Autonomous Luxury Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

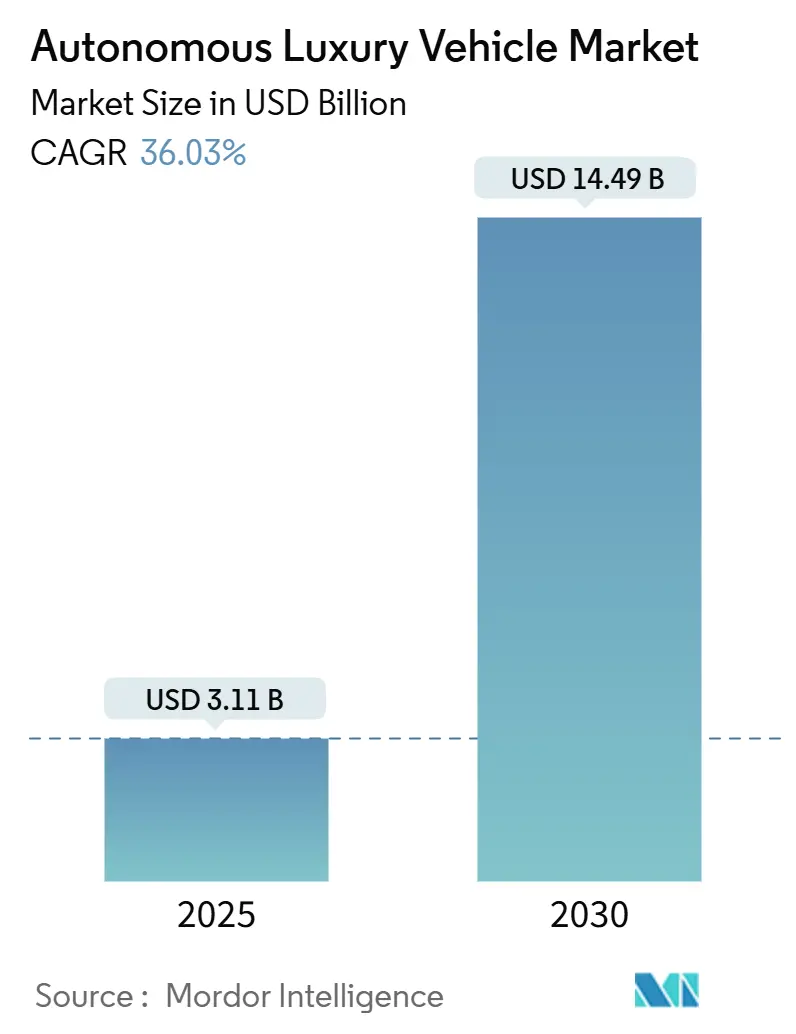

| Market Size (2025) | USD 3.11 Billion |

| Market Size (2030) | USD 14.49 Billion |

| Growth Rate (2025 - 2030) | 36.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Luxury Vehicle Market Analysis by Mordor Intelligence

The autonomous luxury vehicle market size stands at USD 3.11 billion in 2025 and is forecast to reach USD 14.49 billion by 2030, translating into a compelling 36.03% CAGR over the period. Surging demand for premium driver-assistance suites, falling 4D-radar and solid-state LiDAR costs, and widening Level 3 regulatory approvals underpin this acceleration. OEMs are bundling subscription-based software with high-margin hardware, creating fresh recurring revenue streams that offset the steep R&D outlays required for advanced automation. The fast pace of component price erosion—sensor bills of material have dropped, which now allows flagship sedans and SUVs to ship with robust perception stacks once reserved for prototype fleets. Intensifying competition from software-centric EV entrants is compelling heritage luxury marques to strike ecosystem partnerships that shorten development cycles and safeguard brand cachet.

Key Report Takeaways

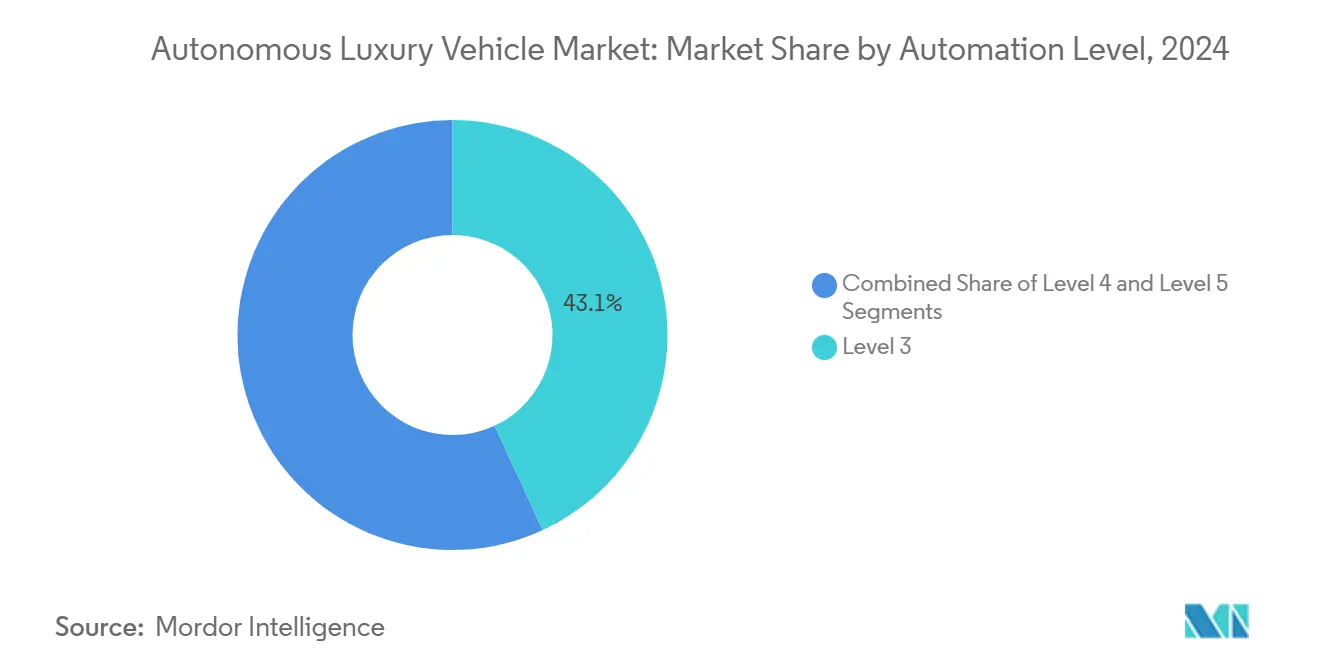

- By automation level, Level 3 systems led with 43.14% of the autonomous luxury vehicle market share in 2024, while Level 5 is projected to expand at a 40.11% CAGR through 2030.

- By component, hardware retained 57.25% of the autonomous luxury vehicle market share in 2024; software is set to rise at a 38.14% CAGR to 2030.

- By sensor, cameras accounted for 36.22% of the autonomous luxury vehicle market size in 2024, and LiDAR is advancing at a 37.66% CAGR.

- By vehicle type, SUVs captured a 39.11% of the autonomous luxury vehicle market share in 2024 and will post the quickest 36.71% CAGR through 2030.

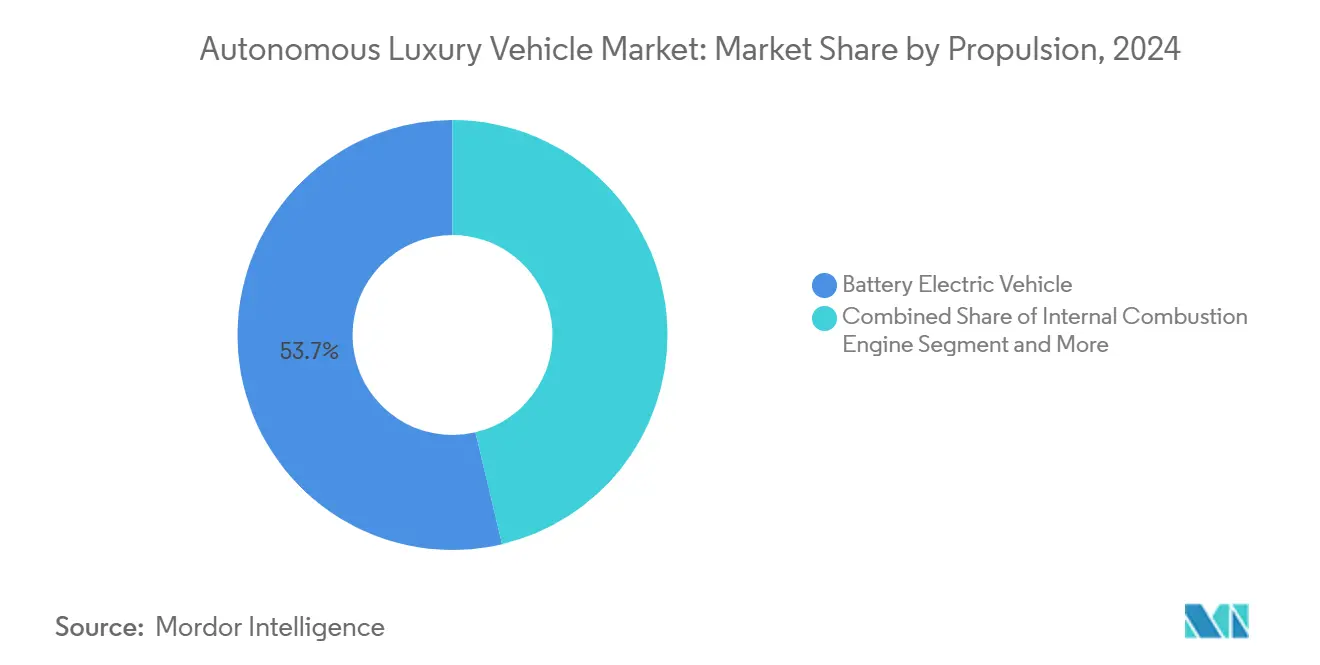

- By propulsion, battery electric vehicles represented 53.66% of the autonomous luxury vehicle market share in 2024 and will climb at a 36.42% CAGR to 2030.

- By end-user, personal mobility contributed 65.06% of the autonomous luxury vehicle market share in 2024, whereas car-sharing solutions are projected to grow at a 38.63% CAGR.

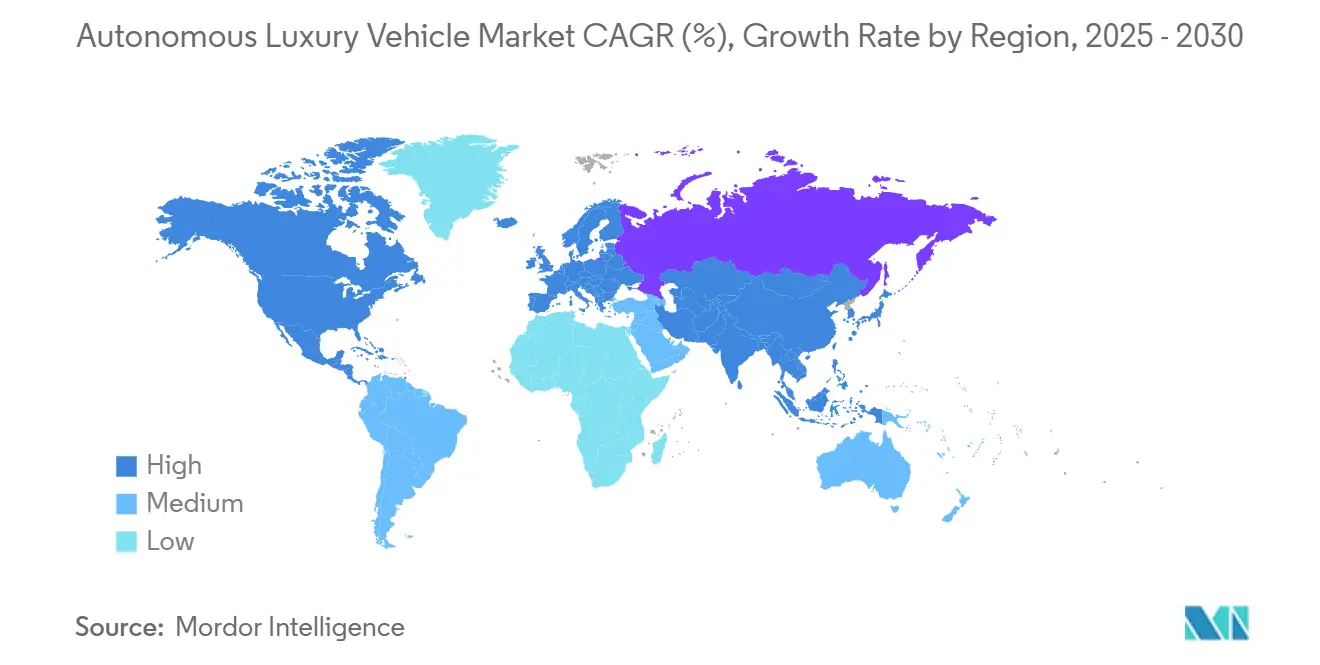

- North America dominated with a 32.46% of the autonomous luxury vehicle market share in 2024, while Asia-Pacific is on track for a 37.12% CAGR during the forecast horizon.

Global Autonomous Luxury Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Battery Cost Decline | +8.2% | China, EU, global premium hubs | Medium term (2-4 years) |

| Expanding Level 3 Approvals | +7.8% | North America, EU, major APAC markets | Short term (≤ 2 years) |

| High-Net-Worth AD Demand | +6.5% | Global metropolitan centers | Long term (≥ 4 years) |

| Subscription Revenues Boost ROI | +5.9% | North America, EU, APAC roll-outs | Medium term (2-4 years) |

| 4D Radar and Solid-State LiDAR Cuts | +4.3% | Global manufacturing hubs | Short term (≤ 2 years) |

| High-Speed OTA Data Monetization | +3.4% | Markets with advanced 5G | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Battery-Cost Decline Plus Premium-EV Synergy

Battery pack prices continue to fall, letting luxury EVs integrate power-hungry sensor suites without breaching margin thresholds. Lower pack costs free capital for domain controllers, high-fidelity maps, and redundant power storage essential for Level 3+ safety. Subscription models, such as a monthly full self-driving plan, illustrate how recurring revenue can amortize both battery and autonomy investment. This dual-track strategy delivers economies of scope that internal-combustion platforms cannot match, encouraging OEMs to prioritize shared skateboard chassis that host both propulsion and perception hardware. As charging infrastructure matures, affluent early adopters gain the confidence to treat autonomy as a premium functionality layered onto a zero-emission flagship.

Expanding Level-3 Regulatory Approvals in United States, EU, China

Regulators are moving faster than expected: Nevada and California certified conditional-automation drive pilots in premium sedans, while the U.K.’s Automated Vehicles Act 2024 lays out liability provisions that shorten time-to-market for luxury brands [1]“Automated Vehicles Act 2024: Full Text,” United Kingdom Parliament, parliament.uk. China’s sandbox zones in Beijing and Shanghai let domestic OEMs iterate sensor calibration in mixed traffic, accelerating validation cycles. BMW’s 2024 flagship integrates both Level 2 and Level 3 functions, proving that harmonized rules can coexist inside a single architecture. Each regulatory nod builds public trust and raises performance baselines; rivals must now develop redundant perception stacks to meet similar safety cases, effectively ratcheting up competitive intensity across the autonomous luxury vehicle market. In turn, insurers gain clearer frameworks, smoothing premium calculations for early buyers.

High-Net-Worth Demand for Flagship AD Features

Wealthy consumers view autonomy less as convenience and more as a status-symbol technology that complements bespoke interiors and concierge services. Surveys show Chinese high-net-worth individuals lead global purchase intent and often equate brand leadership in autonomy with social prestige. Tesla remains the most considered marque among this cohort, though German luxury stalwarts maintain loyalty via heritage quality cues combined with transparent safety credentials. Willingness to pay accelerates cost recovery on complex sensor nodes, giving OEMs room to iterate Level 3 systems while preparing for Level 4 chauffeur modes. Elevated margins also let brands experiment with optional interior layouts, lounging rear seats, panoramic infotainment, and advanced wellness modules, creating tangible differentiation within the autonomous luxury vehicle market.

Subscription Revenues Boosting OEM ROI

Over-the-air architecture turns vehicles into upgradable platforms rather than one-off purchases. General Motors’ unified software stack and Mercedes-Benz’s USD 2,500 annual Drive Pilot subscription demonstrate that affluent owners will pay recurring fees for incremental autonomy zones and feature unlocks. Continuous revenue aligns corporate incentives with constant algorithm refinement, funneling real-world data back into neural-network optimization cycles. This loop shortens release cadences and buffers the heavy fixed costs linked to ASIL-D compute hardware, thus ensuring positive lifetime value on each flagship unit. It also stokes secondary markets for data-driven services—parking reservation, predictive maintenance, personalized infotainment—that further embed owners inside brand ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Liability and Insurance Uncertainty | -4.7% | Global, pronounced in United States litigation | Long term (≥ 4 years) |

| Cyber-security And IP Risks | -3.2% | Regions with weak IP enforcement | Medium term (2-4 years) |

| Luxury-Only Level 3 Roads | -2.8% | Dense urban centers in developed markets | Short term (≤ 2 years) |

| Sensor-Rich Repair Cost Inflation | -2.1% | High-labor-cost markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Liability and Insurance Cost Uncertainty

Premium repair bills for bumper-mounted radar and hidden LiDAR arrays complicate actuarial models. Independent studies show advanced-driver-assist collisions raise average claim amounts due to sensor recalibration, double that of conventional repairs. While long-run autonomous safety gains promise to halve premiums, near-term uncertainty prompts carriers to tack risk surcharges onto luxury policies. Some reinsurers draft special riders that shift product liability onto OEMs once Drive Pilot or similar systems engage, further muddying accountability. Until legal precedents crystallize around fault attribution, the cautious underwriting stance could temper uptake across the autonomous luxury vehicle market.

Cyber-Security and IP-Theft Risks

Sophisticated threat actors target code-signing keys and perception algorithms embedded in high-value luxury fleets. Attack surfaces now span V2X endpoints, over-the-air pipelines, and third-party app stores. Successful exploits can trigger cascade failures, undermining brand reputation and prompting costly recalls. Additionally, corporate spies seek to clone proprietary object-detection stacks, eroding the competitive moat that justifies premium pricing. To mitigate, OEMs invest in hardware-root-of-trust modules and federated-learning defences, but the ongoing expenditure drags on margins and lengthens development timelines for new features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Automation Level: Level 3 Maintains Leadership Yet Level 5 Accelerates

Level 3 conditional automation held 43.14% of the autonomous luxury vehicle market share in 2024, reflecting a sweet spot where legal clarity and component maturity intersect. The continued rollouts in interstate corridors are set to cement its dominance through mid-decade. OEMs employ high-definition maps coupled with redundant ECUs to meet fail-operational requirements, driving robust demand for ASIL-D components. A second tailwind arrives from fleet managers keen to cut driver fatigue in congested commutes, boosting subscription uptake.

Conversely, Level 5 remains pre-commercial, but its 40.11% CAGR underscores investor conviction that full autonomy will define flagship launches toward 2030. Early pilots from all-electric luxury startups favor ride-hailing geofences where machine-learning pipelines can ingest vast urban datasets. The tipping point will hinge on regulatory harmonization across continents; once achieved, the autonomous luxury vehicle market will likely witness a pivot from conditional autonomy toward chauffeur-grade experiences in ultra-high-net-worth circles.

By Component: Hardware Still in Front as Software Gains Traction

Hardware represented 57.25% of the autonomous luxury vehicle market share in 2024, underpinned by multi-modal sensor arrays, high-bandwidth power distribution, and steer-by-wire actuation. Luxury interiors' razor-thin tolerances require custom bracketry and noise-deadening, raising the bill of materials beyond mainstream levels. However, innovations in 5-nanometer SoCs allow OEMs to consolidate domain controllers, freeing cabin space and trimming heat-sink mass.

Software, growing at 38.14% CAGR, is the linchpin for long-term value capture. Continuous integration pipelines let engineers push weekly perception improvements, rendering vehicles smarter as they age. Brands offering tiered autonomy subscriptions can segment owners by usage needs, turning adaptive cruise baselines into upsell funnels for traffic-jam pilot, lane-change assist, and valet-parking modules. As usage data accrues, personalized AI profiles may become a defining marque signature within the autonomous luxury vehicle market.

By Sensor: Cameras Remain Workhorse While LiDAR Races Ahead

Cameras captured 36.22% of the autonomous luxury vehicle market share in 2024, leveraging commodity supply chains and ever-lower pixel costs. Neural networks trained on curated edge cases extract lane geometry, traffic-signal states, and pedestrian intent with growing fidelity. Thermal imaging variants help in low-light scenarios, giving luxury brands an extra safety differentiator.

LiDAR, with a blazing 37.66% CAGR, is quickly transitioning from an ancillary aid to a core sensor in premium stacks. Solid-state designs embedded behind windshield modules now meet aesthetic and aerodynamic constraints prized by luxury designers. Complementary 4D radar fills adverse-weather coverage gaps, ensuring situational redundancy that satisfies regulators. Together, these advances elevate consumer trust, a decisive factor for adoption in the autonomous luxury vehicle market.

By Vehicle Type: SUVs Dominate Premium Automation Rollouts

SUVs commanded 39.11% of the autonomous luxury vehicle market share in 2024, thanks to ample chassis volume for roof-line LiDAR pods and rear-quarter radar placement. Their higher ride height yields better sensor line-of-sight, enhancing prediction algorithms, supporting its fastest growth of 36.71% CAGR. Luxury buyers gravitate toward SUVs for lifestyle versatility, aligning with automakers’ decision to debut top-tier autonomy in this body style.

Crossover-EV derivatives translate skateboard architectures into family-friendly cabins where passengers can recline or engage with immersive infotainment during hands-off cruising. Sedans, while still prestige flagships in many brands, trail in growth as consumer tastes evolve. Yet the segment will remain critical to showcase aerodynamic efficiency and top-speed autonomous calibration, ensuring diversified portfolios inside the autonomous luxury vehicle market.

By Propulsion: Battery Electric Vehicles Anchor Autonomy Economics

Battery electric platforms held 53.66% of the autonomous luxury vehicle market share in 2024, and are set to expand at a CAGR of 36.42% by 2030, as charging corridors densify. EV drivetrains offer instant torque for merge maneuvers and accommodate 800-volt architectures that feed compute-intensive sensor suites without straining alternators. Rising carbon-regulation stringency will likely amplify this dominance.

Hybrid entries serve range-anxious regions but face wiring-harness complexity when integrating ADAS ECUs across dual powertrains. Fuel-cell variants attract attention for inter-city limousine services where hydrogen refueling fits fleet logistics; yet, they remain niche but technologically synergistic with autonomy through high-output electric motors.

By End-User: Personal Ownership Prevails, Car Sharing Surges

Affluent buyers continue to favor outright ownership, driving 65.06% of the autonomous luxury vehicle market share in 2024. Personal garages double as private charging and over-the-air update nodes, ensuring seamless nightly calibration downloads. These owners value tailored seating layouts, fragrance diffusers, and curated material palettes that mass-market robotaxis cannot match.

Corporate car-sharing fleets, however, exhibit a 38.63% CAGR, signaling a pivot toward usage-based luxury experiences. Hotel groups and aviation lounges envision autonomous luxury shuttles as brand-extension touchpoints, while tech campuses eye subscription fleets to elevate executive mobility. Such diversification expands the addressable base for the autonomous luxury vehicle market beyond individual high-net-worth circles.

Geography Analysis

North America led with a 32.46% of the autonomous luxury vehicle market share in 2024, its regulatory agility evident in the first U.S. approvals of Level 3 Drive Pilot for interstate traffic. Wealth concentration in coastal metros supports premium pricing, and contiguous highway networks simplify map maintenance. High-performance computing clusters in Silicon Valley fuel rapid perception-stack iterations, further entrenching regional leadership.

Europe follows closely, anchored by Germany’s heritage marques that pair mechanical excellence with dual-use EV-autonomy skateboards. The continent’s harmonized UNECE regulations create efficiencies in homologation, while vision-zero safety targets push cities to facilitate pilot zones. Nordic countries’ 100% renewable grids add sustainability cachet to autonomous luxury EV rollouts, attracting environmentally focused elites.

Asia-Pacific, projected at a 37.12% CAGR, benefits from China’s unparalleled policy impetus and smart-city investments [2]“China Smart-City Infrastructure Funding 2025,” Ministry of Industry and Information Technology, miit.gov.cn. Domestic champions like NIO and Li Auto test Level 4 valet functions inside geo-fenced urban loops, leveraging dense V2X roadside units. Japan’s aging demographic accelerates interest in hands-free luxury cruising, whereas South Korea’s 5G ubiquity shortens edge-compute latency, enabling early deployment of cloud-based redundancy services. Collectively, these factors position the region to narrow the gap and potentially challenge Western dominance in the autonomous luxury vehicle market.

Competitive Landscape

Incumbent luxury OEMs and emergent software-first EV players are locked in a race to define the gold standard for premium autonomy. Mercedes-Benz and BMW leverage mature supply chains and dealer networks, but Tesla’s agile over-the-air culture pressures update velocity. Strategic alliances multiply: Uber’s deal with Lucid taps a ready fleet for autonomous ride-hailing pilots. Waymo’s Hyundai tie-up packages proven perception stacks with cost-efficient E-GMP platforms [3] “Uber–Lucid Autonomous Partnership,” Uber Technologies, uber.com.

Component specialization creates new kingmakers. Radar innovators such as Arbe supply turnkey 4D chips that allow brands to skip extended in-house R&D, compressing time-to-feature. High-definition mapping vendors sign exclusivity contracts, creating quasi-walled gardens that influence customer lock-in strategies. The resulting ecosystem dynamics designate integration mastery—rather than mere hardware prowess—as the decisive differentiator inside the autonomous luxury vehicle market.

Regulation-shaped barriers favor players with deep compliance benches. Certification under ISO 26262 and UNECE R157 demands years of audit trails, advantaging established automakers. Yet nimble startups circumvent by white-labeling systems to incumbent brands, trading IP royalties for assured volume. Over the forecast horizon, analysts anticipate moderate consolidation as sensor and compute suppliers merge to achieve the scale needed for ASIL-D redundancy at luxury-grade quality.

Autonomous Luxury Vehicle Industry Leaders

Mercedes-Benz Group AG

Tesla Inc.

BMW Group

Audi AG

General Motors Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lucid Group, Uber, and Nuro announced plans to deploy 20,000 self-driving Lucid Gravity SUVs on Uber’s platform across global markets.

- October 2024: Hyundai and Waymo launched a multi-year program integrating Waymo Driver into the all-electric IONIQ 5 for the Waymo One fleet.

- August 2024: Cadillac revealed the Opulent Velocity concept, targeting Level 4 autonomy with an AR head-up display.

- June 2024: BMW secured approvals for both Level 2 Highway Assistant and Level 3 Personal Pilot L3 in the new 7 Series.

Global Autonomous Luxury Vehicle Market Report Scope

| Level 5 |

| Level 4 |

| Level 3 |

| Hardware |

| Software |

| Camera Units |

| Ultrasonic Sensor |

| LiDAR Sensor |

| Radar Sensor |

| Biometric Sensors |

| Hatchback |

| SUV |

| Sedan |

| Battery Electric Vehicle |

| Internal Combustion Engine |

| Hybrid Electric Vehicle |

| Plug-In Hybrid Electric Vehicle |

| Fuel Cell Electric Vehicle |

| Personal Mobility |

| Car Sharing |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Automation Level | Level 5 | |

| Level 4 | ||

| Level 3 | ||

| By Component | Hardware | |

| Software | ||

| By Sensor | Camera Units | |

| Ultrasonic Sensor | ||

| LiDAR Sensor | ||

| Radar Sensor | ||

| Biometric Sensors | ||

| By Vehicle Type | Hatchback | |

| SUV | ||

| Sedan | ||

| By Propulsion | Battery Electric Vehicle | |

| Internal Combustion Engine | ||

| Hybrid Electric Vehicle | ||

| Plug-In Hybrid Electric Vehicle | ||

| Fuel Cell Electric Vehicle | ||

| By End-User | Personal Mobility | |

| Car Sharing | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the autonomous luxury vehicle market in 2025?

It is valued at USD 3.11 billion and is projected to grow to USD 14.49 billion by 2030 at a 36.03% CAGR.

Which automation level currently dominates premium autonomous deployments?

Level 3 conditional automation leads with 43.14% 2024 revenue share, reflecting regulatory and technological readiness.

Why are battery electric platforms favored for luxury autonomy?

They supply ample electrical power for sensor suites and allow seamless over-the-air updates, driving a segment share of 53.66% in 2024.

Which region is expected to grow the fastest?

Asia-Pacific is forecast to record a 37.12% CAGR through 2030, propelled by China’s policy support and smart-infrastructure spending.

Page last updated on: