Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Passenger Information System Market Report Segments the Industry Into by Component (Hardware, Software, and Services), Solution (Information / Display Systems, Announcement Systems, Mobile Applications, and More), Deployment Location (On-Board Systems, and Station / Wayside Systems), Mode of Transportation (Railway, Roadway / Bus and Coach, and Airway / Airports), and Geography.

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

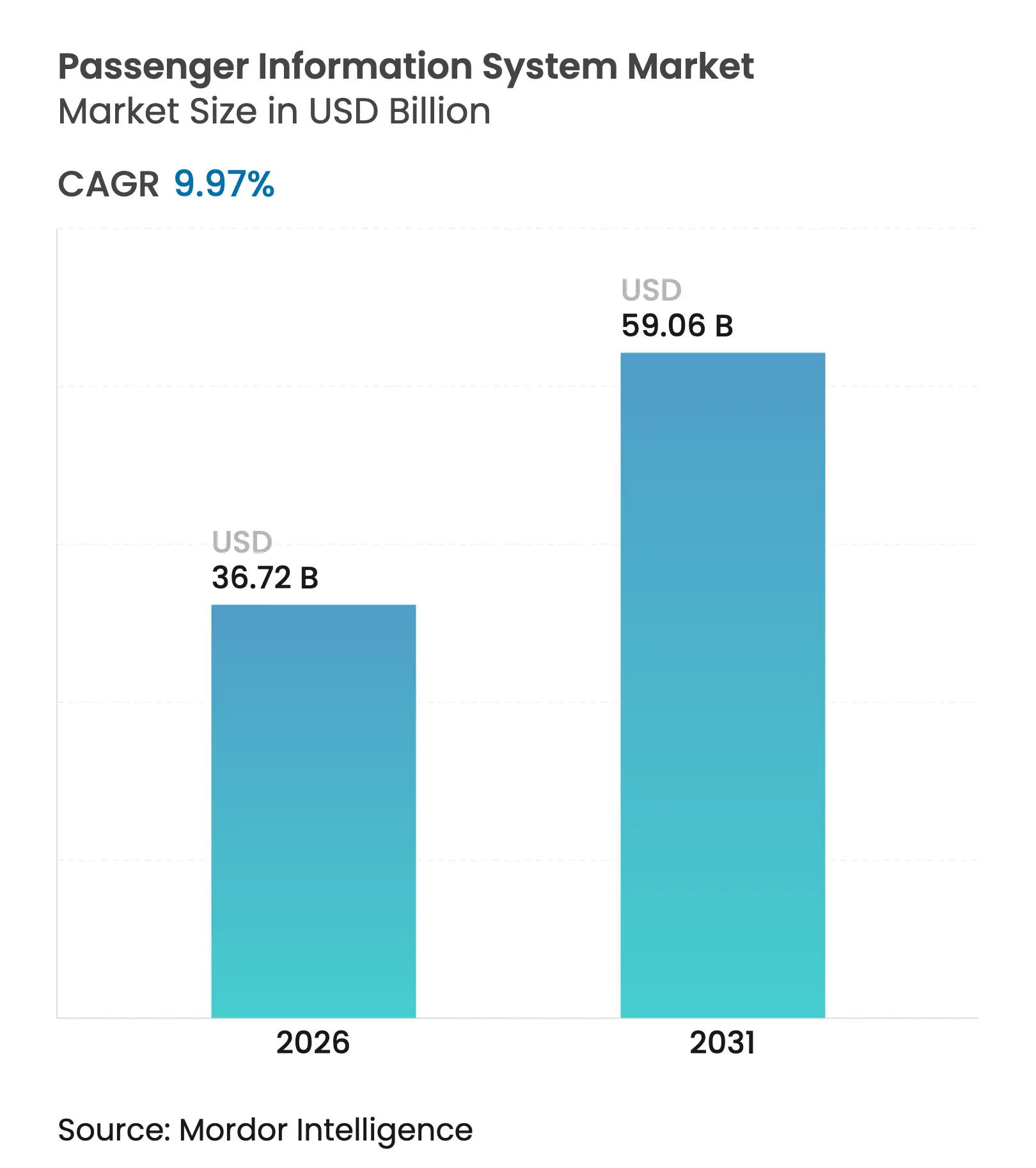

| Market Size (2026) | USD 36.72 Billion |

| Market Size (2031) | USD 59.06 Billion |

| Growth Rate (2026 - 2031) | 9.97 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Passenger Information Systems market size was valued at USD 33.39 billion in 2025 and estimated to grow from USD 36.72 billion in 2026 to reach USD 59.06 billion by 2031, at a CAGR of 9.97% during the forecast period (2026-2031). Rapid digital transformation of transit infrastructure, convergence of 5G, edge computing, and artificial intelligence, and stricter accessibility regulations are turning real-time information from a convenience into an operational linchpin. Transit agencies are shifting from one-off hardware investments toward cloud-centric, continually updated platforms that personalise data, predict disruptions, and synchronise multimodal journeys. Hardware upgrades remain indispensable for high-resolution displays and ruggedised processors, yet software has become the strategic battleground, delivering analytics that trim dwell times, reduce crowding, and support contactless payment. Competitive intensity is rising as established rail-technology firms acquire AI specialists to defend market positions, while new entrants exploit open standards to deliver mobile-first, API-rich solutions. Near-term headwinds—component shortages, LED price inflation, and rural connectivity gaps—temper growth but also accelerate migration to energy-efficient hardware and remote diagnostic software. Overall, the Passenger Information Systems market is transitioning into an ecosystem where value is captured through data-driven services rather than devices alone.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Mobile and

web-platform proliferation

Mobile and

web-platform proliferation

| +2.1% | Global; strongest in Asia-Pacific, North America | Short term (≤ 2 years) |

(~) % Impact on

CAGR Forecast

:

+2.1%

|

Geographic

Relevance

:

Global; strongest in

Asia-Pacific, North America

|

Impact Timeline

:

Short term (≤ 2

years)

|

Urbanization and

smart-city programs

Urbanization and

smart-city programs

| +1.8% | Asia-Pacific core; spill-over to Middle East, Latin America | Medium term (2-4 years) | |||

Public-transport

digitisation funding

Public-transport

digitisation funding

| +1.5% | Europe and North America, expanding to the Asia-Pacific | Medium term (2-4 years) | |||

Multimodal

ride-share data integration

Multimodal

ride-share data integration

| +1.2% | North America and EU; pilots in Asia-Pacific | Long term (≥ 4 years) | |||

Predictive AI/ML

reliability analytics

Predictive AI/ML

reliability analytics

| +1.0% | Global, led by developed markets | Long term (≥ 4 years) | |||

5G edge-computing

for dynamic PIS

5G edge-computing

for dynamic PIS

| +0.9% | Asia-Pacific and North America are early adopters | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Mobile and Web-Platform Proliferation

Smartphone saturation means 70% of rider information requests now arrive via mobile, prompting agencies to prioritise app-based schedules, crowding alerts, and contactless payments that trim boarding by up to 20 seconds per passenger[1]Digi International, “Revolutionizing Public Transit Through TrueTime Mobile Engagement,” digi.com. Pittsburgh Regional Transit’s TrueTime app illustrates how real-time data improves ridership while cutting operating costs through automated density reports and predictive maintenance. Rich behavioural data from apps supports dynamic route optimisation, increasing service relevance with each additional user. Network effects arise as accurate crowdsourced inputs enhance predictions for all travellers, creating stickiness that entrenches early-mover advantage. Still, digital-divide realities force operators to retain traditional signage, raising cost and complexity.

Urbanization and Smart-City Programs

Fast-growing cities view passenger information as a backbone of intelligent transport. Seoul’s TOPIS control tower orchestrates over 100 million annual journeys, cutting congestion 12% and lifting satisfaction 25% through predictive alerts. Ahmedabad’s NEC-supported system trims waiting times 30% via automated fares and live bus tracking. Municipal leaders see superior information services as magnets for residents and businesses, creating economic feedback loops that justify ongoing investment. Integrated data pipes enable coordinated traffic lights, emergency response, and even air-quality management, cementing Passenger Information Systems market relevance in wider urban planning.

Public-Transport Digitization Funding

Targeted grants accelerate deployments. The U.S. Federal Transit Administration dedicated USD 525,000 to Nova Scotia’s on-demand platform across 23 communities, marking North America’s largest demand-responsive rollout. In Europe, mandatory NeTEx and SIRI data formats force legacy upgrades, spurring compliance-driven replacements and opening procurement to cloud-native vendors. Funding is shifting from capex blocks to opex models that favour software-as-a-service, easing budget constraints and ensuring continual updates.

Multimodal Ride-Share Data Integration

Ride2Rail pilots in Athens, Brno, Helsinki, and Padua shorten door-to-door trips 20-25% by merging shared cars and scooters with transit schedules. API-level synchronisation delivers real-time cross-mode options, yet privacy safeguards and competitive tensions slow full rollout. Where cooperation flourishes, integrated workflows boost ridership across all modes, justifying investment in common data layers. Regulators may need to mandate openness to unlock system-wide efficiency gains.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital and

maintenance cost

High capital and

maintenance cost

| -1.4% | Global; acute in developing markets | Short term (≤ 2 years) |

(~) % Impact on

CAGR Forecast

:

-1.4%

|

Geographic

Relevance

:

Global; acute in

developing markets

|

Impact Timeline

:

Short term (≤ 2

years)

|

Rural connectivity

limitations

Rural connectivity

limitations

| -0.8% | Rural zones worldwide | Medium term (2-4 years) | |||

Cyber-security

threats to open data feeds

Cyber-security

threats to open data feeds

| -0.6% | Global critical-infrastructure sites | Long term (≥ 4 years) | |||

Legacy-system

interoperability gaps

Legacy-system

interoperability gaps

| -0.5% | Developed markets with mature assets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital and Maintenance Cost

LED displays cost USD 380-1,200 per sq ft in 2025, with installation adding up to 60% more, pricing out smaller agencies[2]SZ Radiant, “Commercial LED Price Trends 2025,” szradiant.com. Semiconductor bottlenecks lift automotive-grade chip prices 25-40%, stretching project timelines. Chicago Transit Authority tests digital stops with modest USD 55,000 grants before scaling, evidencing cautious spend. Solar-powered units lower lifetime energy bills but raise upfront integration effort. Cloud dashboards delivering remote diagnostics can cut on-site servicing 70%, softening but not eliminating cost barriers that cap adoption in budget-constrained regions.

Legacy-System Interoperability Gaps

Mixing modern APIs with decades-old proprietary protocols often doubles project timelines. California’s statewide ITS evaluation found that data exchange modules ate significant development hours due to obsolete interfaces. The EU’s NeTEx transition demands parallel operations during cut-over, straining staff and budgets. Middleware helps bridge systems, yet adds new failure points requiring specialised skills. Consequently, agencies defer upgrades until bundled with broader vehicle or station refurbishments, slowing the Passenger Information Systems market in mature networks.

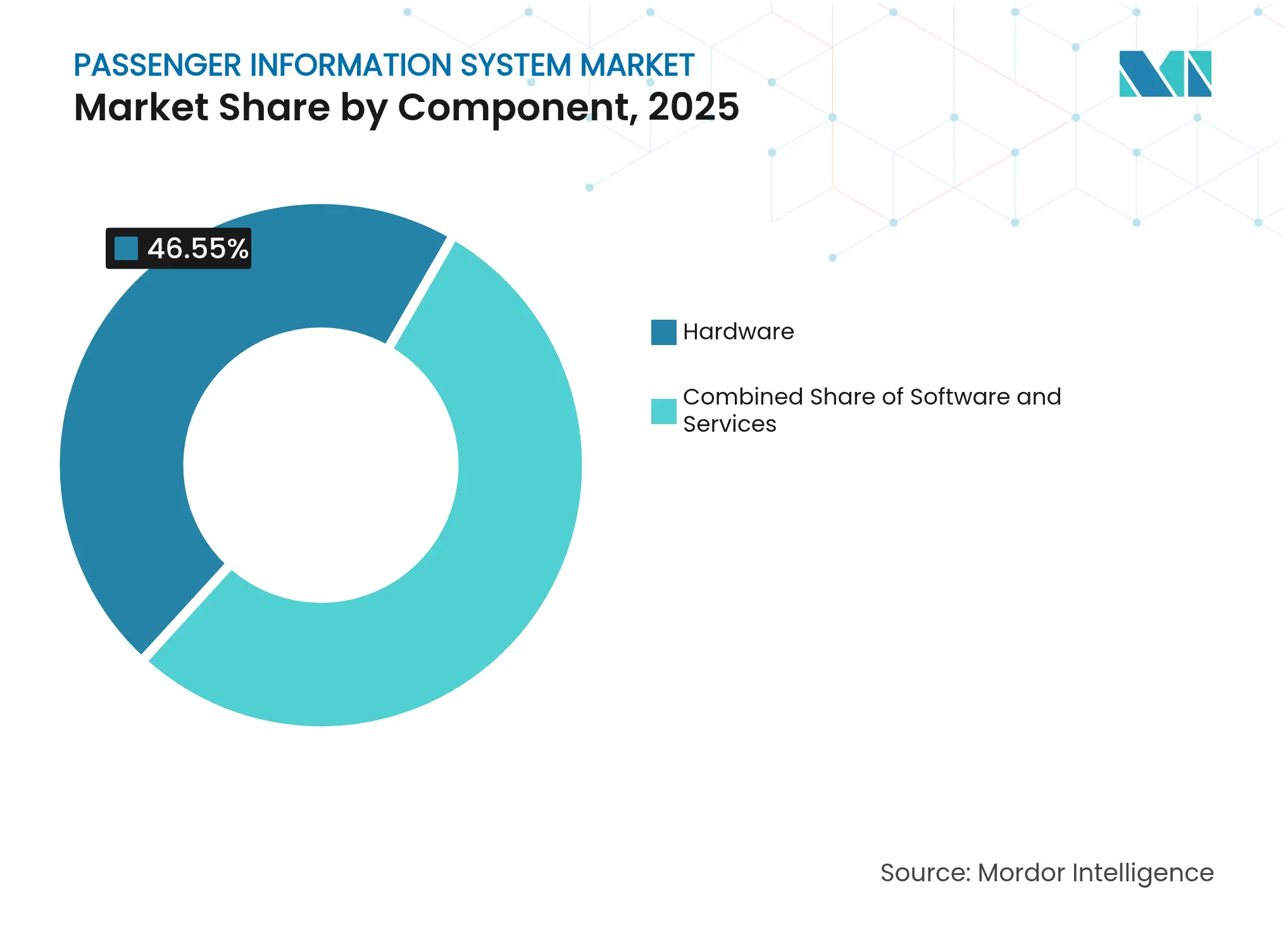

By Component: Hardware Strength Endures as Software Gains Pace

Hardware secured 46.55% of 2025 revenue, anchoring the Passenger Information Systems market through mandatory investments in rugged displays, processors, and connectivity. Upgrades to higher-resolution LED panels and power-efficient drivers justify replacement cycles, even amid semiconductor shortages. Meanwhile, software revenues are accelerating at a 14.45% CAGR as operators migrate to cloud-native suites delivering AI-powered predictions and dynamic content rules. Services, though the smallest slice, enjoy superior margins because integration and lifecycle support require domain expertise scarce among transit agencies. Hardware vendors pivot toward bundled offerings that embed license fees, blurring lines between physical product and digital platform. JR East’s forthcoming AI-infused management system illustrates how software innovation now drives procurement decisions, relegating hardware to a commoditized foundation. Over the forecast horizon, the Passenger Information Systems market will reward suppliers capable of fusing reliable equipment with continuously evolving analytics.

Second-generation hardware increasingly ships with embedded operating systems ready for over-the-air updates, shortening commissioning times and enabling remote feature drops. That capability aligns with operators’ preference for operational rather than capital spending, smoothing budget approvals. Nonetheless, silicon lead-time volatility may prompt strategic stockpiling, inflating working capital needs for hardware-heavy vendors. Cloud-centric suppliers face different challenges, notably data-sovereignty compliance and cybersecurity accreditation, yet gain recurring revenue and higher customer stickiness. The distinction between hardware and software providers will keep narrowing, reshaping competitive clusters within the Passenger Information Systems market.

Note: Segment shares of all individual segments available upon report purchase

By Solution: Mobile Apps Challenge Display Supremacy

Information and display systems accounted for 37.25% of 2025 solution turnover, reflecting longstanding regulations that mandate visual announcements for accessibility. Yet mobile applications are sprinting ahead at a 16.28% CAGR, becoming the primary touchpoint for itinerary adjustments and digital ticketing. Displays are far from obsolete; multilingual translation engines, like Toppan’s neural units at Haneda Airport, modernise signage for global travellers. Emergency communication modules gain traction as security standards tighten, bringing audio-visual alerts and network isolation into unified platforms. Video surveillance and infotainment, once optional, integrate seamlessly with information flows to monetise screen real estate during dwell times.

Operators now weigh app development road-maps as heavily as physical signage upgrades when allocating budgets, signifying a cultural shift in procurement criteria. For suppliers, releasing agile app updates every few weeks contrasts with multi-year display-hardware cycles, requiring new DevOps competences. Apps also unlock anonymised behavioural data, providing feedback loops that inform advertising placements and service planning. As regulators standardise open APIs, solution categories converge, transforming once-discrete silos into federated passenger-experience suites that will underpin the next growth wave in the Passenger Information Systems market.

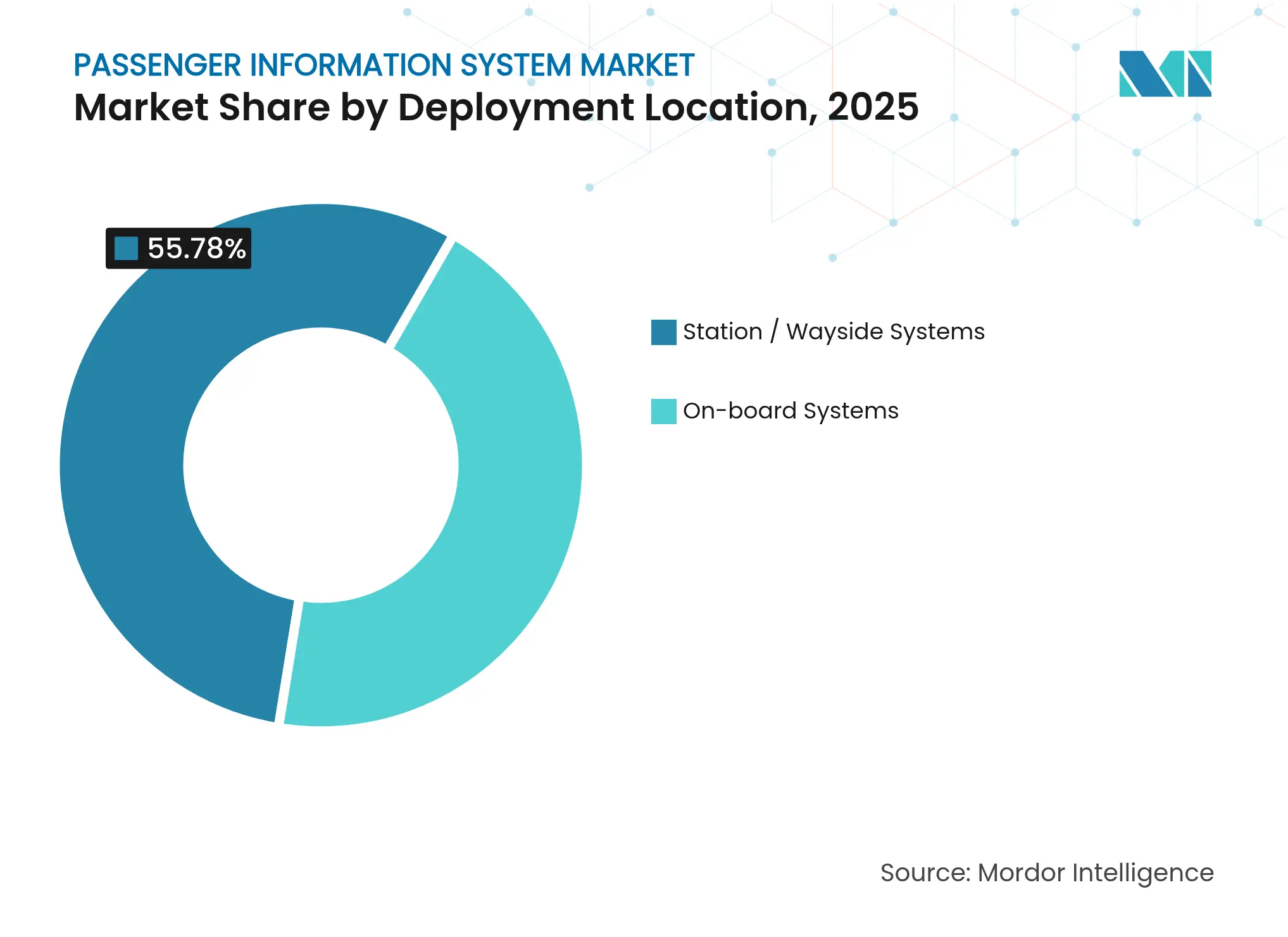

By Deployment Location: On-Board Systems Accelerate

Station and wayside units drove 55.78% of 2025 spend because they serve every traveller and fulfil statutory obligations for public-space information. On-board systems, forecast to climb 15.48% CAGR, benefit from OEM-level integration into new rolling stock and buses. Wabtec’s LED and TFT package for Munich’s S-Bahn trains, featuring Bluetooth Auracast for hearing-impaired users, exemplifies how vehicle-mounted equipment now doubles as accessibility tech and infotainment canvas. Passenger Information Systems market size for on-board installations will therefore outpace station upgrades as large fleet replacement cycles progress.

Still, stations evolve into interactive hubs. Philadelphia International Airport’s AI-powered wayfinding kiosks combine flight data, retail offers, and emergency notifications on large touch LED panels. Seamless hand-off of data between train cars and platforms relies on synchronised back-end content managers, compelling vendors to offer end-to-end orchestration. Agencies weighing investment must balance visibility benefits of station displays against the personalised engagement of in-vehicle screens. Over time, connectivity advances and falling display prices will see a hybrid model dominate, elevating holistic platforms that integrate both environments within the Passenger Information Systems market.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Transportation: Aviation Ramps Up Digitization

Roadway and bus fleets retained 50.95% share in 2025, evidencing the sheer scale of municipal bus networks and mature display specifications. However, airport deployments are expanding at a 13.34% CAGR as authorities pursue contactless journeys and surge management. Collins Aerospace’s AirVue suite aggregates flight, weather, and retail feeds, pushing updates across concourses and mobile apps to meet stringent service-level targets. Rail sits mid-table, with high-speed and metro lines upgrading amid legacy signaling constraints. ST Engineering’s AGIL system in Queensland showcases rail’s shift to video-analytics passenger counting and 5G gateways.

Aviation’s investment intensity accelerates platform standardization, influencing road and rail procurement. Airlines and airports demand cloud scalability to cope with peak seasons and irregular operations, setting performance benchmarks other modes are beginning to adopt. Conversely, bus agencies continue to prioritize cost-efficient rugged hardware and open data that facilitates third-party innovation. The Passenger Information Systems market thus exhibits modal cross-pollination, where breakthroughs in one sector rapidly diffuse into others, raising the baseline for user experience across transport.

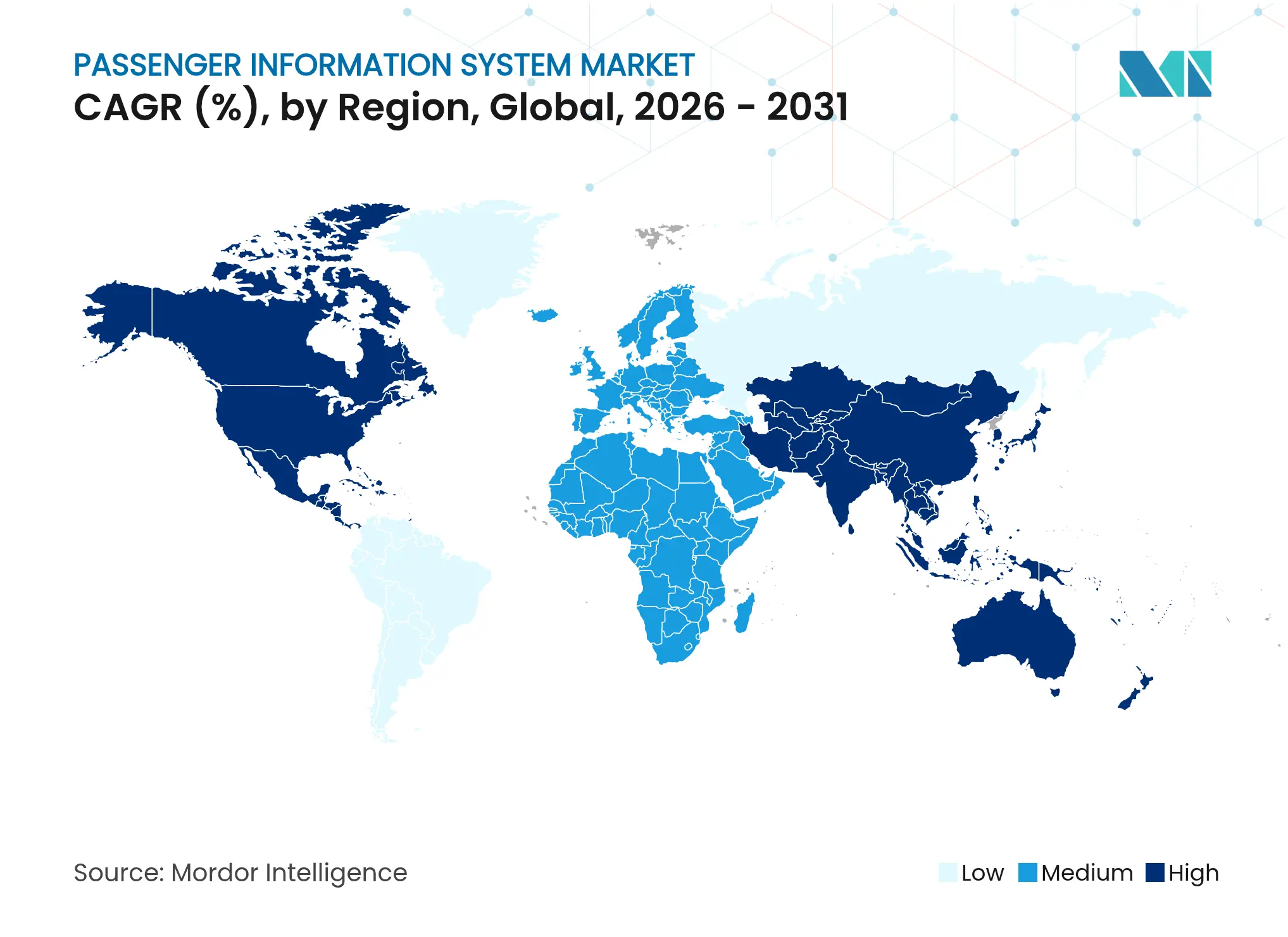

North America commanded 33.62% of 2025 revenue, thanks to decades of transit investment, early 5G rollout, and strict accessibility statutes that drive recurring upgrades. Federal programmes such as the USD 525,000 Nova Scotia demand-responsive grant illustrate ongoing policy support for digital transit. Agencies proceed cautiously, piloting USD 55,000 digital bus-stop signs in Chicago before large tenders. Legacy interoperability challenges and high labour costs temper speed, yet robust cybersecurity frameworks and telco partnerships allow sophisticated edge-AI pilots. Rural connectivity gaps persist, compelling investigation of Dedicated Short-Range Communications for resilience. Urban cores remain the revenue anchor, but suburban and rural programmes hold future upside.

Asia-Pacific is the Passenger Information Systems market’s fastest-growing region at 12.45% CAGR. Intense urbanisation, government-backed smart-city schemes, and tourism growth fuel demand for multilingual, cloud-native systems. Japan targets 45 million annual visitors by 2025, spurring installations of real-time translation displays at Haneda and Shinagawa. Hitachi’s USD 1.77 billion takeover of Thales Ground Transportation Systems doubled its engineering footprint, positioning the conglomerate for megaproject bids across the region. The region leads 5G rail pilots, as shown by CBTC-plus-5G tests in Hong Kong. Government funding typically bundles infrastructure with digital layers, compressing project timelines and widening supplier opportunities.

Europe maintains a sizeable share through regulatory harmonisation. Mandatory NeTEx and SIRI standards compel upgrades, creating a compliance-driven Passenger Information Systems market pipeline. Siemens Mobility’s EUR 2.8 billion deal with Deutsche Bahn to deploy digital signalling over a long-term horizon embodies the region’s shift toward framework contracts that assure integration continuity. Cross-border rail corridors prompt demand for multilingual, multimodal information services, while rural initiatives like RUMOBIL pilot innovative apps to connect low-density areas. Europe’s cybersecurity and data-privacy landscape adds complexity, yet fosters market entry for providers with robust compliance tooling.

Market Concentration

Competitive Landscape

The Passenger Information Systems market exhibits moderate fragmentation. Long-standing rail suppliers such as Siemens, Hitachi, and Wabtec leverage installed bases and integration know-how to win modernisation contracts. Their strengths lie in turnkey hardware plus software portfolios, now buttressed by acquisitions; Hitachi’s Thales deal exemplifies this consolidation[3]Hitachi Ltd., “Acquisition of Thales Ground Transportation,” hitachi.com. Mid-tier challengers differentiate through cloud-native, API-first architectures that interoperate with any display or vehicle bus, eroding vendor lock-in post-standardisation.

Competition pivots on analytics sophistication, real-time processing, and cybersecurity credentials. 5G edge nodes, predictive ML, and accessibility-focused features like Bluetooth Auracast hearing assistance represent key battlegrounds. Vendors race to secure certifications under evolving critical-infrastructure frameworks, as breaches threaten service continuity and passenger trust. Open data mandates in Europe lower barriers for nimble software firms that can plug into existing displays, pressuring incumbents to open interfaces or risk displacement.

Pricing models shift toward subscription bundles coupling hardware warranties with software updates. This realignment attracts venture-backed startups offering low-capex entry and usage-based billing. Established players respond by forming strategic alliances with telecom operators and cloud providers to provide end-to-end service-level agreements. Over the forecast horizon, market power is expected to coalesce around firms combining scale hardware supply chains, AI-driven software, and regulatory compliance toolkits.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECAST (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Passenger Information Systems (PIS) function as advanced digital communication platforms designed to deliver real-time updates to passengers utilizing public transportation networks, including buses, trains, subways, and airports. These systems play a critical role in enhancing the overall passenger experience by providing accurate, timely, and relevant information regarding travel schedules, potential delays, and other essential updates. By ensuring seamless communication, PIS contributes to improved operational efficiency and customer satisfaction within the public transportation sector.

The passenger Information System Market is Segmented by component (hardware, software, service), by solution (display system, announcement system, emergency communication system, mobile applications, video surveillance system emergency communication systems, others), by mode of transportation (railway, roadway, airway) and by geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segment.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.