Automotive Dc-Dc Converter Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

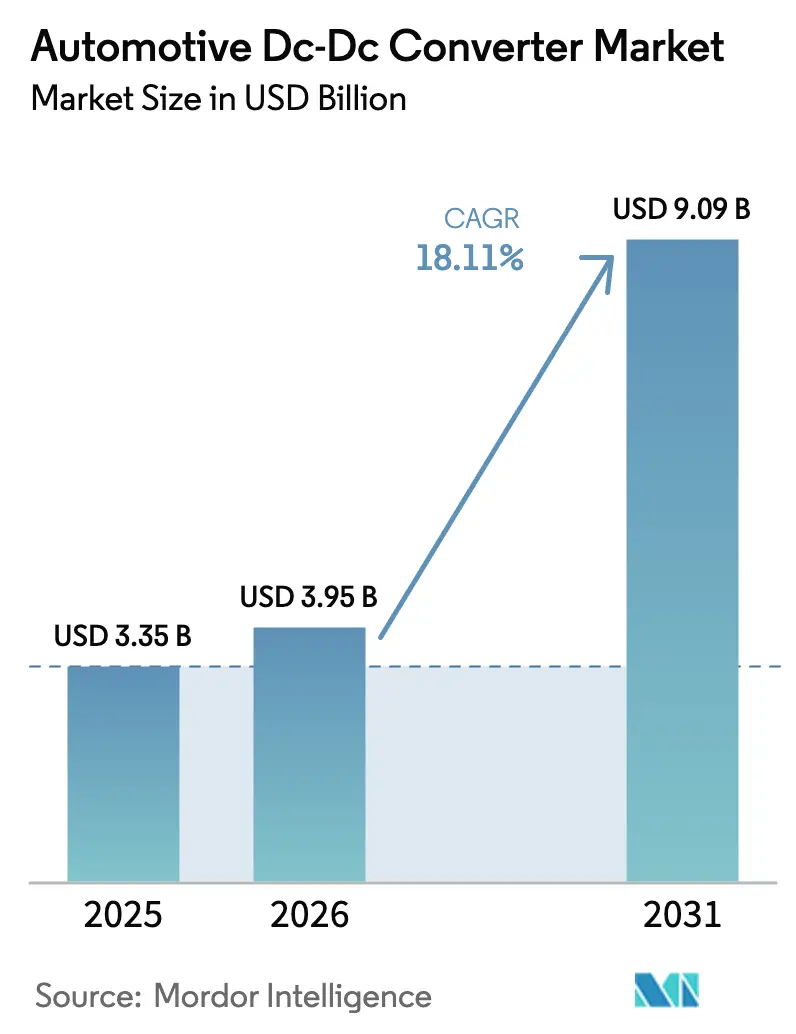

| Market Size (2026) | USD 3.95 Billion |

| Market Size (2031) | USD 9.09 Billion |

| Growth Rate (2026 - 2031) | 18.11% CAGR |

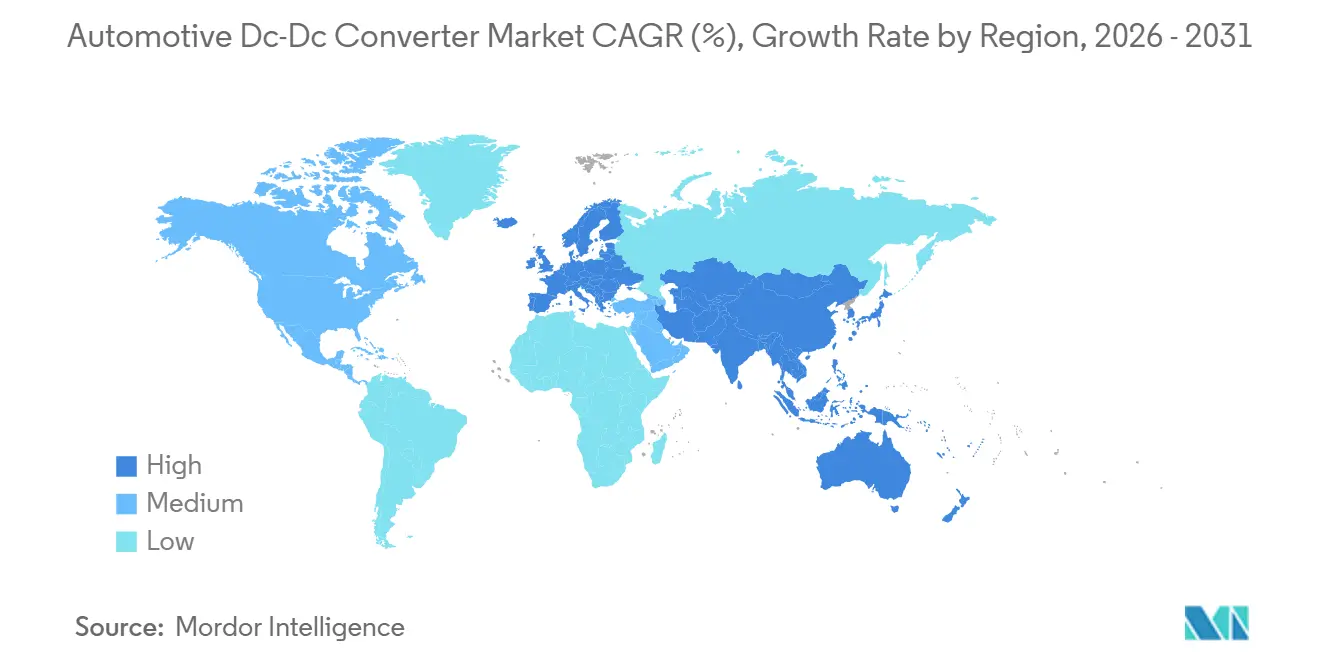

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

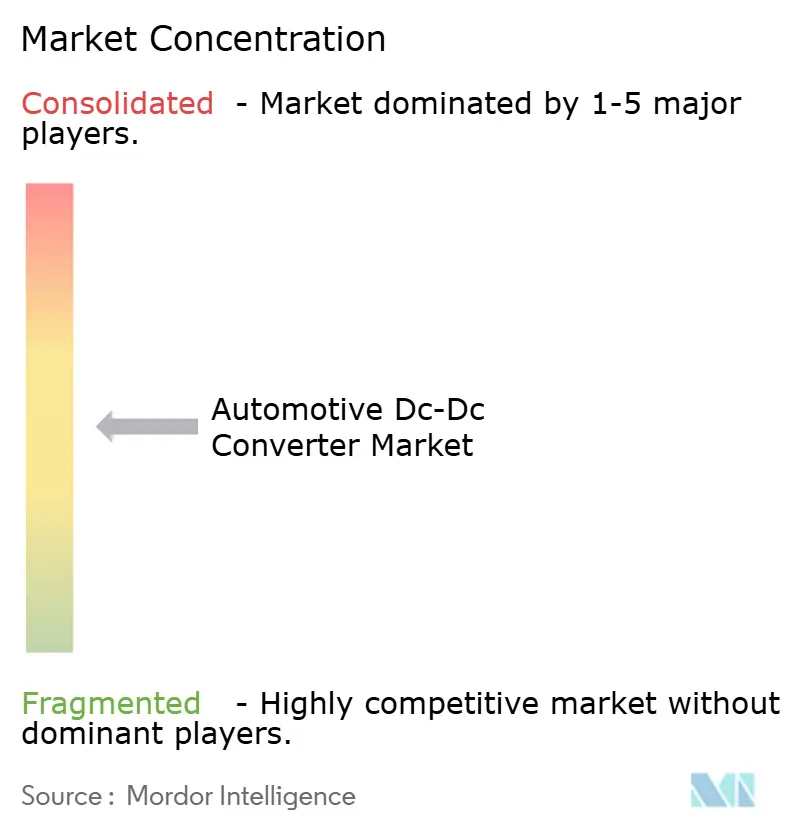

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Dc-Dc Converter Market Analysis by Mordor Intelligence

The Automotive DC-DC Converter Market size is expected to grow from USD 3.35 billion in 2025 to USD 3.95 billion in 2026 and is forecast to reach USD 9.09 billion by 2031 at 18.11% CAGR over 2026-2031. Three key factors underpin the upward trend: the increasing production of battery-electric vehicles (BEVs), regulatory mandates requiring 48-volt mild-hybrid systems on internal combustion platforms, and a significant decline in silicon-carbide (SiC) device prices for automotive-grade modules. These developments expand the market for high-voltage-to-low-voltage converters, leading to a notable increase in average content per vehicle over the forecast period. While demand is currently centered in the Asia Pacific, Europe is poised to lead, driven by Euro 7 real-driving-emission regulations and the phase-out of internal combustion engines, pushing OEMs to electrify even their entry-level models. Converter architectures are shifting: although isolated designs remain prevalent, bi-directional topologies essential for vehicle-to-load (V2L) and vehicle-to-grid (V2G) services are rapidly gaining traction, hinting at new revenue opportunities beyond just propulsion. Moreover, tier-one module manufacturers are forging closer partnerships with semiconductor firms, recognizing that firmware optimization around SiC switching has become a key competitive edge.

Key Report Takeaways

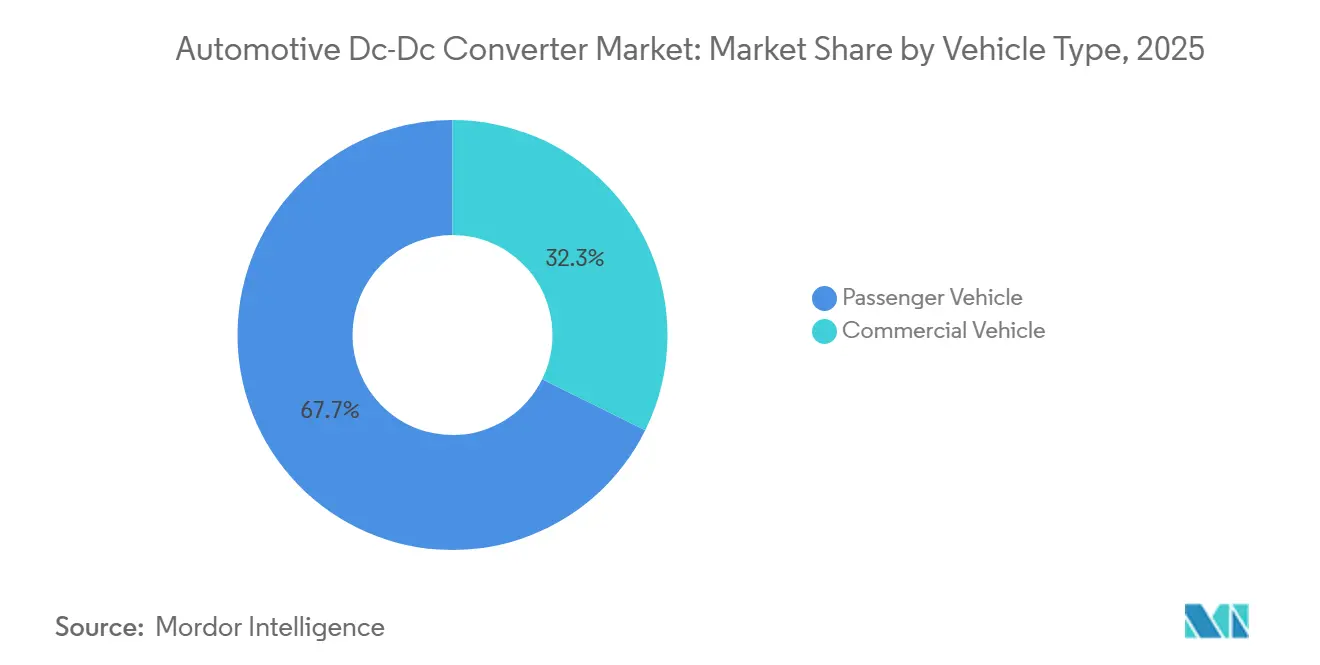

- By vehicle type, passenger cars accounted for 67.71% of 2025 revenue, whereas commercial vehicles are expected to expand at an 18.13% CAGR through 2031.

- By propulsion, BEVs accounted for 77.14% of 2025 sales, yet 48-volt mild-hybrids are projected to record the highest growth rate at 18.21% CAGR to 2031.

- By product type, isolated converters held 52.44% of the auto DC-DC converter market share in 2025, while bi-directional designs are forecast to post the fastest growth at 18.24% CAGR through 2031.

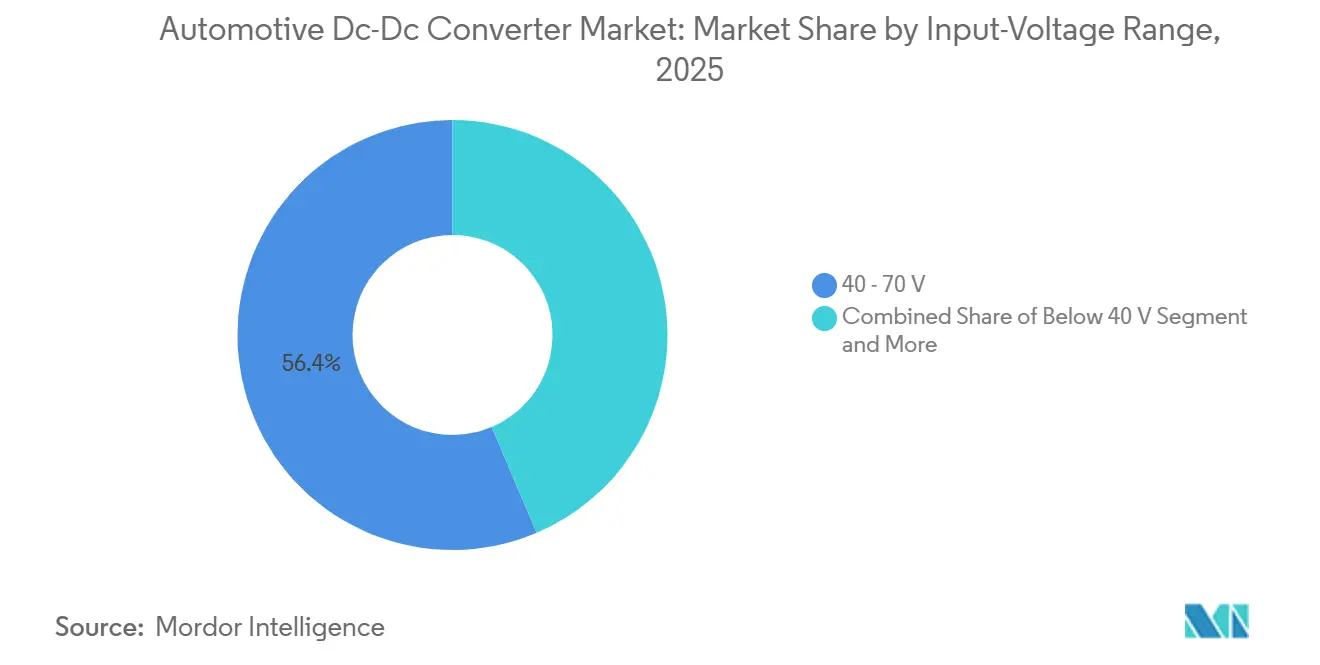

- By input-voltage band, the 40-70-volt segment captured 56.43% of 2025 revenue; converters serving above-70-volt traction batteries should lead gains with an 18.27% CAGR.

- By output power class, sub-3 kW modules accounted for 48.81% of shipments in 2025, while the 3-6 kW range is on track for an 18.15% CAGR through 2031.

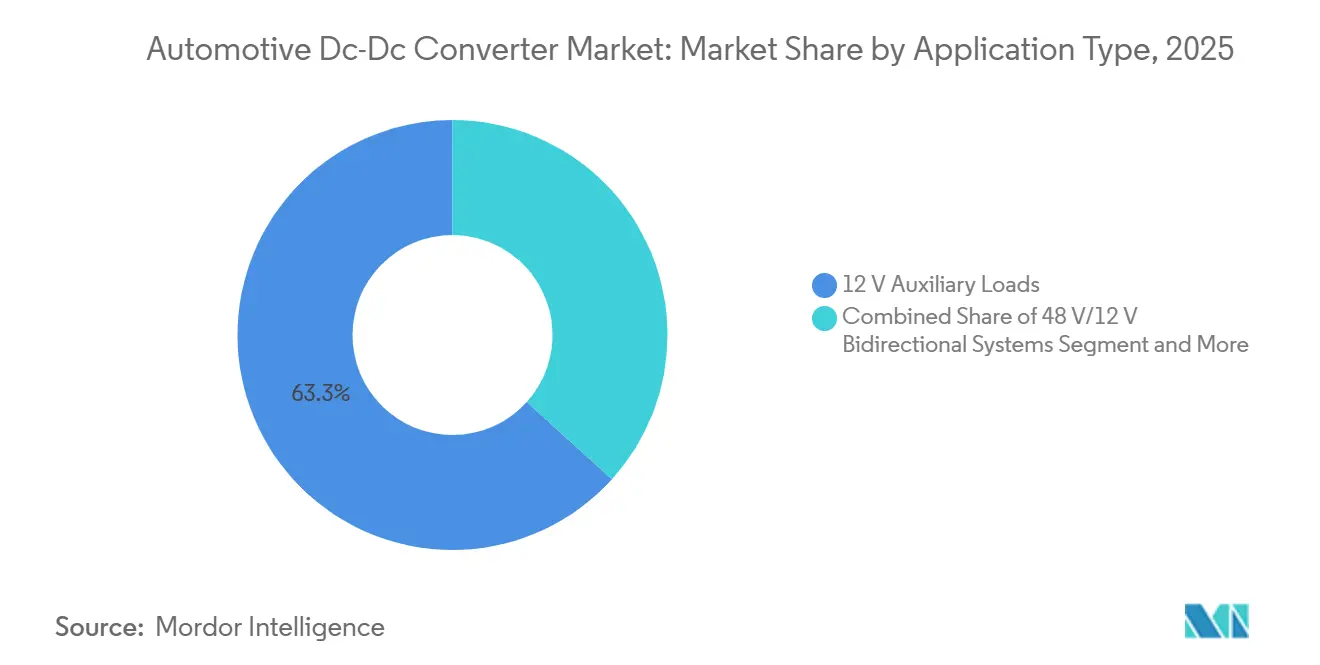

- By application, 12-volt auxiliary loads captured 63.31% of 2025 revenue, while 48V/12V bi-directional systems are projected to expand at an 18.33% CAGR through 2031.

- By end-user, OEM factory-fit installations accounted for 81.27% of 2025 revenue, whereas aftermarket retrofit converters are expected to record an 18.35% CAGR through 2031.

- By geography, Asia Pacific accounted for 44.53% of 2025 sales, but Europe is projected to register the fastest regional expansion at an 18.18% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Dc-Dc Converter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging BEV and PHEV Production | +4.2% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Global 48V Mild-Hybrid Mandates | +3.8% | Europe core, expanding to China and India | Short term (≤2 years) |

| Lower SiC/GaN Device Costs | +2.9% | Global, led by Asia Pacific manufacturing hubs | Medium term (2-4 years) |

| Shift to Zonal E/E Architectures | +2.5% | North America and Europe premium segments, spill-over to Asia Pacific | Long term (≥4 years) |

| Vehicle-to-Load (V2L) Functionality | +2.1% | Japan, South Korea, California; early adoption in Santiago, Valparaíso | Medium term (2-4 years) |

| On-Board E-Power (ePTO) Demand in Commercial EVs | +1.8% | North America, Europe commercial fleets; pilot programs in Brazil | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging BEV and PHEV Production

In 2025, global output of battery electric vehicles (BEVs) and plug-in hybrids experienced significant growth, driven by China's extension of purchase-tax exemptions and the EU's implementation of stricter fleet CO₂ limits [1]“Notice on NEV Purchase-Tax Exemption Extension,” Ministry of Industry and Information Technology, miit.gov.cn . Each BEV requires multiple converters, resulting in a substantial annual demand for these modules. Tesla's Cybertruck and the refreshed Model 3 highlight the use of bi-directional units with advanced capabilities, such as powering V2L camping modes. Hyundai and Ford are now standardizing this feature to enhance their brand differentiation. Plug-in hybrid electric vehicles (PHEVs), which still rely on a 12 V starter circuit, include an isolated step-down converter. This addition increases the electronics content per vehicle. Suppliers are rapidly localizing their operations; for example, Bosch inaugurated a large-scale plant in Chengdu in early 2025, with plans to achieve significant production capacity within a few years [2]“Chengdu Power-Electronics Plant Press Release,” Robert Bosch GmbH, bosch.com .

Global 48 V Mild-Hybrid Mandates

Starting early 2025, Euro 7 regulations mandate that mainstream vehicle models incorporate electrified turbochargers and electrically heated catalysts, both powered by low-voltage rails. Similarly, China's draft CAFC credits offer comparable incentives, and India's FAME III scheme provides rewards for low-voltage systems that achieve significant reductions in fuel consumption. Consequently, models like the Volkswagen Golf, Peugeot 308, and Maruti Suzuki Brezza are now equipped with belt-integrated starter-generators and low-voltage converters. Japan has set an ambitious fleet fuel-economy target for the near future, pushing both Toyota and Honda to adopt mild-hybrid technologies. However, meeting these standards isn't easy; UNECE's ASIL-C compliance requirement adds considerable development time and significant non-recurring engineering costs.

Lower SiC/GaN Device Costs

In early 2025, prices for automotive-qualified 1,200 V SiC MOSFETs declined significantly. This price reduction followed the increased production of larger wafers by industry leaders Infineon, Wolfspeed, and onsemi. As a result, designers were able to substantially increase the switching frequency and achieve a notable reduction in inductor volume. While GaN components remain more expensive, they offer lower switching losses, making them an appealing choice for OEMs exploring bi-directional designs. Texas Instruments reported a substantial increase in automotive GaN revenue, attributing the success to partnerships with major automotive manufacturers. However, as reliability standards become more stringent, updated AEC-Q101 tests now require extended stress testing. By the end of 2025, only Infineon and onsemi had publicly met these rigorous requirements[3]“AEC-Q101 Rev H,” Automotive Electronics Council, aecq.org .

Shift to Zonal E/E Architectures

By transitioning from domain to zonal wiring, automakers have achieved a significant reduction in harness mass and simplified over-the-air updates. GM's Ultium platform employs multiple regional controllers, each powered by isolated converters that step down high voltage to a lower voltage. Stellantis plans to adopt a similar configuration for its future models, integrating Ethernet switching within the converters. Given that these converters control power to safety-critical actuators, they've incorporated a secure-boot chip per unit to comply with ISO 21434 cybersecurity standards. Aptiv's securing of substantial orders for upcoming years underscores OEMs' commitment to these zonal advancements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal-Management Limits on Power Density | -2.3% | Global, acute in high-ambient-temperature regions (Middle East, India) | Short term (≤2 years) |

| Automotive-Grade Passive-Component Shortages | -1.9% | Global supply chain, bottlenecks in Japan and Taiwan MLCC production | Short term (≤2 years) |

| Cyber-Security Homologation Overheads | -1.2% | Europe (UN R155/R156), North America (SAE J3061), China (GB standards) | Medium term (2-4 years) |

| Electromagnetic-Interference (EMI) Compliance at 400 kHz | -1.1% | Global, stricter enforcement in EU (CISPR 25) and Japan (VCCI) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Thermal-Management Limits on Power Density

In hot climates, elevated temperatures can shorten capacitor life and necessitate derating. While liquid-cooled cold plates effectively address this issue, they add significant weight and unit cost. In compact passenger cars, packaging constraints hinder the adoption of high-power converters, causing delays in some bidirectional V2G programs. Suppliers are innovating with planar magnetics and gap-optimized ferrites to reduce loss density, yet mass production is still some time away. This challenge is particularly pronounced in taxis across the Middle East and in fleet cars in India, which often idle with the air conditioner running for extended periods.

Automotive-Grade Passive-Component Shortages

In 2025, a significant fire at a major fab in Taiwan once again tightened the supply of multi-layer ceramic capacitors (MLCCs). This incident significantly extended lead times for high-temperature parts. The shortage of these capacitors has delayed new converter launches by several months, limiting OEMs' ability to refresh trims. While Denso and Panasonic have secured stockpiling agreements, smaller module manufacturers are grappling with allocation caps, hindering their revenue. Design teams are pivoting to film capacitors, but this shift results in a notable increase in board space and costs. Industry experts caution that relief from these challenges isn't expected for a few years, as new MLCC production lines take considerable time to meet AEC-Q200 qualifications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Accelerate Electrification

Passenger cars accounted for 67.71% of 2025 revenue. The automotive DC-DC converter market size for commercial vehicles is projected to advance at an 18.13% CAGR as regulators cut heavy-duty CO₂ limits and fleet operators monetize vehicle-to-depot energy resale. In Europe, the eActros 600 fields a 9 kW converter that supports grid export, recovering around EUR 1,200 per truck each year.

Passenger cars keep the volume edge but must raise power capability. ADAS compute loads of 1.5 kW, electric heat pumps, and audio amplifiers stretch legacy 12 V rails. Consequently, OEMs fit 3 kW step-downs so that accessory power no longer drags the main battery range. The auto DC-DC converter market, therefore, balances mass-production cost targets with higher peak ratings, an area where hybrid ferrite cores and SiC switches help module suppliers stay below the USD 150 price ceiling in B-segment cars.

By Propulsion Type: Mild-Hybrids Gain Traction

BEVs seized 77.14% of 2025 converter revenue, but mild hybrids show faster expansion. Their 48 V battery boosts fuel economy by a minimal amount yet requires a 48 V/12 V bidirectional bridge, raising the converter bill of materials to USD 180. The 48-volt mild-hybrid auto DC-DC converter is expected to grow at a 18.21% CAGR by 2031.

PHEVs and fuel-cell vehicles add isolated converters for galvanic safety, so per-car content tops USD 300. Even so, OEMs favor mild-hybrids for quick regulatory compliance without re-architecting the chassis harness. That keeps the auto DC-DC converter market share of the 48 V segment solid through 2031, preserving high unit volumes for silicon MOSFET-based designs.

By Product Type: Bi-Directional Topologies Emerge

Isolated converters owned 52.44% of 2025 sales due to ISO 6469-3 galvanic rules. Yet bi-directional units are scaling at 18.24% CAGR as household-grade 230 V export becomes a brand differentiator. The auto DC-DC converter market size tied to these reversible modules already passes USD 1 billion.

Non-isolated buck-boost designs keep cost down for 48 V mild-hybrids, but traction-battery markets demand isolated dual-active-bridge circuits hitting 96% peak efficiency. Suppliers bundle IEEE 1547 grid-sync firmware so that future V2G tariffs can be converted into accessory revenue. That ecosystem shift is why the auto DC-DC converter market is tilting toward adaptive digital controllers and secure-boot microcode to handle both propulsion and energy services.

By Input-Voltage Range: 800-V Platforms Gain Share

The 40-70 V band accounted for 56.43% of 2025 turnover because it aligns with the 48 V pack standard in mild-hybrids. Above 70 V converters spanning 400 V and 800 V batteries will grow at a 18.27% CAGR as Porsche, Hyundai, and Lucid legitimize 800 V fast charging. That raises the auto DC-DC converter market share for SiC-based 1,200 V devices year after year.

High-voltage designs face harsher transient and thermal hurdles. Load-dump events can spike to 1,000 V, and heat rejection becomes a bottleneck. Liquid-cooled cold plates add mass and cost but are unavoidable in tight engine bays. Even with those penalties, the efficiency gain shortens charging time, a metric that marketing departments now prominently broadcast to boost EV uptake.

By Output-Power Rating: Mid-Range Demand Surges

Sub-3 kW modules accounted for 48.81% of shipments in 2025, as legacy 12 V lighting and body electronics remain. Yet the 3-6 kW bracket will post an 18.15% CAGR. By the end of the forecast period, the auto DC-DC converter market is expected to grow significantly, driven primarily by increasing demand from heat pumps and ADAS compute blades.

Converters designed for higher-power applications serve refrigeration and hydraulic e-PTOs in trucks. Although this segment represents a smaller share of the market, it commands premium pricing due to features such as ruggedized housings and extended temperature ratings. To support this growth, suppliers are implementing advanced designs, such as interleaved multiphase layouts, to efficiently manage thermal stress across components.

By Application: Bi-Directional Systems Gain Momentum

Auxiliary 12 V loads still accounted for 63.31% of 2025 revenue, but 48 V/12 V bidirectional systems will expand at a 18.33% CAGR. Reversible bridges in the auto DC-DC converter market are gaining traction. These bridges enable a 48 V lithium pack to recharge a 12 V battery, reducing pack capacity needs and resulting in significant cost savings per vehicle.

While high-voltage traction support converters, designed for performance BEVs, represent a small portion of total shipments, they are increasingly being adopted. As digital-cockpit screens and hands-off driver-assist technologies debut, thermal-management modules, ADAS rails, and infotainment systems are experiencing significant demand.

By End-User: OEM Dominance Persists

OEM installations accounted for 81.27% of 2025 revenue, whereas aftermarket retrofit converters are projected to grow at an 18.35% CAGR through 2031. The auto DC-DC converter market in aftermarket channels remains far smaller due to the certification cost per SKU. OEMs co-locate their design teams with suppliers, shrinking assembly time and cutting warranty risk.

In contrast, retrofit specialists serve hobbyists remaking classic cars. Custom 3 kW isolated units cost USD 900, yet miss out on the economies of automated winding. Regulatory exemptions expire in 2028, meaning those players must soon adopt the same EMC paperwork that burdens high-volume OEM units.

Geography Analysis

Asia Pacific generated 44.53% of 2025 revenue, driven by strong NEV sales in China. Converter factories in the region are strategically located near battery and SiC wafer lines. This proximity allows suppliers, such as BYD Semiconductor and Delta Electronics, to maintain competitive per-unit costs. Japan, which holds a substantial share of the global 48 V bidirectional capacity, sees Denso and Panasonic harnessing decades of hybrid expertise to achieve high mean time between failures.

Europe will advance fastest, with an 18.18% CAGR, driven by Euro 7, stringent efficiency mandates under the Ecodesign Directive, and the impending combustion ban. Major players like Bosch, Valeo, and Infineon are amplifying their SiC vertical integration to remain competitive, all while adhering to strict standby-power limits. Meanwhile, automotive giants Porsche, Hyundai, and Kia have debuted advanced passenger cars from exclusive European lines, benefiting module suppliers who swiftly qualified cutting-edge SiC MOSFETs.

North America captured a notable share of the 2025 revenue. The Inflation Reduction Act ties consumer tax credits to a stipulation of domestic content. In response, BorgWarner and Magna are establishing converter plants in Auburn Hills and Ontario, targeting significant production volumes in the coming years. While South America and the Middle East lag with modest shares, both regions are witnessing robust growth rates. This surge is attributed to local assembly incentives, although the intense heat in the Gulf necessitates liquid-cooled designs, increasing the BOM cost per unit.

Competitive Landscape

Market concentration remains moderate. The top five vendors—Bosch, Denso, Valeo, Continental, and Infineon—accounted for a significant share of the 2025 revenue, leaving ample opportunity for specialists. Bosch's partial stake in SiCrystal ensures a steady supply of SiC wafers, potentially reducing device costs in the coming years. Denso collaborates with onsemi to enhance efficiency through adaptive dead-time control firmware, while Continental integrates RESTful APIs, enabling OEMs to remotely update converter parameters.

Vicor leverages its factorized architecture to deliver highly efficient 800 V-to-48 V modules to clients such as Lucid and Rivian. Meanwhile, Chinese competitors Delta and Huawei Digital Power offer bidirectional units at a notable price discount, prompting established players to enhance their offerings with grid-sync firmware and cybersecurity features. Patent filings reveal the next competitive battleground: Infineon's adaptive multi-phase control significantly reduces switching loss, and Denso's liquid-cooled housing substantially lowers thermal resistance, signaling a shift in focus from silicon costs to packaging innovations.

OEMs are increasingly overlapping with traditional tiers; for instance, General Motors and Hyundai now include control-loop source code in their bill of materials. This shift necessitates semiconductor firms to adapt to automotive software life-cycle demands. Consequently, this creates a tighter feedback loop, accelerating design cycles but also tightening margins for module assemblers without firmware intellectual property.

Automotive Dc-Dc Converter Industry Leaders

Robert Bosch GmbH

Denso Corporation

Valeo Group

Continental AG

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Eaton has announced its agreement to acquire Resilient Power Systems Inc., a move aimed at integrating Resilient Power Systems' solid-state transformer technology into high-power automotive DC applications. This acquisition is expected to enhance Eaton's capabilities in addressing the growing demand for advanced power management solutions in the automotive sector.

- April 2025: Navitas has announced that its high-power GaNSafe™ ICs have received automotive qualification. These high-power GaNSafe ICs are now primed for production in electric vehicles (EVs), offering unmatched power density and efficiency, particularly for on-board chargers (OBCs) and HV-LV DC-DC converter applications.

- January 2025: Forvia HELLA has selected Infineon's CoolSiC Automotive MOSFET 1200 V for its upcoming 800 V DC-DC charging solution, aiming to enhance efficiency and performance in next-generation electric vehicle charging systems.

Global Automotive Dc-Dc Converter Market Report Scope

The scope of the report includes Vehicle Type, Propulsion (BEV, PHEV, and More), Product Type (Isolated and More), Input Voltage, Output Power, Application (12V Auxiliary and More), End-User (OEM and Aftermarket), and Geography.

| Passenger Vehicle |

| Commercial Vehicle |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid EV (PHEV) |

| Fuel-Cell EV (FCEV) |

| Mild-Hybrid (48 V MHEV) |

| Isolated Converter |

| Non-Isolated Converter |

| Bi-directional Converter |

| Below 40 V |

| 40 - 70 V |

| Above 70 V |

| Below 3 kW |

| 3 - 6 kW |

| Above 6 kW |

| 12 V Auxiliary Loads |

| 48 V/12 V Bidirectional Systems |

| High-Voltage Traction Support |

| ADAS and Infotainment Power |

| Thermal-Management Systems |

| OEM Factory-Fit |

| Aftermarket Retrofit |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Vehicle | |

| Commercial Vehicle | ||

| By Propulsion Type | Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid EV (PHEV) | ||

| Fuel-Cell EV (FCEV) | ||

| Mild-Hybrid (48 V MHEV) | ||

| By Product Type | Isolated Converter | |

| Non-Isolated Converter | ||

| Bi-directional Converter | ||

| By Input-Voltage Range | Below 40 V | |

| 40 - 70 V | ||

| Above 70 V | ||

| By Output-Power Rating | Below 3 kW | |

| 3 - 6 kW | ||

| Above 6 kW | ||

| By Application | 12 V Auxiliary Loads | |

| 48 V/12 V Bidirectional Systems | ||

| High-Voltage Traction Support | ||

| ADAS and Infotainment Power | ||

| Thermal-Management Systems | ||

| By End-User | OEM Factory-Fit | |

| Aftermarket Retrofit | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the auto DC-DC converter market in 2031?

It is forecast to reach USD 9.09 billion by 2031 on an 18.11% CAGR over 2026-2031.

Which region will grow the fastest through 2031?

Europe is expected to record an 18.18% CAGR as Euro 7 rules, and the 2035 combustion ban accelerates electrification.

Why are bi-directional converters gaining traction?

They enable vehicle-to-load and vehicle-to-grid services, opening revenue streams beyond propulsion and growing at 18.24% CAGR.

How does 48 V mild-hybrid adoption impact converter demand?

Every mild-hybrid needs a 48 V/12 V bridge, pushing mild-hybrid converter sales to an 18.33% CAGR through 2031.

Which power rating segment will expand most quickly?

The 3-6 kW band will grow at 18.15% CAGR as EVs adopt heat pumps and high-power ADAS computers.

Who are the market leaders currently?

Bosch, Denso, Valeo, Continental, and Infineon together hold about more than half of global revenue, yet specialists such as Vicor and Delta are advancing in high-efficiency niches.

Page last updated on: