Mobile Mapping System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

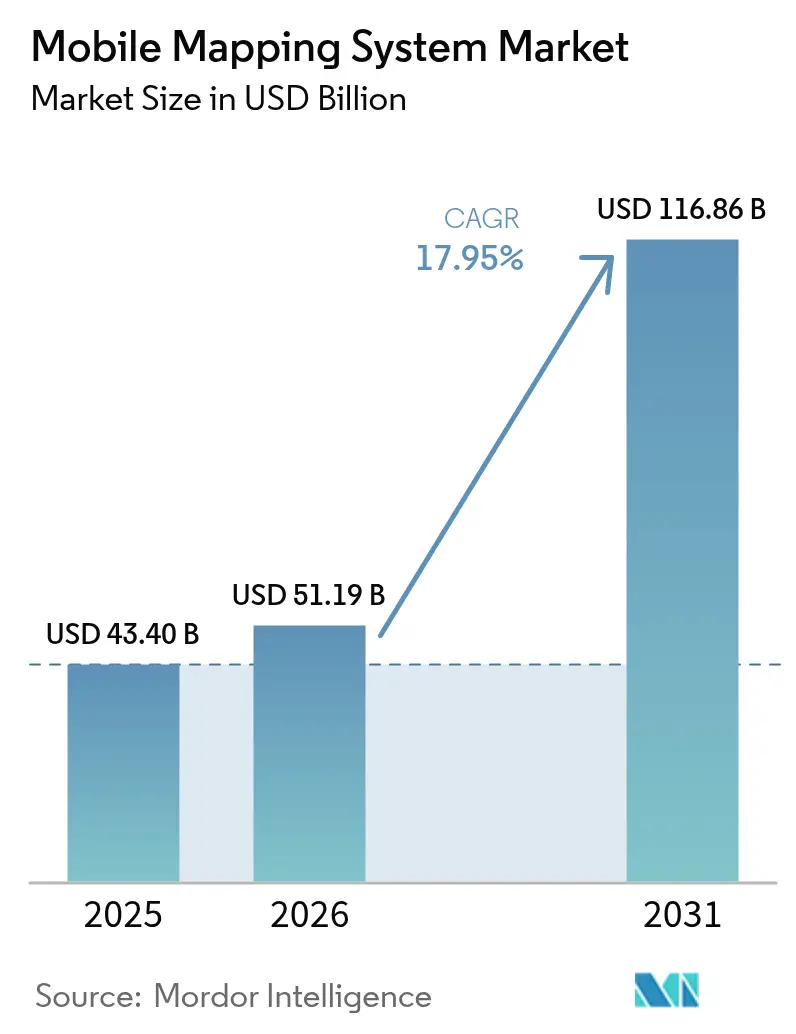

| Market Size (2026) | USD 51.19 Billion |

| Market Size (2031) | USD 116.86 Billion |

| Growth Rate (2026 - 2031) | 17.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Mapping System Market Analysis by Mordor Intelligence

The mobile mapping system market size was valued at USD 43.4 billion in 2025 and estimated to grow from USD 51.19 billion in 2026 to reach USD 116.86 billion by 2031, at a CAGR of 17.95% during the forecast period (2026-2031). Enterprise-grade feature extraction powered by artificial intelligence and steadily falling solid-state LiDAR prices continued to reshape acquisition economics, improving margins for service providers and end users. Government digital-twin mandates, the rise of vehicle-agnostic sensor payloads, and new subscription business models expanded adoption in infrastructure, mining, and emergency management. Meanwhile, vendors increased software integrations that shorten data-to-decision cycles, broadening the mobile mapping system market addressable base and intensifying competition around value-added analytics.

Key Report Takeaways

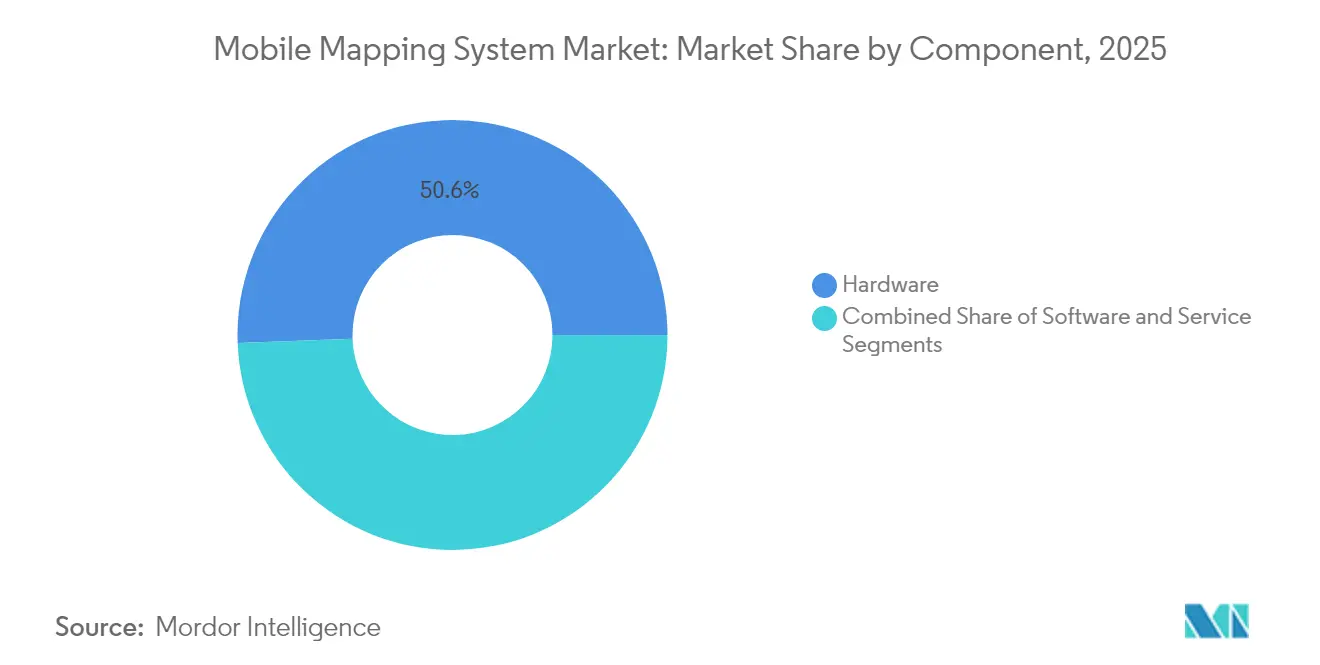

- By component, hardware led with 50.60% of the mobile mapping system market share in 2025; services are forecast to expand at a 20.10% CAGR to 2031.

- By mounting type, vehicle-mounted platforms held 61.30% revenue share in 2025, while drone systems are advancing at a 21.10% CAGR through 2031.

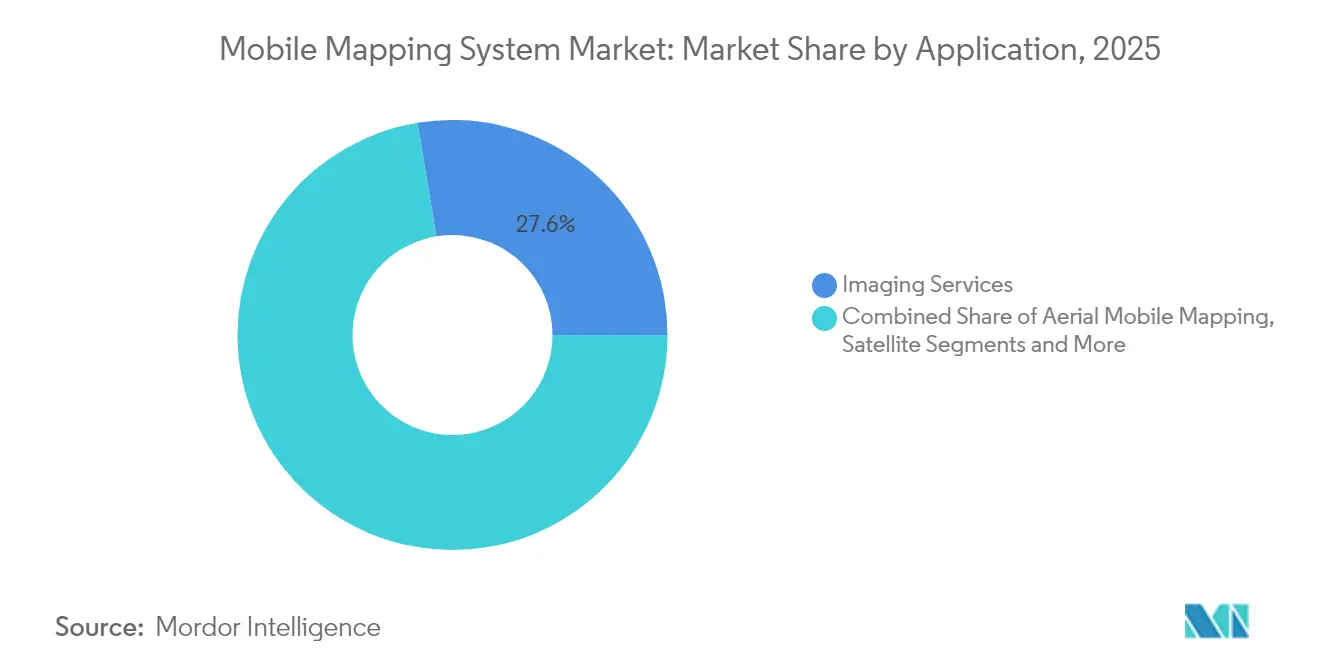

- By application, imaging services commanded a 27.60% share of the mobile mapping system market size in 2025, and emergency-response planning is growing at a 20.60% CAGR.

- By end-user vertical, government agencies accounted for a 34.60% share in 2025; mining is projected to expand at a 19.20% CAGR between 2026-2031.

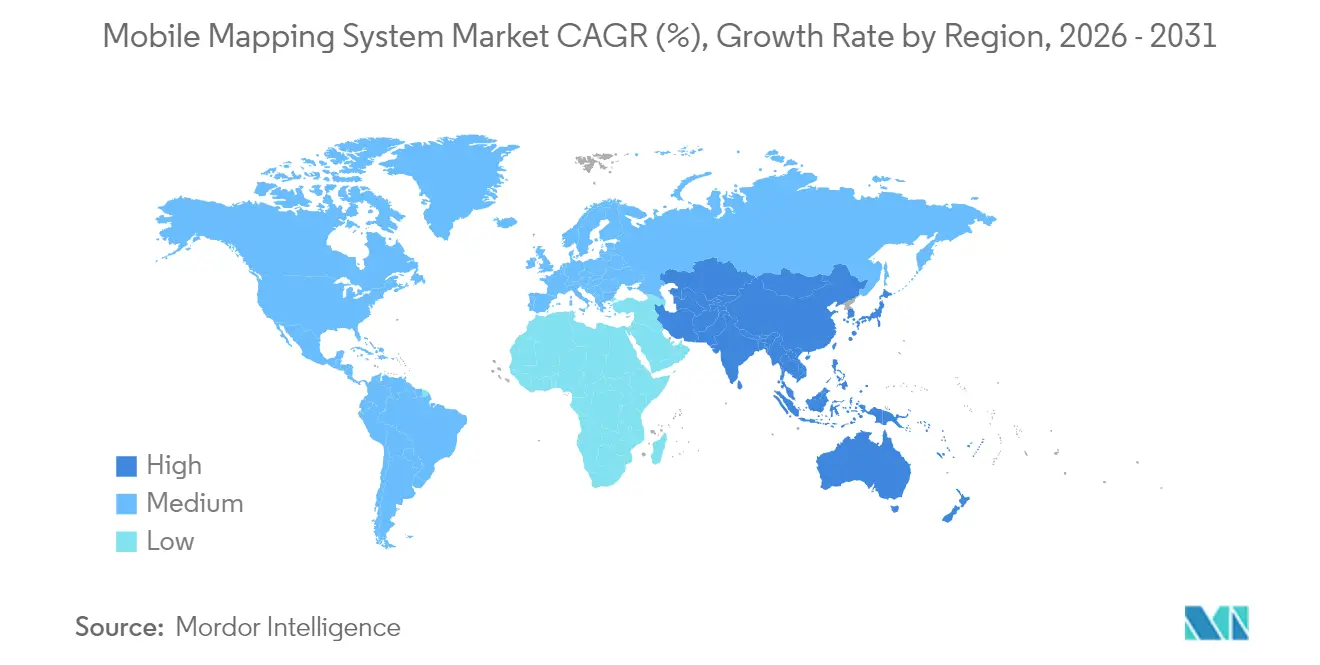

- By geography, North America led with 37.40% share in 2025; Asia-Pacific is forecast to grow at a 18.90% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Mapping System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration with all kinds of vehicles | +4.2% | Global; early adoption in North America, Europe | Medium term (2-4 years) |

| Government digital-twin mandates | +3.8% | North America, Europe, advanced APAC | Long term (≥ 4 years) |

| Declining solid-state LiDAR costs | +3.5% | Global | Short term (≤ 2 years) |

| AI-powered automatic feature extraction | +3.2% | North America, Europe, advanced APAC | Medium term (2-4 years) |

| Autonomous robots and drone adoption | +2.1% | Global | Medium term (2-4 years) |

| Defense ISR modernization budgets | +1.0% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration with All Kinds of Vehicles

The ability to mount sensors on railcars, trucks, autonomous shuttles, and even boats widened the mobile mapping system market scope. Deutsche Bahn certified Trimble’s MX9 platform for 100 km/h rail surveys in 2022, validating non-stop asset capture for European rail corridors.[1]Trimble Inc., “Trimble MX9 Mobile Mapping System Certified by Deutsche Bahn,” geospatial.trimble.com Transportation agencies that previously scheduled weekend closures for manual LiDAR scans now deploy vehicle-independent payloads during regular service, accelerating inspection cycles and reducing safety risks. Similar integrations on autonomous road sweepers enabled night-time curb-level mapping for urban digital-twin programs in Germany and Canada, demonstrating how cross-platform compatibility has become a revenue driver for equipment makers.

Government Digital-Twin Mandates

National programs such as the United Kingdom’s National Digital Twin initiative established compulsory data standards that require centimeter-grade 3D inputs. Municipalities responded by commissioning high-density mobile LiDAR of roadways, bridges, and public buildings to populate city-scale twins, spawning multi-year service contracts and stimulating procurement of modern sensor rigs. Uppsala’s biodiversity corridor planning, which combined LiDAR with GIS analytics, showed how regulatory push translated into immediate demand for dynamic, update-ready spatial datasets. The mobile mapping system market, therefore, benefited from predictable public-sector funding streams tied to long-range infrastructure resilience goals.

Declining Solid-State LiDAR Costs

Solid-state architectures eliminated mechanical components, trimming production expenses and raising durability. Modules based on Opsys Tech’s scanning micro-flash design were reported below USD 200 per unit in 2024 while sustaining 200-meter detection. Fleet operators in mining replaced rotating LiDARs with ruggedized solid-state units, reducing annual maintenance budgets by up to 40% and unlocking multi-sensor deployments on haul trucks. The price trajectory encouraged mid-tier survey firms in Southeast Asia to upgrade legacy rigs, enlarging the active equipment base and lifting annual shipments across the mobile mapping system market.

AI-Powered Automatic Feature Extraction

Trimble’s TBC 2024.10 release integrated trainable neural-network models that located lane markings and pavement defects without manual point cloud editing. Early adopters in state transportation departments reported post-processing time cuts of 60%, allowing field crews to redeploy within 24 hours instead of weeks. Parallel advances from Mach9 and Leica reduced manual edge drafting in utility corridor mapping, broadening access for organizations with limited geomatics staff. Faster turnaround shortened project payback periods, thereby expanding total addressable spend for the mobile mapping system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of system acquisition and deployment | -2.5% | Global; higher impact in emerging markets | Short term (≤ 2 years) |

| Skilled-operator shortage | -1.8% | Global; acute impact in fast-growing regions | Medium term (2-4 years) |

| Data-privacy and surveillance regulations | -1.2% | Europe, North America, APAC | Long term (≥ 4 years) |

| Construction sector cap-ex cyclicality | -0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of System Acquisition and Deployment

Top-tier mobile mapping packages still commanded USD 250,000-750,000, a threshold that remained prohibitive for small civil-engineering firms. A Malaysian road-design study in 2022 highlighted cap-ex as the main reason LiDAR bidding was deferred despite clear technical gains.[2]Fazilah Antah et al., “Factors Influencing the Use of Geospatial Technology with LiDAR,” mdpi.com Financing hurdles were sharper in Latin America and Africa, where local banks rarely offered asset-backed leasing for specialized geospatial hardware. Vendors responded with “mapping-as-a-service” subscriptions, yet up-front investment persisted as the most significant drag on addressable demand within the mobile mapping system market.

Skilled-Operator Shortage

Global surveys by geomatics associations in 2025 reported that firms struggled to hire technicians proficient in multisensor calibration, trajectory processing, and AI-based classification. Training a competent operator frequently required 18-24 months, causing scheduling bottlenecks even when equipment was available. Leica’s Cyclone 3DR AI classification features alleviated some pressure by automating routine segmentation tasks, yet labor scarcity continued to cap project throughput, particularly in booming Asia-Pacific metros where the mobile mapping system market was expanding fastest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Challenged by Services Growth

The hardware segment accounted for 50.60% of the mobile mapping system market share in 2025, underscoring its past reliance on capital-intensive sensor suites. Premium vehicle rigs paired 3.6 MHz laser scanners with 72 MP panoramic cameras, while handheld units such as Leica’s BLK2GO blended LiDAR with visual SLAM in one-kilogram packages. However, shrinking sensor footprints and solid-state innovations compressed unit costs, allowing more frequent refresh cycles and fostering modular upgrades.

The services segment achieved the fastest 20.10% CAGR through 2031 as organizations outsourced complex data processing. AI-enabled cloud platforms converted raw point clouds into CAD-ready deliverables, lowering internal overheads. This model shifted profit pools from hardware margins toward recurring analytics revenue, accelerating a structural transition in the mobile mapping system market. The mobile mapping system market size attached to services is projected to widen as pay-per-use offerings broaden access in emerging economies.

By Mounting Type: Vehicle Platforms Maintain Lead as Drones Accelerate

Vehicle-mounted platforms controlled 61.30% of the mobile mapping system market in 2025, favored for highway and rail corridors where uninterrupted acquisition at posted speeds maximized productivity. Dual-head scanners on SUVs captured both pavement distress and roadside assets during a single pass, consolidating budgets across transportation agencies.

Drone-based payloads, expanding at 21.10% CAGR, opened vertical mines, cliff faces, and disaster zones to rapid LiDAR coverage. Lighter solid-state sensors extended flight endurance while onboard AI filtered vegetation in real time, reducing downstream workload. Railway-specific trolleys and backpack units addressed niche needs yet collectively contributed to a diversified equipment mix underpinning future mobile mapping system market size momentum.

By Application: Imaging Services Lead While Emergency Response Accelerates

Imaging services contributed 27.60% of 2025 revenue as orthophotos and 360-degree panoramas complemented LiDAR-derived meshes for asset inventories. Utilities adopted automated pole detection from imagery to defer field inspections, demonstrating the ongoing relevance of high-resolution photos within an increasingly 3D-oriented mobile mapping system market.

Emergency-response planning, growing at 20.60% CAGR, leveraged near-real-time indoor GIS and drone LiDAR to support flood, wildfire, and earthquake scenarios. Public-safety agencies integrated live sensor feeds into command centers, highlighting the transition from episodic mapping to continuous situational awareness. The rising frequency of climate-related events is therefore anchoring a defensible growth corridor for the mobile mapping system market.

By End-User Verticals: Government Leads While Mining Shows Highest Growth

Government entities held 34.60% revenue in 2025, using mobile platforms for road asset management, cadastral updates, and smart-city analytics. Digital-twin legislation obligated municipalities to refresh 3D baselines annually, locking in multi-year procurement.

Mining registered a 19.20% CAGR as operators adopted vehicle and drone LiDAR for blast optimization and tailings-dam monitoring. Sub-centimeter terrain models replaced manual prism surveys, lowering staff exposure in hazardous pits. Oil-and-gas, defense, and construction round out an increasingly diversified clientele, each amplifying overall mobile mapping system market size through specialized workflows.

Geography Analysis

North America accounted for 37.40% of the mobile mapping system market in 2025. Federal infrastructure funding and strong defense ISR budgets nurtured steady sensor demand. Pilot programs demonstrated a USD 2 return for every USD 1 invested in statewide mobile LiDAR, reinforcing budget allocations. Ecosystem maturity, abundant skilled labor, and aggressive R and D by domestic vendors sustained the region’s leadership.

Asia-Pacific recorded the fastest 18.90% CAGR, driven by smart-city spending in China and India, Japan’s resilience planning, and South Korea’s autonomous-vehicle mapping corridors. Nearly half of global traffic on popular equipment-comparison portals originated from Asia-Pacific users in 2025, signaling high engagement that translated into orders for both drone and vehicle systems. Lower-cost sensors broadened entry-level uptake among provincial agencies, expanding the mobile mapping system market footprint.

Europe, the Middle East, Africa, and South America presented mixed demand profiles. European mandates around sustainability spurred environmental monitoring projects such as truck-traffic lidar in German cities. The Middle East prioritized pipeline and megacity initiatives, while Brazilian and Chilean mines underpinned South American sales. Africa remained nascent but showed momentum in South African infrastructure surveys. Across all regions, integration of mobile mapping with cloud, IoT, and AI underpinned cross-vertical use cases, lifting the global mobile mapping system market momentum.

Regulatory Landscape

Mobile mapping programs are increasingly influenced by geospatial data standards and national mapping rules that affect how LiDAR and imagery are collected, documented, and exchanged. Interoperability expectations commonly reference metadata frameworks such as ISO 19115 and ISO/TS 19139, while agencies publish acquisition and deliverable specifications, including Hong Kong Lands Department guidance on suggested specifications for mobile mapping system (MMS) data.

Jurisdiction-specific requirements also shape production workflows and data handling. China has codified technical practice through GB/T 41452-2022 for 3D model production using vehicle-borne mobile mapping, which defines clearer compliance checkpoints for corridor and city model contractors. In parallel, data sovereignty and governance requirements are tightening in several markets, including Oman, where Royal Decree 43/2026 (effective March 2026) established a National Geospatial Data and Information Law that governs how geospatial data is managed and shared. In Europe, the policy environment is shifting with the EU AI Act entering full enforcement in August 2026 for AI systems, which intersects with location analytics and automated feature extraction used in mobile mapping workflows.

Value Chain Analysis

The mobile mapping system value chain begins with core component suppliers, including LiDAR manufacturers, camera and optics vendors, GNSS-INS providers, compute and storage suppliers, and ruggedized mounting and power subsystems. System integrators and OEMs assemble these into vehicle-, rail-, drone-, and handheld-capable payloads, then package calibration, trajectory processing, and workflow software. Downstream, service providers and engineering firms perform acquisition and deliverables, while cloud and software platforms convert raw point clouds and imagery into GIS, CAD, and asset-management outputs used by transportation agencies, utilities, mining operators, and municipal digital-twin teams.

A key shift in 2026 is tighter coupling between hardware and automated processing to reduce time-to-deliverable and operator burden. For example, Emesent launched the GX1 (February 2026) as an all-in-one mobile mapping system combining SLAM, RTK, and 360-degree imagery, illustrating the move toward integrated capture packages rather than multi-vendor field stacks. In digital mapping, these platform and data-provider interactions also influence mobile mapping economics, as map and data providers, software platform layers, and autonomous-perception players increasingly converge, pushing vendors to offer end-to-end pipelines that connect acquisition to update and distribution workflows.

Competitive Landscape

The mobile mapping system market featured a moderately fragmented field of incumbents and AI-centric newcomers. Hexagon’s Leica division, Trimble, and RIEGL retained strong brand equity by offering integrated hardware-software stacks. Trimble launched the MX90 in February 2025, combining advanced GNSS-INS with highway-speed image capture to strengthen its corridor-mapping franchise. Leica responded in May 2025 with the Pegasus TRK300, targeting mid-range buyers seeking modular payloads.[4]Leica Geosystems, “New Leica Pegasus TRK300 Opens Up Advanced Mobile Mapping,” leica-geosystems.com

Software-led challengers focused on automated feature extraction and cloud collaboration. Mach9’s Digital Surveyor promised 30× faster map production, appealing to service bureaus needing rapid throughput. Subscription-based analytics from SISL and others shifted revenue away from one-time equipment sales toward recurring processing fees, intensifying competitive pressure on hardware margins.

Strategic acquisitions accelerated portfolio expansion. Faro’s earlier purchase of GeoSLAM added indoor mobile LiDAR to its offering, while WSP equipped its survey fleet with RIEGL VMX 2HA systems to augment digital-twin consulting services. Going forward, players that unite rugged sensors, AI workflows, and sector-specific expertise are positioned to capture disproportionate gains within the mobile mapping system market.

Mobile Mapping System Industry Leaders

Trimble Inc.

Leica Geosystems AG (Hexagon AB)

Topcon Corporation

GeoSLAM Ltd.

Teledyne Optech Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are expanding when mobile mapping becomes a repeatable operational input to digital twins, rather than a one-off survey deliverable. This is particularly visible in city-scale street inventories, road-condition monitoring, and utility corridor inspection. Municipal initiatives that capture street-level data for digital twins create pull-through for vehicle-mounted systems and the associated analytics, as demonstrated in April 2026 when Detroit deployed a Trimble vehicle-mounted mobile mapping system for its Detroit Street View initiative. That deployment supports recurring mapping cycles, data refresh contracts, and tighter integration into asset lifecycle management platforms.

Processing automation is also a clear whitespace as acquisition volumes rise faster than manual classification capacity. Vendors are productizing AI to reduce editing and quality-assurance effort, including Leica Geosystems Pegasus OFFICE 2026.1 (May 2026) adding AI-driven image beautification to improve visual clarity and readability for infrastructure datasets, which shifts differentiation toward post-processing software rather than sensors alone. In parallel, new AI approaches that generate 3D digital twins from general-purpose camera footage, such as NECs July 2026 announcement of a system producing high-resolution 3D outputs in roughly 60 seconds, broaden the competitive set for applications where ultra-high-precision LiDAR is not mandatory. This supports tiered MMS offerings, from survey-grade stacks to faster imagery-led capture workflows, and encourages service providers to package update services around change detection and asset condition insights.

Recent Industry Developments

- May 2026: Leica Geosystems released Pegasus OFFICE 2026.1, introducing AI-driven image beautification to enhance visual clarity and improve the readability of mobile mapping outputs for workflows such as rail and utility corridor inspection. The update strengthens differentiation through post-processing capability, where faster QA and clearer imagery reduce downstream interpretation effort and shorten data-to-decision cycles.

- April 2026: The city of Detroit deployed a vehicle-mounted Trimble mobile mapping system for its Detroit Street View initiative to capture high-resolution street-level data for a city-wide digital twin. The deployment indicates continued municipal demand for repeatable capture and refresh programs, supporting ongoing services and analytics consumption beyond single-project surveys.

- February 2024: Exyn Technologies unveiled Nexys, a modular autonomous survey platform designed to increase data-capture speed and accuracy in confined or difficult environments. The launch highlights the growing role of autonomy and modularity in expanding where mobile mapping can be performed safely and consistently, especially in industrial and underground use cases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the mobile mapping system market covers revenue earned from integrated mapping solutions used on moving platforms to capture georeferenced imagery and 3D data, which is then processed into maps, point clouds, and GIS-ready layers.

Scope exclusions: We exclude fixed terrestrial scanning setups and solutions that are only for indoor SLAM without an outdoor georeferencing workflow.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Mounting Type

- Vehicle Mounted

- Railway Mounted

- Drone Mounted

- Others

- By Application

- Imaging Services

- Aerial Mobile Mapping

- Emergency Response Planning

- Internet Applications

- Facility Management

- Satellite

- By End-user Verticals

- Government

- Oil and Gas

- Mining

- Military

- Other End-user Verticals

- By Region

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by defining the market boundaries and demand signals from public sources, then checking them against what suppliers and users describe as real purchasing behavior. We referred to sources such as USGS materials and other national mapping agency publications, transportation and infrastructure statistics from agencies such as the US DOT and Eurostat, and standards references from bodies such as ISO that touch geospatial data and positioning.

To keep inputs grounded, we also reviewed customs and trade statistics where relevant, peer-reviewed remote sensing and photogrammetry papers, and procurement notices that show how mapping services and systems get specified. On the company side, annual reports, earnings notes, and product documentation helped us align component coverage and typical pricing structures. In a few places, paid subscriptions were used to speed up company financial checks and patent lookups for mapping sensors and processing workflows. These sources are illustrative, and we relied on other public references for cross-checks, clarification, and filling small gaps.

Primary Interviews and Surveys

Primary work was used to pressure-test assumptions on platform mix (vehicle, rail, UAV, and backpack), typical contract structures, and how buyers bundle hardware, software licenses, and services. We spoke with system providers, integrators, and end users across the main regions, so adoption drivers tied to infrastructure programs and surveying cycles could be confirmed in practical terms.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 48% |

| Mid tier: 53% | Functional/Unit leaders: 32% | EMEA: 33% |

| Smaller Players: 16% | Managers: 55% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach, using infrastructure and surveying activity along with geospatial data collection intensity to reconstruct the demand pool for mobile mapping deployments by region. We then checked totals with selective bottom-up approximations such as sampled system ASPs times expected unit shipments, and service revenue ranges observed through channel checks, which helped correct pockets that looked overstated or understated.

Key inputs in the model include the mix of mapping platforms (vehicle versus UAV and backpack), sensor pack intensity (LiDAR and camera-heavy systems typically sit in different price bands), project cadence in transportation and utilities, replacement and upgrade cycles for GNSS and imaging payloads, and the split between one-time projects versus recurring software and processing services. For forecasting, we used scenario analysis anchored on capital spending cycles and adoption timing, then refined year-to-year paths using expert consensus from interviews on how quickly platform penetration and average project sizes are changing. When we lacked a bottom-up signal for a country or niche use case, we filled it using proxy ratios from similar markets and then re-validated the implied spend per project with respondents.

Data Validation & Update Cycle

Validation was done by triangulating model outputs against independent signals such as the direction of public infrastructure spending, trade movement where it aligns with sensor payload needs, and the pace of mapping tenders and project announcements. Outliers were reviewed step by step, and assumptions behind platform share, pricing, and service attachment rates were revisited before internal sign-off.

The report is refreshed annually, with interim updates triggered when there is a material shift such as a large regulatory push for digital infrastructure, a major technology cost change in LiDAR and imaging payloads, or a sudden change in public works budgets. Before delivery, we complete a final analyst pass so the numbers reflect the latest available information and any late corrections from follow-up calls.

Mordor Intelligence's Mobile Mapping System Market Market Sizing Compared With Other Published Estimates

Published market numbers for mobile mapping systems can differ even when they appear to cover the same scope, because assumptions around platforms, revenue counting, and the year used for pricing can move the total quickly. The comparison below is intended to show how these choices, plus refresh timing, typically explain most of the spread.

The table shows a tighter 2025 value versus one higher external estimate, and the gap mostly comes from what gets counted as mobile mapping and when it is counted. In Mordor Intelligence's model, revenue is counted only when it ties to moving-platform mapping systems and their related software and services, while excluding fixed terrestrial scanning and indoor-only SLAM offerings that can inflate totals when they get bundled into the same label.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 43.4 B (2025) | |

| Global Consultancy A | USD 44.14 B (2025) | Uses a broader segmentation structure that can pull adjacent GNSS and sensor-led mapping spend into the same bucket, and the component-to-vertical mapping is not always clear on whether service processing revenue is double-counted across layers. |

| Trade Publisher B | USD 54.08 B (2025) | Often reports a wider mobile mapping definition that can include indoor mapping and location-based service revenues, and it also mixes base-year and forecast-year pricing assumptions, which can lift the stated 2025 number. |

Overall, the spread is mainly explained by scope boundaries and how revenues are grouped across hardware, software, and service lines. By tying the size to observable deployment activity, platform mix, and realistic price bands, the final number stays traceable to inputs that can be re-checked and updated each year.

Key Questions Answered in the Report

What is the current value of the mobile mapping system market?

The market was valued at USD 51.19 billion in 2026 and is forecast to reach USD 116.86 billion by 2031, growing at an 17.95% CAGR.

Which region leads the mobile mapping system market?

North America led with 37.40% revenue share in 2025, supported by infrastructure funding and defense ISR programs.

Why are drones gaining traction in mobile mapping?

Drones posted a 21.10% CAGR because lightweight solid-state LiDAR and improved endurance allow safe, rapid data capture in areas inaccessible to vehicles.

How are declining LiDAR costs affecting adoption?

Solid-state unit prices fell below USD 200, enabling multi-sensor deployments that lower project costs and expand the addressable user base.

Which application segment is expanding fastest?

Emergency-response planning is growing at a 20.60% CAGR as agencies integrate real-time mobile mapping into disaster preparedness workflows.

What challenges limit broader market uptake?

High up-front equipment costs and a shortage of trained operators continue to restrain adoption, particularly in emerging economies.

Page last updated on: