Automotive Gesture Recognition Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.28 Billion |

| Market Size (2030) | USD 4.96 Billion |

| Growth Rate (2025 - 2030) | 16.83% CAGR |

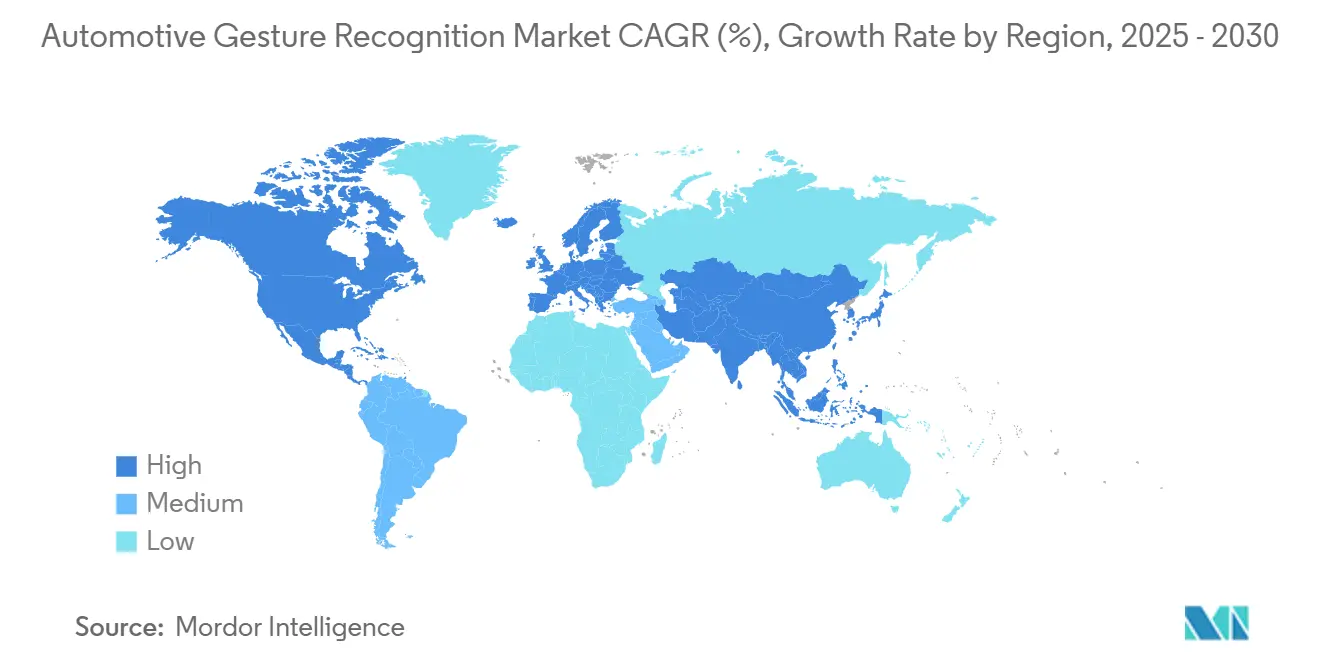

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Gesture Recognition Market Analysis by Mordor Intelligence

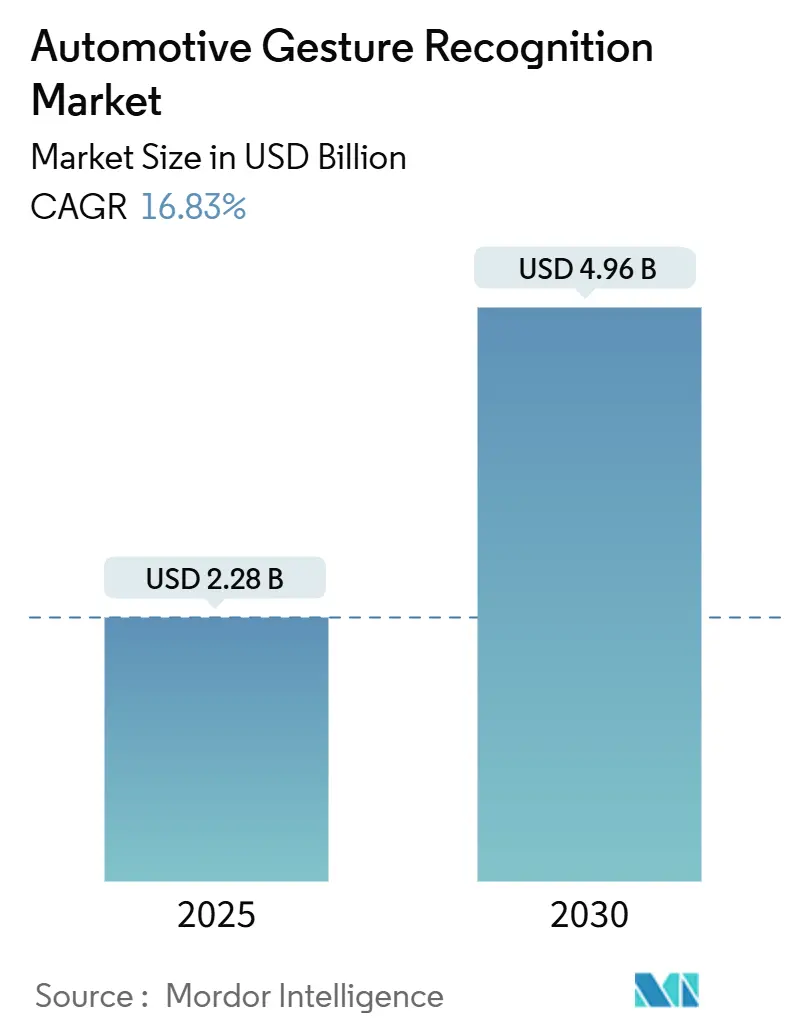

The automotive gesture recognition market size is valued at USD 2.28 billion in 2025 and is projected to climb to USD 4.96 billion by 2030, growing at a 16.83% CAGR during the forecast period. Regulatory deadlines in Europe and North America, the industry-wide shift toward software-defined vehicles, and the appeal of multimodal human–machine interfaces are the primary engines behind this growth. System integrators are repurposing in-cabin cameras mandated for driver monitoring, allowing gesture functionality to scale without prohibitive hardware additions. Sensor cost declines, especially in 3-D Time-of-Flight (ToF) devices, have opened the mid-range vehicle segment to capabilities once restricted to luxury trims. Concurrently, battery electric vehicle (BEV) architectures supply the high-speed data networks and stable power budgets required for continuous gesture processing, positioning the technology as a signature feature in premium EV cabins.

Key Report Takeaways

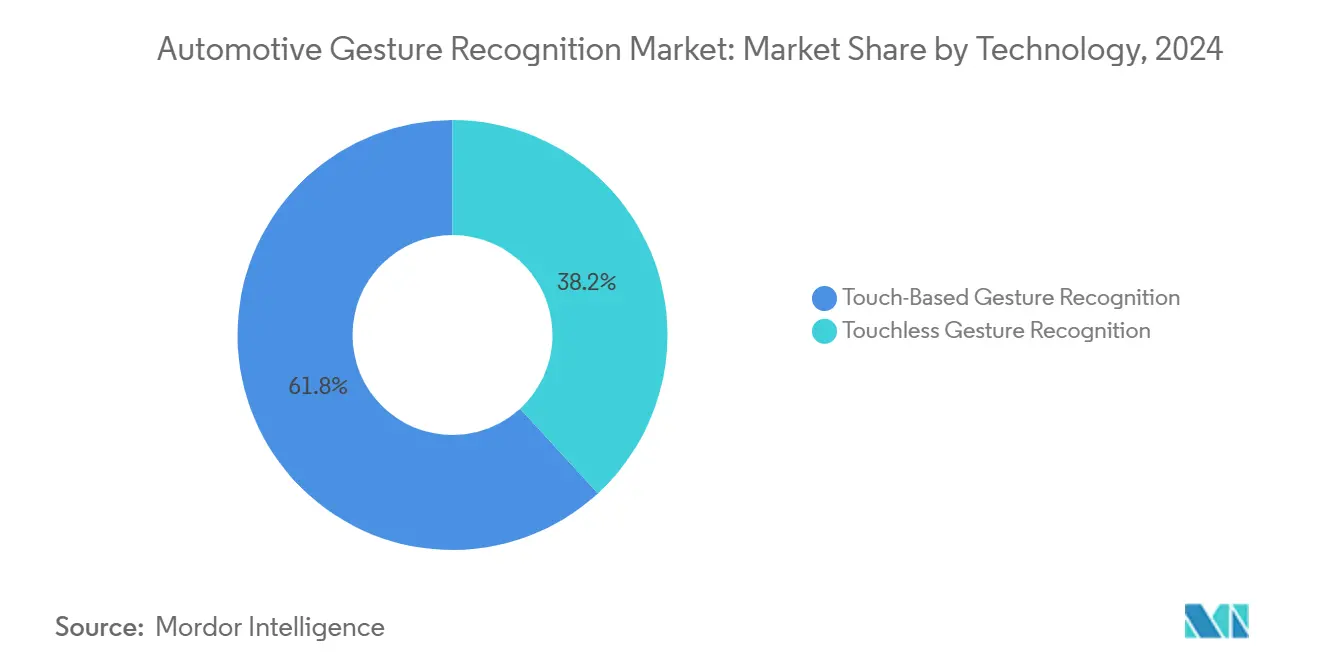

- By technology, touch-based systems led with 61.82% of the automotive gesture recognition market share in 2024, while touchless alternatives are advancing at an 18.23% CAGR through 2030.

- By component, hardware captured 73.26% of the automotive gesture recognition market size in 2024, whereas software is rising at an 18.18% CAGR to 2030.

- By gesture type, online dynamic gestures accounted for 66.29% of the automotive gesture recognition market share in 2024, and offline static gestures are forecast to expand at a 17.12% CAGR over the forecast period.

- By application, infotainment and navigation held 41.35% share of the automotive gesture recognition market size in 2024, while driver monitoring systems are projected to grow at an 18.65% CAGR to 2030.

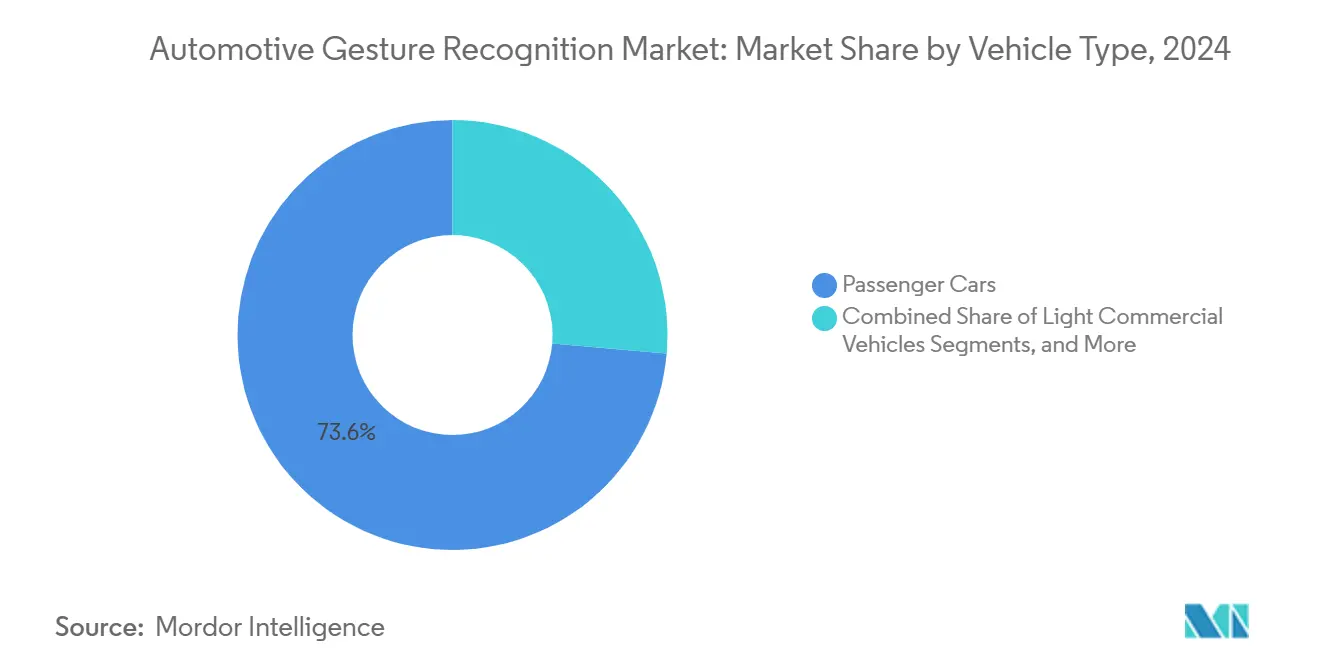

- By vehicle type, passenger cars dominated with 73.63% of the automotive gesture recognition market share in 2024, whereas medium and heavy commercial vehicles are set to record a 17.91% CAGR through 2030.

- By propulsion, internal-combustion vehicles retained the largest slice at 46.31% of the automotive gesture recognition market share in 2024. Still, battery electric vehicles are poised for the fastest expansion at a 19.41% CAGR to 2030.

- By distribution channel, OEM installations commanded 81.28% of the automotive gesture recognition market share in 2024, while the aftermarket segment is projected to climb at an 18.16% CAGR between 2025 and 2030.

- By geography, Asia-Pacific led with 32.73% of the automotive gesture recognition market share in 2024 and is expected to post the fastest regional growth at a 19.12% CAGR to 2030.

Global Automotive Gesture Recognition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory DMS Regulations Enabling Camera Reuse | +3.5% | EU primary, expanding to North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising ADAS-Driven Demand for Safer in-Cabin HMI | +3.2% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Cost Decline and Performance Gains in 3-D/ToF Sensors | +2.8% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Convergence Toward AI-Powered Multi-Modal Cockpits | +2.4% | North America and Europe leading, China scaling rapidly | Long term (≥ 4 years) |

| Premium EV and Luxury UX Differentiation Race | +2.1% | North America, Europe, China premium segments | Medium term (2-4 years) |

| Pandemic-Accelerated Demand for Touch-Free Cabins | +1.9% | Global, with sustained adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising ADAS-Driven Demand for Safer In-Cabin HMI

Level 2 plus automation requires the driver to retake control quickly when the assistance system disengages. Regulators responded by adopting UN ECE Regulation No. 171, effective September 2024, which obliges continuous driver state monitoring. Automakers now extend the same infrared cameras used for gaze tracking to interpret hand gestures that change infotainment settings without taking eyes off the road. Continental demonstrated how hand-on-wheel algorithms evolve into air-gesture engines with only a software update, accelerating deployment schedules and reducing bill-of-materials pressure. Feedback from early fleet trials shows a measurable reduction in interaction time compared with touchscreens, aiding regulatory compliance and safety ratings.

Convergence Toward AI-Powered Multimodal Cockpits

Next-generation cockpits run unified AI stacks that fuse voice, gesture, and gaze into a single intent model. Visteon integrates Qualcomm’s Snapdragon Cockpit for sub-30-millisecond inference latency, removing modality delays that previously confused users. Cerence avatars coordinate voice acknowledgments with on-screen prompts and subtle haptic feedback, closing the loop on confirmation doubts that historically limited gesture acceptance. This orchestration elevates gesture recognition from a novelty to a foundational layer in the human–vehicle relationship.

Premium EV and Luxury UX Differentiation Race

With range parity shrinking as a competitive lever, luxury EV manufacturers pivot to user experience. Mercedes-Benz’s 800-volt platform processes gestures locally, preserving driving range while eliminating latency. Lucid showcases how large curved displays supplement rather than replace touchless input, reserving gestures for tasks that benefit from minimal distraction, such as volume or HVAC controls. Early owner feedback confirms higher satisfaction when gestures complement voice and touch instead of being the sole control channel.

Pandemic-Accelerated Demand for Touch-Free Cabins

Hygiene consciousness persists in shared mobility and commercial fleets. Jaguar Land Rover’s predictive touch solution trims physical contact by half, meeting operators’ sanitation targets without slowing driver workflows. Fleets appreciate faster turnaround times between drivers, translating into more operational hours and lower cleaning costs. These practical benefits reinforce long-term demand even as private consumers return to conventional controls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM Liability Risk from Gesture Mis-Recognition | -2.3% | Global, with varying legal frameworks | Medium term (2-4 years) |

| High BOM and Integration Complexity | -2.1% | Global, particularly impacting volume segments | Short term (≤ 2 years) |

| Absence Of Global Gesture Taxonomy | -1.8% | Global, with fragmentation across regions | Medium term (2-4 years) |

| Data-Privacy Uncertainty for In-Cabin Imaging | -1.4% | EU and North America primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Absence of Global Gesture Taxonomy

Drivers switching between brands confront different motions for identical functions, causing confusion and hindering safety. ISO committees are developing reference libraries, yet regional preferences complicate convergence; subtle finger rolls preferred in Europe differ from broader sweeps favored in North America. Lack of standardization forces each OEM to curate proprietary datasets, increasing R&D cycles and slowing cross-industry learning.

Data-Privacy Uncertainty for In-Cabin Imaging

European privacy statutes treat biometric imagery with strict consent requirements. OEMs respond by processing data locally and discarding frames once inference is complete, but this increases chip cost and curtails cloud-based model improvement. Varying regional regulations demand configurable data pipelines, adding complexity that delays global rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Touch-Based Dominance Faces Touchless Disruption

Touch-based systems retained a 61.82% share of the automotive gesture recognition market in 2024. Capacitive sensors embedded in high-resolution displays let users pinch-zoom maps and swipe menus with familiar smartphone gestures. Although established, growth slows as incremental enhancements plateau. Touchless solutions, advancing at an 18.23% CAGR to 2030, exploit ToF depth data and millimeter-wave radar to capture mid-air motions. EU distraction rules accelerate demand because drivers keep their eyes ahead while gesturing inside a camera’s field of view. Glove-compatible interaction also appeals to commercial drivers working in cold or dusty environments where capacitive screens underperform.

Touchless adoption benefits from software libraries delivered over the air, extending installed hardware lifespans. As display bezels thin and cockpit real estate becomes scarce, eliminating reach-distance requirements helps designers craft minimalist interiors. The trade-off remains feedback; therefore, hybrid interfaces pair touchless input with haptic seat vibrators or voice confirmations to reassure users that a command executed correctly.

By Component: Hardware Foundation Enables Software Innovation

Hardware captured 73.26% share of the automotive gesture recognition market in 2024. Camera modules, illuminators, and controller ASICs form the physical backbone. ToF modules gain prominence over simple IR cameras because depth data raises recognition robustness under varying cabin light. Edge accelerators on zonal controllers perform neural-network inference locally, freeing infotainment SOCs for graphics workloads. Hardware cost curves now decline 8-10% annually, but absolute pricing still dictates feature availability in entry-level vehicles.

Software revenue grows at a CAGR of 18.18% to 2030 as over-the-air updates unlock new gesture vocabularies. Machine-learning pipelines ingest anonymized cabin footage to refine models for different ethnicities, hand sizes, and driving postures. Continuous improvement extends platform relevance, encouraging OEMs to treat gesture recognition as a service line rather than a one-time feature sale.

By Gesture Type: Dynamic Gestures Lead Despite Static Growth

Dynamic gestures, involving continuous movement, held a 66.29% share of the automotive gesture recognition market in 2024. Sweeping a palm to adjust audio or rotating fingers to dim ambient lighting feels natural and receives intuitive visual confirmation. Offline static poses, such as a held open hand signaling system mute, expand at a 17.12% CAGR through 2030. Static gestures excel when movement could impair vehicle control, for example, confirming driver presence on the steering wheel during hands-off automated cruising. Developers increasingly bundle both types, letting context engines decide which to accept based on speed, road conditions, and driver workload.

By Application: Infotainment Leadership Challenged by DMS Growth

Infotainment and navigation functions delivered a 41.35% share of the automotive gesture recognition market in 2024. Map zoom, media browsing, and call handling translate cleanly to gestures and differentiate premium trims. Driver monitoring systems, however, rise at an 18.65% CAGR to 2030 as regulators award safety credits for comprehensive attention assessment. Bundling gesture and monitoring tasks into a single camera shortens payback periods, motivating adoption across mid-range vehicles. Secondary targets include HVAC control, where air swipes adjust fan speed without contaminating screens, and cargo access, where foot kicks or hand waves open tailgates in delivery vans.

By Vehicle Type: Passenger Dominance with Commercial Acceleration

Passenger cars comprised 73.63% share of the automotive gesture recognition market in 2024, reflecting consumer appetite for convenience features. Medium and heavy commercial vehicles ramp at 17.91% CAGR as fleet operators link safer cabins to lower insurance premiums and driver retention. Long-haul fleets value fatigue detection augmented by gesture confirmation; if a driver fails to respond to a static hand pose request, the system flags possible drowsiness. Light commercial vans adopt simple two-gesture sets—door open and door close—supporting rapid curbside delivery without touching handles.

By Propulsion: ICE Baseline with BEV Innovation

Internal-combustion models still represent the most extensive installed base, at 46.31% share of the automotive gesture recognition market in 2024, including gesture capability. BEVs post the most substantial upside, expanding at 19.41% CAGR through 2030. Their 400- to 800-volt architectures supply clean power plus Ethernet or CAN-FD data paths indispensable for multi-sensor fusion. Gestures help declutter dashboards, aligning with minimalist EV design language. Hybrids bridge the gap, often inheriting gesture stacks from pure EV siblings to maintain part commonality.

By Distribution Channel: OEM Integration Dominates

Original equipment manufacturers (OEMs) accounted for an 81.28% share of the automotive gesture recognition market in 2024. Core systems must interface with body control modules and advanced driver-assistance functions that are usually inaccessible to aftermarket retrofits. Nevertheless, retrofit demand grows at a CAGR of 18.16% through 2030, as fleet managers install standalone gesture-enabled driver monitoring kits to meet corporate safety targets without buying new trucks. These plug-and-play kits connect via OBD ports and run on dedicated power inverters, avoiding profound vehicle alterations.

Geography Analysis

Asia-Pacific led 32.73% share of the automotive gesture recognition market in 2024, growing at a 19.12% CAGR to 2030. Chinese automakers fast-track Level 2 plus driver-assistance in mass-market sedans, multiplying addressable volumes. Japanese OEMs, early DMS adopters, embed gesture software into refreshed camera ECUs to maintain compliance with upcoming local guidelines. South Korean component makers leverage memory and imaging sensor expertise to supply competitively priced ToF modules, reinforcing regional supply chains.

North America maintains strong momentum through premium vehicle penetration and regulatory encouragement. The National Highway Traffic Safety Administration signals that driver monitoring will feature in future New Car Assessment Program revisions, prompting manufacturers to integrate gesture recognition alongside gaze tracking. Fleet operators in the United States view touchless control as a hygiene and efficiency enhancer, especially in last-mile delivery vans where drivers enter and exit cabins repeatedly each shift.

Europe spearheads regulatory detail, requiring distraction-warning technology from 2024 onward. German luxury brands embed complex gesture sets into flagship models, using multimodal interfaces to differentiate. Strict data-privacy law shapes architecture decisions; most European vehicles process gesture streams fully on edge devices, discarding images after inference. Eastern European assembly plants adopt the same platforms for export models, propagating technology to wider price bands.

Emerging regions—Latin America, the Middle East, and Africa—see early deployments confined to imported premium vehicles. Once 3-D sensor costs fall further, local assemblers are expected to integrate basic gesture features, propelled by ride-hailing fleets prioritizing low-contact interiors to boost rider confidence.

Competitive Landscape

The automotive gesture recognition market shows moderate concentration. Tier-1 suppliers secure scale advantages by snapping up niche algorithm firms. PreAct’s 2024 purchase of Gestoos supplied hand-trajectory IP, shortening its time to embed gesture capability into existing short-range lidar units. Visteon pairs Snapdragon silicon with its display controllers, delivering turnkey cockpit solutions to OEMs seeking shorter bill-of-materials lists. Cerence links gesture inputs to conversational AI avatars, building lock-in through cloud analytics and over-the-air feature upgrades.

Edge AI specialists such as Cipia position themselves on privacy grounds, offering inside-vehicle inference that satisfies GDPR without cloud links. Camera vendors partner with ASIC providers to offer pre-validated reference designs, cutting certification cycles. Start-up barriers rise as Euro NCAP test protocols grow more stringent, rewarding incumbents that hold automotive-grade functional safety credentials.

White-space remains in heavy-duty trucks, agricultural machinery, and off-highway equipment where vibration and extreme temperatures complicate optical sensing. Suppliers able to ruggedize ToF modules for these environments could unlock new revenue bands while broadening sensor volumes that lower overall cost curves for the automotive gesture recognition market.

Automotive Gesture Recognition Industry Leaders

Continental AG

Robert Bosch GmbH

Visteon Corporation

Sony Corporation

Qualcomm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Fuyao Glass Industry Group Co., Ltd. introduced an intelligent dimming side window glass, offering privacy and sunshade functionality for enhanced mobility. Using dye-based liquid crystal technology, it ensures precise control via voltage adjustments, delivering a response time of under one second for instant brightness adjustments.

- September 2024: UN ECE Regulation No. 171 entered force, mandating continuous driver state monitoring and opening regulatory pathways for camera-enabled gestures in driver control assistance systems.

- July 2024: Stellantis recognized Emotiva in its Venture Awards program for developing AI technology that monitors driver attention and integrates with gesture-controlled infotainment systems for revenue generation.

Global Automotive Gesture Recognition Market Report Scope

| Touch-Based Gesture Recognition |

| Touchless Gesture Recognition |

| Hardware | Sensors |

| Cameras | |

| Controllers | |

| Software | AI Algorithms |

| Gesture Libraries |

| Online Dynamic |

| Offline Static |

| Infotainment and Navigation Control |

| Climate and Lighting Control |

| Door/Window Operation |

| Driver Monitoring Systems (DMS) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-In Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Touch-Based Gesture Recognition | |

| Touchless Gesture Recognition | ||

| By Component | Hardware | Sensors |

| Cameras | ||

| Controllers | ||

| Software | AI Algorithms | |

| Gesture Libraries | ||

| By Gesture Type | Online Dynamic | |

| Offline Static | ||

| By Application | Infotainment and Navigation Control | |

| Climate and Lighting Control | ||

| Door/Window Operation | ||

| Driver Monitoring Systems (DMS) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-In Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the automotive gesture recognition market today?

The automotive gesture recognition market size stood at USD 2.28 billion in 2025 and is forecast to reach USD 4.96 billion by 2030.

What CAGR is expected for gesture technology in cars?

The market is projected to register a 16.83% CAGR from 2025 to 2030, reflecting rapid mainstream adoption.

Which vehicle powertrain segment will see the fastest gesture uptake?

Battery electric vehicles are projected to post a 19.41% CAGR through 2030 as gesture controls complement minimalist EV interiors.

Why is Asia-Pacific the leading region for gesture recognition?

Aggressive autonomous-driving rollouts, supportive regulations, and strong local sensor supply chains give Asia-Pacific the largest share and fastest regional growth.

What regulatory change most influences gesture adoption?

The European Advanced Driver Distraction Warning requirement, effective from 2024, compels in-cabin cameras that can also perform gesture recognition via software updates.

Page last updated on: