Automotive Surround View Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

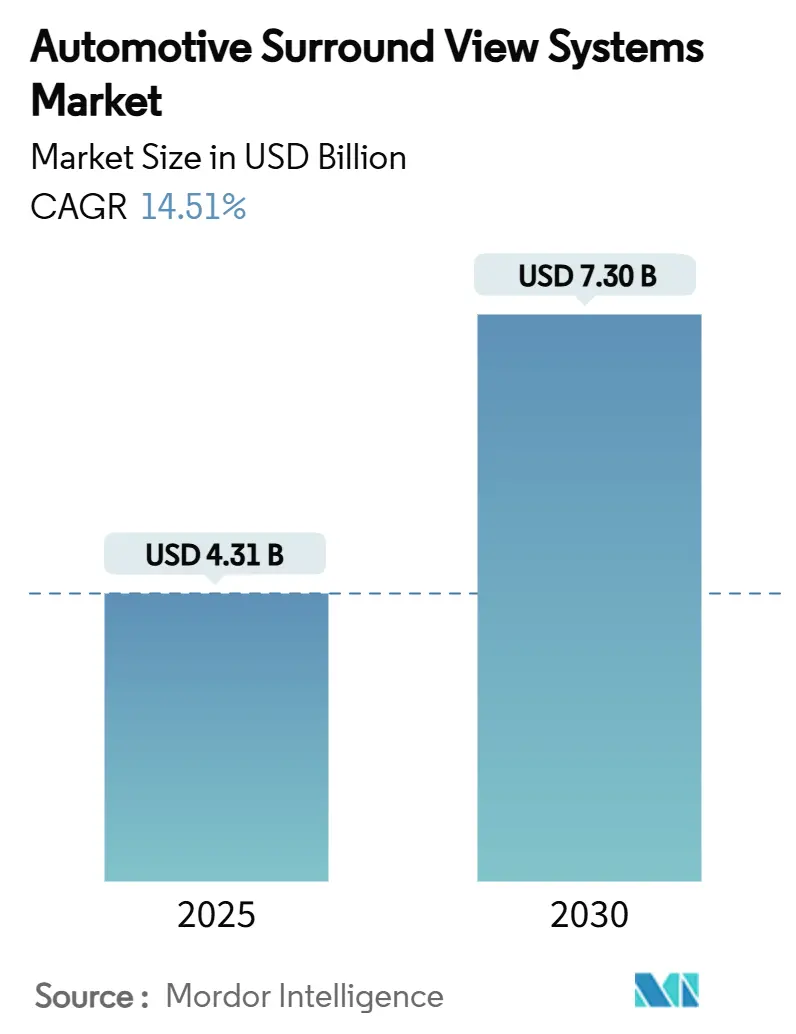

| Market Size (2025) | USD 4.31 Billion |

| Market Size (2030) | USD 7.30 Billion |

| Growth Rate (2025 - 2030) | 14.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Surround View Systems Market Analysis by Mordor Intelligence

The automotive surround view systems market, valued at USD 4.31 billion in 2025, is set to surge to USD 7.30 billion by 2030, marking a robust 14.51% CAGR. This growth is driven by regulatory mandates, swift semiconductor advancements, and a burgeoning demand from premium consumers. In North America and the European Union, rear-visibility regulations have elevated surround-view cameras from mere luxuries to essential compliance tools, fueling consistent growth in the market. As multi-camera average selling prices decline, mid-tier passenger cars are increasingly adopting this technology. Centralized ADAS domain controllers are further enhancing safety functions through 3-D visualization and sensor fusion. Moreover, generative-AI-driven image stitching is boosting perception accuracy, paving the way for Level 2+ autonomy and over-the-air feature unlocks, which in turn, amplify a vehicle's revenue potential over its lifespan. Fleet operators across Asia-Pacific and North America are driving aftermarket demand, leveraging retrofit kits to bolster driver safety and operational visibility.

Key Report Takeaways

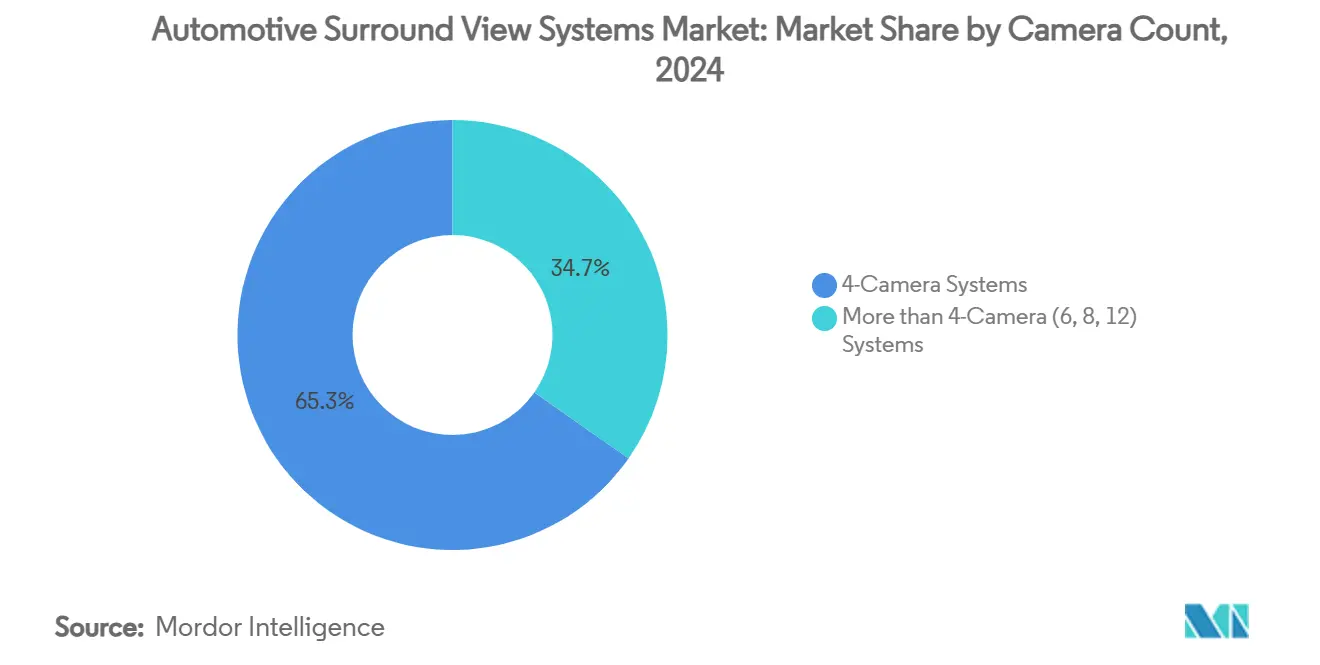

- By camera count, 4-camera systems led the automotive surround view systems market with a 65.27% share in 2024; configurations with more than 4 cameras are forecast to expand at a 19.20% CAGR to 2030.

- By camera functioning, automatic systems captured 75.01% of the automotive surround view systems market size in 2024 and are advancing at a 15.77% CAGR through 2030.

- By vehicle type, passenger cars accounted for 87.13% of the automotive surround view systems market share in 2024, while commercial vehicles recorded the highest projected CAGR at 18.06% through 2030.

- By sales channel, OEM-fitted solutions held 89.59% share of the automotive surround view systems market size in 2024, whereas aftermarket retrofits are growing at a 19.82% CAGR to 2030.

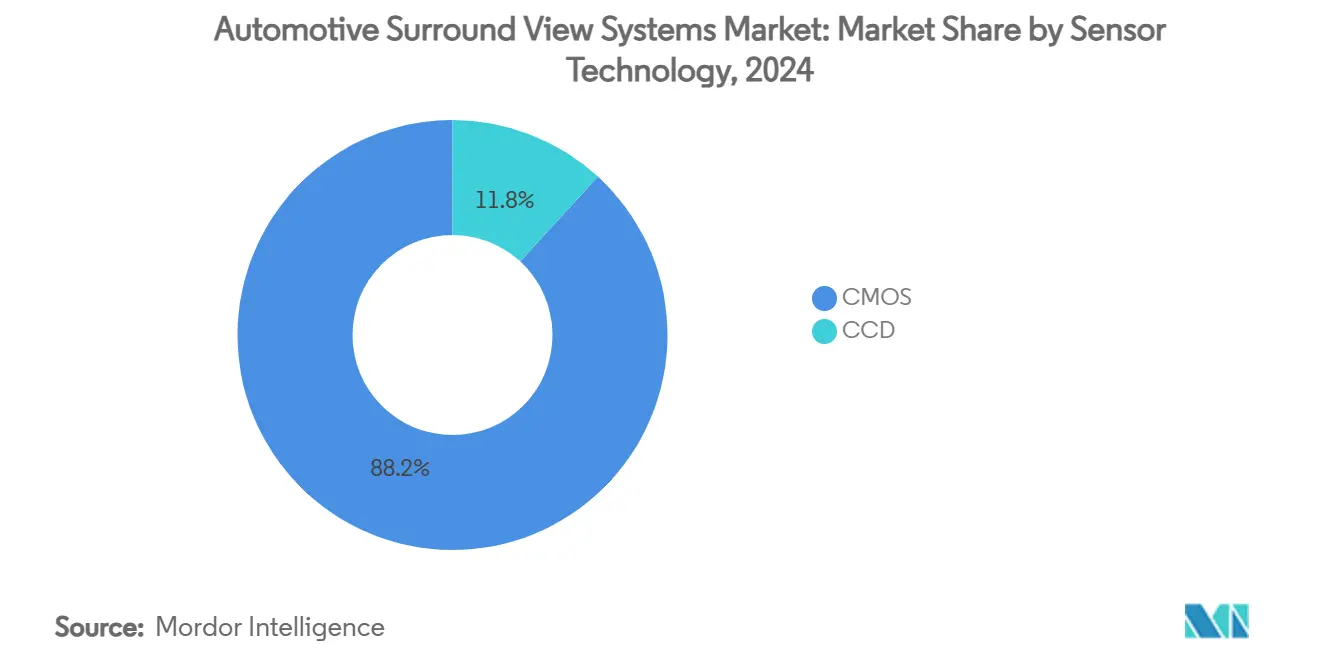

- By sensor technology, CMOS captured 88.18% of the automotive surround view systems market in 2024 and is projected to grow at a 15.36% CAGR through 2030.

- By display type, 2-D systems commanded 68.89% share of the automotive surround view systems market size in 2024, and 3-D/augmented-reality displays are rising at a 22.11% CAGR to 2030.

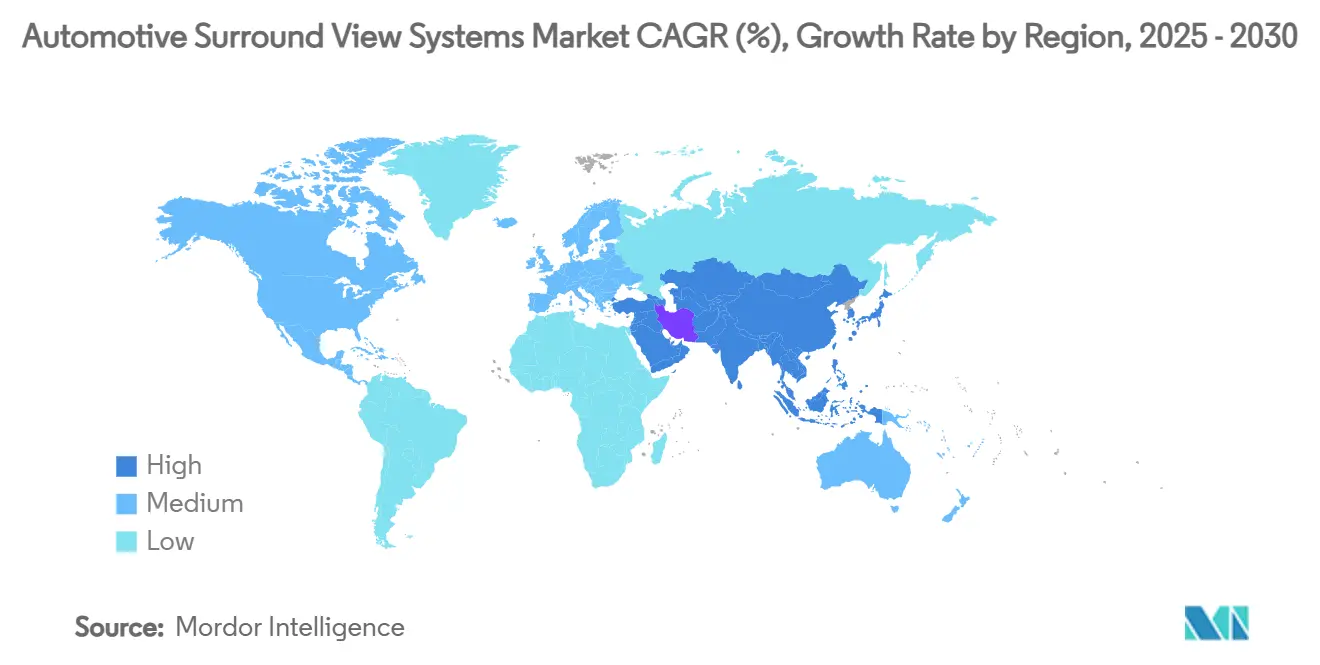

- By geography, Asia-Pacific captured 47.86% share of the market in 2024, and is set to post the fastest CAGR of 15.17% by 2030.

Global Automotive Surround View Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated Rear-Visibility Regulations | +4.2% | Global, with early enforcement in EU and North America | Short term (≤ 2 years) |

| 3-D Surround-View Integration | +3.8% | APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| Falling Multi-Camera ASPS | +2.9% | Global, with pronounced effects in price-sensitive markets | Medium term (2-4 years) |

| Generative-AI-Based Stitching | +2.1% | North America and EU early adoption, APAC scaling | Long term (≥ 4 years) |

| OTA-Driven Feature | +1.8% | Global, with premium segment leadership | Medium term (2-4 years) |

| Retrofit Kit Adoption by Logistics Fleets | +1.4% | APAC and North America logistics hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandated Rear-Visibility Regulations Drive Market Foundation

Global safety rules such as FMVSS-111 in the United States and General Safety Regulation II in the European Union make rear-visibility technology compulsory, locking surround-view cameras into every new-vehicle bill of materials. Compliance removes discretionary purchasing behavior, allowing suppliers to model predictable capacity utilization and optimize cost curves. Harmonized legislation is cascading into Canada, where new school-bus standards require exterior perimeter visibility, broadening the addressable customer base[1]“Regulations Amending the Motor Vehicle Safety Regulations (School Buses),” Government of Canada, canada.ca. OEMs respond by standardizing camera harnesses and adopting scalable electronics architectures that simplify global homologation.

Integration of 3-D Surround-View in ADAS Domain Controllers

Centralized ADAS domain controllers consolidate camera, radar, and LiDAR inputs, enabling surround-view feeds to support lane-keeping and hands-free highway maneuvers. Shared compute resources lower system cost per function, making advanced perception feasible for mid-range models. Tier-1 suppliers integrate automotive Ethernet backbones that transfer uncompressed video with minimal latency, while domain-controller silicon incorporates hardware accelerators for neural-network inference. The result is a seamless blend of parking, cross-traffic, and automated lane-change assistance in a single software stack.

Falling Multi-Camera ASPs Enable Market Democratization

Since 2024, innovations like wafer-level optics and vertically integrated manufacturing, coupled with heightened regional supply competition, have driven down camera module prices by double-digit percentages. This cost reduction allows automakers to include 360-degree cameras in trim packages for moderately priced vehicles, all without sacrificing profit margins. Suppliers, capitalizing on increased unit volumes, are renegotiating contracts for lenses and serializers, further deepening the price decline. Highlighting this trend, Sony's automotive CMOS image sensor division aims for profitability by fiscal 2026, banking on a projected 6.68-fold surge in car camera demand from 2019 to 2030[2]Chiang, Jen-Chieh, Taipei; Willis Ke, "Sony eyes profitability for automotive CIS biz by fiscal 2026 amid 6x growth in car cameras", DIGITIMES Asia, digitimes.com. Meanwhile, in emerging markets, local assemblers are innovatively combining affordable cameras with open-source software, crafting budget-friendly retrofit kits tailored for ride-hailing fleets.

Generative-AI-Based Stitching Boosts Perception Accuracy

Generative AI algorithms trained on diverse driving datasets now correct lighting, parallax, and distortion in real time. Hardware acceleration on graphics-processing units embedded in vehicle computers supports 60 frames per second panoramic output. Higher fidelity enables automatic obstacle classification at low speeds, reducing minor collision rates in urban parking. Automakers incorporate natural-language interfaces that allow drivers to ask for blind-spot visuals verbally, improving user experience and brand differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heat-Dissipation and Networking Bottlenecks | -2.8% | Global, with acute effects in extreme climate regions | Medium term (2-4 years) |

| Price Sensitivity in Entry-Level Cars | -2.3% | APAC and emerging markets primarily | Short term (≤ 2 years) |

| Cyber-Security Certification Delays | -1.9% | EU and regions adopting UNECE standards | Short term (≤ 2 years) |

| Shortage of Wide-Angle Lens Suppliers | -1.2% | Global supply chain impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ECU Heat-Dissipation and In-Vehicle Networking Bottlenecks

High-resolution multi-camera payloads saturate 1-Gbps automotive Ethernet links, forcing upgrades to 10-Gbps backbones that increase thermal load. Hot-climate testing shows accelerated component aging when junction temperatures exceed 125 °C. Liquid-cooled camera ECUs mitigate risk but add cost and package constraints. Automakers explore zonal architectures that decentralize processing to edge nodes near cameras, shortening wiring runs and reducing heat density.

Cyber-Security Certification Delays Under UNECE R155/R156

Surround-view cameras count as networked devices subject to new cybersecurity rules that demand threat analysis, over-the-air update authentication, and incident response planning. Documentation, penetration testing, and third-party audits stretch launch schedules by up to 18 months, tying up engineering resources and slowing revenue recognition. Tier-1 suppliers employ security-by-design frameworks, but smaller retrofit vendors face steep learning curves that limit market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Camera Count: Multi-Camera Configurations Drive Premium Adoption

The automotive surround view systems market size for 4-camera setups captured 65.27% market share in 2024, reflecting their cost-to-function sweet spot. More than 4-camera architectures, however, record a 19.20% CAGR as premium models add trailer, pillar, and interior views for Level 2+ autonomy. Prices of 8-camera sets dropped significantly in 2025, widening the addressable market. Software updates now unlock dormant camera channels post-sale, improving lifelong revenue.

Evolution toward 12-camera arrays is driven by urban delivery vans requiring full-perimeter perception for curbside automation. Edge AI chips compress and encrypt video before routing it to cloud-native data lakes for fleet analytics. As semiconductor costs normalize, mid-range vehicles in Asia adopt six-camera configurations, diversifying supplier portfolios and raising incremental demand inside the automotive surround view systems market.

By Camera Functioning: Automatic Systems Dominate Through AI Integration

Automatic systems held 75.01% of the automotive surround view systems market share in 2024 as deep-learning algorithms superseded manual joystick control. Adaptive exposure and auto-white-balance corrections ensure reliable imagery across tunnels, sunset glare, and snowfall. The automotive surround view systems market size attributable to automatic setups is projected to rise at 15.77% CAGR, powered by fleet mandates for fatigue-monitoring and collision-warning features.

Manual systems persist in niche heavy-equipment applications where operators require joystick precision for crane operations. Yet even in construction vehicles, AI-based scene understanding is phasing in to flag personnel proximity. Function consolidation with panoramic mirrors, blind-spot detection, and reversing aid continues to tilt investments toward automated operation.

By Vehicle Type: Commercial Vehicles Emerge as Growth Leaders

Passenger cars remained the revenue anchor, capturing 87.13% market share in 2024, but commercial vehicles logged 18.06% CAGR as fleet insurers offered premium discounts for camera-verified driver behavior. Logistics operators deploy 360-degree cameras to curb blind-spot accidents in dense urban routes. Retrofit kits add telematics that upload tagged video to cloud dashboards, allowing safety managers to coach drivers and arbitrate claims.

Freight platforms investing in electric vans leverage surround-view footage for autonomous parking in constrained depot slots, reducing labor expenses. School-bus operators adopt exterior perimeter cameras in line with new national safety rules, signaling broader uptake beyond freight applications. These trends raise commercial-vehicle content per unit, re-balancing revenue mix inside the automotive surround view systems market.

By Sales Channel: Aftermarket Retrofit Gains Momentum

OEM-installed systems continued to account for 89.59% of the total market share in 2024, sustained by platform-level economies. Nonetheless, a 19.82% CAGR in retrofit units signals opportunity as fleet operators stretch vehicle lifespans. Plug-and-play harnesses compatible with CAN and LIN buses cut installation time to under two hours, unlocking scale in used-vehicle channels.

Insurance telematics bundles link retrofit cameras to risk-based premiums, reinforcing business cases. Regulatory actions granting mirrorless approvals for heavy trucks accelerate adoption where OEM refresh cycles lag. Tesla's development of retrofit-compatible hardware variants demonstrates the technical feasibility of upgrading existing platforms with advanced camera capabilities.

By Sensor Technology: CMOS Dominance Reflects Performance Advantages

CMOS devices held 88.18% share in 2024, and are expected to register a CAGR of 15.36% through 2030 because they deliver fast readout, lower noise, and embedded HDR at attractive cost points. AI-ready pixels reduce on-chip signal-to-noise ratios, simplifying downstream processing. Automotive surround view systems market share for CMOS is set to climb further as global-shutter architectures mitigate rolling-shutter distortions during rapid maneuvers.

Emerging neuromorphic sensors emulate optic nerves, offering sub-1-millisecond latency, yet commercial scale remains several years out. Meanwhile, global sensor suppliers integrate all-weather coatings and heaters directly into modules, raising reliability for monsoon and winter climates. CCD solutions retain limited traction in specialized broadcast vans where absolute image fidelity outweighs power budgets.

By Display Type: 3-D/Augmented Reality Drives Innovation

2-D head-unit screens dominated shipments in 2024, capturing 68.89% share, but 3-D dashboards and augmented-reality head-up displays grew fastest at 22.11% CAGR. Drivers benefit from depth cues and hazard overlays that cut glance time. Camera feeds blend with navigation arrows projected onto windshields, guiding drivers through complex junctions with less cognitive load.

Premium brands embed haptic steering alerts tied to camera vision, synchronizing tactile and visual feedback. As graphic-processing costs fall, mainstream models adopt stereoscopic center screens delivering bird-eye views with dynamic trajectory lines. This evolution creates new software revenue streams attached to the automotive surround view systems market.

Geography Analysis

Asia-Pacific retained 47.86% share in 2024 and posted the highest 15.17% CAGR outlook. Local governments invest in 5G corridors and smart-city test beds, providing low-latency V2X links that enhance camera fusion. Domestic automakers push software-defined platforms; one-third of new Chinese vehicles will feature centralized electrical architectures by 2025, driving multichannel camera demand. Component makers located near established electronics clusters compress lead times and optimize logistics.

North America recorded 10.40% CAGR as FMVSS-111 compliance became ubiquitous and consumer awareness of ADAS climbed. Fleet retrofits surged, propelled by safety-incentive programs. Europe followed at 9.10% growth, anchored by premium OEMs rolling out 3-D visualization and hands-free motorway features aligned with General Safety Regulation II. Western Asia’s 11.80% pace reflects smart-city investments and rising middle-class car ownership, whereas slower economic activity and regulatory uncertainty kept Russia’s trajectory near 6.50%.

Supply-chain resilience emerged as a key regional variable. Semiconductor capacity centered in East Asia exposes Western OEMs to geopolitical risk, prompting dual-sourcing strategies and on-shoring talks. Camera-module makers are diversifying assembly into Southeast Asia and Mexico to hedge tariff exposure and shorten shipping lanes, sustaining balanced growth across the automotive surround view systems market.

Competitive Landscape

The automotive surround view systems market exhibits moderate concentration, creating opportunities for both established suppliers and emerging disruptors to capture value through technological differentiation and strategic positioning. However, the competitive dynamics are shifting as software capabilities become increasingly important, enabling technology companies and specialized suppliers to challenge incumbent positions through superior AI algorithms and system integration capabilities.

Industry players integrate generative-AI stitching and cyber-secure firmware updates to win long-term module-plus-software contracts. Silicon vendors partner with tier-ones to embed dedicated vision accelerators, shortening development timelines. Strategic investments and joint ventures target control of key algorithms and data pipelines. The entrance of electronics giants considering acquisitions of legacy automotive units underscores the pivot toward software-defined vehicles.

Start-ups backed by venture capital supply perception middleware optimized for commodity cameras, challenging incumbents on innovation speed. Incumbent suppliers counter by offering white-label open-source stacks that reduce integration effort. Cybersecurity certification readiness acts as a barrier to entry, tilting the playing field toward well-capitalized firms able to finance lengthy homologation cycles.

Automotive Surround View Systems Industry Leaders

-

Valeo SA

-

Magna International

-

Continental AG

-

DENSO Corporation

-

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Magna International partnered with NVIDIA to integrate the DRIVE AGX Thor system-on-chip into next-generation surround-view solutions, with demonstrators targeted for Q4 2025.

- March 2025: Volkswagen Group expanded its collaboration with Valeo and Mobileye to deploy 360-degree camera arrays and hands-free functions in future MQB platforms.

- November 2024: onsemi Hyperlux image sensors were selected for Subaru’s next-generation AI-integrated EyeSight system, boosting dynamic-range performance.

- October 2024: Sony Semiconductor Solutions released a CMOS sensor capable of simultaneous RAW and YUV output, simplifying camera electronics and reducing power draw.

Global Automotive Surround View Systems Market Report Scope

| 4-Camera Systems |

| More than 4-Camera (6, 8, 12) Systems |

| Automatic (auto-switching / AI) |

| Manual |

| Passenger Cars |

| Commercial Vehicles |

| OEM-fitted |

| Aftermarket Retrofit |

| CMOS (Complementary Metal-Oxide-Semiconductor) |

| CCD (Charge-Coupled Device) |

| 2-D |

| 3-D / Augmented |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Camera Count | 4-Camera Systems | |

| More than 4-Camera (6, 8, 12) Systems | ||

| By Camera Functioning | Automatic (auto-switching / AI) | |

| Manual | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Sales Channel | OEM-fitted | |

| Aftermarket Retrofit | ||

| By Sensor Technology | CMOS (Complementary Metal-Oxide-Semiconductor) | |

| CCD (Charge-Coupled Device) | ||

| By Display Type | 2-D | |

| 3-D / Augmented | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive surround view systems market?

The market is valued at USD 4.31 billion in 2025 and is set to reach USD 7.30 billion by 2030.

Which region leads the automotive surround view systems market?

Asia-Pacific holds 47.86% share, driven by connected-vehicle initiatives and high local production.

How many cameras are typical in mainstream surround-view systems?

Four-camera configurations dominate with 65.27% share, although 8-camera and 12-camera arrays are growing quickly.

Why are CMOS sensors preferred in automotive cameras?

CMOS offers lower power consumption, faster readout, and easier integration, capturing 88.18% of 2024 shipments.

What is the main restraint for wider deployment of high-resolution camera ECUs?

Thermal management and network bandwidth bottlenecks limit high-performance surround-view expansion in hot climates.

How do regulations influence aftermarket retrofit demand?

Mandated rear-visibility and mirrorless approvals encourage fleets to install retrofit kits on existing vehicles to maintain compliance and lower insurance costs.

Page last updated on: