Automotive Electronic Brake Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

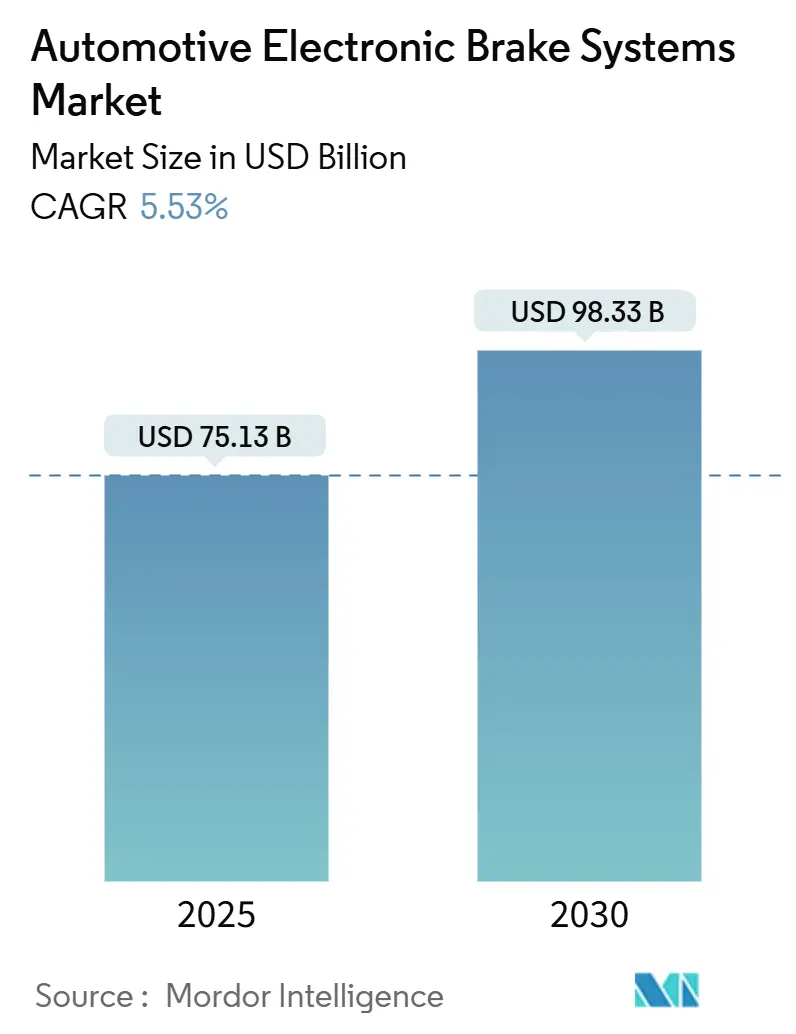

| Market Size (2025) | USD 75.13 Billion |

| Market Size (2030) | USD 98.33 Billion |

| Growth Rate (2025 - 2030) | 5.53% CAGR |

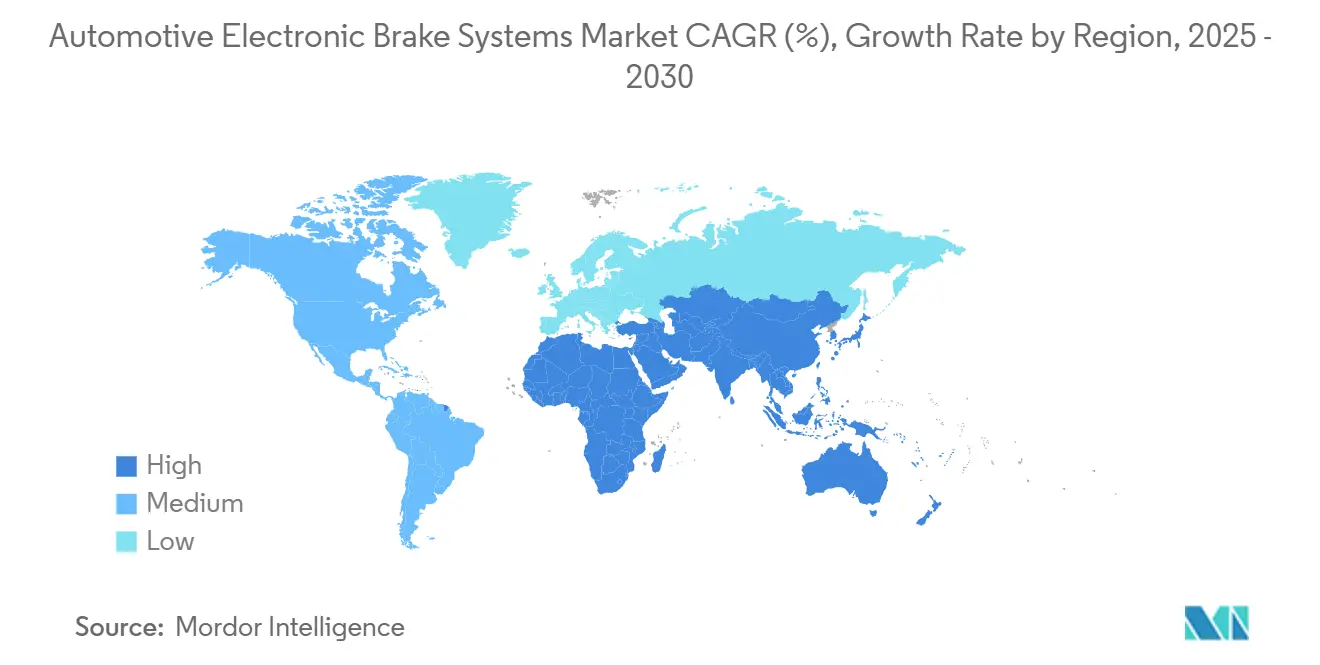

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Electronic Brake Systems Market Analysis by Mordor Intelligence

The Automotive Electronic Brake Systems Market size is estimated at USD 75.13 billion in 2025, and is expected to reach USD 98.33 billion by 2030, at a CAGR of 5.53% during the forecast period (2025-2030). The trajectory is fueled by global mandates for automatic emergency braking, India’s 2026 ABS requirement on two-wheelers, and brake-by-wire integration that aligns with vehicle electrification strategies. The shift toward software-defined braking, the emergence of over-the-air (OTA) update capabilities, and the convergence of regenerative braking with energy-management systems further accelerate demand. Suppliers with validated ESC, ABS, and one-box electro-hydraulic brake (EHB) modules are best positioned as OEMs prioritize turnkey platforms to simplify homologation in multiple regions. The automotive electronic brake system market remains resilient despite semiconductor supply constraints and cost sensitivity in entry-level segments because safety regulations sharply limit substitution options.

Key Report Takeaways

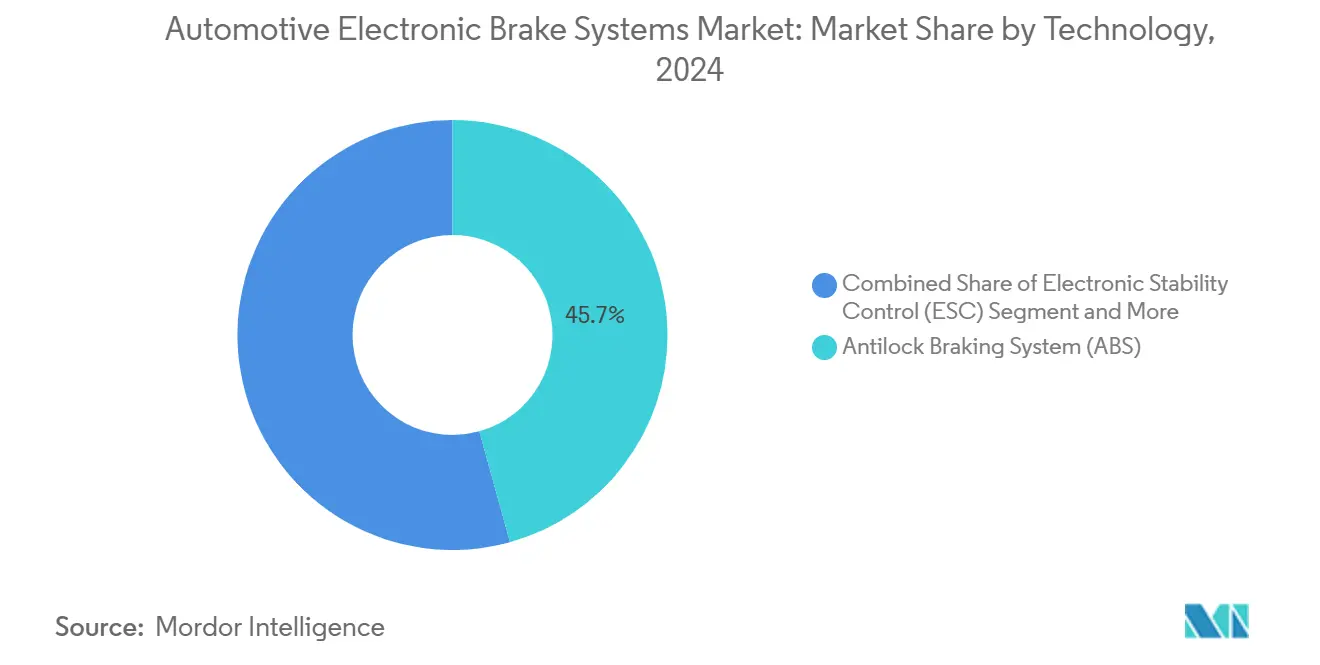

- By technology, ABS captured 45.73% of the automotive electronic brake system market share in 2024, and brake-by-wire is projected to post the fastest 5.55% CAGR to 2030.

- By vehicle type, passenger vehicles held a 66.71% of the automotive electronic brake system market share in 2024, and commercial vehicles are forecast to expand at a 5.64% CAGR through 2030.

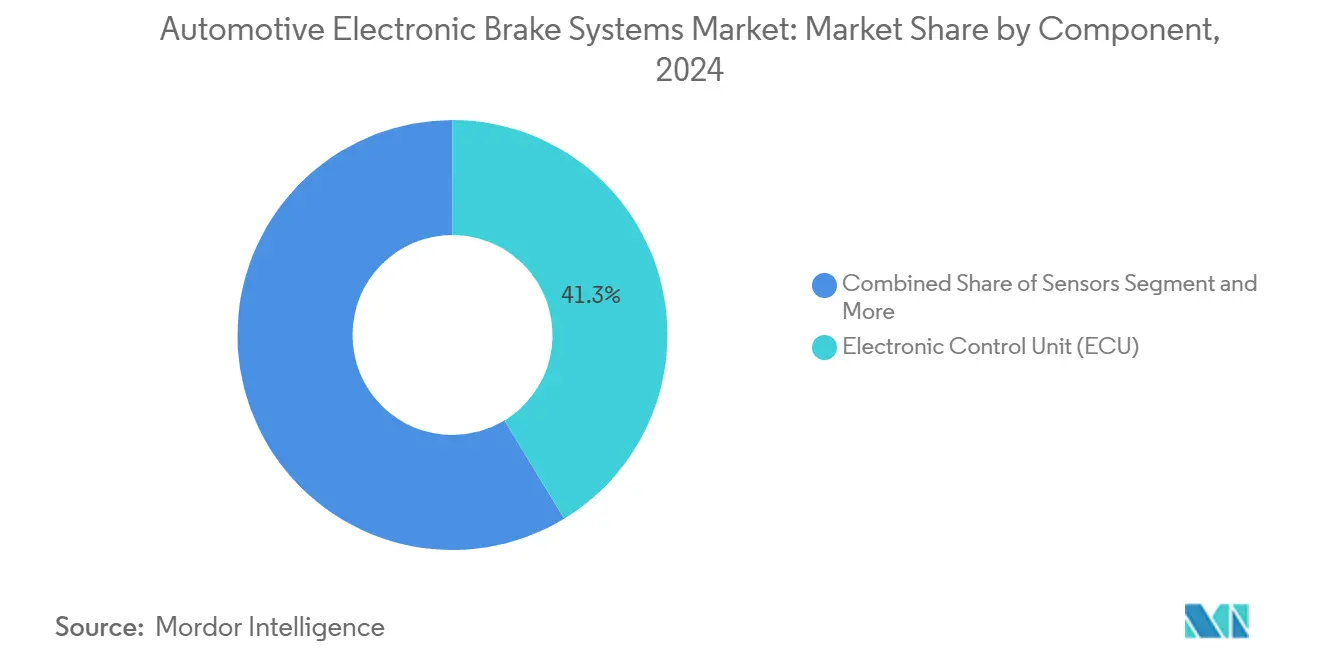

- By component, electronic control units (ECUs) commanded a 41.27% of the automotive electronic brake system market share in 2024, and sensors will register the highest 5.58% CAGR between 2025 and 2030.

- OEM installations accounted for 78.82% of the automotive electronic brake system market share in 2024; the aftermarket channel is projected to expand at a 5.63% CAGR through 2030.

- By geography, the Asia-Pacific contributed 38.94% of the automotive electronic brake system market share in 2024, while the Middle East and Africa are expected to log the fastest 5.57% CAGR to 2030.

Global Automotive Electronic Brake Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Mandates For Mandatory ABS & ESC Fitment | +1.2% | Global, with early gains in India, Philippines, EU | Short term (≤ 2 years) |

| OEM Electrification Road-Maps | +0.8% | North America and EU, Asia Pacific core | Medium term (2-4 years) |

| Lightweight "One-Box" EHB Modules Lowering Total Cost Vs. Legacy Hydraulic Systems | +0.6% | Global, spill-over to MEA | Medium term (2-4 years) |

| Rapid ESC Penetration | +0.5% | Asia Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Cyber-Secure Over-The-Air (OTA) Braking-Software Updates Unlocking Subscription Revenue | +0.4% | North America and EU | Long term (≥ 4 years) |

| Insurance-Premium Discounts Tied To Real-Time Brake-Health Telematics | +0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for Mandatory ABS & ESC Fitment in Light Vehicles

Mandates accelerate adoption by making electronic brake systems non-negotiable across all trims. India’s rule covering more than ten million two-wheelers yearly from 2026, the Philippines’ pending House Bill 11293, and NHTSA’s requirement for automatic emergency braking on new passenger cars by 2029 collectively eliminate pricing levers that once restricted ABS and ESC to premium variants [1]“Notification GSR xx(E) on Fitment of ABS,” Ministry of Road Transport & Highways, morth.nic.in. Cascading standards tied to NCAP protocols harmonize requirements across exporting markets, which pushes OEMs to adopt global platforms instead of regional derivatives.

OEM Electrification Roadmaps Demanding High-Efficiency Regenerative Braking Integration

High-efficiency regeneration has become a core range-extension lever for battery-electric vehicles. Mercedes-Benz’s in-drive brake, Continental’s combined motor-inverter-brake module, and Tesla’s software-controlled blending illustrate why brake-by-wire is integral to next-generation EV architectures [2]“In-Drive Brake Concept for Future EVs,” Mercedes-Benz Group, group.mercedes-benz.com. Energy recovery rates at four-fifths curb rotor wear and unlock software monetization via usage-based performance packages.

Lightweight “One-Box” EHB Modules Lowering Total Cost vs. Legacy Hydraulic Systems

Consolidating the master cylinder, booster, hydraulic modulator, and ECU into a single housing trims line installation time and slashes warranty points. ZF, Nexteer, and Brembo have each released compact units that remove vacuum pumps—critical in EVs where no engine vacuum exists—and deliver shorter response times by cutting fluid path volume [3]“Integrated Brake Control Systems Overview,” Nexteer Automotive, nexteer.com.

Rapid ESC Penetration in Emerging Markets After NCAP-Aligned Safety Rating Changes

Bharat NCAP and similar local programs elevate consumer awareness, driving OEMs to standardize ESC even in sub-compact cars. Local assemblies by ZF Commercial Vehicle Control Systems India and domestic sourcing of low-cost inertial sensors narrow the price gap, enabling mass adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Incremental Cost Of 4-Channel Brake-By-Wire Architecture | -0.7% | Asia Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Sensor-Grade Semiconductor | -0.4% | Global | Medium term (2-4 years) |

| OEM Liability Concerns Around AI-Based Adaptive Braking Algorithms | -0.3% | North America and EU | Long term (≥ 4 years) |

| Brake-Dust Emission Regulations | -0.2% | EU, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Incremental Cost of 4-Channel Brake-By-Wire Architecture for Low-Cost Segments

Once ABS and four-channel architectures are mandated for entry-level motorcycles in India, retail prices will climb by INR 4,500–5,000, equal to one-tenth of the sticker price, spurring vocal pushback from domestic OEMs. Certification bottlenecks further strain adoption as testing agencies race to clear higher volumes before the 2026 deadlines.

Sensor-Grade Semiconductor Shortages Disrupting ESC/ABS ECU Supply

Automotive-grade microcontrollers on mature 55-nm lines remain scarce, leaving brake ECU assemblers vulnerable. Infineon’s 2025–2028 transition toward RISC-V safety controllers helps long-term capacity but imposes near-term re-qualification for Tier-1 suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Brake-By-Wire Drives Innovation Despite ABS Dominance

ABS accounted for 45.73% of the automotive electronic brake system market share in 2024, confirming its status as the baseline safety feature across global production. Brake-by-wire, while smaller in absolute revenue, is expected to expand at a 5.55% CAGR as OEMs look to simplify EV packaging and enable higher regenerative energy capture. Converged platforms that house ABS, ESC, and regenerative control in a single ECU reduce part counts and accelerate type-approval cycles.

Software-centric designs confer upgrade paths via OTA distribution, letting OEMs roll out incremental stopping-distance reductions or refreshed pedal-feel maps without mechanical changes. Risk of liability for AI-based torque commands is tempered by ISO 26262 ASIL-D compliance layers embedded in modern microcontrollers. Suppliers unable to furnish cybersecurity credentials lag in RFQ shortlists as regulators heighten scrutiny of drive-by-data subsystems.

By Vehicle Type: Commercial Acceleration Outpaces Passenger Dominance

Due to sheer volume, passenger vehicles represented 66.71% of the automotive electronic brake system market in 2024, but commercial vehicles will log the quicker 5.64% CAGR through 2030. Fleet operators are increasingly adopting intelligent Electronic Brake Systems (iEBS) to align with mileage-based insurance models and reduce downtime. Real-time brake-wear metrics delivered to telematics dashboards permit optimized maintenance cycles and immediate ROI calculations, accelerating order conversions.

Standard ABS and ESC compliance in passenger cars leaves OEMs to pursue differentiation through customizable pedal response, sprint mode decel maps, and track-use thermal management, all software-enabled within brake-by-wire architectures. Mass-market electrics employ blended regeneration to extend range without upsizing batteries, turning brake modules into energy-saving components rather than pure safety hardware.

By Component: Sensors Surge While ECUs Maintain Leadership

Electronic control units (ECUs) secured 41.27% of the automotive electronic brake system market share in 2024 because no brake action occurs without algorithmic mediation. However, sensor shipments will climb at a 5.58% CAGR as every wheel, axle, and torque vectoring sub-routine demands redundant data feeds. Accelerometers, pressure sensors, and IMUs migrate from 16-bit to 32-bit resolution, enabling finer slip detection thresholds that can shave meters off stopping distance at 62 mph test speed.

The automotive electronic brake system market size allocated to next-generation zone controllers rises as chassis, steering, and brake logic consolidate. Centralized topologies simplify wiring harnesses but heighten semiconductors’ criticality—spotlighting the semiconductor shortage risk noted earlier. Thermal isolation techniques now embed liquid cooling for high-load commercial duty cycles, solving past module derating issues in desert climates.

By Sales Channel: Aftermarket Momentum Builds on OEM Foundation

OEM fitments provided 78.82% of the automotive electronic brake system market share in 2024, yet the aftermarket will grow 5.63% CAGR since almost 50 million vehicles annually age beyond factory warranties. ASK Automotive’s 400-dealer network proves that consumers will retrofit ABS kits when insurers rebate premiums or urban laws restrict non-ABS bikes. Commercial fleet refresh programs retrofit ESC to achieve corporate sustainability targets by mitigating crash-related downtime.

The automotive electronic brake system market’s gasket-less one-box modules lower labor times, supporting mom-and-pop service centers that previously avoided hydraulic bleeds. Predictive maintenance delivered over Bluetooth OBD dongles engages app-savvy motorists, creating parts-plus-software recurring revenue models once unseen in braking components.

Geography Analysis

Asia-Pacific delivered 38.94% of the automotive electronic brake system market share in 2024, underpinned by China’s scale, India’s two-wheeler volumes, and aggressive local supply chains that keep system costs palatable. China’s NEV subsidies prioritize regenerative braking, while India’s 2026 ABS deadline inflates order books for domestic Tier-1 firms. Japan and South Korea advance brake-by-wire R&D to support Level 3 autonomy pilots on expressways.

North America’s upcoming 2029 automatic emergency braking mandate keeps the automotive electronic brake system market size robust. OEMs already embed brake-by-wire on premium crossovers; the directive will cascade that architecture down to compact models. Europe’s General Safety Regulation II mirrors these timelines, prompting suppliers to position ECU plants near final-assembly hubs to avoid semiconductor cross-border delays.

The Middle East and Africa will post the fastest 5.57% CAGR. Saudi Arabia’s Vision 2030 fleet modernization, South Africa’s export-oriented factories, and the UAE ride-hailing electrification jointly spur uptake. Yet supplier footprints remain nascent, making joint ventures between global Tier-1s and regional assemblers pivotal for cost-effective rollouts.

Competitive Landscape

The top five suppliers, including Bosch, Continental, ZF, Hitachi Astemo Ltd., and Mando Corporation, collectively account for a significant share. All maintain worldwide homologation capabilities and vertically integrated electronics manufacturing, challenging entry. Semiconductor houses like Infineon and NXP increasingly co-design reference platforms with Tier-1s, blending chip road maps with brake algorithms to shorten validation cycles.

Technology leadership is the new battleground. Brembo’s Sensify melds machine learning with mechatronics, offering predictive pad-wear alerts that dealerships monetize through subscription packs. Continental demonstrates fully electric braking devoid of hydraulic lines, matching the zero-leak robustness required for autonomous shuttles. ZF’s five-million-vehicle award validates its one-box EHB cost model for mass production.

Regional challengers gain footholds by catering to localized costs and regulation nuance. ASK Automotive dominates Indian two-wheelers, while Fawer in China aligns with domestic inverter suppliers to deliver integrated drive-brake units. Cybersecurity qualification per UNECE R155 is now table stakes; vendors without an ISO 21434 audit trail risk RFQ exclusion.

Automotive Electronic Brake Systems Industry Leaders

Robert Bosch GmbH

Continental AG

ZF Friedrichshafen AG

Hitachi Astemo Ltd.

Mando Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Infineon Technologies announced a RISC-V automotive chip family, prompting Tier-1s to re-architect brake ECUs ahead of 2028 SOP.

- June 2025: India formally gazetted its ABS mandate for all two-wheelers effective Jan 2026, expected to significantly enhance road safety and positively impact the demand curve of automotive electronic brake system.

- March 2025: Volkswagen Group, Valeo, and Mobileye agreed to integrate 360-degree emergency assist, relying on unified brake intervention across MQB models.

Global Automotive Electronic Brake Systems Market Report Scope

| Antilock Braking System (ABS) |

| Electronic Stability Control (ESC) |

| Brake-by-Wire (EHB & EMB) |

| Regenerative Braking System |

| Passenger Vehicles |

| Commercial Vehicles |

| Electronic Control Unit (ECU) |

| Brake Actuator / Modulator |

| Sensors |

| Hydraulic Control Unit |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Antilock Braking System (ABS) | |

| Electronic Stability Control (ESC) | ||

| Brake-by-Wire (EHB & EMB) | ||

| Regenerative Braking System | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Component | Electronic Control Unit (ECU) | |

| Brake Actuator / Modulator | ||

| Sensors | ||

| Hydraulic Control Unit | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive electronic brake system market in 2030?

The market is forecast to reach USD 98.33 billion by 2030, reflecting a 5.53% CAGR.

Which technology segment is growing the fastest?

Brake-by-wire is set to record the quickest 5.55% CAGR through 2030.

Why are sensors attracting higher growth than ECUs?

ADAS integration and health-monitoring functions require more wheel-speed, pressure, and inertial sensors, lifting their CAGR to 5.58%.

Which region is expanding most rapidly?

Due to escalating safety regulations and fleet modernization, the Middle East and Africa will post the fastest 5.57% CAGR.

How will India’s two-wheeler ABS mandate influence demand?

Mandating ABS from 2026 unlocks an extensive OEM installation surge, benefiting local suppliers.

Page last updated on: