Automotive Automatic Transmission Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

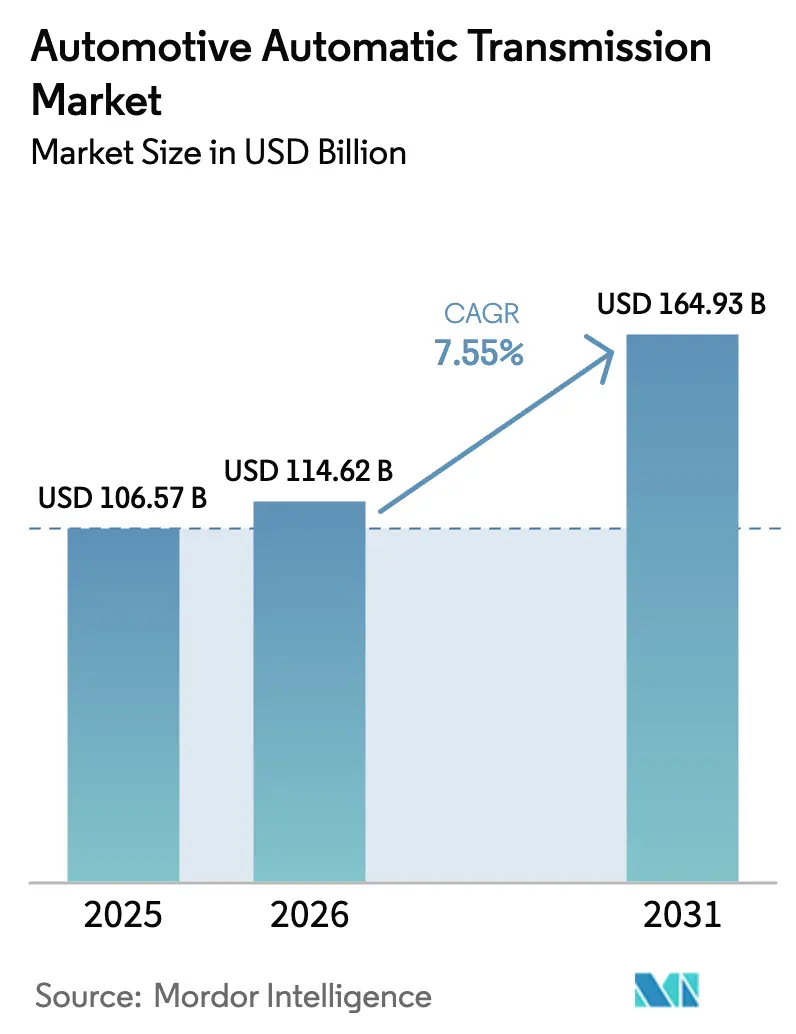

| Market Size (2026) | USD 114.62 Billion |

| Market Size (2031) | USD 164.93 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

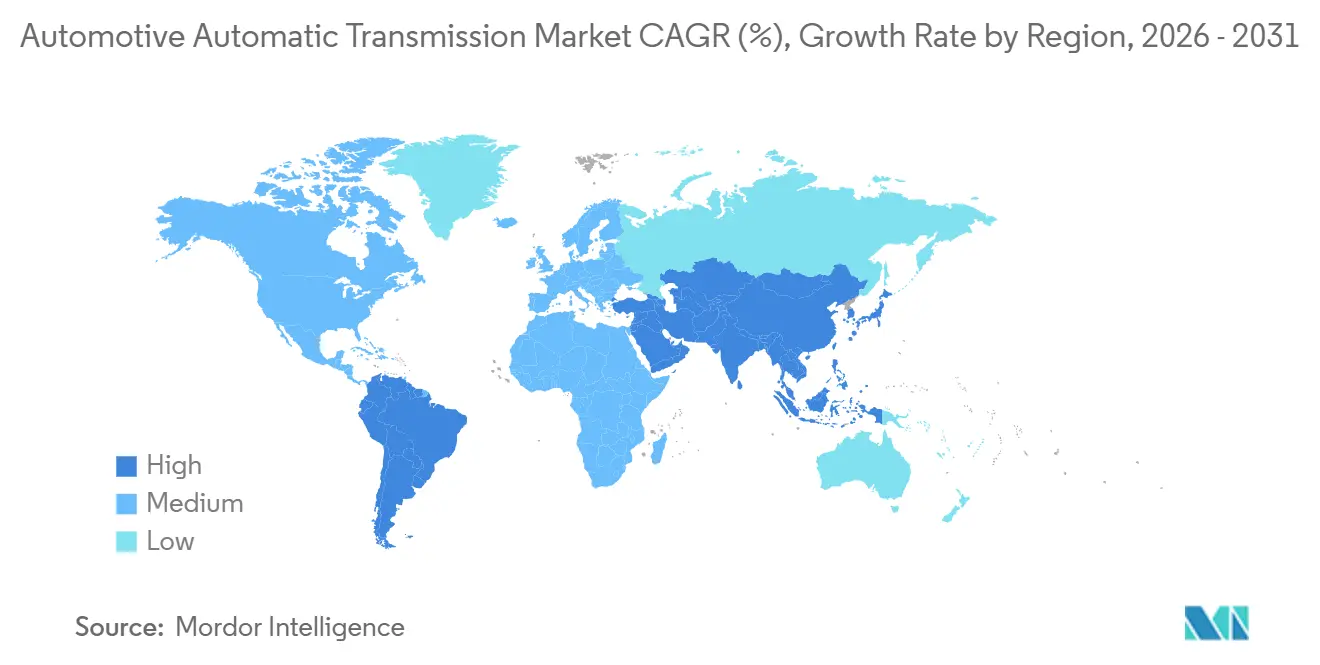

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

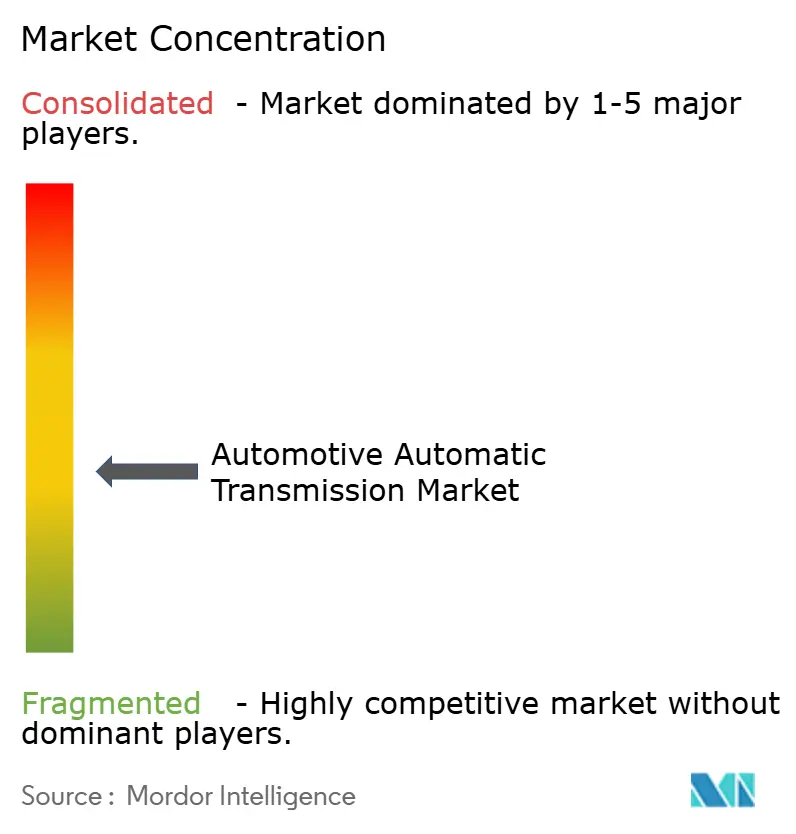

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Automatic Transmission Market Analysis by Mordor Intelligence

The automotive automatic transmission market size is expected to grow from USD 106.57 billion in 2025 to USD 114.62 billion in 2026 and is forecast to reach USD 164.93 billion by 2031 at a 7.55% CAGR over 2026-2031. The rise mirrors a steady move toward higher-gear-count units that deliver measurable fuel-economy gains, satisfy tighter CO₂ rules, and integrate smoothly with hybrid powertrains. Automakers are shifting procurement toward 8-speed and 10-speed designs that cut parasitic losses, while Asia-Pacific incentives encourage local production of advanced gearboxes. Medium and heavy trucks add momentum as fleets pursue better uptime with fully automatic drivetrains. At the same time, over-the-air calibration and cybersecurity compliance costs are turning transmissions into connected electronic devices, opening a new software revenue layer. Regional demand differences persist, yet the automotive automatic transmission market continues to expand its reach as hybrids spread into volume segments.

Key Report Takeaways

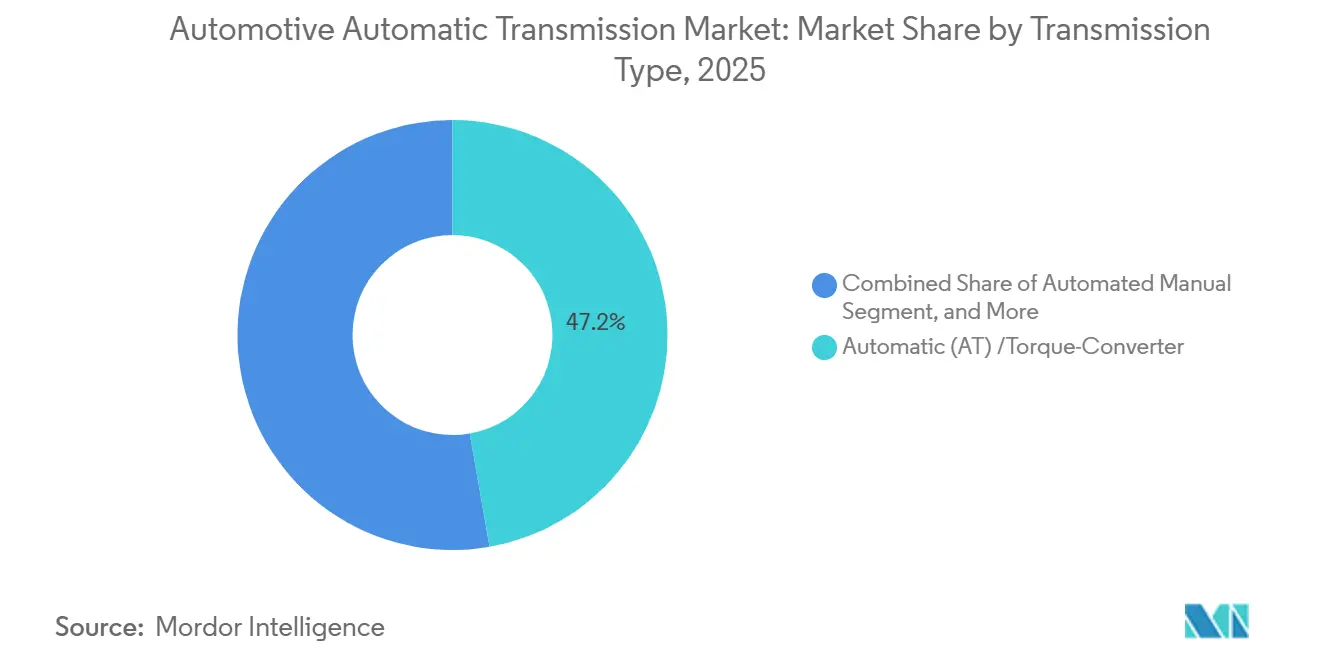

- By transmission type, torque-converter automatics led the automotive automatic transmission market with 47.24% market share in 2025, and the same segment is projected to post the fastest growth at a 7.89% CAGR to 2031.

- By fuel type, gasoline powertrains accounted for 62.18% of the automotive automatic transmission market share in 2025, while hybrid-electric systems are forecast to register the fastest growth at a 13.27% CAGR through 2031.

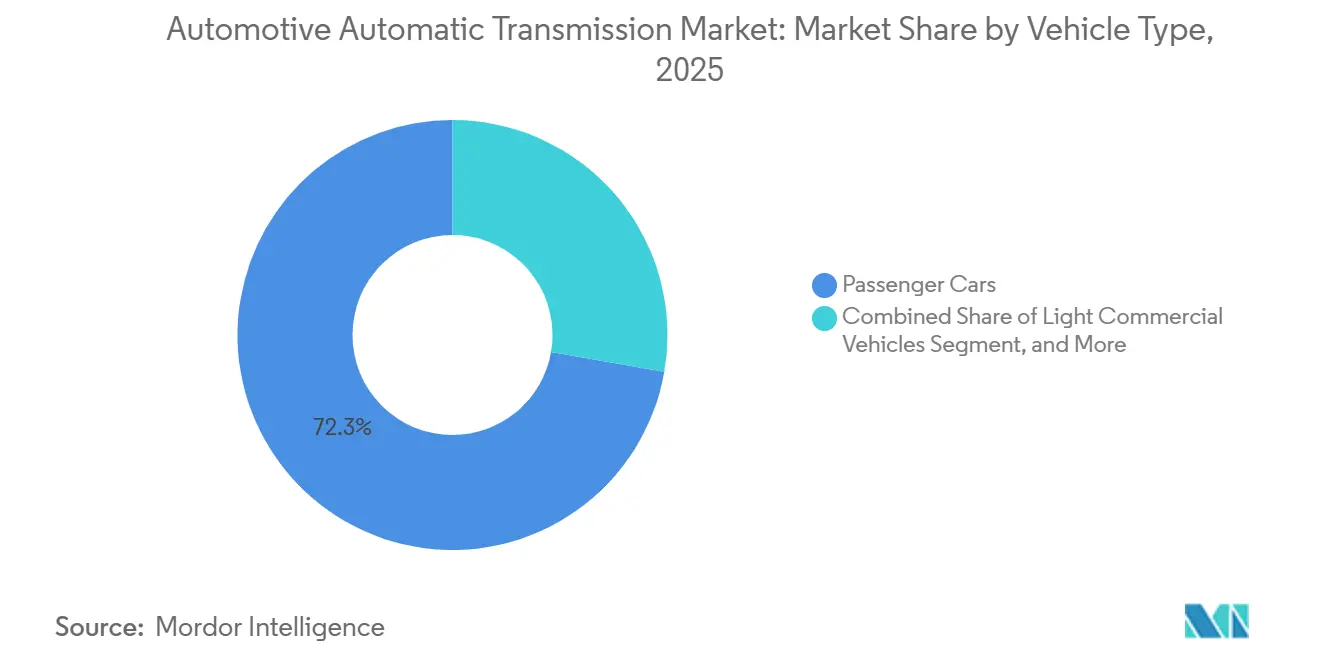

- By vehicle type, passenger cars dominated the automotive automatic transmission market with a 72.27% share in 2025; medium and heavy commercial vehicles are expected to grow the most rapidly at an 11.56% CAGR over 2026-2031.

- By component, torque converters captured 31.28% of the automotive automatic transmission market in 2025 and represent the fastest-growing segment, advancing at an 8.23% CAGR to 2031.

- By geography, Asia-Pacific led the automotive automatic transmission market with a 43.25% share in 2025, while South America is projected to register the highest regional expansion at a 9.24% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Automatic Transmission Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid/xEV e-transmissions | +2.3% | China and Europe Lead | Medium term (2-4 years) |

| Tight Global CO₂ Regs | +1.8% | Europe and North America (Global Spill-over) | Medium term (2-4 years) |

| Urban Congestion Shift | +1.2% | Asia-Pacific Core, Latin America | Long term (≥4 years) |

| Asia-Pacific AT Incentives | +0.9% | Asia-Pacific Hubs | Medium term (2-4 years) |

| AI Shift Scheduling | +0.7% | Global Premium Segment | Long term (≥4 years) |

| OTA-ready TCMs | +0.6% | North America and Europe Premium | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Hybrid and XEV Proliferation Necessitates Dedicated E-Transmissions

BYD's DM-i platform, a plug-in hybrid, integrates dual-motor dedicated hybrid transmissions, enabling electric launches, series cruising, and parallel boosts [1]“DM-i Super Hybrid White Paper,”, BYD Company, byd.com. Geely's Thor DHT optimises engine efficiency, achieving high thermal efficiency. Toyota's latest hybrid transaxle reduces demand for rare earths while maintaining exceptional motor efficiency. Magna's two-speed eDrive enhances the highway range for premium EVs. This hybrid surge significantly boosts the growth rate of the automotive automatic transmission market.

Tightening Global CO₂ / CAFE Regulations Spur OEM Demand for High-Efficiency Transmissions

In response to stricter fuel-efficiency and emissions regulations in the United States and the European Union, carmakers are transitioning from traditional 6-speed units to advanced 8- and 10-speed designs that enhance mechanical efficiency [2]“Light-Duty Vehicle CAFE Standards,”, U.S. Environmental Protection Agency, epa.gov. Policies in China are further accelerating the adoption of power-split eCVTs, enabling pure-electric launches at lower speeds. ZF's advanced transmission systems achieve high efficiency by optimising converter locking during cruising. With new reporting standards requiring brands to document life-cycle efficiency gains, high-efficiency automatic transmissions have become critical for regulatory compliance. These regulatory measures are driving growth in the automotive automatic transmission market.

Urban Congestion Drives Consumer Shift to Automatics in Emerging Economies

In Bengaluru, average traffic speed has decreased significantly, leading to increased clutch-pedal fatigue in manual cars and driving up demand for automatics. This trend is also evident in cities such as Jakarta, Manila, and São Paulo. Maruti Suzuki's budget-friendly automated manual has captured a notable share of India's compact-sedan sales due to its competitive pricing. In Brazil, tax incentives promoting efficient automation have substantially increased their market penetration. This ongoing shift is expected to positively impact the growth rate of the automotive automatic transmission market in the near future.

OTA-Upgradeable Control Modules Open Software Revenue Streams

HARMAN's Smart Delta reduces update file sizes, significantly lowering data-transfer costs per vehicle [3]“Smart Delta OTA Update Technology,”, Harman International, harman.com. This breakthrough not only minimises costs but also eliminates the typical downtime associated with manual reflashing, thereby enhancing operational efficiency. Consequently, fleets can swiftly apply predictive maintenance patches, ensuring seamless functionality and reducing potential disruptions. By enabling these advancements, the transmission control module becomes a highly valuable asset in the automotive transmission market, driving innovation and improving overall performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chip Shortages | -2.2% | Global Manufacturing Hubs | Short term (≤2 years) |

| High cost and Complexity | -1.4% | Global, Price-sensitive Markets | Long term (≥4 years) |

| Warranty Issues | -1.1% | North America, Global GM Markets | Medium term (2-4 years |

| Cybersecurity Compliance | -0.8% | EU and UNECE Adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Shortages Disrupting Control-Module Supply

Transmission ECUs require multiple chips each. Recently, lead times for MCUs significantly increased as fabs prioritized meeting the growing demand for battery management and ADAS. To address these chip shortages, some OEMs opted to ship lower-trim models with older transmissions, delaying the introduction of high-efficiency models. This chip shortage has slightly reduced the near-term growth projection for the automotive automatic transmission market. However, the situation is expected to improve as new fabs begin production.

High Unit Cost and Repair Complexity Versus Manual Transmissions

In India and Africa, adding an 8-speed automatic transmission significantly increases vehicle costs. This rise poses a significant challenge for budget-friendly cars. Consequently, manufacturers face difficulties in incorporating such transmissions into affordable vehicles, limiting their adoption in these regions. Automated manuals, while offering a cost advantage, deliver rougher shifts. This drawback reduces their appeal to consumers who prioritise a smoother driving experience. Additionally, many rural workshops lack the necessary diagnostic tools for mechatronic repairs. This limitation leads to higher service costs and further discourages adoption. These challenges are particularly evident in rural and semi-urban areas, where affordability and service accessibility are critical considerations. As a result, this pricing issue is expected to negatively affect the growth rate of the automotive automatic transmission market in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transmission Type: Torque-Converter Automatics Sustain Growth

Torque-converter automatics hold 47.24% of the automotive automatic transmission market share in 2025, and the cohort is projected to grow at a 7.89% CAGR through 2031. Wide-ratio designs now lock the converter at low speeds, eliminating slip losses. This innovation not only matches the efficiency of dual-clutch systems but also preserves the smooth creep feature that drivers appreciate. As a result, the automatic transmission market sees a surge in demand for these units, particularly in turbocharged trucks and SUVs, where they are known for their durability.

In Japan and Southeast Asia, continuously variable units maintain their dominance, primarily attributed to JATCO’s hybrid system. This system combines a belt variator with an electric starter-generator, effectively reducing engine load. While European sports models have embraced dual-clutch boxes, these face challenges related to cost and thermal management, especially in traffic. On the other hand, price-sensitive light trucks have turned to automated manuals. Collectively, these specialized niches are driving diversification in the broader automotive automatic transmission market, all while keeping the mainstream converter platform intact.

By Fuel Type: Hybrid-Electric Designs Command Attention

Gasoline engines still drive 62.18% of transmission demand in 2025, but hybrid-electric powertrains lead future growth with a 13.27% CAGR through 2031, seizing an ever-larger share of the automatic transmission market. Hybrids can operate more efficiently in city cycles by decoupling engine speed from wheel speed.

BYD's DHT, featuring two electric motors and a single reduction gear, is designed to enhance vehicle performance. Following suit, Geely's Thor DHT and Toyota's fourth-generation hybrid transaxle adopt a similar approach. Meanwhile, Magna's two-speed e-axle caters to premium EVs, prioritizing high-speed efficiency. As diesel penetration declines under Euro 7 regulations and pure battery EVs adopt simpler drives, innovations in hybrids ensure the automotive automatic transmission market remains pivotal for mixed-power fleets.

By Vehicle Type: Commercial Fleets Accelerate Uptake

Passenger cars commanded 72.27% of the automotive automatic transmission market share in 2025, yet medium and heavy trucks posted the fastest growth, with an 11.56% CAGR to 2031. Allison’s 9- and 10-speed full-automatics reduce clutch wear and shorten driver training, factors prized by delivery and refuse operators.

Light commercial vans adopt 8-speed units to meet more stringent emissions rules, and Eaton–Cummins automated manuals keep traction in Class 8 tractors by balancing cost with convenience. Urbanizing emerging markets also drives compact sedans toward automated choices, keeping the automatic transmission market broad across load classes.

By Component: Torque Converter Innovations Lead

Torque converters accounted for 31.28% of the automotive automatic transmission market in 2025 and will grow at an 8.23% CAGR through 2031. Schaeffler's centrifugal pendulum absorber significantly reduces torsional vibration, allowing automakers to eliminate the need for heavy dual-mass flywheels. Valeo's arc-spring damper, housed in a compact shell, effectively handles torque demands and aligns seamlessly with the performance of downsized turbos.

Planetary gearsets now offer enhanced ratios, as demonstrated by Aisin's advanced transmission systems, which provide a broad range of capabilities. Mechatronic control is experiencing rapid growth, with solenoid arrays enabling adaptive shifting and supporting over-the-air updates. High-temperature synthetic fluids from Shell and Mobil maintain stable viscosity, ensuring the automotive automatic transmission market remains resilient under demanding operating conditions.

Geography Analysis

Asia-Pacific held 43.25% of the automotive automatic transmission market share in 2025. China, with BYD and Geely at the forefront, dominates both combustion and hybrid volumes. Urban congestion is fueling India's rising share, bolstered by Tamil Nadu's new Aisin and ZF plants under the Production-Linked Incentive scheme. Japan solidifies its position as the CVT hub through JATCO, while South Korea's Hyundai Transys expands its 8-speed DCT capacity to cater to hybrids.

North America accounts for a significant share of the automotive automatic transmission market, driven by pickup trucks opting for advanced units that balance towing capabilities with fuel regulations. Allison, with its expertise in medium-duty fully automatics, has carved out a significant niche. Meanwhile, Canada's push for a zero-emission mandate is hastening the demand for e-drives.

Europe maintains a notable market share. German giants ZF and Schaeffler cater to premium brands, helping them edge closer to the EU's stringent emissions threshold. Stellantis, hailing from France, has standardized the 8-speed automatic across its core ranges. The UK, on the other hand, is becoming a magnet for new investments in electric axles. However, the introduction of cybersecurity regulations under UNECE WP.29 R155 and R156, while elevating entry barriers, also inflates costs.

South America posts the fastest regional CAGR at 9.24% through 2031, powered by Brazil’s Rota 2030 efficiency tax break. Local assembly by Stellantis and Volkswagen reduces tariff burden and secures supply. The Middle East and Africa remain smaller but are growing as Gulf consumers favor automatics for heat resilience, while South Africa shifts taxis toward manual gearboxes.

Competitive Landscape

The top suppliers—Aisin, ZF, JATCO, Hyundai Transys, and Allison—dominate the automotive automatic transmission market, collectively accounting for a significant share of the volume. ZF offers over-the-air shift-map updates, creating a new recurring software revenue stream. Meanwhile, Chinese OEMs like BYD and Geely are internalizing DHT production, compelling established players to set up localized engineering operations close to Shenzhen and Hangzhou.

Allison is expanding into the electric axle domain with its eGen Power series, while Magna's two-speed eDrive secures a foothold in high-voltage EV programs. BorgWarner's DualTronic DCT, equipped with predictive capabilities, leverages map data to pre-select gears, significantly reducing shift lag. Schaeffler's innovative pendulum absorbers mitigate vibrations, paving the way for lighter driveline packaging.

Meeting regulatory cybersecurity standards increases unit costs, heightening technical challenges and giving financially robust suppliers an edge. In summary, the automatic transmission market finds itself at the crossroads of scale advantages and rapidly evolving technological gaps, creating opportunities for niche innovators.

Automotive Automatic Transmission Industry Leaders

Aisin Seiki Co., Ltd.

ZF Friedrichshafen AG

JATCO Ltd.

Hyundai Transys

BorgWarner Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ZF Friedrichshafen committed USD 500 million to expand its Gray Court, South Carolina plant for 8 HP Gen4 PHEV transmissions, creating 400 jobs and enabling all-electric ranges over 75 miles.

- February 2025: Allison Transmission unveiled a USD 100 million expansion of its Chennai factory to double capacity for fully automatic truck transmissions.

Global Automotive Automatic Transmission Market Report Scope

The automotive automatic transmission market report is segmented by transmission type (automatic transmission (AT)/torque converter, automatic manual (AMT), continuously variable (CVT), and dual-clutch (DCT)), fuel type (gasoline, diesel, hybrid-electric, and battery-electric (single-speed e-drive)), vehicle type (passenger cars, light commercial vehicles, and medium and heavy commercial vehicles), component (torque converter, planetary gear-set, hydraulic and mechatronic controls, and transmission fluid), and geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Automatic (AT)/Torque-Converter |

| Automated Manual (AMT) |

| Continuously Variable (CVT) |

| Dual-Clutch (DCT) |

| Gasoline |

| Diesel |

| Hybrid-Electric |

| Battery-Electric (single-speed e-drive) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Torque Converter |

| Planetary Gear-set |

| Hydraulic and Mechatronic Controls |

| Transmission Fluid |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Transmission Type | Automatic (AT)/Torque-Converter | |

| Automated Manual (AMT) | ||

| Continuously Variable (CVT) | ||

| Dual-Clutch (DCT) | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Hybrid-Electric | ||

| Battery-Electric (single-speed e-drive) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Component | Torque Converter | |

| Planetary Gear-set | ||

| Hydraulic and Mechatronic Controls | ||

| Transmission Fluid | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Automatic Transmission market by 2031?

The market is projected to reach USD 164.93 billion by 2031.

Which region leads current demand for automatic transmissions?

Asia-Pacific held 43.25% share in 2025 and maintains the lead through the forecast.

Which vehicle class shows the fastest transmission adoption?

Medium and heavy commercial vehicles are growing at an 11.56% CAGR as fleets seek uptime gains.

How are hybrids influencing transmission design?

Dedicated hybrid transmissions with dual motors enable electric launch and boost overall drivetrain efficiency, lifting hybrid demand at 13.27% CAGR.

Are software services becoming important for transmission suppliers?

Yes, firms like ZF now sell over-the-air shift-map updates, adding a recurring revenue stream beyond hardware sales.

Page last updated on: