Energy Engineering Services Outsourcing (ESO) Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

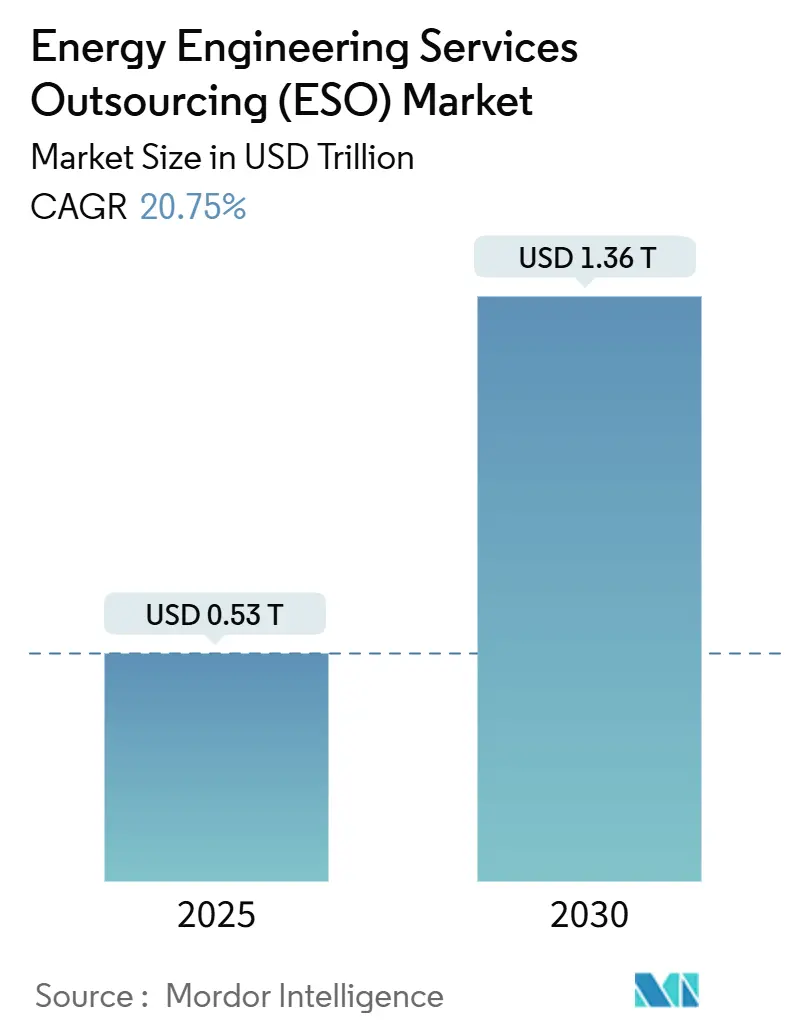

| Market Size (2025) | USD 0.53 Trillion |

| Market Size (2030) | USD 1.36 Trillion |

| Growth Rate (2025 - 2030) | 20.75% CAGR |

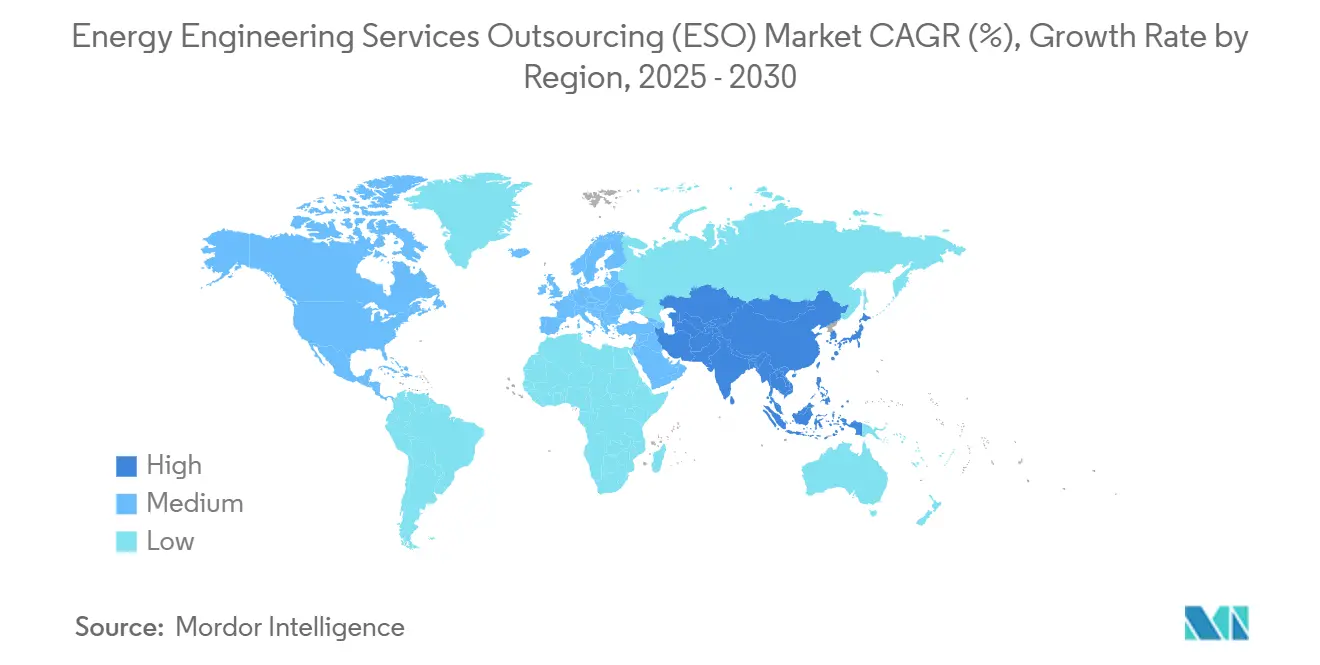

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Energy Engineering Services Outsourcing (ESO) Market Analysis by Mordor Intelligence

The Energy Engineering Services Outsourcing Market size is estimated at USD 0.53 trillion in 2025, and is expected to reach USD 1.36 trillion by 2030, at a CAGR of 20.75% during the forecast period (2025-2030).

The expansion reflects surging demand for external expertise as utilities, oil-and-gas majors, and industrial users reconfigure assets to meet decarbonization deadlines, reduce cost-to-serve, and digitalize operations. Government climate policies, escalating labor costs, and the technical complexity of integrating renewables with legacy grids are converging to fuel sustained outsourcing momentum. Asia-Pacific remains the largest buyer base thanks to massive grid buildouts, while North America records the fastest growth, driven by policy-linked incentives and private capital inflows into hydrogen, offshore wind, and grid-edge technologies. Competitive differentiation is increasingly shaped by digital twin platforms, AI-aided design tools, and domain-centric talent pools that lower time-to-commission and boost asset reliability. As provider capabilities widen from classic engineering to outcome-based, data-rich managed services, the Energy Engineering Services Outsourcing market is set for another cycle of scale consolidation and technology-led value creation.

Key Report Takeaways

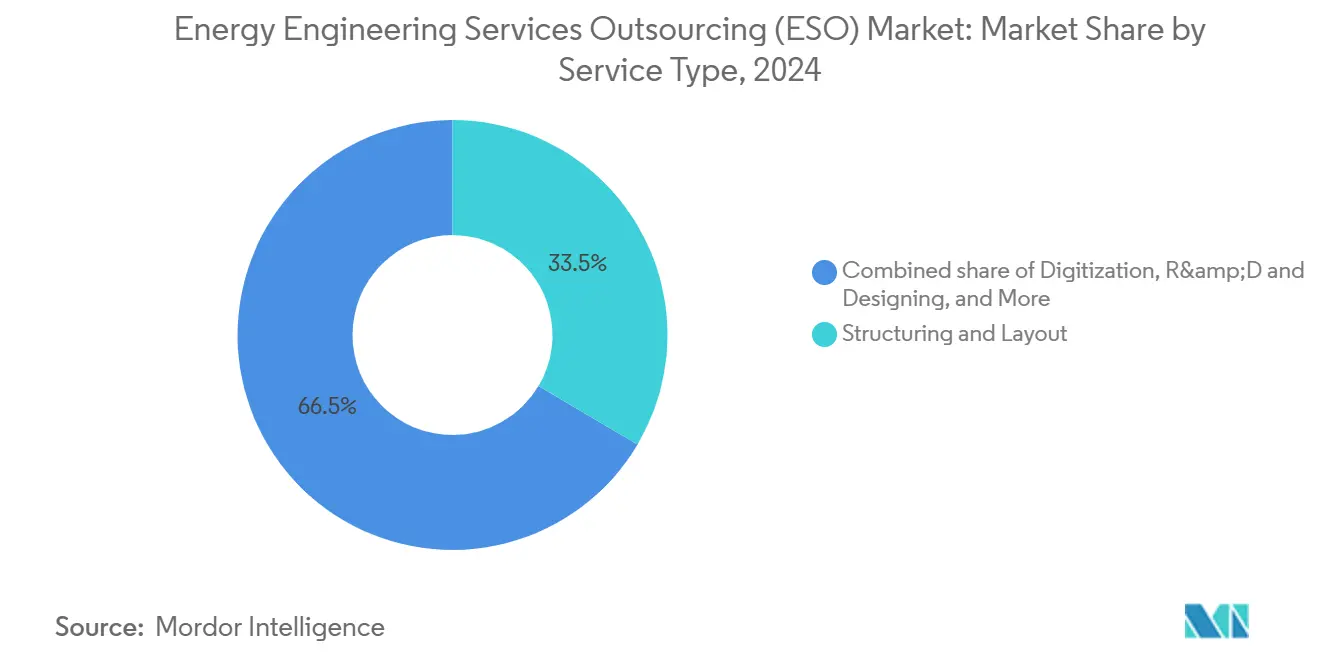

- By service type, Structuring & Layout captured 33.5% of Energy Engineering Services Outsourcing market share in 2024; Digitization is projected to grow at a 25.5% CAGR through 2030.

- By deployment model, the Onshore segment held 61.6% share of the Energy Engineering Services Outsourcing market size in 2024, while Offshore is forecast to expand at a 22.6% CAGR to 2030.

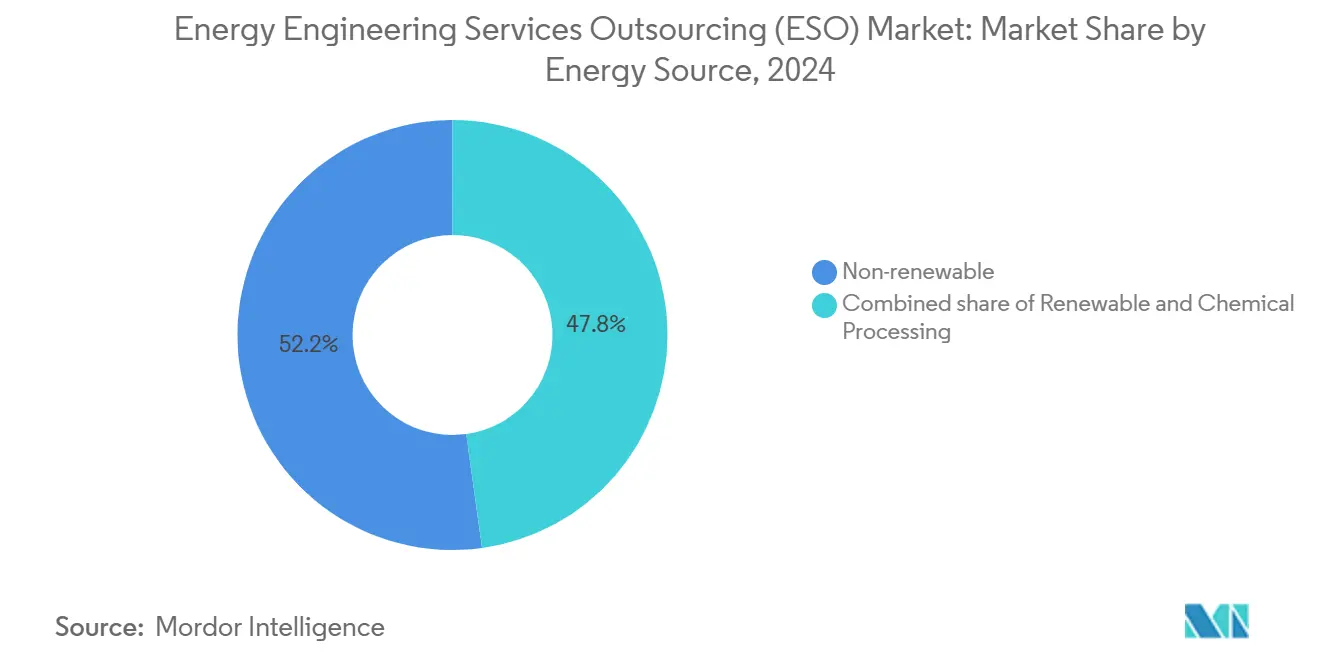

- By energy source, Non-renewable projects accounted for 52.2% of the Energy Engineering Services Outsourcing market size in 2024, and Renewable services are advancing at a 23.2% CAGR through 2030.

- By geography, Asia-Pacific led with 43.8% revenue share in 2024; North America is expected to register the highest regional CAGR of 24.8% between 2025-2030.

Global Energy Engineering Services Outsourcing (ESO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonization mandates & renewable integration | 4.20% | Global, with EU and North America leading | Long term (≥ 4 years) |

| Cost pressure & need for operational efficiency | 3.80% | Global, particularly Asia-Pacific | Medium term (2-4 years) |

| Digitalization & Industry 4.0 adoption | 3.50% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Expansion of LNG & gas infrastructure | 2.90% | North America, Middle East, APAC | Long term (≥ 4 years) |

| Subsea power-cable engineering for offshore wind clusters | 2.10% | Europe, North America, APAC coastal regions | Long term (≥ 4 years) |

| Hydrogen-ready pipeline retrofit demand | 1.80% | EU, North America, Japan, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Decarbonization Mandates Drive Renewable Integration Complexity

Binding climate legislation, such as the European Union Fit for 55 package and the United States Inflation Reduction Act, requires utilities to integrate large volumes of intermittent renewables within compressed timelines.[1]European Commission, “Fit for 55 Package,” europa.eu As grid operators lack in-house skills in power-electronics modeling, harmonics management, and hybrid storage design, they increasingly contract specialist engineering partners to co-design inverter specifications, dynamic line-rating strategies, and advanced energy-management algorithms. The complexity is magnified by the need to retrofit aging substations while maintaining reliability indices. Outsourcing providers now bundle grid-code compliance, protection studies, and commissioning services, creating a one-stop solution that accelerates project approval and reduces schedule risk. Demand is strongest in mature markets where 2030 net-zero targets trigger multibillion-dollar transmission reinforcements and flexible-resource additions.

Cost Pressures Accelerate Operational Efficiency Through Outsourcing

Global engineering wage inflation averaged 15-20% in 2024, eroding margins for asset-heavy energy companies.[2]International Labour Organization, “Global Wage Report 2024-25,” ilo.org Outsourcing converts fixed engineering overheads into variable costs and unlocks up to 60% labor-arbitrage savings when tasks shift to high-skill, lower-cost hubs in India, the Philippines, and Eastern Europe. Providers leverage scale purchasing of design software licenses and standardized work packs to compress unit cost further. Rising interest rates and commodity volatility drive CFOs to prefer outcome-based contracts that tie fee structures to performance metrics such as megawatts installed, downtime avoided, or gas compression efficiency attained. This risk-sharing model incentivizes providers to deploy proven toolkits like lean construction methods and digital workface planning to meet schedule, cost, and quality targets.

Digital Transformation Enables Advanced Engineering Service Models

Industry 4.0 building blocks—digital twins, AI-driven generative design, 5G-enabled edge analytics, and cloud collaboration—redefine how engineering knowledge is created and monetized. Virtual replicas of turbines, substations, and LNG trains enable continuous simulation of operating scenarios, allowing providers to switch from episodic EPC scopes to subscription-based performance services. Real-time condition data flows into prediction models that cut unplanned downtime by up to 30% and extend asset life. AI optimizers reduce line-route design iterations by 40%, freeing scarce senior engineers for higher-value conceptual work. Remote collaboration dissolves geographic constraints, letting domain experts in Houston, Frankfurt, and Bengaluru co-resolve design-interface clashes within shared 3D environments. Providers that embed these tools report win-rates 15 points higher in RFPs that score digital maturity.

LNG Infrastructure Expansion Creates Specialized Engineering Demand

More than 170 Mtpa of new LNG export capacity is under construction or sanctioned for startup before 2030, led by projects in Qatar, the United States, and Mozambique.[3]International Energy Agency, “Global LNG Outlook 2025,” iea.org Each terminal demands cryogenic piping layouts, boil-off gas handling studies, and stringent hazard-operability analyses that exceed the capability of most owner teams. Outsourcing firms with proven FLNG and modular mid-scale reference lists now command premium day-rates. Europe’s rapid re-gas buildout, triggered by the 2022-2024 reduction in Russian pipeline imports, has pushed average FEED cycle time below 12 months, favoring specialist houses that can fast-track procurement packages and integrate Advanced Work Packaging practices. Downstream, distributed LNG micro-plants powering island grids and remote mines open new micro-FEED niches for agile consultants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & IP concerns in outsourcing | -2.10% | Global, particularly critical infrastructure | Short term (≤ 2 years) |

| Oil-price volatility dampening CAPEX | -1.80% | Global, with higher impact in oil-dependent regions | Short term (≤ 2 years) |

| Shortage of niche renewable domain experts | -1.50% | Global, acute in developed markets | Medium term (2-4 years) |

| Geopolitical data-transfer restrictions | -1.20% | Cross-border operations, US-China-EU corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-security Concerns Limit Critical Infrastructure Outsourcing

The 2024 revision of NIST SP 800-82 elevated security baselines for industrial control systems and tightened third-party access provisions.[4]National Institute of Standards and Technology, “SP 800-82 Rev 3 Guide to Industrial Control Systems Security,” nist.gov Utilities now conduct more stringent vendor risk assessments covering supply-chain pedigree, zero-trust architectures, and software bill-of-materials disclosure. Intellectual-property leakage fears are acute in advanced control algorithms that underpin renewable curtailment minimization and voltage-ride-through compliance. Some critical-national-infrastructure owners insist on onshore engineering centers even at 25-30% cost premiums, delaying award timelines and limiting provider pools. Compliance with NERC CIP, ISO 27001, and regional privacy statutes increases transaction cost and slows cross-border file exchange, especially for multi-cloud model hosting.

Oil Price Volatility Constrains Energy CAPEX Investment

Brent crude fluctuated between USD 68-99 per barrel in 2024, prompting upstream operators to defer discretionary projects when prices skirt breakeven levels. Engineering frameworks linked to greenfield deep-water platforms, gas-processing plants, and pipeline expansions face near-term pushouts under down-price scenarios. Although renewables now absorb a rising share of global investment, traditional hydrocarbons still underpin over half of the Energy Engineering Services Outsourcing market. Price-related CAPEX cyclicality therefore ripples through provider order books, compressing utilization and pressuring billing rates. Outsourcing offers clients flexibility to scale headcount, yet shorter commitment horizons challenge providers to maintain stable talent pipelines, aggravating the scarcity of senior subsea, reservoir, and power-electronic specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digitization Transforms Traditional Engineering Models

Structuring & Layout generated 33.5% of 2024 revenue, underscoring the primacy of grid reinforcement, substation re-rating, and balance-of-plant redesign as renewables gain ground within the Energy Engineering Services Outsourcing market. The segment profits from stable project cadence across solar parks, repowered wind clusters, and gas-peaking plants that demand re-layout of conductors, transformers, and grounding systems. Yet Digitization services post a blistering 25.5% CAGR, buoyed by client appetite for AI-assisted design and digital twin lifecycle partnerships, which bundle front-end engineering with multi-year O&M analytics. Providers harness low-code platforms and knowledge graphs to accelerate rule-based sizing of electrical rooms and optimize cable trays, compressing the schedule and cost.

Growth in Digitization reshapes competitive positioning. IT-services majors now secure EPCm sub-lots by demonstrating cloud-native design environments and real-time issue-tracking dashboards. R&D & Designing engages deeply in early-stage techno-economic trade-offs for hydrogen electrolyzers and long-duration storage chemistries. Implementation & Maintenance migrates toward predictive workload orchestration as providers connect digital twins to field-level sensor streams. The Energy Engineering Services Outsourcing industry now prizes integrated digital-physical skill sets that reduce lifecycle emissions and enhance commissioning velocity.

By Deployment Model: Offshore Wind Drives Marine Engineering Surge

Onshore work retained a 61.6% share of the Energy Engineering Services Outsourcing market size in 2024, as utility-scale solar, onshore wind, and gas-fired repowers remained abundant. Familiar construction logistics, mature permitting pathways, and modular kit availability keep risk profiles modest, favoring multi-year framework agreements. Offshore, however, accelerates at a 22.6% CAGR. Deep-water leases awarded in the United States, the United Kingdom, and Japan invite complex mooring and dynamic-cable design tasks that few owner organizations can staff internally. The scarcity of heavy-lift vessel windows amplifies schedule risk, prompting owner-developers to outsource interface management, certification liaison, and electrical-system integration to specialists with North Sea pedigree.

Subsea power-cable engineering forms a high-margin niche as 525 kV HVDC export lines stretch beyond 250 km. Providers deploy integrated geotechnical-route surveys, joint-bay thermal studies, and real-time burial monitoring. Floating wind scale-up pushes engineering further toward the naval-architecture domain, with emphasis on coupled aero-hydro-servo analysis and composite tether fatigue modeling. The distinction between onshore and offshore competencies is blurring as hybrid coastal projects require synchronous substations straddling both terrains.

By Energy Source: Renewable Complexity Drives Service Innovation

Non-renewable projects still contributed 52.2% of 2024 revenue within the Energy Engineering Services Outsourcing market, dominated by LNG export trains, gas turbine upgrades, and life-extension programs for conventional thermal fleets. These scopes rely on well-established codes and procurement channels, making cost-based competition fierce. Renewable scopes, however, accelerate at a 23.2% CAGR as grid-defection risk, policy incentives, and investor ESG mandates align. Battery-coupled solar plants, hybrid wind-hydrogen hubs, and carbon-capture retrofits elevate design-interface counts, inviting specialist integration models. Chemical Processing sub-work—green hydrogen, biofuel refineries, e-methanol conversion—blurs lines between process engineering and power systems, spawning multidisciplinary consortia.

ISO 50001 certification drives meticulous metering, smart-relay specification, and continuous improvement dashboards, compounding data needs. Providers embed cybersecurity-by-design and grid-code conformance routines upfront, shortening owner approval cycles. As capacity factors and ancillary-service revenues hinge on precise controls tuning, demand rises for partners who fuse process simulation with real-time optimizer coding.

Geography Analysis

Asia-Pacific preserved a 43.8% share of the Energy Engineering Services Outsourcing market in 2024. Record-high 300 GW renewable capacity additions in China and India compelled regional TSOs to tap external firms for grid stability models, STATCOM siting, and cross-border HVDC corridor studies. Japanese utilities engaged floating-wind designers to navigate complex bathymetry and typhoon resilience. Southeast Asian IPPs awarded FEED packages for gas-to-power and hybrid solar-storage islands to regional consultancies capable of delivering cost competitiveness alongside English-language project controls.

North America posts the fastest 24.8% CAGR through 2030. The Inflation Reduction Act allocates USD 370 billion of tax credits that unlock flood-gates of green-hydrogen, offshore wind, and microgrid procurements. Developers require guidance on prevailing-wage compliance, domestic-content rules, and interconnection queue maneuvers. Canadian critical minerals policy catalyzes new transmission corridors, while Mexican nearshoring induces combined-cycle and solar expansions along the U.S. border. Engineering providers with policy-interpretation muscle and indigenous engagement experience win a decisive advantage.

Europe sustains growth under the Green Deal and REPowerEU, emphasizing energy independence. German steel decarbonization, Nordic hydrogen valleys, and Iberian floating-solar deployments demand domain experts versed in EU taxonomy, environmental permitting, and multi-lingual stakeholder interfaces. South America, the Middle East & Africa evolve from sporadic award landscapes into structured pipelines as Brazil accelerates wind-south grid ties and the UAE drives gigawatt-scale solar-to-green-ammonia schemes.

Competitive Landscape

The Energy Engineering Services Outsourcing market accommodates a widening spectrum of actors. Traditional EPC/EPCM consultancies—Jacobs, Worley, AtkinsRéalis, AFRY—retain stronghold positions in grid hard assets, LNG, and complex permitting. Digital natives like Wipro, TCS, HCLTech, and Tech Mahindra harness cloud, AI, and software-defined engineering workflows to capture brownfield optimization, digital-twin O&M, and asset-performance contracts. Mid-tier specialists carve footholds in marine cable design, hydrogen pipelines, and battery-gigafactory utilities.

Consolidation gathers pace. WSP’s USD 1.78 billion purchase of Power Engineers reinforces North American grid credentials. AtkinsRéalis reports a record USD 17.2 billion backlog after absorbing major nuclear life-extension and Puerto Rico grid-resilience assignments. ALTEN’s acquisition of Worldgrid brings nuclear-sector systems integration into its portfolio. Acquirers pursue cross-selling synergies, regional footholds, and talent de-risking. Digital capability tuck-ins, such as AFRY’s analytics-driven asset-management toolsets, address client demand for insights rather than drawings.

Technology adoption remains the decisive differentiator. Providers deploying generative AI for cable routing and clash detection reduce design hours, translating to bid-win premiums. Firms offering platform-as-a-service for virtual FATs shorten project timelines and carbon footprints. White-space opportunities thrive in emerging themes: hydrogen-ready compressor stations, carbon-capture FEED, long-duration storage commissioning, and transmission reconductoring using advanced composite conductors. Firms with proven value chain partnerships—from OEMs to cyber-security vendors—secure program integrator roles across multi-gigawatt portfolios.

Energy Engineering Services Outsourcing (ESO) Industry Leaders

Wipro

Capgemini Engineering

Jacobs Engineering

L&T Technology Services (LTTS)

Tata Consultancy Services (TCS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AtkinsRéalis selected to reinforce Puerto Rico’s transmission and distribution network under an Architecture & Engineering contract with LUMA Energy ServCo, focusing on hurricane-resilient design.

- March 2025: Hitachi Energy committed USD 250 million to expand global transformer manufacturing capacity to ease shortages linked to data-center and AI power demand.

- February 2025: AFRY appointed principal engineering partner for SSAB’s fossil-free steel plant in Luleå, a flagship industrial decarbonization project.

- January 2025: ALTEN completed the acquisition of WORLDGRID from Atos, adding EUR 170 million (USD 187 million) revenue in energy and utilities solutions.

Global Energy Engineering Services Outsourcing (ESO) Market Report Scope

| Structuring and Layout |

| Digitization |

| R&D and Designing |

| Implementation and Maintenance |

| Other Services |

| Onshore |

| Offshore |

| Captive Outsourcing |

| Third-party Outsourcing |

| Renewable |

| Non-renewable |

| Chemical Processing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Service Type | Structuring and Layout | |

| Digitization | ||

| R&D and Designing | ||

| Implementation and Maintenance | ||

| Other Services | ||

| By Deployment Model | Onshore | |

| Offshore | ||

| By Sourcing Model (Qualitative Analysis Only) | Captive Outsourcing | |

| Third-party Outsourcing | ||

| By Energy Source | Renewable | |

| Non-renewable | ||

| Chemical Processing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of Energy Engineering Services Outsourcing market by 2030?

The market is forecast to reach USD 1,363.36 billion by 2030.

Which region is expected to grow fastest through 2030?

North America is projected to post a 24.8% CAGR, the highest among all regions.

Which service type currently holds the largest revenue share?

Structuring & Layout accounts for 33.5% of 2024 revenue.

What drives the rapid rise of Digitization services?

Adoption of digital twins, AI-based design and cloud collaboration boosts Digitization at a 25.5% CAGR.

How are offshore deployments influencing outsourcing demand?

Offshore wind and subsea cable projects require specialized marine engineering, driving a 22.6% CAGR in offshore outsourcing scopes.

Which energy source segment is expanding fastest?

Renewable-energy related services are advancing at a 23.2% CAGR due to global decarbonization targets.

Page last updated on: