Autonomous Navigation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 13.47 Billion |

| Market Size (2030) | USD 29.79 Billion |

| Growth Rate (2025 - 2030) | 15.12% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Navigation Market Analysis by Mordor Intelligence

The autonomous navigation market size stood at USD 13.47 billion in 2025 and is on track to reach USD 29.79 billion by 2030, reflecting a 15.12% CAGR. Growth has been powered by regulatory approvals for Level-3 passenger cars, multi-platform sensor cost compression, and scaled commercial pilots across road, air, sea, and industrial settings. During 2024, solid-state LiDAR price declines shifted total cost of ownership economics, while venture funding and sovereign programs supported new deployments. Competitive pressure has driven rapid software iteration cycles, which in turn reinforce hardware demand as OEMs add redundancy to meet safety rules. Finally, persistent venture and defense capital inflows ensure that the autonomous navigation market continues to attract new firms despite fragmented incumbency

Key Report Takeaways

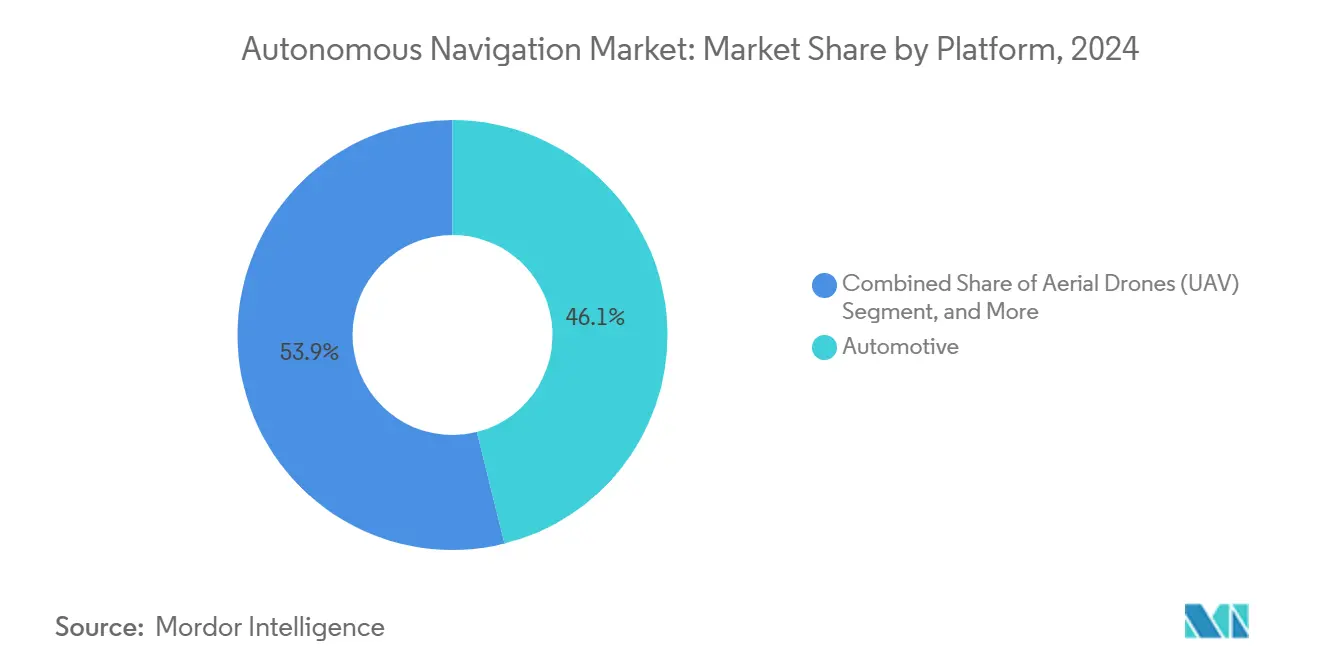

- By platform, automotive captured 46.12% of autonomous navigation market share in 2024.

- By component, hardware dominated with 54.34% share in 2024, while software is advancing at a 16.87% CAGR.

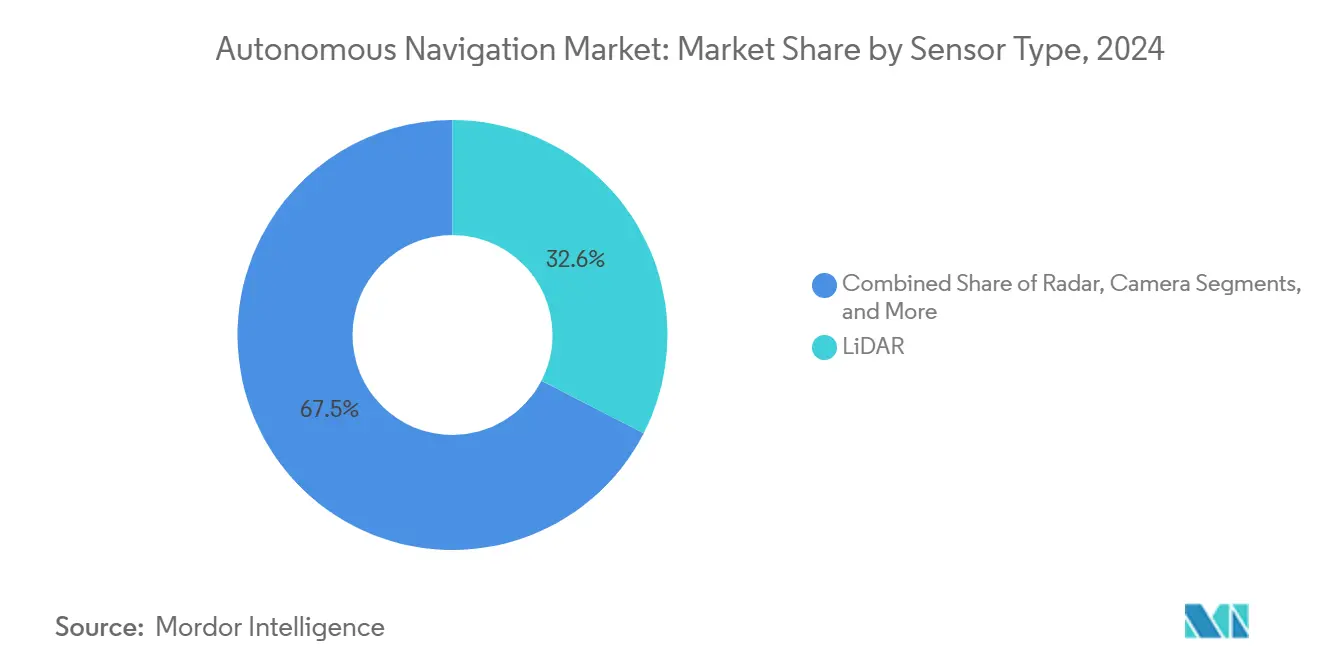

- By sensor type, LiDAR commanded 32.55% share and is poised for a 17.17% CAGR to 2030.

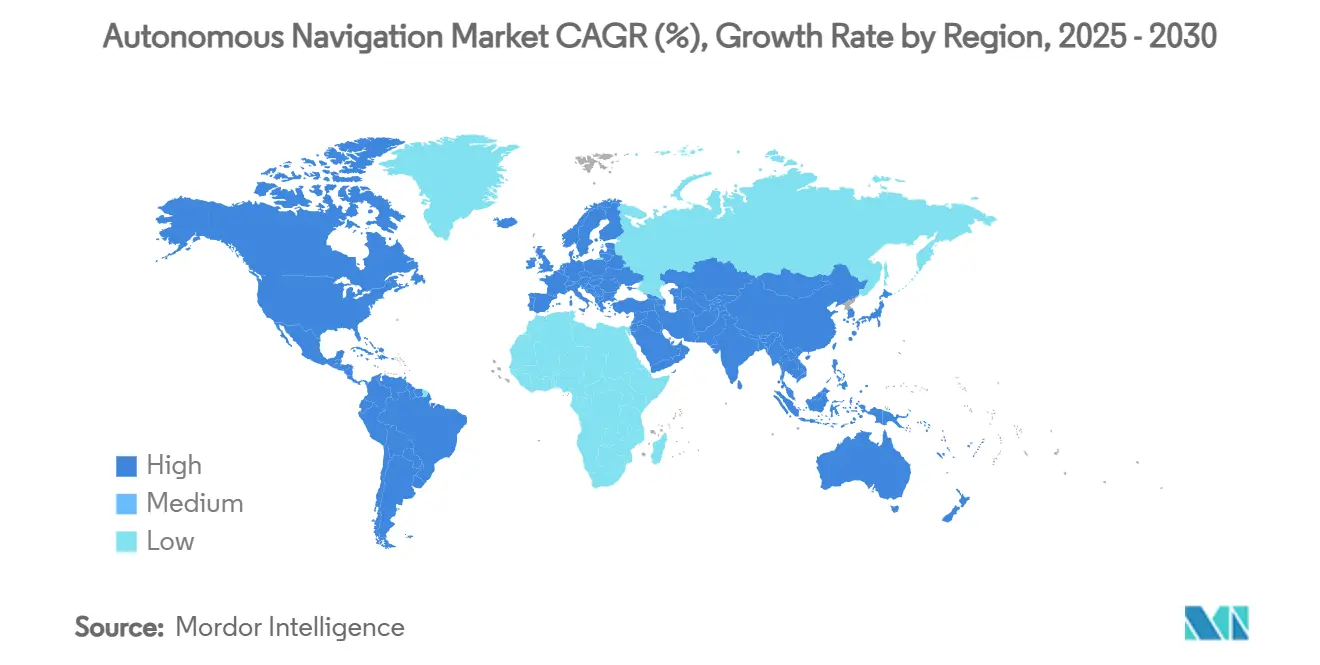

- By geography, North America held 38.89% share in 2024; the Middle East records the fastest 17.47% CAGR outlook.

Global Autonomous Navigation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating regulatory approvals for Level-3 passenger cars | +2.1% | Global, with early gains in EU, Japan, China | Medium term (2-4 years) |

| Rapid decline in solid-state LiDAR ASPs | +1.8% | Global, concentrated in automotive hubs | Short term (≤ 2 years) |

| Commercial drone delivery network pilots reach scale in OECD cities | +1.5% | OECD core, spill-over to emerging markets | Medium term (2-4 years) |

| IMO MASS Code adoption for autonomous vessels | +1.2% | Global maritime routes, early adoption in Northern Europe | Long term (≥ 4 years) |

| Under-reported: Autonomous haul-truck retrofits in Latin-America | +0.9% | Latin America, expansion to Africa and Asia | Medium term (2-4 years) |

| Under-reported: Sovereign investment in maritime surveillance | +0.7% | Asia-Pacific, Middle East, Northern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating regulatory approvals for Level-3 passenger cars

Multiple jurisdictions approved Level-3 highway systems during 2024, cutting certification cycles and encouraging OEM investment. Germany green-lit Drive Pilot for conditional automation, Japan broadened its framework, and China’s sandbox corridors offered city-level permits. The unified EU type-approval regulation removed country-by-country filings, shrinking compliance lead times. Together these moves reduced capital risk for suppliers and created global scale for safety-critical components.[1]TÜV SÜD, “Permit for Operating Autonomous Vehicles,” tuv-sud.com

Rapid decline in solid-state LiDAR ASPs

Automotive-grade solid-state LiDAR fell significantly during 2024 after semiconductor integration replaced mechanical assemblies. Suppliers leveraged silicon photonics and automotive packaging lines to reach cost parity with radar in some use cases. The drop has allowed mass-market vehicles to install multiple LiDAR units for 360-degree coverage, accelerating Level-3 and Level-4 feasibility.[2]Photonics Media editors, “Viavi Solutions Acquires Inertial Labs,” photonics.com Source: Federal Aviation Administration, “Accepted Means of Compliance for Small

Commercial drone delivery pilots reach scale in OECD cities

Urban drone delivery networks logged hundreds of thousands of flights in 2024. Civil aviation regulators in the United States and Europe authorized Category 3 operations over people, and several Asian cities opened low-level air corridors. These milestones provided dense real-world data, lowering insurance costs and validating autonomy stacks for GPS-challenged environments.[3]Federal Aviation Administration, “Accepted Means of Compliance for Small Unmanned Aircraft Category 3 Operations,” faa.gov

IMO MASS Code adoption for autonomous vessels

The IMO’s Maritime Autonomous Surface Ships Code entered force in 2024. Norway cleared the first autonomous container vessel and Singapore demarcated testing lanes. Clear rules for safety, communication, and crew competency unlocked commercial interest in cargo, offshore energy, and surveillance applications.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security certification gaps across platforms | -1.3% | Global, acute in defense and critical infrastructure | Short term (≤ 2 years) |

| High-precision HD-map maintenance cost | -0.8% | Urban centers globally, severe in rapidly changing cities | Medium term (2-4 years) |

| Talent bottleneck in real-time embedded AI engineers | -0.6% | Silicon Valley, Europe, China tech hubs | Medium term (2-4 years) |

| Export-control restrictions on tactical-grade IMUs | -0.4% | Global supply chains, concentrated impact on defense applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-security certification gaps across platforms

ISO/SAE 21434 became mandatory for new cars in 2024, yet equivalent rules for maritime, aerial, and industrial robots lagged. Suppliers must therefore tailor separate security architectures, inflating non-recurring engineering spend and lengthening validation schedules. Fragmentation also leaves multi-platform fleets with uneven threat coverage, a challenge that specialized cyber firms aim to close.

High-precision HD-map maintenance cost

Operating centimeter-grade maps can be highly expensive annually in congested cities where lane-level changes occur daily. For smaller service areas the fixed cost per kilometer rises sharply, hampering commercial deployment. Crowdsourced and real-time mapping technologies are under development but have not yet met functional safety targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Automotive scale leads, marine surges

The autonomous navigation market size for automotive platforms stood at USD 6.22 billion in 2025, equal to 46.12% of revenue. Regulatory clarity and consumer software-update models helped Tesla, Waymo, and legacy OEMs push robotaxi pilots. Marine and offshore platforms, while only 9% of 2025 revenue, are projected to grow at 16.3% CAGR as sovereign navies fund unmanned patrol craft and shipping lines pursue crew-light cargo runs. Aerial drones leveraged commercial delivery demand, and mining fleets retrofitted haul trucks for strip-pit workloads. Cross-platform knowledge transfer has blurred historic boundaries as firms port automotive sensor fusion into vessels and adapt aviation redundancy strategies for trucks.

Automotive dominance has spawned a vibrant component ecosystem that supplies smaller niches. Defense programs retrofit Black Hawk helicopters with civil-grade autonomy kits, validating commercial software in mission-critical sorties. Warehouse robots, although mature, continue to absorb algorithms refined on highways, proving that research amortizes across use cases. Consequently, platform segmentation is expected to narrow as software abstraction layers let developers target multiple vehicles with minimal code change.

By Component: Software acceleration reshapes margins

Hardware represented 54.34% of 2024 revenue but now faces share erosion as value migrates to perception and decision-making code. The autonomous navigation market size attributed to software is projected to reach USD 13.1 billion by 2030, riding a 16.87% CAGR on the back of over-the-air feature releases and data-anchored service contracts. Nvidia’s centralized compute boards illustrate how tight hardware-software coupling reinforces platform stickiness, yet margins increasingly accrue to the algorithm layer where differentiation resides.

Automotive OEMs purchase turnkey compute stacks, while drone makers prioritize weight and battery life, leading to heterogeneous bill-of-materials profiles. Robotaxi consortiums such as the 2025 Uber–Lucid–Nuro partnership favor software-defined vehicles that accept iterative updates, extending fleet life and reducing capital tied to hardware refresh cycles.

By Sensor Type: LiDAR retains lead amid fusion

LiDAR accounted for 32.55% of sensor spending in 2024 and is forecast for a 17.17% CAGR, underpinned by solid-state reliability and falling cost curves. Still, camera, radar, and inertial sensors remain indispensable for all-weather redundancy. Multi-modal fusion has become de-facto architecture: cars now embed four to six LiDAR units, high-resolution surround cameras, and corner radar to meet fault-tolerant safety cases.

Performance-cost trade-offs define verticals. Freight trucks operating along fixed corridors can limit LiDAR count, whereas robotaxis navigating urban density require maximal coverage. Viavi’s planned integration of Inertial Labs inertial measurement units shows demand for specialized sensors to anchor navigation when GNSS signals are obstructed.

Geography Analysis

North America held 38.89% of 2024 revenue thanks to progressive testing rules and concentrated venture pools. California’s permit regime let Waymo expand into Los Angeles in early 2024, and Tesla obtained its first robotaxi operating consent in 2025. Canada authorized six multi-province pilots, while Mexico’s Tier-1 supply base strengthened regional resilience. The autonomous navigation market share advantage is reinforced by public-private partnerships and consistent federal research grants.

Asia-Pacific experienced rapid city-level deployments where sandbox policies in China allowed BYD and WeRide to earn incremental permits. Japan’s roadmap toward Level-4 highway drives for 2027, alongside South Korea’s 5G-linked smart city corridors, bolsters medium-term growth. Australia, New Zealand, and Indonesia pursued autonomous haulage in mining and plantations, demonstrating how industrial use cases often precede passenger services.

Europe benefited from the EU-wide type-approval, giving OEMs a single route to acceptance and enabling cross-border sales. Germany’s automotive cluster accelerated component integration, and the United Kingdom prepared its commercial self-driving regulations for a 2026 launch. Sovereign investment pushed the Middle East to a 17.47% CAGR outlook, focusing on smart-city logistics corridors in the Gulf. Latin America and parts of Africa exploited autonomous trucks and survey drones in mining, turning challenging terrain into economic rationale for autonomy.

Competitive Landscape

The autonomous navigation market is fragmented. Automotive supply features legacy Tier-1s such as Bosch and Continental competing with software-centric players like Waymo and Tesla. Maritime autonomy is more concentrated, with Saab and Kongsberg commanding early share through turnkey combat and logistics solutions. Startups leverage domain-specific algorithms-Tera AI raised USD 7.8 million to tackle visual navigation in GPS-denied spaces-illustrating low barriers to proof-of-concept yet high capital needs for scale.

Consolidation accelerated in 2025 as General Motors bought the remaining stake in Cruise and Redwire acquired Edge Autonomy. These moves reveal a pursuit of vertical integration to control data loops and accelerate certification. Government contracts continue to set performance benchmarks: Leidos secured a USD 248 million Navy award, supplying cash flow that private robotaxi ventures often lack. Strategic focus has shifted toward software ecosystems and long-tail service revenue over pure hardware sales, with players courting academic partnerships to ease engineering scarcity.

Autonomous Navigation Industry Leaders

NVIDIA Corporation

Mobileye Global Inc.

Tesla Inc.

Continental AG

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Advanced Navigation expanded its U.S. defense presence by appointing a Global Head of Defense, signalling deeper engagement with military customers.

- March 2025: Tesla obtained an initial CPUC permit to run a robotaxi fleet in California, marking the company’s first commercial ride-hailing credential.

- March 2025: Tera AI emerged from stealth with USD 7.8 million in seed funding for vision-based navigation software.

- April 2025: The U.S. Army awarded Near Earth Autonomy and Honeywell a USD 15 million program to retrofit UH-60L helicopters with autonomy kits.

Global Autonomous Navigation Market Report Scope

| Automotive |

| Aerial Drones (UAV) |

| Marine and Offshore |

| Defence and Space |

| Industrial and Logistics Robots |

| Hardware |

| Software |

| LiDAR |

| Radar |

| Camera |

| GNSS + INS |

| Other Sensor Types |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Platform | Automotive | ||

| Aerial Drones (UAV) | |||

| Marine and Offshore | |||

| Defence and Space | |||

| Industrial and Logistics Robots | |||

| By Component | Hardware | ||

| Software | |||

| By Sensor Type | LiDAR | ||

| Radar | |||

| Camera | |||

| GNSS + INS | |||

| Other Sensor Types | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue size is autonomous navigation expected to reach by 2030?

The space is forecast to climb from USD 13.47 billion in 2025 to USD 29.79 billion by 2030, reflecting a 15.12% CAGR.

Which platform currently generates the highest share of autonomous navigation revenue?

Automotive applications led with 46.12% of global revenue in 2024.

Where is the fastest regional growth projected over the next five years?

The Middle East shows the steepest outlook at a 17.47% CAGR through 2030.

How much did solid-state LiDAR prices decline during 2024?

Automotive-grade units fell below USD 500, down from USD 8,000–10,000 for mechanical systems only three years earlier.

What is the biggest near-term restraint facing autonomous deployments?

Fragmented cyber-security certification across road, sea, and air platforms is trimming the overall growth rate by roughly 1.3 percentage points.

Page last updated on: