Flight Simulator Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

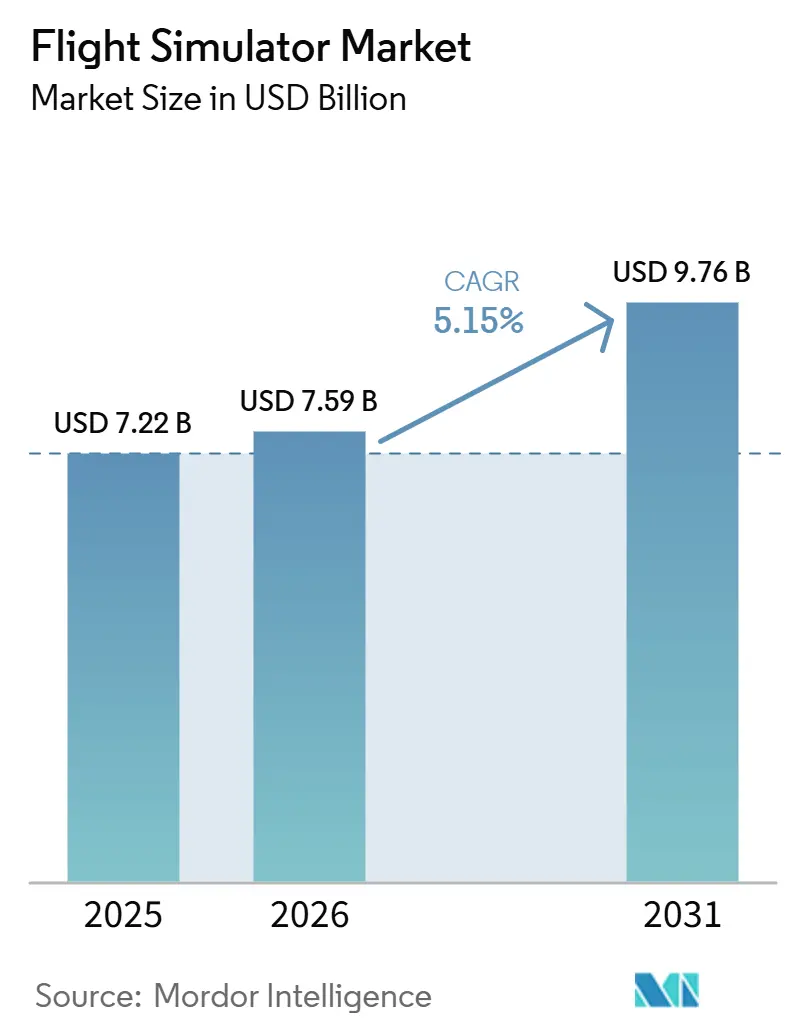

| Market Size (2026) | USD 7.59 Billion |

| Market Size (2031) | USD 9.76 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

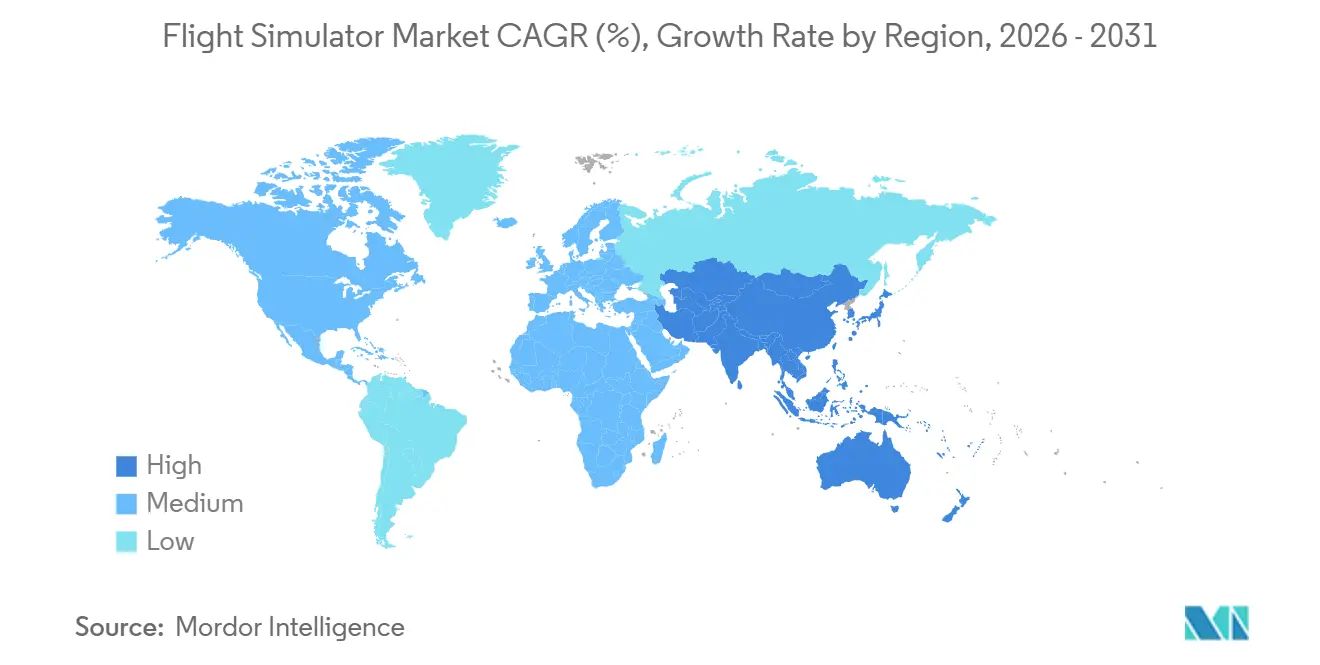

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

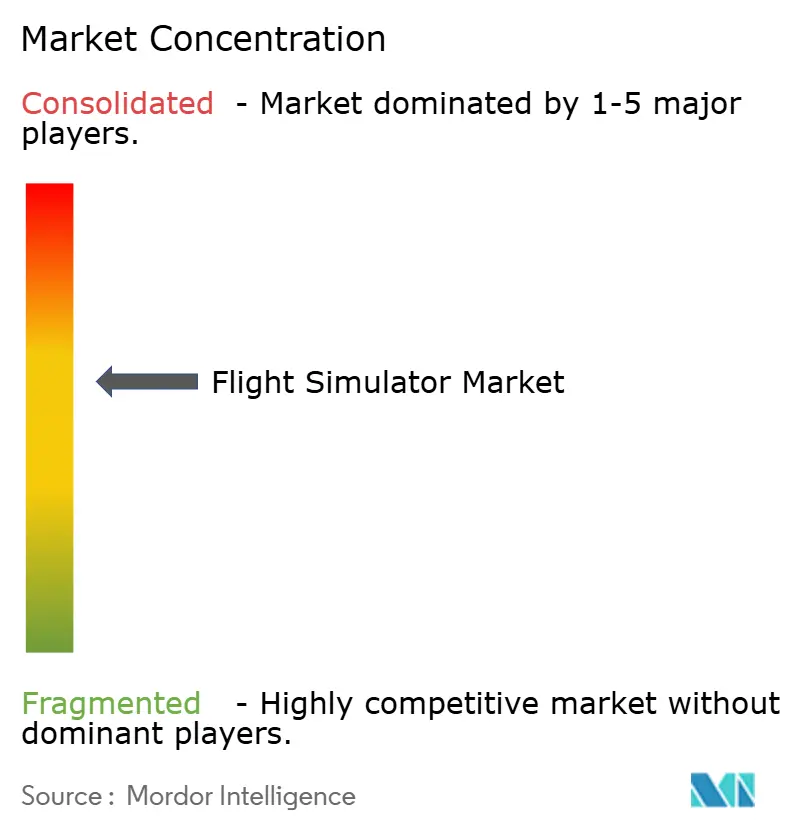

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flight Simulator Market Analysis by Mordor Intelligence

The flight simulator market size is expected to grow from USD 7.22 billion in 2025 to USD 7.59 billion in 2026 and is forecast to reach USD 9.76 billion by 2031 at a 5.15% CAGR over 2026-2031. Mandatory training regulations, a widening pilot shortage, and the shift toward advanced air-mobility platforms keep demand on a steady, structural growth path even as post-pandemic catch-up spending fades. Airlines and militaries are modernizing curricula around competency-based frameworks, prompting sustained investment in immersive technologies that compress training cycles while protecting safety margins. Service-oriented business models increasingly dominate procurement, insulating operators from upfront capital burdens and allowing suppliers to monetize lifetime support. Regionally, North America maintains scale leadership, yet Asia-Pacific shows the fastest capacity build-out as India and China race to staff their record aircraft backlogs. Consolidation among top vendors is accelerating as companies seek vertical integration that bundles hardware, software, and training analytics into a single outcome-based offering.

Key Report Takeaways

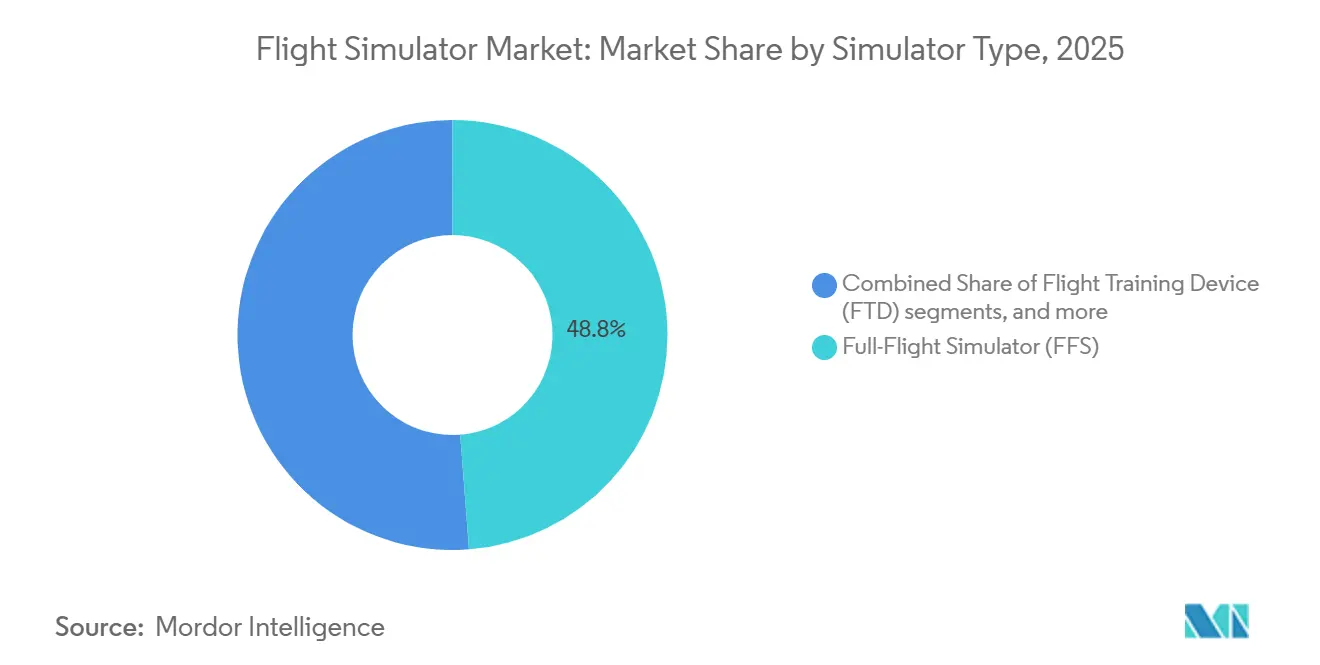

- By simulator type, full flight simulators (FFS) captured 48.78% of the flight simulator market share in 2025, while mixed- or virtual-reality procedural trainers are projected to grow at a 7.23% CAGR through 2031.

- By aircraft platform, fixed-wing devices held a 59.92% share of the flight simulator market in 2025, yet the advanced air mobility/eVTOL category is forecast to grow at a 9.42% CAGR through 2031.

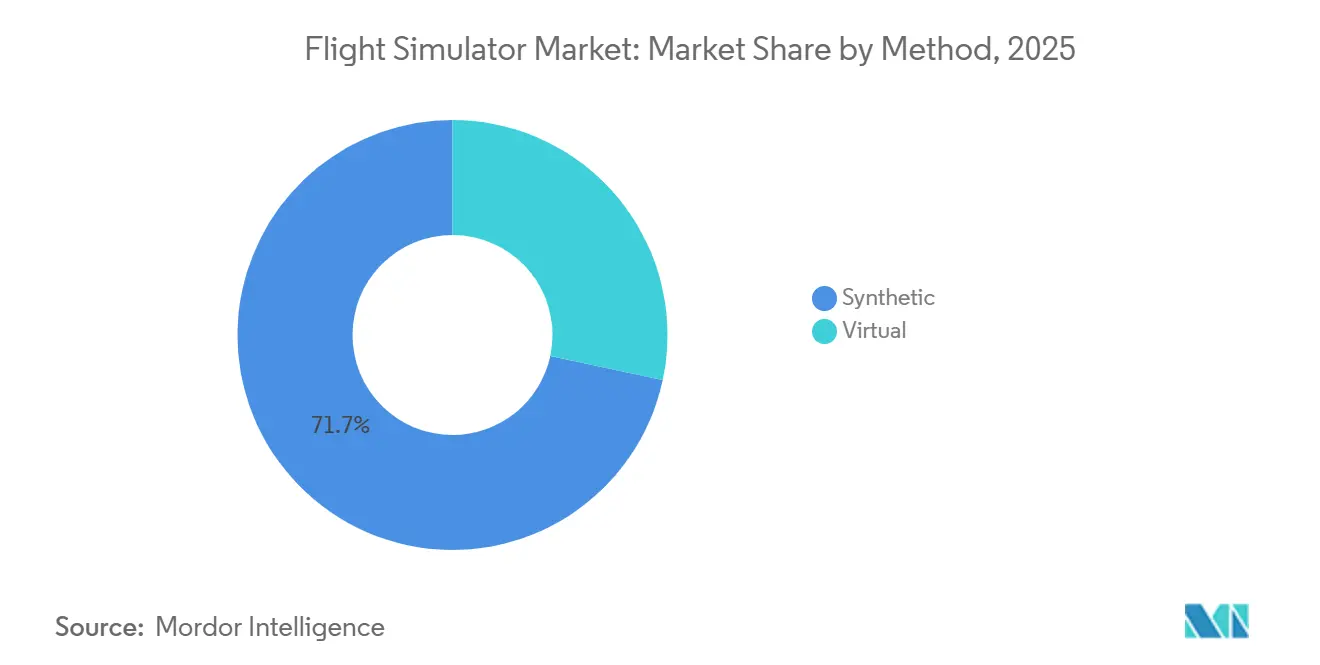

- By training solution, synthetic environments accounted for 71.65% revenue share in 2025, and virtual solutions are projected to grow at a 7.78% CAGR through 2031.

- By end-user, commercial aviation accounted for 45.24% of the flight simulator market in 2025, whereas military aviation is forecast to grow at a 6.45% CAGR through 2031.

- By geography, North America led with 39.45% revenue share in 2025; Asia-Pacific is projected to grow at a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flight Simulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID pilot-shortage accelerating simulator demand | +1.20% | North America, Asia-Pacific | Medium term (2-4 years) |

| Defense shift to Live-Virtual-Constructive (LVC) training | +0.90% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Mandatory upset-recovery and MPL curriculum adoption | +0.80% | Global | Long term (≥ 4 years) |

| Fleet renewal toward composite and e-propulsion aircraft | +0.60% | North America, European Union | Long term (≥ 4 years) |

| eVTOL type-rating regulations (Part 419) | +0.40% | North America initially, global later | Long term (≥ 4 years) |

| AI-enabled adaptive training analytics | +0.30% | Developed markets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-COVID Pilot Shortage Accelerating Simulator Demand

Global pilot pipelines remain stressed even after temporary hiring pauses, keeping full-motion device utilization at record levels. Regional carriers in the US report fewer resignations but cannot meet long-term cockpit staffing needs as fleet growth outpaces training capacity. Australia lost 25,000 aviation workers during the pandemic, forcing Boeing Australia to double the number of technician apprenticeship slots to maintain maintenance schedules. India’s plan for more than 50 new academies underscores how emerging markets institutionalize simulators to close a projected 30,000-pilot gap within 15–20 years. These structural shortages boost recurring demand for both initial and recurrent training devices, anchoring revenue visibility across the flight simulator market.

Mandatory Upset Recovery and MPL Curriculum Adoption

Regulators have codified upset-prevention and recovery training, transforming what was once best practice into a legal obligation. The International Civil Aviation Organization’s (ICAO's) competency-based template now guides FAA and EASA rulemaking, embedding high-fidelity simulation into core syllabi.[1]Airbus, “Is CBTA the Future of Pilot Training?” aircraft.airbus.com Multi-Crew Pilot License (MPL) pathways further compress live-flight hour requirements, redirecting training budgets toward full-motion and mixed-reality devices replicating complex scenarios. Airlines adopting CBTA frameworks report measurable gains in flight path management and crew resource management skills, reinforcing demand for simulators across recurrent cycles.

Fleet Renewal Toward Composite and E-Propulsion Aircraft

Operators are phasing in composite and electric-propulsion fleets that behave very differently from legacy metal airframes. Pilots must master new energy-management techniques, automation layers, and envelope protections long before line operations begin, so OEMs now embed high-fidelity simulators in every certification program. The FAA’s powered-lift regulations formalize this need by requiring dedicated type-rating courses for eVTOL crews, locking in a predictable block of simulator hours per pilot. Airlines are therefore accelerating the replacement of devices that cannot replicate glass cockpits, fly-by-wire logics, or electric power-loss scenarios. Training centers report that demand for retrofits and new mixed-reality rigs already exceeds pre-pandemic peaks, creating multi-year backlogs for visual and motion subsystems. As composite and e-propulsion programs scale, the flight simulator market gains a durable stream of refresh orders that decouple revenue from the airline traffic cycle.

Defense Shift to Live-Virtual-Constructive Training

Modern threat environments require aircrews to rehearse integrated air, land, sea, space, and cyber missions without the expense of full live-force deployments. The US Navy’s roadmap targets seamless detection and engagement of synthetic adversaries by 2035, effectively mandating networked simulators for every carrier air wing. Boeing, Cubic, and Patria have already demonstrated interoperable LVC suites that link real jets to virtual assets and constructive targets, slashing fuel burn while expanding the variety of scenarios. NATO partners are now incorporating LVC credit into readiness metrics, which elevates procurement from discretionary status. Secure data links, latency controls, and cyber-hardened gateways become critical differentiators, steering contracts toward suppliers with proven multi-domain architectures. These dynamics embed sustained growth for networked simulators as defense ministries substitute expensive flight hours with agile synthetic sorties.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain constraints on visual-display collimators | -0.70% | North America, EU | Short term (≤ 2 years) |

| Rising cyber-hardening certification costs (DO-326A) | -0.50% | Global | Medium term (2-4 years) |

| Mid-tier flight schools’ capital-access squeeze | -0.40% | North America, EU | Short term (≤ 2 years) |

| Increasing availability of low-cost PC-based sims | -0.30% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Constraints on Visual Display Collimators

High-fidelity Level D devices rely on precision optics built by several suppliers. Delivery of collimated display assemblies is slipping as aerospace primes pull critical components into their programs, delaying acceptance tests and inflating backlogs.[2]FlightSafety International, “FlightSafety Simulation,” flightsafety.com An industry survey found that 60% of tier-2 avionics vendors cited the B737 MAX production ramp as the single largest bottleneck, dragging down deliveries across the training device ecosystem. The shortage inflates unit prices and forces OEMs to prioritize airline contracts over flight-school orders, slowing adoption of mixed-reality trainers that rely on the same projection glass. Some operators resort to interim retrofits that fall short of FAA Level-D fidelity, delaying regulatory approvals and revenue service. Unless new suppliers enter the optics niche, these constraints will cap near-term growth despite strong demand signals.

Rising Cyber-Hardening Certification Costs (DO-326A)

Simulators increasingly connect to cloud analytics, airline IP networks, and defense training ranges, making them subject to aviation-grade cybersecurity rules. The FAA’s proposed Equipment, Systems, and Network Information Security Protection rule, aligned with EASA ED-202A guidance, obliges manufacturers to document threat assessments and life-cycle mitigations for every connected component. Compliance adds specialized engineering, penetration testing, and recurrent audit costs that smaller builders cannot spread across large fleets. Airlines fear downtime due to evolving security patches, so they gravitate toward providers offering turnkey cyber-maintenance services. These factors accelerate consolidation and favor vertically integrated vendors with in-house security labs. As AI analytics and remote-update functions proliferate, cyber-hardening will remain a rising cost curve that suppliers must either absorb or pass through to customers, constraining margins in price-sensitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Simulator Type: Mixed Reality Drives Training Evolution

Full-flight simulator (FFS) retained 48.78% of 2025 revenue, yet mixed- and virtual-reality procedural trainers are pacing the flight simulator market with a 7.23% CAGR, signaling operator confidence in immersive technologies for non-maneuver tasks. The cost of a compact VR trainer can be a fraction of that of a full-motion device, enabling airlines to deploy multiple units at crew bases and reduce travel overhead. Alaska Airlines’ investment in Loft Dynamics VR B737 platforms exemplifies the shift, with installations planned at several hubs pending FAA sign-off.

Immersive headsets paired with motion-cueing now deliver sufficient fidelity for cockpit familiarization and emergency drills, freeing scarce Level D capacity for final proficiency checks. The FAA’s joint program with Vertex Solutions and Varjo to develop XR standards should streamline certification pathways, accelerating adoption among regional carriers and flight schools. As device prices fall and software ecosystems mature, mixed-reality trainers will capture a larger market share in the flight simulator market by the early 2030s.

By Aircraft Platform: eVTOL Creates New Training Paradigms

Fixed-wing devices commanded 59.92% of the 2025 flight simulator market size on the back of commercial airline demand, but the eVTOL segment is slated for the fastest expansion at 9.42% CAGR. FAA Part 419 establishes a new type-rating regime for powered-lift aircraft, making simulator hours a prerequisite for airline-style urban air mobility (UAM) operations. CAE’s 700MXR leverages mixed-reality visuals, compact six-axis motion, and AI traffic generators to create urban environment scenarios that legacy helicopter simulators cannot replicate.

Rotary-wing and unmanned platforms continue to see steady demand for replacement, particularly in utility missions and offshore support. Militaries also pool fighter and drone simulators into common LVC networks, boosting cross-domain proficiency and squeezing incremental efficiencies from tight defense budgets. Still, eVTOL remains the headline growth story, and suppliers that can validate training devices ahead of Type Certification are positioned to win early-adopter contracts.

By Training Solution: Virtual Training Gains Acceptance

Synthetic environments dominated 2025 revenues, accounting for 71.65% of spend; however, pure virtual methods delivered via distributed PCs or the cloud are growing fastest, at a 7.78% CAGR. Airlines used pandemic downtime to trial remote recurrent programs and discovered measurable reductions in dead-head travel and roster disruptions. Scientific literature shows strong pilot acceptance of medium-fidelity desktop devices for routine and abnormal procedure rehearsal, particularly when augmented reality overlays are added to reinforce spatial cues.

Regulators remain cautious, limiting credit for purely virtual hours; however, the line between virtual and synthetic is blurring as head-tracking and haptic feedback improve. Airlines now sequence training so that procedural skill-building happens remotely, with Level D sessions focused on maneuver validation and upset recovery. This model optimizes scarce capacity in the flight simulator market while trimming total program cost.

By End-User: Commercial Aviation Leads, Military Aviation to Witness Rapid Growth

The commercial aviation segment accounted for 45.24% of the market share and is expected to remain the largest end-user in the flight simulator market through the end of the forecast period. Sustained growth in global air travel, expanding commercial aircraft fleets, and the need to address pilot shortages are driving investments in advanced full-flight simulators for type rating, recurrent training, and competency-based instruction. These simulators also help reduce operational costs, fuel consumption, and environmental impact associated with live-flight training. Advancements in AI-enabled training analytics, VR, MR, and cloud-based simulation platforms are enhancing training effectiveness and accessibility. Growth may be constrained by high capital investment requirements, lengthy certification processes, and fluctuations in airline profitability, which can delay investments in training infrastructure.

The military aviation segment is projected to grow at the fastest rate, with a 6.45% CAGR during the forecast period, driven by rising defense expenditures, military modernization initiatives, and the procurement of next-generation aircraft and unmanned aerial systems. Armed forces are adopting simulation technologies for mission rehearsal, tactical training, electronic warfare, and LVC environments to improve operational readiness while reducing costs and risks. Growing emphasis on networked simulation, digital twins, and AI-powered mission planning is expected to further accelerate demand. Budgetary constraints, long procurement cycles, cybersecurity concerns, and challenges integrating new platforms with legacy infrastructure may limit expansion.

The civil aviation segment, encompassing general aviation, flight training academies, business aviation, government agencies, and research institutions, is expected to grow steadily. Rising demand for pilot training, increasing business jet and helicopter operations, and growing UAV operator training are supporting this growth. Regulatory emphasis on aviation safety and competency-based training, along with more affordable fixed-base and virtual simulators, is encouraging adoption among smaller operators and educational institutions. Limited training budgets, lower purchasing power among small flight schools, and slower technology adoption in developing markets may moderate growth.

Geography Analysis

North America retained 39.45% of 2025 spending thanks to entrenched airline hubs, military budgets, and FAA regulatory sway. Yet Asia-Pacific is slated to post 7.12% CAGR as Indian and Chinese carriers induct thousands of narrowbodies and retirees drive attrition across regional fleets. Domestic training capacity is racing to catch up, prompting joint ventures with global providers and government incentives for greenfield academies.

Europe remains a steady contributor, propelled by Airbus’s new Toulouse campus, which will train 10,000 personnel annually and house 12 FFS. The Middle East continues to invest in hub-based training centers aligned with its global airline strategy. At the same time, Africa and South America progress more slowly as economic volatility affects capital flows. Nevertheless, local regulators are aligning with ICAO standards, opening the door to new training partnerships that will expand the addressable flight simulator market over the next decade.

Competitive Landscape

The glight simulator market shows moderate consolidation, with the top five vendors accounting for an estimated 55–60% of global revenue, resulting in an overall concentration score of 6. CAE’s USD 1.05 billion takeover of L3Harris’s Military Training unit broadened its reach across the land, sea, space, and cyber domains, adding economies of scale that drive price competition.[3]CAE, “CAE to Acquire L3Harris Military Training,” cae.com L3Harris’s divestiture of its Commercial Aviation Solutions arm (now Acron Aviation) introduces a focused mid-cap challenger in avionics and civil simulators.[4]FlightGlobal, “Acron Aviation Emerges,” flightglobal.com

Technology plays are redefining rivalry. Vertex Solutions, Varjo, and Aechelon collaborate with the FAA on XR standards, gaining early access to regulatory insights that can translate into a competitive advantage once guidelines are finalized. Loft Dynamics targets narrow niches with compact full-motion VR rigs, securing equity from Alaska Airlines to accelerate B737 productization.

Strategic moves emphasize service synergies. CAE increased its stake in SIMCOM and signed a long-term exclusive training agreement with Flexjet, strengthening its presence in business aviation. HAVELSAN secured repeat orders from Turkish Airlines for B737 MAX devices, signaling Türkiye’s growing domestic capability. Collectively, these developments suggest that incumbents will continue to integrate hardware, content, and analytics to protect margins and deter new entrants.

Flight Simulator Industry Leaders

CAE Inc.

The Boeing Company

FlightSafety International Inc.

L3Harris Technologies, Inc.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: The Airports Authority of India (AAI) announced its plans to enter the pilot training ecosystem by establishing FFS and Type Rating Training Organization facilities across its airport network in India.

- June 2025: HAVELSAN, a flight simulator manufacturer based in Ankara, Türkiye, received a new order from Turkish Airlines for a B737 MAX full flight simulator, with delivery scheduled for January 2026.

- February 2025: Rheinmetall will supply C-390 flight simulators to the Royal Netherlands Air Force under a contract with Embraer. The contract includes a full flight and mission simulator and a Cargo Handling Station Trainer. The production of these simulators will commence immediately, with delivery expected by the end of 2026. The contract value exceeds EUR 10 million (USD 11.59 million) and was recorded in Q1 2025.

Global Flight Simulator Market Report Scope

A flight simulator is designed to train aircraft pilots and crew members by simulating flight conditions. Simulation-based training involves using essential equipment or computers to model real-world scenarios. During training, the pilot learns to perform specific tasks or activities in various circumstances. Simulation is also helpful for reviewing and training pilots with new modifications to existing craft. Simulation software in the market delivers a robust virtual environment for analyzing, testing, and optimizing processes, systems, and operations.

The flight simulator market is segmented by simulator type, aircraft platform, training solution, end-user, and geography. By simulator type, the market is segmented into full-flight simulator (FFS), flight training device (FTD), fixed-base and desktop trainer, and mixed- or virtual-reality procedural trainer. By aircraft platform, the market is segmented into fixed-wing, rotary-wing, unmanned aerial vehicle (UAV), and advanced air mobility/eVTOL. BY training solution, the market is segmented into synthetic and virtual. By end-user, the market is segmented into commercial aviation, civil aviation, and military aviation. The report also covers the market sizes and forecasts for the flight simulator market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Full-Flight Simulator (FFS) |

| Flight Training Device (FTD) |

| Fixed-Base and Desktop Trainer |

| Mixed- or Virtual-Reality Procedural Trainer |

| Fixed-Wing |

| Rotary-Wing |

| Unmanned Aerial Vehicle (UAV) |

| Advanced Air Mobility/eVTOL |

| Synthetic |

| Virtual |

| Commercial Aviation |

| Civil Aviation |

| Military Aviation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Simulator Type | Full-Flight Simulator (FFS) | ||

| Flight Training Device (FTD) | |||

| Fixed-Base and Desktop Trainer | |||

| Mixed- or Virtual-Reality Procedural Trainer | |||

| By Aircraft Platform | Fixed-Wing | ||

| Rotary-Wing | |||

| Unmanned Aerial Vehicle (UAV) | |||

| Advanced Air Mobility/eVTOL | |||

| By Training Solution | Synthetic | ||

| Virtual | |||

| By End-User | Commercial Aviation | ||

| Civil Aviation | |||

| Military Aviation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the flight simulator market in 2026?

The flight simulator market size reached USD 7.59 billion in 2026 and is projected to grow to USD 9.76 billion by 2031 at a 5.15% CAGR over 2026-2031.

Which simulator segment is expanding the fastest?

Mixed- or Virtual-Reality Procedural Trainers lead growth at a 10.23% CAGR as operators adopt immersive technologies for procedural training.

Why is Asia-Pacific a priority region for vendors?

Rapid fleet expansion and a forecasted need for 30,000 new pilots over the next 15 years are driving 7.12% CAGR growth in Asia-Pacific demand.

What is the main restraint facing manufacturers?

Supply-chain delays for high-fidelity visual collimators are extending delivery schedules and elevating costs for Level D devices.

How are service models changing procurement?

Airlines prefer long-term, outcome-based contracts that bundle equipment, maintenance and analytics, shifting revenue from hardware to services.

Will eVTOL operations boost simulator demand?

Yes; FAA type-rating rules for powered-lift aircraft lock in simulator hours and fuel a 9.42% CAGR for eVTOL training devices.

Page last updated on: