Automotive Smart Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

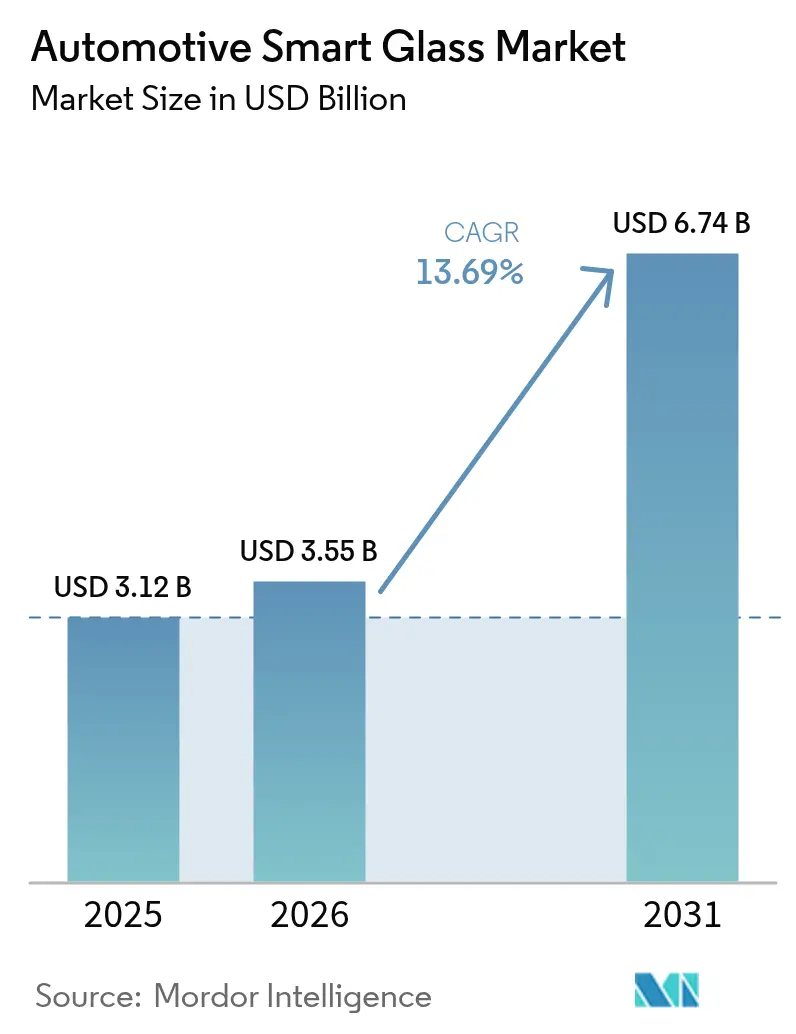

| Market Size (2026) | USD 3.55 Billion |

| Market Size (2031) | USD 6.74 Billion |

| Growth Rate (2026 - 2031) | 13.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Smart Glass Market Analysis by Mordor Intelligence

The automotive smart glass market size in 2026 is estimated at USD 3.55 billion, growing from 2025 value of USD 3.12 billion with 2031 projections showing USD 6.74 billion, growing at 13.69% CAGR over 2026-2031. This growth trajectory is anchored in the rapid electrification of premium vehicles, the broader deployment of advanced driver assistance systems, and new cabin-comfort regulations emphasizing glare reduction and thermal efficiency. Continued price declines for electrochromic modules, paired with faster-switching suspended particle devices, are reshaping OEM design choices and shortening innovation cycles. Automakers increasingly seek large-area panoramic roofs and HUD-ready windshields that combine dimmability with weight savings. At the same time, suppliers race to secure indium tin oxide reserves and to certify alternative transparent conductors. Competitive intensity remains moderate yet rising, as integrated module offerings promise more straightforward final assembly and help tier-1 suppliers defend margins. In parallel, retrofit demand emerges from fleet operators who view smart glass as a quick route to boost passenger comfort and differentiate services.

Key Report Takeaways

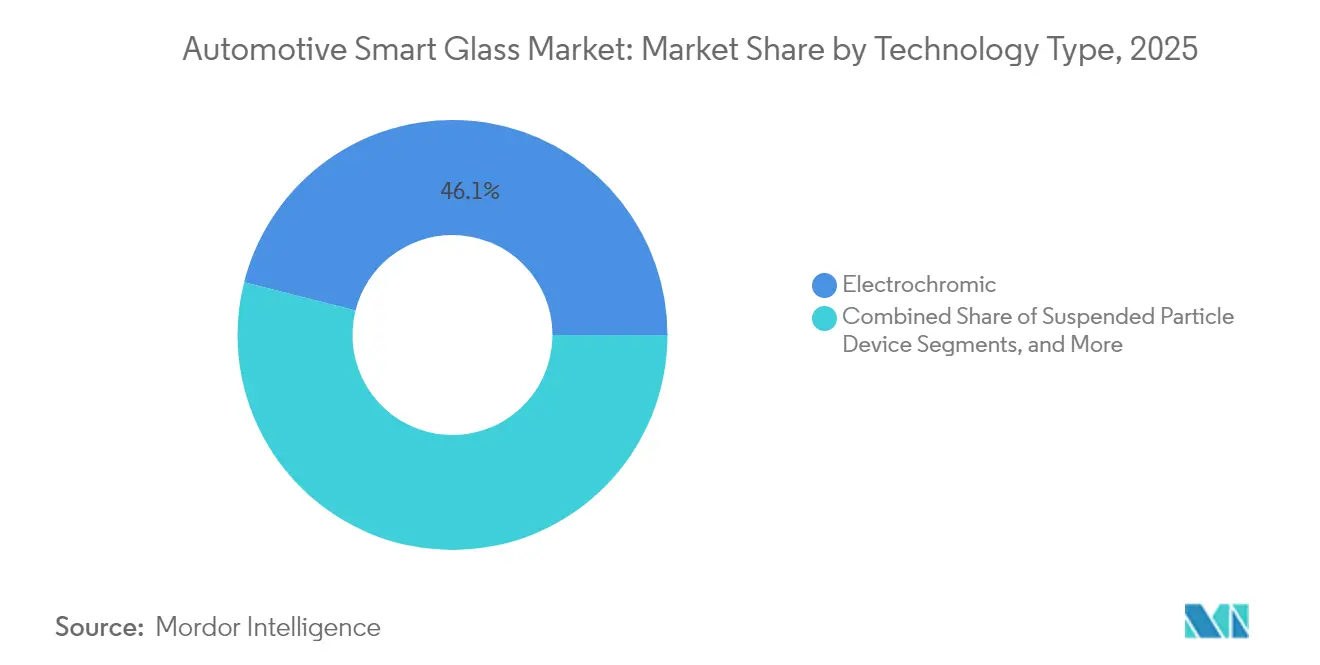

- By technology, electrochromic glazing led with 46.05% of the automotive smart glass market share in 2025; suspended particle devices are projected to post a 14.63% CAGR through 2031.

- By application, sunroof glass captured 73.42% of the automotive smart glass market size in 2025; smart HUD and display panels are forecast to expand at a 16.44% CAGR to 2031.

- By vehicle type, passenger cars accounted for 62.98% of the automotive smart glass market size in 2025; the segment is on course for a 16.05% CAGR through 2031.

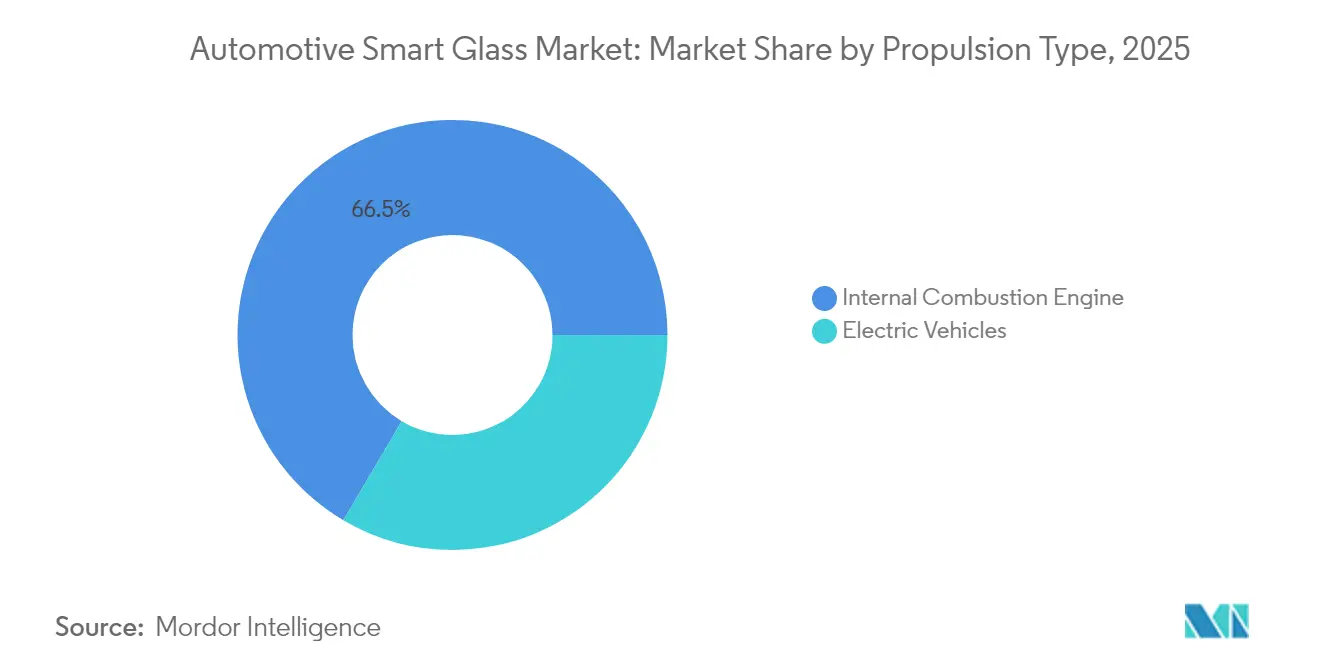

- By propulsion, internal combustion engine models represented 66.52% of the automotive smart glass market size in 2025; electric vehicles are poised for a 17.03% CAGR through 2031.

- By sales channel, OEM installations controlled 85.77% of the automotive smart glass market size in 2025; the aftermarket channel exhibits the fastest progression at 16.25% CAGR to 2031.

- By geography, North America commanded 41.92% of the automotive smart glass market share in 2025; Asia-Pacific is expected to chart a 16.02% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Smart Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS-Ready Windshields Needing Dimmable HUD Zones | +3.2% | North America and Europe; expanding in Asia-Pacific | Medium term (2-4 years) |

| Larger Panoramic Roofs in EVs To Offset Battery Heat | +2.8% | China, Europe, North America EV hubs | Short term (≤ 2 years) |

| Luxury And Premium Vehicles with Electrochromic Sunroofs | +2.1% | North America and Europe; spillover to Asia-Pacific | Medium term (2-4 years) |

| Stricter EU Glare and UV Norms | +1.9% | Europe with global regulatory ripple | Long term (≥ 4 years) |

| Tier-1 Integrated Smart-Roof Modules | +1.7% | Germany, Japan, Michigan | Short term (≤ 2 years) |

| Carbon-Neutral Glass Furnaces Lowering Cost | +1.4% | Europe and North America early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ADAS-Ready Windshields Driving Demand for Dimmable HUD Glass

Advanced driver assistance suites depend on heads-up displays that must stay visible under direct sunlight, dawn glare, and tunnel exit transitions. Saint-Gobain and AGC have jointly validated laminated windshields incorporating a thin electrochromic interlayer that darkens only the HUD patch, preserving windshield clarity everywhere else [1]“Solarbay SPD Demonstrator,”, Gauzy Ltd., gauzy.com. Lumineq’s transparent TFEL stack, mounted behind the protective glass, delivers high-contrast augmented-reality arrows that remain legible at 10,000 cd/m² peak exterior luminance. Automakers pursuing higher SAE automation levels embrace dimmable HUD zones to reduce driver workload and to keep dashboard operations minimal. As HUD content density rises toward augmented navigation and ADAS alerts, windshield smart glass emerges as a functional safety component rather than a mere comfort upgrade.

OEM Push for Larger Panoramic Roofs in EVs To Offset Battery-Pack Heat

Electric platforms generate surplus heat under fast-charge and high-load conditions, putting fresh emphasis on passive thermal management. Panoramic roofs fabricated with suspended particle devices can switch from clear to opaque in milliseconds, slashing solar heat gain before HVAC compressors engage [2]“Electrochromic Windshield Whitepaper,”, AGC Inc., agc.com . Renault’s Solarbay prototype demonstrates that dynamic opacity scheduling can lift real-world EV range by several percentage points during summer cycles. Because battery cooling remains a cost-intensive subsystem, OEM engineers view smart glazing as a low-hanging lever that complements new heat-pump architectures. The resulting design freedom supports sleeker rooflines without mechanical shades, reinforcing distinctive EV styling cues that are impossible to replicate with fixed-tint glass.

Stricter EU Glare and UV Norms Encouraging Smart Glazing

Revised UNECE Regulation 43 mandates dual compliance on minimum visible-light transmission and maximum ultraviolet exposure for panoramic areas, rendering conventional deep-tint coatings insufficient [3]“UNECE R43 Amendments,”, European Commission, europa.eu. Smart glass circumvents this constraint by toggling tint on demand, delivering complete daytime clarity during low-glare conditions while meeting UV limits during high-insolation events. European OEMs pre-engineered global vehicle variants around these stricter norms to avoid region-specific glazing SKUs, indirectly boosting the automotive smart glass market. The policy pressure extends to corporate fleet procurement rules that reward low-glare cabins, nudging leasing companies to favor models with built-in dimmable roofs.

Tier-1 Suppliers Offering Integrated Smart-Roof Modules to Reduce Assembly Time

Module suppliers like Webasto and Continental have moved beyond bare glazing to deliver turnkey roof systems with embedded control electronics, LED mood lighting, sunload sensors, and diagnostic software. Factory drop-in modules compress takt time by eliminating separate wiring and sealant steps, which can unlock several hours of aggregate productivity per shift in high-volume lines. OEMs appreciate the single-supplier warranty model accompanying these modules, reducing logistics overhead and simplifying homologation. The resulting value migration from glass fabricators to system integrators reshapes bargaining power across the automotive smart glass industry, incentivizing joint ventures combining material science and mechatronic expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Component and Integration Cost | -2.9% | Global; sharpest in emerging markets | Short term (≤ 2 years) |

| Scarcity Of Auto-Grade Indium Tin Oxide | -2.1% | Global supply chain; production concentrated in China | Long term (≥ 4 years) |

| Limited Temperature Operability of PDLC Films | -1.8% | Middle East, Northern Canada, Siberia | Medium term (2-4 years) |

| Aftermarket Calibration Complexity for ADAS Windscreens | -1.3% | North America and Europe; broadening as ADAS proliferates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Component and Integration Cost

Electrochromic and SPD roof modules add USD 200-800 per vehicle, a premium that remains difficult to absorb in B-segment or cost-sensitive markets [4]“Smart Glass Cost Structure Analysis,”, AGC Inc., agc.com. Beyond raw materials, OEMs must requalify roof crash performance, add wire routing, and validate software that interfaces with body-control modules. The steep learning curve and line-side tooling charges deter smaller automakers from early adoption. Tier-1 suppliers therefore pursue high-margin luxury contracts first, which postpones volume scale economies that would otherwise accelerate price declines. Although ongoing R&D promises inline coating and film-on-roll processes, the near-term cost hurdle continues to cap penetration in lower segments of the automotive smart glass market.

Aftermarket Calibration Complexity for ADAS Windscreens

Smart windshields paired with camera-based ADAS demand precise optical calibration after replacement, often requiring OEM-level tooling and target boards. Independent glass shops lack capital for such equipment, causing more extended vehicle downtime and higher service fees. Insurers in North America and Europe report rising claim costs, prompting higher deductibles on vehicles fitted with dimmable HUD glass. This service-chain friction dissuades resale-oriented fleet buyers and restrains aftermarket upgrade momentum, even as smart glass retrofit kits become more available.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Electrochromic Leadership Faces SPD Innovation

Electrochromic glazing accounted for 46.05% of the automotive smart glass market size in 2025, a share supported by its balanced switching speed, lifecycle durability, and falling unit cost. Suspended particle devices are projected to grow at a CAGR of 14.63% through 2031. Suspended particle devices are closing the gap by offering sub-second tint changes and richer mid-tone gradients, attributes that resonate with performance-oriented interiors and user-controlled shading presets. Gentex’s film-based electrochromic architecture further flattens the learning curve for tier-1 roof suppliers by enabling roll-to-roll lamination at automotive line speeds.

Over the forecast period, hybrid stacks that merge SPD for fast response with electrochromic layers for deep opacity could capture crossover demand, especially in panoramic roofs that must address glare and privacy. Competition among these technologies catalyzes co-investment in next-generation transparent conductors, as each architecture seeks to mitigate shared ITO constraints. Amid this race, the automotive smart glass market continuously benefits from cross-pollinated breakthroughs that raise overall performance benchmarks.

In parallel, polymer-dispersed liquid crystal and thermo-chromic films hold niche roles where passive modulation suits cost-constrained trim lines. Although their uptake is comparatively slower, PDLC variants with infrared-absorbing nanoparticles show promise for coach-built luxury shuttles serving hot-climate tourism routes. Thermo-chromic roof panels darken above 35 °C without electrical input and appeal to last-mile delivery vans seeking energy-neutral cabin cooling. These smaller technology slices collectively broaden the addressable spectrum for smart glass, allowing the automotive smart glass market to serve mainstream models that might otherwise miss the feature due to cost barriers. As tier-2 suppliers license key patents from early movers, pricing pressures are expected to sharpen, eventually compressing margins but expanding installed base.

By Application Type: Sunroofs Dominate While HUDs Accelerate

Sunroof installations represented 73.42% of the automotive smart glass market size in 2025, benefiting from straightforward roof-module swaps that avoid structural windshield requalification. Consumer demand for open-air ambience, amplified by social-media influencer content, makes panoramic roofs a near-default upsell on premium trims. Smart glass delivers tangible benefits such as glare mitigation without blocking scenery, reinforcing brand storytelling around advanced comfort. Meanwhile, smart HUD and display panels are tracking a 16.44% CAGR through 2031, as the industry pivots toward augmented-reality guidance and driver monitoring overlays. Automakers recognize that windshield-level content must remain visible across lighting extremes, making dimmable patches a functional necessity rather than a luxury flourish.

Secondary applications on side and rear windows focus on privacy and uniform cabin temperature, prized by ride-sharing fleet operators. Front windshields, though technically more challenging due to lamination thickness and safety codes, unlock incremental revenue per vehicle thanks to ADAS compatibility. Kuraray’s SkyViera interlayer, recently adopted by Mahindra’s XUV 9e, integrates ambient lighting grooves synchronizing with the roof’s dimming state, providing a cohesive visual experience. The application landscape is evolving from single-panel novelty to multi-surface ecosystems, a transformation that underpins deeper per-vehicle content and propels the automotive smart glass market.

By Vehicle Type: Passenger Cars Drive Volume Growth

Passenger cars commanded 62.98% of the automotive smart glass market size in 2025 and are projected to grow at a CAGR of 16.05% through 2031, as mainstream marques, including Ford and Toyota, launched mid-trim variants with optional dimmable roofs. Volume leverage allows glass makers to amortize R&D across millions of units, cutting incremental cost by double-digit percentages within successive model cycles. Notably, compact crossovers—the world’s fastest-growing body style—feature roof apertures large enough to justify smart glass even at mid-market price points. Although smaller in volume, commercial vehicles demonstrate higher per-unit revenue because regulatory and operational imperatives favor quick-clearing rear windows for safety and depot-based fast charging. Gauzy’s SmartVision installation on New York’s MTA buses illustrates how public-sector fleets can act as early adopters, validating durability under high-duty schedules.

A feedback loop is forming: as ride-hailing companies prioritize passenger experience, they specify smart glass for their premium tiers, nudging OEMs to include pre-wire options across product lines. This latent demand feeds the passenger-car pipeline, creating a virtuous cycle of scale that lowers price points further. Therefore, the automotive smart glass market anticipates sustained momentum in personal and shared mobility segments, provided suppliers continue to drive material sustainability and circular-economy credentials.

By Propulsion Type: EVs Emerge as Growth Catalyst

Internal combustion platforms still held 66.52% of the automotive smart glass market size in 2025, reflecting the legacy fleet’s dominance. Yet electric vehicles register the fastest 17.03% CAGR through 2031 because bright roofs dovetail seamlessly with the EV value proposition of silent, tech-rich cabins. EV architecture supplies ample low-voltage DC power for glass controllers without auxiliary converters, simplifying integration relative to 12-V ICE boxes. Moreover, the drivetrain’s efficiency obsession turns every watt of saved HVAC load into real-world range, a metric that resonates with regulators and consumers. Faraday Future’s FX Super One MPV exemplifies the frontier, merging an ultra-wide display roof with battery thermal offset strategies for cabin climates –30 °C to 55 °C.

Conversely, hybrid platforms present an intermediary step: OEMs experiment with smart sunvisors and smaller dimmable patches, gathering telematics data to justify full-roof deployment in subsequent EV generations. As charging infrastructure densifies and battery prices drop, some forecasters predict that by 2030, more than half of smart-glass-equipped vehicles will be fully electric, cementing propulsion bias as an enduring growth accelerant for the automotive smart glass market.

By Sales Channel: OEM Dominance with Aftermarket Acceleration

Factory fitments accounted for 85.77% of the automotive smart glass market size in 2025, yet aftermarket kits now post a 16.25% CAGR through 2031, as supply chains mature. Early aftermarket adopters include limousine services and specialty upfitters that retrofit dimmable partitions in chauffeur-driven sedans. The installation process has been simplified via plug-and-play roof modules pre-bonded with control electronics, shrinking labor time to under four hours at certified workshops. Initially wary of recalibration expenses, insurance companies have offered discounted premiums when aftermarket kits include anti-glare fail-safe modes that can lower accident risk during dawn and dusk. Simultaneously, DIY enthusiasts remain a fringe customer base due to specialized bonding adhesives and safety coding required post-installation.

OEMs have begun to view aftermarket robustness as a brand-equity lever, approving select accessory packages to keep residual values high. This co-existence model means the automotive smart glass market benefits from dual revenue pipelines: stable OEM volumes and agile aftermarket innovation. Long term, breakthroughs in self-healing coatings and wireless power transfer for roof panels could further democratize retrofit opportunities, broadening total addressable demand beyond first-owner vehicles.

Geography Analysis

North America retained 41.92% of the automotive smart glass market size in 2025, buoyed by luxury-vehicle density, fast-moving ADAS regulations, and extensive tier-1 supply footprints clustered around Michigan and Ontario. United States buyers are willing to pay for tech-enhanced comfort, as evidenced by Tesla’s Model Y optional dimmable roof package. Canadian fleets, facing harsher winters, test electrochromic roofs for de-icing aid by modulating infrared absorption, a feature under active validation by Saint-Gobain. Cross-border regulatory alignment on windshield HUD parameters simplifies homologation, sustaining OEM appetite for multi-surface smart glass.

Europe ranks second in overall revenue but continues to shape global technical standards. German premium marques pioneer new stack chemistries, while French and Swedish regulators push circular-economy metrics that address end-of-life delamination. The region’s laser focus on low-glare, low-UV cabins has propelled adoption across B-segment hatchbacks. Volkswagen’s ID.3 facelift introduces a partial-roof dimming zone to meet customer comfort surveys. EU Horizon research grants fund carbon-neutral furnaces, underwriting future scale gains that will ripple across the automotive smart glass market worldwide.

Asia-Pacific represents the fastest-growing theater, charting a 16.02% CAGR through 2031. China, the epicenter of global EV production, leverages domestic glass giants like Fuyao to secure supply chain resilience. The government’s sun-roof incentive for NEVs accelerates rooftop smart glass penetration in Tier-1 cities, where summer urban heat islands drive HVAC overuse. Japan’s kei-car segment is pilot-testing compact SPD panes for rear liftgates, underscoring how space-constrained interiors value dynamic shading. South Korea fosters strategic alliances among memory-chip leaders and tier-1 roof suppliers to integrate driver-state sensing with roof tint adjustments, reinforcing the region’s system-level innovation culture.

Although smaller today, Latin America and the Middle East illustrate niche opportunities. Tourism fleets in Mexico retrofit electrochromic side windows for scenic routes, while Gulf-state luxury SUVs adopt tri-zone tint control to cope with 50 °C ambient peaks. These examples signal an eventual Baseline of smart glass expectations among global car buyers, ensuring that regional adoption gaps narrow.

Competitive Landscape

The competitive matrix remains moderately fragmented, with legacy glass conglomerates exploiting economies of scale while specialized innovators chase patent-fortified niches. Saint-Gobain, AGC, and Guardian Industries jointly control a dominant share of OEM roof programs thanks to decades-long supply contracts and localized float lines. Their vertical integration enables swift line conversion for smart-glass lamination, shielding from spot shortages in PVB and ITO. Conversely, Gentex, Gauzy, and View concentrate on differentiated chemistries and drive higher per-square-meter pricing through performance leadership, often partnering with system integrators to access mass-production lines.

AGC showcased transparent display windshields capable of overlaying AR navigation, which positions the company against electronics suppliers eyeing the same windshield real estate. Patent analytics reveal a clustering of new filings around hybrid stack interfaces and self-diagnostics that detect delamination before optical performance degrades, highlighting how software and sensor fusion are becoming decisive.

Price pressure grows as Chinese entrants deploy aggressively priced SPD variants, leveraging subsidies tied to domestic EV volumes. In response, Western incumbents seek cross-licensing pacts to avoid litigation gridlock and maintain time-to-market advantages. The net result is a market structure where differentiation hinges on holistic system integration—combining smart glass, ambient lighting, and connected-car data—rather than raw tinting technology alone. These dynamics sustain a balanced rivalry that spurs innovation while preventing monopolistic lock-in, keeping the automotive smart glass market vibrant and adaptive.

Automotive Smart Glass Industry Leaders

AGC Inc.

Saint-Gobain S.A

Gentex Corporation

Nippon Sheet Glass Co. Ltd.

Corning Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Gauzy Ltd. launched the automotive industry's first prefabricated smart glass stack, a turnkey solution to enhance manufacturing efficiency and accelerate smart glass adoption in vehicles. This fully industrialized product supports scalable integration across vehicle platforms.

- March 2025: Miru Smart Technologies introduced a large electrochromic sunroof device for the automotive sector, showcasing the scalability and value of Argotec's advanced TPU interlayer films in next-gen vehicle design.

Global Automotive Smart Glass Market Report Scope

Automotive smart glass uses a switchable film made from SPD, which is a tinted material for providing shade. In addition, the film blocks 99% of light while maintaining the transparency needed for the driver to safely operate the vehicle.

The automotive smart glass market has been segmented by technology, application, vehicle type, and geography. By technology, the market is segmented by electrochromic, polymer dispersed liquid device (PDLC), and suspended particle device (SPD). By application, the market is segmented by rear and side windows, sunroof glass, and front and rear windshields. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By geography, the market is segmented by North America, Europe, Asia-Pacific, and Rest of the World.

The report covers the market size and forecast in Value (USD) for all the above-mentioned segments.

| Electrochromic |

| Suspended Particle Device (SPD) |

| Polymer Dispersed Liquid Crystal (PDLC) |

| Thermo/Photo-chromic |

| Hybrid / Multi-stack |

| Sunroof Glass |

| Rear & Side Windows |

| Front & Rear Windshields |

| Smart HUD / Display Panels |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Bus and Coaches |

| Internal Combustion Engine |

| Electric Vehicles |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology Type | Electrochromic | |

| Suspended Particle Device (SPD) | ||

| Polymer Dispersed Liquid Crystal (PDLC) | ||

| Thermo/Photo-chromic | ||

| Hybrid / Multi-stack | ||

| By Application Type | Sunroof Glass | |

| Rear & Side Windows | ||

| Front & Rear Windshields | ||

| Smart HUD / Display Panels | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Bus and Coaches | ||

| By Propulsion Type | Internal Combustion Engine | |

| Electric Vehicles | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the automotive smart glass market?

The market is valued at USD 3.55 billion in 2026 and is projected to exceed USD 6.74 billion by 2031.

Which application currently dominates demand?

Panoramic sunroof glass leads with 73.42% share owing to straightforward integration and strong consumer appeal.

How fast is electric-vehicle adoption influencing smart glass uptake?

Electric vehicles represent the fastest-growing propulsion segment, logging a 17.03% CAGR through 2031 as smart roofs aid thermal management.

Who are key players shaping technology evolution?

Saint-Gobain, AGC, Gentex, Gauzy, and Guardian Industries command major OEM programs and steer patent filings.

What is the main supply-chain risk facing manufacturers?

Indium tin oxide scarcity remains the chief bottleneck, exposing suppliers to price volatility and sourcing uncertainty.

Page last updated on: