Aviation Crew Management Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.34 Billion |

| Market Size (2030) | USD 4.85 Billion |

| Growth Rate (2025 - 2030) | 7.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

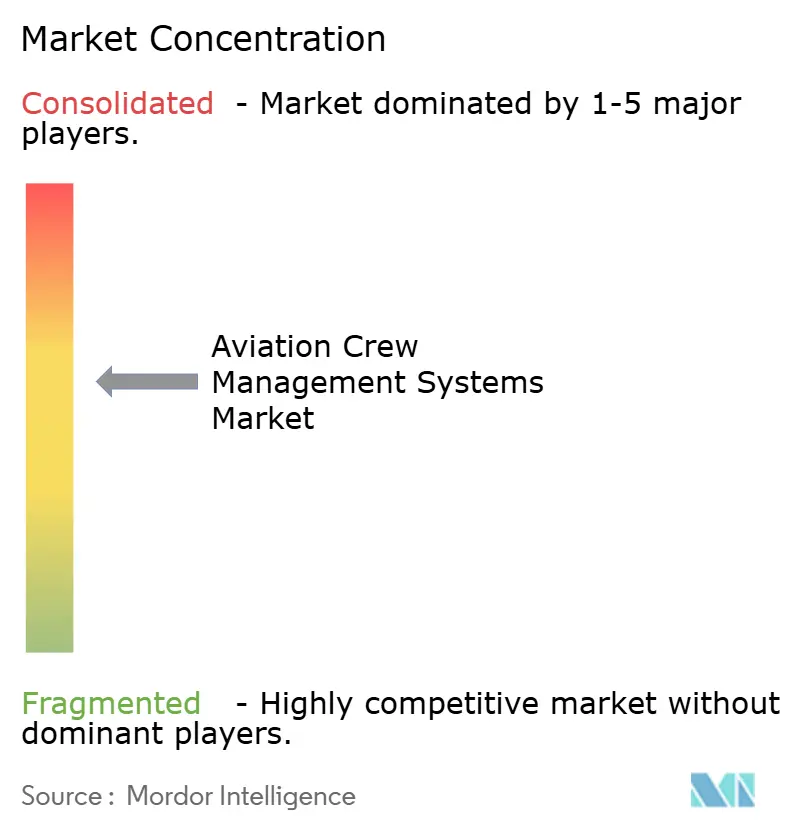

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Crew Management Systems Market Analysis by Mordor Intelligence

The aviation crew management systems market size stood at USD 3.34 billion in 2025 and is expected to advance to USD 4.85 billion by 2030, reflecting a 7.75% CAGR. Strong enterprise demand for cloud-native platforms, rising regulatory scrutiny of crew fatigue, and AI-enabled disruption management are sustaining double-digit technology spending by airlines. Vendors are racing to consolidate adjacent capabilities planning, training, and day-of-operations control into suites that cut manual work and improve crew utilization. Strategic acquisitions, such as CAE’s purchase of Sabre’s AirCentre portfolio, have shifted competitive dynamics. At the same time, Boeing’s divestiture of Jeppesen to Thoma Bravo underscores the value investors assign to data-rich aviation software assets. Airlines n ow view modern crew platforms as mission-critical for cost control, schedule reliability, and employee well-being.

Key Report Takeaways

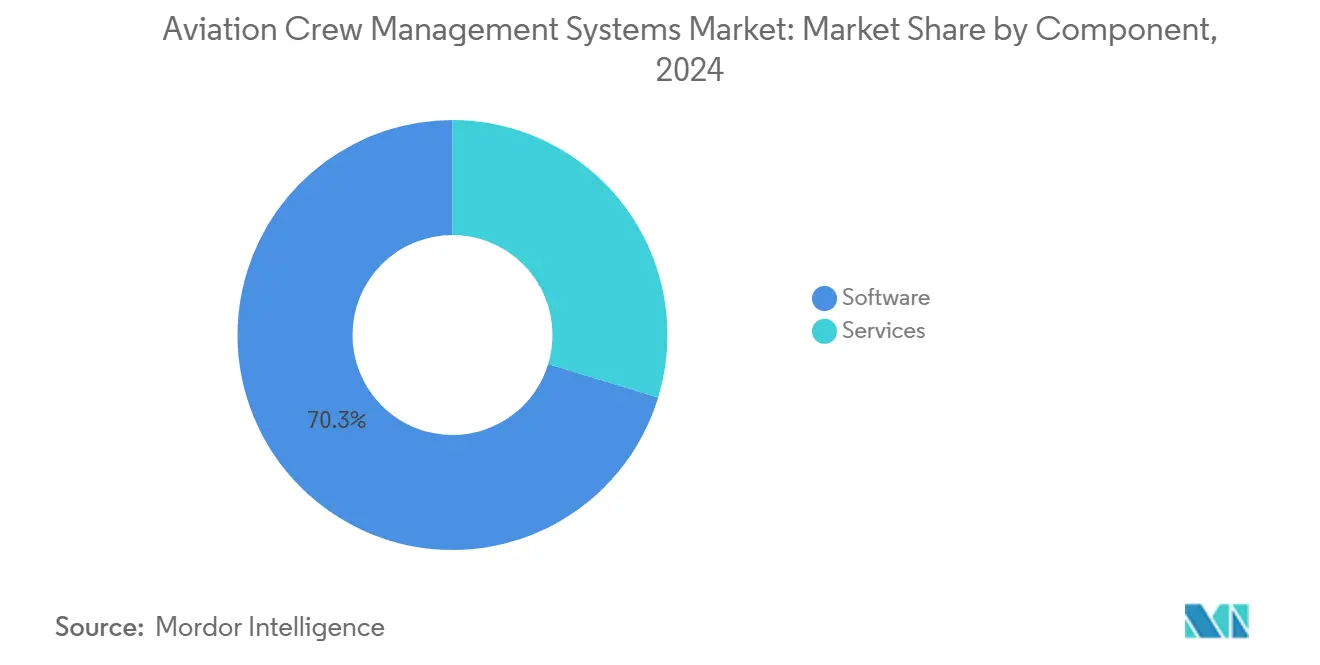

- By component, software led with 70.30% of the aviation crew management systems market share in 2024, whereas services are projected to post the fastest 9.30% CAGR through 2030.

- By deployment, cloud captured 67.82% of the aviation crew management systems market size in 2024 and is also forecasted to expand at the highest 9.56% CAGR to 2030.

- By airline type, passenger airlines commanded a 69.90% share of the aviation crew management systems market in 2024, while cargo airlines are set to advance at a 9.21% CAGR over the outlook period.

- By application, planning applications held a 40.50% share of the aviation crew management systems market size in 2024, and training applications are projected to grow at a 10.54% CAGR to 2030.

- By geography, North America accounted for 35.65% of the aviation crew management systems market share in 2024, whereas Asia-Pacific is poised for the quickest 10.20% CAGR up to 2030.

Global Aviation Crew Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud‐first migration across airline IT stacks | +2.1% | Global, early adoption in North America and EU | Medium term (2–4 years) |

| Stricter fatigue and flight-time limitation rules (FAA, EASA, CAAC) | +1.8% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Integrated operations-control suites replacing stand-alone tools | +1.5% | Global, major airline hubs | Medium term (2–4 years) |

| AI-powered predictive disruption management | +1.2% | North America and APAC, spill-over to Europe | Long term (≥ 4 years) |

| Generative-AI smart crew assistants for cockpit and cabin | +0.9% | Global, pilot programs in North America and Europe | Long term (≥ 4 years) |

| LEO satellite connectivity enables real-time in-flight crew scheduling, boosting adoption | +0.8% | Global, early deployment on long-haul routes | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Migration Across Airline IT Stacks

Slow release cycles, expensive hardware refreshes, and limited integration pathways box in airlines still relying on decades-old mainframe software. Moving those workloads to scalable cloud environments rewrites the economics of crew management because processing power and storage scale elastically with network size, simulator output, and regulatory updates. Lufthansa Systems’ decision to host Japan Airlines’ NetLine modules in the Global Aviation Cloud has revealed how quarterly feature releases give planners faster access to algorithm refinements, fatigue-model tweaks, and security patches, all delivered without the multi-day outages typical of on-premise upgrades.[1]Source: Lufthansa Systems, “Global Aviation Cloud,” lhsystems.com A shared, multi-tenant architecture lets smaller carriers piggyback on the same AI engines used by global network airlines, bringing parity in optimization quality across airline tiers. Operating costs fall because the cloud provider assumes responsibility for redundancy, disaster recovery, and penetration testing, which are costly for individual IT departments to maintain. These benefits allow crew controllers to focus on flight recovery and employee engagement instead of server upkeep, pushing the entire aviation crew management systems market toward subscription pricing and continuous delivery.

Stricter Fatigue and Flight-Time Limitation Rules

Regulatory agencies like the FAA and EASA have tightened definitions of acceptable duty periods, mandated data-driven Fatigue Risk Management Systems (FRMS), and expanded oversight audits, creating real-time compliance pressure. Airlines can no longer rely on spreadsheet trackers because cumulative limits span multiple pairings and time zones, making manual cross-checks impractical. Modern rostering engines ingest biomathematical models that estimate alertness scores by factoring circadian rhythm, schedule history, and time-zone crossings, then instantly flag potential violations before bids are awarded. This proactive compliance workflow saved Air India from additional fines after the carrier installed automated alerts following the INR 10.1 million penalty imposed by India’s DGCA in 2024.[2]Source: South China Morning Post, “India’s Aviation Sector Sets Sights on Growth,” scmp.com Crew scheduler dashboards now display a traffic-light system, green for compliant, amber for caution, red for breach, simplifying decision-making for frontline staff while creating an auditable data trail for regulators. The result is fewer last-minute roster changes, lower fatigue-related sick leave, and improved labor-management relations because transparency removes accusations of unfair scheduling.

Integrated Operations-Control Suites Replacing Stand-Alone Tools

Historically, crew departments, maintenance planners, and flight dispatchers used different software, leading to latency in information flow whenever an aircraft swap or weather delay occurred. Integrated Operations Control Center (IOCC) suites knit those data streams together through a common service bus, so when a maintenance task overruns, the crew optimizer immediately reevaluates pairing legality without manual triggers. Lufthansa Systems reports that carriers adopting its IOCC platform have eliminated duplicate data entry and realized up to USD 20 million annually in savings through better fuel planning, smoother diversions, and quicker passenger reaccommodation. Consolidated views let network controllers see gate availability, aircraft readiness, and crew legality on a single screen, allowing minute-by-minute scenario modeling during disruptions. Airlines also capture richer post-mortem analytics, identifying systemic bottlenecks such as chronic under-staffing at specific hubs or recurring aircraft type substitutions. Over time, this closed-loop feedback elevates decision quality and fosters a culture of continuous improvement that stand-alone tools cannot replicate.

AI-Powered Predictive Disruption Management

Machine-learning (ML) algorithms trained on years of delay codes, weather radar, and fleet utilization can spot patterns invisible to deterministic rule sets, letting planners take preventive action long before a mis-connect cascades. McKinsey found that AI-enhanced demand models improve pilot forecasting accuracy by 8%, freeing simulator slots and reducing training backlogs by up to 10%.[3]Source: McKinsey & Company, “AI Can Transform Workforce Planning for Travel and Logistics Companies,” mckinsey.com In practice, the platform assigns probability scores to each flight for potential delay, then produces alternate crew assignments ranked by legality, cost, and downstream impact. Dispatchers receive these recommendations inside their existing workflow rather than toggling between screens, shortening response time from hours to minutes. Airlines report material improvements in on-time performance, reduced hotel costs, and higher employee satisfaction because proactive reassignments respect contractual rest windows. As datasets grow, the models learn seasonal runway constraints, staffing patterns, and airport curfews, further sharpening prediction accuracy and strengthening the business case for continued AI investment.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High switching and data-migration costs | −1.8% | Global, highest in North America and Europe | Medium term (2–4 years) |

| Aviation-specific cyber-security and regulatory compliance burden | −1.5% | Global, strongest in US and EU | Short term (≤ 2 years) |

| Legacy narrow-band ACARS connectivity limits real-time updates | −1.2% | Global, acute in remote regions | Medium term (2–4 years) |

| Skills gap for advanced optimization and AI tools | −0.9% | Global, challenges in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Switching and Data-Migration Costs

Legacy crew systems often contain twenty-plus years of customized rules, bid periods, seniority logic, and union agreements that must migrate intact to avoid contractual breaches. Airlines underestimate the mapping effort required to transfer these rules into new database schemas, leading to scope creep and swollen budgets that can triple original license quotes. FlightGlobal’s historical survey of reservation system upheavals underscores similar pain points, highlighting multimillion-dollar write-offs when parallel runs uncovered data corruption. The operational risk is acute because any mis-assignment can snowball into mass cancellations, driving executives to mandate 12–18 months of shadow operation. During that time, staff managed two platforms, doubling the workload and delaying efficiency gains. Smaller carriers, lacking deep capital reserves, often postpone upgrades indefinitely, creating a two-tier market where technologically lagging airlines face higher disruption costs and reduced labor morale.

Aviation-Specific Cyber-Security and Compliance Burden

Unlike generic enterprise software, aviation systems must align with DO-178C development standards, TSA security directives, and cross-border data privacy laws such as GDPR. Each layer demands evidence, test artifacts, penetration reports, and change-control logs that auditors can trace from requirement to release. Clyde & Co’s industry review suggests cyber incidents in aviation rose sharply, prompting regulators to draft rules that add 15–25% overhead to project budgets. Airline IT teams must coordinate with national authorities, airport operators, and telecom providers to maintain compliance matrices that evolve almost monthly. Vendors compensate by building dedicated security operations centers, but those costs ultimately flow into subscription fees, increasing the total cost of ownership. For start-ups, the certification burden acts as a moat protecting incumbents, but it also slows the introduction of disruptive features because every new module triggers another compliance review cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Momentum Accelerates Amid Software Scale

Software licenses still generate the most vendor revenue of 70.30% of the aviation crew management systems market in 2024, because core pairing, rostering, and tracking engines underpin every airline workforce. Services, however, are racing ahead at a 9.30% CAGR through 2030. The growing sophistication of these platforms, integrating fatigue models, real-time data feeds, and AI explainability layers, makes configuration a specialist task. Airlines without in-house data scientists outsource model calibration, rules mapping, and security hardening to vendors like CAE, whose managed crews total more than 1,200 pilots across fifty airlines. These recurring service contracts convert one-time license deals into multiyear revenue streams, changing vendor economics from product sales to subscription annuities. Continuous regulatory amendments, such as evolving EASA fatigue matrices, guarantee a steady pipeline of change requests that airlines prefer to offload rather than staff internally. Consequently, the aviation crew management systems market size attributed to services is projected to grow faster than the underlying software base, reinforcing a virtuous cycle where new compliance mandates generate additional consulting and support demand.

The outsourcing trend also mitigates the talent shortages plaguing airline IT teams. By delegating 24/7 monitoring, patch management, and audit preparation to specialized providers, carriers stabilize labor costs and reduce the turnover risk associated with scarce optimization expertise. Vendors benefit from aggregated operational insight across multiple customers, which feeds back into product roadmaps and machine-learning models. This network effect raises entry barriers for newcomers and strengthens incumbent positions, concentrating the market around full-service providers capable of delivering code and continuous optimization.

By Deployment: Cloud Platforms Secure Dual Leadership

Cloud captured 67.82% share and posted the fastest 9.56% CAGR, evidencing a decisive pivot from on-premise limitations to elastic capacity. Cloud deployments have crossed the tipping point because they slash capital expenditure, shorten implementation timelines, and offer built-in scalability that mirrors airline growth ambitions. Lufthansa Systems’ Global Aviation Cloud shows how a private virtual data center tailored to aviation needs can maintain ISO 27001 compliance, deliver 24/7 support, and roll out feature updates every quarter without grounding a single aircraft. Airlines using such environments shift expenses to predictable operating-expenditure lines, avoiding peak replacement cycles that compete with fleet-renewal budgets. The cloud’s elasticity becomes vital during seasonal peaks when flight frequencies spike; additional compute can be provisioned instantly, keeping optimization runtimes within operational decision windows.

On-premise installations persist mainly where national regulations enforce data residency or where legacy enterprise agreements make exit costly. Hybrid architectures act as transitional bridges, allowing sensitive data to stay behind corporate firewalls while less critical workloads—such as training analytics—run in vendor clouds. Over time, however, the security certifications, disaster-recovery features, and AI toolchains offered by hyperscale providers will likely outpace what individual IT shops can replicate, nudging even conservative flag carriers toward more comprehensive cloud adoption.

By Airline Type: Cargo Growth Outpaces Passenger Scale

Passenger airlines held a 69.90% share in 2024 because their crew rosters dwarf those of cargo and charter operators, reflecting complex hub-and-spoke networks and dense daily schedules. Cargo operators, pressured by e-commerce surges and irregular routing, register the fastest 9.21%, lifting the most rapid expansion rate because e-commerce drives unpredictable demand spikes, requiring nimble crew scheduling that differs markedly from passenger patterns. Platforms that can model irregular routes, overnight airport curfews, and ad-hoc charters gain traction among operators such as FedEx and UPS, which test semi-autonomous freighter concepts to mitigate pilot shortages. These experiments, while long-term, already push developers to embed human–machine teaming logic into rostering tools, preparing the ecosystem for gradual reductions in cockpit crew counts.

For passenger airlines, growth is steadier, but the absolute market size remains large because fleet modernization and network diversification continuously raise optimization complexity. Charter and business-jet segments add incremental demand, especially as corporate travel rebounds and owners seek commercial-grade compliance systems to satisfy increasingly stringent regulatory scrutiny.

By Application: Training Leads in Growth, Planning Remains Core

Planning modules command 40.50% of the aviation crew management systems market share, because pairing and rostering determine downstream cost, compliance, and employee satisfaction. Training logs the quickest 10.54% CAGR as global pilot shortages raise simulator scheduling complexity. Boeing’s Integrated Flight School Solutions demonstrates how linking qualification databases with crew scheduling avoids wasted simulator slots by matching trainee readiness with aircraft and instructor availability. Integrated platforms track expiry dates for licenses, medicals, and type ratings, automatically inserting sessions into future rosters before regulators suspend crew privileges.

Advances in VR and augmented-reality simulation drive digital record-keeping, feeding granular performance metrics into crew management dashboards. Planners can then align high-performing crews with complex sectors, optimizing safety and cost. Tracking and fatigue-risk applications complete the suite, leveraging wearables and mobile alerts to ensure day-of-operations compliance, closing the loop between long-range planning and real-time execution.

Geography Analysis

North America commands the largest regional market share at 35.65% in 2024, driven by the concentration of major airlines, advanced regulatory frameworks, and early adoption of sophisticated crew management technologies. The region benefits from regulatory stability through the FAA's comprehensive flight and duty time regulations, which create standardized compliance requirements that favor automated crew management solutions. Major carriers, including American Airlines, Delta, and United, operate complex hub-and-spoke networks that require advanced optimization capabilities. At the same time, the presence of leading technology vendors such as Boeing, CAE, and specialized software providers creates a competitive innovation ecosystem. The region's mature market characteristics include high penetration of cloud-based solutions and increasing integration of AI-powered predictive analytics for disruption management.

Asia-Pacific is the fastest-growing region at 10.20% CAGR, propelled by rapid fleet expansion, acute pilot shortages, and regulatory modernization across key markets. India's aviation sector exemplifies this growth trajectory, targeting doubled passenger traffic by 2030 from its current position as the world's third-largest civil aviation market with 153+ million passengers in 2023. Regulatory scrutiny is intensifying across the region. India's DGCA is imposing INR 10.1 million (USD 0.11 million) in fines on Air India for safety protocol breaches related to crew scheduling, creating urgent demand for automated compliance management systems. China's projected demand of approximately 3,500 new aircraft through 2047 creates substantial crew management requirements. Meanwhile, the region's pilot shortage projections of ~371,000 through 2043 drive demand for optimization systems that maximize crew utilization efficiency.

Europe represents a mature market with steady growth, characterized by complex multi-jurisdictional operational requirements that create sophisticated crew management system demands. The region's regulatory environment combines EASA-wide standards with varying national requirements, necessitating crew management systems capable of handling diverse regulatory frameworks across operational networks. European carriers operate extensive international networks that cross multiple time zones and regulatory jurisdictions, creating complex duty time calculations and crew positioning requirements. As outlined in the ITF/OECD analysis of aviation decarbonization consequences, the region's emphasis on sustainability and decarbonization initiatives will drive demand for crew management systems to optimize operations under carbon pricing and sustainable aviation fuel constraints. Regulatory compliance frameworks, including GDPR data protection requirements, create additional complexity for crew management system implementations, favoring vendors with specialized European market expertise.

Competitive Landscape

The global supplier base is moderately concentrated, a figure set to rise following CAE’s acquisition of Sabre’s AirCentre portfolio. Boeing’s USD 10.55 billion sale of Jeppesen and ForeFlight to Thoma Bravo may inject fresh capital and accelerate cloud re-platforming of these legacy assets, intensifying competitive pressure. Vendors now compete on ecosystem depth, integrating crew planning with maintenance, passenger recovery, and even carbon reporting rather than isolated functionality. Lufthansa Systems promotes its IOCC suite as a holistic decision-making cockpit, an approach mirrored by CAE’s end-to-end Flight Operations Solutions.

Successful providers emphasize out-of-the-box API connectivity, mobile app usability, and AI explainability to win carrier trust. Emerging challengers carve niches in real-time disruption management, leveraging micro-services and event-streaming platforms that bolt onto incumbent cores without complete system replacement. Price competition remains subdued because switching costs deter rapid churn; instead, vendors differentiate on measurable KPIs such as duty-violation reduction, pairing productivity, and crew satisfaction scores. Managed-service offerings further deepen customer relationships by embedding vendor staff in airline operations centers, ensuring continuous optimization and creating high exit barriers.

Aviation Crew Management Systems Industry Leaders

Lufthansa Systems GmbH & Co. KG (Deutsche Lufthansa AG)

Sabre GLBL Inc. (Sabre Corporation)

Boeing Digital Solutions, Inc., d/b/a Jeppesen (The Boeing Company)

AIMS INTL DWC - LLC

IBS Software Europe Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Boeing partnered with Transavia France to fully implement Jeppesen’s Crew Rostering SaaS on a cloud-based platform. This transition to an optimized system enhances operational efficiency, reduces rostering times, and improves crew management flexibility, marking a significant advancement in aviation technology for the airline.

- August 2024: Neos, part of Alpitour World, selected Lufthansa Systems' NetLine/Crew for crew management as its fleet expands from 16 to 20 aircraft. The solution, operated on the Global Aviation Cloud, automates processes, enhances scalability, and ensures adaptability to dynamic business needs, marking a significant step in Neos' operational optimization.

Global Aviation Crew Management Systems Market Report Scope

| Software |

| Services |

| Cloud |

| On-premise |

| Hybrid |

| Passenger Airlines |

| Cargo Airlines |

| Charter and Business Jet Operators |

| Planning |

| Tracking |

| Training |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment | Cloud | ||

| On-premise | |||

| Hybrid | |||

| By Airline Type | Passenger Airlines | ||

| Cargo Airlines | |||

| Charter and Business Jet Operators | |||

| By Application | Planning | ||

| Tracking | |||

| Training | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Aviation Crew Management Systems market?

The aviation crew management systems market is valued at USD 3.34 billion in 2025 and is set to reach USD 4.85 billion by 2030, reflecting a 7.75% CAGR.

How fast is cloud deployment growing within crew management systems?

Cloud solutions hold 67.82% share today and are expanding at a 9.56% CAGR to 2030 on the back of scalability and faster compliance updates.

Which segment is expected to grow the quickest through 2030?

Training applications are projected to post the highest 10.54% CAGR as airlines tackle global pilot shortages.

Why are services becoming more important than before?

Complex regulations and scarce AI talent push airlines to outsource configuration, data science, and audit preparation, driving a 9.30% CAGR for services.

Which region offers the strongest growth outlook?

Asia-Pacific is slated for a 10.20% CAGR thanks to rapid fleet expansion in India and China and tightening regulatory oversight.

How are recent acquisitions reshaping competition?

CAE’s takeover of Sabre’s AirCentre and Boeing’s sale of Jeppesen to Thoma Bravo consolidate capabilities and may accelerate innovation under new ownership structures.

Page last updated on: