Aviation Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

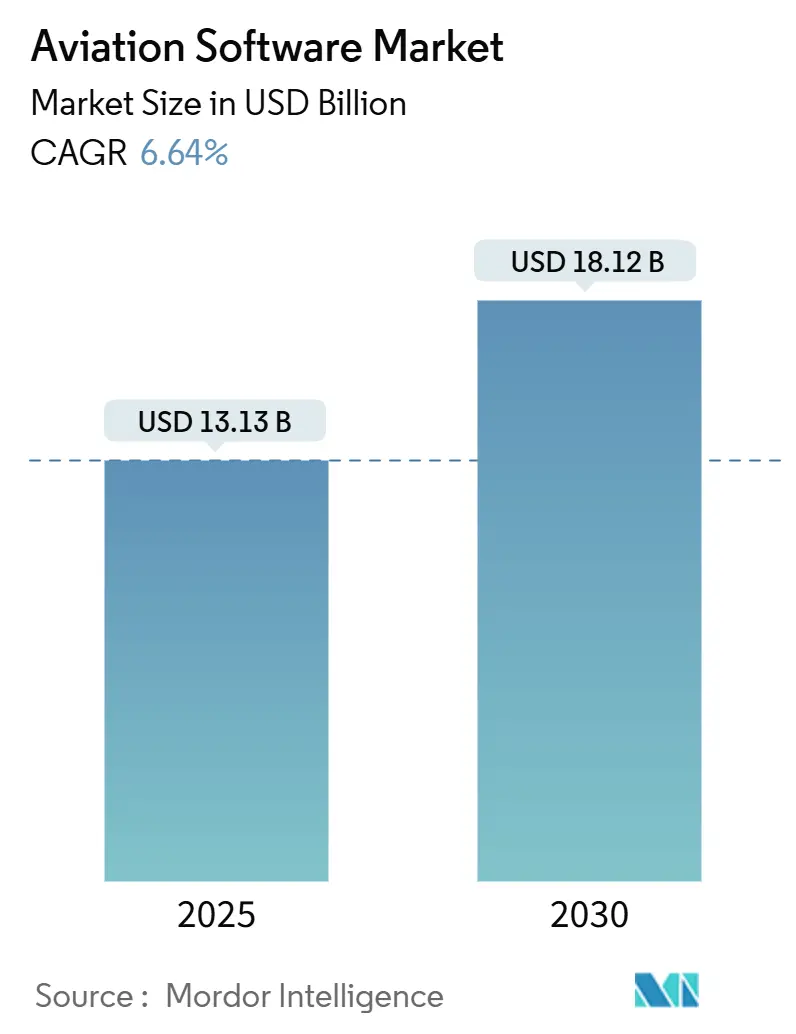

| Market Size (2025) | USD 13.13 Billion |

| Market Size (2030) | USD 18.12 Billion |

| Growth Rate (2025 - 2030) | 6.64% CAGR |

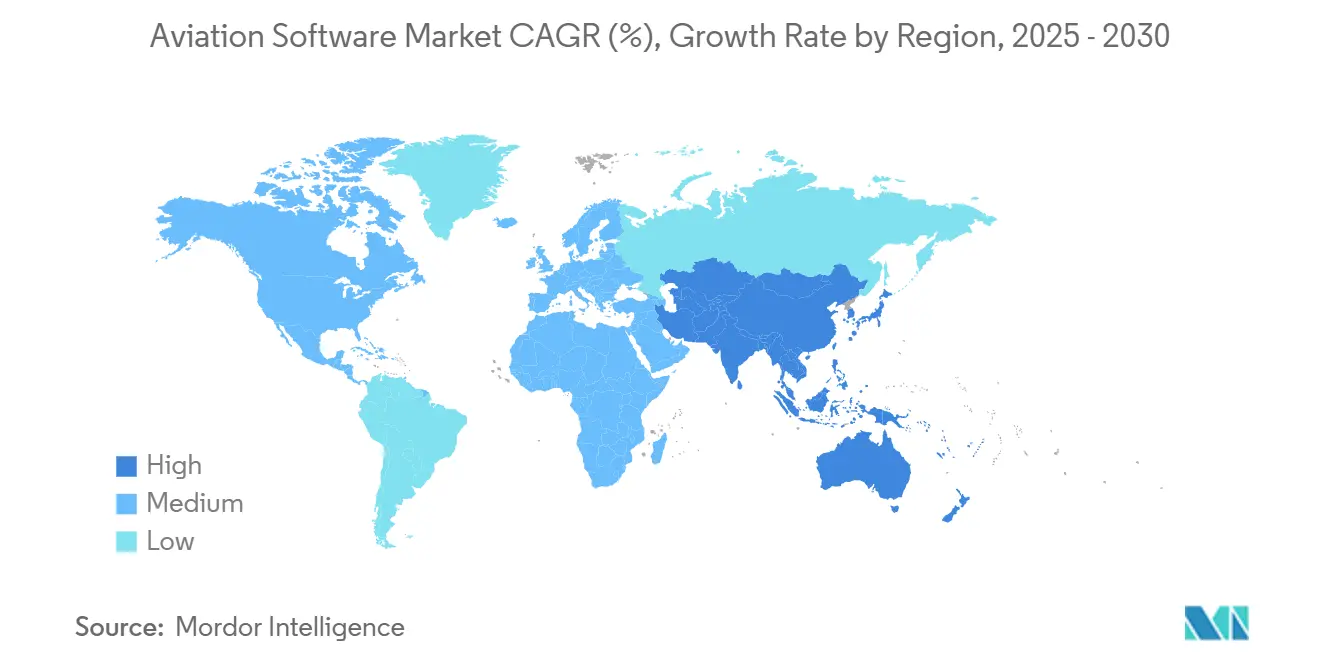

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Software Market Analysis by Mordor Intelligence

The aviation software market size is USD 13.13 billion in 2025 and is forecasted to reach USD 18.12 billion by 2030, implying a 6.64% CAGR. Digital transformation agendas among airlines, airports, and maintenance organizations continue accelerating, positioning the aviation software market as a fundamental enabler of predictive maintenance, seamless passenger journeys, and advanced air-mobility operations. Carriers are intensifying investment in artificial-intelligence applications that lower fuel burn and reduce unplanned maintenance events. At the same time, regulators such as EASA drive mandatory cybersecurity upgrades that expand the addressable demand for compliance software. Consolidation deals from Boeing’s divestiture of non-core digital assets to IFS’s acquisition of EmpowerMX reshape competitive dynamics and open white-space opportunities for specialized vendors. Meanwhile, cloud-native delivery models, now preferred by 95% of airline CIOs, allow rapid scaling and lower total cost of ownership, reinforcing the aviation software market’s migration toward subscription economics.

Key Report Takeaways

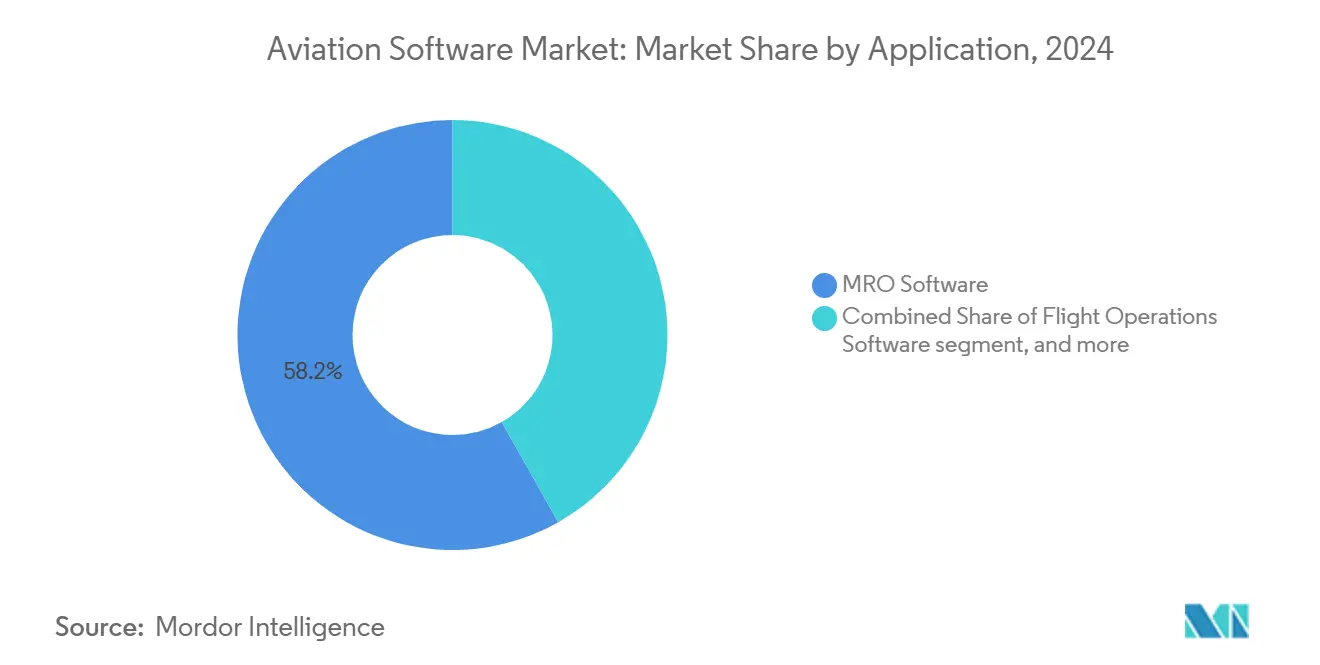

- By application, MRO software captured 58.18% of the aviation software market share in 2024, whereas safety and compliance management is projected to grow at a 7.89% CAGR to 2030.

- By deployment, cloud solutions held 49.80% revenue share of the aviation software market size in 2024; hybrid architectures are advancing at an 8.45% CAGR through 2030.

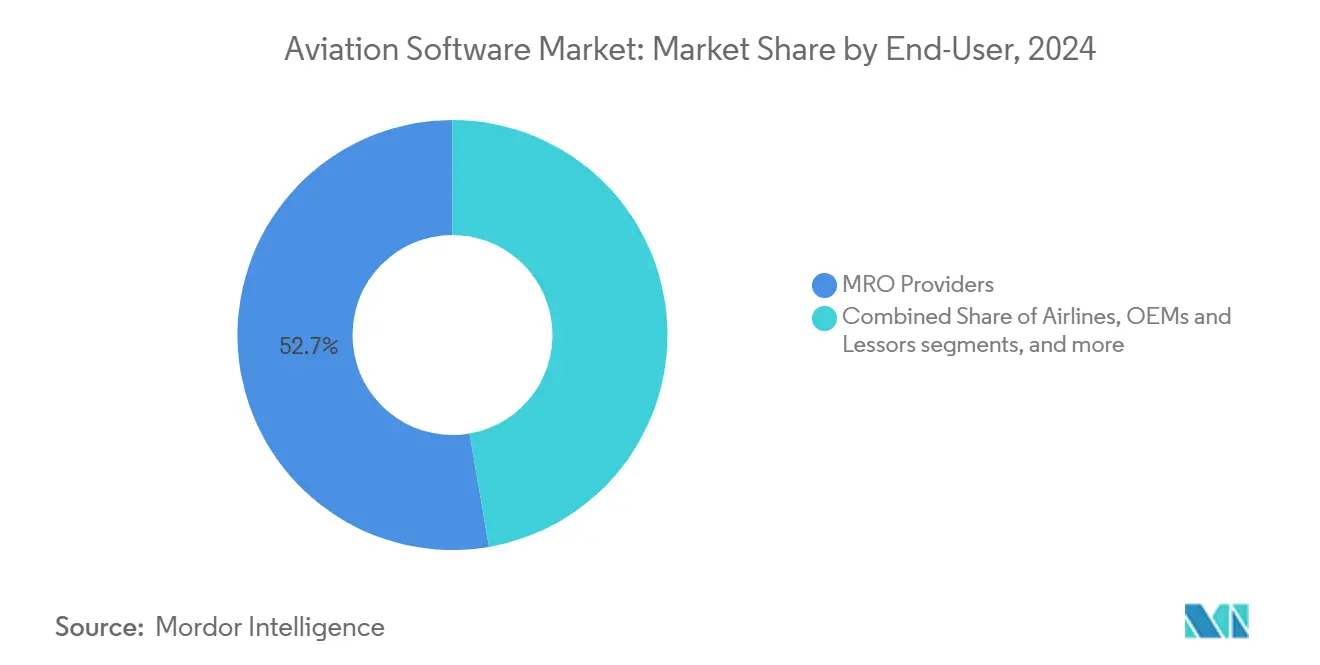

- By end-user, MRO providers led with 52.71% share of the aviation software market in 2024, while airlines exhibit the fastest growth at a 7.91% CAGR to 2030.

- By software licensing model, subscription agreements accounted for 59.25% of the aviation software market size in 2024; perpetual licenses are poised for a 6.23% CAGR through 2030.

- Geographically, North America commanded 37.45% of 2024 revenues, yet Asia-Pacific is the fastest-expanding region with a 7.01% CAGR forecasted to 2030, indicating significant growth opportunities in the aviation software market.

Global Aviation Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased adoption of AI/ML for fuel optimization | +1.20% | North America, Europe, global roll-out | Medium term (2-4 years) |

| Rising demand for real-time flight data analytics | +1.00% | Emerging Asia-Pacific, global airlines | Short term (≤ 2 years) |

| Shift toward cloud-native aviation platforms | +0.90% | North America, European Union | Medium term (2-4 years) |

| Growth in low-cost carrier fleets in emerging markets | +0.80% | Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Regulatory mandates for safety management systems integration | +0.70% | Europe, expanding globally | Short term (≤ 2 years) |

| Surge in advanced air mobility (AAM) ecosystem software needs | +0.60% | North America, European Union, worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased adoption of AI/ML for fuel optimization

Airlines are deploying artificial-intelligence engines that deliver 2–5% direct fuel savings, a compelling economic case that accelerates software procurement cycles. United Airlines’ AWS-hosted TCS Aviana platform exemplifies how real-time analytics simultaneously improve flight planning, crew rostering, and predictive maintenance.[1]Tata Consultancy Services, “United Airlines TCS Aviana Case Study,” tcs.com Airbus’ Skywise ecosystem, already supporting 48,000 users across 11,900 aircraft, illustrates the scalability of AI-enabled maintenance intelligence. Sector-wide savings potential is estimated at USD 15 billion annually by 2035, reinforcing the aviation software market’s importance to long-term airline economics. Investors and OEMs alike now prioritize AI-adjacent functionality in platform roadmaps, ensuring sustained momentum for aviation software market growth.The aviation software market is further expected to benefit as airlines increasingly integrate machine learning into fuel and route optimization systems.

Rising demand for real-time flight data analytics

Carriers are ingesting terabytes of operational data per day and require tools that transform these streams into actionable insights within minutes. GE Aerospace’s Event Measurement System offers 10,000-plus pre-built analytics that help airlines cut delay minutes and improve safety margins.[2]GE Aerospace, “Event Measurement System,” geaerospace.com Lufthansa Technik’s AVIATAR suite integrates internal and partner datasets to produce predictive maintenance alerts and cost-saving recommendations. Cloud-native analytics also support passenger-centric use cases; Korean Air’s Red Hat-based modernization doubled transaction processing speeds, impacting customer experience. As flight volumes rebound, real-time analytics underpin operational resilience, cementing their status as a pivotal aviation software market driver. The aviation software market continues to evolve with enhanced big data processing capabilities, enabling faster decision-making and optimized fleet operations.

Shift toward cloud-native aviation platforms

Ninety-five percent of airlines now place cloud technology among their top three IT priorities, citing scalability, resilience, and faster release cycles.[3]Infosys, “Airline Cloud Priorities,” infosys.com American Airlines’ migration to IBM Cloud reduced unplanned outages and enabled microservice-based application delivery, shortening development timelines.[4]IBM, “American Airlines Cloud Migration,” ibm.com Using Microsoft Azure AI services, Pegasus Airlines reported a 20% rise in employee satisfaction and doubled customer-service chat resolution rates a tangible endorsement of the cloud’s operational upside. Cloud architectures lower the barrier to entry for emerging carriers, thereby expanding the accessible aviation software market and supporting subscription models that align costs with usage. The aviation software market is witnessing rapid adoption of cloud-based integration frameworks that enhance cross-department collaboration and data accessibility.

Growth in low-cost carrier fleets in emerging markets

Asia-Pacific low-cost carriers (LCCs) represent 29% of regional seat capacity and are escalating technology budgets by 14.4% to support network expansion, automated pricing, and mobile passenger services. A strategic focus on indirect sales channels compels the adoption of modular revenue-management and crew-optimization tools tailored to ultra-lean cost structures. Emerging Southeast Asian markets and India each surpassing 50% domestic LCC penetration provide the aviation software market with a deep runway for growth as fleets and route networks proliferate.. The aviation software market is poised to see stronger traction in these regions as LCCs increasingly rely on digital platforms to manage operations efficiently.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cybersecurity compliance costs | –0.8% | Europe, global roll-out | Short term (≤ 2 years) |

| Legacy system integration complexities | –0.6% | Established global carriers | Medium term (2-4 years) |

| Shortage of aviation-specific software talent | –0.5% | North America, Europe | Long term (≥ 4 years) |

| Volatile airline profitability impacting IT budgets | –0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cybersecurity compliance costs

European carriers face steep near-term spending to align with EASA Part-IS mandates covering incident response, penetration testing, and continuous monitoring. Smaller operators often lack dedicated cyber teams, forcing reliance on managed-service providers and inflating total compliance costs. Capital diverted to mandatory security upgrades can delay discretionary digital projects, dampening immediate expansion of the aviation software market in affected jurisdictions. The aviation software market is also witnessing increased demand for cybersecurity-integrated solutions as airlines prioritize data protection and regulatory adherence.

Legacy system integration complexities

Many flag carriers operate decades-old mainframes that underpin crew scheduling, flight planning, and inventory management. Upgrading these mission-critical systems without service disruption demands dual-running environments and extensive data-migration validation. The resulting cost and timeline overruns diminish ROI visibility and can stall modernization cycles, tempering aviation software market uptake among incumbents. Vendors that supply robust APIs and phased-migration toolkits help mitigate integration risk and sustain adoption momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: MRO software drives digital transformation

MRO platforms controlled 58.18% of 2024 revenue, underscoring maintenance efficiency as airlines’ foremost digital priority. Air India’s AMOS roll-out across a 470-aircraft fleet illustrates how large-scale deployments improve turnaround times and parts inventory accuracy. Flight operations suites benefit from AI-enabled trajectory optimization that reduces block times, while crew management solutions such as Rosterize trim staffing requirements by 10% through machine-learning-driven pairing logic. Safety-and-compliance tools, expanding at 7.89% CAGR, respond to cybersecurity-inclusive oversight regimes. As carriers quantify downtime savings, the aviation software market size attributable to MRO applications is expected to widen its lead through 2030.

Rapid uptake of predictive-maintenance functionality makes MRO software the gateway for wider digitalization across airline departments. Subscription pricing lowers entry hurdles for mid-tier operators, while API-centric architectures facilitate data interchange with ERP and flight-operations systems. Safety-and-compliance platforms, integrating SMS and ISMS workflows, form the fastest-moving niche as regulators codify cyber-safety convergence. The aviation software market continues to reward vendors that embed analytics, mobile capability, and paperless task-cards within their MRO stacks.The aviation software market will further expand as airlines increasingly standardize on unified MRO ecosystems to optimize fleet reliability and operational visibility.

By Deployment: Cloud adoption accelerates digital migration

Cloud delivery models commanded 49.80% of 2024 sales as carriers favor OpEx-oriented procurement and elastic compute capacity. American Airlines documented material reliability gains after migrating legacy workloads to IBM Cloud. Hybrid configurations projected to grow 8.45% CAGR balance sovereignty requirements with platform agility, reflecting regulated data concerns in Europe and the Middle East. On-premise installations persist for flight-planning and weight-and-balance systems bound by deterministic latency needs, yet their share diminishes annually within the overall aviation software market.

As 57% of airlines actively use SaaS applications, vendor roadmaps now default to multi-tenant architectures that enable weekly feature releases and seamless security patching. The aviation software market share advantage that cloud vendors enjoy expands as legacy customers retire monolithic systems. Hybrid adoption accelerates where operators leverage private-cloud substrates for core data while consuming analytics and mobility modules as public-cloud services, ensuring gradual migration paths without compromising governance mandates. The aviation software market continues to benefit from cloud ecosystem partnerships that drive continuous delivery and operational efficiency.

By End-User: MRO providers lead digital adoption

Third-party maintenance organizations accounted for 52.71% of 2024 purchases, validating their role as digital-investment front-runners. Lufthansa Technik’s AVIATAR platform, covering 38,000-plus aircraft, showcases how independent MROs leverage data aggregation to sell condition-monitoring and performance-prediction services. Posting a 7.91% CAGR, airlines are narrowing the gap by funding cross-functional transformation initiatives spanning engineering, flight ops, and customer experience, thereby expanding total aviation software market demand.

Airports increasingly deploy resource-management and collaborative-decision-making suites, as evidenced by Bogotá’s A-CDM implementation that improved turnaround predictability. OEMs and lessors invest in digital twin technology to monitor asset health and residual value, while air navigation service providers focus on trajectory-based operations. The aviation software market thus reflects a diversified buyer landscape. Yet, providers that tailor offerings to MRO pain points such as parts logistics and certificate management retain a defensible revenue base.

By Software Licensing Model: Subscription models transform economics

Subscription agreements represented 59.25% of 2024 revenue because they minimize upfront spend and offer continuous innovation streams. SaaS penetration simultaneously broadens geographic reach, allowing smaller carriers in Latin America and Africa to access tier-one capability sets. Outcome-based pricing concepts, gaining traction in AI-heavy modules, mirror evolving customer preferences and solidify annuity revenue within the aviation software market.

Unexpectedly, perpetual licenses register a 6.23% CAGR as certain flag-carriers negotiate long-term ownership for mission-critical systems to ensure modification autonomy. Pay-as-you-go tariffs have gained popularity for seasonal demand forecasting and simulator scheduling, underscoring the flexibility spectrum that is now available. As the global SaaS sector is predicted to climb toward USD 462.94 billion by 2028, subscription penetration inside the aviation software market is set to deepen, even as niche perpetual and consumption-based models coexist in specialized use cases.

Geography Analysis

North America commanded 37.45% of 2024 spending, supported by early adoption of AI-driven maintenance analytics and a mature cloud-infrastructure footprint. Flag-carriers such as United and Delta deploy advanced operational-efficiency suites, while regional MRO hubs in the United States and Canada pioneer paperless work-packages, reinforcing dominance within the aviation software market. Venture-capital activity centered on Silicon Valley and Seattle accelerates startup formation, feeding innovation pipelines that benefit the entire region. Robust regulatory oversight coupled with steady airline profitability sustains technology budgets through 2030.The aviation software market in North America is further strengthened by consistent investments in automation, cybersecurity, and next-generation flight analytics platforms.

Asia-Pacific delivers the fastest expansion, advancing 7.01% CAGR to 2030 due to surging low-cost carrier fleets and rapid middle-class travel demand. India and Indonesia invest heavily in cloud-native revenue-management and crew-scheduling systems, each exceeding 50% of the domestic LCC seat share. China’s modernization drive opens opportunities for predictive-maintenance and air-traffic-optimization platforms, even as regulatory nuances shape localization requirements. Ramco Systems’ partnership with Hanjin Information Systems to digitize Korean operations typifies region-specific collaborations that enlarge the aviation software market footprint.The aviation software market across Asia-Pacific is poised for continued growth as governments champion digital aviation ecosystems and sustainability-linked innovations.

The Middle East and Africa region benefits from fleet growth projected at 5.1% annually through 2035, spurring MRO capacity developments and airport megaprojects valued at USD 151 billion. Emirates-led hubs in Dubai and Etihad-backed programs in Abu Dhabi seek cloud-enabled passenger-journey orchestration, while Saudi Arabia’s Vision 2030 underwrites large-scale digital-airport investments. African adoption remains nascent but gains momentum as South African operators implement cloud-based maintenance tracking, demonstrating the aviation software market’s widening reach into emerging geographies.

Competitive Landscape

The aviation software market displays fragmented concentration, with incumbent OEM-affiliated vendors coexisting alongside agile cloud-native entrants. Boeing’s USD 10.55 billion divestiture of digital-aviation subsidiaries signals a strategic retrenchment that unlocks space for niche specialists. Consolidation remains a defining theme: IFS’s purchase of EmpowerMX injects AI-backed workflow automation into its enterprise suite, while Veryon’s acquisition of Rusada broadens maintenance-management breadth. Vendors differentiate via technology depth particularly AI, blockchain provenance tracking, and integrated cybersecurity rather than price alone.

Product roadmaps now spotlight advanced-air-mobility modules, positioning suppliers for first-mover advantage as eVTOL commercialization nears. Ramco Systems’ Aviation 6.0 release incorporates machine-learning diagnostics that preempt component failure and automate inventory ordering. Startup entrants such as Airspace Intelligence, backed by USD 34 million in Series B funding, deliver “Waze-like” flight-routing optimization that challenges legacy flight-planning paradigms. High certification barriers and domain-expertise requirements temper competitive intensity, yet strategic partnerships allow smaller players to scale globally without prohibitive capital outlays, maintaining dynamic evolution within the aviation software market.

Aviation Software Industry Leaders

International Business Machines Corporation (IBM)

Honeywell International Inc.

The Boeing Company

SITA N.V.

Lufthansa Systems GmbH (Deutsche Lufthansa AG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Ramco Systems completed the implementation of its Aviation Software at Indamer Technics Private Limited. Indamer Technics provides technical, operational, and financial solutions to improve efficiency in the Indian commercial aviation and government sectors.

- May 2025: El Dorado Airport became Latin America’s first to deploy A-CDM, enhancing collaborative decision-making efficiency.

- April 2025: Trax and Rolls-Royce launched an interface linking eMRO with the Blue Data Thread platform, streamlining engine maintenance data exchange.

- February 2025: The Civil Aviation Authority of the Philippines (CAAP) awarded Metron Aviation a contract for software for air traffic flow management (ATFM). The system aims to enhance the Philippines' regional situational awareness capabilities for air traffic management in Southeast Asia.

Global Aviation Software Market Report Scope

| Flight Operations Software |

| MRO Software |

| Crew and Workforce Management |

| Airport Operations Management |

| Revenue and Inventory Management |

| Safety and Compliance Management |

| On-Premise |

| Cloud |

| Hybrid |

| Airlines |

| Airports and Ground Handlers |

| MRO Providers |

| OEMs and Lessors |

| Air Navigation Service Providers |

| Subscription (SaaS) |

| Perpetual Licence |

| Pay-as-you-go |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Application | Flight Operations Software | ||

| MRO Software | |||

| Crew and Workforce Management | |||

| Airport Operations Management | |||

| Revenue and Inventory Management | |||

| Safety and Compliance Management | |||

| By Deployment | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By End-User | Airlines | ||

| Airports and Ground Handlers | |||

| MRO Providers | |||

| OEMs and Lessors | |||

| Air Navigation Service Providers | |||

| By Software Licensing Model | Subscription (SaaS) | ||

| Perpetual Licence | |||

| Pay-as-you-go | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aviation software market?

The aviation software market size is USD 13.13 billion in 2025 and is projected to reach USD 18.12 billion by 2030, implying a 6.64% CAGR.

Which application area holds the largest revenue share?

Maintenance, repair and overhaul (MRO) software leads with a 58.18% share of 2024 revenues, reflecting airlines’ focus on operational reliability.

Which region is growing the fastest?

Asia-Pacific is expanding at a 7.01% CAGR through 2030 due to rising low-cost-carrier fleets and rapid passenger-traffic growth.

Why are subscription licensing models preferred?

Subscription plans align costs with usage, deliver continuous upgrades and reduce upfront capital requirements, capturing 59.25% of 2024 spending.

How are regulatory mandates influencing demand?

EASA Part-IS cybersecurity rules compel European operators to adopt integrated safety-and-information-security software, adding steady baseline demand.

What new opportunities are emerging for vendors?

Advanced air-mobility operations require novel traffic-management, maintenance and scheduling platforms, creating fresh growth pockets for specialized suppliers.

Page last updated on: