Navigation System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

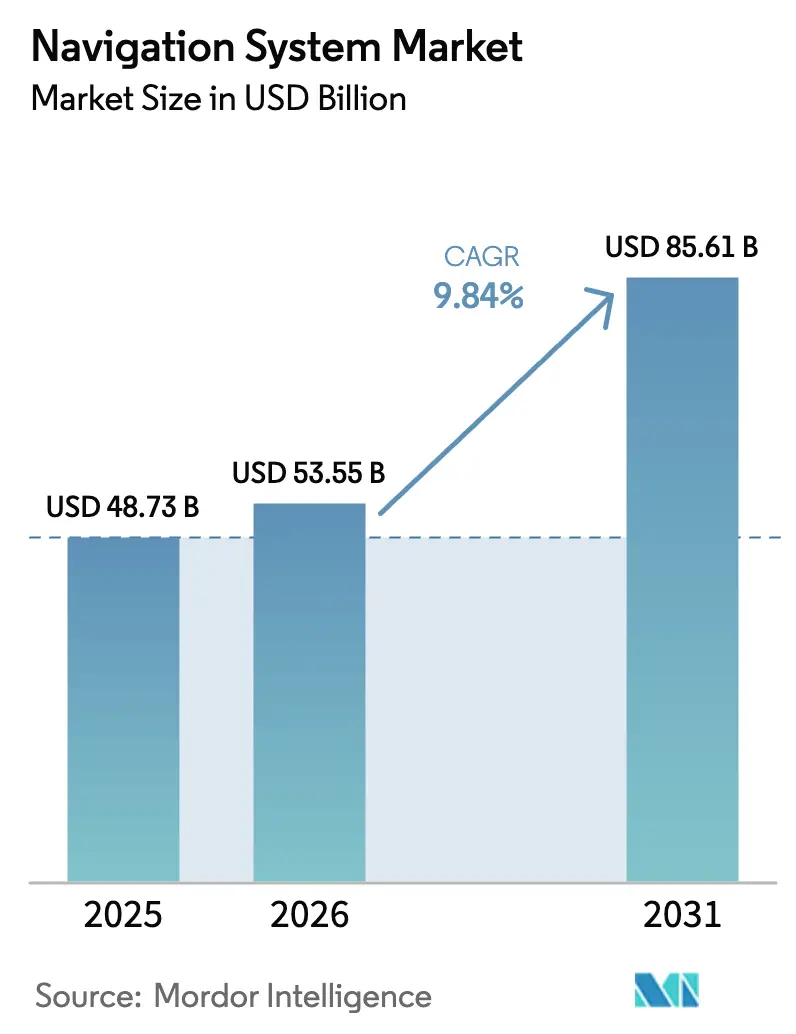

| Market Size (2026) | USD 53.55 Billion |

| Market Size (2031) | USD 85.61 Billion |

| Growth Rate (2026 - 2031) | 9.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Navigation System Market Analysis by Mordor Intelligence

The Navigation System Market size is estimated at USD 53.55 billion in 2026, and is expected to reach USD 85.61 billion by 2031, at a CAGR of 9.84% during the forecast period (2026-2031). Demand is shifting from incremental hardware upgrades to resilient positioning, navigation, and timing solutions that maintain service continuity when satellite signals degrade or are unavailable. Finland and Estonia experienced a 300% increase in deliberate GNSS interference in 2024, while the Resilient Navigation and Timing Foundation documented more than 46,000 aviation disruptions in the Baltic region alone, highlighting the need for regulators and integrators to favor hybrid architectures that combine inertial, optical, and quantum sensors with satellite data.[1]Resilient Navigation and Timing Foundation, “GPS Interference Events in the Baltic Region,” rntfnd.org Defense programs in North America and Europe earmarked USD 2.8 billion for assured-PNT technologies in 2025, a sign that navigation resilience underpins both military readiness and civilian infrastructure. Consumer-electronics volumes continue to compress module prices, making dual-frequency receivers economically viable in scooters, wearables, and rental bicycles. At the same time, software-defined maps, AI-driven sensor fusion, and open-source stacks are lowering integration barriers for smaller entrants, intensifying competitive dynamics at the edge of this rapidly evolving value chain.

Key Report Takeaways

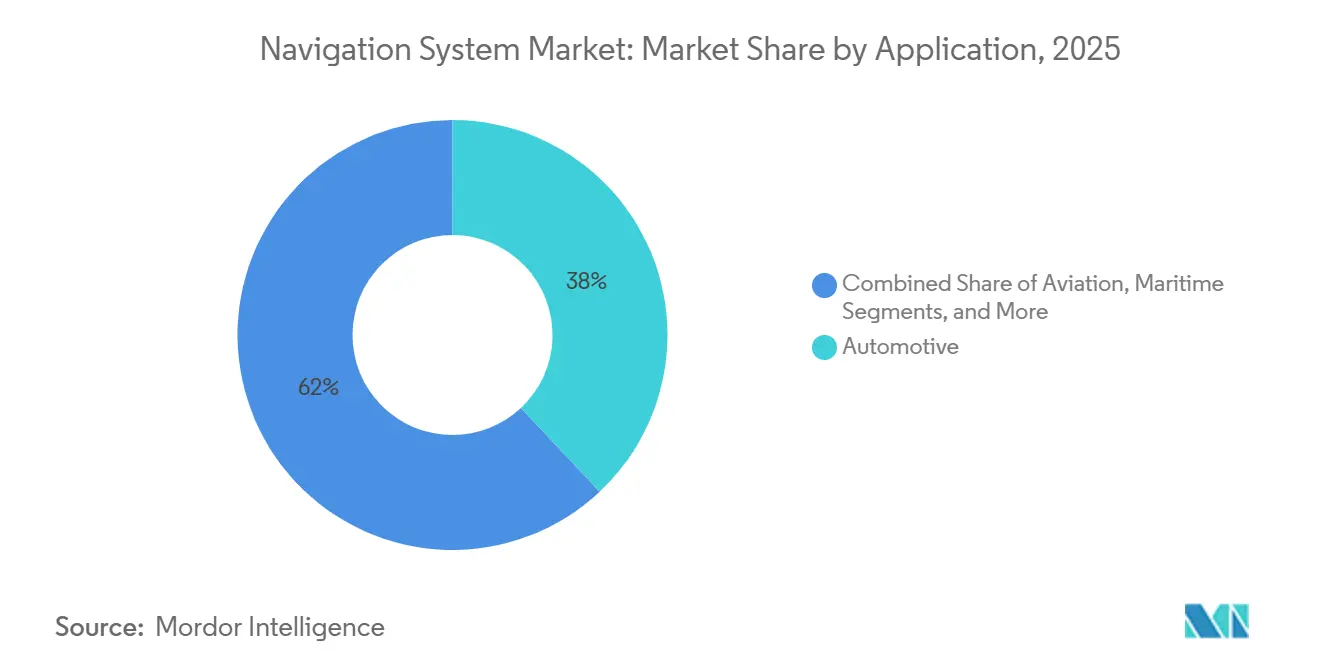

- By application, automotive systems led the navigation systems market with a 38% share in 2025, while industrial and surveying solutions are expected to expand at a 12.60% CAGR through 2031.

- In 2025, navigation technology, including satellite receivers, commanded a 49% share of the navigation systems market size. However, hybrid and sensor-fusion architectures are projected to post the fastest growth at a 14.40% CAGR from 2026 to 2031.

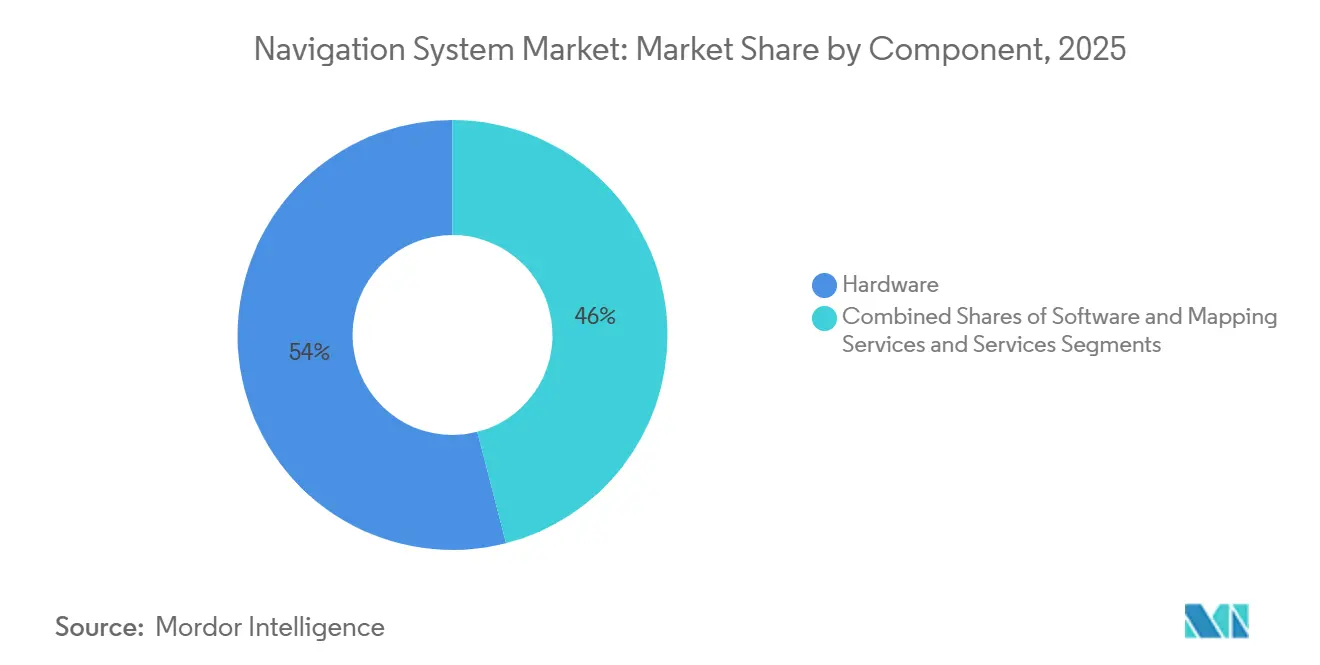

- By component, hardware captured 54% of the navigation systems market in 2025, whereas software and mapping subscriptions are growing at a 13.90% CAGR.

- By platform, land vehicles accounted for 42% of the navigation systems market share in 2025, while spacecraft guidance is forecast to grow at a 11.80% CAGR.

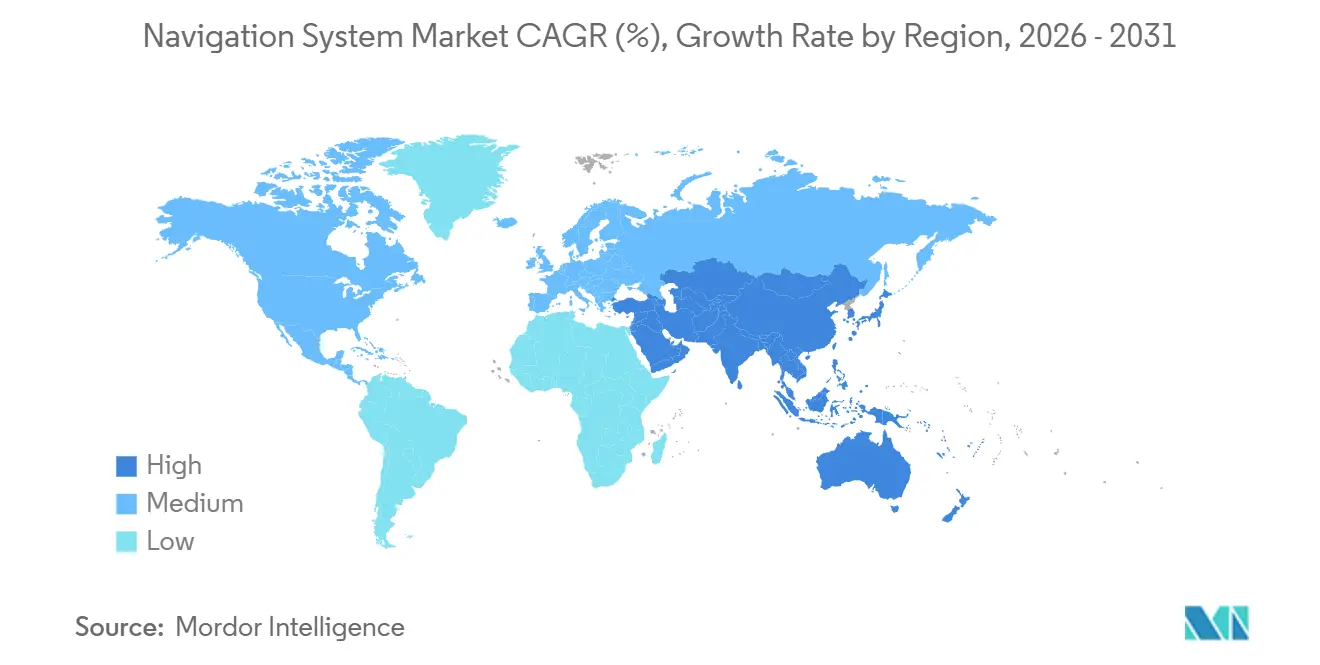

- By geography, the Asia Pacific accounted for 38% of the 2025 revenue and is forecast to register a 10.50% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Navigation System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Factory-Fitted Navigation in Passenger and Commercial Vehicles | +1.8% | Global, with concentration in Asia Pacific and Europe | Medium term (2-4 years) |

| Rapid Expansion of GNSS-Enabled Consumer Electronics | +1.5% | Global, led by Asia Pacific smartphone production hubs | Short term (≤ 2 years) |

| Aviation Demand for Performance-Based Navigation Compliance | +1.2% | North America, Europe, Asia Pacific aviation corridors | Medium term (2-4 years) |

| Defense Modernization Programs Requiring Assured-PNT Solutions | +2.1% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Emergence of Quantum and Optical Gyro Technologies for GPS-Denied Environments | +1.4% | North America, Europe, select Asia Pacific defense markets | Long term (≥ 4 years) |

| AI-Driven Sensor-Fusion Software Enhancing Real-Time Accuracy | +1.6% | Global, with early adoption in automotive and industrial segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Factory-Fitted Navigation in Passenger and Commercial Vehicles

Automakers now embed positioning hardware at the assembly stage, reducing bill-of-materials cost and tying buyers into proprietary map ecosystems. Volkswagen’s CARIAD unit partnered with TomTom in October 2024 to deliver the IndiGO.NDS stack across 15 million vehicles by 2028, enabling over-the-air map updates that eliminate the need for dealership visits. BMW’s Operating System 9, released in 2025, merges HERE HD Live Map with real-time overlays to deliver 200-millisecond route recalculations, a latency that aftermarket devices cannot match.[2]BMW Group, “Operating System 9 Integration with HERE HD Live Map,” bmwgroup.com On the commercial side, the European Union’s Mobility Package I, fully effective as of February 2025, requires cross-border trucks weighing more than 3.5 tonnes to carry GNSS-enabled tachographs, creating a captive replacement cycle and promoting lane-level positioning as a precursor to premium driver-assistance features.

Rapid Expansion of GNSS-Enabled Consumer Electronics

Dual-frequency receivers processed both L1 and L5 signals in 68% of smartphones shipped during 2025, up from 41% in 2023, thanks to Qualcomm’s Snapdragon X80 modem that fuses GPS, Galileo, BeiDou, and NavIC inputs for sub-meter accuracy in urban canyons. Apple’s U2 ultra-wideband chip combines GNSS with UWB to deliver centimeter-level peer-to-peer localization for indoor retail and healthcare navigation, a capability now replicating across Android ecosystems. Wearables account for 22% of consumer GNSS modules, while logistics operators such as DHL deployed 1.2 million trackers across Europe in 2024, resulting in a 40% reduction in customer location queries. Higher shipment volumes drove module prices below USD 2, allowing low-cost e-scooters and rental bikes to integrate positioning for anti-theft and usage-based billing.

Aviation Demand for Performance-Based Navigation Compliance

As of the end of 2025, 87% of ICAO member states had at least one Required Navigation Performance approach in place, up from 74% in 2023. FAA Order 8260.58D, issued March 2025, mandates RNP Authorization Required procedures at terrain-constrained airports, forcing 6,800 U.S. airliners to upgrade avionics. EASA’s 2024 roadmap sets a 2028 sunset date for many European ground-based aids, adding momentum to the development of satellite-augmented receivers. Airlines implementing RNP at hubs such as London Heathrow report fuel savings of 8-12% per landing, recouping retrofit costs in under two years.

Defense Modernization Programs Requiring Assured-PNT Solutions

The U.S. Department of Defense’s 2024 strategy allocates USD 1.6 billion over five years to alternative PNT, while DARPA’s Adaptable Navigation Systems prototype sustained 20-meter accuracy for 72 hours without GPS, blending signals of opportunity from LEO satellites and 5G beacons. Northrop Grumman is retrofitting 18,000 guided munitions with chip-scale atomic clocks under an August 2024 contract that cuts drift to under 1 meter per hour. The United Kingdom awarded Thales GBP 120 million (USD 152 million) in January 2025 to fit quantum-inertial modules on Type 26 frigates, enabling covert operations without detectable RF emissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of High-Precision Systems | –1.3% | Global, pronounced in price-sensitive emerging markets | Medium term (2-4 years) |

| Vulnerability to Jamming and Spoofing Attacks | –0.9% | Europe, Middle East, contested Asia Pacific zones | Short term (≤ 2 years) |

| Short Product Life-Cycles Versus Automotive Design Cycles | –0.7% | North America, Europe, Asia Pacific hubs | Long term (≥ 4 years) |

| Talent Shortage in Advanced Navigation Algorithm Development | –0.6% | Global, clustered in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of High-Precision Systems

Centimeter-level receivers list between USD 5,000 and USD 15,000, a hurdle for cost-sensitive users. Trimble’s R12i sells for USD 12,800 and requires an additional USD 1,200-2,400 per year for correction services, limiting its adoption to surveyors and well-capitalized farms. John Deere’s StarFire 7000 costs USD 9,500, with an annual subscription of USD 1,800, pricing out smallholders cultivating under 50 hectares. Septentrio’s Mosaic-X5 module, priced at USD 800 in high volume, lowers entry costs but still needs paid corrections to reach sub-decimeter precision.

Vulnerability to Jamming and Spoofing Attacks

The Resilient Navigation and Timing Foundation logged 46,000 interference events in the Baltic region during 2024, forcing Helsinki flights to revert to legacy aids and consume an additional 220 kg of fuel per affected arrival. Low-cost jammers priced under USD 300 can deny GNSS signals across a 30 km range, while maritime spoofing in the Black Sea has placed vessels up to 50 km off course, posing a threat to collisions. Anti-jamming antennas add USD 2,000-8,000 per platform, yet advanced spoofing still exploits civilian signal weaknesses, highlighting the urgency of authenticated and multi-sensor navigation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Industrial Automation Outpaces Automotive Integration

Industrial and surveying solutions are projected to rise at a 12.60% CAGR, the fastest among all applications, as RTK and precise point positioning converge with machine vision and robotics. Trimble’s 2024 Bilberry acquisition added AI weed-detection to its GNSS toolset, reducing herbicide use by 70% in spot-spraying trials, while the March 2025 Agri-Trak deal extended variable-rate seeding to mainstream farmers. Construction adopts similar patterns; Caterpillar stated that 38% of North American dozers shipped in 2024 carried factory-installed 3D grade control, trimming rework by USD 18,000 per project.

Automotive uses dominated revenue, with a 38% market share in navigation systems in 2025; however, growth is moderating as carmakers pivot toward decoupled software platforms. Fleet regulations such as the EU tachograph rule push steady, but slower, replacement cycles. Aviation, maritime, and defense niches command premium pricing due to strict integrity, redundancy, and anti-spoofing needs.

By Navigation Technology: Hybrid Architectures Capture GPS-Denied Demand

Hybrid and sensor-fusion architectures are set to expand at a 14.40% CAGR through 2031. The United Kingdom’s November 2024 flight test utilized cold-atom interferometry to achieve 10-meter accuracy for 90 minutes without the aid of satellites, thereby confirming the quantum inertial potential in commercial aviation. DARPA’s Micro-PNT prototypes integrate chip-scale atomic clocks and MEMS gyros in a 10-cm³ package, achieving sub-meter drift for infantry navigation.

Satellite receivers still hold a 49% share of the navigation systems market in 2025, largely due to their integration with consumer electronics. Inertial-only units are used in submarines, mines, and indoor robots where GNSS is unavailable, but the high cost of high-performance INS limits their wider use. Optical and electromagnetic surgical platforms operate entirely outside GNSS, yet they benefit from broader hybrid sensor advances.

By Component: Software Subscriptions Monetize Installed Hardware Base

Software and mapping services are forecast to expand at a 13.90 percent CAGR from 2026 to 2031, outpacing hardware growth as vendors transition from one-time equipment sales to recurring-revenue models. HERE Technologies' HD Live Map, which updates road geometry and traffic conditions in real-time, generated EUR 420 million (USD 462 million) in licensing revenue during 2024, with automotive OEMs accounting for 68% of subscriptions and logistics fleets contributing the remainder. TomTom's Orbis Maps platform, launched in September 2024, delivers map updates over-the-air within 24 hours of infrastructure changes, enabling autonomous-vehicle developers to maintain lane-level accuracy without manual data collection. Google Maps introduced AI-powered route optimization in March 2025, utilizing historical traffic patterns and real-time incident data to reduce average trip times by 8 percent in urban areas. This feature attracted 40 million new monthly active users within the first quarter. Correction-service providers such as Trimble RTX and Hexagon SmartNet are bundling GNSS data with analytics dashboards, charging USD 1,200 to USD 2,400 annually per receiver and achieving gross margins above 70 percent.

Hardware comprising receivers, inertial measurement units, and antennas held a 54 percent share in 2025, reflecting the capital-intensive nature of initial system deployment. Bosch Sensortec's BMI323 six-axis IMU, introduced in January 2025, integrates accelerometers and gyroscopes with on-chip sensor fusion, reducing power consumption to 0.65 milliwatts and enabling always-on positioning in wearable devices. STMicroelectronics' LSM6DSV16X, launched in mid-2024, features machine-learning cores that classify motion patterns, such as walking, running, and driving, to optimize GNSS duty cycling and extend battery life by 25 percent in fitness trackers. Services, encompassing installation, training, and maintenance, capture a smaller revenue share but command higher margins in defense and aviation segments, where system certification and ongoing compliance support justify premium pricing.

By Platform: Spacecraft Guidance Systems Lead Growth Trajectory

Spacecraft and launch vehicles are projected to grow at 11.80 percent CAGR through 2031, the fastest rate among all platform segments, driven by the proliferation of low-Earth-orbit constellations and the commercialization of space logistics. NASA's CAPSTONE mission, which completed lunar orbit insertion in November 2024, demonstrated autonomous navigation using onboard optical sensors and inter-satellite ranging, reducing ground-station dependency and enabling real-time trajectory adjustments. Terran Orbital's satellite buses, deployed across 14 missions in 2024 and 2025, integrate GPS receivers with star trackers to achieve positional accuracy within 5 meters in LEO, a capability that supports formation flying and on-orbit servicing applications. SpaceX's Starlink constellation, which exceeded 6,200 operational satellites by mid-2025, relies on GPS-disciplined rubidium clocks to synchronize inter-satellite laser links, maintaining network latency below 25 milliseconds for global broadband coverage. The International Space Station's Neutron Star Interior Composition Explorer, launched in 2017 but upgraded with new navigation algorithms in 2024, uses X-ray pulsar timing to achieve positional accuracy within 10 kilometers in deep space, demonstrating a pathway for GPS-independent navigation beyond Earth orbit.

Land vehicles accounted for 42 percent of platform revenue in 2025, encompassing passenger cars, commercial trucks, agricultural equipment, and construction machinery. Airborne platforms, including commercial aircraft, business jets, helicopters, and uncrewed aerial vehicles, benefit from PBN mandates and the integration of navigation with flight management systems. Maritime and sub-sea platforms are adopting autonomous technologies; Kongsberg's K-Mate system, deployed on 18 vessels in 2024, combines GNSS, inertial, and radar inputs to enable remote piloting from shore-based control centers, reducing crew requirements by 40 percent on short-sea routes. Wärtsilä's autonomous navigation solution, installed on a 64-meter ferry operating in Finnish waters, completed 12,000 autonomous docking maneuvers in 2025 with zero collisions, demonstrating the maturity of sensor-fusion algorithms in challenging maritime environments.

Geography Analysis

Asia Pacific seized 38% of 2025 revenue and is forecast to grow at a 10.50% CAGR through 2031. China’s January 2025 mandate that all new smartphones support BeiDou instantly converted 300 million devices per year into a domestic user base. India’s NavIC constellation expanded coverage across the Indian Ocean Region in mid-2025, cutting maritime reliance on GPS and driving dual-constellation receiver demand.[3]Indian Space Research Organisation, “NavIC Constellation Expansion to Indian Ocean Region,” isro.gov.in Japan’s Quasi-Zenith System reached seven satellites in 2024, enabling autonomous vehicle trials operating without detailed HD maps. South Korea reported that 42% of new farm machinery shipped in 2025 was equipped with RTK receivers. Thailand deployed 12 SBAS reference stations in 2024, enabling RNP approaches at 18 airports and reducing monsoon-season delays by 14%.

North America and Europe combined for 47% of annual revenue. FAA mandates are driving 6,800 avionics retrofits between 2025 and 2027, while EU tachograph rules created a captive cycle for 4.2 million trucks. Precision agriculture in the U.S. Midwest conserved 22% irrigation water after the 2024 droughts through RTK-guided variable-rate systems. Defense modernizations remain robust, with NATO adopting a multi-source PNT requirement in April 2025.

The Middle East and Africa trail in volume but post double-digit growth, particularly in areas with sovereign smart-city and logistics projects. The UAE’s Falcon Eye network had covered 87% of urban areas by mid-2025, enabling the coordination of emergency services and traffic in real-time. These initiatives encourage the adoption of hybrid navigation beyond traditional aviation and maritime domains.

Regulatory Landscape

Navigation systems face cross-sector compliance requirements across aviation performance, spectrum protection, and national technical standards for receiver components. In aviation, ICAO guidance continues to shape state-level adoption of GNSS-based procedures, including updates such as the ICAO GNSS Manual (Doc 9849) corrigendum dated November 2025, while regulators in the United States and Europe have progressed performance-based navigation and retrofit programs that pull certified avionics and databases into tighter conformance regimes.

On the spectrum and standards side, regulators are tightening guardrails around radionavigation bands and chip performance. CEPT/ECC Decision (25)01 (enacted July 2025) targets protection of RNSS in the 1258-1300 MHz band with a preferred implementation date of 27 December 2025, reinforcing interference-management expectations for equipment ecosystems. In China, GB/T 47326-2026, published by the State Administration for Market Regulation in March 2026 and implemented starting 1 July 2026, specifies performance requirements and test methods for BeiDou/GNSS broadband RF chips, affecting qualification pathways for suppliers shipping into Chinese device and automotive programs. In parallel, the European Commission introduced Proposal 2026/0084(COD) in April 2026 to establish a self-standing founding act for EUSPA, signaling continued institutional evolution around EU space services that influence downstream navigation service governance and procurement.

Value Chain Analysis

The navigation system value chain is increasingly layered, beginning with signal and reference infrastructure (GNSS constellations and supporting geodetic networks), moving through semiconductor chipsets and modules (GNSS receivers, IMUs, antennas), and extending into augmentation and correction services (RTK/PPP networks), software and map platforms (HD maps, routing engines, positioning SDKs), and finally OEM and integrator deployment across automotive, aviation, maritime, defense, industrial, and consumer devices. Within the report scope, the economics are shifting toward software-defined stacks and recurring data subscriptions, with software and mapping services taking a larger share versus one-time hardware sales.

Two structural bottlenecks shape competitive behavior. First, accuracy and integrity depend on foundational geodesy capabilities that are under-resourced relative to the downstream revenue pool, which increases systemic risk for high-precision and safety-critical use cases. Second, localization pressures around data sovereignty and compliance encourage region-specific integration patterns; for example, foreign automotive OEMs expanding into Europe often rely on established mapping and service providers to meet local requirements. As a result, ecosystem power consolidates around a small set of map and platform providers (e.g., HERE and TomTom) and correction networks, while device OEMs and tier suppliers differentiate through multi-sensor fusion, anti-jam/anti-spoof features, and integrated subscription bundles.

Competitive Landscape

The navigation systems market remains moderately fragmented. The top five suppliers, Honeywell, Garmin, Collins Aerospace, Trimble, and Thales, collectively held 35% revenue in 2025, leaving room for regional experts and technology disruptors. Trimble’s precision-agriculture roll-ups of Bilberry and Agri-Trak strengthen its vertically integrated model, blending RTK receivers with AI agronomy to lock clients into high-margin subscriptions. Honeywell’s Anthem avionics were launched in mid-2024, merging navigation, communications, and surveillance into a single, line-replaceable unit that airlines can enhance through software, thereby deferring the need for full cockpit swaps.

White-space opportunities emerge at the intersection of quantum sensing and commercial aviation. Vector Atomic raised USD 30 million in Series B funding in August 2024 to commercialize quantum accelerometers that maintain accuracy even during GPS denial. Smaller entrants exploit open-source firmware and commodity chipsets. For instance, Swift Navigation prices its Skylark corrections at USD 49 per month, delivering decimeter accuracy at one-tenth the cost of Trimble’s. Australian supplier Advanced Navigation provides fiber-optic gyroscopes for autonomous underwater vehicles, surpassing MEMS drift performance for multi-day subsea missions.

Patent data signal divergent bets: Garmin submitted 14 filings in 2024-2025 on multi-frequency antennas and AI sensor fusion, while Thales focused on quantum clocks and cryptographic anti-spoofing. Module pricing below USD 5 in the automotive and consumer electronics sectors compresses margins, favoring vertically integrated semiconductor companies such as Qualcomm and Broadcom, which can spread R&D costs across their connectivity portfolios.

Navigation System Industry Leaders

Garmin Ltd.

Honeywell International Inc.

Collins Aerospace Inc.

Safran Electronics & Defense Inc.

KVH Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Assured positioning, navigation, and timing (PNT) is a key whitespace where hybrid architectures and alternative signals are moving from defense programs into broader aviation, maritime, and critical-infrastructure deployments. The scale of the interference problem is now visible in operational disruption metrics, including the Resilient Navigation and Timing Foundation logging more than 46,000 aviation disruptions in the Baltic region during 2024, and Finland and Estonia reporting a 300% increase in deliberate GNSS interference in 2024. Under these conditions, demand shifts toward architectures that combine inertial, vision, magnetic anomaly, and signals-of-opportunity, aligning with industry moves such as Honeywell launching its Alternative Navigation Architecture (HANA) in October 2025 and defense-backed development work like DIU contracts for quantum sensor-based navigation announced in July 2025.

A second opportunity band is emerging in compliance-driven retrofit and certified database expansion in civil aviation. Regulators have tightened procedure requirements, and operators are upgrading avionics and navigation data to maintain access and efficiency. Events such as FAA Order 8260.58D (March 2025) and European planning for navigation aid transitions create a pipeline for cockpit retrofits, certified receivers, and navigation databases, supported by supplier actions including Garmin securing EASA certifications for multiple retrofit solutions in April 2026 and expanding its navigation database coverage to Africa in June 2026. In parallel, space and spectrum governance changes introduce integration openings for providers that can connect satellite, terrestrial, and software layers; April 2026 marked a major program inflection when the U.S. Space Force terminated the GPS OCX program, while March 2026 saw the FCC adopt an NPRM on spectrum for space TT&C, both of which increase attention on modernization pathways, operational continuity, and cross-domain interoperability.

Recent Industry Developments

- July 2026: Garmin unveiled AXIS, a new generation of highly integrated flight displays for aviation. The launch advances cockpit consolidation of navigation and situational-awareness functions, helping operators modernize capabilities while managing retrofit complexity and lifecycle costs.

- November 2025: Honeywell received U.S. government authorization (MSO-c145b) for its FALCN embedded GPS Inertial Navigation System (EGI). This completes certification for its full EGI portfolio and strengthens Honeywell's position in programs that require assured PNT, including environments where M-Code readiness and resilience to interference are key procurement criteria.

- July 2025: Safran announced the acquisition of Collins Aerospace's flight control and actuation activities, spanning 180 platforms. The deal deepens Safran's control over key aircraft systems that interface with guidance and navigation architectures, influencing supplier selection and integration pathways for avionics modernization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the navigation system market as the revenue earned from solutions that determine position, route, and guidance using satellite signals, inertial sensors, and supporting software, sold into transportation, defense, industrial, and healthcare use cases.

Scope exclusions: Standalone consumer navigation mobile apps that are not monetized as a navigation product or service are excluded.

Segmentation Overview

- By Application

- Automotive

- Aviation

- Maritime

- Defense and Security

- Industrial and Surveying

- By Navigation Technology

- Satellite Navigation Systems (GNSS)

- Inertial Navigation Systems

- Surgical Navigation Systems

- Hybrid and Sensor-Fusion Systems

- By Component

- Hardware (Receivers, IMUs, Antennas)

- Software and Mapping Services

- Services (Installation, Training, Maintenance)

- By Platform

- Land Vehicles

- Airborne Platforms

- Maritime and Sub-Sea Platforms

- Spacecraft and Launch Vehicles

- Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Benelux

- Nordics

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Oceania

- Rest of Asia Pacific

- Middle East

- Turkey

- Israel

- GCC

- Rest of Middle East

- Africa

- North Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To set a clean base, we start with public signals that describe the real demand pool and the technology supply chain. This includes sources such as U.S. Department of Transportation and FAA publications for aviation activity, NOAA and IMO related references for maritime navigation themes, and defense budget documents for modernization priorities tied to assured positioning and timing.

We also review non-paywalled technical and adoption indicators, such as GNSS and sensor research in peer reviewed journals, patent databases for navigation and sensor fusion activity, and trade data from customs portals that helps explain hardware flows where visible. These are then paired with company filings, investor presentations, and credible press coverage to check product mix changes and pricing direction. For company financials and broader news screening, paid subscriptions that cover company intelligence and news are used to speed up validation. The sources listed here are illustrative, and many other public references were used for data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary work is used to convert broad indicators into usable model inputs, especially where public data is not specific enough for navigation systems. We interview and survey OEMs, subsystem suppliers, software and mapping providers, and buyers across automotive, aviation, maritime, defense, and healthcare. Coverage is spread across major demand regions so assumptions are not driven by one geography.

The respondent set also clarified how navigation solutions are packaged (hardware only versus bundles that include software, mapping, and services) and how attach rates differ by end use.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | APAC: 41% |

| Mid tier: 51% | Functional/Unit leaders: 31% | EMEA: 37% |

| Smaller Players: 17% | Managers: 52% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand reconstruction, where platform production, fleet activity, and installed base signals are translated into navigation system attach rates and average selling prices, then rolled up by region and application. The totals are checked using selective bottom-up approximations, such as sampled supplier revenue splits, channel checks for aftermarket units, and ASP times unit sanity tests, which helps adjust for gaps where public reporting is thin.

Key inputs used in the model include vehicle production and parc trends, aircraft deliveries and retrofit activity, defense procurement cycles for resilient PNT upgrades, GNSS availability and jamming awareness (as a demand catalyst for hybrid solutions), and the hardware versus software and services mix that shifts pricing over time. Where unit data is not observable, we handle the gap by using interview-based ranges for attach rate, replacement cycle, and ASP bands, then stress test outcomes against known adoption patterns in each end use.

Forecasts are built using scenario analysis, since adoption is sensitive to regulatory timing, platform refresh cycles, and budget release patterns that do not move in a straight line. The scenarios are anchored to consensus views from practitioners, then averaged into a base case that stays traceable to the same input variables year to year.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the final numbers do not rely on one data stream. We compare model totals against independent signals like platform counts, shipment direction from trade data where applicable, and reported revenue exposure in public filings, followed by variance checks at region and application levels.

When an outlier shows up, assumptions are revisited and, if needed, respondents are re-contacted to confirm whether the change is real or a data artifact. Before sign off, the work goes through stepwise analyst reviews that focus on unit logic, pricing realism, and year over year continuity. Reports are refreshed annually, and interim updates are made when material events occur, with a final pre delivery pass to ensure the latest information is reflected.

Mordor Intelligence's Navigation System Market Size Compared Against Other Published Estimates

Published market sizes for navigation systems can look far apart because the underlying scope and the year used for comparison are not always aligned. Differences also come from whether a study counts only hardware boxes, or also includes software, mapping content, and services that sit around the navigation function.

The benchmark table shows a higher 2026 value than some other public figures. In Mordor Intelligence's model, the scope includes navigation solutions across automotive, aviation, maritime, defense, industrial, and healthcare, instead of narrowing the count to only one end use or only device hardware revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 53.55 B (2026) | |

| Trade Journal A | USD 33.63 B (2023) | The figure is anchored to an earlier base year and may reflect a narrower monetized definition, with less consistent inclusion of software, mapping, and service revenue beyond core system sales. |

| Industry Publisher B | USD 0.91 T (2023) | This estimate is presented as total sales revenue for navigation systems and can over expand scope by folding in adjacent platform electronics and broad regional revenue pools, which makes year to year comparability harder. |

The comparison mainly shows that year selection and what gets counted as navigation revenue drive most of the spread. By keeping the scope explicit and tying totals back to observable demand indicators like platform activity, adoption rates, and price bands, the model stays easy to follow and repeat when assumptions are updated.

Key Questions Answered in the Report

What is the projected value of the navigation systems market in 2031?

The sector is expected to reach USD 85.61 billion by 2031, reflecting a 9.84% CAGR from 2026 to 2031.

Which application segment is growing fastest?

Industrial and surveying use cases are set to expand at 12.60% CAGR through 2031 as RTK and machine-vision tools penetrate agriculture and construction.

Why are hybrid and sensor-fusion technologies gaining traction?

They blend inertial, optical, and quantum sensors with satellite data to maintain accuracy when GNSS signals are jammed or spoofed, driving a 14.40% CAGR.

How large is Asia Pacific’s share of sector revenue?

Asia Pacific held 38% of 2025 revenue and is forecast to post a 10.50% CAGR to 2031, underpinned by BeiDou and NavIC adoption.

Which companies lead precision-agriculture navigation?

Trimble, John Deere, and CAT dominate through RTK receivers, variable-rate seeding, and grade-control systems, supported by recent acquisitions and product launches.

What is the main challenge to wider adoption of centimeter-level accuracy?

High capital costs—up to USD 15,000 per receiver plus annual correction fees—limit uptake among small farms and price-sensitive construction firms.

Page last updated on: