Luxury SUV Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

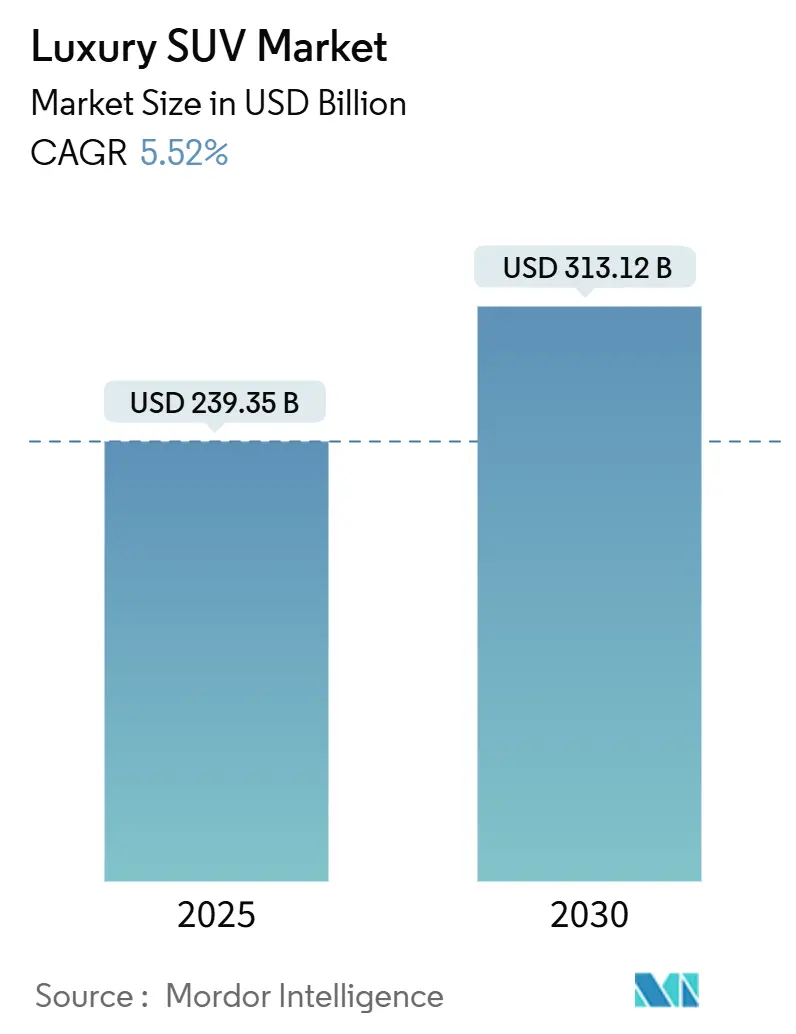

| Market Size (2025) | USD 239.35 Billion |

| Market Size (2030) | USD 313.12 Billion |

| Growth Rate (2025 - 2030) | 5.52% CAGR |

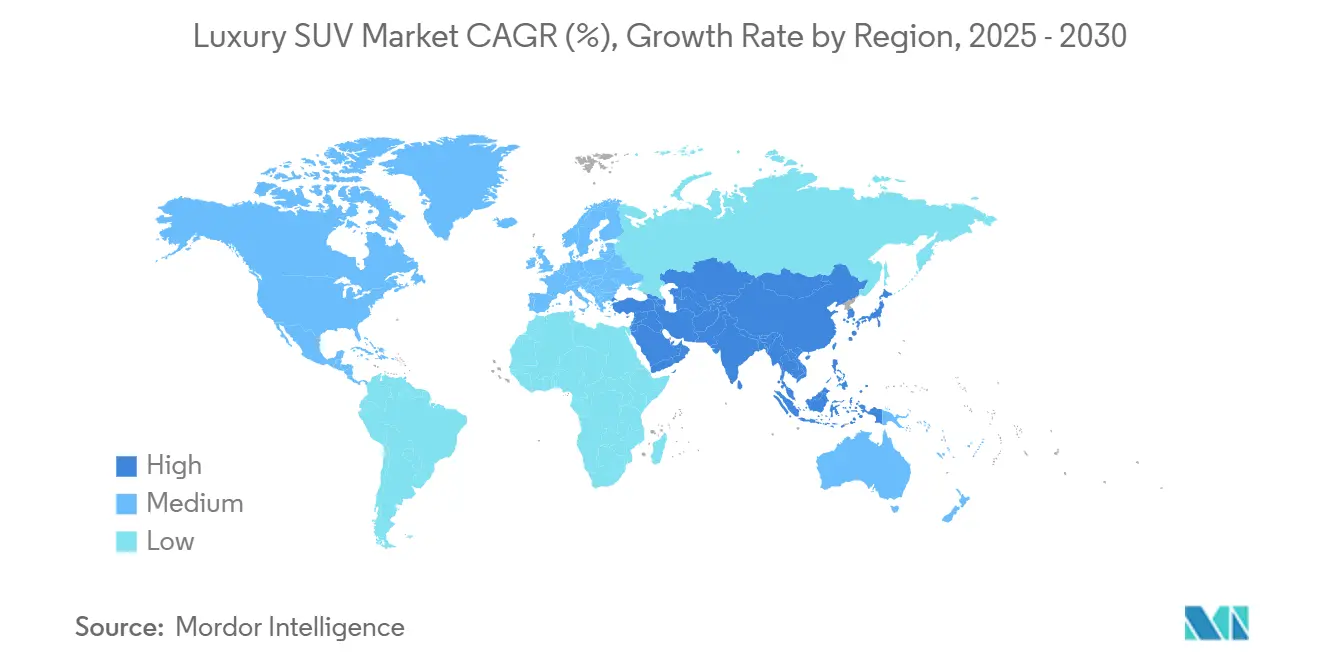

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxury SUV Market Analysis by Mordor Intelligence

The luxury SUV market reached USD 239.35 billion in 2025 and is forecast to expand at a 5.52% CAGR to USD 313.12 billion by 2030. Continued gains in global high-net-worth populations, rapid model electrification, and a clear buyer shift from sedans to sport-utility body styles underpin this expansion. Crossover architectures give automakers the flexibility to offer coupe-like silhouettes while preserving interior space, and over-the-air software services add recurring revenue that boosts total lifetime value per vehicle. Europe keeps its premium lead through brand heritage and supportive zero-emission incentives. At the same time, Asia-Pacific records the quickest unit and revenue growth on the back of rising affluence and charging-network build-outs.

Key Report Takeaways

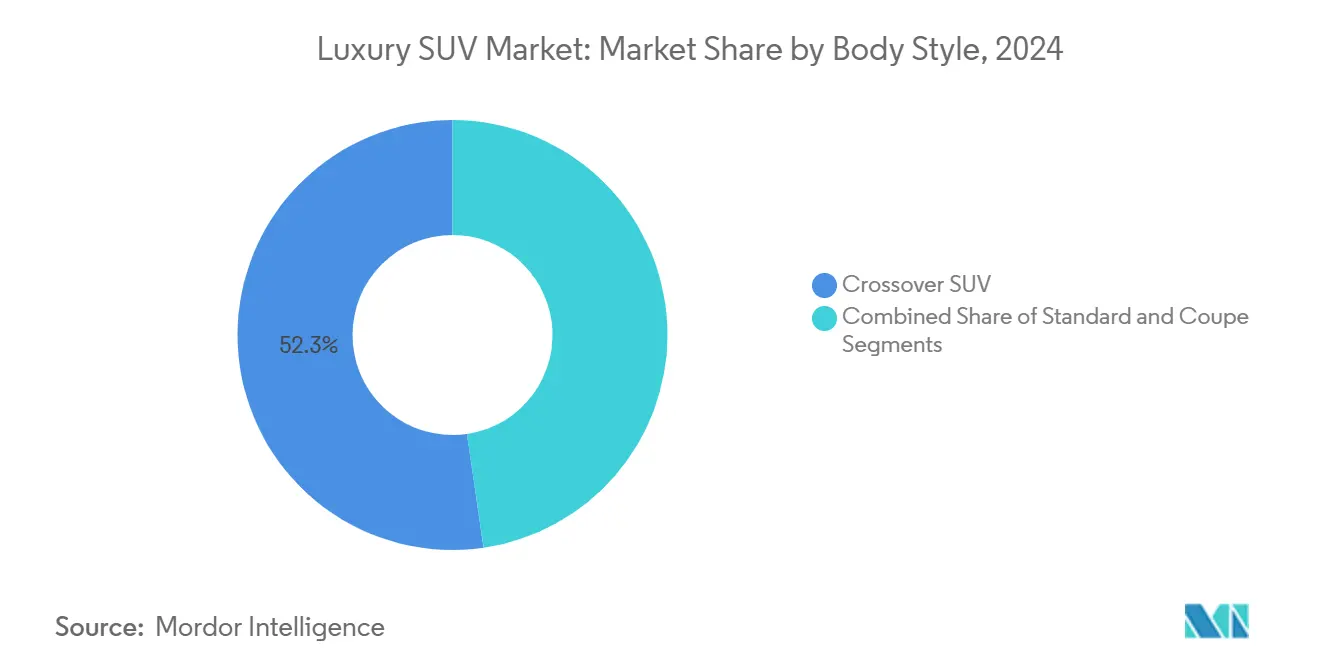

- By body style, crossover SUVs held 52.31% of the luxury SUV market share in 2024, while coupe SUVs are projected to advance at an 11.82% CAGR to 2030.

- By fuel type, petrol powertrains captured 61.24% of the luxury SUV market size in 2024; battery-electric variants are set to post a 25.15% CAGR through 2030.

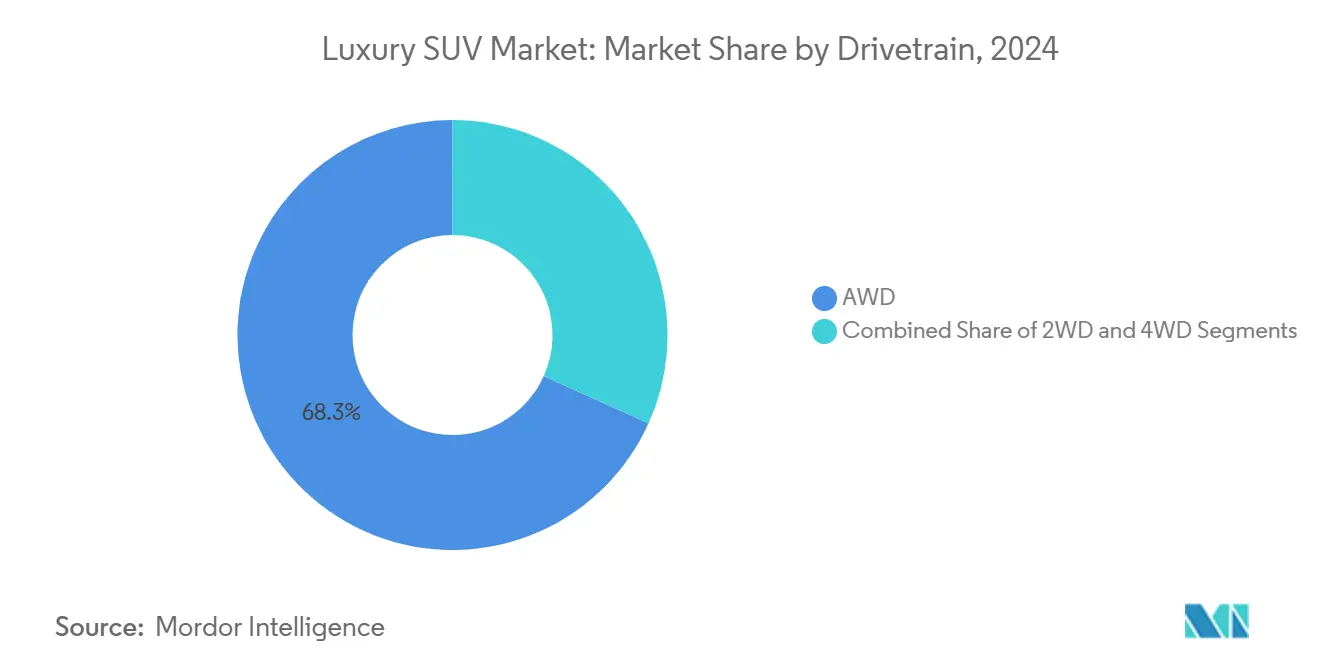

- By drivetrain, AWD configurations accounted for 68.27% of the luxury SUV market size in 2024 and are forecast to climb at a 9.72% CAGR over the forecast period.

- By seating capacity, five-seat layouts commanded 71.28% of the luxury SUV market share in 2024, whereas seven-seat formats will register an 8.42% CAGR to 2030.

- By geography, Europe captured a 32.13% share of the luxury SUV market in 2024, while Asia-Pacific is projected to be the fastest-growing region, with a 10.62% CAGR through 2030.

Global Luxury SUV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HNWI And UHNWI Population | +2.1% | Global, with early gains in North America, Asia-Pacific core | Long term (≥ 4 years) |

| E-SUV Launches | +1.8% | Global, spill-over to Europe and China | Medium term (2-4 years) |

| SUV Body-Style Preference | +1.2% | North America and EU, APAC core | Long term (≥ 4 years) |

| AI-Led In-Car Personalisation | +0.9% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Compact/Crossover Sub-Segment Expansion | +0.7% | Global | Medium term (2-4 years) |

| Subscription-Based Access Models | +0.4% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising HNWI and UHNWI Population Worldwide

Global HNWI ranks expanded in 2024 to more than 2.3 million individuals, supplying a steady pool of buyers for high-margin SUVs[1]“The Wealth Report 2024,” Knight Frank, knightfrank.com. Growth is strongest in the United States and Asia, reinforcing demand in markets where luxury vehicles remain a key status asset. Utility, prestige, and advanced technology converge in modern premium SUVs, making them preferred mobility symbols over discretionary purchases. Wealth creation in emerging economies also pulls first-time luxury buyers into the category. The demographic trajectory supports sustained volume and revenue growth over the long term.

Electrification Push Creating New Luxury E-SUV Launches

Premium automakers introduced multiple battery-electric SUVs during 2024-2025 to align with stricter CO₂ limits and growing eco-consciousness. Europe’s escalating malus tax raises the ownership cost of conventional powertrains, while similar credit schemes in China favor zero-emission production[2]“Malus écologique 2024,” Service-Public.fr, service-public.fr. Electric luxury SUVs now match or exceed petrol peers in range and torque, and simplified drivetrains lift gross margins by trimming mechanical content. These factors reinforce the luxury SUV market’s pivot toward high-priced electric derivatives and accelerate portfolio electrification up to 2030.

SUV Body-Style Preference Over Sedans Among Affluent Buyers

SUV penetration in Europe hit 54% in 2024, and the luxury slice grew 13%, confirming sustained buyer tilt toward raised ride heights and flexible cargo space[3]“European SUV Market Analysis 2024,” European Automobile Manufacturers Association, acea.auto. Similar patterns appear in North America and key Asian economies as affluent households juggle work, family, and leisure without sacrificing prestige. Crossover and coupe silhouettes widen the appeal by blending practicality with sporty aesthetics, allowing brands to boost average selling prices while serving multiple lifestyle needs. The preference gap over sedans is expected to widen as city infrastructure adapts to SUV dimensions and fuel-economy penalties on traditional large sedans rise.

AI-Led In-Car Personalization and OTA Upgrades Boosting Loyalty

Key automotive companies have shown how AI controls climate, music, and seat settings to individual preferences, raising perceived luxury and stickiness. Quarterly over-the-air updates let owners unlock new functions post-purchase, turning each vehicle into a software platform that remains current through its lifecycle. Similar strategies from BMW and other premium marques enable modular feature sales and recurring subscription income. The net result is higher customer retention and incremental revenue, which uplifts long-term segment profitability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High MSRP and Inflationary Cost | -1.4% | Global | Short term (≤ 2 years) |

| Stricter CO₂ / Luxury-Tax Regimes | -1.1% | Europe and China, spill-over to Global | Medium term (2-4 years) |

| Semiconductor and Material Supply Constraints | -0.8% | Global | Short term (≤ 2 years) |

| Cyber-Security Compliance | -0.3% | Global, with early impact in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High MSRP and Inflationary Cost Pressures

Average transaction prices for luxury SUVs climbed in 2024-2025 as raw-material costs and chip shortages squeezed supply, forcing automakers to raise sticker prices or prioritize higher-spec trims. While ultra-high-net-worth buyers absorb increases, price-sensitive affluent households delay purchases or switch to certified pre-owned units. Elevated interest rates further dampen short-term demand. The temporary squeeze trims immediate sales growth even as structural wealth trends remain favorable.

Stricter CO₂ / Luxury-Tax Regimes in Europe and China

France’s steep malus levy and China’s dual-credit targets elevate compliance costs for combustion-engine luxury SUVs. OEMs must either offset penalties through electric volumes or pay fines that erode margins. Smaller niche brands with limited electrification resources face added pressure, potentially consolidating share into the hands of larger players. Over the medium term, such regulation shifts demand from petrol and diesel toward hybrids and fully electric SUVs, altering model-mix profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Body Style: Crossover Dominance Drives Market Evolution

Crossover SUVs controlled 52.31% of the luxury SUV market share in 2024, owing to their sedan-like ride quality alongside higher seating and cargo flexibility. Automakers exploit shared unibody platforms to roll out multiple silhouettes quickly, cutting development costs while broadening buyer choice. Coupe SUVs, though smaller in volume, post the fastest 11.82% CAGR as younger, wealthy drivers seek expressive design aligned with sports-car lineage. Traditional body-on-frame SUVs retain traction among buyers valuing towing muscle and rugged aesthetics, especially in North America.

Cost-efficient modular architectures let brands such as Mercedes-Benz and BMW launch conventional and electric crossovers on the same underpinnings, preserving margins and hastening time to market. Superior aerodynamics in crossover shells aid regulatory compliance by extending electric driving range and trimming fleet CO₂ averages. These tailwinds assure crossovers of leadership in the luxury SUV market through the decade.

By Fuel Type: Electric Surge Challenges Petrol Dominance

Petrol engines still represent 61.24% of the luxury SUV market in 2024, benefiting from established refueling networks and instant performance familiarity. Yet battery-electric SUVs expand at a blazing 25.15% CAGR as high-capacity packs deliver 400-mile ranges and as charging infrastructure scales worldwide. Hybrids act as strategic bridges in regions where full-EV charging remains sparse, while diesel fades under tightening emission rules.

European markets spearhead electric adoption, bolstered by regulatory incentives and a robust charging infrastructure. Meanwhile, North American and Asian markets trail, showcasing diverse adoption rates influenced by regional policies and the state of their infrastructure. Premium brands exploit simpler electric drivetrains to pack in advanced infotainment and ADAS functions. The shift helps OEMs avoid punitive taxes and meet more demanding fleet standards, making electric share of the luxury SUV market inevitable by 2030.

By Drivetrain: AWD Systems Enhance Luxury Positioning

AWD layouts captured 68.27% of the luxury SUV market size in 2024, and are forecast to climb at a 9.72% CAGR as affluent buyers equate permanent traction with safety, confidence, and high-performance pedigree. Torque-vectoring, air-suspension, and predictive damping now come bundled with AWD packages, delivering sure-footed cornering and refined ride quality in snow, gravel, or city traffic. Electric dual-motor setups replicate these benefits while removing driveshaft bulk, freeing cabin space, and trimming mechanical losses that can dampen efficiency. Luxury brands highlight these technical gains in marketing campaigns that frame AWD as an indispensable hallmark of modern prestige. As a result, consumers increasingly treat the technology as table stakes rather than an optional upgrade, locking in its revenue dominance for the forecast horizon.

RWD and FWD derivatives still serve mild-climate or entry-luxury price points, yet their slice of the luxury SUV market share contracts as AWD trickles down the trim ladder. Automakers justify the wider rollout by bundling traction systems with profitable appearance packs and software-enabled drive modes that deepen customer personalization. High-output models layer electronic locking differentials and rally-inspired launch control on top of standard AWD, reinforcing exclusivity for performance enthusiasts. Regulatory fuel-economy pressures also favor sophisticated torque management that balances grip with energy efficiency, making basic two-wheel-drive variants less compelling. Consequently, even value-oriented luxury buyers are migrating toward AWD as the default specification.

By Seating Capacity: Family Dynamics Shape Configuration Preferences

Five-seat configurations led with 71.28% of the luxury SUV market share in 2024, because they merge city maneuverability with lounge-class rear comfort. Automakers lavish these cabins with ventilated massaging chairs, dual 5G infotainment screens, and scent-diffusion systems, elevating perceived luxury without the engineering complexity of a third row. Shorter wheelbases make parking and curb-side valet easier in dense urban centers, a priority for many HNWI households that cycle between multiple properties. The layout also supports larger cargo holds when seats fold flat, appealing to owners who split time between weekday commutes and weekend leisure activities. These attributes solidify the five-seater as the segment’s volume anchor through 2030.

Seven-seat formats, however, post an 8.42% CAGR as multi-generational travel and chauffeur-driven use cases gain popularity among wealthy families. Long-wheelbase EV platforms deliver flat floors that unlock generous third-row legroom, while captain’s chairs, rear-seat entertainment, and individual climate zones protect brand cachet. Demand is strongest in North America, the Middle East, and parts of Asia, where cultural norms favor group mobility and stature on the road. With charging infrastructure maturing, electric seven-seat SUVs further expand choice, ensuring sustained growth within this higher-capacity niche.

Geography Analysis

Europe retained 32.13% of the luxury SUV market share in 2024, anchored by storied marques, dense charging grids, and policy carrots that favor zero-emission premium models. Germany, the United Kingdom, and France dominate the showroom mix, with buyers eager to adopt cutting-edge ADAS and bespoke trim packages. The luxury SUV market size in the region also benefits from company-car taxation that increasingly rewards low-CO₂ fleets, steering corporate buyers into electric and plug-in hybrids. Though slower than Asia, near-term growth remains stable as replacement cycles shorten for tech-savvy owners.

Asia-Pacific is the fastest-growing luxury SUV territory at a 10.62% CAGR. China leads volume gains under supportive NEV quotas, a swelling upper-middle class, and domestic premium challengers. India posts double-digit expansion as wealthy consumers prioritize automotive symbols of success, while Japan and South Korea maintain steady replacement demand tied to tech updates. Localized production by global brands helps mitigate tariffs and currency swings, further stoking unit growth across the region.

North America advances because deeply entrenched SUV culture and affluent consumers favor high-output powertrains and spacious interiors. HNWI counts in the United States rose in 2024, translating directly into demand for high-priced trims with AI-driven personalization. Competitive leasing, long loan terms, and robust dealer networks sustain luxury SUV turnover. Manufacturers continue to localize battery-electric assembly to capture federal incentives and shield margins against import duties.

Competitive Landscape

The luxury SUV market demonstrates moderate concentration with established European and Japanese brands maintaining leadership through heritage, technology, and distribution advantages. Mercedes-Benz leads, followed by BMW, Audi, Jaguar Land Rover, and Lexus, collectively controlling the majority of sales. European incumbents leverage century-old craftsmanship reputations while accelerating portfolio electrification and Level-3 autonomy deployment. Brand equity, vertically integrated drivetrains, and dealer-network reach ensure scale advantages that latecomers struggle to match.

Strategic alliances and component sharing shape cost curves. BMW’s powertrain collaboration with Jaguar Land Rover lets both groups amortize R&D across greater volume, while Mercedes-Benz invests in proprietary software stacks to own the customer experience end-to-end. Chinese innovators and tech giants experiment with direct-to-consumer channels and subscription models, challenging the traditional franchise system and keeping incumbent pricing strategies in check.

White-space opportunities lie in ultra-luxury electric SUVs, software-as-a-service bundles, and urban subscription fleets. Players that integrate AI-based cockpit intelligence and seamless over-the-air commerce are poised to gain wallet share. Conversely, brands slow to electrify or to secure semiconductor supply risk ceding ground as buyers equate software prowess with modern luxury.

Luxury SUV Industry Leaders

Jaguar Land Rover

Lexus

Audi AG

BMW AG

Mercedes-Benz Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Xiaomi announced plans to sell its YU7 luxury electric SUV in Europe by 2027, promising Porsche-rivaling styling at disruptive price points.

- July 2025: BYD’s luxury marque Yangwang confirmed a 2026 Europe entry after domestic success with its floating-capable U8 EREV SUV.

- July 2025: Mazda Motor Europe unveiled the all-new MAZDA CX-5 crossover SUV to strengthen its regional premium push.

- March 2025: Lexus introduced the all-electric Lexus RZ, centering development on driving pleasure, extended range, fast charging, and expressive design.

Global Luxury SUV Market Report Scope

| Standard SUV |

| Crossover SUV |

| Coupe SUV |

| Petrol |

| Diesel |

| Hybrid |

| Electric |

| 2WD |

| 4WD |

| AWD |

| 5-Seater |

| 7-Seater |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Body Style | Standard SUV | |

| Crossover SUV | ||

| Coupe SUV | ||

| By Fuel Type | Petrol | |

| Diesel | ||

| Hybrid | ||

| Electric | ||

| By Drivetrain | 2WD | |

| 4WD | ||

| AWD | ||

| By Seating Capacity | 5-Seater | |

| 7-Seater | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current revenue size of the luxury SUV market?

The luxury SUV market size reached USD 239.35 billion in 2025.

How fast is the segment expected to grow through 2030?

The market is projected to record a 5.52% CAGR, taking revenue to USD 313.12 billion by 2030.

Which body style holds the largest share among premium SUVs?

Crossover models dominate with 52.31% luxury SUV market share in 2024.

Which powertrain is expanding the quickest?

Battery-electric luxury SUVs are forecast to post a 25.15% CAGR over the next five years.

Which region leads volume growth?

Asia-Pacific registers the fastest regional CAGR at 10.62% through 2030.

Page last updated on: