Automotive USB Power Delivery System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.55 Billion |

| Market Size (2030) | USD 1.03 Billion |

| Growth Rate (2025 - 2030) | 13.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive USB Power Delivery System Market Analysis by Mordor Intelligence

The automotive USB power delivery system market size stands at USD 0.55 billion in 2025 and is forecasted to reach USD 1.03 billion by 2030, reflecting a 13.27% CAGR through 2030. The growth curve stems from parallel trends in cockpit digitization, wide-bandgap semiconductor use, and regulatory harmonization around USB-C ports. European regulations mandating USB-C across electronic devices, including automotive interfaces, drive OEM standardization to streamline production and avoid region-specific variants. This aligns with trends in digital cockpit integration, where consumer electronics are increasingly integrated into vehicle power and data systems. Advances in gallium nitride (GaN) and silicon carbide (SiC) power stages enable ultra-fast charging over 100 watts per port without compromising space or thermal efficiency. The competitive landscape remains open, with the top supplier holding a modest market share, offering opportunities for new entrants and scale-ups. However, supply constraints for SiC and GaN controllers pose short-term challenges, particularly for high-volume applications. Tier-one suppliers expect these issues to ease post-2026, enabling broader adoption and stronger supply chains in automotive electronics.

Key Report Takeaways

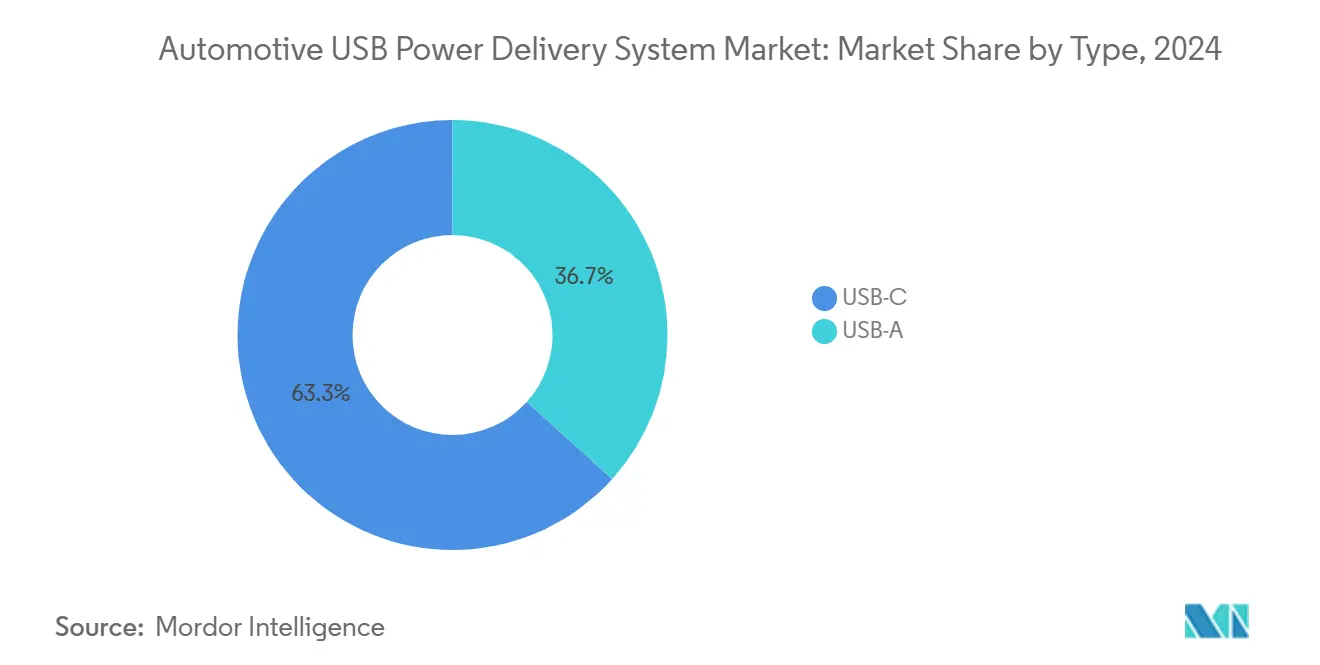

- By type, USB-C accounted for 63.32% of the Automotive USB Power Delivery System market share in 2024, and is projected to post the fastest CAGR of 19.11% to 2030 .

- By application, head units led with 49.53% revenue share of the automotive USB power delivery system market size in 2024; rear-seat chargers are projected to expand at a 15.57% CAGR through 2030.

- By vehicle type, passenger cars commanded 73.94% share of the automotive USB power delivery system market size in 2024, whereas medium and heavy commercial vehicles are forecasted to grow at 13.95% CAGR to 2030.

- By distribution channel, OEM installations held 84.77% of the automotive USB power delivery system market size in 2024; the aftermarket is expected to advance at a 15.07% CAGR over the forecast period.

- By geography, Europe maintained the largest regional position with a 35.75% share of the automotive USB power delivery system market size in 2024; Asia-Pacific is on track for the fastest regional CAGR of 14.38% through 2030.

Global Automotive USB Power Delivery System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Penetration and Cockpit Digitization | +1.2% | Global, with early gains in Europe, China, North America | Medium term (2-4 years) |

| USB-C As Common In-Vehicle Connector | +1.1% | Europe core, spill-over to North America & APAC | Short term (≤ 2 years) |

| Shift to GaN-Based PD Modules | +0.9% | Global, led by premium OEMs in Europe & North America | Medium term (2-4 years) |

| Fleet Electrification | +0.7% | North America & Europe commercial corridors | Long term (≥ 4 years) |

| Dynamic Port-Level Power-Throttling | +0.5% | APAC core, early adoption in premium segments | Long term (≥ 4 years) |

| In-Cabin Gaming/Streaming | +0.3% | Global urban markets, premium vehicle segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mainstream EV Penetration and Cockpit Digitization

EV adoption ushers in 48 V architectures that raise available bus power and streamline DC-DC conversion, enabling USB-C ports to reach 100 W and beyond[1]“Enable Automotive USB Power: Managing the Increasing Currents, Longer Cables, and Tight Portable-Device Specifications,” Analog Devices, analog.com. Digitized dashboards are reshaping the interior architecture of electric vehicles (EVs), leading to a surge in power and data ports in each car. While older models had only a handful of ports, modern EVs now boast a multitude of interfaces. These are essential for accommodating display-rich head units, rear-seat entertainment systems, and augmented-reality heads-up displays. Since these components require a continuous power supply, optimizing the power budget has become a paramount design focus for OEMs and suppliers. With diminishing concerns about EV range, consumers now prioritize seamlessly integrating their personal devices into vehicles. This shift underscores the strategic importance of suppliers capable of providing high-wattage charging solutions, especially those with integrated thermal management. Additionally, the increasing adoption of over-the-air firmware updates enriches this landscape. Manufacturers can adjust charging behaviors even after the vehicle's sale, enhancing user experience. This boosts user satisfaction and paves the way for recurring software revenue streams, supplementing traditional hardware profits.

EU Mandate for USB-C as Common In-Vehicle Connector

Brussels’ directive removes connector fragmentation by stipulating USB-C for handheld electronics, thus compelling automakers to migrate vehicle ports to the same format[2]“Commission welcomes agreement on common charger,” European Commission, ec.europa.eu. The EU's USB-C standardization mandate transforms automotive supply chains and product strategies. By consolidating SKUs, suppliers achieve economies of scale, reduce costs, and streamline production. OEMs are expediting design updates to meet compliance deadlines and maintain market access. Suppliers are shifting to USB-C-only production lines, improving efficiency and capacity. While North American and Asian regulators have not enforced similar mandates, OEMs are standardizing electrical platforms to avoid regional variations. This drives global demand for USB-C components and positions compliant suppliers to benefit from the shift toward standardized connectivity.

Tier-1/OEM Shift to GaN-Based High-Watt PD Modules

Gallium nitride (GaN) is revolutionizing automotive power electronics, delivering unmatched efficiency and compactness. Its rapid switching capability minimizes energy loss and enables smaller supporting components, a boon for space-limited vehicle cabins. Designed to endure extreme heat, automotive-grade GaN controllers are ideal for sun-exposed settings. Suppliers embracing GaN technology can drastically shrink power module sizes, creating room on dashboards for advanced features like occupant sensing and lidar. Top semiconductor roadmaps now integrate dense power architectures with thermal safeguards, simplifying safety certification. With rising production scales, GaN's cost benefits are becoming more pronounced, appealing to automakers who prioritize efficiency and integration.

Fleet Electrification Raising Multi-Port Fast-Charge Demand

Commercial vans and heavy trucks double as mobile offices, requiring simultaneous laptop, tablet, and handheld charging at 65 W-plus per port during long hauls. Fleet managers stipulate ruggedized connectors and extended thermal cycling beyond passenger-car norms. Multi-port USB-C hubs route dynamic power budgets, prioritizing mission-critical devices such as electronic logging units over passenger electronics. Software-defined power allocation enables load balancing based on battery state of charge (SoC), improving uptime. Fleet telematics interfaces increasingly expose charging analytics, helping operators optimize port usage and schedule preventative maintenance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PD Controller Supply Crunch | -1.2% | Global, acute in APAC manufacturing hubs | Short term (≤ 2 years) |

| USB-PD Cyber-Intrusion | -0.8% | Global, heightened in connected vehicle markets | Medium term (2-4 years) |

| Tariff-Driven EMS Relocation | -0.5% | US-China trade corridors, EMS manufacturing | Short term (≤ 2 years) |

| Thermal Runaway Recalls | -0.2% | Global aftermarket, emerging markets focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short-Term PD Controller Supply Crunch (SiC/GaN)

Automakers are increasingly adopting wide-bandgap semiconductors, such as gallium nitride, despite production challenges stemming from complex manufacturing processes. Supply bottlenecks persist as facilities struggle to meet quality and volume demands. To address these issues, automakers are diversifying sourcing or relying on silicon-based alternatives for entry-level models while prioritizing premium lines for advanced components. Although new production capacities are underway, supply-demand imbalances will continue, influencing procurement and product strategies across the automotive sector.

USB-PD Cyber-Intrusion and Firmware-Level Attack Risk

USB Power Delivery negotiates voltage and current profiles via packetized data, creating an entry point for malware-loaded devices. Tests show malicious firmware can handshake with in-car ports, escalate privileges, and pivot into CAN bus gateways unless air-gapped or cryptographically authenticated[3]“Cybersecurity Best Practices for Modern Vehicles,” National Highway Traffic Safety Administration, nhtsa.gov. Hardening introduces a modest cost per port, an incremental cost that induces delays in entry-level trims. Automakers establish over-the-air patch pipelines but must manage homologation across 10-year service lives, straining software maintenance budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Regulatory Push Consolidates USB-C Leadership

USB-C captured 63.32% of the automotive USB power delivery system market share in 2024, dwarfing USB-A’s residual presence in legacy trims. The Automotive USB Power Delivery System market size for USB-C implementations is projected to grow at a 19.11% CAGR, buoyed by mandated standardization and its 240 W ceiling that accommodates laptops and gaming consoles. OEMs redesign wiring harnesses to move high-speed data lines farther from electromagnetic interference, optimizing signal integrity while keeping costs flat. For entry-level models, optional USB-A ports remain to serve older devices, yet deletion roadmaps target full phaseout by 2028. Unit economics favor single-connector platforms, and component suppliers reduce product lines, bolstering factory throughput and yield.

Adoption permeates premium segments first, where consumer expectation for laptop-class charging has moved from novelty to baseline. Infotainment architectures centralize high-bandwidth links over PCIe network backbones, with USB-C ports doubling as firmware update paths, eliminating separate diagnostic connectors. Wireless CarPlay and Android Auto shift some data off physical buses, yet high-wattage power remains localized to USB-C, sustaining silicon demand across controller, switch, and protection ICs. Legacy USB-A volumes gravitate to aftermarket retrofits, prolonging but not reversing decline trajectories.

By Application: Head Units Steady While Rear-Seat Chargers Accelerate

Head-unit USB clusters held 49.53% of the automotive USB power delivery system market in 2024, anchored by their role as primary infotainment and navigation gateways. Cost-sensitive models integrate two high-current ports for smartphone mirroring and podcast streaming, whereas luxury trims add dual 100 W-capable outlets for laptops. Market saturation limits incremental port additions, yet software-updatable power profiles create ancillary revenue as automakers upsell higher wattage via subscription.

Rear-seat charger installations grow at a 15.57% CAGR through 2030, the fastest within the application spectrum. Multi-row SUVs and premium sedans tout theater-class screens and fold-out worktables, demanding distributed power architecture. Supply-chain investments emphasize low-profile edge modules that mount flush in seatbacks without impeding cushion thickness. ISO working groups draft new seat-mount connector specifications, integrating power, Ethernet, and audio. This move underscores the rising importance of standardization and paves the way for increased attach-rate opportunities for PD controller suppliers. The pivot reflects a broader cabin reinvention that treats every passenger as a potential content creator, reinforcing the car as an extension of home and office.

By Vehicle Type: Passenger Cars Dominate, Fleets Propel Commercial Upside

Passenger cars accounted for 73.94% of the automotive USB power delivery system market share in 2024, owing to sheer production volumes and consumer appetite for device-friendly cabins. Feature roll-downs from high-end trims to mass-market segments accelerate port proliferation, evidenced by mid-tier crossovers shipping with four or more USB-C outlets as standard. Despite scale advantages, per-vehicle revenue growth moderates as module costs decline, shifting supplier focus to value-added firmware and analytics.

Medium and heavy commercial vehicles register the top CAGR at 13.95% through 2030, reflecting electrification mandates for urban delivery and growing driver welfare regulations. High-watt outlets power refrigeration monitors, inventory scanners, and electronic logging devices simultaneously. Ruggedization factors, vibration dampers, IP6X ingress protection, and surge suppression inflate ASPs relative to passenger equivalents. Fleet telematics systems now integrate power-consumption dashboards, enabling operators to detect failing ports pre-emptively, a service play that reinforces recurring revenue.

By Distribution Channel: OEM Integration Prevails, Aftermarket Surges

OEMs held 84.77% of the automotive USB power delivery system market share in 2024, leveraging factory integration to assure electromagnetic compatibility and warranty coverage. Design-for-assembly initiatives merge PD boards with wireless-charging coils, leaving only a decorative bezel visible to the occupant. Software lockouts tie port activation to paid digital packages, representing a nascent but lucrative income vertical for automakers. The aftermarket segment is projected to grow at a 15.07% CAGR, appealing to owners who retrofit legacy vehicles with 65–100 W capability.

Tool-free clip-in modules simplify DIY installation, and retailers bundle certified cables to sidestep thermal runaway concerns. Regulatory oversight intensifies; ports installed post-sale must meet the same functional safety metrics as factory units, raising the technical bar for aftermarket players yet validating premium positioning. Ecosystem expansion into recreational vehicles (RVs) and marine craft offers adjacent volume, further turbocharging channel momentum.

Geography Analysis

Europe retained the top position at 35.75% share of the automotive USB power delivery system market in 2024, underpinned by regulatory certainty and strong EV penetration. Germany’s premium marques bundle high-current USB-C ports across trim lines, shrinking optional-equipment lists and simplifying procurement. Subsidy frameworks that reward zero-emission sales indirectly lift demand by increasing EV output volumes, multiplying embedded port counts. Regional Tier-ones maintain local assembly for PD modules to meet just-in-time production schedules and circumvent tariff risks. Importantly, the European Automobile Manufacturers Association collaborates on cross-OEM interoperability tests, ensuring cable safety and performance uniformity across brands.

Asia-Pacific is the growth engine, charting a 14.38% CAGR through 2030. China ships more EVs than the rest of the world, embedding at least four USB-C ports per mass-market compact sedan. Government incentives for new energy vehicles dovetail with domestic semiconductor ambitions, catalyzing joint ventures focused on GaN PD controllers. India joins the ascent as component giants commit to greenfield fabs, leveraging cost arbitrage to supply global lines. South Korea and Japan contribute advanced ceramic capacitors and thermal interface materials, completing the regional value chain and accelerating time-to-market cycles.

North America posts a healthy CAGR, driven by electrified pickup trucks and fleet delivery vans that prioritize high-duty-cycle charging solutions. Federal cybersecurity guidelines compel the adoption of secure firmware, lifting controller ASPs. Supply-chain diversification from Chinese assembly to Mexican and United States facilities mitigates geopolitical risk but introduces near-term cost headwinds. Consumer behavior also leans toward power-hungry devices; average connected horsepower, Watts consumed per occupant, outpaced global averages and setting a lucrative stage for premium PD modules.

Competitive Landscape

The automotive USB power delivery system market exhibits moderate fragmentation, yielding a concentration score indicative of competitive headroom. Front-runners pursue vertical integration, coupling GaN transistor design, silicon interposers, and firmware stacks to shorten qualification cycles and secure lifetime design-in royalties. Patent filings increasingly cluster around adaptive power negotiation and cable-authentication schemes, forming intangible moats.

Strategic partnerships are underscoring the drive for innovation. A European semiconductor giant partnered with a luxury carmaker to roll out high-power GaN modules and craft thermal modeling tools aimed at dashboard optimization jointly. Meanwhile, a fabless company from the United States unveiled an AI-powered controller, designed to smartly redistribute power, thereby slashing charging times across several devices. An Asian tier-one supplier has seamlessly integrated USB PD with Qi wireless charging on a sleek mezzanine board, leading to a notable decrease in wiring weight and complexity.

Supply-chain resilience takes center stage; leading players secure multi-source wafer agreements across Europe and Southeast Asia to mitigate geopolitical disruption. Collaboration with cable-assembly firms extends product lifecycle coverage, offering end-to-end warranties that bundle port electronics and certified cables. The resulting ecosystem approach shifts procurement discussions from per-unit costs toward total installed-system value, raising switching barriers and locking in annuity-like revenue structures.

Automotive USB Power Delivery System Industry Leaders

STMicroelectronics

Infineon Technologies AG

Texas Instruments Inc.

NXP Semiconductors N.V.

Renesas Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: As Apple unveiled its iPhone 17 series, LISEN rolled out its Retractable Cable Car Charger Series, tailored specifically for the new lineup. These chargers, crafted to integrate effortlessly into contemporary car interiors, boast a retractable cable that ensures tidy storage and easy accessibility. Capable of charging up to four devices at once, ranging from smartphones and tablets to headphones, the series promises swift and dependable power, catering to road trips, family outings, and urgent charging demands.

- December 2024: Renesas Electronics Corporation unveiled the RAA489118 buck-boost battery charger and the RAA489400 USB Type-C® port controller. Together, these two integrated circuits (ICs) deliver a top-tier Extended Power Range (EPR) USB Power Delivery (PD) solution.

Global Automotive USB Power Delivery System Market Report Scope

| USB-A |

| USB-C |

| Head Units |

| Rear-Seat Entertainment Systems |

| Rear-Seat Chargers |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| OEM (Original Equipment Manufacturer) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | USB-A | |

| USB-C | ||

| By Application | Head Units | |

| Rear-Seat Entertainment Systems | ||

| Rear-Seat Chargers | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Distribution Channel | OEM (Original Equipment Manufacturer) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR does the Automotive USB Power Delivery System market expect between 2025 and 2030?

The market is projected to expand at a 13.27% CAGR, moving from USD 0.55 billion in 2025 to USD 1.03 billion by 2030.

Which connector type leads current adoption in vehicles?

USB-C dominates with 63.32% share in 2024 and is on track for 19.11% CAGR, driven by regulatory mandates and high-wattage capabilities.

Why is Europe the largest regional market?

Europe holds 35.75% share owing to the EU’s USB-C regulation, high EV density, and premium OEM focus on digital cockpits.

Where is the fastest growth regionally?

Asia-Pacific registers the strongest outlook at 14.38% CAGR due to China’s EV scale and India’s emerging component manufacturing base.

Which application segment is growing quickest through 2030?

Rear-seat chargers lead in growth at 15.57% CAGR as automakers transform cabins into entertainment and productivity hubs.

What supply-chain risk currently restrains market expansion?

Limited SiC and GaN wafer capacity inflates PD controller lead times to as much as 52 weeks, dampening near-term volume expansion.

Page last updated on: