Autonomous Truck Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

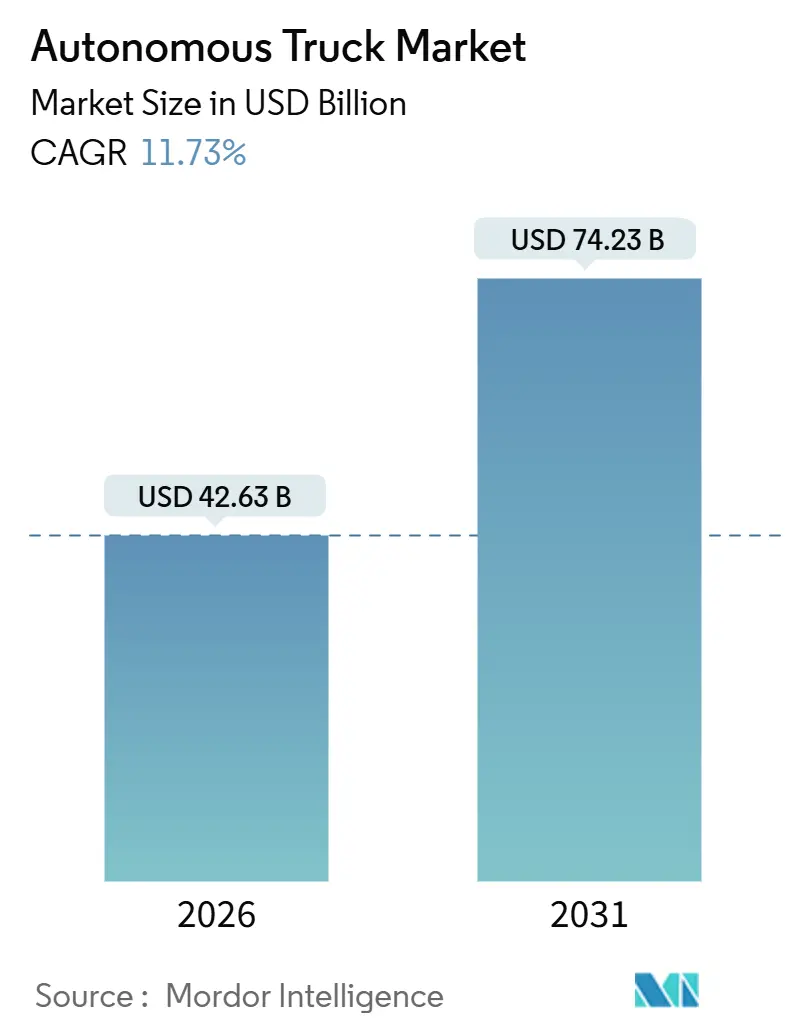

| Market Size (2026) | USD 42.63 Billion |

| Market Size (2031) | USD 74.23 Billion |

| Growth Rate (2026 - 2031) | 11.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

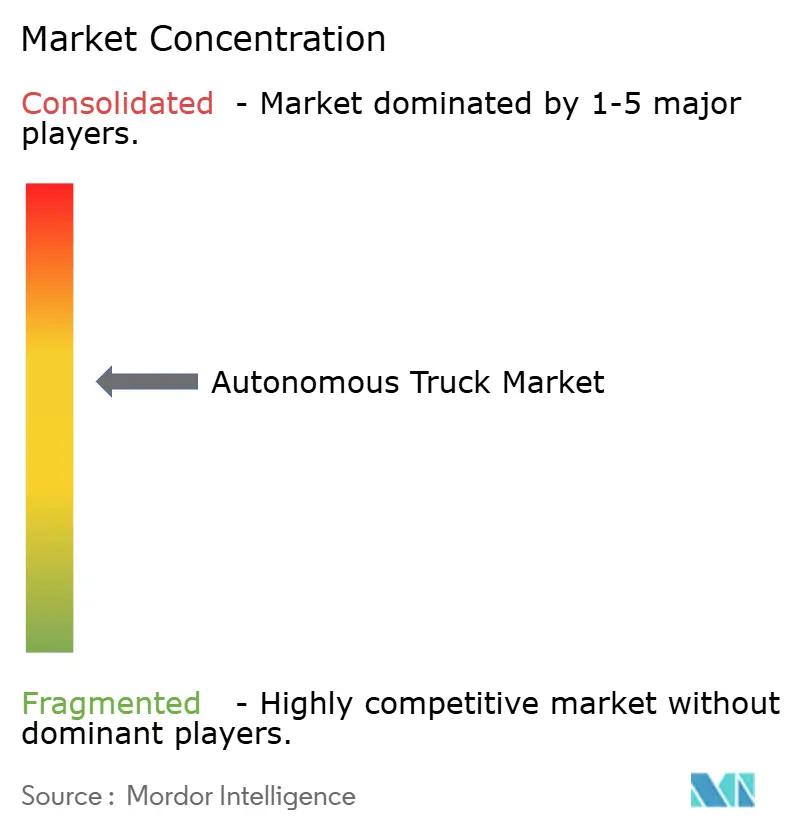

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Autonomous Truck Market Analysis by Mordor Intelligence

The autonomous truck market size reached USD 42.63 billion in 2026 and is projected to attain USD 74.23 billion by 2031, representing an 11.73% CAGR. Acute driver shortages, the need for continuous hub-to-hub logistics, and cost convergence between zero-emission powertrains and Level 4 highway-pilot systems underpin demand growth. The autonomous truck market continues to benefit from sensor‐suite price declines, government incentives for low-carbon freight corridors, and the emergence of software-defined vehicle architectures that shorten development timelines. Competitive intensity is rising as established original-equipment manufacturers integrate proprietary stacks while software-first newcomers license their platforms broadly. Moderate market concentration leaves room for regional and application-specific challengers, especially in middle-mile and port drayage segments.

Key Report Takeaways

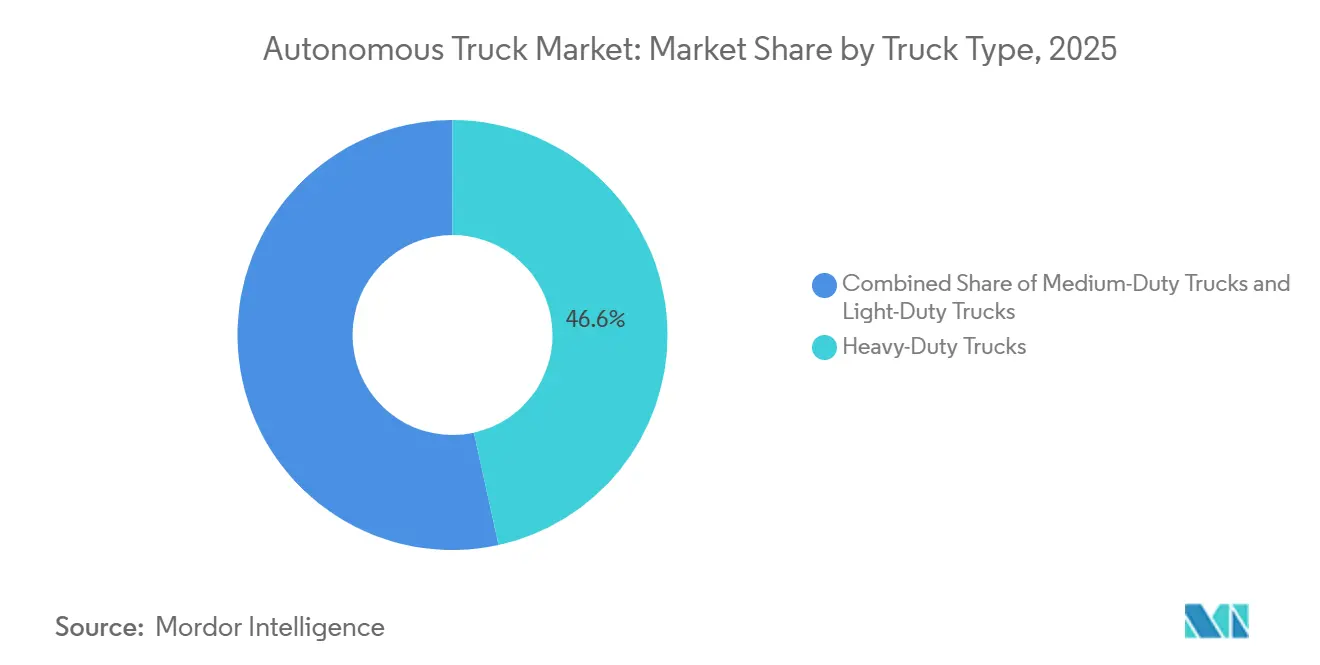

- By truck type, heavy-duty platforms led with 46.57% of the autonomous truck market share in 2025, while medium-duty trucks are forecast to advance at a 13.34% CAGR through 2031.

- By autonomy level, SAE Level 1-2 systems held 71.87% of the autonomous truck market in 2025, whereas Level 4 platforms record the fastest trajectory at a 15.21% CAGR to 2031.

- By ADAS feature, adaptive cruise control accounted for 35.43% of the autonomous truck market size in 2025, and highway-pilot capability is poised to expand at a 15.56% CAGR through 2031.

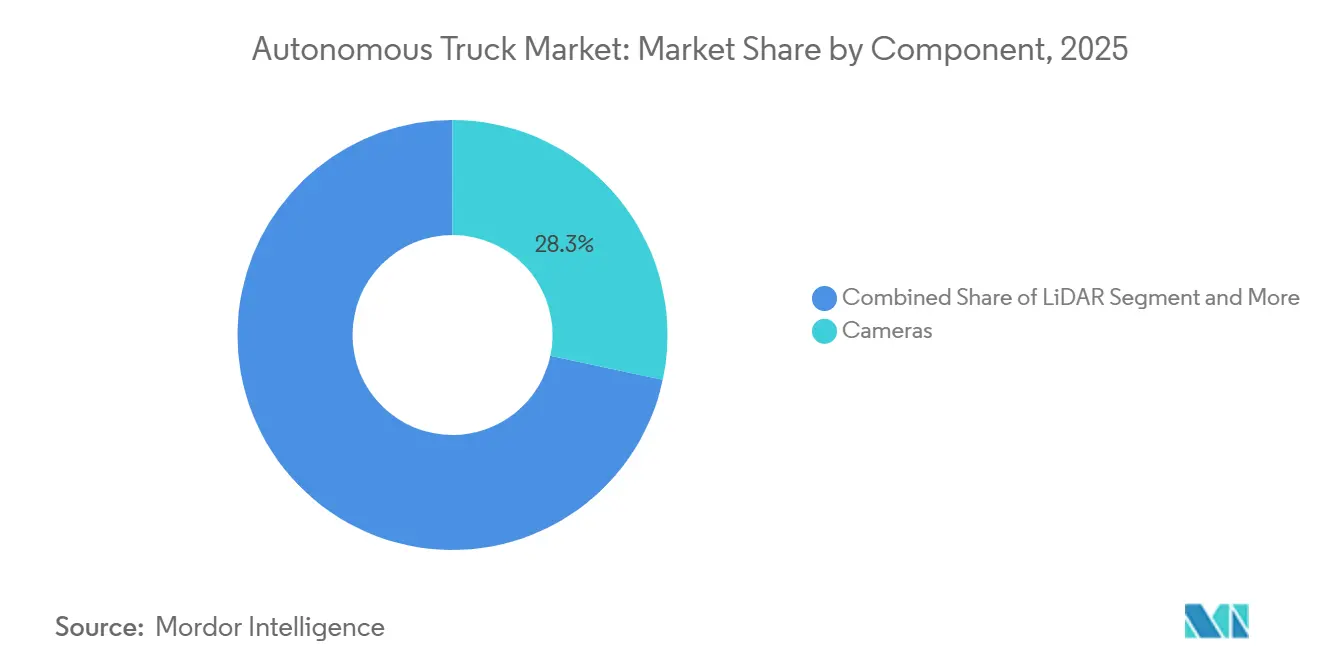

- By component, cameras captured 28.34% of the autonomous truck market in 2025; LiDAR adoption will outpace peers at a 15.24% CAGR to 2031.

- By drive type, internal-combustion trucks represented 64.79% of the autonomous truck market share in 2025, while battery-electric trucks will rise at a 17.78% CAGR through 2031.

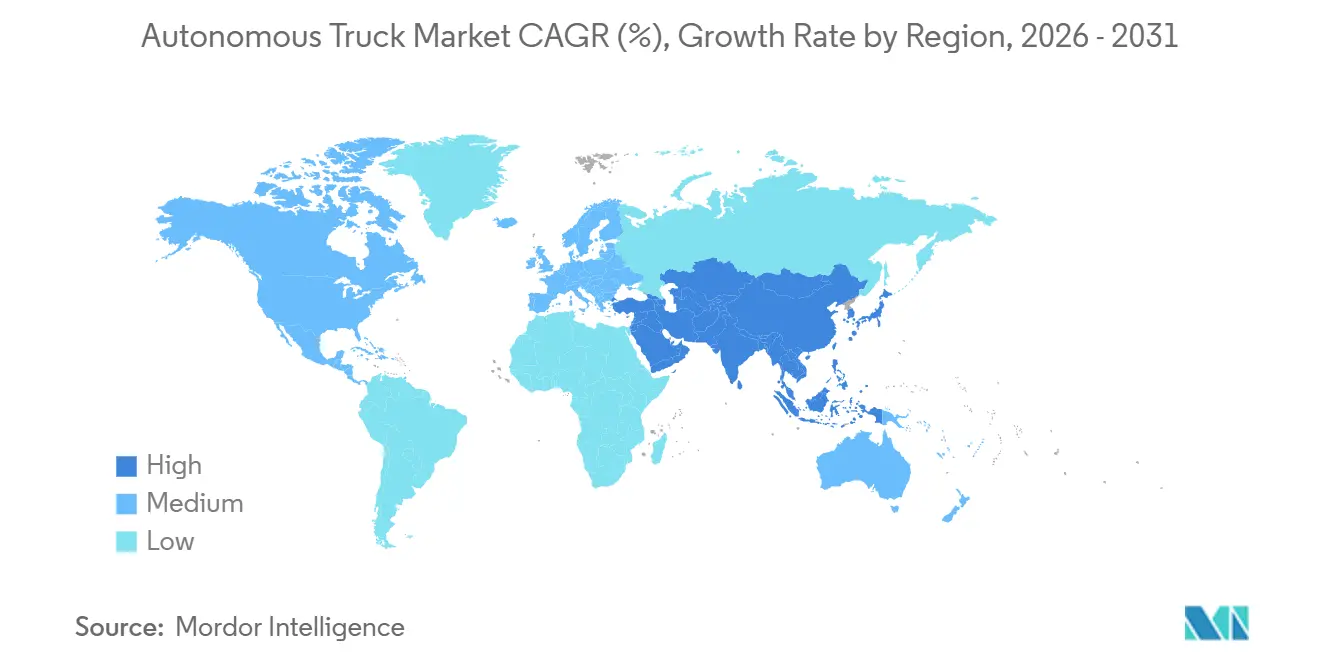

- By geography, North America held 37.46% of 2025 revenue, and Asia-Pacific is set to grow at a 13.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Autonomous Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver Shortage and Line-Haul Labor Cost | +2.8% | North America, Europe, Japan | Medium term (2-4 years) |

| 24/7 Hub-to-Hub Logistics | +2.3% | Global, concentrated in North America & China | Short term (≤ 2 years) |

| Zero-Emission Powertrains | +2.0% | North America, EU, China | Long term (≥ 4 years) |

| Edge-AI Foundation Models | +1.7% | Global, early adoption in North America & EU | Medium term (2-4 years) |

| Green-Corridor Tax Incentives | +1.5% | United States, EU member states | Long term (≥ 4 years) |

| Tightening Safety Regulations | +1.2% | North America, EU, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Driver Shortage and Rising Line-Haul Labor Cost

Chronic gaps in driver availability and escalating wages redefine freight economics in favor of automated line-haul operations. The Federal Motor Carrier Safety Administration limits human operators to 11 driving hours within a 14-hour window, a regulation that caps asset utilization at roughly half of every day[1]"Summary of Hours of Service Regulations", Federal Motor Carrier Safety Administration, fmcsa.dot.gov. Autonomous tractors running mapped interstate corridors can operate for extended hours, limited mainly by fueling/charging, inspections, and maintenance. ATA-reported large-truckload driver turnover has been around/above 90% in some periods, intensifying the incentive to deploy Level 4 trucks on predictable lanes. European and Japanese fleets face similar demographic pressure as younger workers avoid long-haul careers. Autonomous hub-to-hub shuttles, therefore, enable carriers to redeploy scarce human drivers to first-mile and last-mile routes that remain regulation-bound.

Demand for 24/7 Hub-to-Hub Logistics

E-commerce growth and just-in-time manufacturing create demand for nonstop freight flows that manual operations cannot sustain under hours-of-service rules. Autonomous trucks on fixed terminals can deliver round-the-clock service without contravening rest mandates. Freight integrators have already demonstrated overnight pilot lanes (e.g., Dallas–Houston) aimed at materially improving tractor utilization. China’s national modernization plan designates key manufacturing corridors for autonomous freight, targeting significant reductions in average transit time. Retailers and third-party logistics providers see continuous autonomy as a hedge against driver-availability volatility, especially during seasonal spikes when spot rates often triple.

Collaboration of Autonomy with Zero-Emission Powertrains

Bundling autonomous stacks with battery-electric and hydrogen fuel-cell platforms unlocks cost collaborations, since sensors, compute, and traction inverters leverage a common high-voltage backbone. The U.S. Environmental Protection Agency mandates that 40% of new heavy-duty sales reach zero emissions by 2032, accelerating joint development programs that combine autonomy, connectivity, and electrification[2]Yihao Xie, "U.S. EPA Phase 3 greenhouse gas emission standards for heavy-duty vehicles", International Council on Clean Transportation, theicct.org. Regenerative braking and torque vectoring simplify autonomous control logic, improving emergency-stop reliability. Fleet operators gain an additional incentive because long duty cycles inherent in electric freight help amortize sensor costs. Hydrogen fuel-cell models offer quick refueling that complements autonomous long-haul routes, although infrastructure availability remains limited.

Edge-AI Foundation Models Cut Validation Cycles

Transformer-based perception models and edge AI accelerators reduce the volume of real-world mileage needed to certify autonomy. Integrated systems now perform real-time inference on complex traffic scenarios within a consolidated, ~1,000 INT8 TOPS-class onboard compute envelope. Faster learning curves permit software updates that correct edge cases in weeks rather than months. Regulators weigh how to adapt functional-safety rules written for deterministic code toward probabilistic neural networks, but the technology’s ability to generalize across unseen conditions still accelerates commercialization. In parallel, on-board inference reduces latency dependency on the cloud, supporting safe operation in cellular dead zones common to rural corridors.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-Border Liability | -1.8% | Global, acute in EU cross-border routes & U.S. interstate | Long term (≥ 4 years) |

| LiDAR/Sensor-Suite Costs | -1.5% | Global, most constraining in price-sensitive South America & Africa | Medium term (2-4 years) |

| Cybersecurity and OTA Updates | -1.2% | Global, heightened scrutiny in North America & EU | Short term (≤ 2 years) |

| Opaque Transformer Models | -0.9% | North America, EU, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patchwork Global Regulation and Cross-Border Liability

Divergent legal frameworks divide the autonomous truck market across regions. Germany has established a legal framework for Level 4 autonomous driving in defined operating areas, subject to approval and oversight; however, it still requires safety drivers in France and Spain, creating a discontinuity that disrupts cross-border logistics. The United States governs autonomy largely at the state level, resulting in a mosaic of insurance and data-sharing mandates. Liability allocation remains unresolved regarding the distribution of fault among the OEM, software provider, and fleet operator. Such uncertainty elevates insurance premiums and deters small and mid-size carriers from investing until precedents stabilize. Harmonization efforts continue, but the timeline spans beyond the current forecast horizon, thereby tempering growth.

High LiDAR/Sensor-Suite Costs

Equipping a Class 8 tractor with redundant cameras, LiDAR, RADAR, ultrasonic sensors, and high-performance computing adds up to USD 50,000 per vehicle. Although unit prices for solid-state LiDAR have declined to below USD 1,000, integration labor and redundant actuators keep the total bill-of-materials high. Smaller fleets lack negotiating leverage for volume discounts. Emerging leasing and sensor-as-a-service models convert large capital expenditures into operational fees, yet these structures are not universally available in developing regions. High acquisition cost, therefore, postpones adoption in price-sensitive markets until economies of scale mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Truck Type: Medium-Duty Gains on Urban Autonomy

Heavy-duty tractors retained 46.57% of 2025 revenue due to their dominance in long-haul applications where labor savings and high mileage maximize payback. Light-duty trucks remain niche because lower payload limits dilute the economic advantage of costly sensor suites. Medium-duty platforms account for a smaller base yet will advance at a 13.34% CAGR from 2026 to 2031, driven by regional-haul and last-mile routes within geofenced areas that experience predictable traffic patterns. The autonomous truck market benefits from retailers linking micro-fulfillment centers via dedicated Class 6 box trucks outfitted with Level 4 stacks.

The shift toward medium-duty autonomy aligns with rising e-commerce density inside metropolitan regions. High stop-start duty cycles favor electrification, and electric drivetrains integrate efficiently with autonomous control logic. Heavy-duty tractors continue to test multi-state corridors, yet regulatory risk concentrates investment in locations where statutes explicitly permit driverless operation. Light-duty experimentation centers on campus environments where speed is limited, suggesting that broader scale will follow only when combined payload and autonomy economics improve. Overall, these dynamics reinforce medium-duty trucks as the fastest growing slice of the autonomous truck market.

By Level of Autonomy: Level 4 Surges as Sandboxes Expand

SAE Level 1-2 driver-assist systems captured 71.87% of the 2025 autonomous truck market, reflecting a large installed base of adaptive cruise control and lane-keeping features. However, Level 4 platforms are projected to scale at a 15.21% CAGR through 2031 as state-approved sandboxes in Texas, Arizona, and Bavaria allow fully driverless operation on mapped highways. The autonomous truck market size for Level 3 systems remains modest because handoff requirements create liability risk that many fleets avoid. Level 5 universal autonomy remains beyond the current forecast window due to sensor and compute constraints.

Commercial pilots show that Level 4 highway-pilot routes capture most of the economic benefit without requiring complete geographic coverage. Remote supervision centers monitor multiple tractors, amplifying labor productivity. Safety regulators focus on performance within defined operating domains rather than theoretical perfection everywhere, which accelerates certification for corridor-specific deployments. Level 1-2 features will continue as mandatory safety baselines, yet their contribution to total addressable value diminishes over time. Consequently, Level 4 systems become the primary revenue engine of the autonomous truck market.

By ADAS Feature: Highway Pilot Leads Innovation

Adaptive cruise control retained 35.43% of the autonomous truck market share in 2025, yet highway-pilot functionality is positioned to expand at a 15.56% CAGR through 2031. Highway-pilot stacks integrate lane-keeping, lane-change automation, and congestion management into a cohesive package that handles 95% of interstate driving. Blind-spot detection and lane-departure warning are now standard equipment on most new tractors, so their incremental growth slows.

Traffic jam assist delivers automation at speeds below 40 km per hour but remains less relevant to long-haul economics. Automatic emergency braking is mandated by European regulation, ensuring near-universal presence but limited differentiation. Lane-keeping assist prevents drift accidents yet lacks the situational awareness to negotiate complex merges. Highway pilot systems supplement sensor fusion with high-definition maps and vehicle-to-vehicle communication, which elevates fuel efficiency through optimized platooning. This broader capability set underpins their position as the leading driver of feature-level revenue within the autonomous truck market.

By Component: Solid-State LiDAR Gains on Cost Decline

Cameras led 2025 revenue with a 28.34% share, reflecting their low cost and dual function in driver monitoring and road-scene interpretation. Nonetheless, LiDAR units will grow at a 15.24% CAGR through 2031, increasing the autonomous truck market size for perception technology. Solid-state architectures have crossed the USD 1,000 price threshold, enabling mass-market adoption. RADAR sensors remain essential for all-weather detection, yet their spatial resolution is insufficient alone for centimeter-level localization.

AI compute modules escalate in value as sensor streams proliferate. System-on-chip designs integrate sensor preprocessing, neural inference, and motion control in one package, reducing latency and power draw. Ultrasonic sensors retain utility in low-speed maneuvers but contribute marginal revenue due to limited unit price. The shift toward sensor fusion increases demand for redundant networking and thermal management solutions, which adds ancillary opportunities for suppliers. Overall, LiDAR maturity changes the bill-of-materials mix and accelerates penetration within the autonomous truck market.

By Drive Type: Battery-Electric Leads Autonomy Integration

Internal-combustion trucks held 64.79% of the autonomous truck market share in 2025, yet battery-electric vehicles are forecast to expand at a 17.78% CAGR, the fastest among drive types. Regulatory mandates for zero-emission freight corridors drive fleet interest, and bundling autonomous stacks with electric drivetrains enables longer daily utilization that optimizes return on investment. Hybrid trucks serve transitional applications but add weight and complexity. Hydrogen fuel-cell models suit routes exceeding 500 miles, although refueling infrastructure availability limits deployment scale.

Battery-electric tractors simplify autonomous control due to their instantaneous torque delivery and regenerative braking capabilities. Eligibility for purchase incentives under clean-transport policies further improves payback. Internal-combustion vehicles continue to dominate regions lacking charging networks, yet diesel’s growth slows as carbon-border adjustments raise costs. Hybrid solutions cater to operators reluctant to adopt full electrification but face diminishing value as battery ranges extend. Hydrogen fuel-cell expansion depends on national fueling strategies and fleet clustering in ports and mining sites. These dynamics collectively shape drive-type allocation within the autonomous truck market.

Geography Analysis

North America accounted for 37.46% of 2025 revenue and is projected to register a 9.52% CAGR through 2031. Multiple states authorize driverless testing on public highways, making the region the largest commercial sandbox. Ten U.S. DOT-designated Automated Vehicle Proving Grounds support testing and validation, and cross-border lanes into Mexico and Canada stand to benefit once legal harmonization advances. Dense interstate freight networks and generous clean-transport subsidies underpin sustained demand across long-haul, refrigerated, and parcel segments.

Europe is forecasted to expand at a 9.43% CAGR to 2031. EU CO₂ standards for new heavy-duty vehicles aim for a reduction of ~45% by 2030, 65% by 2035, and 90% by 2040 (compared to the baseline), with specific rules in place for each vehicle category, catalyzing investment in combined electric and autonomous technologies. Germany leads with dedicated autobahn corridors, while France and Spain progress at a measured pace due to safety driver stipulations. Eastern Europe remains early-stage as infrastructure and financing mature. Western Asia shows double-digit growth as sovereign wealth funds modernize port logistics through 24-hour autonomous container shuttles.

Asia-Pacific will grow fastest at a 13.33% CAGR, reflecting national pilot zones in China and government-backed truck platooning programs in Japan and South Korea. Dense manufacturing clusters and aging workforces accelerate adoption. China’s Greater Bay Area supports the world’s largest fleet of driverless trucks on dedicated lanes linking factories to port terminals. South Korea invests heavily in 5G-enabled highways tailored for connected autonomy. Southeast Asian nations adopt a wait-and-see approach until sensor costs fall and financing mechanisms adapt to local conditions. Collectively, rising freight volumes and supportive policy drive regional leadership in the autonomous truck market.

Competitive Landscape

The autonomous truck market displays moderate concentration. Global OEMs such as Daimler, Volvo, and Traton leverage manufacturing scale and service networks to bundle autonomous software with vehicle sales. Technology specialists pursue asset-light models that license their stacks across multiple brands, enabling faster iteration and broader reach. Strategic partnerships dominate as capital requirements and regulatory complexity encourage shared risk.

Joint ventures align complementary strengths. An alliance between PACCAR and a leading autonomy developer targets production of Level 4 tractors for a 2027 launch, merging manufacturing expertise with perception and planning software. Tier-one suppliers invest in redundant braking and steering, positioning themselves as critical gatekeepers for functional safety. Start-ups secure equity from traditional OEMs in exchange for exclusive supply agreements, illustrating co-dependency across the value chain.

Patent activity reveals competitiveness. Filing volumes concentrate on sensor fusion, fail-safe control, and energy management. Standardization efforts under SAE International guide interoperability, shaping whether proprietary stacks remain walled gardens or converge on open architectures. Market expansion into retrofit kits opens a path for software-centric challengers to access the legacy fleet. Overall, diverse strategies coexist as players vie for share in a rapidly scaling autonomous truck market.

Autonomous Truck Industry Leaders

-

Daimler Truck AG

-

AB Volvo

-

Traton SE

-

PACCAR Inc.

-

BYD Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Pony.ai announced Gen-4 autonomous trucks co-developed with SANY Truck and Dongfeng Liuzhou Motor.

- September 2025: International Motors announced customer fleet trials of second-generation autonomous vehicles (with PlusAI) along the I-35 corridor.

- September 2025: Toray and T2 announced an autonomous truck trial, with runs scheduled to start on September 16, 2025.

- May 2025: Aurora Innovation inaugurated a commercial self-driving trucking service in Texas and plans expansion to El Paso and Phoenix by the end of 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the autonomous truck market as the annual revenue generated by new light, medium, and heavy-duty trucks equipped with at least SAE Level 1 driver-assist hardware and software that can be upgraded to higher autonomy through over-the-air or embedded stacks.

Vehicles retrofitted after first registration, pilot-only mining haulers, and autonomous yard tractors are outside this remit.

Segmentation Overview

-

By Truck Type

- Light-Duty Trucks

- Medium-Duty Trucks

- Heavy-Duty Trucks

-

By Level of Autonomy

- SAE Level 1- 2 (Driver Assist)

- SAE Level 3 (Conditional)

- SAE Level 4 (High)

- SAE Level 5 (Full)

-

By ADAS Feature

- Adaptive Cruise Control

- Lane Departure Warning

- Traffic Jam Assist

- Highway Pilot

- Automatic Emergency Braking

- Blind-Spot Detection

- Lane-Keeping Assist

-

By Component

- LiDAR

- RADAR

- Cameras

- Ultrasonic and Other Sensors

- AI Compute Modules

-

By Drive Type

- Internal-Combustion

- Battery-Electric

- Hybrid

- Hydrogen Fuel-Cell

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- India

- China

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- Egypt

- South Africa

- Rest of Middle-East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview fleet planners, Tier-1 ADAS suppliers, sensor fabs, and highway regulators across North America, Europe, and Asia Pacific.

Desk Research

We start with production and registration statistics from bodies such as the Organisation Internationale des Constructeurs d'Automobiles, the US Federal Motor Carrier Safety Administration, Eurostat road freight tables, and the International Transport Forum. Sensor import-export lines from UN Comtrade, patent trends gathered through Questel, and cost curves in academic journals on LiDAR and AI compute give early benchmarks. Company 10-Ks, investor decks, and press releases supply price points, while D&B Hoovers offers unit shipment clues for selected OEMs. The titles listed illustrate, not exhaust, the reference pool that analysts scan continuously.

Our desk work is complemented by periodic sweeps of trade association briefs, regional safety mandates, and open regulatory dockets that hint at the pace of Level 4 route approvals. Many smaller yet insightful documents surface only through Dow Jones Factiva's curated archive.

Market-Sizing & Forecasting

A blended top-down, bottom-up construct is applied. Global Class 6-8 production and freight-ton-kilometer pools are sized first, then adjusted by autonomy penetration rates derived from primary interviews, before supplier roll-ups and sampled ASP × volume checks fine-tune totals. Key inputs include driver shortage ratios, LiDAR cost declines, regulatory go-live corridors, battery-electric adoption in heavy haul, and platooning mileage incentives. Multivariate regression with scenario analysis projects each driver, while gap years lacking hard data are smoothed using three-year moving averages reviewed with subject experts.

Data Validation & Update Cycle

Outputs pass variance screens versus historical freight earnings, peer financials, and customs flows, followed by a two-level analyst review. Reports refresh yearly, and interim updates trigger when rule-making, price shocks, or landmark pilots materially shift baselines.

Why Mordor's Autonomous Truck Baseline Commands Reliability

Published figures diverge because firms pick different autonomy levels, exclude certain truck classes, or lock models to one currency snapshot. Buyers notice the spread.

Scope alignment, variable transparency, and our annual refresh cadence narrow that spread; others often bundle software platforms or retrofit kits, freeze exchange rates, or lift optimistic OEM press targets without cross-checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 39.51 B (2025) | Mordor Intelligence | - |

| USD 47.40 B (2025) | Global Consultancy A | Includes retrofit conversions and mining-only haulers |

| USD 267.38 B (2024) | Industry Journal B | Applies fleet asset value, not annual new-vehicle revenue |

The comparison shows how selective scope stretch or asset-value approaches inflate totals. Our disciplined variable set and live update loop give decision-makers a balanced, traceable baseline they can replicate with public data and modest resources.

Key Questions Answered in the Report

What is the projected value of the autonomous truck market by 2031?

The autonomous truck market size is forecast to reach USD 74.23 billion by 2031.

Which truck type is expected to grow fastest through 2031?

Medium-duty trucks are projected to post a 13.34% CAGR through 2031, the highest among truck types.

How will Level 4 autonomy impact fleet economics?

Level 4 trucks operate up to 22 hours per day, doubling asset utilization compared with human-driven vehicles constrained by hours-of-service rules.

Why are battery-electric trucks significant for autonomy?

Battery-electric drivetrains simplify control logic, qualify for zero-emission incentives, and pair well with autonomy to amortize sensor costs over high daily mileage.

Which region is expected to lead growth in autonomous trucking?

Asia-Pacific is forecasted to register a 13.33% CAGR to 2031, the fastest regional expansion rate.

Page last updated on: