Automotive Transmission Engineering Services Outsourcing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 13.20 Billion |

| Market Size (2030) | USD 17.34 Billion |

| Growth Rate (2025 - 2030) | 5.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Transmission Engineering Services Outsourcing Market Analysis by Mordor Intelligence

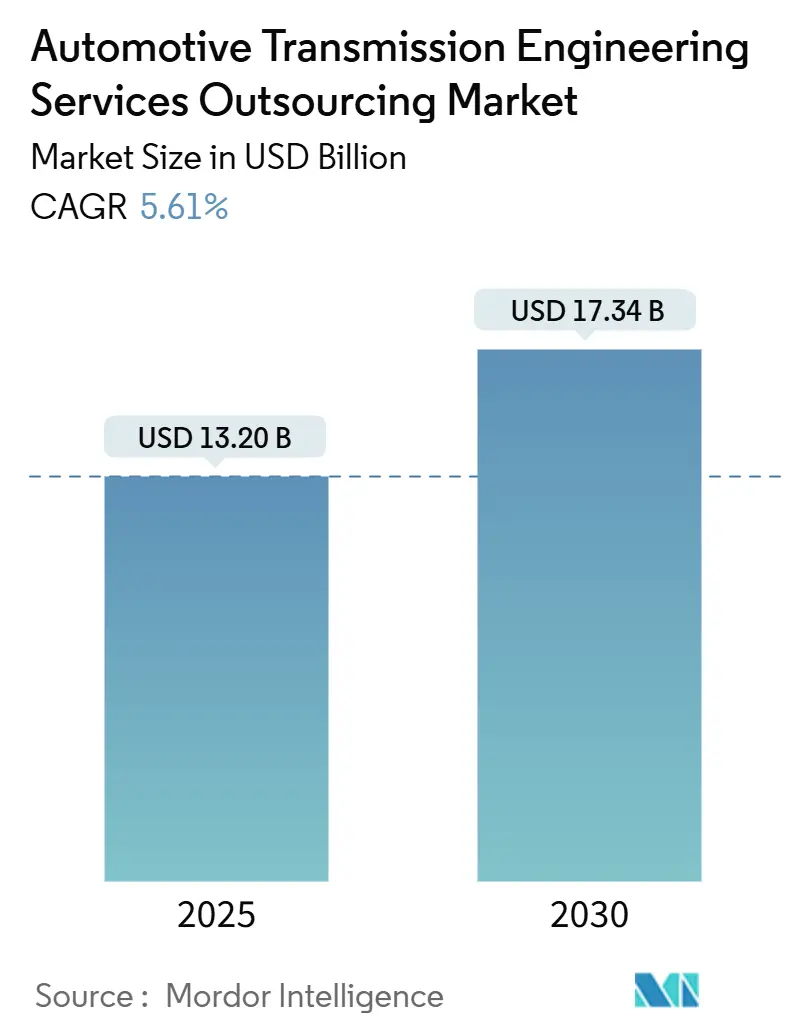

The automotive transmission engineering services outsourcing market is valued at USD 13.20 billion in 2025 and is forecast to reach USD 17.34 billion by 2030, which will expand at a 5.61% CAGR over the period. Demand escalates as electrification, advanced driver-assistance features, and software-defined vehicle architectures transform transmission design. OEMs trim engineering budgets yet face rising complexity in multi-speed electric drives, dual-clutch units, and hybrid systems, so they look outward for specialized talent and digital toolchains. On the supply side, tier-1 engineering providers deepen virtual calibration, digital-twin, and AI capabilities to cut prototype cycles and win higher-margin programs. Globalization of vehicle platforms sustains cross-border outsourcing despite security concerns, while emerging two-wheeler and light-commercial electrification adds incremental service volumes.

Key Report Takeaways

- By service type, design engineering led with 39.12% of the automotive transmission engineering services outsourcing market share in 2024, whereas simulation and modeling recorded the highest growth at 6.14% CAGR through 2030.

- By transmission type, automatic systems accounted for 47.05% of the automotive transmission engineering services outsourcing market share in 2024, and dual-clutch transmissions are projected to rise at a 7.09% CAGR to 2030.

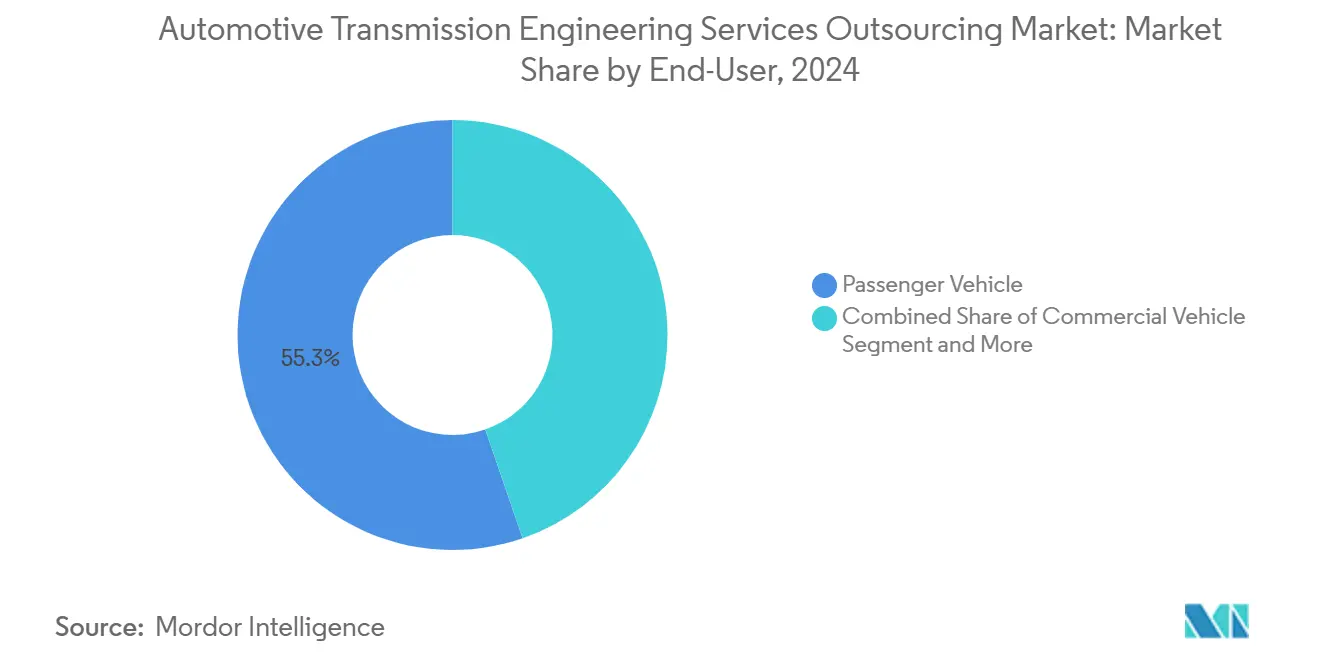

- By end-user, passenger vehicles dominated with 55.33% of the automotive transmission engineering services outsourcing market share in 2024; two-wheelers post the fastest trajectory at 6.48% CAGR to 2030.

- By technology, mechanical engineering retained a 42.61% of the automotive transmission engineering services outsourcing market share in 2024, while electronics and software integration advanced at a 7.55% CAGR to 2030.

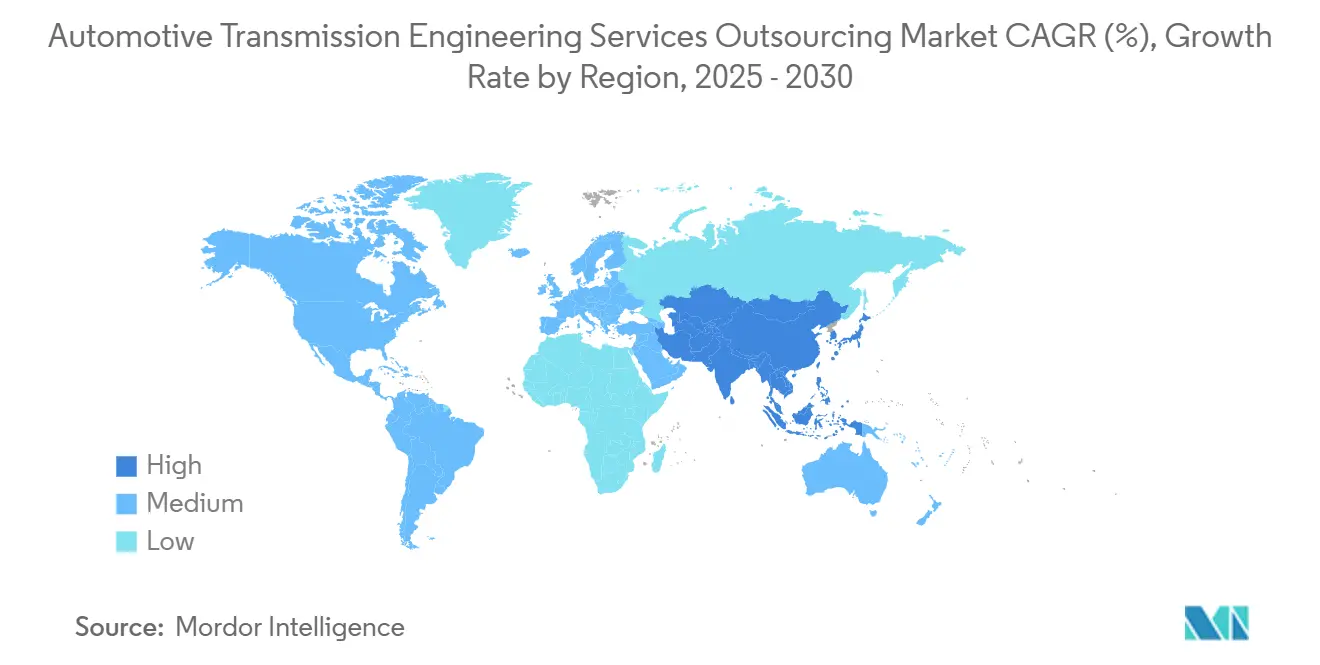

- By geography, Asia-Pacific secured 49.18% of the automotive transmission engineering services outsourcing market share in 2024 and is projected to grow at a 5.95% CAGR, outpacing all other regions.

Global Automotive Transmission Engineering Services Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification and Transmission Redesign | +1.2% | Global; early uptake in EU and China | Medium term (2–4 years) |

| Widespread Adoption of CVT and DCT | +0.9% | APAC core; spill-over to emerging markets | Medium term (2–4 years) |

| Cost-Saving Drives Engineering Outsourcing | +0.8% | Global; strongest in North America and Europe | Short term (≤2 years) |

| Shorter Lifecycles Force Simultaneous Engineering | +0.7% | Global; premium segments prominent | Short term (≤2 years) |

| AI Optimizes Calibration and Strategy | +0.6% | North America and EU; spreading to APAC | Long term (≥4 years) |

| Connected Transmissions for ADAS/AV | +0.5% | Global; led by premium OEMs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Electrification-Driven Redesign of Transmission Architectures

Transmission layouts change fundamentally as vehicle propulsion pivots toward battery-electric and hybrid power. Single-speed and two-speed e-drive units replace legacy eight- to ten-speed automatics, yet still need thermal management, power-electronics packaging, and torque coordination across multiple motors. Engineering partners now handle integration of liquid-cooled gearboxes, silicon-carbide inverters, and functional-safety software aligned with ISO 26262. Mercedes-Benz validated AI-based clutch control models for hybrid units in this collaborative mode [1]M. Kist and B. Müller, “Application of Neural Networks in Hybrid Clutch Development,” Springer, springer.com. Such high-fidelity toolchains shorten test loops while meeting escalating safety audits, turning specialist outsourcing into a strategic lever for OEMs.

Rapid Adoption of CVT and DCT for Fuel-Efficient ICEs

CVT and dual-clutch boxes remain critical bridges to full electrification. Their slip control, belt geometry, and clutch thermal loads demand sophisticated co-simulation of fluid, mechanical, and control domains. Researchers showed that road-slope and adhesion variations alter DCT startability and driveline oscillations, compelling granular calibration. Asian compacts now standardize CVT to meet fleet-average targets without costly battery packs. Outsourcing thrives because niche firms already own belt fatigue models, electro-hydraulic valve libraries, and real-road replay rigs that OEMs cannot duplicate quickly.

OEM Cost-Saving Mandates Accelerating Engineering Outsourcing

Manufacturers scramble to serve parallel ICE, hybrid, and full-electric programs without ballooning fixed headcount. Variable-cost outsourcing lets them scale talent pool, add niche skills, and hedge currency swings. Heavy-duty truck makers illustrate the trend: they rely on external teams for torque-converter math models, NVH root-cause analysis, and aftertreatment calibration to offset supplier pricing power. Tier-1 service firms, therefore, bundle multi-disciplinary squads, co-development platforms, and outcome-based pricing frameworks that resonate with finance chiefs steering margin recovery.

Shrinking Model Lifecycles Requiring Simultaneous Engineering

Product refresh cycles are compressed in 2025, so brands run multiple transmission variants in parallel. Coordinating thermal simulation, supplier drawings, and regulatory dossiers across overlapping milestones taxes internal resources. External partners contribute concurrent design cells that mirror OEM agile sprints and plug into cloud-based PDM vaults. Modular libraries for clutch control code exemplify reusable assets that de-risk simultaneous programs. The result is faster platform turnover without sacrificing driveline quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IP and Security in Multi-Region Projects | −0.4% | Global; acute in the United States–China work | Short term (≤2 years) |

| OEM Integration Creates Cost Pressure | −0.3% | North America and EU premium OEMs | Medium term (2–4 years) |

| Shortage of Mechatronics Specialists | −0.3% | Global; sharper in developed markets | Medium term (2–4 years) |

| Ambiguous ICE Phase-Out Timelines | −0.2% | Global; varies by market | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

IP and Data-Security Concerns in Multi-Region Projects

OEMs hesitate to share proprietary shift algorithms or gear micro-geometry with overseas partners amid heightened geopolitical scrutiny. The United States. National Security Commission on Artificial Intelligence warned that model-extraction attacks can lift core IP from black-box systems [2]“Final Report,” National Security Commission on Artificial Intelligence, nscai.gov. Bosch researchers replicated such exploits on driveline ML models. Outsourcers must therefore add zero-trust architectures, regional data centers, and compliance audits to win cross-border contracts, which inflates overhead and elongates deal cycles.

Cost Pressure From OEM Vertical Integration of E-Drive Units

Some premium brands, notably German and United States luxury players, insource electric drivetrain design to safeguard differentiation and cut supplier margins. Virtual TCU stacks built internally demonstrate this pivot[3]“Virtual ECU Development for Next-Generation Drivetrains,” Synopsys Inc., synopsys.com. As e-drive layouts simplify relative to multi-gear automatics, economics tilt toward in-house squads. Outsourcers counter by offering niche value, such as thermal-runaway mitigation or silicon-carbide inverter tuning, where OEM skill sets remain thin.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Design Engineering Retains Lead, Simulation Surges

Design engineering held 39.12% of the automotive transmission engineering services outsourcing market share in 2024, reflecting the bedrock role of system architecture, geartrain sizing, and control-hardware layout. Even as software depth grows, physical packaging, NVH mitigation, and bear-load durability still command high-value hours. Testing and validation clusters around durability rigs, real-time hardware-in-loop benches, and emissions conformity, anchoring multiyear retainers.

The simulation and modeling arena is expected to expand at a 6.14% CAGR through 2030, benefiting the automotive transmission engineering services outsourcing market as OEMs chase shorter sprints. High-order finite-element meshes, lubricant CFD, and system-level digital twins elevate up-front fidelity, slicing prototype loops. Consequently, many design contracts now bundle co-simulation seats, model maintenance, and physics-informed AI modules, an avenue for price premiums and stickier client engagement.

By Transmission Type: Automatic Systems Prevail, DCT Accelerates

Automatic transmission controlled 47.05% of the automotive transmission engineering services outsourcing market share in 2024. Their electro-hydraulic valve bodies, multi-plate clutches, and torque-converter damper logic create dense engineering workloads that OEM core teams rarely maintain. New-generation 10-speed units and e-axle gear reducers preserve momentum for outsourced design reviews and thermal-soak campaigns.

While representing a smaller base, dual-clutch solutions are projected to grow at a 7.09% CAGR, the fastest among architectures. Efficient power flow, launch smoothness, and low CO₂ scores make DCT a go-to option for sporty hybrids and premium compacts. Complex slip-control models and multi-gear preselection algorithms necessitate mechatronic expertise, reinforcing outsourcing reliance for bench calibration, adaptive friction mapping, and live-road validation.

By End-User: Passenger Vehicles Dominate, Two-Wheelers Escalate

Passenger vehicles contributed 55.33% of the automotive transmission engineering services outsourcing market share in 2024, anchored by high-volume global platforms and the drive toward electrified multi-speed boxes in SUVs and crossovers. Fleet EV vans and pickups add incremental projects focused on high-torque reduction stages and thermal-constrained duty cycles, extending the scope of the automotive transmission engineering services outsourcing market.

Two-wheelers, projected at 6.48% CAGR, push innovation in compact e-drives, single-clutch AMTs, and regenerative braking controllers. Asian megacities underpin volumes, and start-ups favor asset-light business models, outsourcing drivetrain design to compress launch schedules. Service firms deploy modular motor-control library assets and battery-thermal codexes to accelerate scooter and motorcycle programs.

By Technology Used: Mechanical Core Persists, Electronics and Software Lead Growth

Mechanical engineering still anchors 42.61% of the automotive transmission engineering services outsourcing market share in 2024, confirming that gears, shafts, and bearing sets remain foundational. Advanced finishing, low-friction coatings, and topology-optimized casings keep mechanical know-how in demand.

Electronics and software integration should grow at a 7.55% CAGR. Transmission control units link with vehicle domain controllers, cloud dashboards, and cybersecurity frameworks. Service partners, therefore, embed DevSecOps disciplines, compile AUTOSAR-adaptive stacks, and validate FOTA over 5G channels. Expanding code content inflates project scope per gearbox, propelling service revenue even as component counts shrink.

Geography Analysis

Asia-Pacific preserved a 49.18% of the automotive transmission engineering services outsourcing market share in 2024 and is forecast to register a 5.95% CAGR to 2030. Dense manufacturing clusters in China, India, and Thailand underpin economies of scale, while local champions like Tata Technologies and KPIT anchor domain expertise in model-based design and virtual calibration. Regional governments extend tax credits for EV component R&D, deepening the automotive transmission engineering services outsourcing market moat.

Europe and North America's mature ecosystems prize simulation accuracy, functional-safety audits, and ADAS gearbox harmonization. Service contracts in these zones emphasize AI-ready datasets, cloud-native verification rigs, and agile governance that aligns with ISO 21434 cyber mandates. Reshoring debates inject moderate friction, yet a scarcity of specialist talent sustains cross-border engagement, especially for peak-load phases.

South America, the Middle East, and Africa remain emerging pockets, jointly holding a nominal share yet trending upward. Brazil and Mexico drive LatAm demand via localized automatic-gearbox lines plus export programs for compact pickups. Gulf states explore electric taxi fleets that need lightweight reduction boxes and thermal-robust lubricants, while South Africa’s supplier parks court EV start-ups eyeing EU tariff bypass routes. Limited native skillsets open doors for global providers to seed satellite hubs and ramp under-utilized CAD benches.

Competitive Landscape

The automotive transmission engineering services outsourcing market sits in the moderate-fragmentation zone. AVL, FEV Group, and Ricardo headline global rosters, capturing a minimal share. They differentiate with proprietary digital-twin frameworks, model libraries, and turnkey validation cells that fold mechanical, electronic, and software deliverables into single contracts.

Mid-tier regional players in India, China, and Eastern Europe compete mainly on labor cost, yet climb the value curve by licensing open-source simulation cores and recruiting expatriate specialists. Software-centric disruptors target control algorithm niches, cloud test orchestration, and MLOps pipelines, capturing projects where hardware scope is small but code density is high.

Strategic moves include AVL’s rollout of an end-to-end battery-electric two-speed e-drive design kit, FEV Group’s acquisition of a German cybersecurity boutique, and Ricardo’s expansion of its California tech center to embed AI-enabled calibration bays. M&A rationalizes fragmented tool ecosystems and widens geographic footprints, preserving vendor relevance as OEMs demand holistic mechatronics competence.

Automotive Transmission Engineering Services Outsourcing Industry Leaders

AVL List GmbH

FEV Group

Ricardo plc

IAV GmbH

Alten Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Toyota previewed an eight-speed DAT upgrade for the GR Corolla, leveraging outsourced partners for calibration and validation of new control software.

- June 2024: KTM demonstrated its automated manual transmission prototype at the Red Bull Erzbergrodeo, a project supported by external firms specializing in electro-hydraulic actuation and control integration.

Global Automotive Transmission Engineering Services Outsourcing Market Report Scope

| Design Engineering |

| Testing and Validation |

| Prototyping |

| Simulation and Modeling |

| Automatic Transmission |

| Manual Transmission |

| Continuous Variable Transmission |

| Dual-Clutch Transmission |

| Two-Wheeler |

| Three-Wheeler |

| Passenger Vehicle |

| Commercial Vehicle |

| Mechanical Engineering |

| Electronics and Software Integration |

| Control Systems |

| Manufacturing Technologies |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | Design Engineering | |

| Testing and Validation | ||

| Prototyping | ||

| Simulation and Modeling | ||

| By Transmission Type | Automatic Transmission | |

| Manual Transmission | ||

| Continuous Variable Transmission | ||

| Dual-Clutch Transmission | ||

| By End-User | Two-Wheeler | |

| Three-Wheeler | ||

| Passenger Vehicle | ||

| Commercial Vehicle | ||

| By Technology Used | Mechanical Engineering | |

| Electronics and Software Integration | ||

| Control Systems | ||

| Manufacturing Technologies | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive transmission engineering services outsourcing market in 2025?

The value stands at USD 13.20 billion in 2025, moving toward USD 17.34 billion by 2030 on a 5.61% CAGR trajectory.

Which service type shows the fastest growth through 2030?

Simulation and modeling is projected to lead with a 6.14% CAGR as virtual development replaces physical prototypes and trims timelines.

Why does Asia-Pacific hold nearly half of global revenue?

High vehicle production volumes, cost-competitive engineering labor, and strong EV policy support give the region 49.18% share and the fastest 5.95% CAGR.

What technology area is expanding quickest inside outsourced transmission projects?

Electronics and software integration grows at 7.55% CAGR as gearboxes become software-defined and connected with ADAS architectures.

Page last updated on: