Aviation Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.2 Billion |

| Market Size (2031) | USD 7.47 Billion |

| Growth Rate (2026 - 2031) | 12.21% CAGR |

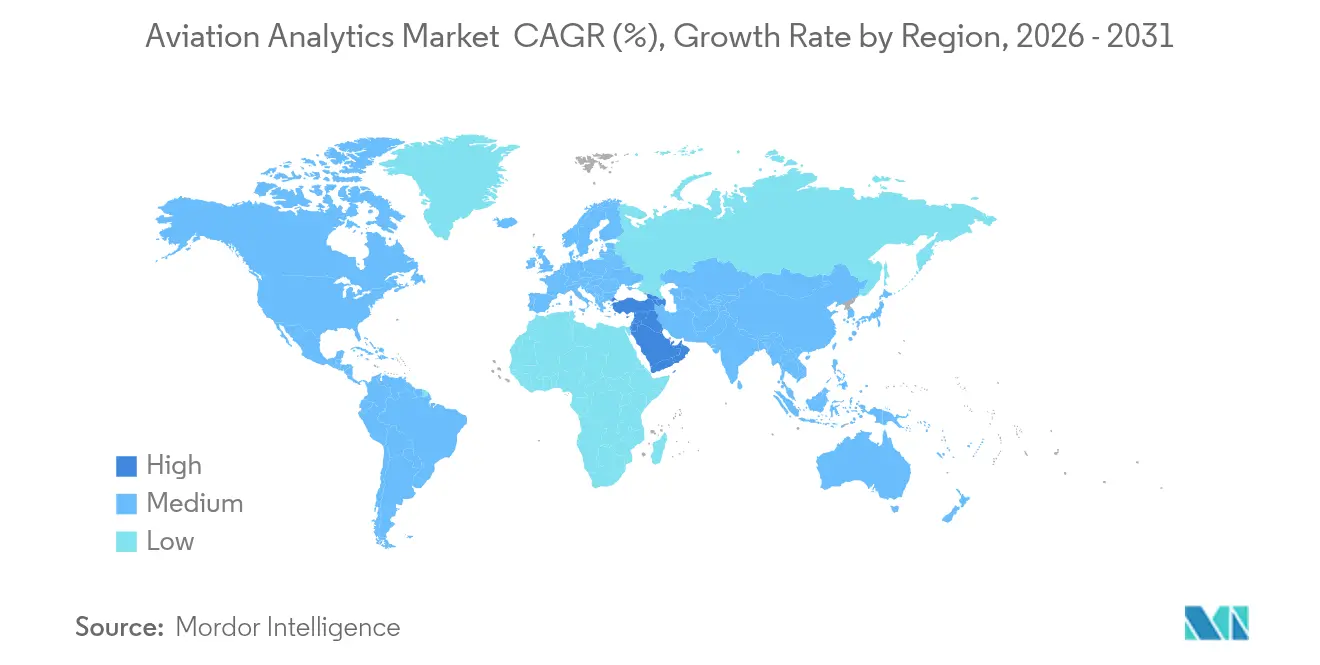

| Fastest Growing Market | Middle East |

| Largest Market | North America |

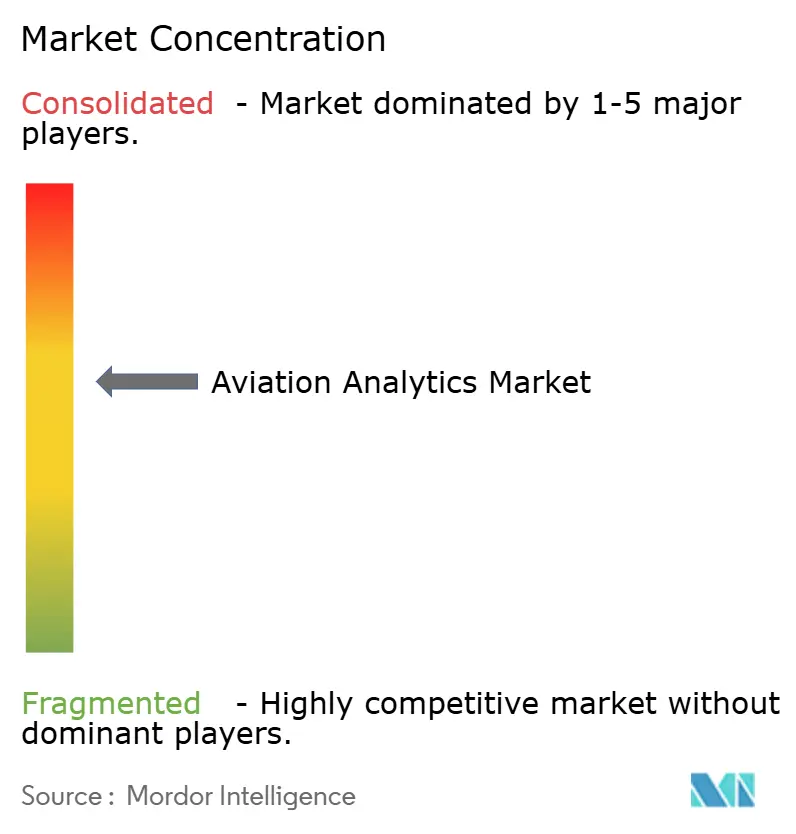

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

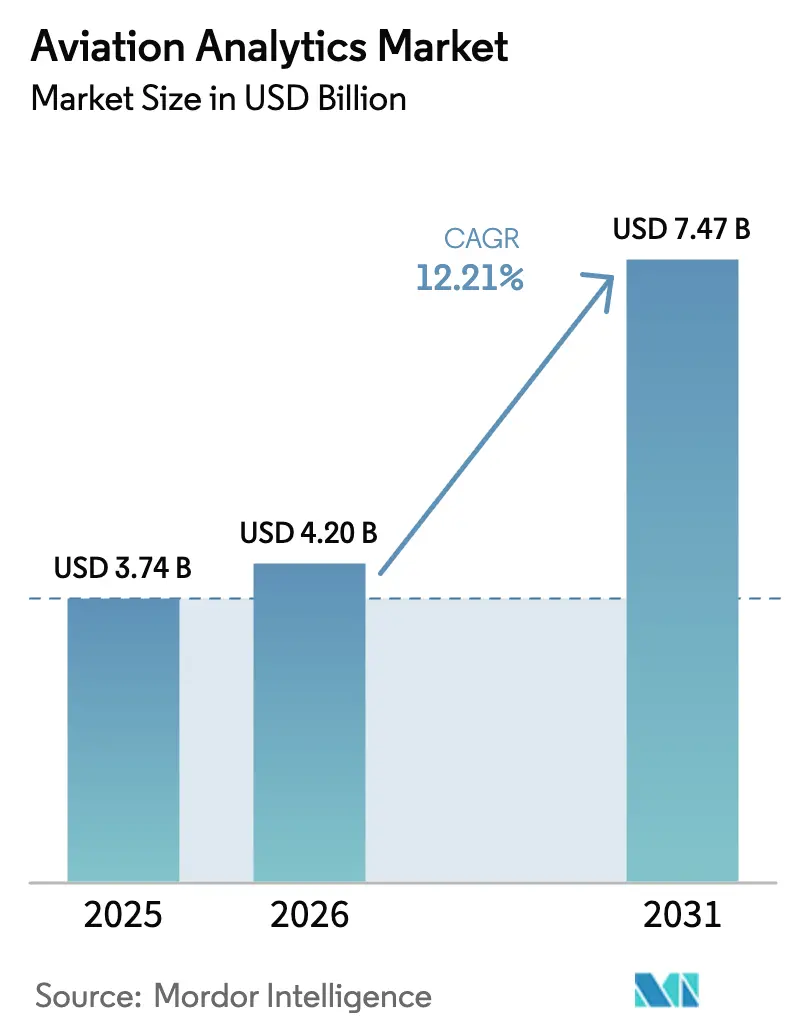

Aviation Analytics Market Analysis by Mordor Intelligence

Aviation analytics market size in 2026 is estimated at USD 4.2 billion, growing from 2025 value of USD 3.74 billion with 2031 projections showing USD 7.47 billion, growing at 12.21% CAGR over 2026-2031. Expansion reflects operators’ need to curb fuel costs, comply with safety mandates, and exploit data streaming from new-generation aircraft. Predictive maintenance is being adopted to prevent Aircraft on Ground events that can cost up to USD 100,000 per hour. Fuel-management platforms remain the largest application as airlines use machine-learning models to trim 1–4.3% of total fuel spend. Cloud deployment dominates because scalable infrastructure supports real-time decision-making and AI-driven personalization initiatives. Regional growth is led by the Middle East, where airport capacity programs and fleet renewals require sophisticated data solutions.

Key Report Takeaways

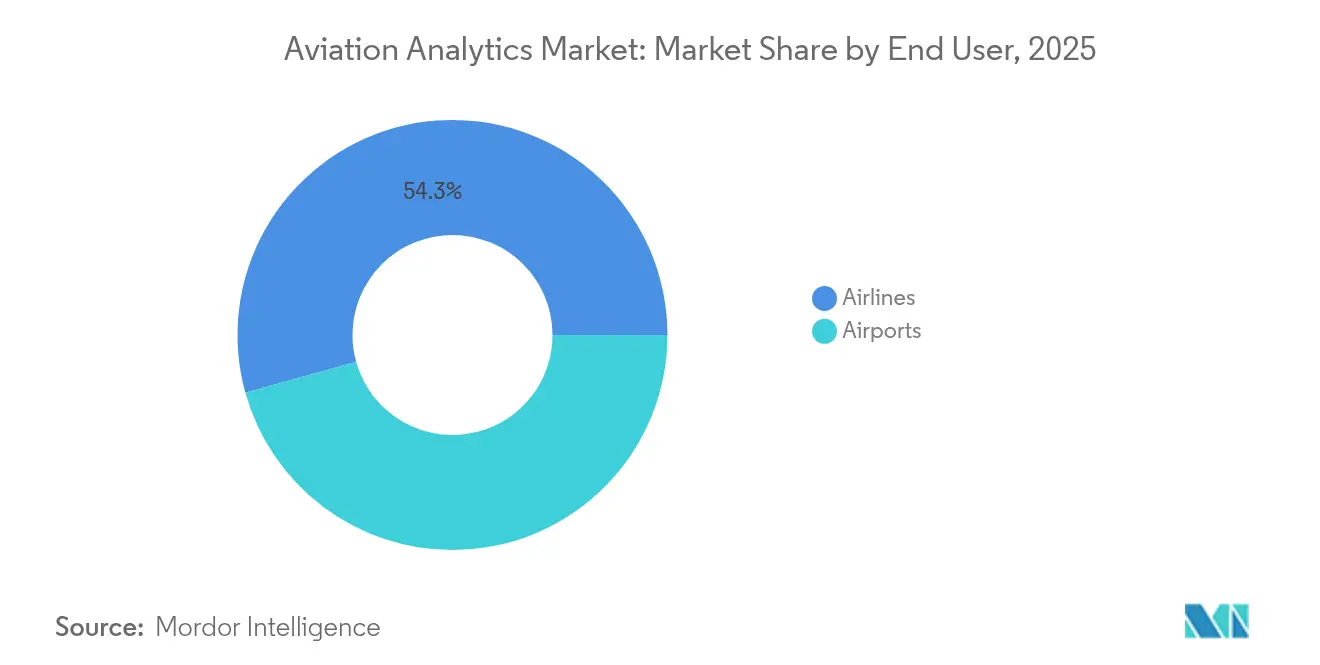

- By end user, airlines led with 54.32% revenue share in 2025, while airports are growing the fastest at a 15.05% CAGR through 2031.

- By application, fuel management captured 29.55% of the aviation analytics market share in 2025; the segment is projected to expand at a 14.08% CAGR to 2031.

- By analytics type, predictive analytics held 45.02% of the aviation analytics market size in 2025; prescriptive analytics is advancing at the highest 13.18% CAGR to 2031.

- By deployment, cloud solutions accounted for 67.12% of 2025 revenue and posted the strongest 15.21% CAGR.

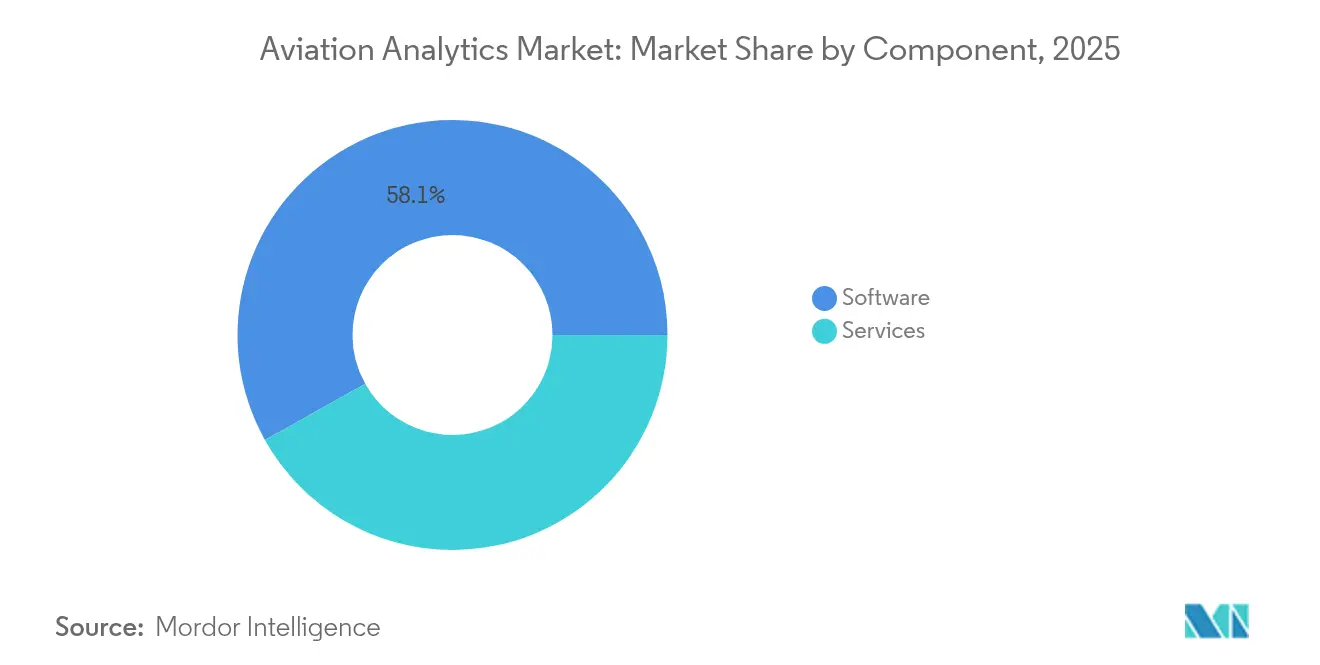

- By component, software represented 58.12% of 2025 sales, whereas services recorded a 12.05% CAGR through 2031.

- By business function, finance commanded 32.10% of the aviation analytics market size in 2025, while supply chain analytics posts a 10.62% CAGR.

- By geography, North America held a 35.21% share in 2025, whereas the Middle East grew the fastest at an 11.31% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aviation Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of predictive maintenance to cut AOG losses | +2.8% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Fuel-burn optimization amid SAF cost pressures | +3.1% | Global, strongest in Europe due to regulation | Short term (≤ 2 years) |

| Big-data monetization from new-gen aircraft sensors | +2.2% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Safety-management mandates driving FDM analytics | +1.9% | Europe and North America | Medium term (2-4 years) |

| Real-time SAF performance datasets enabling dynamic routing | +1.7% | Europe and North America, spreading to Asia-Pacific | Short term (≤ 2 years) |

| Edge-AI telemetry from eVTOL fleets creating micro-service analytics demand | +0.8% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of Predictive Maintenance to Cut AOG Losses

Airlines connect aircraft to cloud-based diagnostics that analyze real-time sensor feeds and flag impending faults. Airbus estimates predictive programs could save operators USD 4 billion annually by 2043 as 11,600 aircraft stream data into its Skywise ecosystem.[1]Airbus, “Skywise: Digital Alliance for Aviation,” airbus.com United Airlines has demonstrated schedule-reliability gains after scaling fleet health analytics, while Collins Aerospace reports a 30% reduction in maintenance-driven delays through its Ascentia platform.[2]Source: Collins Aerospace, “Ascentia Predictive Maintenance Case Studies,” collinsaerospace.com Veryon Diagnostics notes a 50% drop in troubleshooting time and a 10% cut in delays after embedding AI models that learn from historical part failures. As predictive insights mature, airlines shift from interval-based to condition-based maintenance, freeing labor capacity and spare-parts inventory.

Fuel-Burn Optimization Amid SAF Cost Pressures

Sustainable Aviation Fuel prices sit well above conventional jet fuel, intensifying the need for granular efficiency analytics. Virgin Atlantic’s 100% SAF transatlantic flight saved 95 tonnes of CO₂, validating data-driven flight-planning techniques. Alaska Airlines employs AI to refine track selection and descent profiles, lowering emissions while maintaining on-time performance. Boeing’s Fuel Analytics module analyses more than 650 parameters per flight, delivering 1–3% consumption savings that can top USD 1 million annually for wide-body fleets. Access to real-time SAF performance datasets enables airlines to reroute dynamically based on fuel availability and pricing differentials across hubs.

Big-Data Monetization from New-Gen Aircraft Sensors

Modern airframes generate terabytes of data per flight through advanced avionics and IoT nodes. Academic studies confirm that integrated sensor networks underpin predictive analytics and operational optimization in civil aviation. Platforms such as GE Aerospace FlightPulse convert raw flight parameters into actionable insights for crews, improving approach stability and climb performance.[3]GE Aerospace, “Safety Insight and FlightPulse Product Sheets,” geaerospace.com Airlines increasingly commercialise anonymised operational data by providing benchmarking services to peer carriers and OEMs, creating fresh revenue streams without disrupting core transport operations.

Safety-Management Mandates Driving FDM Analytics

Forty years of evolution of flight data monitoring (FDM) contributed to the fall in global hull-loss accident rates. Teledyne Controls links modern FDM systems with weather and scheduling feeds to contextualise exceedances and spot systemic hazards. GE Aerospace Safety Insight automates data cleaning and risk scoring, helping operators benchmark performance against aggregated peer datasets. European regulators now require continuous safety-performance measurement, accelerating global adoption of comprehensive FDM analytics platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy IT silos hamper data interoperability | -1.8% | Global, most acute in incumbent carriers | Medium term (2-4 years) |

| Shortage of aviation-savvy data scientists | -1.4% | Severe in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Cyber-risk of streaming flight data to cloud | -1.1% | Heightened in security-sensitive regions | Short term (≤ 2 years) |

| Passenger-privacy rules limiting behavioural analytics | -0.9% | Europe under GDPR, spreading worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy IT Silos Hamper Data Interoperability

Many established airlines run bespoke reservation, maintenance, and finance systems built over decades, resulting in fragmented data landscapes. Integrating these environments demands major investment in middleware and ETL pipelines. Lufthansa broke through this constraint by linking over 10 ERP instances to a unified procurement analytics layer, unlocking spend visibility across the group.[4]Source: “Digital Procurement at Lufthansa,” Lufthansa Group, lufthansagroup.com Nevertheless, change-management hurdles and competing budget priorities slow migration toward real-time enterprise architectures that fully exploit analytics potential.

Shortage of Aviation-Savvy Data Scientists

Advanced analytics projects require professionals versed in both aeronautical engineering and machine learning. Retirements among experienced technicians coincide with intense demand for AI talent, producing a skills gap that delays project timelines. Airlines counter by partnering with universities and offering rotation programs that pair graduates with flight operations mentors. AI-enabled workforce-planning software assists recruiters, yet the depth of domain knowledge still grows slowly compared with technology ambition, constraining the rapid scaling of complex analytics use cases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Airlines Lead, Airports Surge

The aviation analytics market size attributed to airlines reached USD 2.03 billion in 2025, equal to 54.32% of global revenue. Full-service carriers invest in integrated revenue-management engines, which boosted operating income at Delta Air Lines by 10% after full cloud migration. Low-cost operators apply dynamic ancillary-pricing algorithms; airBaltic raised passenger spending by 6% through AI-guided offers. Cargo airlines deploy route-optimization tools to mitigate volatility in fuel and charter rates.

Although smaller in absolute terms, airports register a 15.05% CAGR to 2031. Large hubs automate baggage tracing with IDEMIA and SITA’s ALIX solution, lifting match accuracy and reducing mishandled bags. Medium hubs such as Orlando International handle 2,800 bags per hour through computer-vision sorting belts. Regional airports embrace cloud dashboards to visualise queue times and asset utilization, narrowing the technology gap with metropolitan gateways and reinforcing an analytics adoption cycle.

By Application: Fuel Management Dominates, Safety Analytics Accelerate

Fuel management contributed 29.55% of the aviation analytics market share in 2025 and is expected to maintain the lead with a 14.08% CAGR, the highest among application groups. Boeing’s Fuel Analytics interrogates 200 standard analyses per leg to detect drag-producing events and recommend optimised speeds. Airlines link these insights with procurement datasets to align hedging strategies, amplifying financial returns. Inventory-management modules reduce surplus spares by up to 30%, freeing working capital for newer digital tools.

Flight-safety analytics benefit from regulatory scrutiny. Teledyne Controls reveals a strong correlation between expanded FDM coverage and declining approach-and-landing incidents. Risk-management analytics embed AI to forecast knock-on delays caused by storms, enabling proactive crewing and gate assignment. Disruption-management platforms from Amadeus shorten recovery windows when events still occur, protecting network integrity and passenger goodwill.

By Analytics Type: Predictive Dominance, Prescriptive Momentum

Predictive solutions held 45.02% of the aviation analytics market size in 2025, buoyed by decades of digital flight-data accumulation and proven return on investment in maintenance. Airbus Skywise synthesises historical and in-flight telemetry, identifying component-failure patterns long before scheduled inspections. Diagnostic analytics remain vital for root-cause investigations, yet newer prescriptive models recommend immediate actions.

Prescriptive adoption is set to grow 13.18% annually as algorithms mature. GE Aerospace’s Network Operations platform evaluates aircraft, crew, and gate variables to offer disruption-recovery scenarios that slash irregular-operation costs by 15%. Airlines integrate prescriptive outputs directly into crew-scheduling and load-planning systems, opening a pathway toward semi-autonomous network control.

By Deployment: Cloud First, Hybrid Expands

Cloud deployments captured 67.12% of 2025 spending as carriers converted legacy workloads to hyperscale environments capable of processing millions of telemetry points every hour. Delta’s end-to-end shift enabled real-time re-accommodation during weather events, improving customer-satisfaction metrics. Elastic compute power allows airlines to test new optimization models without adding on-premises servers, accelerating innovation cycles.

Security-sensitive functions, such as aircraft-configuration data, continue to reside on premises. Rising cyber-threats—including a major 2024 attack that caused substantial flight cancellations at a US carrier—prompt boards to maintain air-gapped repositories for critical systems. Consequently, hybrid architectures gain traction, pairing local data guardianship with cloud-based advanced analytics. New FAA rules mandate that electronic system security be demonstrated for network-connected avionics, shaping investment decisions.

By Component: Software Core, Services Scale

Software generated 58.12% of 2025 revenue, spanning visual dashboards, AI inferencing engines, and mobile decision-support apps. GE Aerospace, Boeing, and Collins Aerospace provide end-to-end suites that harmonise fuel, maintenance, and safety modules under uniform data models. Open APIs promote ecosystem development as third-party startups add specialist algorithms for weather risk or slot-swap optimization.

Services outpace software growth at 12.05% CAGR. Managed-service agreements help carriers lacking in-house data science talent to extract value from complex platforms. Collins Aerospace offers Ascentia Analytics Services that manage ingestion, validation, and rule-writing tasks on behalf of operators. Training and change-management engagements ensure frontline acceptance, improving project returns and cementing supplier relationships.

By Business Function: Finance Tops Budgets, Supply Chain Gains Urgency

Finance claimed 32.10% of the 2025 revenue mix as airlines prioritised fare personalization and cost oversight. LATAM Airlines adopted Sabre Air Price IQ to move from filed fares to dynamic offers, improving unit revenue resilience through market swings. Cirium and Aerlytix launched a joint risk-analysis suite for lessors, reflecting heightened scrutiny of asset valuations amid interest-rate volatility.

Supply-chain analytics is rising fastest at a 10.62% CAGR, responding to chronic parts shortages that prolong AOG events. Aviation Week projects global MRO outlays to hit USD 119 billion by 2026, intensifying the need for predictive spare-parts planning. Ramco’s maintenance-platform clients automate 90% of routine purchase orders, reducing mechanic foot-time and freeing scarce labor for complex tasks. Inventory-visibility dashboards integrate supplier delivery forecasts, enabling planners to reroute parts shipments and avoid cascading schedule disruptions.

Geography Analysis

North America contributed 35.21% of the 2025 global revenue, supported by early passenger-data connectivity and the presence of major aerospace OEMs. United Airlines extended predictive maintenance to its entire narrow-body fleet, improving on-time departures, while Alaska Airlines harnessed AI for route upslope adjustments that save fuel on Seattle departures. FAA guidance on AI and cybersecurity gives carriers regulatory clarity, but rising attack frequency prompts renewed investment in perimeter defenses.

Asia-Pacific presents a multifaceted outlook. China and India ramp up analytics around growing domestic networks, whereas Japan and South Korea integrate datasets from aging and next-gen aircraft to secure fleet-wide efficiencies. Thailand’s airport-expansion plan relies on passenger-flow dashboards to keep queue times below regulatory thresholds, underscoring rising demand for real-time situational awareness.

The Middle East records the fastest 11.31% CAGR as fleets double under Vision 2030 initiatives. Seat capacity in the region rose from 70 million in 2000 to 257 million in 2024, with Emirates and Qatar Airways adopting integrated network-planning suites to balance hub-bank waves. Saudi Arabia’s launch of Riyadh Air adds further complexity, making prescriptive crew-pairing tools essential to keep utilization high. Airport operators in Dubai and Doha deploy computer-vision platforms that track passenger density and adjust resource rosters in real time.

Latin America and Africa show accelerating adoption from low bases. LATAM implements intelligent pricing, while Ethiopian Airlines introduces cloud-based maintenance logs to support regional MRO growth. Currency volatility and uneven connectivity infrastructure temper deployment speed, yet partnerships with global platform providers lower entry barriers and encourage phased rollouts across secondary hubs.

Competitive Landscape

Competitive Landscape

The aviation analytics market features moderate concentration: aerospace incumbents supply vertically integrated platforms, technology majors contribute cloud and AI pipelines, and startups target narrow pain points. Boeing’s agreement to divest Jeppesen, ForeFlight, and AerData to Thoma Bravo for USD 10.55 billion signals portfolio realignment toward core manufacturing and safety analytics niches. Safran’s EUR 220 million (USD 255.1 million) purchase of AI specialist Preligens underscores the premium on autonomous-system competencies.

Competition intensifies in predictive maintenance and fuel optimization, where return on investment is easy to quantify. GE Aerospace leverages engine digital twins, while SITA and Amadeus capitalise on their extensive airline-IT footprints to feed models high-quality operational data. Emerging whitespace includes eVTOL fleet analytics, airport curb-to-gate synchronization, and cross-operation control towers that break legacy silos. Providers that bundle multiple use cases under a unified data fabric gain an edge as airlines look to reduce vendor complexity and support costs.

Supplier power remains balanced because switching requires complex integration and user retraining. However, long-term service contracts and proprietary algorithms can lock clients into specific ecosystems. Successful challengers differentiate through open architectures and outcome-based pricing models that share efficiency gains with customers, aligning incentives and expanding addressable budgets.

Aviation Analytics Industry Leaders

International Business Machines Corporation (IBM)

Honeywell International Inc.

SAP SE

GE Digital (General Electric Company)

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Boeing agreed to sell parts of its Digital Aviation Solutions business to Thoma Bravo for USD 10.55 billion, focusing internal resources on core airframe programs while supplying maintenance analytics under long-term contracts.

- December 2024: IDEMIA and SITA launched the Augmented Luggage Identification Experience, which applies biometrics to cut baggage mishandling.

- December 2024: Lufthansa Technik embedded AI into MRO workflows to enhance parts forecasting and repair-slot allocation.

- September 2024: Safran acquired AI firm Preligens for EUR 220 million (USD 255.1 million) to deepen analytics capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the aviation analytics market covers all software and related service spend that lets airlines, airports, and MRO teams capture, store, and interrogate flight, fleet, passenger, finance, and operational data to improve efficiency, safety, and revenue. It spans descriptive through prescriptive analytics deployed on-premise or in the cloud across commercial, cargo, and regional aircraft. We size only licensed software and paid analytics services; hardware, generic BI platforms, and stand-alone consulting fees are outside scope.

Exclusion: Pure consulting projects with no recurring software or analytics component are not counted.

Segmentation Overview

- By End User

- Airlines

- Full-Service Carriers

- Low-Cost Carriers

- Cargo and Charter Operators

- Airports

- Large Hub Airports

- Medium Hub Airports

- Small and Regional Airports

- Airlines

- By Application

- Risk Management

- Inventory Management

- Fuel Management

- Revenue Management

- Customer Analytics

- Flight Safety Analytics

- Crew Management

- Disruption Management

- By Analytics Type

- Descriptive Analytics

- Diagnostic Analytics

- Predictive Analytics

- Prescriptive Analytics

- By Deployment

- On-Premises

- Cloud

- By Component

- Software

- Services

- Managed Services

- Professional Services

- By Business Function

- Sales and Marketing

- Finance

- MRO Operations

- Supply Chain

- Flight Operations

- Network Planning and Scheduling

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Conversations with flight operations directors, airport CIOs, MRO planners, and analytics product leads across North America, Europe, Asia, and the Middle East validated adoption timelines, average selling prices, and cloud migration rates. Surveys with digital transformation managers clarified spending intentions that were missing from filings, thereby closing input gaps before modeling.

Desk Research

Our analysts assembled baseline inputs from public domain pillars such as IATA traffic statistics, ICAO fleet registers, FAA and EASA safety filings, Eurocontrol air traffic flow data, and fuel price curves from the U.S. EIA. Industry white papers from trade groups (Airports Council International, RTCA) added functional benchmarks, while investor presentations and 10-K filings helped profile airline IT spend. Subscription tools, including D&B Hoovers for company financials and Aviation Week for program intelligence, supplied granular revenue splits that desk sources rarely show. These references are illustrative, not exhaustive; many other open sources informed the desk phase.

Market Sizing & Forecasting

The model begins with a top-down reconstruction of global commercial and cargo aircraft counts, average analytics spend per tail, and airport IT budgets, which are then cross-checked with sampled supplier revenues (a selective bottom-up roll-up) to align totals. Key variables include passenger kilometer growth, jet fuel volatility, installed narrow body versus wide body mix, cloud penetration in airline IT, and predictive maintenance adoption rates. A multivariate regression projects demand to 2030, with elasticities vetted during expert interviews. Where bottom-up evidence is thin for smaller regional carriers, spend ratios from similar fleets are imputed and flagged for review.

Data Validation & Update Cycle

Before sign-off, results pass variance checks against independent traffic and IT spend indices. Senior analysts review anomalies, and any outlier triggers a re-interview with source contacts. Reports refresh annually, with interim updates when material events such as a major fleet grounding shift underlying drivers.

Why Our Aviation Analytics Baseline Commands Reliability

Published numbers differ because firms pick varying scopes, input series, and refresh windows.

Some tally generic BI tools, others fold adjacent cloud platforms, and currency conversions also vary.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.74 B (2025) | Mordor Intelligence | - |

| USD 2.60 B (2023) | Global Consultancy A | Excludes airport analytics spend and uses 2023 exchange rates without inflation normalization |

| USD 2.34 B (2023) | Industry Publishing House B | Counts only solutions revenue, ignores recurring service contracts, leading to lower base |

| USD 2.50 B (2022) | Regional Consultancy C | Older base year and conservative traffic recovery scenario depress current year estimate |

Differences generally stem from scope cuts, dated baselines, or single source revenue rolls. Mordor's blended top-down and corroborated bottom-up approach, anchored to clearly stated inclusions and refreshed each year, offers decision makers a balanced, transparent starting point they can trace back to observable variables.

Key Questions Answered in the Report

What is the current size of the aviation analytics market?

The aviation analytics market stands at USD 4.2 billion in 2026 and is set to reach USD 7.47 billion by 2031, reflecting a 12.21% CAGR.

Which application area generates the most revenue?

Fuel-management analytics leads, holding 29.55% of 2025 revenue and expanding at a 14.08% CAGR as airlines chase fuel and SAF efficiency gains.

Why are airlines migrating analytics to the cloud?

Cloud platforms offer elastic compute power and real-time data-processing capabilities that support AI-driven decision systems while reducing on-premises infrastructure costs.

Which region is growing the fastest?

The Middle East posts the highest CAGR at 11.31% due to large-scale fleet expansion plans, airport capacity investments, and national aviation-sector strategies.

What restraints could slow market growth?

Legacy IT silos hinder data integration, and a shortage of aviation-savvy data scientists limits the speed at which complex analytics projects scale globally.

How concentrated is the supplier landscape?

With the top five vendors controlling about half of global revenue, the market shows moderate concentration, leaving opportunities for specialized startups.

Page last updated on: