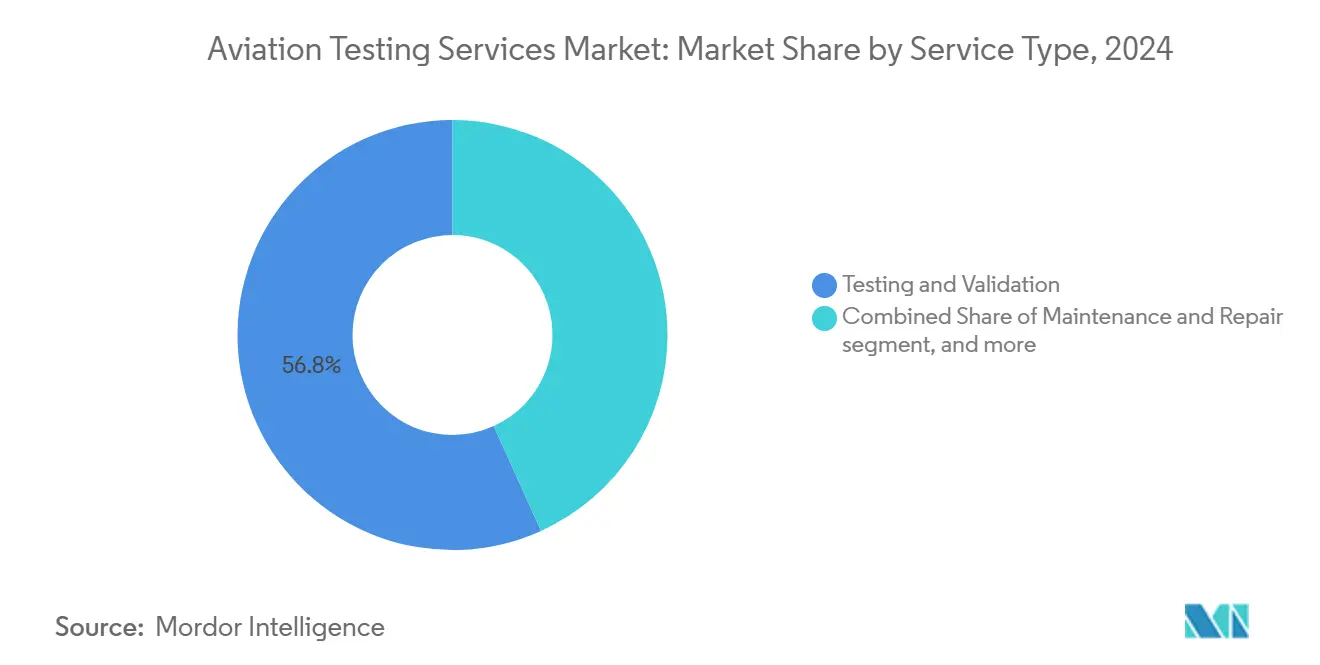

- By service type, validation services held 56.76% of the aviation testing services market in 2024, while test-as-a-service is positioned for a 4.91% CAGR between 2025 and 2030.

- By end user, OEMs and Tier-1s commanded 56.46% revenue in 2024; defense agencies register the fastest projected CAGR at 3.95% through 2030.

- By geography, North America represented 41.43% of 2024 revenues. Yet, Asia-Pacific is expected to lead to growth at a 4.28% CAGR through 2030.

Global Aviation Testing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet expansion and MRO surge | +0.80% | Global, APAC and North America focus | Medium term (2-4 years) |

| Digital avionics modernization | +0.60% | North America and EU, extending into APAC | Long term (≥ 4 years) |

| Defense UAV investment | +0.50% | US, China, EU defense programs | Medium term (2-4 years) |

| Regulatory compliance pressure | +0.40% | Global, with FAA and EASA spearheading standards | Short term (≤ 2 years) |

| Predictive-maintenance self-test adoption | +0.30% | North America and EU core, spillover to APAC | Long term (≥ 4 years) |

| Localization driven by tariffs | +0.20% | APAC focus, emerging presence in MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fleet Expansion and MRO Surge

Commercial traffic recovery pushes worldwide flight hours back to pre-2020 levels, lifting inspection volumes for aging narrowbody fleets and initiating certification of new wide-body programs. The aviation testing services market responds by scaling non-destructive evaluation, digital-radiography, and computed-tomography capabilities that detect micro-fatigue in composite primary structures.[1]Graham Warwick, “2024 Review: Propulsion,” Aviation Week Network, aviationweek.com Airlines increasingly outsource structural validation to preserve turnaround time, motivating specialized laboratories to establish on-airport mini-hubs that deliver same-shift results. Digital twins feed predictive maintenance algorithms, obliging providers to validate sensor fidelity and anomaly detection code before deployment. This continuous-monitoring paradigm replaces calendar-bound inspections and creates recurring revenue for data analytics–enabled test firms. Asia-Pacific’s order backlog for narrowbody aircraft meets the demand for life-extension certification on older airframes that are being redeployed to secondary routes, cementing structural testing as the anchor of the aviation testing services market.

Digital Avionics Modernization

Software-defined cockpits, high-bandwidth gateways, and over-the-air updates stretch validation requirements beyond legacy hardware conformance. The US is finalizing cyber-protection rules that obligate airframers to prove resilience against unauthorized electronic interaction, including field-loadable software and wireless sensor nodes. Europe is advancing comparable guidance under EASA’s powered-lift framework, driving harmonization of security test cases. Testing providers must master penetration testing, fuzzing, and secure-boot verification alongside traditional electromagnetic interference and functional-safety checks. Integrating AI-powered flight control modules further intensifies validation complexity because deterministic evidence must cover dynamic algorithm adaptation. These factors propel avionics and electronics to be the fastest-growing slice of the aviation testing services market.

Defense UAV Investment

Defense ministries accelerate autonomous-systems budgets, spawning new flight-test corridors and ground-simulation suites that validate swarm logic, sense-and-avoid algorithms, and battlefield datalinks. Unlike civil certification, military programs demand mission-scenario stress tests under contested RF environments, raising the bar for hardware-in-the-loop simulation fidelity. Testing organizations that couple AI-driven scenario generation with high-speed telemetry analytics win contracts to compress prototype cycles. Dual-use technology transfer flows back into civil applications, especially for urban air mobility platforms, expanding the total addressable aviation testing services market while deepening potential for cross-sector synergies.

Regulatory Compliance Pressure

Evolving carbon-reduction policy and cybersecurity directives initiate cascading compliance checkpoints. The European Union's (EU's) sustainable aviation fuel mandate introduces new assays for blend composition, thermal stability, and life-cycle emissions.[2]Airbus, “5 Actions to Protect Your Aircraft From Cyberattacks,” airbus.com The US requires foreign repair stations to implement drug-testing programs by 2027 and embed additional audits and sample-handling protocols within maintenance workflows. Concurrently, FAA and EASA coordination on eVTOL ruleset creation forces parallel validation streams for structural crashworthiness, energy-storage safety, and autonomous flight software. Collectively, these initiatives enlarge the aviation testing services market and obligate providers to maintain multi-jurisdictional expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital costs | -0.40% | Global, particularly affecting smaller providers | Short term (≤ 2 years) |

| Lengthy certification cycles | -0.30% | Global, varies by regulatory authority | Medium term (2-4 years) |

| RFIC supply-chain shortages | -0.20% | Global, concentrated in semiconductor-dependent regions | Short term (≤ 2 years) |

| Cybersecurity of networked testers | -0.10% | North America and EU, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs

A single environmentally controlled, multi-axis structural rig can exceed USD 10 million, while hypersonic test tunnels approach USD 100 million, locking out entrants and stressing mid-tier firms. Rapid obsolescence forces accelerated depreciation schedules, causing revenue profiles to lag investment outlays. Test-as-a-service business models partially alleviate cost barriers by spreading equipment usage across clients, but require high uptime and rigorous calibration traceability to stay profitable. Capital intensity, therefore, remains the most immediate brake on smaller providers joining the aviation testing services market.

Lengthy Certification Cycles

Complex avionics suites can spend five years in qualification as regulators digest novel architectures. Sustaining engineering-grade facilities idle during approval lulls suppresses cash flow, especially for suppliers dependent on single programs.[3]European Union Aviation Safety Agency, “Guidelines on Certification Timelines,” easa.europa.eu As airframers pivot to agile development, the mismatch between iterative design and static approval milestones widens. Recent regulatory sandbox initiatives aim to shorten timelines, yet practical implementation lags, perpetuating revenue uncertainty in the aviation testing services industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Testing Type: Structural Validation Drives Market Foundation

Structural and component evaluations generated 39.45% of the aviation testing services market in 2024 on the strength of intensive non-destructive inspection for aging widebody fleets. Demand centers on computed tomography, phased-array ultrasonics, and thermographic inspection that uncover subsurface flaws in carbon-fiber skins and titanium bulkheads.[4]Paul E. Eden, “Aircraft Testing,” Key.Aero, key.aero These services collectively represent the largest single contributor to the aviation testing services market size and remain indispensable because regulatory authorities mandate recurring airframe life-extension checks at tight intervals. The discipline also underpins certification of hydrogen tanks and cryogenic lines now entering the prototype phase, guaranteeing durable revenue even as digital systems proliferate.

Propulsion, fuel, and environmental test benches occupy a robust second tier, validating turbine durability across bird-strike, sand-ingestion, and icing conditions while vetting sustainable aviation fuel for seal compatibility and thermal performance. Electric-propulsion rigs add high-voltage isolation and electromagnetic-emission characterization, expanding the technical scope. Avionics and electronics, though accounting for a smaller 2024 base, deliver the highest forward CAGR at 4.29% because cybersecurity and AI verification overlay existing hardware conformance. As software content approaches 40% of aircraft development spend, electronics testing is forecast to erode structural dominance, yet will continue to rely on foundational environmental chambers, linking both domains within a converged aviation testing services market.

By Platform: Commercial Dominance Meets UAV Disruption

Commercial airline programs retained 64.25% of 2024 revenue, demonstrating the sustained pull of narrow-body production lines and wide-body upgrades on validation labor. Mature certification pathways help compress risk, positioning commercial aircraft as the anchor client group for the aviation testing services market. Business jet and rotorcraft segments supply steady yet flatter growth, typically emphasizing time-and-materials contracts tailored to lower serial production.

UAVs, however, command the steepest expansion slope at 6.5% CAGR as defense ministries and logistics operators explore heavy-payload drones and swarm concepts. Their rise introduces novel requirement matrices—flight-control redundancy, satellite-link latency resilience, and fully autonomous decision loops—that legacy rig layouts cannot fully address. Testing firms respond by integrating hardware-in-the-loop simulators with artificial-intelligence scenario generation, widening the overall aviation testing services market size through cross-fertilizing civil and defense technology portfolios.

By Service Type: Validation Services Lead Digital Transformation

Core validation suites encompass static load tests, system-integration labs, and environmental chambers, and held 56.76% of 2024 spending. These high-throughput assets represent a baseline entry into the aviation testing services market. Instrumentation calibration and certification underpin traceability to ISO 17025, while repair services sustain uptime, embedding providers deeper within customer operations cycles.

Test-as-a-service and managed offerings, leveraging cloud-hosted data dashboards and remote rig control, are forecasted for a 4.91% CAGR. Customers pay per test hour, converting capex to opex and widening access to advanced assets like hypersonic tunnels. This model raises utilization, allowing providers to amortize equipment faster and balloon the aviation testing services market size without parallel capital growth. Concurrently, consulting engagements covering data analytics and regulatory navigation capture margin as airframers steer through expanding cyber and sustainability rulesets.

By End User: OEM Leadership Faces Defense Acceleration

Airframe, avionics OEMs, and Tier-1 suppliers accounted for 56.46% of revenue in 2024 as integrated development cycles bundle testing into program budgets. Their captive facilities nonetheless subcontract peak workloads to independent labs, particularly for specialized electromagnetic-compatibility and high-strain-rate testing. MRO shops exploit outsourcing to focus on turnaround-time metrics, sending non-destructive evaluation and calibration tasks to external partners.

Defense agencies represent the speed lane, growing at a 3.95% CAGR as hypersonic weapons, directed-energy systems, and sixth-generation fighters stretch operating envelopes. Security-cleared laboratories that meet ITAR rules harvest high-margin contracts, although the lumpy nature of defense budgeting injects volatility. Airlines experiment with in-house data analytics validation for predictive maintenance, yet still rely on accredited labs for airworthiness sign-off, knitting them into a multi-tier demand web that sustains holistic expansion of the aviation testing services industry.

Geography Analysis

North America commanded 41.43% of 2024 revenue, anchored by the FAA’s regulatory gravity and clustered OEM ecosystems in Washington State, Kansas, Quebec, and Arizona. Investments in AI-enabled cybersecurity testbeds and the FAA’s foreign-repair-station drug-testing rule reinforce the region’s benchmark status. Canada supplements capacity through Montréal’s composites and icing tunnels, while Mexico’s low-cost MRO hubs import portable non-destructive rigs, enlarging the continental aviation testing services market.

Asia-Pacific is projected to scale at a 4.28% CAGR to 2030, driven by China’s C919 follow-on programs, widebody ambitions, and India’s Production-Linked Incentive scheme for aerospace manufacturing. Indigenous airframers contract foreign labs to qualify for composite wings and avionics, yet domestic facilities are under construction, especially around Shanghai and Bengaluru. Japan’s material-science prowess spills into fatigue-resistant alloys, necessitating local environmental and corrosion chambers. Australia’s Loyal Wingman UAV and South Korea’s KF-21 fighter further diversify demand, positioning the Asia-Pacific as the locomotive of the incremental aviation testing services market size.

Europe sustains a sophisticated network of environmental, acoustics, and sustainable-fuel labs under EASA oversight. Toulouse, Hamburg, and Bristol anchor full-scale structural rigs, while Nordic nations specialize in cold-soak and icing certification. The EU’s sustainable aviation fuel mandate generates new sample-integrity, calorimetry, and lifecycle-emissions testing streams. Middle East and Africa remain nascent but receive tailwinds from Gulf carrier fleet expansions and Saudi Arabia’s Vision 2030 aerospace cluster, prompting the build-out of electromagnetic-compatibility bays in Dubai and Riyadh. Latin America concentrates on regional-jet support and ethanol-blend fuel trials, seeding modest yet strategic opportunities for providers willing to deploy mobile labs.

Competitive Landscape

The aviation testing services market exhibits moderate fragmentation. Tier-1 system integrators such as Collins Aerospace and Honeywell deploy vertically integrated labs that span prototype to in-service monitoring, capturing synergies across product lines. Independent specialists, including Astronics and Marvin Test Solutions, carve niches in avionics and PXI-based automated-test-equipment, prompting OEMs to outsource peak volumes and specialized tasks. Element Materials Technology and NTS acquire boutique labs for structural and environmental work to gain geography and accreditation scale, signaling an industry consolidation wave aimed at amortizing million-dollar rigs.

Technology differentiation drives competitive positioning. Providers that embed digital twins of entire flight-control chains cut iteration loops by simulating load cases in the cloud and pushing condensed physical tests to rigs, slashing schedules by up to 30%. AI-powered anomaly detection within data lakes now flags test-article deviation in near real time, improving first-pass yield and cementing long-term contracts. Cyber-resilience emerges as a blue-water opportunity; players with in-house penetration-testing teams secure avionics contracts as connected cockpits proliferate.

Partnership strategies multiply. Wisk Aero’s purchase of Verocel sealed autonomous-software verification competence, indicating that integrated compliance portfolios will become table stakes. Hypersonic development triggers alliances between traditional aero labs and defense primes, pairing high-enthalpy tunnels with classified analytics cells. Sustainable fuel trials attract cross-value-chain consortia including energy majors, engine OEMs, and test labs to share cost and intellectual property, broadening the competitive canvas while elevating the aviation testing services market brand to a strategic enabler of aviation’s decarbonization targets.

Aviation Testing Services Industry Leaders

Keysight Technologies, Inc.

Marvin Test Solutions, Inc.

Astronics Corporation

Rohde & Schwarz GmbH & Co. KG

VIAVI Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AvionTEq showcased avionics test equipment and calibration services at MRO Americas to address heightened fleet maintenance workloads.

- February 2025: Safran Data Systems Inc. (DSI) secured a contract with Bell Textron to provide flight testing solutions and antennas for the US Army's Future Long Range Assault Aircraft (FLRAA) program.

- January 2025: Turbotech, Safran, and Air Liquide completed liquid-hydrogen gas-turbine ground tests under the BeautHyFuel project, creating new cryogenic validation needs.

Global Aviation Testing Services Market Report Scope

| Material Testing |

| Fuel Testing |

| Environmental Testing |

| Structural/Component Testing |

| Avionics/Flight and Electronics Testing |

| Propulsion System Testing |

| Other Testing Types |

| Commercial Aviation |

| Business and General Aviation |

| Military Aviation |

| Unmanned Aerial Vehicles (UAVs) |

| Urban Air Mobility (UAM)/eVTOL |

| Testing and Validation |

| Calibration and Certification |

| Maintenance and Repair |

| Consulting and Training |

| Test-as-a-Service/Managed Services |

| Avionics OEMs and Tier-1 Suppliers |

| MRO Providers |

| Airlines/Operators |

| Defense Agencies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Testing Type | Material Testing | ||

| Fuel Testing | |||

| Environmental Testing | |||

| Structural/Component Testing | |||

| Avionics/Flight and Electronics Testing | |||

| Propulsion System Testing | |||

| Other Testing Types | |||

| By Platform | Commercial Aviation | ||

| Business and General Aviation | |||

| Military Aviation | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Urban Air Mobility (UAM)/eVTOL | |||

| By Service Type | Testing and Validation | ||

| Calibration and Certification | |||

| Maintenance and Repair | |||

| Consulting and Training | |||

| Test-as-a-Service/Managed Services | |||

| By End User | Avionics OEMs and Tier-1 Suppliers | ||

| MRO Providers | |||

| Airlines/Operators | |||

| Defense Agencies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the aviation testing services market in 2025?

The aviation testing services market size stands at USD 3.58 billion in 2025 with a projected value of USD 4.21 billion by 2030, advancing at a 3.28% CAGR.

Which testing type generates the most revenue?

Structural and component testing accounts for 39.45% of 2024 revenue, remaining the largest contributor because of aging fleets and composite airframe proliferation.

What is the fastest-growing segment by platform?

UAVs recorded the highest growth at a 6.50% CAGR through 2030 as defense and logistics operators expand autonomous capabilities.

Why are avionics tests rising faster than structural tests?

Cyber-security mandates, software-defined avionics, and AI flight-control modules require new verification methods, making avionics and electronics the fastest-growing testing type at 4.29% CAGR.

Which region will add the most new testing capacity?

Asia-Pacific is forecasted for the quickest expansion, driven by Chinese and Indian aircraft programs plus regional defense projects, growing at 4.28% CAGR to 2030.

What business model is gaining popularity among small operators?

Test-as-a-service, which offers pay-per-use access to high-value rigs and cloud analytics, is advancing at a 4.91% CAGR, democratizing sophisticated validation capabilities.

Page last updated on: