Route Optimization Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

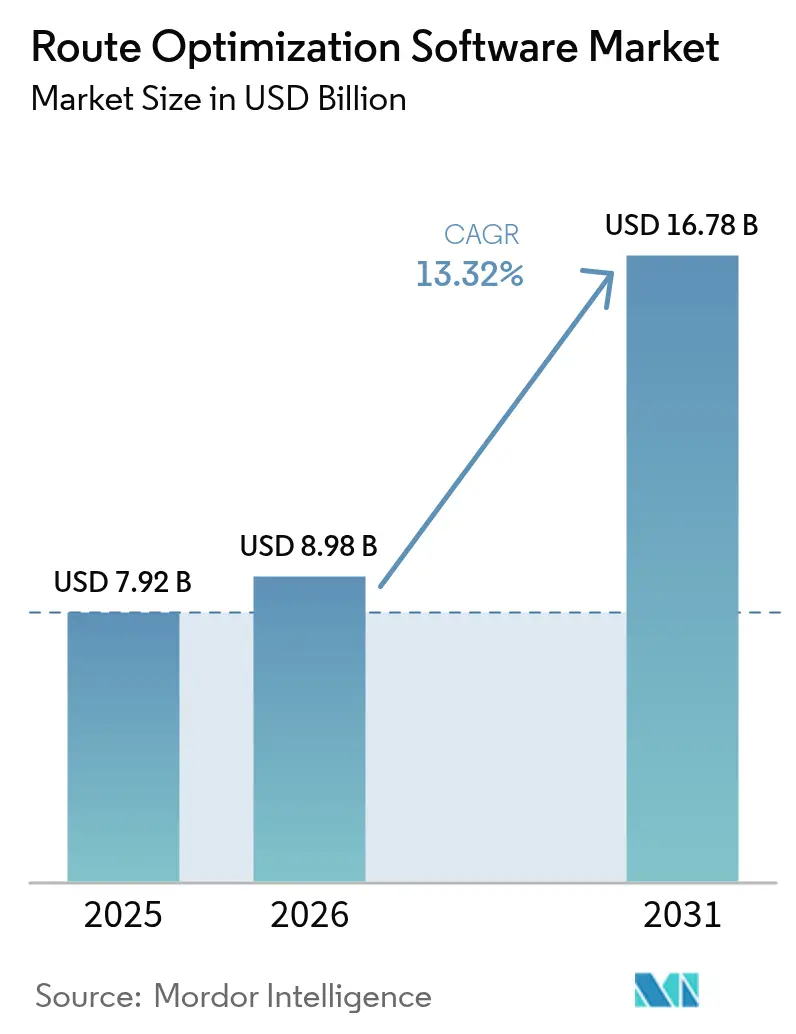

| Market Size (2026) | USD 8.98 Billion |

| Market Size (2031) | USD 16.78 Billion |

| Growth Rate (2026 - 2031) | 13.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

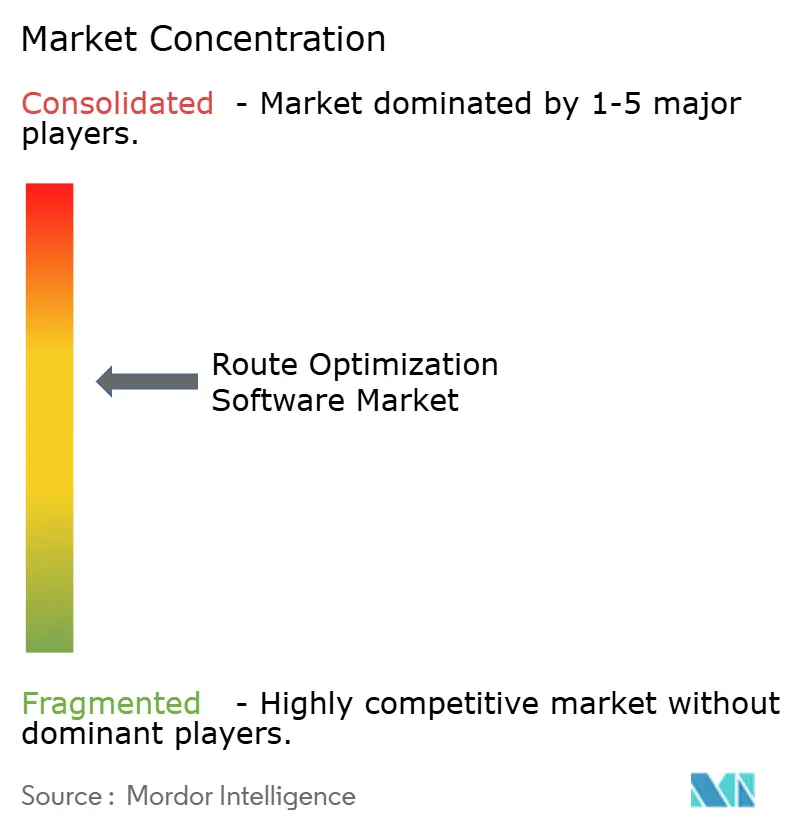

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Route Optimization Software Market Analysis by Mordor Intelligence

The Route Optimization Software market size was valued at USD 7.92 billion in 2025 and estimated to grow from USD 8.98 billion in 2026 to reach USD 16.78 billion by 2031, at a CAGR of 13.32% during the forecast period (2026-2031). Continuous e-commerce growth, artificial intelligence integration, and persistent driver shortages are reshaping logistics economics, spurring global adoption of automated route-planning engines. Cloud-native platforms accelerate deployment times, while 5G connectivity enables sub-second traffic recalculations that slash idle miles and overtime costs. Low-emission zone mandates, telematics–AI convergence, and national smart-logistics programs amplify demand as fleets seek to comply with environmental targets and labor constraints. Commercial offerings increasingly bundle predictive maintenance, driver safety analytics, and vehicle-agnostic optimization features, turning route software into a control tower for last-mile orchestration.

Key Report Takeaways

- By solution component, software platforms led with 62.15% revenue share of the Route Optimization Software market size in 2025, whereas services are expanding at a 14.08% CAGR through 2031.

- By end-user vertical, on-demand food delivery posted the fastest 15.03% CAGR through 2031, while retail and FMCG commanded 31.25% of the Route Optimization Software market share in 2025.

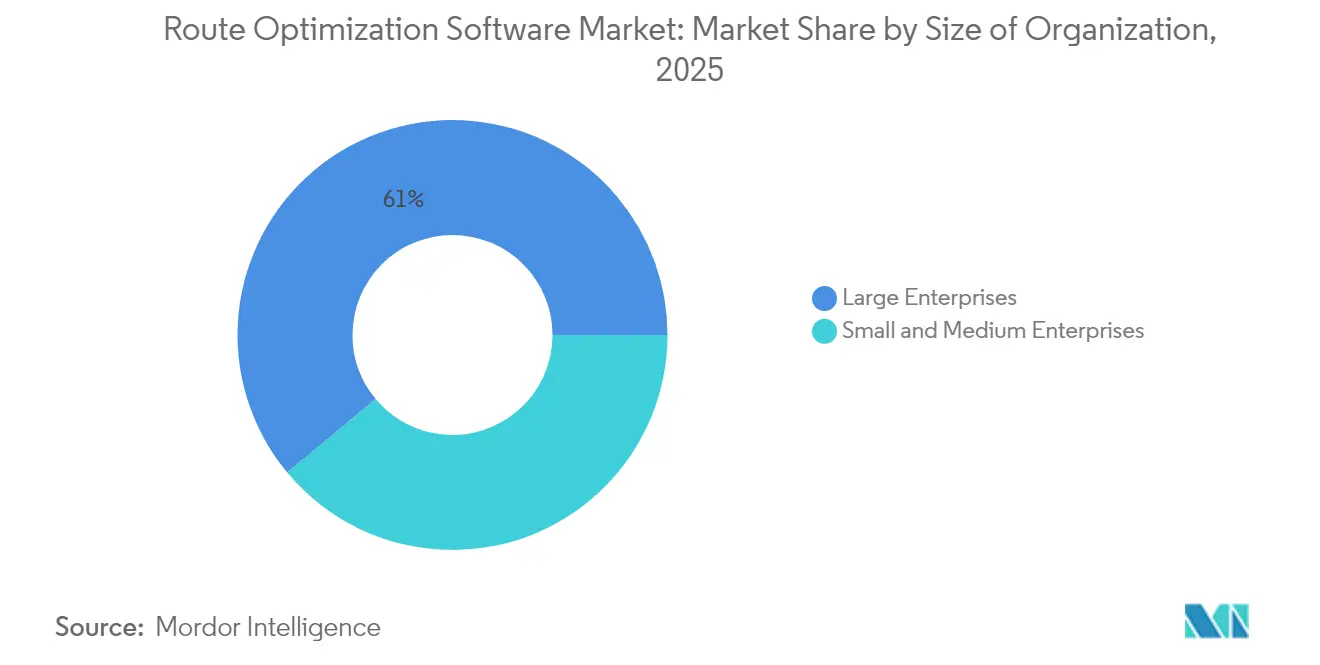

- By organization size, large enterprises accounted for 61.05% of the Route Optimization Software market size in 2025, yet SMEs record the highest 14.12% CAGR through 2031.

- By deployment mode, cloud solutions represented 65.74% of the Route Optimization Software market share in 2025 and are progressing at a 13.95% CAGR to 2031.

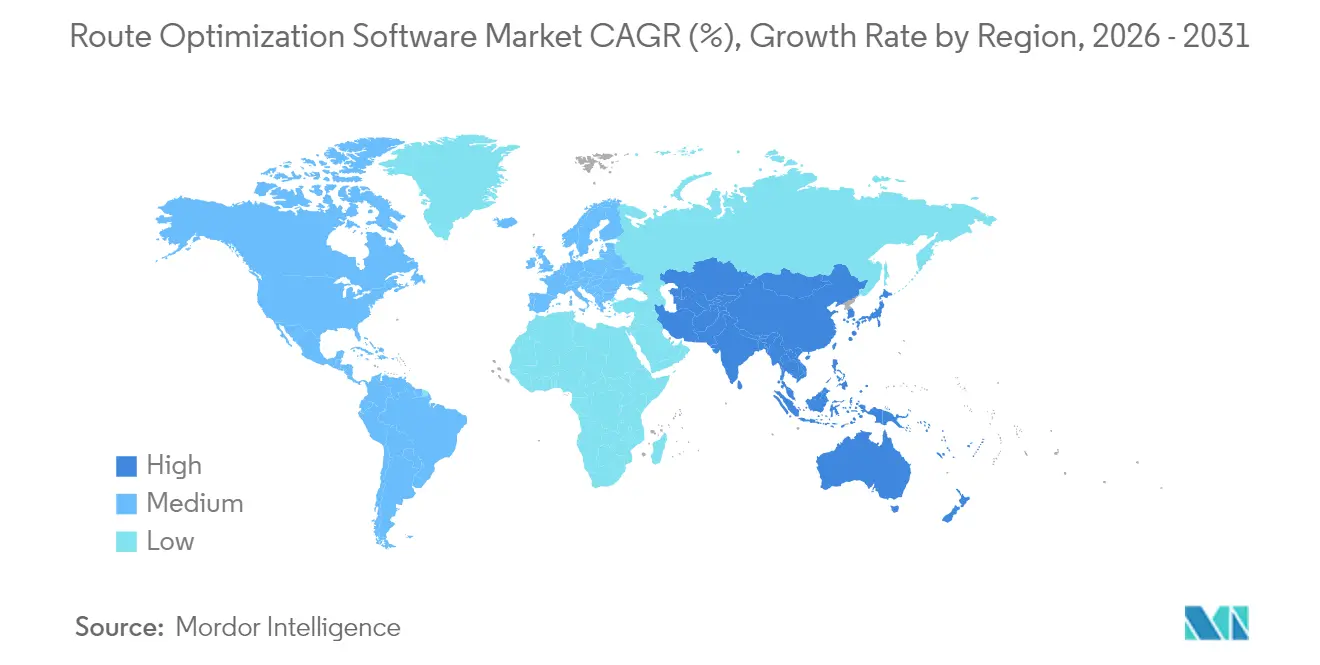

- By geography, North America captured 38.05% revenue share of the Route Optimization Software market in 2025, whereas Asia-Pacific is set to expand at a 14.82% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Route Optimization Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth in e-commerce parcel volume | +3.2% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Driver-assistance mandates from urban low-emission zones | +2.1% | Europe and select North American cities | Medium term (2-4 years) |

| 5G-enabled real-time optimization for gig economy fleets | +1.8% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Convergence of telematics and AI-powered route engines | +2.5% | Global | Long term (≥ 4 years) |

| Dynamic pricing models lowering TCO for SMB adopters | +1.4% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| National smart-logistics programs (e.g., EU DTLF, India ULIP) | +1.7% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth in E-commerce Parcel Volume

E-commerce parcels soared to multibillion annual counts, collapsing legacy hub-and-spoke models and forcing software providers to handle millions of dynamic delivery points within tight windows. Amazon alone processed over five billion packages in 2024, underscoring the need for algorithms that juggle inventory proximity, micro-fulfillment center locations, and real-time traffic predictions. High-density urban drops now require machine-learning engines able to pre-optimize routes from historical demand, weather, and driver behavior data. Platforms unable to deliver millisecond-level recalculations lose relevance as retailers scale omnichannel services and same-day promises.[1]Amazon.com, “Amazon Delivers Five Billion Packages in 2024,” amazon.com

5G-enabled Real-time Optimization for Gig-Economy Fleets

Millisecond latency from 5G and Multi-Access Edge Computing turns batch scheduling into continuous optimization. Food-delivery platforms leverage local network edges to recompute routes instantly when orders surge or traffic bottlenecks emerge. Edge nodes cut round-trip computation times to 1–10 milliseconds, meaning a driver can receive an updated drop sequence before the next traffic light. Coverage is still city-centric, so rural fleets experience fewer gains until national roll-outs mature.[2]GSMA, “5G Edge Computing for Logistics,” gsma.com

Convergence of Telematics and AI-powered Route Engines

Modern engines ingest vehicle diagnostics, fuel-burn curves, driver fatigue sensors, and live congestion feeds to maximize multiple objectives: cost, speed, emissions, and driver safety simultaneously. Predictive maintenance schedules now feed directly into route assignments, preventing breakdowns that derail tight delivery promises. Long-haul carriers report 1-2% fuel-burn reductions once AI models reorder delivery sequences based on historical terrain, load weight, and traffic cyclicality.[3]Daimler Truck AG, “Fuel-Smart Routing with AI Telematics,” daimlertruck.com

Dynamic Pricing Models Lowering TCO for SMB Adopters

Cloud platforms popularized pay-per-use and savings-share models that eliminate large upfront license fees. Local courier firms can deploy enterprise-grade optimization within days, capitalizing on shared algorithm improvements drawn from anonymized fleet data. Outcome-based contracts align vendor incentives with client productivity gains, accelerating adoption among cost-sensitive markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex data rights in crowdsourced driving datasets | -1.5% | Global, with stricter enforcement in Europe | Medium term (2-4 years) |

| Driver push-back against hyper-dense delivery schedules | -2.1% | Global, with concentration in developed markets | Short term (≤ 2 years) |

| Limited map accuracy in emerging markets rural networks | -1.2% | Asia-Pacific, Africa, and Latin America rural areas | Long term (≥ 4 years) |

| Fragmented last-mile regulations raising compliance cost | -1.8% | Global, with particular complexity in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Data Rights in Crowdsourced Driving Datasets

GDPR and similar statutes curtail the volume and granularity of behavioral data available for machine-learning pipelines. Software vendors must embed consent management, data lineage tracking, and selective deletion workflows that inflate compliance overhead. Smaller vendors lacking dedicated legal teams face barriers to cross-border expansion, nudging market concentration upward as well-capitalized players absorb compliance costs.[4]Europa.eu, “GDPR and Cross-Border Data Transfers,” europa.eu

Driver Push-back Against Hyper-dense Delivery Schedules

Field reports show that optimization algorithms often overlook curb-side realities, parking scarcities, building access codes, and dwell times, creating schedules drivers deem unrealistic. Unions and gig-driver coalitions have launched strikes across major metros, forcing fleets to insert buffer times and human override mechanisms. These manual interventions erode projected efficiency gains and can lengthen ROI horizons, especially where labor negotiations remain volatile.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Component: Services Growth Outpaces Platforms

Software platforms retained a 62.15% stake in the Route Optimization Software market share during 2025, reflecting their role as the backbone of automated dispatch systems. Consulting and integration services, though smaller in absolute value, are growing at 14.08% CAGR as enterprises grapple with multi-vendor IT landscapes and change-management hurdles. Implementers re-engineer warehouse workflows, transportation management system interfaces, and CRM notifications to unlock software-promised savings. Vendors increasingly bundle advisory engagements, recognizing that platform deployments without process redesign rarely achieve double-digit delivery-cost reductions.

Enterprises also lean on services teams for ongoing model-tuning, benchmarking, and edge-case exception handling, which are critical once fleets scale beyond pilot districts. As a result, recurring optimization-as-a-service contracts are cannibalizing perpetual licenses, smoothing revenue streams for providers. The Route Optimization Software market size allocated to professional services is expected to cross USD 4.72 billion by 2031, signaling a shift toward outcome-based collaboration models.

By End-user Vertical: Food Delivery Drives Fastest Growth

Retail and FMCG suppliers dominated revenue, yet on-demand food delivery is accelerating with a 15.03% CAGR as 30-minute promise windows become a competitive baseline. The Route Optimization Software market size tied to meal-delivery fleets will exceed USD 2.32 billion by 2031, fueled by dynamic rider pools and perishable payloads that demand real-time recalculations. Algorithms must re-optimize routes every few minutes, balancing heat-loss constraints and kitchen throughput.

Field services, healthcare, and ride-hailing each require tailored constraint libraries, temperature monitoring for pharmaceuticals, technician skill matching, or driver re-positioning models. Such verticalization spurs vendors to release plug-ins rather than one-size-fits-all engines, fragmenting the platform landscape but lifting total addressable value across specialized niches.

By Size of Organization: SMEs Embrace Cloud-native Solutions

Large multinationals held 61.05% of the Route Optimization Software market size in 2025, deploying sophisticated multi-modal coordinators that integrate air cargo, rail, and drayage legs. However, SMEs display the strongest 14.12% CAGR because cloud deployments slash infrastructure and support burdens. Usage-based fees align with sporadic shipment volumes, making optimization economical for regional couriers and specialty distributors.

SME uptake is also propelled by intuitive dashboards and wizard-based route builders that forego steep learning curves. As marketplaces and e-commerce platforms embed “optimize” buttons within seller portals, micro-merchants gain one-click access to routing intelligence once reserved for enterprises. This democratization widens competitive parity, pressuring incumbents to investigate hyper-local service guarantees.

By Deployment Mode: Cloud Dominance Reflects Real-time Requirements

Cloud configurations captured 65.74% of the Route Optimization Software market share in 2025 and are tracking a 13.95% CAGR through 2031. Real-time API calls to traffic, weather, and point-of-delivery confirmation systems saturate bandwidth that on-premise instances struggle to provision. Auto-scaling elasticity handles seasonal spikes, holiday e-commerce, and harvest logistics without cap-ex overruns.

Nevertheless, sectors handling sensitive military or pharmaceutical payloads persist with on-premise or hybrid deployments. Edge-optimized appliances now run localized optimization for minute-by-minute updates while synchronizing anonymized aggregates to cloud models for fleet-wide learning. Such architectures blend compliance with innovation, a compromise likely to sustain a double-digit hybrid footprint across heavily regulated verticals.

Geography Analysis

North America commanded 38.05% of 2025 revenue, buoyed by e-commerce maturity and acute driver shortages that make algorithmic mileage savings mission-critical. Amazon’s proprietary systems set benchmarks that ripple through competitors, while Canada leverages cross-border modules to synchronize NAFTA corridors. Mexico’s manufacturing upswing drives inbound-outbound balancing algorithms that minimize empty miles across industrial clusters. Regional regulatory stances toward data sharing remain comparatively lenient, enabling rapid roll-out of driver-behavior training and fuel-savings dashboards.

Asia-Pacific is the fastest-expanding theatre, clocking a 14.82% CAGR on the back of megacity congestion and state-sponsored digital logistics schemes. India’s ULIP ushers standardized data pipes among 500-plus carriers, allowing small fleets to tap shared optimization engines without bespoke integrations. China’s 5G-blanketed metros support sub-second recalculations for grocery and parcel delivery swarms, while Japan’s “2024 Problem” overtime cap mandates productivity jumps to keep freight flowing despite constrained driver hours. Southeast Asian growth rides on smartphone-first commerce, cloud penetration, and rising export-oriented manufacturing zones requiring synchronized port logistics.

Europe exhibits steady uptake driven by environmental regulation. Low-emission zones across more than 250 cities impose time-window and payload constraints that only AI-enhanced routing can satisfy economically. The EU’s Digital Transport and Logistics Forum releases harmonized APIs that trim compliance costs for cross-border consignments. Yet GDPR’s stringent consent rules restrain crowdsourced telemetry usage, nudging vendors to pioneer privacy-preserving learning techniques such as federated optimization and differential masking.

Mordor Intelligence provides coverage of the route optimization software market across other key regional markets. Detailed country-level analysis extends to United Kingdom incorporating local coverage and market participation, as required.

Competitive Landscape

The Route Optimization Software market features moderate fragmentation, but consolidation trends are unmistakable as telematics giants acquire niche AI specialists. Trimble’s 2025 partnership with Microsoft Azure adds predictive maintenance, folding route planning into broader fleet-health ecosystems. Verizon Connect exploits its 5G backbone to launch sub-second rerouting, differentiating against legacy batch-processing rivals. ORTEC extends capabilities into electric-vehicle range modeling, positioning for fleets migrating to zero-emission vans.

Emerging cloud-native entrants court SMEs with wizard-driven UIs and pay-per-delivery pricing, capturing share in segments historically underserved by enterprise-centric suites. Vertical specialists such as Locus.sh for healthcare logistics and Bringg for driver coaching underscore the value of domain-specific constraint libraries. Intellectual property moats revolve around real-time compute architectures, federated privacy safeguards, and proprietary data partnerships with mapping or traffic-sensor providers. Market incumbents must either accelerate in-house AI investments or pursue tuck-in acquisitions to stave off niche erosion.

Route Optimization Software Industry Leaders

Trimble Inc.

Verizon Connect Solutions Inc.

The Descartes Systems Group Inc.

Omnitracs LLC

ORTEC B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Trimble integrated its route platform with Microsoft’s Azure IoT to enable predictive maintenance scheduling across 10,000-plus vehicles in North America and Europe.

- August 2025: Verizon Connect released 5G-powered dynamic routing across 15 U.S. metros, promising sub-second recalculations during peak traffic.

- July 2025: The EU Digital Transport and Logistics Forum published standardized APIs for cross-border route optimization, lowering compliance overhead for pan-European carriers.

- June 2025: ORTEC unveiled an electric-vehicle range-aware module incorporating charger availability and dwell-time optimization.

- May 2025: India’s ULIP went fully live, connecting 500 logistics providers with standardized data-exchange interfaces that feed national optimization engines.

- April 2025: Descartes Systems acquired a last-mile optimization specialist for USD 125 million to enhance urban delivery orchestration capabilities.

Global Route Optimization Software Market Report Scope

The route optimization software market is defined based on the revenues generated from the software used in various end-user verticals across the world. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting its growth in terms of drivers and restraints.

The route optimization software market is segmented by end-user vertical (on-demand food delivery, retail, and FMCG, ride-hailing and taxi services, and other end-user verticals), size of the organization (small and medium enterprises, large enterprises), deployment mode (cloud, on-premises), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Software Platforms |

| Services |

| On-Demand Food Delivery |

| Retail and FMCG |

| Field Services |

| Ride Hailing and Taxi Services |

| Healthcare and Pharmaceuticals |

| Other End-user Verticals |

| Small and Medium Enterprises |

| Large Enterprises |

| Cloud |

| On-Premise |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Solution Component | Software Platforms | ||

| Services | |||

| By End-user Vertical | On-Demand Food Delivery | ||

| Retail and FMCG | |||

| Field Services | |||

| Ride Hailing and Taxi Services | |||

| Healthcare and Pharmaceuticals | |||

| Other End-user Verticals | |||

| By Size of the Organization | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected CAGR for the Route Optimization Software market to 2031?

The market is slated to expand at a 13.32% CAGR from 2026 to 2031.

Which region will register the fastest growth through 2031?

Asia-Pacific leads with a 14.82% CAGR driven by smart-logistics programs and 5G coverage.

Why are services growing faster than software platforms?

Enterprises need integration, change management, and model-tuning expertise to capture full optimization benefits, pushing services to a 14.08% CAGR.

How are 5G networks influencing route optimization?

5G enables sub-second route recalculations via edge computing, enhancing real-time fleet responsiveness in dense urban areas.

What challenges limit software adoption among fleets?

Data-privacy compliance, driver push-back against dense schedules, and inconsistent rural mapping accuracy temper adoption rates.

How are SMEs benefiting from cloud-native route solutions?

Usage-based fees and no-infrastructure deployments allow SMEs to deploy enterprise-grade optimization quickly and cost-effectively.

Page last updated on: