Automotive Gear Shift System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

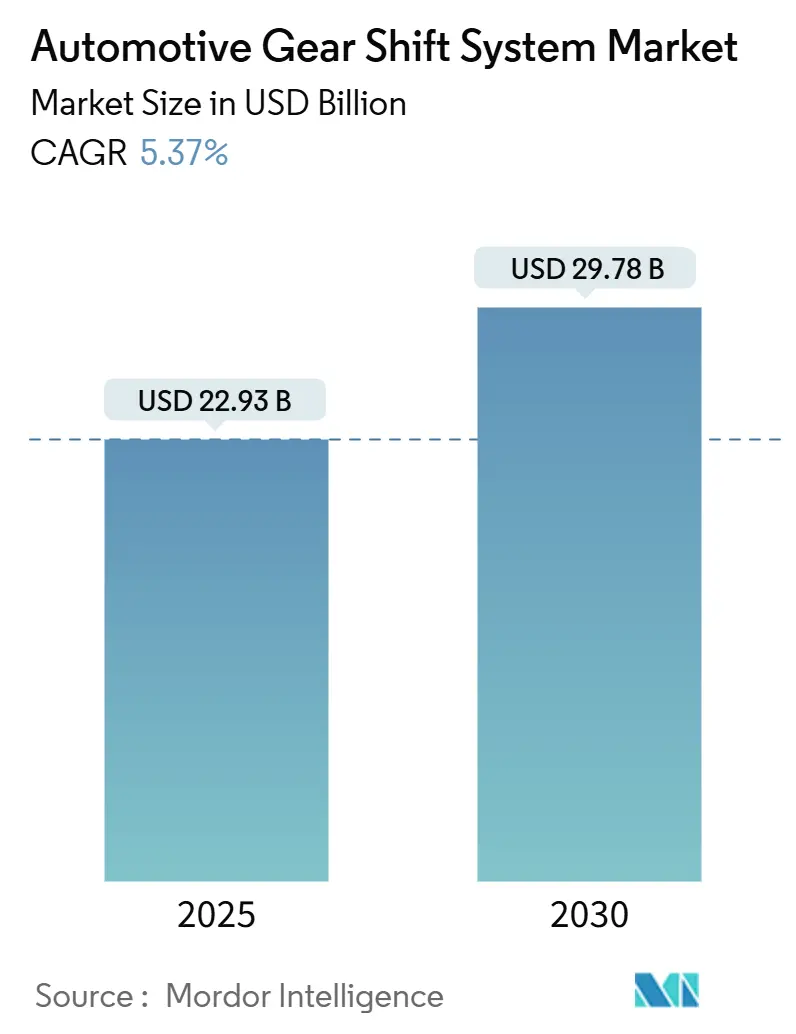

| Market Size (2025) | USD 22.93 Billion |

| Market Size (2030) | USD 29.78 Billion |

| Growth Rate (2025 - 2030) | 5.37% CAGR |

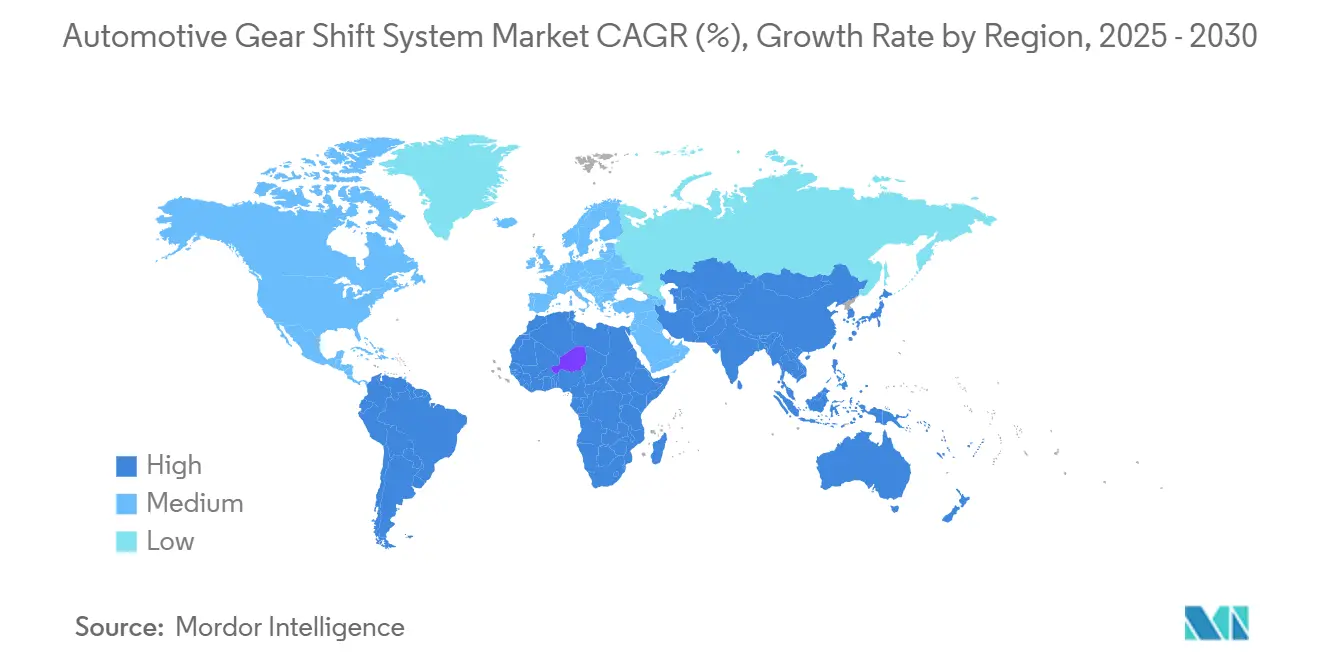

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Gear Shift System Market Analysis by Mordor Intelligence

The Automotive Gear Shift System Market size is estimated at USD 22.93 billion in 2025, and is expected to reach USD 29.78 billion by 2030, at a CAGR of 5.37% during the forecast period (2025-2030). This steady expansion mirrors the sector’s pivot toward electronically controlled transmission architectures as regulators tighten CO₂ rules and automakers roll out electrified powertrains. The European Union’s forthcoming Euro 7 framework and California’s Advanced Clean Cars II mandate for 100% zero-emission sales by 2035 accelerate the migration to shift-by-wire designs that eliminate hydraulic linkages and enable seamless integration with electric drivetrains. Semiconductor availability is gradually recovering, yet the 2021-2024 chip crunch underscored the importance of dual-sourcing strategies for transmission control units. Automakers also view over-the-air-updatable shifters as a fresh revenue stream because predictive shift algorithms can be refined remotely during a vehicle’s life cycle.

Key Report Takeaways

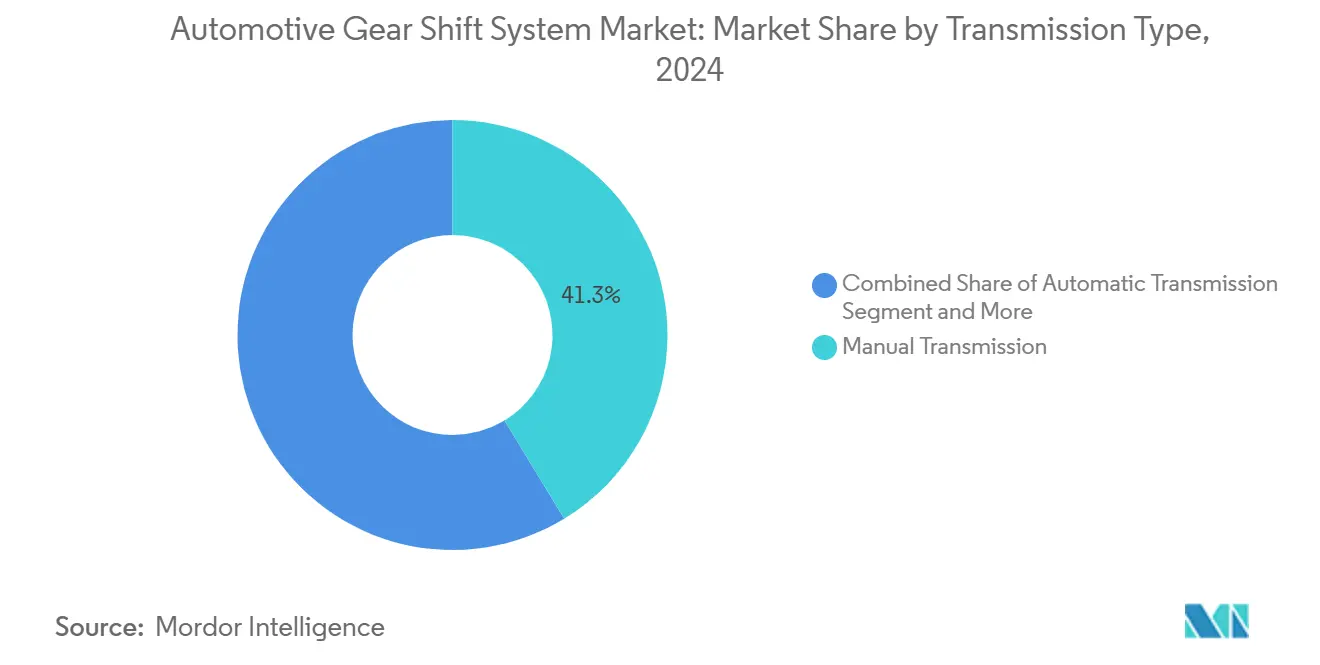

- By transmission type, manual systems held 41.27% of the automotive gear shift system market share in 2024, whereas dual-clutch transmissions are projected to register the highest 5.39% CAGR during the forecast period (2025-2030).

- By technology, electronic shifters led with 37.83% revenue share in 2024, while shift-by-wire solutions are forecast to expand at a 5.47% CAGR during the forecast period (2025-2030).

- By component, electronic control units captured 37.28% of the automotive gear shift system market size in 2024; solenoid actuators are expected to post the fastest 5.43% CAGR during the forecast period (2025-2030).

- By vehicle type, light commercial vehicles comprised 66.37% of 2024 revenue, whereas passenger vehicles are anticipated to grow at a 5.46% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific commanded 37.71% of the automotive gear shift system market share in 2024, whereas South America is forecast to expand at a 5.44% CAGR during the forecast period (2025-2030).

Global Automotive Gear Shift System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift-By-Wire Adoption | +1.2% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Global Preference Shift | +0.9% | Asia Pacific core, spill-over to South America | Long term (≥ 4 years) |

| Stricter CO₂ / Fuel-Efficiency Norms | +0.8% | EU and North America, expanding to Asia Pacific | Short term (≤ 2 years) |

| OEM Cost-Down | +0.6% | Global | Medium term (2-4 years) |

| Demand for flexible in-Cabin HMI | +0.4% | North America and EU premium segments | Long term (≥ 4 years) |

| OTA-Enabled Predictive Shift Monetization | +0.3% | North America and EU, pilot programs in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift-By-Wire Adoption in EV & ADAS Vehicles

Eliminating mechanical linkages in battery electric vehicles allows shift-by-wire systems to synchronize motor torque delivery and gear selection electronically, improving drivetrain efficiency. Fleets that deploy commercial EVs appreciate the multi-speed architectures enabled by electric shift actuators, which help maintain optimal motor RPM on gradients. Advanced driver assistance features leverage the architecture to pre-select gears based on GPS elevation and traffic flow, as demonstrated by predictive gear change trials conducted on North American heavy-duty routes. Over-the-air calibration updates further enhance performance and create subscription-based revenue models for OEMs. U.S. FMVSS 305a electrical isolation rules guide the validation of these high-voltage sub-systems [1]“FMVSS 305a Final Rule,” National Highway Traffic Safety Administration, nhtsa.gov .

Global Preference Shift Toward Automatic & DCTs

Urban congestion and driver comfort considerations steer consumers toward automatic transmissions while retaining demand for dual-clutch designs that blend performance and efficiency [2]“Next-Generation CVT-XS Production,” JATCO Ltd., jatco.co.jp . Toyota’s Direct Automatic Transmission showcases how conventional automatics can integrate DCT-like rapid shifting for better fuel economy. Fleet buyers of medium-duty trucks also migrate to automated manuals to ease driver fatigue and broaden the labor pool. This behavioral shift underpins sustained growth in the automotive gear shift system market.

Stricter CO₂ / Fuel-Efficiency Norms

Euro 7’s real-world driving emissions tests necessitate high-precision gear selection that keeps engines near their most efficient load point. EPA’s Multi-Pollutant rule encourages hybrid architectures during the transition to full electrification, heightening the need for electronically coordinated multi-mode transmissions [3]“Multi-Pollutant Emissions Standards,” United States EPA, epa.gov . In modern control units, machine-learning shift strategies adjust to individual driving styles to maintain compliance.

OEM Cost-Down Via Modular Shifter Platforms

Platform strategies that share actuators, ECUs, and software across vehicle lines reduce tooling expense and time to market. ZF’s scalable control module portfolio exemplifies how one electronics package can support automatic, dual-clutch, and CVT layouts with only minor harness changes. Standard validation reduces certification budgets, reinforcing supplier competitiveness in the automotive gear shift system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Cost | -0.7% | Asia Pacific emerging markets, South America | Short term (≤ 2 years) |

| Semiconductor Shortages | -0.6% | Global, particularly affecting Asia Pacific production | Short term (≤ 2 years) |

| Reliability Issues | -0.4% | Middle East, Africa, extreme climate regions | Medium term (2-4 years) |

| Cyber-Security Risk On CAN/Shift-By-Wire | -0.3% | North America and EU regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High System Cost in Entry-Level Vehicles

In markets like Southeast Asia and Latin America, the introduction of electronic shifters, equipped with sensors, motors, and wiring, escalates material costs. This makes them less appealing for cost-sensitive A- and B-segment vehicles, where affordability is a key purchasing factor. Additionally, a scarcity of skilled technicians for diagnostics in rural locales heightens the perceived ownership burden, as consumers may face challenges in accessing timely repairs and maintenance. This further solidifies the consumer's preference for traditional manual transmissions, which are simpler and more cost-effective to maintain in these regions.

Semiconductor Shortages for ECUs

From 2021 to 2024, the global semiconductor shortage underscored the industry's reliance on mature 40-nanometer processes, predominantly in East Asia, especially for automotive needs. Microcontrollers used in gear-shift control units are frequently the same ones found in body electronics. This overlap means that disruptions in production can ripple through various vehicle models, leading to delays and increased costs for manufacturers. Suppliers are now dual-sourcing and pre-qualifying semiconductor dies in response to this vulnerability. These strategies aim to enhance supply chain resilience and reduce single-source dependency. Yet, with significant capacity expansion not anticipated until 2026, the prospects for a swift recovery in growth remain constrained, leaving the industry to navigate ongoing challenges in the short term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transmission Type: Automation Pressure on Manual Dominance

Manual assemblies retained a 41.27% share of the automotive gear shift system market in 2024, sustained by price advantages in emerging economies. Nonetheless, automatic and dual-clutch options drew urban buyers who navigate stop-start traffic daily. The dual-clutch units segment is expected to outpace all others at 5.39% CAGR during the forecast period (2025-2030) because they couple fuel savings with sporty acceleration, which is critical for Euro 7 compliance and performance branding.

The gradual phase-out of stick-shift models in North America and Europe demonstrates how consumer comfort reshapes drivetrain portfolios, while fleet operators prize automated manuals that lower driver-training time. OEMs collaborate with software specialists to fine-tune clutch-to-clutch transitions, squeezing emissions margins without hardware redesign. These converging trends ensure automation gains share through 2030, though manuals remain relevant in low-cost geographies.

By Technology: Electronic Systems Lead Shift-By-Wire Evolution

Electronic architectures captured a 37.83% share of the automotive gear shift system market in 2024, confirming the sector’s turn from mechanical linkages. The fastest-growing slice is shift-by-wire, climbing 5.47% CAGR during the forecast period (2025-2030), as electric vehicles delete hydraulic circuits entirely. While mechanical systems still lead the entry-level segment, automakers are intensifying efforts to lighten drivetrains. This shift paves the way towards lighter, electronically controlled actuators. These advanced systems, equipped with integrated fail-safe logic and redundant sensors, are designed to comply with the rigorous ISO 26262 functional safety standards. With the growing adoption of advanced driver-assistance systems (ADAS), drive-by-wire technologies are stepping up as the digital backbone, managing longitudinal and lateral vehicle controls and producing enhanced data streams for AI-driven fleet management.

By Component: ECU Dominance Drives System Intelligence

Due to rising software content per vehicle, electronic control units represented a 37.28% share of the automotive gear shift system market in 2024. High-speed multicore processors enable edge machine-learning algorithms that tailor shift maps to driver behavior.

Solenoid actuators will log the quickest 5.43% CAGR during the forecast period (2025-2030), because they remain vital for clutch and valve actuation in dual-clutch and automatic boxes. Suppliers integrate position sensing to reduce part count and simplify diagnostics. Concurrently, gear levers evolve into minimalist selectors communicating via CAN-FD, reinforcing the transition from mechanical to electronic command.

By Vehicle Type: Commercial Vehicles Drive Market Scale

Light commercial vehicles contributed a 66.37% share of the automotive gear shift system market in 2024, buoyed by e-commerce parcel volumes that magnify duty cycles. Fleet managers embrace automated manuals that reduce fuel bills in city delivery routes. Passenger cars are expected to grow with a 5.46% CAGR during the forecast period (2025-2030) as automated and shift-by-wire conveniences trickle down to mainstream segments. Electrified SUVs combine two-speed e-axles with torque vectoring for traction control, showcasing how innovation in commercial platforms migrates to consumer lines and fuels the overall automotive gear shift system market.

Geography Analysis

Asia-Pacific held a 37.71% share of the automotive gear shift system market in 2024, owing to China’s vast car production base and India’s commercial vehicle growth. Regional suppliers benefit from proximity to semiconductor fabs in Taiwan and South Korea, ensuring quicker ECU lead times. Japan’s technology leadership in continuously variable transmissions further anchors the supply chain.

South America is projected to clock a 5.44% CAGR during the forecast period (2025-2030). Brazil’s resurgent assembly plants and Argentina’s incentives for local sourcing encourage the adoption of electronic shifters in export-grade pickups. Ethanol-compatible engines require dynamic shift scheduling to match fluctuating calorific values, prompting investment in smarter control units. Europe remains a technology pacesetter as Euro 7 rules catalyze efficient multi-mode transmissions. German OEMs collaborate with Tier-1 suppliers to standardize modular dual-clutch gearsets across platforms, while Italy’s supercar makers pioneer shift logic that balances emissions caps with brand-signature performance. Over-the-air re-flash capability becomes standard to comply with future real-world driving compliance checks.

North America’s early move into shift-by-wire for pickups and SUVs supports stable demand. The EPA rule package incentivizes hybrid pickups that need specialized power-split gearboxes, reinforcing domestic ECU output. Canada’s cross-border logistics sector favors automated manuals for long-haul rigs, boosting unit volumes. The Middle East & Africa offer emerging upside. Gulf nations’ construction booms spur orders for automated heavy trucks, yet harsh temperatures test actuator seals and electronics. Regional assembly in Turkey and South Africa provides staging points for sub-Saharan distribution, albeit at lower volume bases relative to other continents.

Competitive Landscape

The automotive gear shift system market is moderately fragmented. ZF Friedrichshafen, BorgWarner, and Continental leverage control-software depth and global production footprints to win OEM platforms [4]“Annual Report 2024,” ZF Group, zf.com . American Axle’s takeover of Dowlais Group in February 2025 exemplifies vertical integration as suppliers chase e-axle scale.

Software competence differentiates leaders. Continental’s unified BASIS controller manages shifting, braking, and propulsion torque on one silicon platform, reducing wiring by 12 m per vehicle. BorgWarner’s compact dual-motor eDCT for plug-in hybrids highlights mechanical-software symbiosis.

Niche entrants target specialist verticals. RENK’s naval and military gearboxes offer insulation from passenger-car cycles, while emerging Asian players focus on low-cost mechanical shifters for entry-level A-segment cars. As electrification widens, partnerships between inverter suppliers and transmission makers proliferate to deliver turnkey e-drive modules.

Automotive Gear Shift System Industry Leaders

Robert Bosch GmbH

Continental AG

BorgWarner Inc.

ZF Friedrichshafen AG

JTEKT Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Allison Transmission announced a USD 2.7 billion deal to acquire Dana’s Off-Highway business, broadening exposure to mining and construction drivetrains.

- April 2025: Hendrickson and Voith formed a strategic alliance to co-develop electric suspensions and axle-integrated drives for zero-emission trucks.

- April 2025: Garrett Motion and Shaanxi HanDe Axle secured a multi-year production award to supply electric beam axles for medium and heavy trucks beginning in 2027.

Global Automotive Gear Shift System Market Report Scope

| Manual Transmission |

| Automatic Transmission |

| Semi-Automatic Transmission |

| Dual-Clutch Transmission (DCT) |

| Electronic Gear Shift System |

| Hydraulic Gear Shift System |

| Mechanical Gear Shift System |

| Shift-by-Wire |

| Gear Lever |

| Transmission Control Module (TCM) |

| Electronic Control Unit (ECU) |

| Shift Sensors |

| Solenoid Actuator |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Transmission Type | Manual Transmission | |

| Automatic Transmission | ||

| Semi-Automatic Transmission | ||

| Dual-Clutch Transmission (DCT) | ||

| By Technology | Electronic Gear Shift System | |

| Hydraulic Gear Shift System | ||

| Mechanical Gear Shift System | ||

| Shift-by-Wire | ||

| By Component | Gear Lever | |

| Transmission Control Module (TCM) | ||

| Electronic Control Unit (ECU) | ||

| Shift Sensors | ||

| Solenoid Actuator | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive gear shift system market in 2025?

It stands at USD 22.93 billion, reflecting the baseline for the current forecast period.

What CAGR is projected for automotive gear shift systems through 2030?

The market is expected to grow 5.37% annually between 2025 and 2030.

Which transmission technology shows the fastest growth?

Shift-by-wire is forecast to advance at a 5.47% CAGR from 2025 to 2030.

Which vehicle category dominates revenue?

Light commercial vehicles held 66.37% of 2024 revenue due to e-commerce logistics demand.

What region will grow the quickest?

South America is projected to register a 5.44% CAGR through 2030.

Who are the leading suppliers in this space?

ZF, BorgWarner, Continental, and Allison Transmission headline the supplier landscape with integrated electronic control portfolios.

Page last updated on: