Autonomous Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

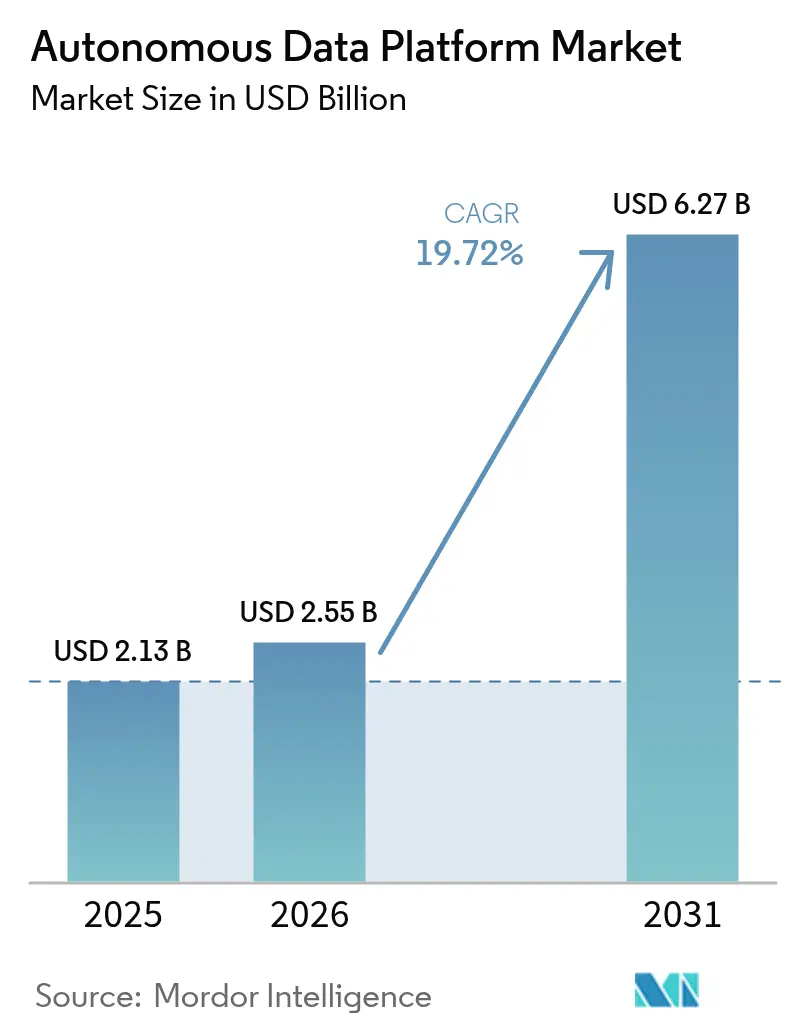

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 6.27 Billion |

| Growth Rate (2026 - 2031) | 19.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Data Platform Market Analysis by Mordor Intelligence

The autonomous data platform market size is expected to grow from USD 2.13 billion in 2025 to USD 2.55 billion in 2026 and is forecast to reach USD 6.27 billion by 2031 at 19.72% CAGR over 2026-2031. This growth path shows how enterprises are shifting from manually tuned data stacks toward fully autonomous, AI-first operations that reduce human intervention in storage, optimization, and lifecycle management. Cloud hyperscalers have turned autonomy into a core feature of their infrastructure portfolios, allowing users to provision, govern, and scale databases without specialized skills. Falling storage costs now let companies keep petabyte-scale historical data online, improving model accuracy and time-series analytics at manageable budgets. At the same time, regional data-sovereignty laws force organizations to architect multiregional replication strategies, creating demand for platforms that deliver low-latency performance while still enforcing residency controls. Competitive intensity is rising as established database vendors, lake house specialists, and hyperscalers race to embed automated performance tuning, self-healing features, and integrated Gen-AI copilots that democratize complex tasks.

Key Report Takeaways

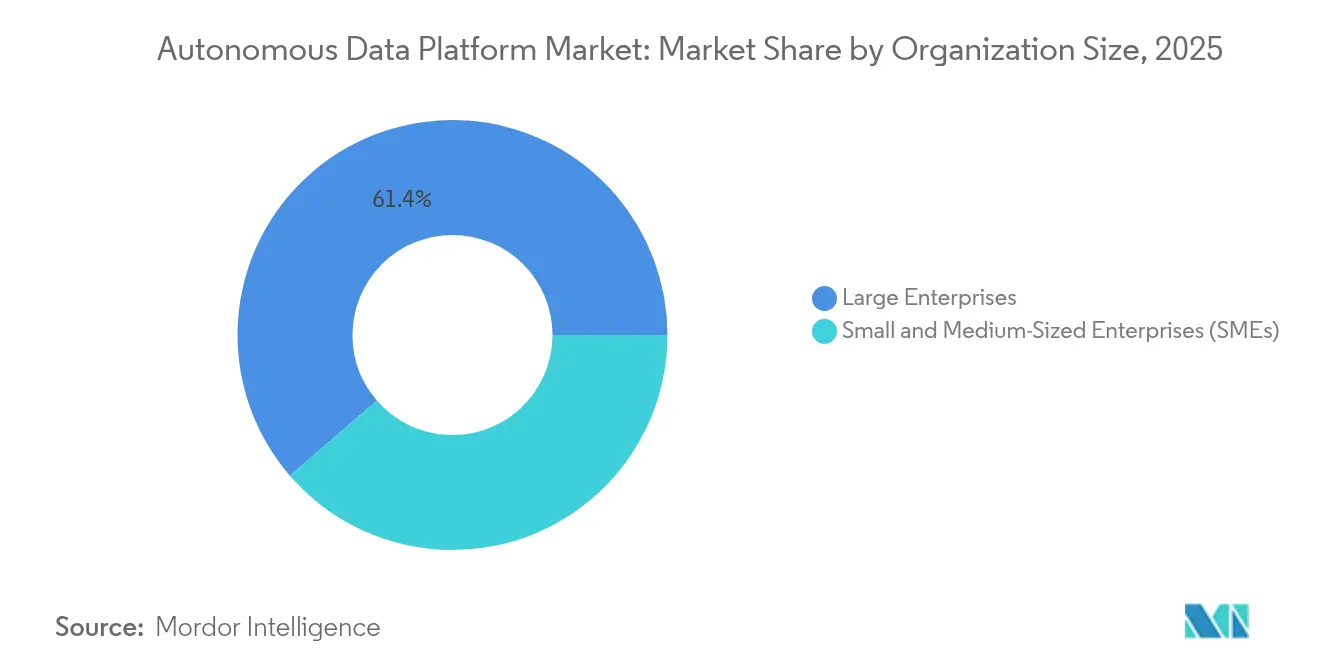

- By organization size, large enterprises held 61.35% of the autonomous data platform market share in 2025, while small and medium-sized enterprises are advancing at a 25.18% CAGR through 2031.

- By deployment type, the public-cloud segment captured 53.20% revenue share in 2025; hybrid configurations are forecast to expand at a 28.14% CAGR to 2031.

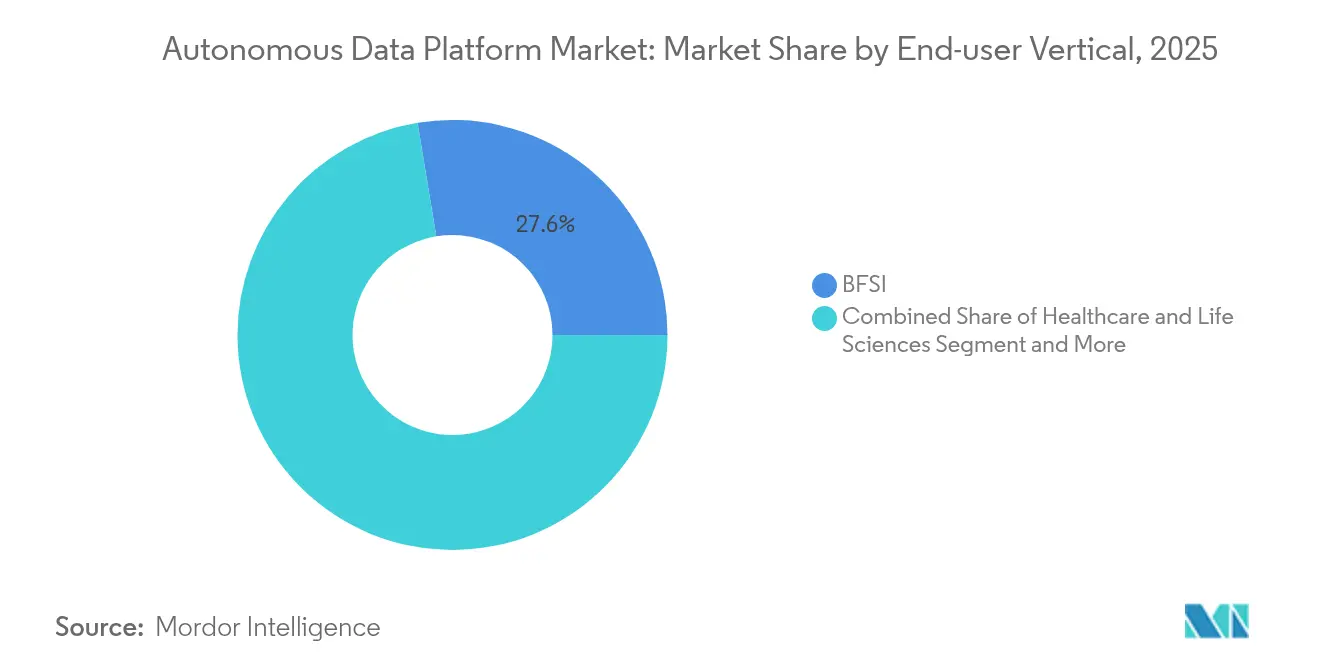

- By end-user vertical, banking, financial services, and insurance led with a 27.60% share of the autonomous data platform market size in 2025, whereas healthcare and life sciences are growing at a 24.61% CAGR through 2031.

- By component, platform and solution offerings accounted for a 69.20% share in 2025, while managed services are expanding at a 26.29% CAGR to 2031.

- By data type, unstructured data processing commanded a 56.30% share of the autonomous data platform market size in 2025, and semi-structured workloads are rising at a 29.76% CAGR through 2031.

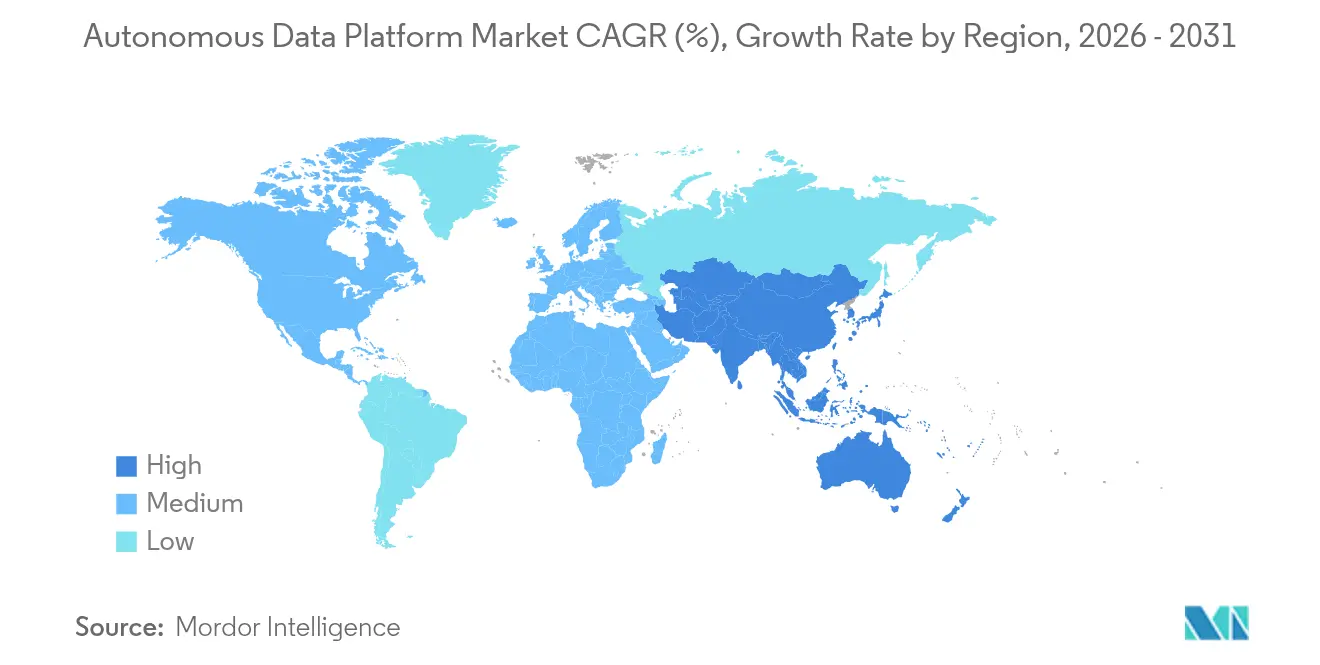

- By geography, North America led with 40.60% revenue share in 2025; the Asia-Pacific region is on track for a 22.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autonomous Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-first data-ops strategies adopted by cloud hyperscalers | 4.20% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rapid fall in data-storage cost enabling petabyte-scale ingestion | 3.80% | Global, particularly benefiting APAC emerging markets | Short term (≤ 2 years) |

| Rising enterprise move toward data-mesh & fabric architectures | 3.10% | North America and Europe leading, APAC following | Long term (≥ 4 years) |

| Mandatory data-residency/sovereign-cloud rules in Europe & APAC | 2.90% | Europe and APAC core, spillover to MEA | Medium term (2-4 years) |

| Integration of Gen-AI copilots for low-code data engineering | 2.70% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Industry-specific packaged analytics accelerators (banking, life-science) | 2.10% | Global, sector-specific concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-first data-ops strategies adopted by cloud hyperscalers

Cloud providers have begun embedding autonomous optimization, self-patching, and self-scaling directly into baseline services. Amazon earmarked USD 100 billion for AWS AI infrastructure in 2025, signalling that autonomy is now table stakes for large-scale data operations. Snowflake’s partnership with NVIDIA makes specialized retrieval and inference tooling available inside the data platform, removing the traditional gap between storage and model execution. Oracle’s autonomous database revenue jumped 104% year-over-year in fiscal 2025 as firms moved away from manual optimization to real-time, self-tuning services. These developments cut administration costs and shorten analytics cycles from hours to minutes, enabling frontline teams to run live experiments on production-grade datasets. [1]Jordan Novet, “Oracle shares climb 8% as earnings, revenue top estimates,” CNBC, cnbc.com

Rapid fall in storage cost enabling petabyte-scale ingestion

The National Academies projects installed storage capacity will cross 26.3 zettabytes by 2030 while cost per terabyte keeps dropping. Enterprises can now keep historical video, sensor, and document archives online, raising AI model accuracy without prohibitive budgets. Western Digital research shows hard-disk drives still deliver favourable total cost of ownership for bulk data, so firms maintain cold-tier lakes without sacrificing margin. TELUS migrated 14 petabytes to Google BigQuery, shed 30% obsolete data, and optimized 200 pipelines that feed new Gen-AI use cases. Lower storage barriers push the autonomous data platform market toward always-on ingestion that fuels predictive systems and multimodal AI. [2]Google Cloud, “Telus Case Study,” cloud.google.com

Rising enterprise move toward data-mesh and data-fabric architectures

Enterprises are breaking up centralized warehouses and delegating ownership to domain teams that treat “data as a product.” Siemens built an enterprise-wide mesh on Snowflake that accelerates innovation and keeps governance centralized yet lightweight. German manufacturers report that traditional ETL pipelines cannot keep pace with demand for real-time analytics, forcing cultural change alongside technology upgrades. ABB unified 40 disparate ERP systems under a single mesh, unlocking multimillion-dollar savings and revenue growth. With data spread across business lines, autonomous platforms must self-discover metadata, auto-catalogue assets, and enforce policies at the edge.

Mandatory sovereignty rules in Europe and APAC

The EU Data Act enforces cloud portability and fee-free exits by 2027, reshaping provider selection criteria. India’s Digital Personal Data Protection Act and Japan’s pending AI Basic Law add regional layers that compel local replication, auditing, and policy enforcement. Amazon will invest AU$20 billion to build Australian data centers through 2029, reflecting how hyperscale’s chase compliance-ready regions. Enterprises that master multiregional governance gain faster market entry and reduced regulatory friction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing skills gap for composite AI and MLOps orchestration | -2.80% | Global, particularly acute in APAC and emerging markets | Long term (≥ 4 years) |

| Escalating cloud egress fees impacting TCO | -2.10% | Global, with higher impact on multi-cloud deployments | Short term (≤ 2 years) |

| Persistent security debt from legacy ETL pipelines | -1.90% | North America and Europe, legacy system concentration | Medium term (2-4 years) |

| Vendor lock-in concerns hindering multicloud portability | -1.60% | Global, affecting large enterprise segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ongoing skills gap for composite AI and MLOps orchestration

End-to-end autonomous systems need niche skills covering distributed architectures, model governance, and real-time streaming. Upskilling programs such as IVADO’s MLOps boot camp attempt to shrink the gap yet demand still outstrips supply. A Fortune 100 healthcare firm relied on TrueFoundry specialists to deploy 30+ LLM use cases, cutting time-to-value but underscoring workforce dependence on outside talent. Without internal expertise, organizations struggle to operationalize autonomous features at scale, dampening ROI and adoption pace.

Escalating cloud egress fees impacting TCO

Large data transfers among clouds can double operating costs, especially for AI training workloads that shuffle terabytes daily. Google scrapped egress fees for customer exits, but AWS and Azure charges remain. Oracle offers 10 TB free each month, positioning itself as a lower-cost alternative for multicloud architectures. When fees surpass compute spend, architects may co-locate workloads sub-optimally, reducing the performance gains autonomy promises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Advance Platform Democratization

Large enterprises currently generate most revenue with a market share of 61.35%, yet small and medium-sized firms fuel the fastest expansion of the autonomous data platform market. The autonomous data platform market size attributable to SMEs is projected to widen swiftly thanks to natural-language copilots that replace code-heavy interfaces. Prophecy’s transformation assistant lets functional teams at consumer-focused brands orchestrate data flows without engineering backlogs. Meanwhile, mega-enterprises rely on federated data-mesh rollouts across geographies and business units, driving complex governance implementations that sustain platform vendors’ enterprise licensing streams.

SMEs view autonomous data tools as an equalizer that shortens innovation cycles. Case studies such as F45 Training’s deployment with Fiveonefour illustrate tangible returns, reporting 50% cost reductions and 10× faster development cycles on consumer analytics pipelines. As accessible pricing tiers spread, the autonomous data platform market gains a broader long-tail customer base, challenging vendors to maintain usability while preserving advanced enterprise functionality.

By Deployment Type: Hybrid Configurations Address Sovereignty Requirements

Public-cloud services deliver the bulk of current spending, yet hybrid models expand at a pace that reshapes the autonomous data platform market. Sovereignty concerns and performance optimization drive enterprises to keep sensitive workloads on-premises while bursting analytics and AI training to scalable public resources. Deutsche Bank’s phased data-platform migration blended on-premises systems with Google Cloud services for 20 million customers, proving hybrid’s compliance value.

The autonomous data platform market size tied to hybrid deployments is forecast to accelerate as frameworks such as the EU Data Act compel portability. Oracle’s Cloud@Customer nodal offering appeals to firms seeking public-cloud autonomy inside private facilities, indicating that location-agnostic control planes will define competitive positioning. Pure private-cloud growth slows because in-house hardware and skills cannot match public-cloud innovation velocity, nudging firms toward hybrid compromises.

By End-User Vertical: Healthcare Accelerates Through AI Integration

BFSI remains the single largest adopter with 27.60%, yet healthcare and life sciences produce the steepest trajectories in the autonomous data platform market. Banking institutions employ real-time risk scoring to meet tightening capital and liquidity mandates, whereas pharmaceutical leaders such as Sanofi use autonomous lake houses to speed analysis of real-world clinical data.

Health-sector growth is amplified by vast image, genomic, and clinical-trial files that benefit from autonomous scaling and policy-based lifecycle management. Sanofi reported accelerated drug-discovery analytics after moving workloads to Snowpark, underscoring the sector’s appetite for turnkey compliance and compute elasticity. Consequently, vendors craft HIPAA-ready blueprints and 21 CFR Part 11 attestations to win share as the autonomous data platform market expands in regulated life-science domains.

By Component: Managed Services Address Complexity Challenges

Platform software still captures most spending, yet managed services record the sharpest climbs because many enterprises outsource operations that exceed internal abilities. Fidelity Investments operates hundreds of models but cautions that creativity must coexist with governance, inspiring demand for managed MLOps orchestration. The autonomous data platform market size credited to managed services will keep widening as organizations favour outcome-based contracts that guarantee uptime, latency, and cost thresholds.

Vendors respond by bundling run-operations with product licenses or partnering with service specialists. ServiceNow’s acquisition of data. World shows how cataloging, lineage, and workflow automation converge under service umbrellas, offering a cradle-to-grave data pipeline managed by one provider. Differentiation increasingly hinges on measurable value such as performance benchmarks and financial savings rather than feature lists alone.

Geography Analysis

North America commanded 40.60% of autonomous data platform market share in 2025, underpinned by early adoption of AI-first strategies and substantial data-center investments. Amazon alone plans USD 150 billion for additional facilities that will run GPU clusters needed for large language models. Oracle’s infrastructure revenue surged 70% year-over-year in fiscal 2025 as enterprises embraced self-tuning databases that meet stringent uptime and compliance standards. A mature venture ecosystem funds specialized startups focusing on data observability, cataloging, and real-time AI, further enriching the regional technology stack.

The Asia-Pacific region shows the fastest CAGR at 22.54%, driven by India’s data-protection framework and Japan’s AI Basic Law proposal, both of which require tightly governed yet innovation-friendly platforms. Government programs funding digital public infrastructure shorten procurement cycles, letting firms adopt autonomous solutions early in their modernization journeys. Hyperscalers rapidly expand local zones to meet residency rules, while regional service providers create sovereign platforms that integrate with global clouds through standardized APIs.

Europe sustains growth through privacy leadership and the new Data Act, which mandates vendor-agnostic portability. Platform providers respond with open-format catalogs and zero-copy data-sharing innovations to reduce exit friction. The region’s insistence on explainability and audit trails favors autonomous platforms that embed lineage tracking and AI model governance by default. South America, the Middle East, and Africa trail in current adoption but show high project pipelines as telecom operators, banks, and public agencies pursue cloud-first roadmaps that leapfrog legacy infrastructure.

Competitive Landscape

Competition centers on a handful of scale players contending with nimble specialists. Snowflake, Databricks, Oracle, and the hyperscale clouds invest heavily in autonomous optimizers, Gen-AI assistants, and cross-cloud interoperability. Snowflake’s patent portfolio spans adaptive query aggregation and zero-copy sharing, reinforcing its data-cloud vision. Databricks fuses structured and unstructured analytics under the lakehouse, while Oracle touts self-patching databases that run on dedicated, security-hardened hardware.

Acquisition activity underscores the premium on differentiated AI capabilities. Snowflake’s planned purchase of Crunchy Data aims to bring fully managed PostgreSQL into its ecosystem, whereas IBM’s intent to buy DataStax targets NoSQL and vector search features vital for retrieval-augmented generation. ServiceNow’s move for data. world blends workflow orchestration with cataloging, extending platform influence deeper into operational processes.

Emerging ventures focus on data mesh, domain accelerators, and observability. Many position themselves as neutral layers that sit above hyperscalers, promising reduced lock-in. Patent filings on auto-indexing, cache management, and privacy-preserving query rewrite signal perpetual innovation. Price competition intensifies around storage compression and autonomous workload placement, while value discussions shift toward measurable outcomes such as time-to-insight and cost-per-query rather than raw capacity. [4]Chris Zeoli, “Data platforms Snowflake and Databricks acquiring model developers,” DataGravity, datagravity.dev

Autonomous Data Platform Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Snowflake Inc.

Oracle Corporation

Databricks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Snowflake announced agreement to acquire Crunchy Data to create an enterprise-ready PostgreSQL service.

- June 2025: Oracle reported fiscal 2025 Q4 revenue of USD 15.9 billion with cloud revenue at USD 6.7 billion, predicting >40% cloud growth in fiscal 2026.

- June 2025: Databricks projected annualized revenue of USD 3.7 billion with nearly 50 clients each spending over USD 10 million.

- May 2025: ServiceNow acquired data.world to augment cataloging and governance capabilities.

Global Autonomous Data Platform Market Report Scope

An autonomous data tool analyzes a specific customer's big data infrastructure to address essential business problems and assure optimal database usage. This supports businesses to develop and enhance their data management abilities. They are specifically created to control and optimize big data infrastructure. Many firms are embracing this platform because it encourages the IT professional to manage processes more efficiently.

| Large Enterprises |

| Small and Medium-Sized Enterprises (SMEs) |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Retail and Consumer Goods |

| Media and Telecommunications |

| Government and Public Sector |

| Manufacturing |

| Platform / Solution | |

| Services | Professional Services |

| Managed Services |

| Structured Data |

| Semi-Structured Data |

| Unstructured Data |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises (SMEs) | |||

| By Deployment Type | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By End-user Vertical | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Retail and Consumer Goods | |||

| Media and Telecommunications | |||

| Government and Public Sector | |||

| Manufacturing | |||

| By Component | Platform / Solution | ||

| Services | Professional Services | ||

| Managed Services | |||

| By Data Type | Structured Data | ||

| Semi-Structured Data | |||

| Unstructured Data | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

.What is the current size and growth outlook for the autonomous data platform market?

The autonomous data platform market reached USD 2.55 billion in 2026 and is on course for USD 6.27 billion by 2031, posting a 19.72% CAGR.

Which deployment model is growing fastest?

Hybrid cloud configurations are expanding at a 28.14% CAGR as firms balance latency, cost, and data-sovereignty obligations.

Why are healthcare and life-science firms adopting autonomous data platforms rapidly?

They need to process large clinical and genomic datasets securely and at speed, driving a 24.61% CAGR for the vertical through 2031.

How do sovereignty regulations influence platform choice?

Mandates such as the EU Data Act require easy portability and local data residency, pushing enterprises toward providers with multiregional compliance features.

What role do managed services play in adoption?

Managed services offset skills shortages in MLOps and governance, growing at a 26.29% CAGR as organizations seek turnkey operations.

What is the biggest technical restraint hindering wider rollout?

A persistent skills gap in composite AI and distributed MLOps orchestration slows enterprise ability to harness full autonomy, reducing overall CAGR by an estimated 2.8%.

Page last updated on: