Automotive Power Electronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

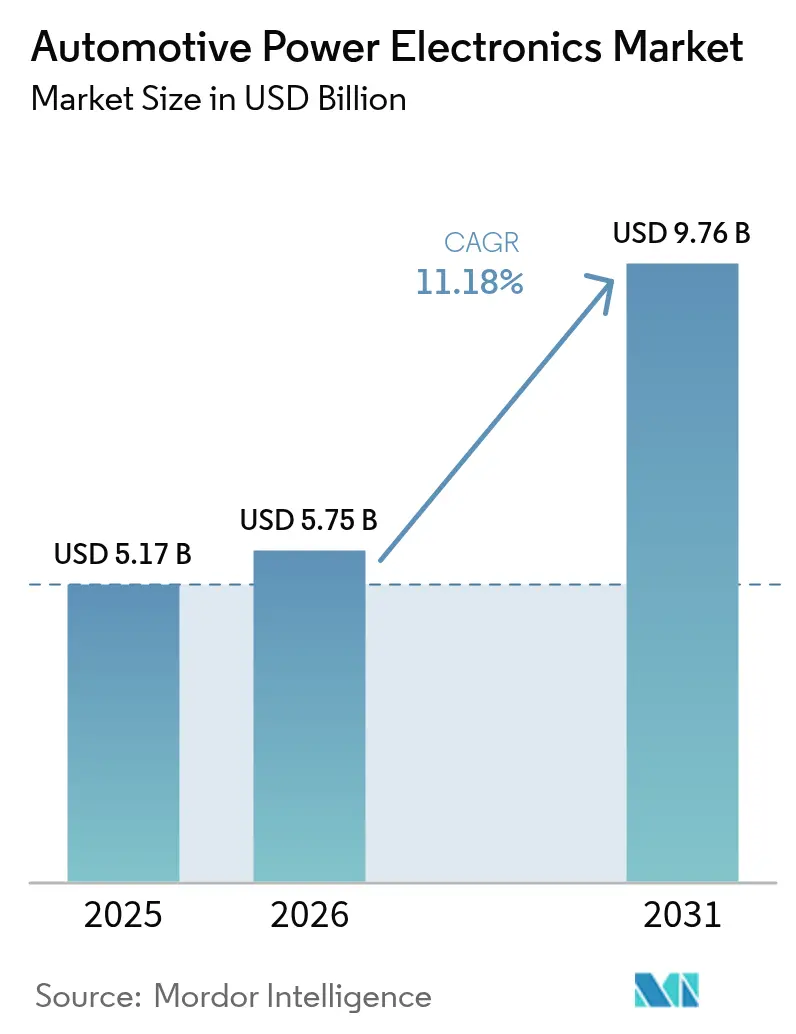

| Market Size (2026) | USD 5.75 Billion |

| Market Size (2031) | USD 9.76 Billion |

| Growth Rate (2026 - 2031) | 11.18% CAGR |

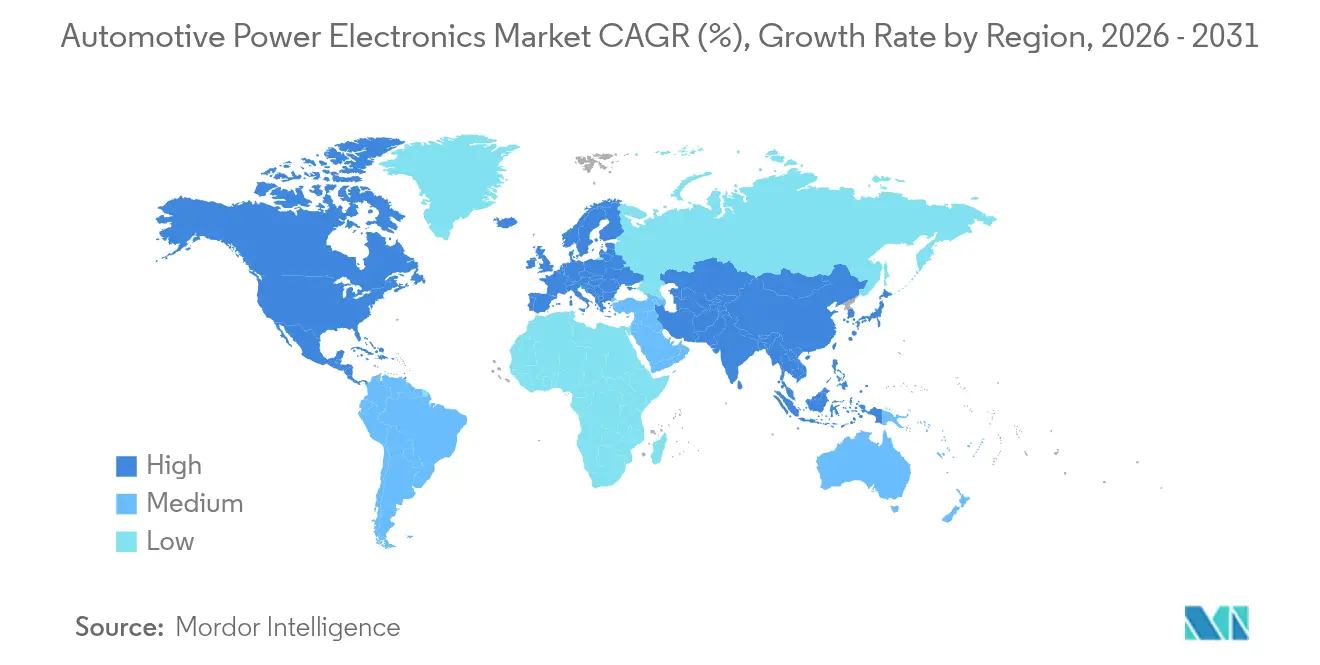

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Power Electronics Market Analysis by Mordor Intelligence

The automotive power electronics market size is projected to expand from USD 5.17 billion in 2025 and USD 5.75 billion in 2026 to USD 9.76 billion by 2031, registering an 11.18% CAGR between 2026 and 2031. Rapid electrification, driven by policy mandates and consumer demand for lower charging times, is pushing original-equipment manufacturers (OEMs) toward 800-volt architectures that require silicon-carbide and gallium-nitride devices. Tier-1 suppliers are racing to secure design wins in traction inverters and on-board chargers as passenger-car platforms migrate from 400-volt systems, while bidirectional charging capabilities are opening new revenue models such as vehicle-to-grid services. Regional policy signals, including China’s dual-credit system and the Inflation Reduction Act in the United States, are accelerating local semiconductor investment, allowing OEMs to shorten supply chains and qualify for incentives. The resulting demand for high-efficiency power modules outstrips wafer capacity, making substrate expansion a strategic imperative across the supply base.

Key Report Takeaways

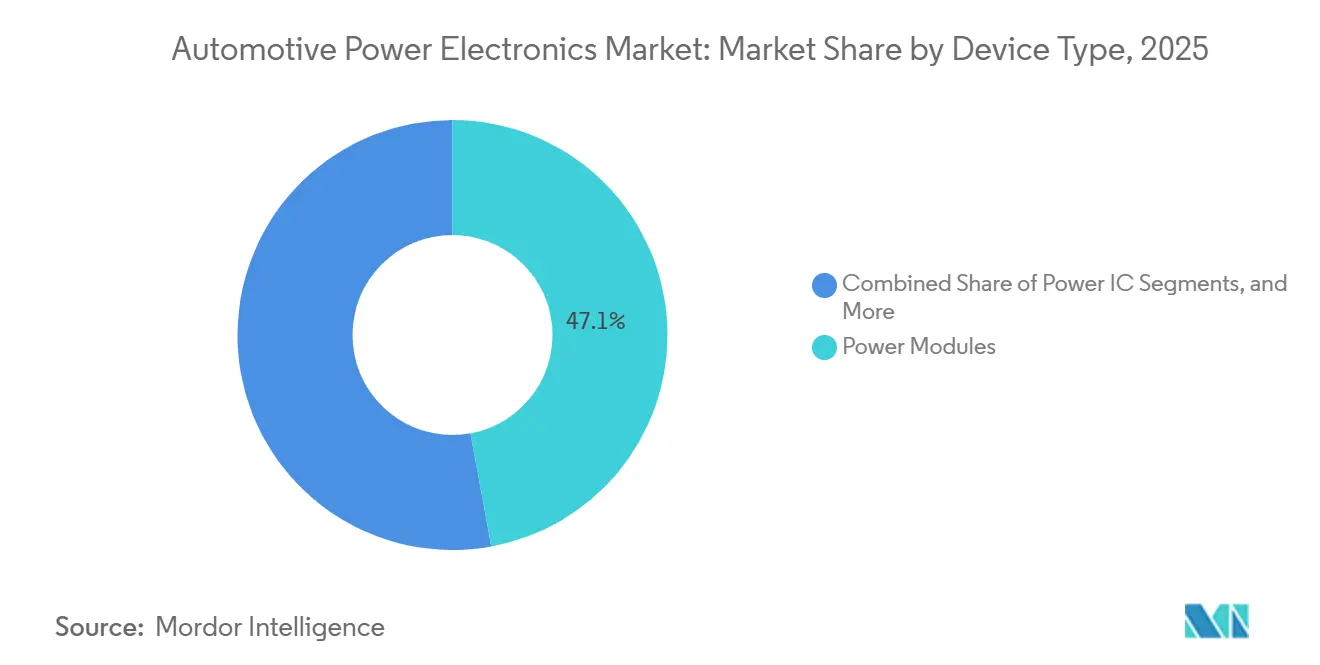

- By device type, power modules accounted for 47.12% of the automotive power electronics market share in 2025, with SiC power modules projected to advance at a 13.97% CAGR through 2031.

- By application, powertrain systems commanded a 62.54% share of the automotive power electronics market in 2025 and are expected to expand at a 14.15% CAGR through 2031.

- By vehicle type, passenger cars led the automotive power electronics market, accounting for 54.27% of market share in 2025 and projected to grow at a 12.23% CAGR through 2031.

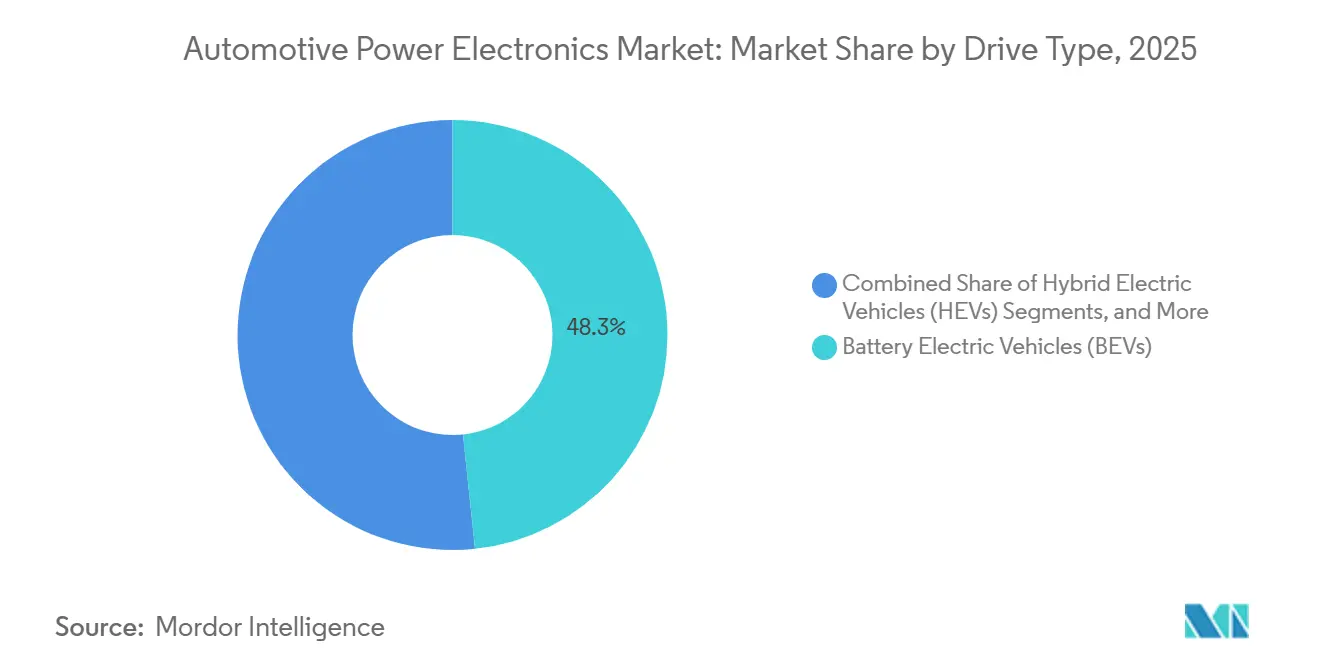

- By drive type, battery-electric vehicles accounted for 48.34% of the automotive power electronics market in 2025 and are expected to grow at a 14.67% CAGR through 2031.

- By component, power modules accounted for 41.91% of the automotive power electronics market in 2025, while on-board chargers were the fastest-growing line item, growing at a 16.16% CAGR through 2031.

- By geography, the Asia-Pacific region accounted for 42.88% of the automotive power electronics market share in 2025, while the North American region is expected to scale at a 12.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Power Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Charging Infrastructure Build-Out | +2.5% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Migration to 800V Architectures | +2.1% | North America, Europe, APAC premium segments | Medium term (2-4 years) |

| Design-In of SiC/GaN Devices | +1.8% | Global, concentrated in premium EV platforms | Long term (≥4 years) |

| Vehicle-Emission Regulations | +1.4% | Europe, North America, China | Short term (≤2 years) |

| Advanced Safety Electronics Demand | +1.2% | Europe, North America, with spillover to APAC | Medium term (2-4 years) |

| Integration of Inverter Functions | +1.0% | Global, led by European OEMs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in EV Adoption and Charging Infrastructure Build-Out

In 2025, battery-electric cars accounted for 17.4% of the EU market, with 1,880,370 new registrations[1]"New car registrations", ACEA, acea.auto. This installed base is stimulating demand for on-board chargers capable of managing peak loads above 350 kilowatts without thermal runaway. As of early 2026, the United States boasted around 85,000 public EV charging stations, totaling over 230,000 individual ports. This marks a significant jump from the 50,000 stations recorded in 2022, yet the charger-to-vehicle ratio still trails recommended levels, supporting continued infrastructure rollouts[2]"How Many EV Charging Stations Are in the US? 2026 Numbers and Growth Trends", Charge Rigs, chargerigs.com. OEMs are equipping 2026 model-year vehicles with bidirectional capability that monetizes stationary battery storage during grid peaks. This shift, in turn, elevates the requirements for high-frequency switching devices and robust thermal paths.

OEM Migration to 800 V Electrical Architectures

Automakers moving to 800-volt platforms slash charging times and trim copper mass in wiring harnesses. BMW’s Neue Klasse platform, set to launch in 2027, features four individual wheel motors, an 800-volt charging system, a battery surpassing 100 kWh, and lightweight construction elements made from natural fibers that deliver materially higher efficiency than legacy 400-volt systems[3]WEB TEAM, "BMW M plans performance EVs with 800-Volt technology and four-motor system", Electric and Hybrid Vehicle Technology International, electrichybridvehicletechnology.com. Such architectures demand semiconductors rated above 1,200 volts while maintaining junction temperatures below 175 °C. Supply is constrained by wafer availability, spurring vertically integrated investments in substrate capacity that secure long-term volumes for premium EV lines.

Rapid Design-In of SiC/GaN Power Devices by Tier-1 Suppliers

Tier-1s are embedding wide-bandgap switches into traction inverters and DC-DC converters to meet OEM efficiency targets. Silicon-carbide wafer prices dropped in 2025, but remain several times higher than silicon equivalents, limiting adoption to high-margin models. Cost curves are improving as new fabs reach scale, helped by incentives under the CHIPS and EU Chips Acts. Gallium nitride parts are finding a foothold in compact on-board chargers, where high-frequency operation shrinks passive components.

Stricter Global Vehicle-Emission Regulations

China’s dual-credit mechanism obliges automakers to reach around 48% new-energy vehicle sales in 2026, penalizing shortfalls and turbo-charging electrification programs. The United States finalizes tougher Corporate Average Fuel Economy rules for 2027-2031, effectively steering OEMs toward battery-electric lineups. Europe’s postponement of Euro 7 emissions to 2027 has not slowed investment; instead, firms are front-loading electrification to avoid stranded assets in combustion platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal-Management Challenges | -1.8% | Global, particularly compact vehicles | Short term (≤ 2 years) |

| Cyclical Semiconductor Supply Constraints | -1.4% | Global, acute in Europe and North America | Medium term (2–4 years) |

| High Material Cost | -1.1% | Global, price-sensitive emerging markets | Medium term (2–4 years) |

| Absence of Unified Global Standards | -0.7% | Global, fragmented regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Wide-Bandgap Materials

Silicon-carbide substrate production is capital-intensive, with new fabs requiring multibillion-dollar investments and extended ramp-up periods before yields stabilize. That burden filters down the chain, keeping wide-band-gap devices largely confined to premium trims and specialized commercial fleets where efficiency gains justify the price. While substrate defect densities continue to fall, the pace of cost reduction still trails the aggressive electrification schedules mandated by regulators, forcing OEMs to adopt hybrid strategies that mix silicon IGBTs with SiC MOSFETs. Suppliers are therefore prioritizing long-term supply agreements and kernel-level co-design with automakers to lock in volume and secure predictable depreciation on new equipment.

Thermal-Management Challenges at Higher Power Densities

Power densities above 200 W/cm³ place severe stress on conventional air-cooled heat sinks, especially in tightly packaged skateboard platforms where airflow is limited. Moving to liquid loops improves heat extraction but adds weight, complexity, and potential leak points, thereby elevating validation and service costs for fleet operators. Immersion cooling shows promise for peak-power events, yet its maintenance demands confine adoption to niche motorsport or demonstrator programs. Suppliers are experimenting with high-conductivity graphite pads and phase-change interface materials to trim thermal resistance, but durability under vibration and temperature cycling remains a concern.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Power Modules Lead Integration Trend

Power modules command a 47.12% share in 2025, underscoring their pivotal role in efficient power conversion and thermal handling across today’s vehicle platforms. Automakers count on these compact, high-performance blocks for electrified drivelines, DC-DC converters, traction inverters, and battery links, all of which need durable, low-loss switching. Surging electric- and hybrid-vehicle adoption amplifies demand, as modules ensure reliable energy delivery under heavy loads. As 800-volt designs spread, modules stay vital for safety, output, and economy, solidifying their place at every major OEM.

Silicon-carbide power modules are the fastest-growing segment, growing at a 13.97% CAGR due to superior switching speed, heat tolerance, and lower energy waste. SiC lets carmakers shrink, lighten, and sharpen powertrains, directly boosting range and charging times, prime EV metrics. Adoption is quick in new inverters, onboard chargers, and fast-charge gear, and as 800-volt EVs advance, SiC becomes central to meeting performance targets and rules. Their swift uptake marks a long-term shift in automotive semiconductor choices.

By Application: Powertrain Systems Drive Market Evolution

Powertrain systems lead with 62.54% of 2025 sales, reflecting power electronics’ core roles in propulsion, regenerative braking, inverter control, and battery maintenance. Electrified drivelines require smart semiconductors to manage energy between motors, packs, and auxiliaries, making these devices the backbone of modern EVs and hybrids. OEM acceleration toward electric platforms keeps demand climbing, and richer motor-control units plus high-voltage DC-DC converters only deepen this lead. Thus, powertrain electronics remain the main contributor to sector revenue.

Powertrain systems also post the quickest growth, advancing at a 14.15% CAGR as EV use spreads worldwide. Makers are shifting to wide-bandgap chips and dense modules to meet tougher efficiency goals, and high-voltage layouts in premium and long-range EVs are widening power electronics’ influence on total vehicle tuning. Integrated e-drives that merge motor, inverter, and gearbox add further lift, confirming powertrain electronics as the prime engine of innovation and spending.

By Vehicle Type: Passenger Cars Maintain Leadership

Passenger cars account for 54.27% of the 2025 market, mirroring their global dominance and rapid tech adoption across mainstream models. Modern cars lean on power electronics for e-propulsion, ADAS, efficient HVAC, and smart energy oversight. Rising hybrid and EV demand is boosting the number of inverters, battery managers, and chargers per vehicle, while buyers seek efficient, connected, and safer mobility. These trends cement passenger cars as the top growth engine.

This segment also grows fastest, at a 12.23% CAGR, as EV adoption quickens across all central regions. Subsidies, emission rules, and broader charging networks lift semiconductor content, and compact EVs, premium SUVs, and sporty sedans each need tailored power solutions. Falling battery costs and better efficiency speed uptake in mid-income markets, keeping passenger cars both the largest and most dynamic slice.

By Drive Type: BEVs Lead Electrification Wave

Battery electric vehicles (BEVs) account for 48.34% of 2025 turnover, spotlighting momentum toward zero-emission travel under strict climate targets. BEVs depend on power electronics for drive control, rapid charging, high-voltage energy routing, and regenerative braking, raising chip usage far above that of ICE or hybrids. Longer-range models and larger packs intensify this need, and as platforms pivot to 800-volt setups, BEVs anchor overall demand.

BEVs are also anticipated to grow the fastest, at a 14.67% CAGR, as policies tighten and charging grids expand. Next-gen 800-volt designs and ultra-fast DC stations drive advanced semiconductors, accelerating the take-up of SiC and GaN. Makers add advanced inverters, cooling, and converters to maximize output and cut waste, and with cheaper batteries and more models, BEVs stay the future core of power-electronics use.

By Component: On-Board Chargers Show Fastest Growth

Power modules top the component list with 41.91% in 2025, owing to broad use in traction inverters, DC-DC units, e-axles, and control blocks. Their high-voltage switching, compact heat paths, and efficiency make them essential to electric and hybrid designs, while ruggedness against temperature swings, vibration, and cycling seals OEM trust. These factors keep modules central to global demand.

Onboard chargers are the fastest-growing segment, rising at a 16.16% CAGR amid soaring home, work, and destination charging needs. Buyers want quicker AC charging and smarter energy use, prompting suppliers to craft compact, bidirectional-ready units. V2G and V2H features turn OBCs into advanced energy hubs, and higher voltages plus SiC designs fuel uptake, making them a vital EV electronics node.

Geography Analysis

Asia-Pacific commands 42.88% of the 2025 share, led by China’s concentrated battery-electric vehicle production and vertically integrated semiconductor supply chains. Government mandates that tie sales quotas to new-energy vehicles sustain multi-year visibility for local wafer, module, and packaging plants, encouraging capacity expansion across the region. Japan and South Korea add depth through mature power-integrated-circuit ecosystems, even though their automakers have been slower to migrate to 800-volt platforms. India’s fast-growing two-wheeler segment amplifies demand for cost-optimized silicon devices, creating a parallel low-power volume stream that stabilizes fab utilization.

North America shows the fastest regional growth rate at 12.68% CAGR through 2031, as domestic fabrication attracts public incentives and private capital. Public charging networks are expanding along interstate corridors, reinforcing consumer confidence and supporting higher-capacity on-board chargers that use advanced power modules. Canadian battery-material projects complement this build-out by anchoring upstream inputs and offering OEMs a nearshore path from raw materials to finished vehicles. These combined moves foster a closed-loop ecosystem that reduces lead times, trims working capital tied up in inventory, and encourages additional module-assembly investment in Mexico’s existing automotive clusters.

Europe balances deep semiconductor heritage with some of the world’s strictest emissions regimes, making the bloc both a technology leader and a regulatory pace-setter. Automakers headquartered in Germany, France, and Sweden continue front-loading electrification programs despite the later Euro 7 implementation date, partly to avoid stranded internal-combustion investments. Eastern European nations are benefiting as lower-cost assembly sites for inverters and on-board chargers, spreading production beyond the traditional industrial heartland. A continent-wide push to harmonize charging standards is also nudging suppliers toward interoperable power-conversion topologies, lowering duplication across vehicle lines.

Competitive Landscape

The automotive power electronics market remains moderately concentrated, with the five most prominent vendors still holding sizable shares. Yet, fresh pressure is coming from Chinese entrants and niche wide-bandgap specialists. Incumbents such as Infineon, onsemi, and STMicroelectronics rely on decades of automotive qualification know-how and long-standing OEM ties to defend their positions. Meanwhile, up-and-coming rivals pursue lower-cost SiC and GaN products that squeeze traditional price structures. Wide-band-gap specialists continue to win high-voltage inverter slots by delivering thermal-optimized packages that shorten OEM validation cycles, forcing legacy suppliers to accelerate their own substrate roadmaps or risk share erosion.

Patent activity around multi-chip packaging with embedded sensing has intensified, signaling an industry pivot toward domain-controller consolidation where hardware and firmware co-design becomes a competitive moat. Chinese entrants, buoyed by local policy support and cost-focused domestic demand, are sharpening price competition in 400-volt segments and compelling incumbents to segment their portfolios more finely between premium efficiency and mainstream affordability. Further, collaboration across the value chain is emerging as a critical success factor. Automakers are increasingly entering joint development agreements that lock in device roadmaps 3 to 5 years before vehicle launch, effectively reserving future wafer capacity in exchange for early-stage design input.

Tier-1 suppliers are bundling power electronics with thermal and controls software into single service contracts, shifting negotiations from component pricing toward total system performance guarantees. Private-equity investors have begun consolidating mid-tier module houses, betting on scale synergies in packaging know-how and backend automation. Finally, the race to master embedded security for over-the-air inverter updates introduces a new axis of differentiation that favors suppliers with strong microcontroller and firmware pedigrees, broadening the definition of competition beyond pure silicon metrics.

Automotive Power Electronics Industry Leaders

-

Infineon Technologies AG

-

Texas Instruments Incorporated

-

Renesas Electronics Corporation

-

STMicroelectronics NV

-

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Toyota chose Infineon's silicon carbide power semiconductors for its new bZ4X battery-electric vehicle. Infineon's CoolSiC MOSFETs will feature in the vehicle's on-board charger (OBC) and DC/DC converter.

- October 2025: Infineon Technologies AG achieved a pivotal milestone in its quest to lead in gallium nitride (GaN) technology. The firm has unveiled its inaugural 100V CoolGaN™ Automotive Transistor G1 family, marking it as the first series of GaN transistors to receive AEC-Q101 certification for automotive use.

- October 2025: STMicroelectronics (ST) introduced the L98GD8, an 8-channel gate driver for 48V mild-hybrid systems. It features configurable channels for high-side and low-side MOSFET driving, operates on a 58V supply, and includes advanced diagnostics and protection for safety. Optimized for NMOS or PMOS FET gates, it efficiently supports 48V-powered systems.

- September 2025: STMicroelectronics introduced the SPSA068, a compact and cost-effective PMIC for automotive applications. Qualified to AEC-Q100, it supports ISO 26262 FuSa approval up to ASIL-B. Designed for MCUs with single-supply voltage, this device features a 1A buck voltage regulator, a 1% voltage reference, watchdog supervisors, diagnostic indicators, MCU reset control, and SPI for configuration and monitoring.

Global Automotive Power Electronics Market Report Scope

Automotive power electronics is a modern technology that efficiently converts, conditions, and controls electrical power in an automobile.

The Automotive Power Electronics Market has been segmented by device type, application, vehicle type, drive type, component, and geography. By Device Type, the market is segmented into Power ICs, Power Modules, and Discrete Devices. By Application, the market is segmented into Powertrain Systems, Body Electronics, and Safety and Security Electronics. By Vehicle Type, the market is segmented into Passenger Cars, Light Commercial Vehicles, Two-Wheelers, and Medium and Heavy-Duty Vehicles. By Drive Type, the market is segmented into Internal Combustion Engine, Hybrid Electric Vehicles, and Battery Electric Vehicles. By Component, the market is segmented into Power Modules, Converters, Controllers, Switches, Battery Management Systems, and On-Board Chargers. By Geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. For each segment, the market sizing and forecast have been done based on value (USD).

| Power ICs |

| Power Modules |

| Discrete Devices |

| Powertrain Systems |

| Body Electronics |

| Safety and Security Electronics |

| Passenger Cars |

| Light Commercial Vehicles |

| Two-Wheelers |

| Medium and Heavy-Duty Commercial Vehicles |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEVs) |

| Battery Electric Vehicles (BEVs) |

| Power Modules |

| Converters |

| Controllers |

| Switches |

| Battery Management Systems |

| On-Board Chargers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Device Type | Power ICs | |

| Power Modules | ||

| Discrete Devices | ||

| By Application | Powertrain Systems | |

| Body Electronics | ||

| Safety and Security Electronics | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Two-Wheelers | ||

| Medium and Heavy-Duty Commercial Vehicles | ||

| By Drive Type | Internal Combustion Engine (ICE) Vehicles | |

| Hybrid Electric Vehicles (HEVs) | ||

| Battery Electric Vehicles (BEVs) | ||

| By Component | Power Modules | |

| Converters | ||

| Controllers | ||

| Switches | ||

| Battery Management Systems | ||

| On-Board Chargers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the automotive power electronics market be by 2031?

It is forecasted to reach USD 9.76 billion, reflecting an 11.18% CAGR over 2026-2031.

Which component is growing the fastest?

On-board chargers post the quickest growth thanks to rising demand for bidirectional vehicle-to-grid functionality.

Why are 800-volt architectures important?

They cut charging times and reduce copper weight, but require silicon-carbide or gallium-nitride devices to handle higher voltages safely.

Which region is expanding most rapidly?

North America leads future growth as domestic fabrication and tax incentives under the Inflation Reduction Act accelerate local supply chains.

Which region is growing the fastest?

North America shows the highest regional CAGR at 12.68% due to policy incentives and domestic manufacturing expansion.

What is the main restraint on wide-bandgap adoption?

High substrate cost keeps silicon-carbide and gallium-nitride devices concentrated in premium vehicle segments, slowing penetration into mass-market models.

Page last updated on: