Low-Cost Carrier Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

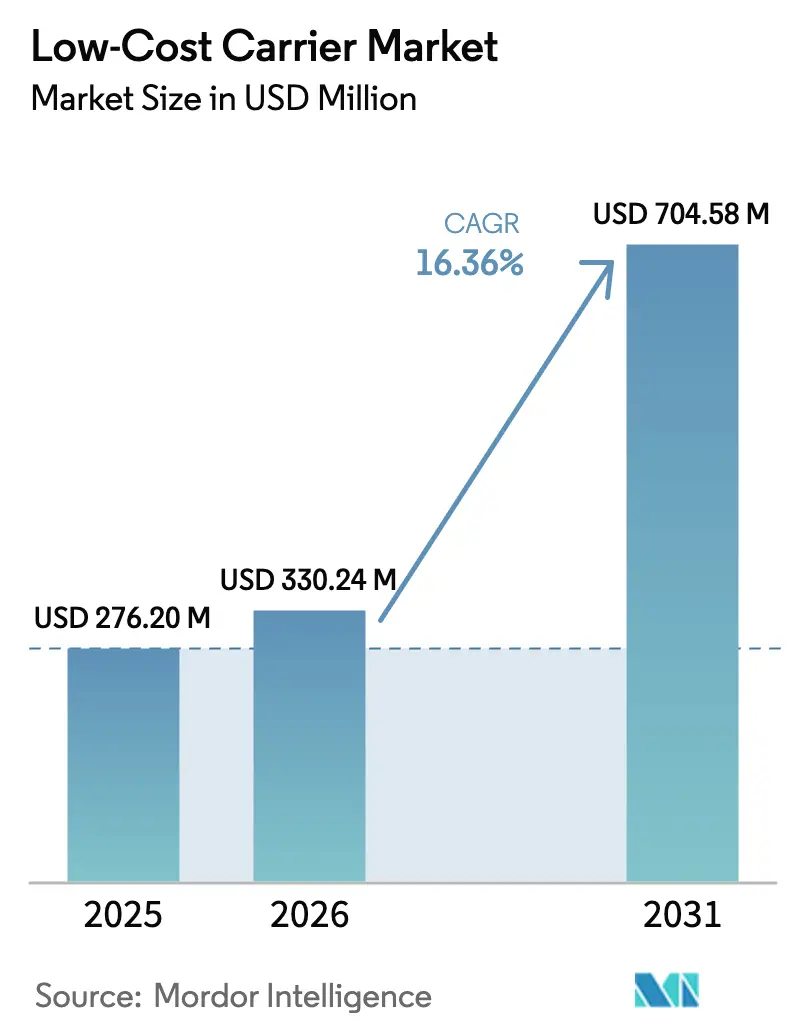

| Market Size (2026) | USD 330.24 Million |

| Market Size (2031) | USD 704.58 Million |

| Growth Rate (2026 - 2031) | 16.36% CAGR |

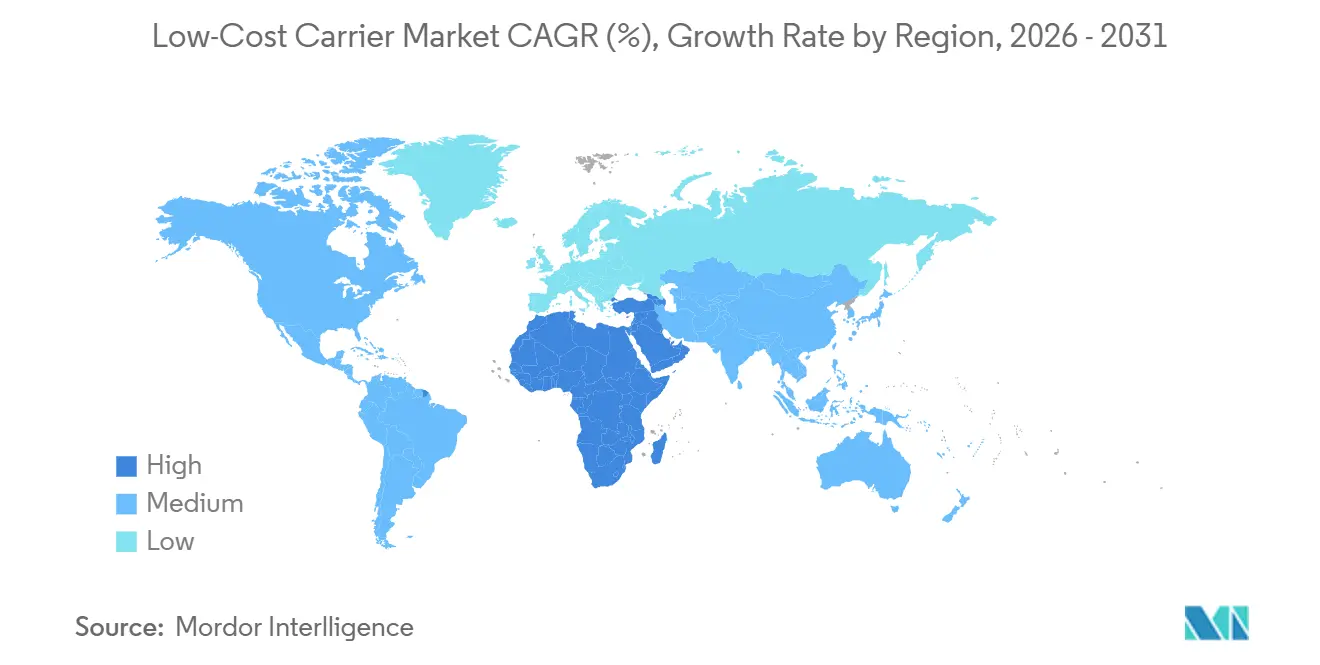

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

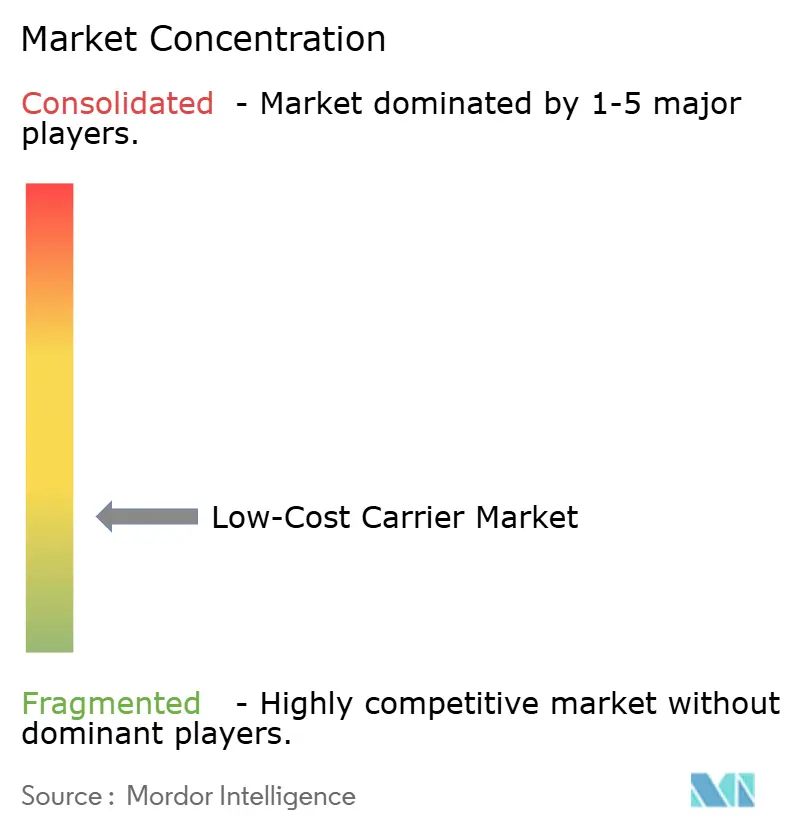

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low-Cost Carrier Market Analysis by Mordor Intelligence

The low-cost carrier market size is expected to grow from USD 276.20 million in 2025 to USD 330.24 million in 2026 and is forecasted to reach USD 704.58 million by 2031 at a 16.36% CAGR over 2026-2031. Sustained leisure and visiting-friends-and-relatives traffic, the shift to single-type narrowbody fleets, and the maturity of ancillary-revenue ecosystems together explain why growth stems from structural change rather than from simple capacity additions. High aircraft utilization keeps unit costs low, secondary airport access cuts landing fees by 30-50%, and liberalized air service agreements unlock new city pairs that bypass congested hubs. Rapid mobile adoption enables carriers to push real-time offers, which now account for 55-62% of total income, transforming the base fare from a volume driver to the primary profit engine. Finally, market leaders are committing to next-generation aircraft even as supply chain constraints tighten, ensuring that cost advantages endure when environmental compliance fees rise.

Key Report Takeaways

- By aircraft type, narrowbody jets led with 82.01% of the low-cost carrier market share in 2025, while widebody operations are advancing at a 16.87% CAGR through 2031.

- By destination, domestic routes accounted for 57.24% of the low-cost carrier market size in 2025, and international services are set to expand at an 18.01% CAGR through 2031.

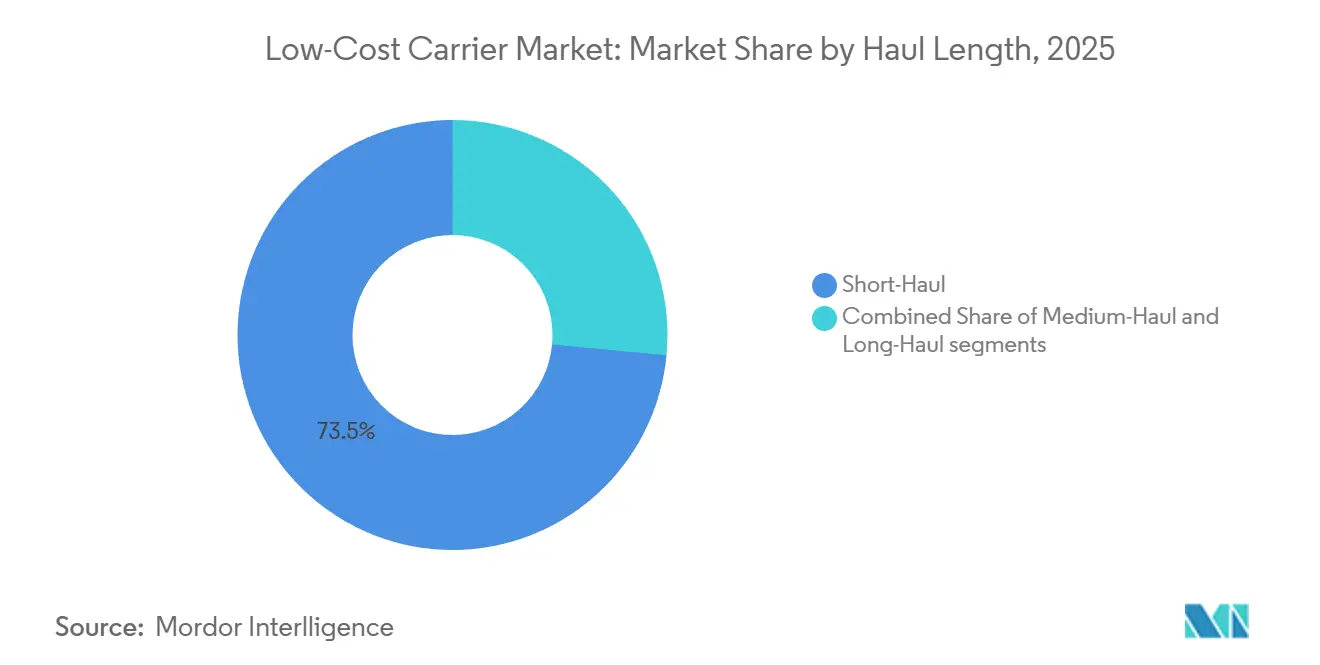

- By haul length, short-haul flying held a 73.49% share of the low-cost carrier market size in 2025; long-haul models are projected to grow at a 17.76% CAGR between 2026 and 2031.

- By distribution channel, direct online bookings captured a 93.22% share in 2025 and are projected to rise at a 17.24% CAGR through 2031.

- By region, Asia-Pacific led with a 34.89% revenue share in 2025, while the Middle East and Africa region is forecasted to post the fastest growth at a 17.43% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low-Cost Carrier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained growth in price sensitive leisure and VFR travel demand | +3.2% | Global, South Asia-Middle East, South America-US, Eastern-to-Western Europe | Long term (≥ 4 years) |

| Single-type fleet strategies enabling cost-efficient narrowbody operations | +2.8% | Global, notably Europe and Asia-Pacific | Medium term (2–4 years) |

| Liberalization of air service agreements expanding point-to-point connectivity | +2.5% | Asia-Pacific, Middle East and Africa, South America | Medium term (2–4 years) |

| High aircraft utilization and quick turnaround operating models | +2.1% | Global | Short term (≤ 2 years) |

| Scalable ancillary revenue ecosystems improving per-seat profitability | +3.0% | Global, led by North and South America | Medium term (2–4 years) |

| Access to low-cost secondary airports supporting ultra-low operating expenses | +1.8% | Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustained Growth in Price-Sensitive Leisure and VFR Travel Demand

Visiting friends and relatives account for 20-30% of international passengers and exhibit higher price elasticity than business travel, steering volumes toward fares that undercut legacy carriers by 30-50%.[1]International Air Transport Association, “Air Transport Statistics 2024-2025,” iata.org India’s middle-class expansion has driven demand for one-way flights under USD 50, pushing IndiGo past 2,000 daily flights by the third quarter of FY2025. High-frequency immigrant corridors, such as the South Asia-Gulf, South America-US, and Eastern-Western Europe, buffer load factors during downturns because the trips are quasi-essential.[2]IndiGo, “Investor Relations Presentations 2024-2025,” goindigo.in Dynamic pricing now splits long weekends across multiple fare buckets, boosting yield without undermining occupancy. The rise of independent travel shifts bookings to direct channels where carriers capture every ancillary dollar. Mobile penetration exceeds 70% at leading low-cost carriers, enabling push offers that monetize seats, bags, meals, and insurance just moments before departure.

Single-Type Fleet Strategies Enabling Cost-Efficient Narrowbody Operations

Operating a single aircraft family simplifies training, parts inventory, and crew-rostering complexity, yielding durable cost advantages. Ryanair’s all-B737 model and Southwest’s B737 focus allow shared pilot pools and minimal standby staff. The A320neo family burns 15-20% less fuel than earlier variants, reducing direct operating expenses by 30-40%. IndiGo secured 500 A320neo-family deliveries in 2023, insulating itself from lease-rate increases as OEM backlogs extend beyond seven years. Uniform cabins reduce ground time; easyJet’s standardized galleys and single-class seats enable sub-30-minute turns, supporting 11-13 hours of daily utilization.

Liberalization of Air-Service Agreements Expanding Point-to-Point Connectivity

Open Skies accords now cover more than 100 US partnerships, removing capacity caps that once shielded flag carriers. The EU–ASEAN Comprehensive Air Transport Agreement, signed in 2022, is eliminating bilateral quotas, allowing low-cost carriers to introduce new non-stop services between Europe and Southeast Asia. Saudi Arabia’s Vision 2030 aims to attract 330 million passengers by 2030 through the licensing of new carriers and the upgrading of secondary airports. China’s Civil Aviation Administration (CAAC) revised traffic-rights rules in 2025 to prioritize secondary international links, opening routes previously reserved for incumbents. Such policies reduce start-up capital and lead times, thereby accelerating network growth for airlines that have spare aircraft and crews.

High Aircraft Utilization and Quick-Turnaround Operating Models

Low-cost operators routinely schedule more than 11 hours of block time daily by minimizing ground dwell and adding overnight red-eye sectors that legacy carriers decline due to crew rest constraints. Ryanair’s 25-minute standard relies on single-class seating, prepaid ground handling, and smaller airports with less congestion. Southwest’s point-to-point network avoids complex bag transfers that delay hub-and-spoke rivals. New tech narrowbodies achieve dispatch reliability of better than 99%, enabling operators to publish tighter rotations without requiring backup aircraft. More cycles per day dilute fixed ownership costs, preserve fare advantages, and protect margins when fuel prices spike.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural aircraft and engine supply chain constraints limiting fleet growth | -2.4% | Global | Short term (≤ 2 years) |

| Rising environmental compliance costs on short-haul aviation | -1.9% | Europe, North America | Medium term (2–4 years) |

| Jet fuel price volatility impacting operating margins | -1.5% | Global | Short term (≤ 2 years) |

| Global pilot and maintenance workforce shortages increasing unit costs | -1.3% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Structural Aircraft and Engine Supply Chain Constraints Limiting Fleet Growth

Airbus planned to deliver up to 800 jets in 2025, yet faced CFM LEAP engine shortages and fuselage quality snags that slowed handovers. Boeing’s B737 MAX line also lagged targets after manufacturing audits, forcing many low-cost carriers to extend leases on older aircraft. Lease rates for A321neo and B737 MAX variants rose more than 15% in 2024–2025, compressing returns when fuel savings fail to offset higher capital costs. With order backlogs stretching back more than 7 years, carriers cannot scale their fleets fast enough to capture demand spikes, thereby throttling market growth.

Rising Environmental Compliance Costs on Short-Haul Aviation

The EU Emissions Trading System will eliminate free allowances for aviation by 2026, requiring airlines to purchase permits priced above EUR 80 (USD 94.22) per ton of CO2. CORSIA similarly mandates offsets for emissions growth above 2019 baselines across 129 states. Sustainable aviation fuel (SAF) costs remain three to five times those of kerosene, and blending mandates in Europe and California force carriers to either absorb the cost or raise fares, threatening price-sensitive traffic. Low-cost carriers often lack the balance-sheet strength to invest directly in SAF production, exposing them to higher compliance costs compared to their diversified legacy peers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbody Dominance With Selective Widebody Upside

Narrowbody jets generated 82.01% of capacity in 2025, underscoring their status as the economic backbone of the low-cost carrier market.[3]Airbus, “Global Market Forecast 2024-2043,” airbus.com They remain crucial because runways, gate sizes, and passenger volumes across secondary airports are tailored to single-aisle operations. The low-cost carrier market size attributable to narrowbodies is projected to keep rising at double-digit rates, fueled by A320neo and B737 MAX deliveries that cut per-trip fuel burn. Order backlogs protect fleet expansion plans through 2031 even under supply chain stress.

Widebody operations, though still niche, are expanding at a robust 16.87% CAGR as the 4,700-nautical-mile A321XLR unlocks long-thin routes such as Rome to Boston and Kuala Lumpur to Tokyo. Airlines like Norse Atlantic and AirAsia X demonstrate that dense, no-frills cabins can deliver sub-USD 200 transoceanic fares when load factors exceed 85%. Success hinges on high aircraft days of use and seat density; Norse’s 338-seat B787 layout spreads ownership costs across more travelers. As utilization improves, the widebody slice of the low-cost carrier market could double by 2031, although slot scarcity at major long-haul airports remains a limiting factor.

By Destination: Domestic Breadth Plus Liberalized International Upside

Domestic services retained a 57.24% share of the low-cost carrier market in 2025 because of regulatory simplicity, quick turnaround times, and the absence of immigration procedures, which make trips under three hours profitable. In the US, Southwest, Frontier, and Allegiant collectively schedule thousands of daily legs, while IndiGo operates more than 2,000 domestic flights across 80 Indian cities. Domestic dominance will persist, but its CAGR lags as saturation sets in mature corridors.

International point-to-point flights are growing at an 18.01% CAGR because bilateral reforms have slashed entry barriers. The low-cost carrier market size for international routes is rising fastest along corridors such as South Asia–Middle East and Europe–Southeast Asia, following the EU–ASEAN pact.[4]European Commission, “EU-ASEAN Comprehensive Air Transport Agreement,” ec.europa.eu Air Arabia, flydubai, and Wizz Air are adding secondary city pairs that network carriers have long overlooked. Liberal policies, combined with the A321XLR's range, will expand this slice of the low-cost carrier market, although visas and currency volatility remain planning challenges.

By Haul Length: Short-Haul Core with Ramping Long-Haul Potential

Flights under three hours accounted for 73.49% of the low-cost carrier market size in 2025, as short sectors enable 25-minute turns and 11 hours of daily utilization. These economics underpin Ryanair’s 183 million passengers in 2023 and keep average base fares below USD 35 on many intra-European routes. Margins remain intact when ancillaries account for more than half of revenue, demonstrating the resilience of the short-haul model.

Long-haul segments exceeding six hours are advancing at a 17.76% CAGR as the A321XLR and low-density long-range narrowbodies close cost gaps. Norse Atlantic’s B787 network demonstrates that dense cabins and secondary US airports, such as Stewart, can yield sustainable unit costs, even if daily cycles decline. The low-cost carrier market share in long-haul is still small, yet it could double this decade as leisure travelers accept tight seating in exchange for fares 35% below those of legacy airlines. Medium-haul (three- to six-hour) services bridge the models, offering flexible aircraft scheduling without overnight crew layovers.

By Distribution Channel: Digital Direct Control Over Yield

Online direct platforms captured a 93.22% share in 2025 due to their mobile-first design, AI-powered fare engines, and real-time ancillary offers, which lower acquisition costs while increasing conversion rates. The low-cost carrier market thrives on this control because every non-ticket product, from seat selection to travel insurance, stays entirely inside the airline’s ecosystem. Travel agency volumes shrink as GDS fees raise total trip costs and dilute revenue shares.

Mobile apps now handle more than 70% of direct bookings at Ryanair and Southwest, letting airlines push upgrades, bags, and lounge passes with personalized messaging. NDC promises cheaper API links for agencies, yet most low-cost carriers resist partial control. Online direct sales will likely exceed 95% by 2031, giving carriers complete visibility into search and purchase data, a critical asset for dynamic pricing and loyalty targeting within the low-cost carrier industry.

Geography Analysis

Asia-Pacific held 34.89% of the low-cost carrier market in 2025, anchored by India’s double-digit domestic growth and Southeast Asia’s open-skies reforms. However, engine shortages limit aircraft additions, creating pent-up demand that supports fare strength. China’s Spring Airlines, Cebu Pacific, and VietJet continue to expand their regional routes, which bypass hubs such as Bangkok and Kuala Lumpur.

The Middle East and Africa region is the fastest growing, with a 17.43% CAGR to 2031, as Vision 2030 deregulation spurs new entrants and secondary airport upgrades in Saudi Arabia. flydubai’s 150-plane B737 MAX order underscores ambition to link underserved city pairs across Africa and South Asia. In Europe, mature penetration slows growth, but not competition; Ryanair, easyJet, and Wizz Air, together, control more than 40% of intra-European ASKs, yet still chase niche, secondary city pairs.

North America witnessed Spirit Airlines’ November 2024 Chapter 11 filing, following its blocked merger with JetBlue, which opened up valuable slots for rivals and signaled a regulatory determination to preserve fare competition. South America remains fragmented as carriers navigate currency fluctuations and fuel cost spikes, although Volaris and Viva Aerobus continue to expand cross-border into the US. Overall, geographic divergence influences the risk-reward profiles within the global low-cost carrier market.

Competitive Landscape

The low-cost carrier market remains fragmented due to regulatory barriers that confine most carriers to their home regions. Ryanair leads Europe with 183 million passengers in 2023, while Southwest tops the US with more than 140 million. IndiGo controls 60% of India's domestic seats; however, none of these airlines hold 10% of the worldwide capacity. The competitive moat stems from cost leadership, ancillary depth, and secondary-airport access. Frontier and Spirit monetize more than half of their revenue through ancillaries, whereas Southwest differentiates itself with free checked bags, despite remaining firmly within the low-cost carrier model.

Technology investment widens performance gaps. Ryanair's mobile penetration exceeds 80%, enabling AI-driven personalization that promotes in-app seat upgrades and car rentals. Wizz Air deploys machine-learning tools to adjust fares up to 200 times per day based on search patterns, competitor prices, and historical curves. Biometric boarding and RFID bag tracking trim turnaround times, preserving aircraft utilization above 11 hours even at slot-restricted airports.

Strategic fleet planning also diverges. IndiGo's September 2024 purchase of 30 A350-900 jets signals a long-haul challenge to state carriers on India–Europe and India–North America routes. flydubai's B737 MAX order aims to enhance connectivity in Central Asia and East Africa, complementing Emirates' widebody network. Norse Atlantic, Zipair, and AirAsia X are pursuing widebody low-cost carrier models on leisure-heavy corridors that legacy alliances deprioritized, exemplifying white-space exploitation in the low-cost carrier industry.

Low-Cost Carrier Industry Leaders

Southwest Airlines Co.

Ryanair

easyJet PLC

Indigo (InterGlobe Aviation Limited)

Wizz Air Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IndiGo signed an agreement with Norse Atlantic Airways, a Norwegian low-cost carrier, for the damp leasing of two B787 Dreamliner aircraft, expanding its widebody fleet.

- May 2024: Travelport, a global travel technology company that processes bookings for travel suppliers worldwide, renewed its LCC content agreement with flynas, a major low-cost airline in the Middle East.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

In our study, Mordor Intelligence defines the low-cost carrier (LCC) market as the worldwide ticket and ancillary revenue earned by scheduled airlines that operate single-class, point-to-point services, use a lean cost structure, and charge separately for optional conveniences. We track only commercial passenger flights operated by jet aircraft and converted passenger freighters.

Scope Exclusion: charter-only flights, cargo-only operators, and turboprop commuter services lie outside this analysis.

Segmentation Overview

- By Aircraft Type

- Narrowbody

- Widebody

- By Destination

- Domestic

- International

- By Haul Length

- Short-Haul

- Medium-Haul

- Long-Haul

- By Distribution Channel

- Online Direct

- Travel Agency

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview airline revenue-management executives, aircraft lessors, and online travel agency leaders across North America, Europe, Asia-Pacific, and the Middle East. These conversations validate ancillary penetration, average stage length, and expected capacity additions, helping us refine assumptions that could never be confirmed by desk work alone.

Desk Research

Our team begins with global aviation traffic statistics from sources such as the International Civil Aviation Organization, IATA's World Air Transport Report, and regional regulators that release passenger-kilometer data. We then gather fleet delivery, utilization, and fuel price trends from Airbus, Boeing, and Eurocontrol dashboards, which are invaluable for cost benchmarks.

Company filings, airline investor presentations, airport authority throughput sheets, and trade association briefs (Airlines for America, ACI World, CAPA insights) help us narrow typical fares, ancillary share, and load factors by region. Subscription databases like D&B Hoovers and Dow Jones Factiva are tapped for historical revenue splits and news on surcharge policies. This list is illustrative; many additional sources support data collection and cross-checks.

Market-Sizing & Forecasting

The model starts with a top-down build: global scheduled passenger revenue is reconstructed, then filtered through LCC seat-capacity share, region-specific load factors, and ancillary-to-ticket ratios. Select bottom-up checks, sampled airline revenues and aircraft counts multiplied by stage length and average seat-kilometer yields, calibrate totals.

Key variables include jet fuel spot prices, delivered A320neo/B737 MAX counts, digital booking penetration, and government tourism indices, each influencing cost per available seat-mile and fare elasticity. A multivariate regression with these drivers projects revenue through 2030, while scenario analysis handles swings in fuel and taxation. Where bottom-up samples fall short, we adjust using median variance from audited carriers in similar markets.

Data Validation & Update Cycle

Draft outputs go through variance checks against independent passenger data, analyst peer reviews, and anomaly resolution before sign-off.

Reports refresh yearly, and any material event, such as fleet groundings, open-skies pacts, or sudden tax hikes, triggers an interim update so clients receive the freshest view.

Why Mordor's Low-Cost Carrier Baseline Proves Dependable

Published market values often diverge because each firm selects distinct service scopes, fare definitions, and refresh cadences.

Key gap drivers include whether charter and cargo revenue is folded into totals, how ancillary sales are treated, the vintage of fleet data, and currency conversion dates. Mordor favors current-year airline filings, excludes non-passenger revenue, and refreshes annually, whereas many publishers rely on broader IATA aggregates or older averages, creating wider figures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 287.95 million (2025) | Mordor Intelligence | |

| USD 320.61 billion (2025) | Global Consultancy A | Includes charter and cargo revenue, gross fare without ancillary split |

| USD 316.97 billion (2024) | Trade Journal B | Uses passenger volume × average fare and 2023 fleet data |

The comparison shows that numbers swing widely when scope or inputs drift. By anchoring estimates to audited airline revenue streams, timely capacity data, and clearly documented exclusions, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to reproducible steps.

Key Questions Answered in the Report

How large is the low-cost carrier market in 2026?

The low-cost carrier market size stood at USD 330.24 million in 2026 and is projected to more than double to USD 704.58 million by 2031.

Which aircraft type dominates capacity?

Narrowbody jets, led by A320neo and B737 MAX families, accounted for 82.01% of deployed capacity in 2025.

What is driving long-haul LCC growth?

The A321XLR’s extended range and widebody density models such as the B787 enable profitable transoceanic routes at fares 30–40% below legacy carriers.

Why are ancillary revenues important?

Leading LCCs derive 55–62% of revenue from ancillaries, allowing base fares to stay ultra-low while preserving margins.

What are the biggest restraints facing the sector?

Supply chain delays on new aircraft and tightening environmental levies on short-haul flights currently subtract an estimated 4.3 percentage points from otherwise higher growth momentum.

Which region will grow fastest to 2031?

The Middle East and Africa is forecasted to register a 17.43% CAGR as liberalization and secondary-airport upgrades unlock new demand.

Page last updated on: