Flight Management Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

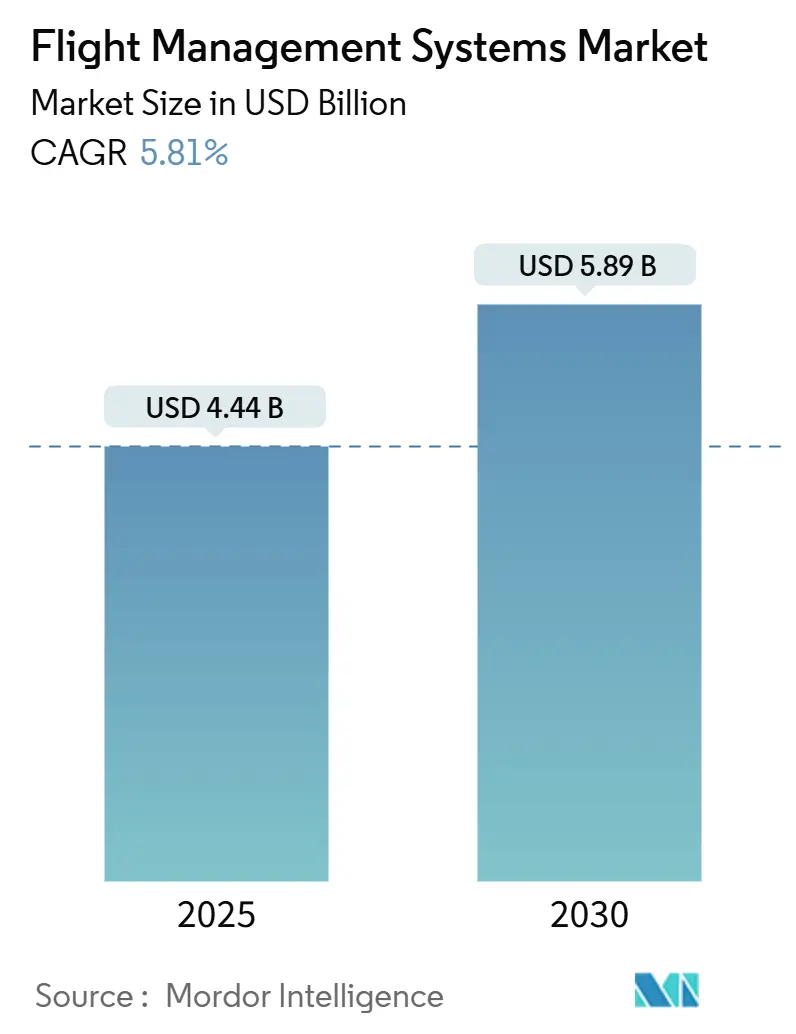

| Market Size (2025) | USD 4.44 Billion |

| Market Size (2030) | USD 5.89 Billion |

| Growth Rate (2025 - 2030) | 5.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flight Management Systems Market Analysis by Mordor Intelligence

The flight management systems market size stands at USD 4.44 billion in 2025 and is forecasted to reach USD 5.89 billion by 2030, expanding at a 5.81% CAGR. Rising single-aisle aircraft production, mandatory navigation performance requirements, and the integration of AI-enabled decision-support tools collectively propel growth in every significant aviation segment. Airlines deploy advanced trajectory-optimization algorithms to cut fuel burn, while OEMs embed smart flight decks at the factory to streamline certification cycles. Software-defined architectures open recurring revenue streams for data analytics providers, and hardware suppliers capitalize on multi-redundant computing suites demanded by safety regulations. Competitive intensity is accelerating as incumbents forge semiconductor and cloud partnerships to compress development timelines and protect aftermarket positions.

Key Report Takeaways

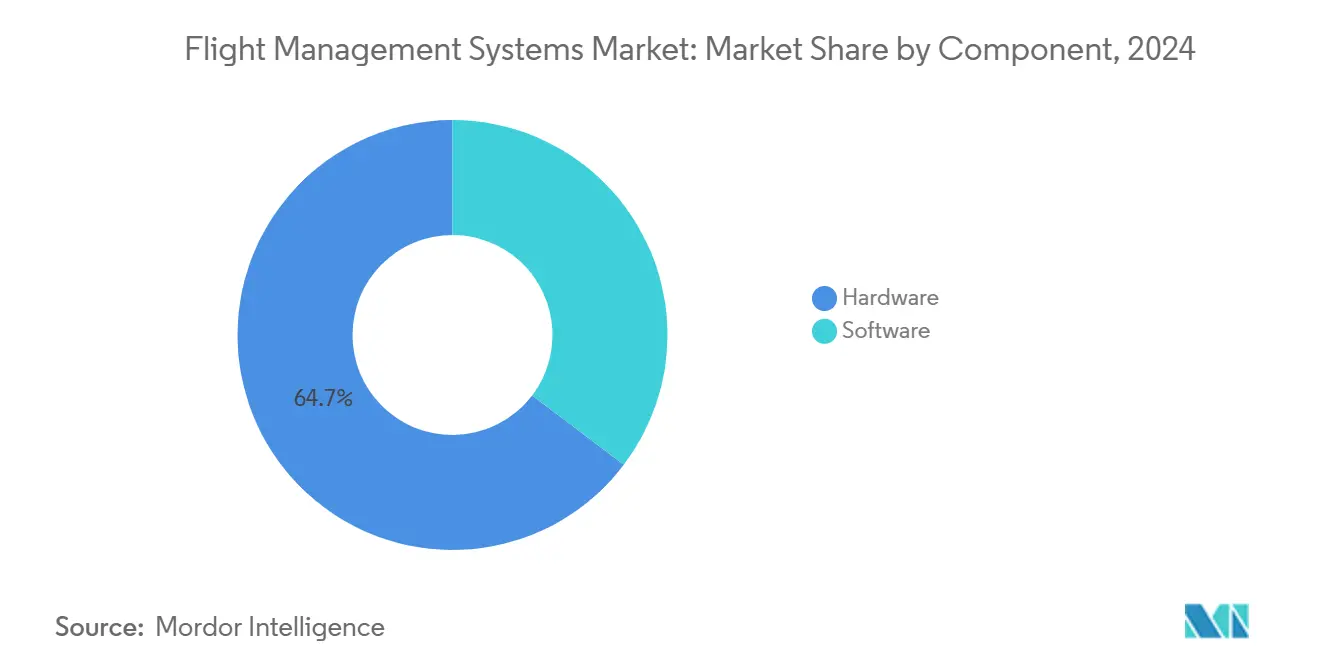

- By component, hardware led with 64.68% of the flight management systems market share in 2024; software is projected to expand at a 7.21% CAGR through 2030.

- By aircraft type, commercial aviation commanded 76.52% of the flight management systems market in 2024, and urban air mobility is advancing at a 10.01% CAGR to 2030.

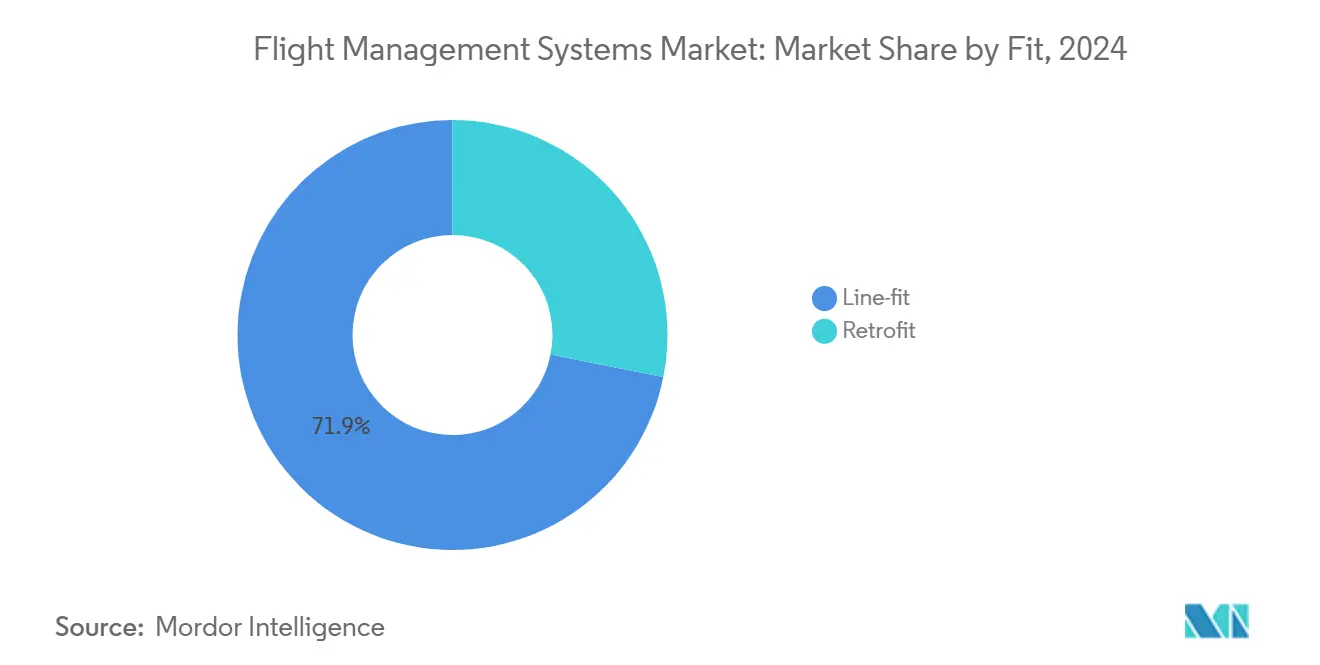

- By fit, line-fit installations captured 71.87% revenue share in 2024, whereas retrofit demand is growing at a 6.21% CAGR through 2030.

- By installation type, dual and triple-redundant suites held a 56.65% share of the flight management systems market size in 2024 and are rising at a 6.42% CAGR to 2030.

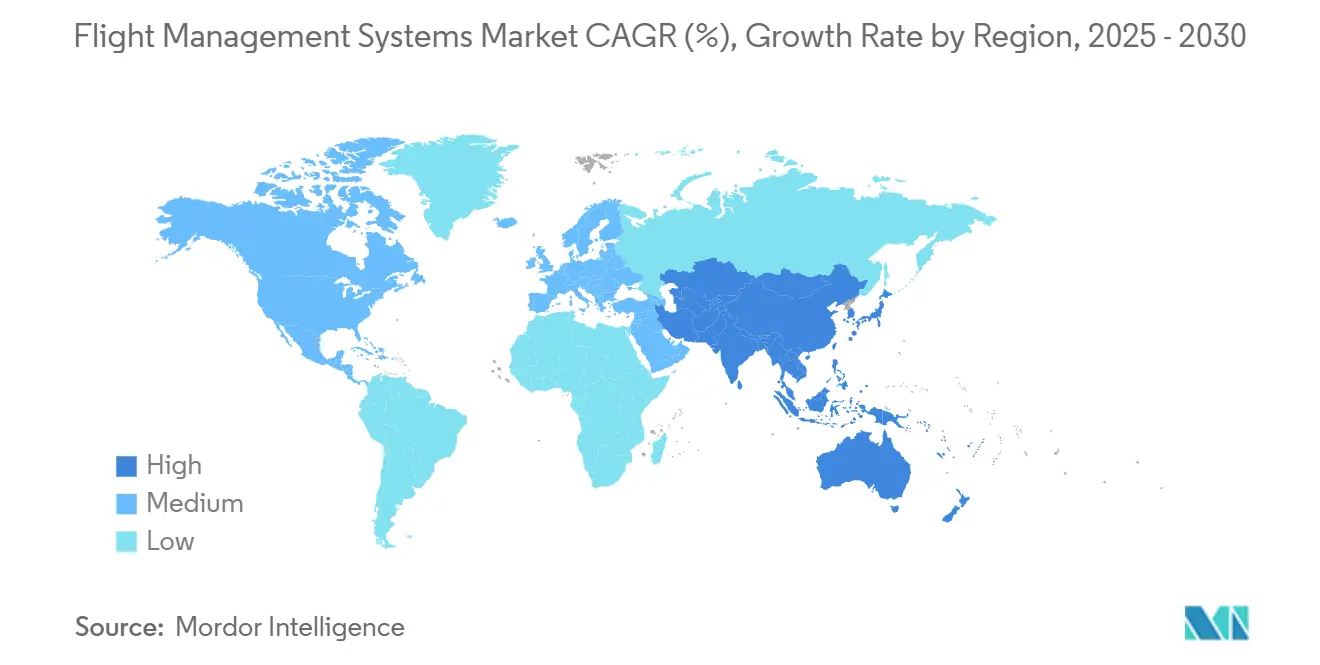

- By region, North America dominated with a 34.80% share in 2024; Asia-Pacific records the highest projected CAGR at 7.25% through 2030.

Global Flight Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising production rates of single-aisle commercial aircraft | +1.2% | North America, Europe, expanding Asia-Pacific | Medium term (2-4 years) |

| Increasing airline focus on fuel efficiency and operating cost reduction | +1.0% | Asia-Pacific, North America, global | Long term (≥ 4 years) |

| Mandatory compliance with advanced navigation performance standards | +0.9% | Europe, North America | Short term (≤ 2 years) |

| Expanding adoption of connected aircraft and real-time analytics | +0.8% | North America, Europe | Medium term (2-4 years) |

| Advancements in AI-enabled cockpit decision-support systems | +0.7% | Global, led by North America | Long term (≥ 4 years) |

| Integration of FMS with next-generation air traffic management platforms | +0.6% | Europe, North America, gradual Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Production Rates of Single-Aisle Commercial Aircraft

Boeing’s plan to lift B737 MAX output from 38 to 42 jets per month and possibly 47 by late 2025 directly boosts factory demand for integrated FMS suites, as each new airframe ships with dual-redundant computers and high-resolution control displays.[1]Liam Dawson, “Boeing prepares for 737 production rate hikes this year,” Flightglobal.com Airbus delivered 766 aircraft in 2024, underscoring the production race that locks in large multiyear orders for FMS vendors. With the global backlog stretching 14 years at current delivery rates, hardware providers secure a stable pipeline, while software suppliers embed optimization algorithms tuned to each airframe variant. Tighter assembly cadences favor line-fit over retrofit work, reinforcing OEM relationships for Thales, Honeywell, and Collins.

Increasing Airline Focus on Fuel Efficiency and Operating Cost Reduction

Virgin Atlantic’s Flight100 saved 95 tons of CO2 using 100% sustainable aviation fuel, illustrating how carriers lean on advanced FMS to unlock measurable burn reductions.[2]Virgin Atlantic, “Flight100 saved 95 t of CO₂,” corporate.virginatlantic.com Thales PureFlyt continually recalculates optimum climb and descent profiles, blending real-time weather and ATC data to trim block times. Honeywell Forge analytics cuts up to 50% of unscheduled disruptions, proving that modern FMS value extends from cockpit to maintenance control. Airlines treat such gains as core to net-zero roadmaps, channeling capital toward software upgrades that pay back in under two years.

Mandatory Compliance with Advanced Navigation Performance Standards

The FAA’s AC 90-101A mandates strict RNP AR criteria, compelling US operators to upgrade navigation computers, databases, and crew procedures. Europe requires RNAV 1 adherence on all SIDs and STARs by 2030, fixing a definitive retrofit timeline for legacy fleets. The 2025 ICAO autonomous distress-tracking rule for heavy aircraft further integrates positioning, communication, and surveillance within unified FMS stacks. Providers with proven certification backlogs enjoy a compliance premium as operators avoid the risks of emerging suppliers.

Expanding Adoption of Connected Aircraft and Real-Time Analytics

Thales PureFlyt streams live data to cloud engines that recalculate lateral and vertical profiles thousands of times per flight without compromising cyber isolation. Boeing’s Airplane Health Management 2.0 applies sensor feeds to condition-based maintenance approved by the FAA, slashing heavy-check downtime. Rolls-Royce IntelligentEngine pushes engine analytics into the cockpit to suggest fuel-optimum speed changes, reinforcing the FMS as a central processing node. These use cases shift competitive advantage toward suppliers marrying avionics pedigree with cloud-software agility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged aircraft delivery backlogs affecting new system installations | -0.8% | North America, Europe, global | Medium term (2-4 years) |

| Delays in certification of cyber-secure avionics architectures | -0.6% | Europe, North America | Short term (≤ 2 years) |

| Shortages of application-specific integrated circuits for avionics systems | -0.5% | Asia-Pacific manufacturing hubs, global | Medium term (2-4 years) |

| High retrofit costs limiting adoption in older aircraft fleets | -0.4% | Emerging markets, global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prolonged Aircraft Delivery Backlogs Affecting New System Installations

With open orders equaling 14 years of current output, OEMs re-sequence production slots, delaying cockpit technology refresh cycles that depend on new airframes. Supply bottlenecks on CFM LEAP engines and certified semiconductors prolong narrowbody rollouts, forcing airlines to fly older jets longer and defer embedded FMS upgrades. Margins shrink as vendors pivot to piecemeal retrofits instead of high-volume factory lines.

Delays in Certification of Cyber-Secure Avionics Architectures

The FAA’s draft rule on electronic-system security obliges applicants to demonstrate system-wide threat mitigation, adding months to approval cycles and inflating program costs. EASA’s Part-IS imposes parallel audits for operators, MROs, and training bodies, complicating cross-border projects. FMS developers must allocate extra engineering resources, drawing capital away from product-line expansions targeted at Urban Air Mobility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Drives Integration Complexity

Hardware contributed 64.68% revenue in 2024, underscoring the continued demand for ruggedized flight-management computers, multi-slot control-display units, and high-luminance panels. The flight management systems market size for hardware reached USD 2.87 billion in 2024, benefiting from line-fit programs at Boeing and Airbus, where fully redundant processors are baseline equipment. Providers embed multicore safety-certified chips that enable complex RNP and GLS algorithms without weight penalties. Vendors also lock in multidecade aftermarket contracts covering spares and long-term performance-based logistics.

Software, though comprising a smaller share, is scaling at a 7.21% CAGR as airlines migrate to data-centric operations. Providers market open-architecture suites aligned with FACE 3.0 that let carriers integrate third-party fuel analytics or ADS-B apps rapidly.[3]GE Aerospace, “Flight Management Software meets FACE 3.0,” geaerospace.com Software revenue ties to subscription models for continuous navigation database and machine-learning updates, smoothing cyclic aircraft delivery exposure.

By Aircraft Type: Commercial Aviation Leads, Urban Mobility Emerges

Commercial aviation accounted for 76.52% of the flight management systems market size in 2024, anchored by narrowbody demand as carriers refresh fleets for fuel savings. Widebody programs adopt dual-FMS architectures capable of oceanic GLS approaches, and regional jets integrate compact touch-control units optimized for short segments. Military orders remain steady across tanker, trainer, and rotary-wing platforms that demand combat-proven triple-redundant logic and jam-resistant navigation.

Urban Air Mobility (UAM) shows the fastest trajectory at 10.01% CAGR through 2030. eVTOL developers collaborate with Honeywell Anthem to achieve catastrophic failure probabilities of 10-9 per flight hour, blending fly-by-wire, FMS, and health-monitoring on a single modular computer. This new segment incentivizes lightweight, cloud-connected stacks that auto-update landing-site databases and urban air-traffic corridors.

By Fit: Line-Fit Preference Reflects Integration Advantages

Line-fit deliveries covered 71.87% of shipments in 2024, supported by OEM emphasis on harmonized cockpit baselines that reduce pilot-training and maintenance variance. The flight management systems market share gain for line-fit reflects direct installation into the aircraft production sequence, allowing tight coupling with engine-performance models and flight-control laws. Forward integration guarantees the avionics suite meets the latest cybersecurity and data-integrity standards on the first flight.

Retrofit activity is building momentum at 6.21% CAGR as carriers extend airframe service lives beyond original economic limits. Programs such as the AeroNav upgrade for Citation light jets, priced under USD 400,000 installed, illustrate how targeted packages can yield 2% fuel-cycle savings within 18 months. Parts obsolescence relief and mandated ADS-B tracking sustain the retrofit pipeline for business aviation and older narrowbodies.

By Installation Type: Redundancy Requirements Drive Safety Standards

Dual- and triple-redundant configurations secured 56.65% revenue in 2024 and are expanding at 6.42% CAGR, reflecting the regulator's insistence that no single failure end an IFR flight. Airlines adopt cross-channel monitoring that automatically reverts to a backup computer without pilot action, while military transports equip tertiary units guarded inside armored bays for battle resilience. Predictive diagnostics housed within redundant networks isolate latent faults early, reducing nuisance messages.

Single-FMS architectures persist in light GA and turboprop categories where weight and acquisition cost dominate. Even here, software-partitioning enables virtual redundancy on a single board, foreshadowing future upgrades once certification frameworks evolve. AI-enabled cross-checking routines will let smaller aircraft climb to regional routes formerly reserved for twins, broadening the addressable base for suppliers.

Geography Analysis

North America retained a 34.80% share in 2024, buoyed by B737 MAX and B787 assembly lines, large defense budgets, and FAA rule-setting that steers global avionics specifications. United States operators pioneer connected-fleet programs that feed live telemetry into maintenance control, driving early adoption of software-rich FMS packages. Canada augments regional jet output through De Havilland and Bombardier service centers, while Mexico supplies wiring harnesses and PCB assemblies that lower unit costs for Tier-1 vendors.

Asia-Pacific is the fastest-growing territory, with a 7.25% CAGR to 2030. China's COMAC series spurs indigenized avionics sourcing, yet domestic airlines still procure certified Western FMS suites for international operations. India's airline traffic boom elongates narrowbody order books, and South Korea's plan for an additional 36 AH-64E Apaches injects high-spec military demand.[4]Army Recognition, “South Korea plans to acquire 36 AH-64E Apaches,” armyrecognition.com Regional MRO hubs in Singapore and Thailand upgrade aging widebodies to RNAV-1-ready status, amplifying retrofit sales.

Due to Airbus's final assembly lines and stringent EASA certification, Europe has a substantial scale, pushing the early adoption of cyber-secure architectures. Thales contracted to supply next-generation FMS for A320, A330, and A350 platforms entering service from 2026, embedding cloud-connected capabilities as a baseline. The region also hosts emergent quantum navigation trials, witBoeing's’s successful 4-hour GPS-free sortie offering strategic autonomy for transpolar flights.

Competitive Landscape

The flight management systems market shows moderate consolidation. Honeywell International Inc., Thales Group, RTX Corporation, and Garmin Ltd. collectively shipped 58% of units in 2024, leveraging legacy certification portfolios and broad MRO networks. Honeywell’s alliance with NXP supplies i.MX 8 processors that underpin the Anthem flight deck, fusing AI accelerators with touchscreen interfaces for eVTOL and business-jet programs. Thales pivots toward connected-fleet analytics, while Collins embeds predictive maintenance dashboards inside its Ascentia suite.

White-space opportunities appear in quantum navigation, urban air mobility, and cloud-deployed optimization engines. Boeing validated a six-axis quantum IMU on a four-hour flight in July 2025, proving resilience in GPS-denied zones and setting a new technology race. Start-ups such as FLIGHTKEYS attract venture funding by pitching dynamic flight-planning algorithms that dovetail with legacy FMS via open-data buses.

Strategic moves in 2025 include Honeywell acquiring Civitanavi for inertial navigation expertise and announcing a spin-off forming three focused entities, likely sharpening product roadmaps. Boeing’s divestiture of USD 10.55 billion in aviation-software assets signals renewed concentration on core assembly lines, shifting digital-service share to agile providers.

Flight Management Systems Industry Leaders

Honeywell International Inc.

Thales Group

RTX Corporation

Garmin Ltd.

GE Aerospace (General Electric Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SkyDrive completed its first flight using Thales's FlytRise flight control system, which is designed for urban air mobility operations. The FlytRise system enables safe eVTOL operations in urban environments and significantly develops aerial autonomy.

- May 2022: Airbus selected Thales Group to provide a new flight management system for its commercial airliners. Based on PureFlyt technology and customized for Airbus requirements, the system will be integrated into A320, A330, and A350 aircraft by late 2026.

Global Flight Management Systems Market Report Scope

| Hardware | Flight Management Computer (FMC) |

| Control Display Unit (CDU) | |

| Visual Display Unit (VDU) | |

| Software |

| Commercial Aircraft | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aircraft | Combat |

| Transport | |

| Special Mission | |

| Helicopters | |

| General Aviation | Business Jets |

| Piston and Turboprops | |

| Commercial Helicopters | |

| Unmanned Aerial Systems (UAS) | Civil and Commercial |

| Defense and Government | |

| Urban Air Mobility (UAM) |

| Line-fit |

| Retrofit |

| Single-FMS |

| Dual/Triple-Redundant FMS |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Hardware | Flight Management Computer (FMC) | |

| Control Display Unit (CDU) | |||

| Visual Display Unit (VDU) | |||

| Software | |||

| By Aircraft Type | Commercial Aircraft | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aircraft | Combat | ||

| Transport | |||

| Special Mission | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Piston and Turboprops | |||

| Commercial Helicopters | |||

| Unmanned Aerial Systems (UAS) | Civil and Commercial | ||

| Defense and Government | |||

| Urban Air Mobility (UAM) | |||

| By Fit | Line-fit | ||

| Retrofit | |||

| By Installation Type | Single-FMS | ||

| Dual/Triple-Redundant FMS | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the global flight management systems market in 2025?

The flight management systems market size is USD 4.44 billion in 2025 and is forecasted to reach USD 5.89 billion by 2030.

Which region is growing fastest for advanced flight-management adoption?

Asia-Pacific records a 7.25% CAGR through 2030 owing to expanding aircraft production and rising airline efficiency goals.

Why are airlines investing in new FMS software now?

Carriers target measurable fuel-burn and maintenance savings, with modern FMS delivering trajectory optimization and predictive analytics that lower operating costs.

What drives retrofit demand for existing aircraft?

Mandated RNP and ADS-B compliance, parts obsolescence, and fuel-efficiency upgrades compel operators to install new FMS suites mid-life.

Who are the leading FMS suppliers?

Honeywell, Thales, Collins Aerospace, and Garmin collectively shipped 58% of units in 2024, supported by broad certification track records and global service networks.

How does redundancy influence FMS architecture?

Dual- and triple-computer configurations dominate because regulators require fault-tolerant navigation; these setups seamlessly transfer control if a component fails.

Page last updated on: