Aviation Augmented And Virtual Reality Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

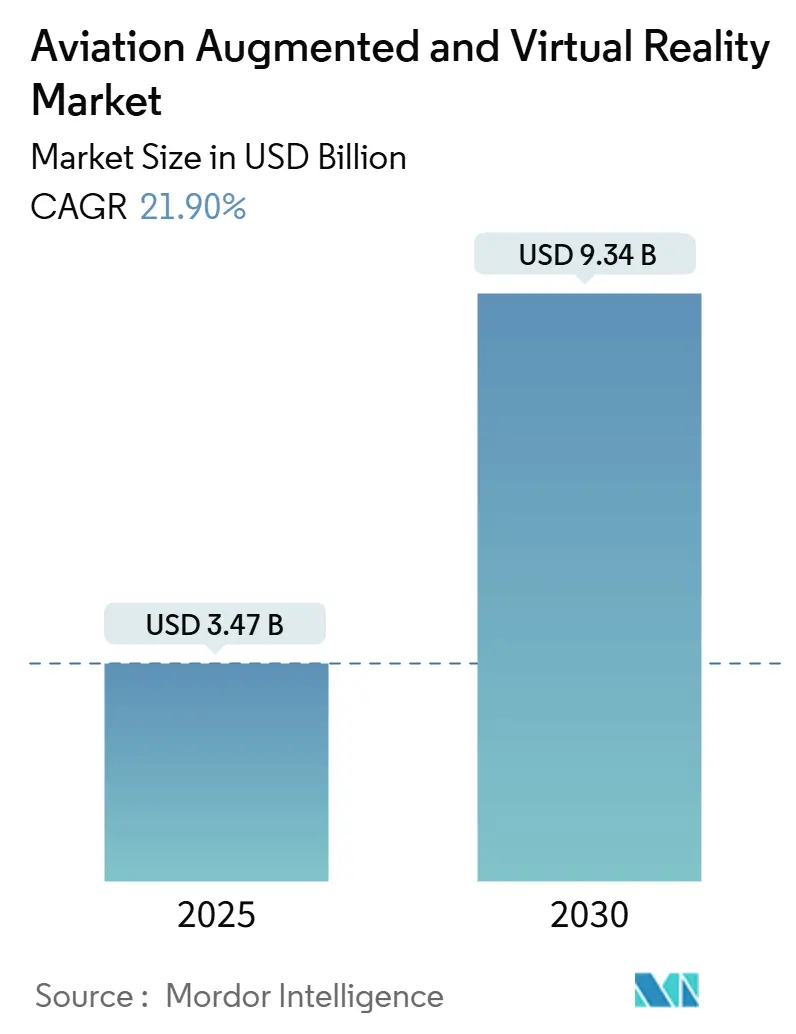

| Market Size (2025) | USD 3.47 Billion |

| Market Size (2030) | USD 9.34 Billion |

| Growth Rate (2025 - 2030) | 21.90% CAGR |

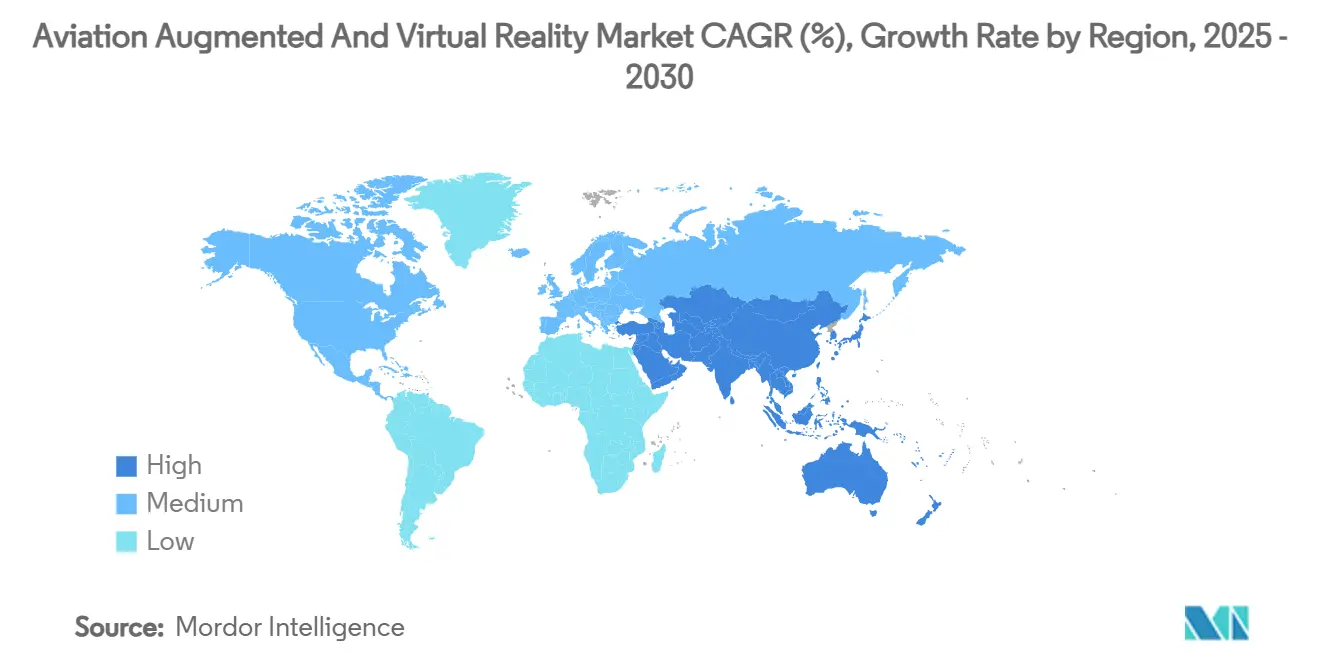

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Augmented And Virtual Reality Market Analysis by Mordor Intelligence

The aviation augmented and virtual reality (AR/VR) market size stood at USD 3.47 billion in 2025 and is projected to reach USD 9.34 billion by 2030, reflecting a 21.90% CAGR. Robust demand for immersive pilot-training solutions, rising regulatory acceptance of extended-reality simulators, and mixed-reality use cases in maintenance and cabin-crew instruction are accelerating adoption. Hardware prices are declining, 5G connectivity at airports is lacking, and airline efforts to differentiate in-flight entertainment further expand the addressable base. At the same time, high upfront headset costs and human-factor concerns such as simulator sickness temper near-term penetration but are expected to ease as technology fidelity improves. The competitive field remains moderately fragmented, with aerospace OEMs partnering with technology giants and specialist start-ups to address aviation-specific certification requirements.

Key Report Takeaways

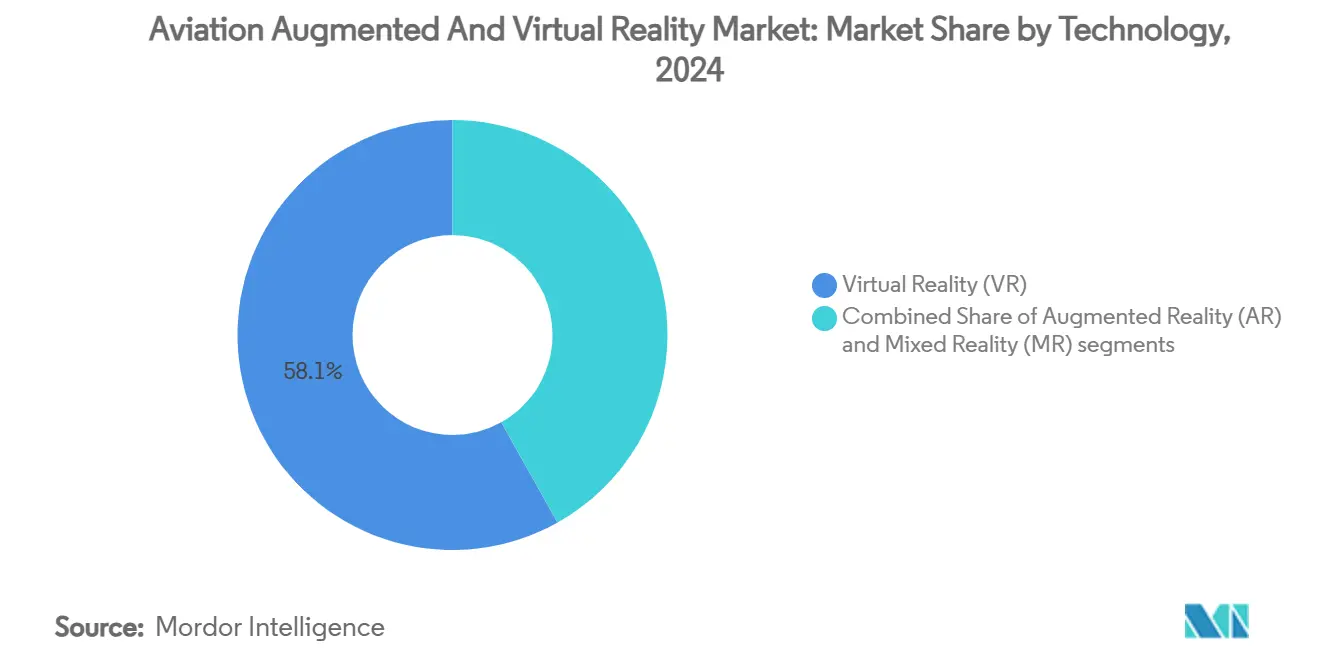

- By technology, virtual reality led 58.12% of the aviation AR/VR market share in 2024, while mixed reality is projected to grow at 22.10% CAGR to 2030.

- By component, hardware accounted for a 47.25% share of the aviation AR/VR market size in 2024, whereas services are forecast to expand at a 23.32% CAGR through 2030.

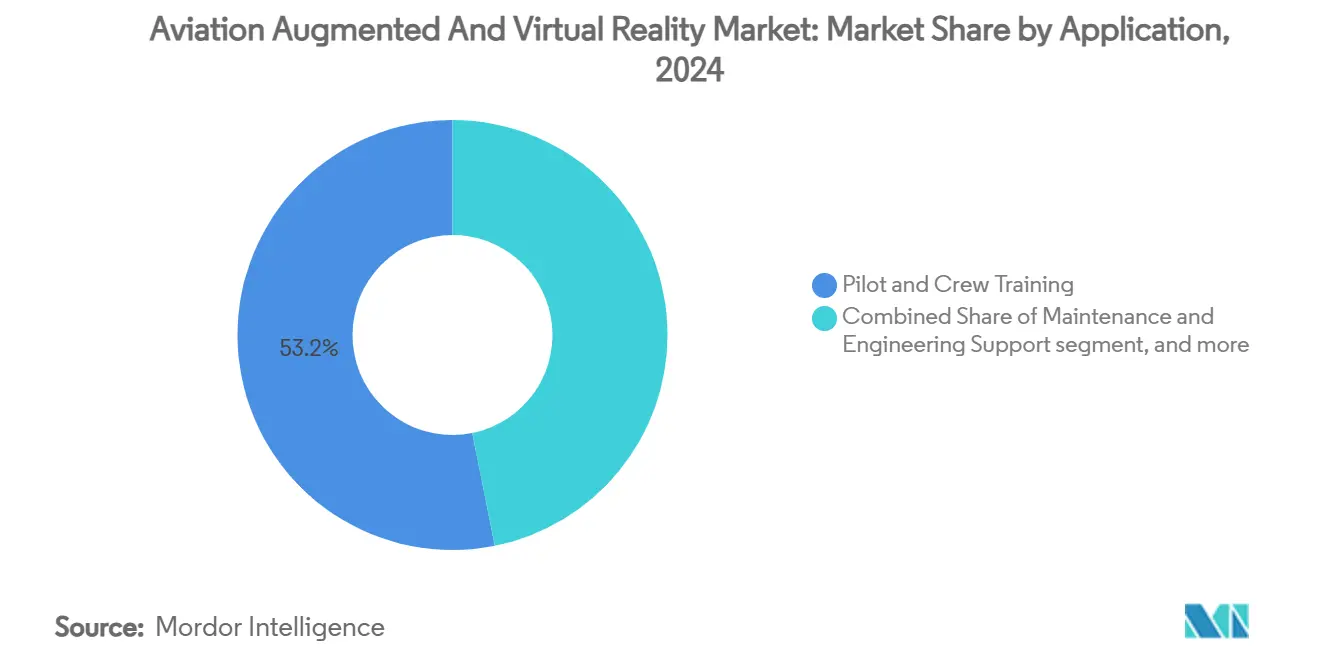

- By application, pilot and crew training commanded a 53.15% share of the aviation AR/VR market size in 2024, and in-flight passenger entertainment is projected to advance at a 22.13% CAGR through 2030.

- By end-user, airlines held 49.18% of the aviation AR/VR market share in 2024, while airport authorities were projected to have the highest CAGR of 23.25% from 2024 to 2030.

- By geography, North America led with a 39.19% share in 2024; the Asia Pacific region is expected to exhibit the fastest growth, with a 24.22% CAGR between 2025 and 2030.

Global Aviation Augmented And Virtual Reality Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust demand for immersive pilot-training solutions | +6.2% | Global; North America, Asia Pacific high focus | Medium term (2–4 years) |

| VR-enabled maintenance cost-reduction mandates by Original Equipment Manufacturers (OEMs) | +4.8% | Europe, North America | Long term (≥ 4 years) |

| Regulatory acceptance of extended reality simulators for recurrent training | +5.1% | North America, Europe | Short term (≤ 2 years) |

| Expansion of 6-DoF cabin-crew safety drills | +2.3% | Global; premium carriers early adopters | Medium term (2–4 years) |

| Edge-based AR for real-time MRO documentation | +3.2% | Developed markets worldwide | Long term (≥ 4 years) |

| Metaverse-style collaborative aircraft-design reviews | +1.8% | North America, Europe expanding to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Demand for Immersive Pilot-Training Solutions

The aviation industry is adopting AR and VR technologies for pilot training to reduce costs and eliminate risks. Boeing will require 2.4 million new aviation professionals by 2044, which will strain existing simulator capacity.[1]Boeing, “Global Demand for 2.4 Million Aviation Professionals,” boeing.com Virtual reality systems can reduce training costs by up to 40% by eliminating aircraft fuel and maintenance expenses. CAE’s Apple Vision Pro application shortens preparation time by 25%, and the US Air Force models annual savings of USD 350 million through VR adoption.[2]CAE, “Immersive Pilot Training on Apple Vision Pro,” cae.com Airlines such as Alaska Airlines validated full-motion VR 737 simulators to shrink classroom hours and facility footprints. These technologies create simulated cockpits and three-dimensional environments that provide realistic, scenario-based training, eliminating the need for fuel or airspace. Airlines and military operators are implementing AR/VR solutions to improve pilot preparedness while decreasing training expenses.

VR-Enabled Maintenance Cost-Reduction Mandates by OEMs

Aircraft manufacturers are increasingly utilizing VR for maintenance training to lower lifecycle costs and reduce aircraft downtime. VR enables technicians to practice complex procedures in simulated environments, thereby improving accuracy and safety without requiring physical access to an aircraft. Maintenance accounts for 10–15% of an airline's operating expenses, motivating OEM requirements for AR-based procedures. Boeing's ATOM trials improved installation speed by 30% on C-17 aircraft. Airbus's mixed-reality deployments reduced design validation time by 80% and accelerated assembly by 30% through the integration of Microsoft HoloLens.[3]Microsoft, “Airbus Mixed Reality Integration,” microsoft.com Mandate-driven programs embed AR/VR clauses in long-term support contracts, making compliance a key purchasing criterion. This approach enables airlines to minimize maintenance errors, implement consistent protocols worldwide, and train technicians more efficiently. The adoption of VR training by manufacturers supports digital transformation initiatives, improves operational efficiency, reduces costs, and meets regulatory requirements.

Regulatory Acceptance of Extended-Reality Simulators

Aviation regulatory authorities worldwide now accept extended-reality (XR) simulators, including AR and VR platforms, as certified training tools for pilots and crew members. This regulatory recognition allows operators to substitute traditional flight training hours with XR-based simulations. EASA special conditions for head-mounted displays and FAA performance-based Part 60 updates validate XR devices for official training time. Varjo secured the first EASA-qualified mixed-reality simulator, setting benchmarks for fidelity in terms of latency and resolution. New powered-lift rules covering eVTOL aircraft further favor XR methods as flight envelopes remain fluid. The approval has increased XR adoption in commercial and military aviation sectors, providing standardized training solutions that reduce costs, enhance safety, and enable virtual assessment of procedures under regulatory supervision.

Expansion of 6-DoF Cabin-Crew Safety Drills

Airlines are enhancing their training programs by implementing advanced six-degrees-of-freedom (6-DoF) cabin crew safety simulations. These simulations use motion platforms and XR environments to create precise virtual aircraft cabins where crew members practice emergency procedures, including evacuation, fire response, and decompression scenarios. Lufthansa Aviation Training completes 20,000 VR sessions yearly, mixing Apple Vision Pro scenarios with dynamic motion platforms. Carriers report 40% confidence gains in emergency response and 25% quicker certification cycles. IATA RampVR tools, adopted during the pandemic, extend the same model to ramp workers and baggage teams. Realistic training environments enhance emergency response times, team coordination, and critical decision-making capabilities. This virtual approach reduces the need for physical aircraft mockups, enabling airlines to provide standardized training across multiple locations cost-effectively.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront hardware capital expenditure | −3.8% | Global; small operators affected most | Short term (≤ 2 years) |

| Human-factor issues: simulator sickness and eye fatigue | −2.1% | Global; intensive programs impacted | Medium term (2–4 years) |

| Cybersecurity exposure of connected headsets | −1.9% | Global; defense users high concern | Long term (≥ 4 years) |

| Limited content standardisation across fleets | −2.7% | Global; multi-fleet airlines hardest hit | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware Capital Expenditure

The substantial initial investment required for AR/VR equipment, including headsets, motion platforms, and spatial tracking systems, remains a significant barrier to adoption in aviation training. Airlines and training centers face budget constraints that make it challenging to justify large capital expenditures, despite the potential for long-term returns on investment. Enterprise-grade headsets range from USD 3,000 to USD 5,000, while full installations exceed USD 50,000, and bespoke AR software can cost over USD 250,000.[4]DesignRush, “Augmented Reality Pricing,” designrush.com Smaller regional carriers lack comparable capital reserves, delaying rollouts despite clear ROI. These cost constraints particularly affect small airlines and operators in emerging markets, limiting the widespread implementation of immersive training systems across the aviation industry.

Human-Factor Issues: Simulator Sickness and Eye Fatigue

Despite technological improvements, AR/VR systems face physiological challenges, including simulator sickness, eye strain, and cognitive overload. Users experience disorientation and nausea during extended headset use, particularly in motion-intensive aviation simulations. More than 50% of trainees report nausea or visual disturbance during early VR sessions, capping exposure windows to roughly 30 minutes. High-fidelity optics and adaptive motion algorithms continue to mitigate symptoms, yet regulators maintain strict monitoring. These physical limitations affect training quality, reduce practice time, and necessitate additional adjustment periods, thereby impacting the adoption of time-critical aviation training. Resolving these physiological issues remains essential for user well-being and effective learning outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Mixed Reality Gains Momentum

Virtual reality retained 58.12% of 2024 revenue, underscoring its established regulatory footing and pilot-training pedigree. The aviation AR/VR market size attached to mixed reality is projected to expand at a 22.10% CAGR as operators seek context-aware overlays for maintenance and live-flight support. Two-way data streams between aircraft sensors and headsets enable in situ troubleshooting, while sunlight-readable waveguide optics address prior usability gaps. Early mixed-reality adopters demonstrate 30% efficiency rises in wing assembly inspections, validating the segment’s operational value. Hardware makers align road maps with aviation certifications. Varjo’s XR-4 headset now ships with flight-deck-specific lenses, and Distance Technologies develops windshield-integrated holographic displays. Regulatory milestones, including the first EASA-qualified mixed-reality simulator, reduce perceived certification hurdles and foster wider acceptance among airline pilots. The result is an ecosystem shift where pure-play VR incumbents partner with AR specialists to offer blended solutions.

By Component: Services Transform Economics

Hardware represented 47.25% of 2024 revenue, reflecting investment cycles in headsets and motion platforms. Yet services show the steepest 23.32% CAGR as subscription-based training, content refresh, and cloud analytics gain favor. Airlines prefer operational-expenditure models that spread costs and keep curricula evergreen. CAE’s global network exemplifies the pivot: the firm opened new centers in Las Vegas and Savannah to deliver headset-agnostic courseware on demand.[5]Aerospace and Defense Review, “Future of Aviation Training,” aerospacedefensereview.com Vendors bundle headset rentals, software updates, and performance analytics into multi-year agreements, limiting asset obsolescence. Cloud-native authoring tools enable instructors to rapidly tailor lesson variants, accelerating the addition of fleet-type aircraft after certification. The convergence of 5G and edge computing further shifts value from hardware to managed services, underpinning the durability of recurring revenue.

By Application: Entertainment Redefines In-Cabin Experience

Pilot and crew training held 53.15% of 2024 spending owing to mandated proficiency standards and established ROI. However, in-flight passenger entertainment is growing at a 22.13% CAGR as carriers seek to differentiate their premium cabins. After positive customer feedback, Lufthansa and Meta expanded Quest 3 trials to additional routes, signaling mainstream acceptance of headset-based IFE. Maintenance crews leverage AR overlays to cut wiring-harness installation errors, and cabin-crew drills harness 6-DoF platforms for realistic fire-suppression practice. Airports explore AR way-finding and baggage logistics, and MRO facilities integrate headset-guided torque verification. Each use case feeds a virtuous cycle that broadens platform utilization beyond training hours.

By End-User: Airport Authorities Accelerate Digitisation

Airlines dominated 49.18% of 2024 demand, justified by direct safety, cost, and passenger-experience gains. Airport authorities, though, are on a 23.25% CAGR trajectory, using digital twins and AR dashboards to optimize gate allocation and crowd flow. Hamad International Airport’s immersive control center demonstrates how headset-equipped staff can visualize live passenger densities and asset status, thereby improving response times. MRO providers embed AR in electronic task cards to meet regulatory traceability requirements, and aircraft OEMs integrate headset-guided customer demonstrations during sales campaigns. Defense academies continue to scale VR syllabi for rotary-wing and powered-lift platforms, supported by recent FAA powered-lift rules that call for new curricula formats.

Geography Analysis

North America contributed 39.19% of 2024 revenue, driven by large defense budgets, mature simulator infrastructure, and proactive FAA guidance that legitimizes mixed-reality training. The region's AR/VR market size benefits from partnerships, such as those between Boeing and Microsoft, which have demonstrated double-digit reductions in aircraft downtime through HoloLens maintenance programs. Venture capital supports emerging headset firms, and unionised labor costs reinforce technology adoption to reduce classroom hours.

The Asia Pacific region is projected to grow at a 24.22% CAGR, reflecting rapid fleet expansion and the region's anticipated need for 19,500 new aircraft by 2043. China's aviation services market is projected to grow from USD 23 billion in 2024 to USD 61 billion by 2043, with maintenance services expected to account for the largest share. Airports like Beijing Daxing deploy 5G-enabled AR facial recognition gates that cut boarding times, signaling ecosystem readiness for immersive workflows.

Europe sustains balanced growth underpinned by EASA's clear special-condition framework and Airbus's mixed-reality production lines, which report 80% cuts in design-validation time. Lufthansa's 20,000 VR sessions exemplify the maturity of airline programs, which are conducted annually, while OEM-supplier clusters in France and Germany test metaverse design reviews. Middle East and Africa adoption remains nascent but is accelerated by hub modernisation; Hamad International Airport's digital twin proves early ROI and attracts regional peers.

Competitive Landscape

The aviation AR/VR industry exhibits moderate fragmentation. Top aerospace incumbents, such as The Boeing Company, Airbus SE, and CAE Inc., leverage deep domain expertise, while technology majors, including Microsoft Corporation and Magic Leap, Inc., supply advanced optics and cloud stacks. Niche players Varjo Technologies Oy, SimX, Inc., and Vrgineers, Inc. concentrate on aviation-specific headsets and simulators. Partnerships dominate go-to-market strategies; for example, CAE Inc. teams with advanced air mobility OEMs for eVTOL training, and The Boeing Company collaborates with Microsoft on mixed-reality maintenance.

Competition is increasingly centered on regulatory credentials, mitigation of simulator sickness, and the openness of content pipelines, rather than basic headset specs. White-space opportunities persist in airport ground-handling automation and fleet-wide content standardisation. Intellectual-property depth and certification track records are key entry barriers that deter new pure-play entrants.

Aviation Augmented And Virtual Reality Industry Leaders

CAE Inc.

The Boeing Company

Airbus SE

Microsoft Corporation

Honeywell International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: At APEX FTE EMEA, airlines were encouraged to adopt XR and AI to modernize training and the passenger experience, continuing the rollout at FTE Global.

- April 2025: Following successful business-class trials, Lufthansa and Meta expanded the Quest 3 in-flight entertainment program.

- January 2025: CAE and Vertical Aerospace formed a global eVTOL pilot-training alliance using mixed-reality simulators.

- December 2024: Vertex Solutions, Varjo, and Aechelon won an FAA contract to redefine VR flight-simulation standards.

- October 2024: CAE launched the first Apple Vision Pro immersive pilot-training application.

Global Aviation Augmented And Virtual Reality Market Report Scope

| Augmented Reality (AR) |

| Virtual Reality (VR) |

| Mixed Reality (MR) |

| Hardware |

| Software |

| Services |

| Pilot and Crew Training |

| Maintenance and Engineering Support |

| Cabin-Crew and Safety Drills |

| In-flight Passenger Entertainment |

| Airport Operations and Ground Handling |

| Airlines |

| MRO Providers |

| Aircraft OEMs |

| Airport Authorities |

| Defence Academies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Technology | Augmented Reality (AR) | ||

| Virtual Reality (VR) | |||

| Mixed Reality (MR) | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Application | Pilot and Crew Training | ||

| Maintenance and Engineering Support | |||

| Cabin-Crew and Safety Drills | |||

| In-flight Passenger Entertainment | |||

| Airport Operations and Ground Handling | |||

| By End-User | Airlines | ||

| MRO Providers | |||

| Aircraft OEMs | |||

| Airport Authorities | |||

| Defence Academies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aviation augmented and virtual reality market in 2025?

The aviation augmented and virtual reality (AR/VR) market size is USD 3.47 billion in 2025.

Which technology segment is growing fastest?

Mixed reality (MR) is projected to expand at a 22.10% CAGR through 2030 due to its dual virtual–physical overlay benefits.

What drives airline investment in AR/VR training?

Airlines aim to cut training costs up to 40% and address pilot shortages of 2.4 million professionals forecast by 2044.

Why are airport authorities adopting AR/VR?

They use digital twins and AR dashboards to manage passenger flow and operations, supporting a 23.25% CAGR for the segment.

What is the main restraint to wider adoption?

High upfront hardware and content costs reduce near-term affordability for smaller operators.

Which region will grow fastest by 2030?

Asia-Pacific leads with a 24.22% CAGR, driven by fleet expansion and large-scale infrastructure investment.

Page last updated on: