Luxury EV Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 254.08 Billion |

| Market Size (2031) | USD 530.16 Billion |

| Growth Rate (2026 - 2031) | 15.86% CAGR |

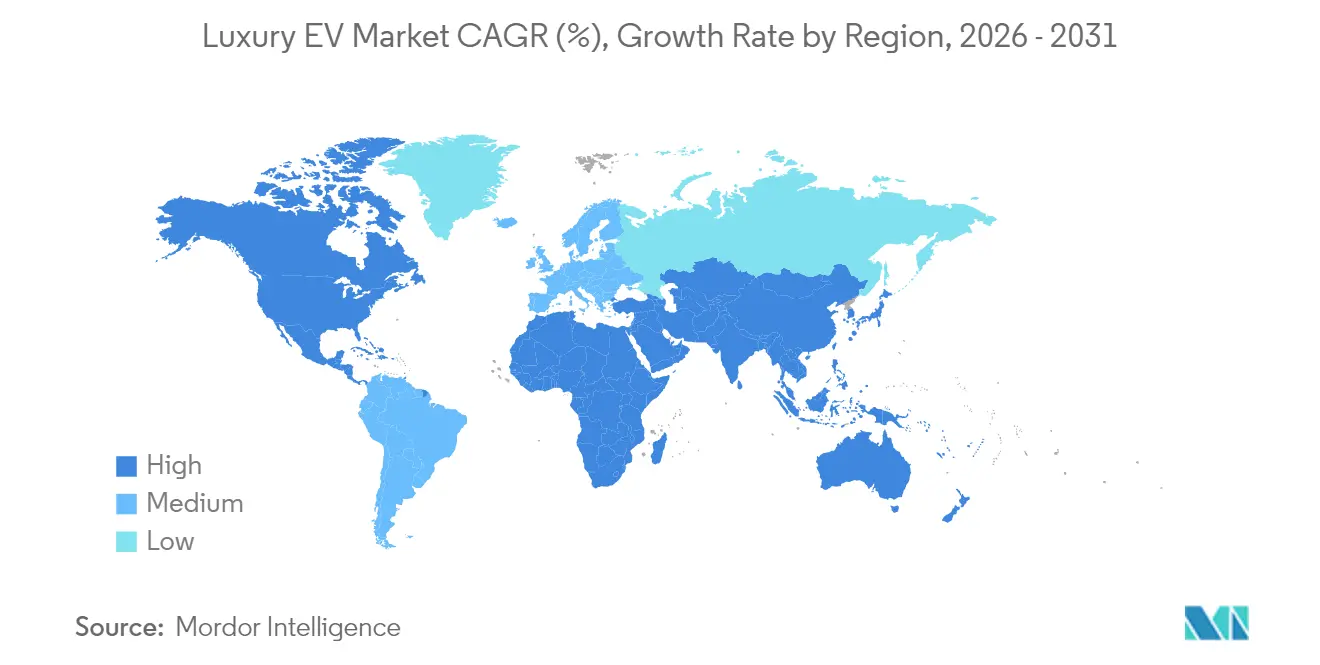

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

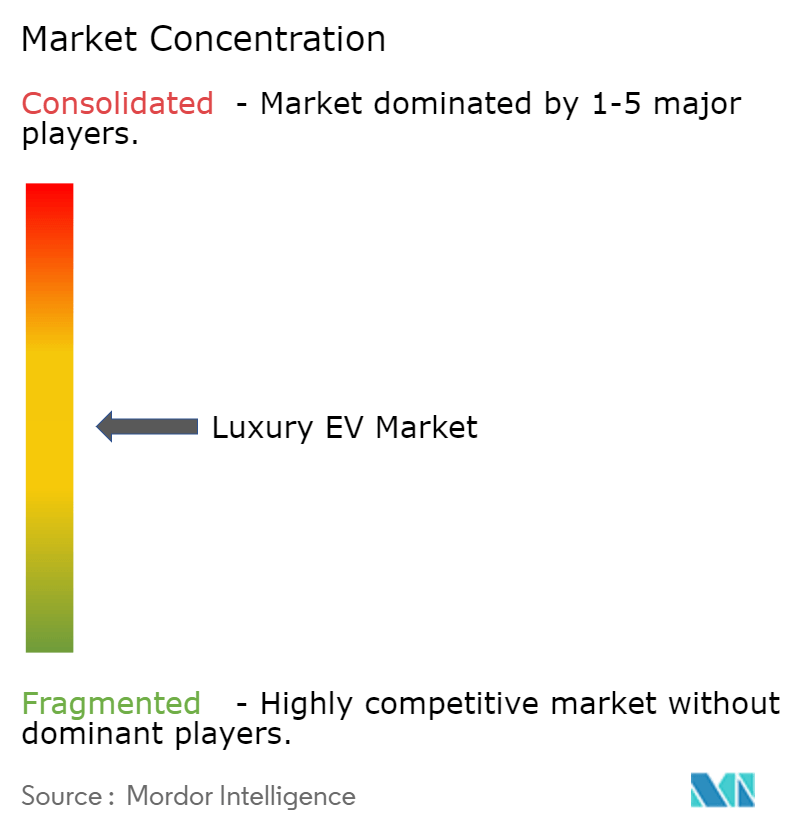

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxury EV Market Analysis by Mordor Intelligence

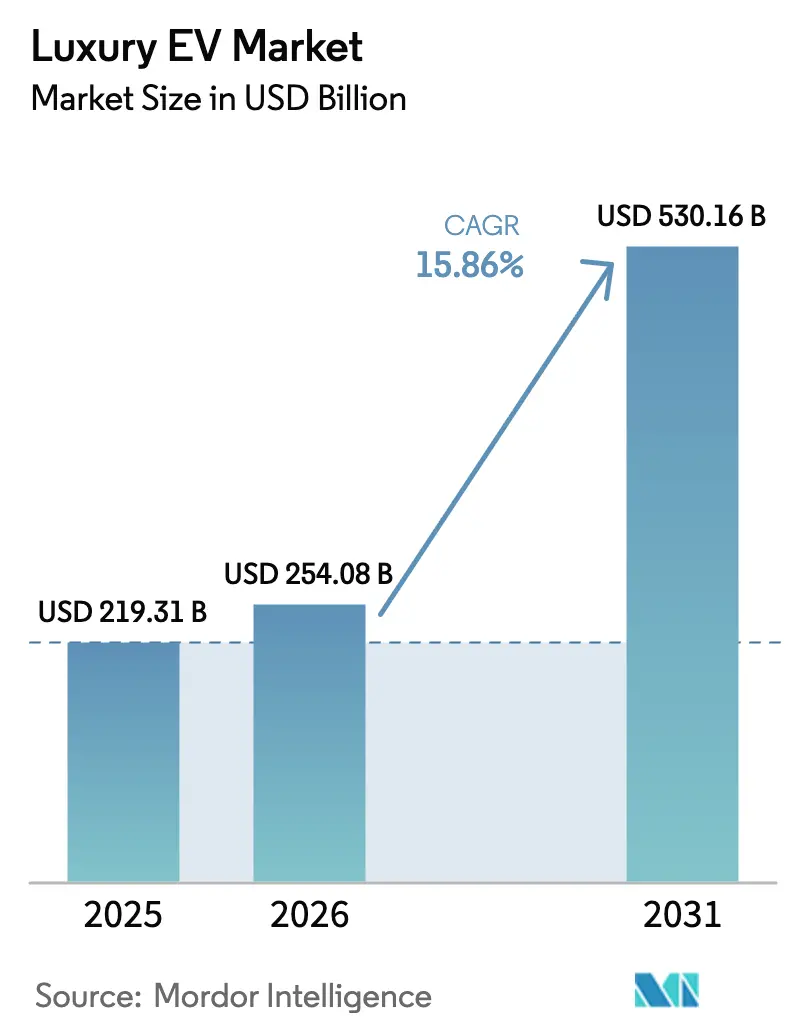

The Luxury EV market size is expected to grow from USD 219.31 billion in 2025 to USD 254.08 billion in 2026 and is forecast to reach USD 530.16 billion by 2031 at 15.86% CAGR over 2026-2031. Automakers are shrinking model-development cycles from seven years to four as brand-level electrification pledges accelerate launches and channel supplier innovation toward the premium tier. Alongside hardware advances, connected-car data monetisation now delivers recurring revenues that rival traditional after-sales profits, cementing software as a core differentiator within the Luxury EV market.

Key Report Takeaways

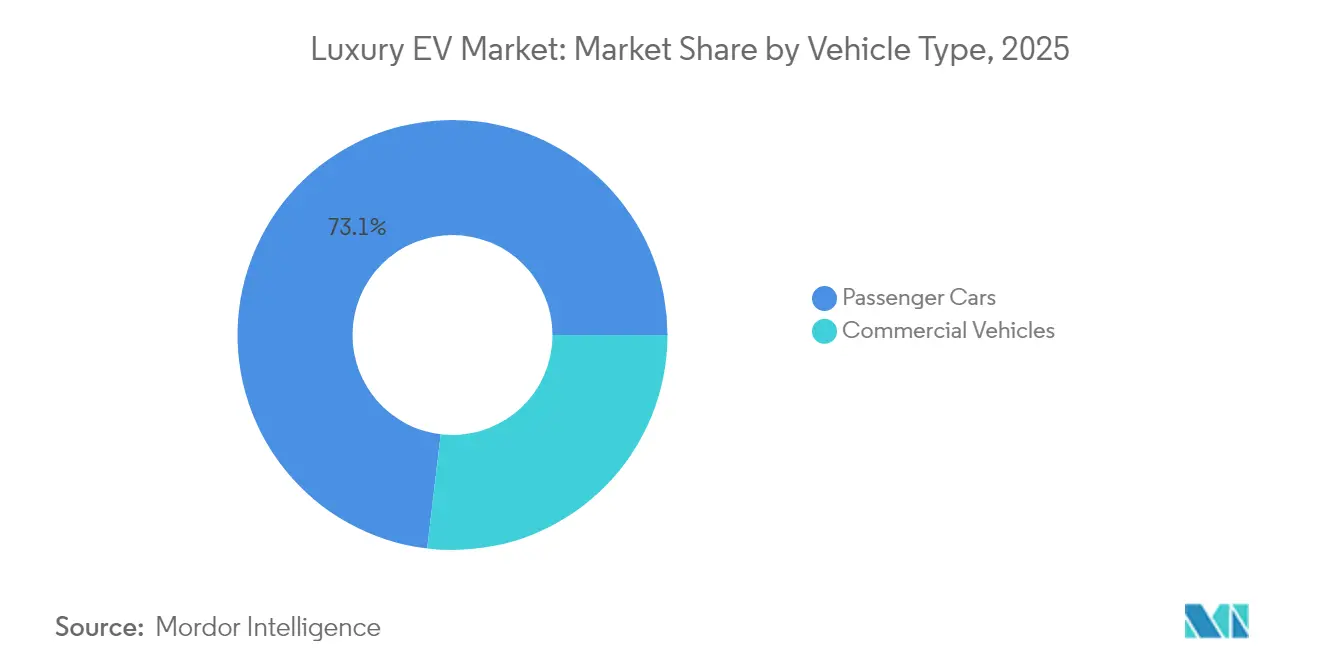

- By vehicle type, passenger cars held 73.12% share in 2025, whereas commercial fleets post the fastest 16.08% CAGR on the back of corporate electrification mandates.

- By propulsion, BEVs commanded 75.82% share of the Luxury EV market size in 2025 and continue to log the segment’s highest 16.63% CAGR through 2031.

- By price tier, the USD 80,000-149,000 bracket captured 38.05% of the Luxury EV market share in 2025, while the USD 500,000+ tier is projected to expand at a 16.31% CAGR through 2031.

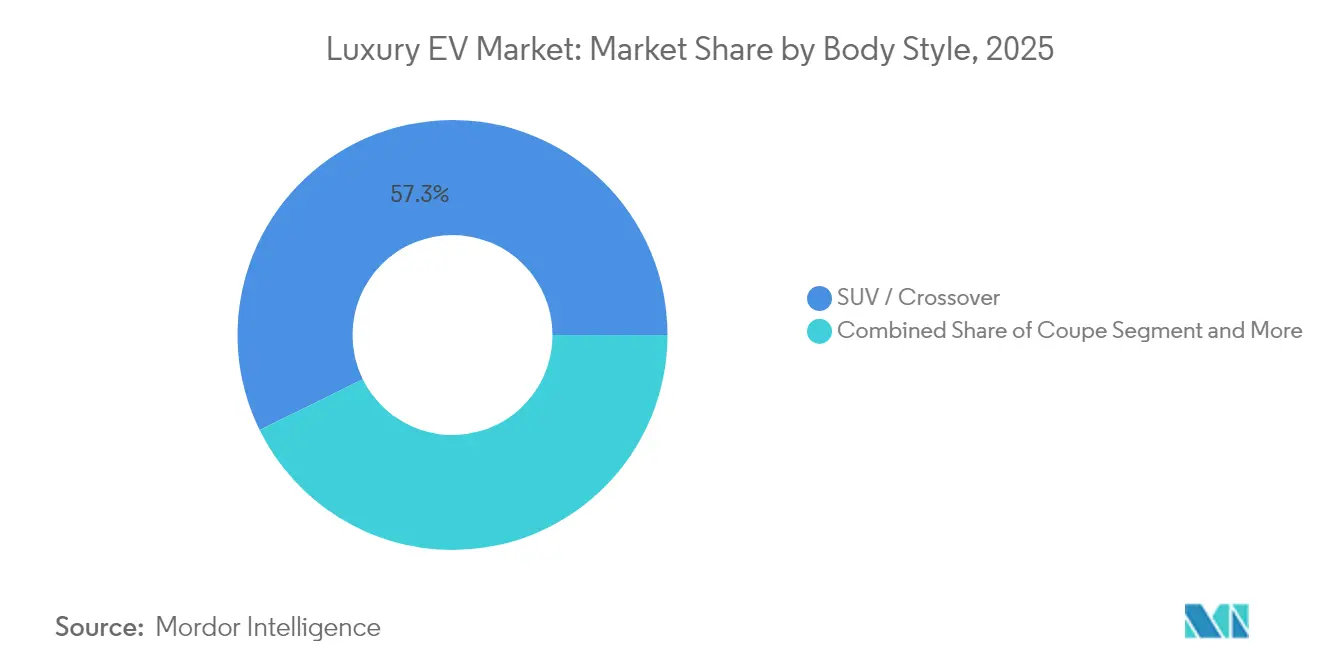

- By body style, SUVs and crossovers led with 57.28% revenue share in 2025; convertibles are advancing at a 16.78% CAGR to 2031.

- By ownership model, individual retail maintained 86.74% dominance of the Luxury EV market in 2025, yet subscription and leasing formats are set to grow at a 16.15% CAGR through 2031.

- By geography, Asia Pacific accounted for 35.84% of global revenues in 2025, while the Middle East & Africa region is forecast for the strongest 16.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Luxury EV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid battery-cost decline | +4.1% | Global, manufacturing cost advantages in Asia-Pacific | Long term (≥ 4 years) |

| Brand electrification pledges | +3.2% | Global, concentrated in premium segments | Medium term (2-4 years) |

| Premium-buyer EV tax incentives | +2.8% | North America and EU, selective Asia-Pacific markets | Short term (≤ 2 years) |

| Ultra-fast 800V charging platforms | +2.5% | North America and EU corridors, premium urban centers | Medium term (2-4 years) |

| Data-monetization and in-car subscription | +1.9% | Global, early adoption in North America and China | Long term (≥ 4 years) |

| Private-jet-to-garage carbon-offset programs boosting HNWI adoption | +1.2% | Global HNWI concentrations, UAE and North America leading | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Battery-Cost Decline Crossing USD 100/kWh Threshold

Lithium-ion pack costs slid below USD 100 per kWh in 2025 and are projected to reach USD 82 by 2026, slashing variable costs for 400-mile luxury models.[1]“Battery Metals Outlook 2025-2026,” Goldman Sachs, goldmansachs.com Silicon-carbide inverters add 15-20% drivetrain efficiency, effectively lowering the kilowatt-hours needed per mile and magnifying savings. Asian cell manufacturing hubs compound the cost tailwind, letting brands with established China-Korea supply chains undercut rivals on transaction price while preserving margins. Freed capital is redirected toward cabin-level differentiators such as mixed-reality head-up displays, enhancing the value proposition of the Luxury EV market. As economic parity with combustion luxury sedans is achieved, psychological barriers fall, converting the merely EV-curious into committed buyers.

Brand Electrification Pledges Accelerating Model Launches

Public promises from marquee automakers are compressing development cycles and reallocating capital toward high-end EV platforms. Porsche targets 80% of sales from battery models by 2030, compelling suppliers to prioritise 900 V lightweight traction systems for the brand’s premium volumes. Bentley’s full-electric commitment in the same year pulls partner ecosystems into rapid-iteration sprints, doubling the cadence of historically seven-year product refreshes. BMW’s Neue Klasse architecture will underpin six electric launches by 2028, a timeline that would once have covered a single flagship update. Investor pressure punishes laggards, evidenced by valuation discounts for luxury marques whose EV share trails premium peers. Collectively, these pledges expand the Luxury EV market by swelling model availability and fostering cross-brand competition that accelerates innovation.

Premium-buyer EV Tax Incentives Intensifying Demand

Targeted fiscal programmes now remove ownership penalties that historically muted luxury EV uptake. The United Kingdom scrapped its GBP 410 “expensive-car supplement” for zero-emission vehicles, collapsing the total-cost gap in the USD 80,000-150,000 band and triggering a pull-forward of affluent purchase intent.[2]“Vehicle Excise Duty Reform for Zero-Emission Vehicles,” UK HM Treasury, gov.uk Similar perks in several US states extend sales-tax waivers to models topping USD 80,000, driving showroom traffic ahead of scheduled sunset dates. European schemes cap corporate taxation for zero-emission company cars, creating incremental lift in executive-fleet procurement. The short-term geographic clustering of these benefits explains why the Luxury EV market scales faster in London, California and Germany than in comparable high-income regions without such levers. Urgency is heightened because incentive budgets are finite, fostering a now-or-never mindset among high-net-worth buyers.

Ultra-Fast 800 V Charging Platforms Enabling Long-Distance Touring

Porsche’s Taycan demonstrated 270 kW peak rates that restore 200 miles of range in 15 minutes, reframing public-charging dwell times for segment leaders. BMW’s forthcoming 800 V roll-out will extend similar convenience to its i5 and i7 successors, positioning the Luxury EV market for highway touring acceptance. Infrastructure partners, from Ionity to Electrify America, now co-site 350 kW dispensers along premium corridors—think Frankfurt-Monaco or Los Angeles-Las Vegas—closing the experiential gap with aviation lounge hospitality. For buyers accustomed to concierge-level travel, the ability to add 150-200 miles during a coffee stop extinguishes residual range anxiety. The medium-term impact is greatest in regions pitching leisure drive tourism, supporting second-home EV ownership and cross-border luxury excursions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Luxury-EV average transaction price | -3.7% | Global, acute in emerging markets | Medium term (2-4 years) |

| Public DC-fast-charger under-build | -2.9% | North America and developing markets, rural corridors | Long term (≥ 4 years) |

| OEM 800V supply-chain bottlenecks | -2.1% | Global, concentrated in premium EV manufacturing hubs | Medium term (2-4 years) |

| Import-tariff uncertainty | -1.8% | EU and GCC markets, spillover to luxury import corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Luxury-EV Average Transaction Price More Than USD 90,000 Limiting TAM

Luxury EV transaction prices average above USD 90,000, setting a practical ceiling on how many households can participate in the segment.[3]“Luxury EV Transaction Pricing Report 2025,” J.D. Power, jdpower.com In emerging economies, luxury penetration is already below 2% of total new-car sales, so incremental cost carries outsized demand risk. Corporate fleet budgets, often capped around USD 60,000, cannot justify executive EV sedans that list at USD 100,000-plus even after lifetime TCO savings. Sensitivity analyses show that when the electric premium exceeds 40% over a brand’s petrol equivalent, purchase intent drops sharply. Until battery cost declines track through to MSRP relief or innovative financing spreads the hit, the total addressable Luxury EV market remains constrained.

Public DC-Fast-Charger Under-Build vs. ICE Refuelling Density

Outside dense urban cores, charger count per vehicle lags internal-combustion pump density by a factor of five in North America and by seven in parts of Southeast Asia. Rural luxury owners who shuttle between city and vacation property still face 15-30 minute stops compared with sub-five-minute gasoline refuelling. The opportunity cost of that extra dwell time clashes with luxury expectations of frictionless mobility. Brands mitigate risk via private or semi-exclusive charging networks, but deployment costs feed back into higher sticker prices. As long as the infrastructure mismatch persists, the Luxury EV market will see geographically uneven adoption dominated by city-based buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Electrification

Commercial luxury vehicles generated 16.08% CAGR through 2031, the steepest ascent in the Luxury EV market. Fleet electrification mandates in New York, Paris and Shanghai require executive shuttles and premium ride-hailing services to pivot toward zero-emission drivetrains. Cadillac’s Escalade IQ arrives purpose-built for corporate clients who view carbon-neutral transportation as a stakeholder imperative. High daily utilisation makes fuel and maintenance savings tangible, supporting quicker payback and offsetting depreciation. Regulators issue green-lane privileges that shorten airport curb times, further sweetening adoption economics.

Passenger cars still wield 73.12% share but now grow slower than fleet counterparts. The segment thrives on brand loyalty and model variety; BMW’s i7 and Mercedes-Benz EQS offer flagship comfort with 400-mile ranges. Yet suburban infrastructure gaps temper long-distance appeal, and affluent households increasingly amortise their luxury budgets across SUVs and sports cars. Over-the-air software adds value by rolling out Level 3 driver assistance, though the upgrade revenue is proportionately smaller than in connected commercial vehicles where fleet managers subscribe to advanced telematics. The evolving mix suggests the Luxury EV market will trend towards balanced volumes between personal chauffeurs and discerning individual owners.

By Propulsion: Battery-Electric Dominance Accelerates

Battery-electric drivetrains commanded 75.82% share of 2025 segment revenues, and continue to post a leading 16.63% CAGR. Silent torque, zero tailpipe emissions, and regulatory perks solidify BEVs as the aspirational gold standard in luxury garages. Technology roadmaps point to solid-state cells post-2028, which will lift gravimetric density past 450 Wh/kg, compressing pack mass and liberating cabin space. That leap is poised to push the Luxury EV industry into competitive parity with mid-size business jets for regional travel convenience.

Plug-in hybrids serve as transitional hedges for buyers tied to long-range fuel infrastructure, but complexity and duplicated powertrains erode brand margins. Their global share is unlikely to rise above low double digits before tapering, as BEV infrastructure densifies and battery cost curves sink. Fuel-cell electric vehicles register negligible volumes because hydrogen dispensing is scarce outside Japan and California. Until refuelling economics improve, FCEVs remain showcase technology rather than a revenue pillar within the Luxury EV market.

By Price Tier: Ultra-Luxury Segment Leads Growth

The USD 500,000+ echelon, anchored by the USD 400,000 Rolls-Royce Spectre and Ferrari’s pending electric GT, logs the fastest 16.31% CAGR. Orders often close out two delivery cycles ahead, turning wait-lists into a marketing asset that elevates brand cachet and supports gross margins above 30%. These ultrahigh-net-worth clients treat environmentally conscious motoring as a status symbol, paying premiums for bespoke battery chemistries and artisanal interiors.

At the other end, the USD 80,000-149,000 bracket delivers volume, seizing 38.05% share in 2025. Automakers rely on modular skateboard platforms to streamline variants spanning performance tunes, wheel-base lengths and body styles. The segment’s competitiveness squeezes cycle-plan timetables; BMW’s i5 entered showrooms barely 30 months after initial concept freeze. Price-sensitive entrepreneurs in this bracket still weigh residual values; generous buy-back guarantees therefore underpin dealer finance programmes. Despite margin pressure, rivalry ensures the Luxury EV market continues to democratise access to advanced technology without diluting brand prestige.

By Body Style: SUV Dominance with Convertible Resurgence

SUVs and crossovers deliver 57.28% of total revenues as of 2025, benefiting from favourable ride height, cargo flexibility and family acceptance. Electric skateboard architectures tuck battery slabs low between the axles, preserving interior volume and refining driving dynamics. In fast-growing Asia, chauffeur-driven executives prefer rear-compartment leg-room that SUV cabin geometries naturally supply. Vehicles such as the Mercedes-Benz EQS SUV package 110 kWh usable energy yet still offer flat-floor seating for six adults, reinforcing SUV supremacy in the Luxury EV market.

Convertibles, once sidelined by structural-rigidity penalties, now emerge as the fastest 16.78% CAGR sub-segment. Purpose-built aluminium-spaceframe engineering offsets the mass of retractable roofs, while instantaneous electric torque makes top-down acceleration addictive. Silent propulsion amplifies open-air ambience—drivers can converse at highway speeds, an advantage over combustion sports cars. Premium brands like Maserati position their Folgore GranCabrio as an emotional complement to daily-driver SUVs, not a replacement, thus unlocking incremental rather than cannibalistic sales.

By Ownership Model: Subscription Models Transform Access

Retail ownership keeps a commanding 86.74% stake in the Luxury EV market, reflecting the cultural value affluent buyers place on sole title, personalised spec sheets and unlimited mileage freedom. Bespoke paint, interior trims and concierge-level after-sales reinforce the emotional bond difficult to replicate in shared-use schemes. However, software-defined vehicles now enable post-delivery monetisation—owners can subscribe to dynamic-light animations, Level 3 driver assistance or wellness-seat massages, pushing recurring revenue without surrendering title.

Subscription and leasing channels are nonetheless climbing at a brisk 16.15% CAGR. Ferrari’s forthcoming battery-subscription reduces up-front price shock by billing cell depreciation separately over three years, mirroring aircraft engine-hour contracts. Jaguar Land Rover bundles insurance, charging and maintenance into one payment, resonating with urban professionals who value convenience above permanent asset accumulation. Corporate fleets evaluate total mobility cost and carbon reporting obligations, making operational leases with guaranteed residuals attractive. Such models expand the Luxury EV industry to users who prioritise access over asset appreciation.

Geography Analysis

Asia Pacific contributed 35.84% of global turnover in 2025, confirming the region as the volumetric anchor of the Luxury EV market. China’s tier-one cities deploy preferential license plates and congestion exemptions that lift luxury EV deliveries to double-digit penetration. Domestic champions NIO and Xiaomi buttress volumes while imported flagships from Porsche and BMW benefit from localised battery supply chains that suppress landed cost. Japan’s battery know-how and South Korea’s materials science shorten innovation lead-times, reinforcing the regional ecosystem. Exchange-rate volatility and policy shifts are watchpoints, yet the structural tailwinds remain intact.

Middle East & Africa records a forecast 16.28% CAGR, the fastest worldwide. UAE’s Masdar City and Saudi Arabia’s Neom mandate zero-emission vehicle fleets, catalysing orders for Rolls-Royce Spectre and Lucid Air Dream Edition. Sovereign wealth funding excises infrastructure-financing risk; for example, Abu Dhabi installs 350 kW chargers at marina docks frequented by super-yacht owners. Harsh desert temperatures challenge battery thermal envelopes, so OEMs field specialised cooling loops, which in turn validate premium price tags. South Africa and Turkey represent secondary hubs where regional logistics and assembly incentives could blossom into export corridors for the Luxury EV market.

North America remains a core profit pool, shielded by entrenched dealer relationships and high-income demographics in Los Angeles, Miami and Toronto. Federal clean-vehicle credits, combined with state-level rebates, narrow transaction gaps and encourage model proliferation. The Supercharger network’s coast-to-coast coverage sets a baseline experience standard that rivals must now match by partnering with established operators. Nonetheless, rural charger scarcity restricts second-home owners in mountain or lake regions from relying solely on battery power, slightly tempering penetration growth. Europe’s luxury heartland extends from Stuttgart to Modena, leveraging stringent emission zones that bar combustion flagships from old-town districts, thereby nudging affluent collectors toward zero-tailpipe alternatives and cementing the Luxury EV market as a pillar of continental industrial policy.

Competitive Landscape

The Luxury EV market exhibits moderate concentration; the top five manufacturers account for roughly around three fifth of shipments, granting them pricing latitude yet preserving room for differentiated entrants. BMW sold more luxury EVs than the combined tallies of Mercedes-Benz and Audi in 2024, a payoff from early modular-platform bets and thermal-management patents. Tesla still leads global unit volume but feels the pinch of comparably priced German sedans that now match interior quality while offering access to broader service networks.

Platform consolidation dominates strategy. Volkswagen’s USD 5.8 billion stake in Rivian buys access to next-gen skateboard underpinnings with 900 V architecture, shaving development risk and accelerating Bentley’s EV portfolio. Mercedes and Porsche co-invest in synthetic-fuel research as hedge against regulatory divergence, but maintain electrification timelines to guard brand equity among eco-progressive clientele. Competitive pressure today revolves less around headline acceleration times and more around cockpit software fluidity, over-the-air update cadence and data privacy assurances.

Barrier-to-entry remains formidable: battery joint-venture equity, dedicated 350 kW charging alliances and brand-consistent digital ecosystems each require multibillion-dollar allocation. Start-ups outside China must therefore either specialise in ultra-niche designs above USD 500,000 or license core systems from incumbents. Private-equity interest persists in specialised suppliers—solid-state electrolyte makers, silicon-carbide inverter fabs—rather than in new badge aspirants, reinforcing the notion that coordination with established OEMs is the pragmatic pathway into the Luxury EV industry.

Luxury EV Industry Leaders

BMW AG

Mercedes-Benz Group AG

Tesla Inc.

BYD Co. In

Volkswagen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BMW announced production of electric X5, X6 and X7 SUVs at its Spartanburg plant by 2028, backed by a USD 1.7 billion US investment programme that adds an in-house battery assembly line.

- June 2025: General Motors committed USD 4 billion across US sites to scale luxury EV output for Chevrolet Silverado EV, GMC Sierra EV, Cadillac Escalade IQ and Cadillac Lyriq, targeting 2 million annual units.

- June 2025: Cadillac delivered the first hand-built Celestiq at USD 350,000, establishing a new pricing watermark for bespoke electric luxury.

- March 2025: Hyundai expanded its Georgia EV plant to 500,000-unit capacity under a USD 7.6 billion outlay, part of a USD 21 billion US roadmap driving premium-segment localisation.

Global Luxury EV Market Report Scope

Luxury electric vehicles, or high-end electric vehicles, are exclusively or partially powered by electric power. They are equipped with one or more electric motors and rely solely on energy stored in rechargeable batteries for propulsion.

Luxury EV Market is segmented by vehicle type, propulsion, and geography. By Vehicle Type, the market is segmented into Passenger cars, Vans, Medium and Heavy-Duty trucks, and Buses. By Propulsion, the market is segmented into Battery Electric Vehicle, Plug-In Hybrid Electric Vehicles, and Fuel Cell Electric Vehicles. By Geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market sizing and forecast have been done based on the value (USD) and Volume (Units).

| Passenger Cars |

| Commercial Vehicles |

| Battery-Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| USD 80k – USD 149k |

| USD 150k – USD 299k |

| USD 300k – USD 499k |

| More than or equal to USD 500k |

| Coupe |

| Convertible |

| SUV/Crossover |

| Sedan |

| Individual Retail |

| Subscription/Leasing |

| Corporate and Fleet |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Propulsion | Battery-Electric Vehicles (BEV) | |

| Plug-in Hybrid Electric Vehicles (PHEV) | ||

| Fuel-Cell Electric Vehicles (FCEV) | ||

| By Price Tier | USD 80k – USD 149k | |

| USD 150k – USD 299k | ||

| USD 300k – USD 499k | ||

| More than or equal to USD 500k | ||

| By Body Style | Coupe | |

| Convertible | ||

| SUV/Crossover | ||

| Sedan | ||

| By Ownership Model | Individual Retail | |

| Subscription/Leasing | ||

| Corporate and Fleet | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Luxury EV Market?

The segment is valued at USD 254.08 billion in 2026 and is projected to climb to roughly USD 530.16 billion by 2031.

Which price tier leads Luxury EV sales?

Vehicles priced between USD 80,000 and USD 149,000 hold 38.05% of 2025 revenue, making it the largest bracket.

Why are SUVs dominant in the Luxury EV space?

SUV and crossover layouts offer battery-pack packaging benefits, elevated driving positions and roomier cabins, securing 57.28% of 2025 sales.

Which region is growing the fastest for luxury EVs?

Middle East & Africa posts the highest 16.28% CAGR to 2031, driven by carbon-neutral megacity projects in the Gulf.

How do automakers monetise luxury EVs after the sale?

Connected-car data services, over-the-air feature unlocks and in-vehicle subscriptions generate recurring revenues approaching USD 310 per vehicle annually by 2030.

What limits broader adoption of luxury EVs?

High average transaction prices above USD 90,000 and slower deployment of fast-charging stations beyond major cities remain the primary constraints.

Page last updated on: