Automotive Touch Screen Control Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

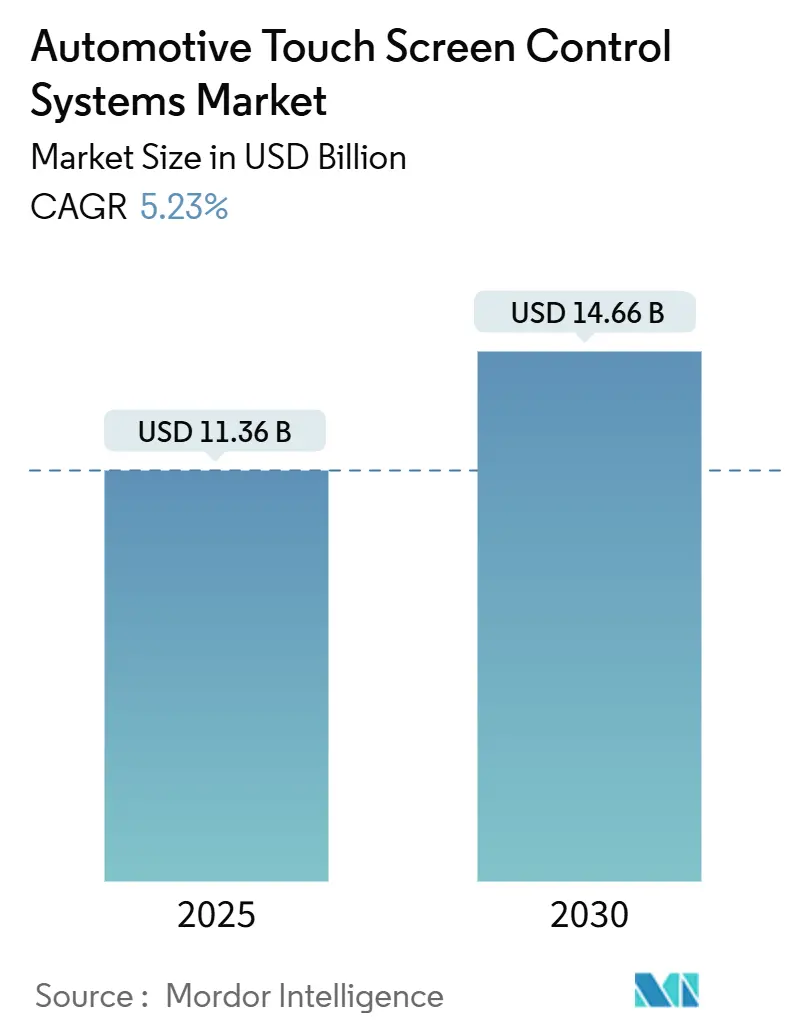

| Market Size (2025) | USD 11.36 Billion |

| Market Size (2030) | USD 14.66 Billion |

| Growth Rate (2025 - 2030) | 5.23% CAGR |

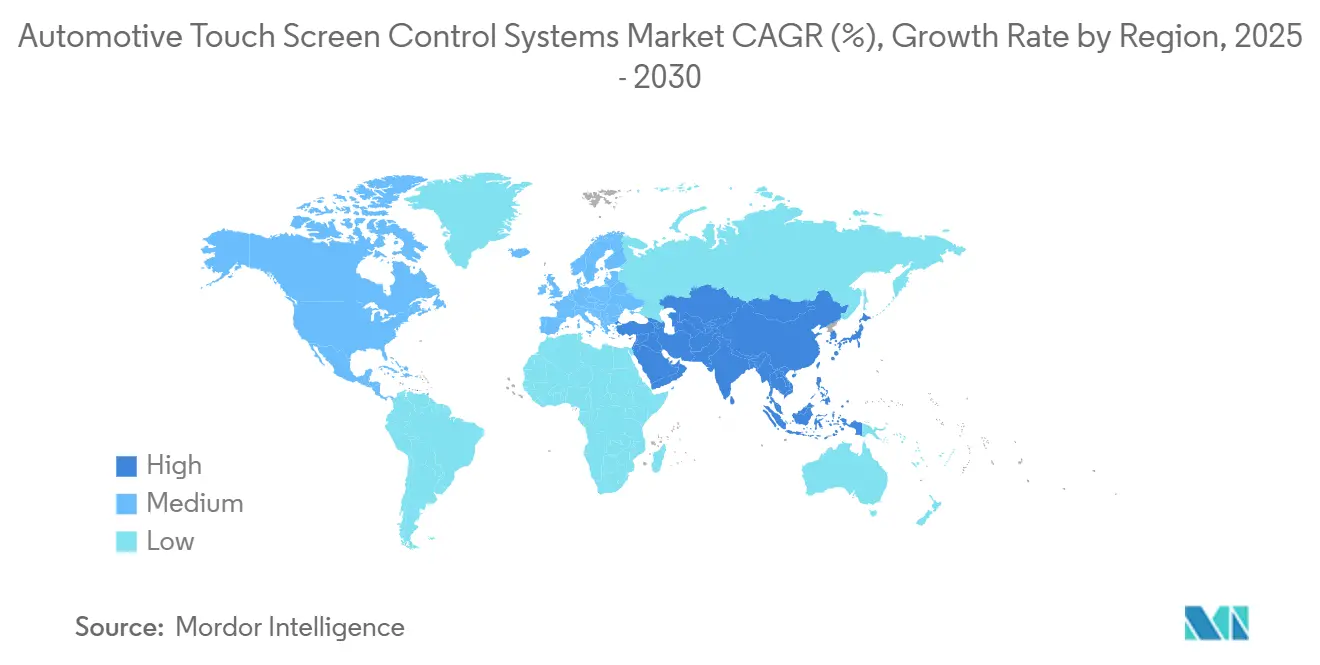

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Touch Screen Control Systems Market Analysis by Mordor Intelligence

The automotive touch screen control systems market size stands at USD 11.36 billion in 2025 and is forecast to reach USD 14.66 billion by 2030, reflecting a 5.23% CAGR during the forecast period (2025-2030). Accelerating electrification, consumer demand for smartphone-style cockpit experiences, and falling hardware costs underpin this steady expansion. In the electric and premium vehicle segments, larger in-vehicle displays have become prominent status symbols, underscoring a consumer preference for high-tech interiors. Dominating the landscape, capacitive touch technology stands out for its unmatched usability and responsiveness. The Asia-Pacific region, with China at the forefront, is spearheading this adoption, buoyed by a surge in electric vehicle production. Worldwide, automakers are pivoting towards software-defined vehicle architectures, enabling regular over-the-air updates that enrich user experience and offer feature flexibility. Yet, challenges loom: supply constraints on specialty glass and heightened regulatory scrutiny on driver distraction are shaping design decisions and influencing cost structures.

Key Report Takeaways

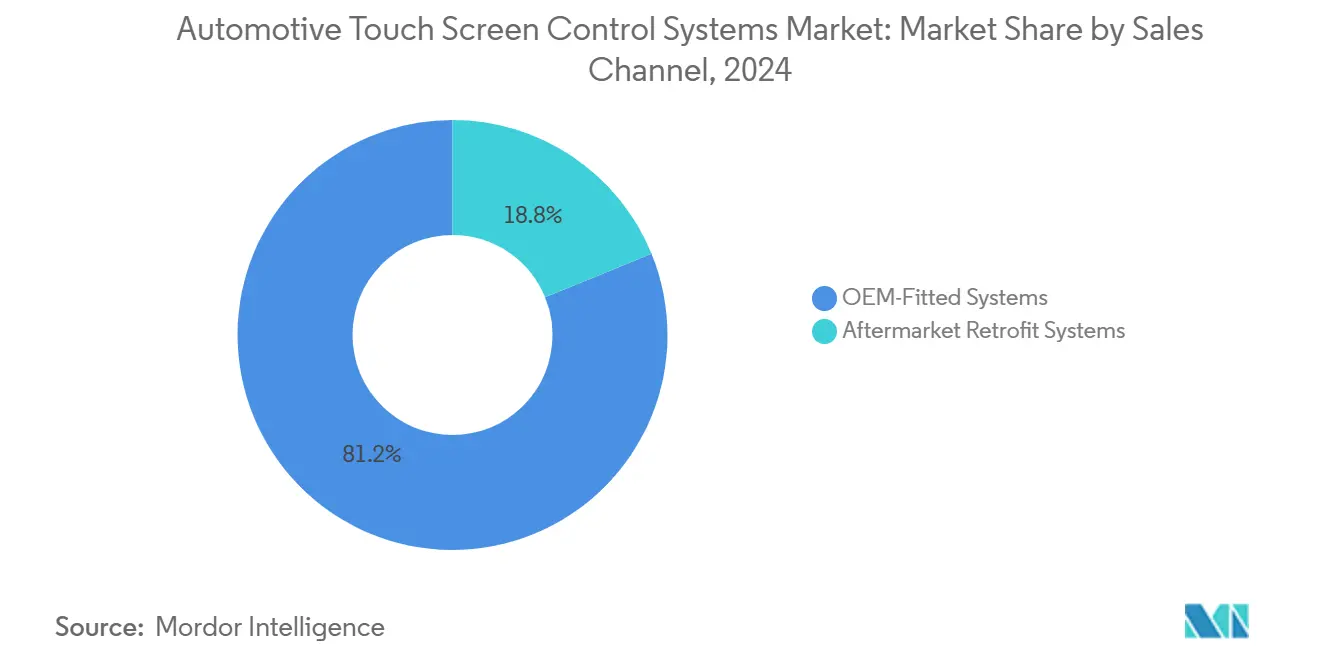

- By sales channel, OEM-fitted systems accounted for 81.17% of the automotive touch screen control systems market share in 2024, while the aftermarket retrofit segment is projected to expand at a 7.12% CAGR during the forecast period (2025-2030).

- By screen size, 9-to-15-inch displays dominated 2024 revenue with a 62.34% share of the automotive touch screen control systems market; displays above 15 inches are poised for the fastest 8.98% CAGR during the forecast period (2025-2030).

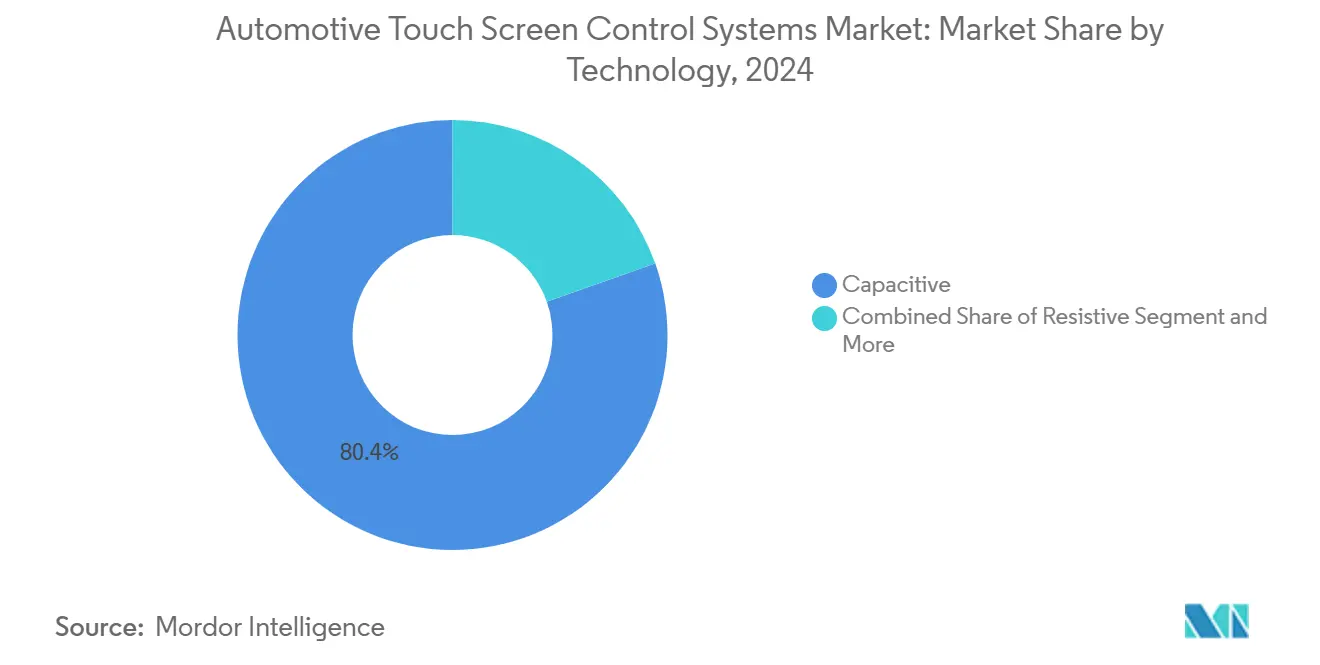

- By technology, capacitive solutions retained an 80.41% share of the automotive touch screen control systems market in 2024, whereas surface acoustic wave screens are set to grow at a 7.65% CAGR during the forecast period (2025-2030).

- By application, passenger cars captured 73.19% of 2024 revenue of the automotive touch screen control systems market in 2024; light commercial vehicles are registering the highest 6.11% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific captured 34.69% market share of the automotive touch screen control systems market in 2024 and is projected to grow at a 6.39% CAGR during the forecast period (2025-2030).

Global Automotive Touch Screen Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Larger Infotainment Displays | +1.8% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Falling Unit Costs | +1.2% | Global, particularly benefiting emerging markets | Short term (≤ 2 years) |

| Regulatory Mandates | +0.9% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Consumer Preferences | +0.8% | Global, with higher adoption in developed markets | Medium term (2-4 years) |

| OTA-Upgradable Architectures | +0.7% | North America and EU early adoption, APAC following | Long term (≥ 4 years) |

| Antiviral / Antimicrobial Touch Coatings | +0.3% | Global, with premium segment focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Larger Infotainment Displays in EVs and Premium Vehicles

Electric brands brandish vast screens as tangible proof of digital sophistication. Mercedes-EQS debuted a 56-inch hyperscreen, and BMW’s curved 14.9-inch console on the iX set a benchmark for intuitive, multi-surface control[1]“iX Display Technology Integration,” BMW Group, bmwgroup.com. Mainstream EV makers such as BYD and Tesla now standardize 15-inch-plus centers to host HVAC, navigation, and diagnostics in a single pane. Consolidating functions slashes wiring harnesses and assembly time, while the capacity to unlock features over the air expands post-sale revenue horizons. These advantages swell average display size norms and cement the automotive touch screen control systems market as a key battleground for user-experience differentiation.

Falling Unit Costs of Capacitive Touch Panels and Controllers

Scale economies from smartphones continue spilling over into automotive, pushing panel prices down since 2022. In-cell touch integration eliminates extra sensor layers, curbing material use and assembly time. Stabilizing controller IC pricing after semiconductor shortages further relieves bill-of-materials pressure, allowing larger displays to migrate into mid-tier trims without sacrificing profit. Low-cost modules, especially from APAC fab lines, accelerate the standardization of multi-gesture interfaces across mainstream models.

Regulatory Mandates for Camera / Infotainment Integration

North American and European safety agencies now require backup-camera images and advanced driver-assistance visualizations to appear on central screens. NHTSA’s Phase 3 driver-distraction guidelines limit visual-manual tasks to 2-second glances, effectively dictating display size, layout, and tactile response[2]“Driver Distraction Guidelines Phase 3,” National Highway Traffic Safety Administration, nhtsa.gov. UNECE rules take a similar stance for automated driving features. Larger, higher-resolution touch screens that clearly render complex overlays become mandatory for compliance, removing cost-cutting incentives that once favored smaller panels.

Consumer Preference for Smartphone-Like HMI

Drivers expect pinch-to-zoom maps, carousel menus, and personal-assistant voice integration mirroring daily phone usage. Continental’s Emotional Cockpit platform adapts layouts to user habits, while BMW’s Intelligent Personal Assistant continually adds voice intents through software updates. High-resolution screens with fine touch granularity and robust processing capacity are therefore essential, tilting procurement toward premium suppliers able to guarantee smartphone-grade responsiveness under harsh automotive conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration and Validation Cost | -0.8% | Global, particularly affecting smaller OEMs | Medium term (2-4 years) |

| Driver-Distraction Regulations | -0.6% | North America and EU primarily | Long term (≥ 4 years) |

| Supply-Chain Risk | -0.5% | Global, with APAC manufacturing concentration | Short term (≤ 2 years) |

| EMI Issues | -0.3% | Global EV markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration and Validation Cost

Automotive touch interfaces undergo stringent testing for thermal resilience, vibration tolerance, and electromagnetic compatibility, standards that far surpass those in consumer electronics. Obtaining functional safety certification for screens managing vehicle operations not only prolongs development timelines but also escalates costs. These largely fixed expenses present hurdles for smaller automakers, whereas high-volume manufacturers can more readily absorb them and sustain profitability. The melding of various in-vehicle networks, including CAN, LIN, and Ethernet, amplifies system complexity, necessitating specialized facilities and tools that only a select few suppliers can competitively provide.

Driver-Distraction Regulations Limit Screen Interaction

Regulatory bodies in the United States and Europe are tightening controls on driver distractions, mandating swift and minimal visual engagement for crucial in-vehicle tasks. In response, user experience teams are refining interface designs, emphasizing primary functions, and delegating less critical tasks to voice commands or passengers. Consequently, design cycles are evolving to be more iterative, and the potential to profit from expansive entertainment screens is diminishing. Although advancements such as context-aware interfaces and haptic feedback provide some respite, they simultaneously escalate software intricacies and development challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sales Channel: OEM Integration Sustains Command

OEM-fitted systems held 81.17% of revenue of the automotive touch screen control systems market in 2024, reflecting automakers’ preference for seamless cockpit design and single-supplier accountability. The automotive touch screen control systems market size for OEM programs is climbing as brands embed larger, richer displays into almost every trim. Factory installs secure CAN and Ethernet gateway access, enabling over-the-air feature sales that the retrofit trade cannot match. Warranty alignment and crash-worthiness validation further reinforce OEM dominance.

Aftermarket installers, however, ride a 7.12% CAGR as owners of legacy vehicles chase connectivity upgrades.General Motors (GM) plan to phase out the Apple CarPlay and Android Auto technologies, which allow drivers to sidestep a vehicle's native infotainment systems. GM is pivoting towards proprietary infotainment systems, co-developed with Google, for its upcoming electric vehicles. This shift is pushing many drivers towards third-party retrofit kits that maintain smartphone mirroring capabilities. While enhanced harness adapters and dropping display prices make conversions easier, these retrofitted systems often lag behind factory-installed ones due to restricted data-bus access. Meanwhile, specialized shops that provide integrated camera and parking assistance are strategically positioned to tap into this segment of the automotive touch screen control systems market.

By Screen Size: Large Formats Ascend Premium Hierarchy

Displays sized 9-15 inches controlled 62.34% share of the automotive touch screen control systems market in 2024, balancing usability and cost for mass-market interiors. The segment’s automotive touch screen control systems market share stems from ample real estate for navigation and media while fitting conventional dashboard hardpoints. Economies of scale in LCD and OLED fabrication continue to drive panel affordability, supporting OEM plans to upgrade base trims.

Screens exceeding 15 inches post an 8.98% CAGR to 2030, propelled by pillar-to-pillar concepts. Cadillac’s 33-inch curved OLED and Lincoln’s 48-inch panorama prove that immersive surfaces can host clusters, infotainment, and passenger entertainment concurrently. Cost-per-square-inch metrics improve each production cycle, bringing once-exclusive formats into near-luxury crossovers. Smaller sub-9-inch displays endure primarily in cost-sensitive fleets and basic commercial cabins, where touch targets stay minimal and glove compatibility trumps aesthetics.

By Technology: Capacitive Leadership Confronts SAW Upswing

Capacitive modules owned 80.41% revenue of the automotive touch screen control systems market in 2024, their dominance built on multi-finger gestures, durability, and supply-chain maturity. The automotive touch screen control systems market size for capacitive units is growing, owing to in-cell architectures that integrate sensor and display layers, trimming bezels, and reducing weight. Force-sensing capacitive variants add haptics without moving parts, further lifting perceived quality.

Surface acoustic wave (SAW) registers a 7.65% CAGR, carving share in commercial and industrial vehicles where thick gloves and dirt challenge capacitive detection. SAW’s ability to read touches through protective glass suits construction trucks, agricultural machinery, and military transports. Cost declines as fabs adopt smaller transducer pitch and automated calibration. Resistive and infrared remain confined to low-end dashboards and extreme-temperature roles, with limited R&D inflows.

By Application: Commercial Vehicles Accelerate Digital Adoption

Passenger cars commanded 73.19% revenue of the automotive touch screen control systems market in 2024, standardizing touch functions from seat massage to energy management on EVs. The automotive touch screen control systems market size for passenger cars is projected to hit USD 10.7 billion by 2030, buoyed by luxury trickle-down and software-enabled personalization. OEMs leverage touch dashboards to simplify cockpit layouts, replacing clusters of physical switches with contextual menus.

Light commercial vehicles (LCVs) grow fastest at 6.11% CAGR, spurred by last-mile logistics and electrification mandates that reward cockpit digitization. Volkswagen’s 2025 Crafter refresh introduced a 10.4-inch display linked to fleet-management analytics, allowing route updates and driver scorecards. Medium and heavy trucks adopt touch solutions more cautiously, citing cost and reliability, yet remote-diagnostics portals and regulatory e-logging requirements gradually tip ROI equations.

Geography Analysis

Asia-Pacific leads with 34.69% share of the automotive touch screen control systems market in 2024 and a brisk 6.39% CAGR through 2030, powered by China’s EV volume and supportive incentives. Touch screens ride the region’s vast battery-electric output, with domestic suppliers scaling panels and controllers at globally competitive prices. Southeast Asia benefits from reshored electronics assembly and rising middle-class car ownership that prioritizes digital amenities. Investments by battery and display giants speed localization of entire cockpit stacks, insulating OEMs from cross-ocean freight volatility.

North America retains a sizeable slice of the automotive touch screen control systems market as federal tax credits and expanding charging infrastructure lure buyers toward electric SUVs and pickups. NHTSA’s backing-camera and ADAS-display rules cement demand for larger screens, while infotainment feature bundling drives subscription revenue. Supply issues for advanced driver-monitoring cameras and low-iron cover glass remain growth throttles but are expected to ease as domestic fabs come online between 2026 and 2027.

Europe mirrors North American CAGR at 4.55%, albeit under stricter carbon targets. Automakers there must balance sustainability metrics with premium infotainment expectations. UNECE mandates around automated lane-keeping visualization support continued screen upsizing, yet austerity in entry segments tempers total dollar growth. Regional Tier-1s push software-defined platforms that separate hardware cycles from UI innovation, aligning with consumer appetite for frequent updates without new-model purchases.

Competitive Landscape

The automotive touch screen control systems market is moderately concentrated. Collectively, the top five major players capture a significant share, yet leaving room for mid-tier challengers and niche specialists. Strategic activity tilts toward vertical integration: Continental expanded display backplane capacity, while Visteon teamed with Qualcomm to bundle AI cockpit chips and Android-based UX stacks. Deal flow shows suppliers diversifying into cover-glass coating and touch-controller firmware to secure value beyond commoditized panels.

Technology differentiation is pivoting from pure hardware to life-cycle software. Over-the-air update capability, cyber-security hardening, and app-store ecosystems increasingly shape RFQ scoring. Suppliers offering turnkey cockpit domains that merge infotainment, ADAS visualization, and cluster functions gain favor with OEMs looking to trim ECU count. Patent filings around EMI shielding for 800-V EV architectures and tactile feedback algorithms signal future battlefields.

Aftermarket brands chase gaps left by OEM lock-in. Firms specializing in retrofit kits exploit willingness of existing vehicle owners to pay for Apple CarPlay or Android Auto, especially after select makers blocked native phone mirroring. Partnerships with installer chains widen reach, while white-label units for ride-hailing fleet refreshes present volume upside. Cost-optimized SAW and resistive variants serve work trucks and agricultural vehicles where glove-friendly input and ruggedness trump elegance.

Automotive Touch Screen Control Systems Industry Leaders

Continental AG

Robert Bosch GmbH

Panasonic Holdings Corporation

DENSO Corporation

Visteon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hyundai Motor Group unveiled the Pleos mobility software platform featuring Pleos Connect, an Android Automotive-based infotainment system anchored by a 15.6-inch touch screen and extensive UI customization.

- March 2025: ChangAn launched its all-electric Deepal S07 in Europe, equipped with a Snapdragon 8155-powered 15.6-inch adjustable touch screen allowing seamless Apple CarPlay and Android Auto connectivity.

- January 2025: BMW previewed its production-ready BMW iDrive with Panoramic Vision at CES 2025, running on the new BMW Operating System X and slated for rollout in late-2025 models.

Global Automotive Touch Screen Control Systems Market Report Scope

| OEM-Fitted Systems |

| Aftermarket Retrofit Systems |

| Below 9 inches |

| 9 to 15 Inches |

| Above 15 Inches |

| Capacitive |

| Resistive |

| Infrared |

| Surface Acoustic Wave |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Sales Channel | OEM-Fitted Systems | |

| Aftermarket Retrofit Systems | ||

| By Screen Size | Below 9 inches | |

| 9 to 15 Inches | ||

| Above 15 Inches | ||

| By Technology | Capacitive | |

| Resistive | ||

| Infrared | ||

| Surface Acoustic Wave | ||

| By Application | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive touch screen control systems market in 2025?

The market stands at USD 11.36 billion in 2025 and is on course for USD 14.66 billion by 2030.

What CAGR is expected for automotive touch screens over 2025-2030?

A steady 5.23% CAGR is projected for the period.

Which region leads current adoption?

Asia-Pacific holds 34.69% share in 2024 and shows the fastest 6.39% CAGR through 2030.

What screen size segment is growing fastest?

Displays larger than 15 inches register the quickest 8.98% CAGR due to luxury and EV demand.

What factor most constrains future growth?

High integration and validation costs, especially for smaller OEMs, shave a significant portion from potential CAGR.

Page last updated on: