Automotive Gesture Recognition Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

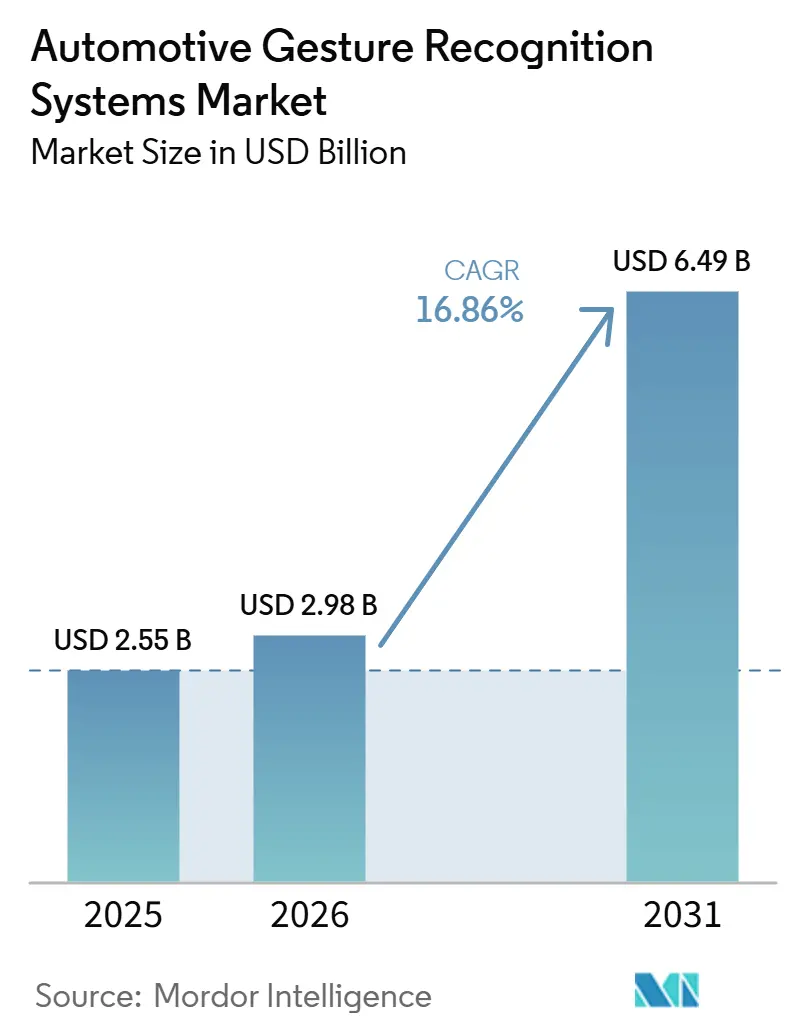

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 6.49 Billion |

| Growth Rate (2026 - 2031) | 16.86% CAGR |

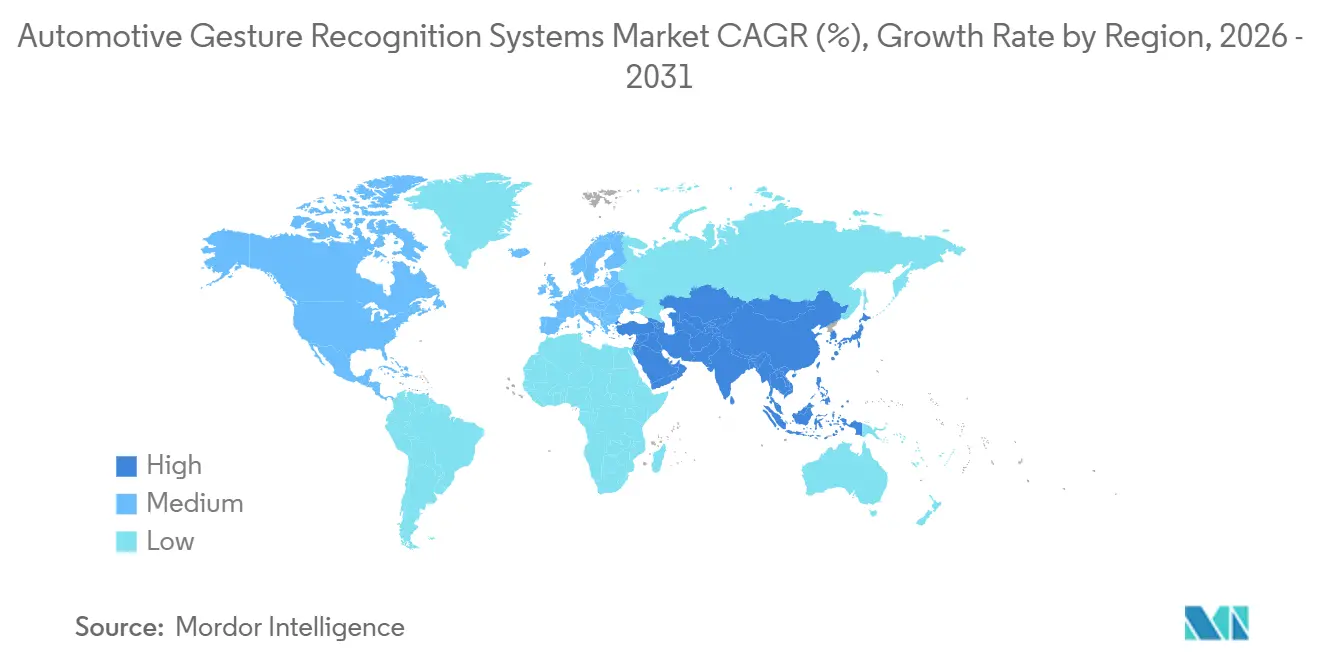

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Gesture Recognition Systems Market Analysis by Mordor Intelligence

The automotive gesture recognition systems market size was valued at USD 2.55 billion in 2025 and is projected to reach USD 6.49 billion by 2031 from USD 2.98 billion in 2026, expanding at a 16.86% CAGR. Rising demand for touch-free human-machine interfaces, AI-enabled in-cabin monitoring, and premium cockpit experiences continues to shape this growth trajectory. At the same time, stricter regulations aimed at reducing driver distraction are speeding up deployment in Europe and North America. Camera-based platforms currently lead the market, but AI software engines that enhance context awareness and combine inputs from multiple sensors are gaining ground quickly as over-the-air upgradable software becomes a key differentiator. Post-pandemic hygiene expectations, fleet efficiency goals, and autonomous vehicle roadmaps are also driving investment, giving suppliers that bring together hardware, algorithms, and systems integration a clear advantage. However, higher system costs and inconsistent environmental performance limit adoption in price-sensitive segments, prompting OEMs to adopt modular architectures that support phased feature rollouts.

Key Report Takeaways

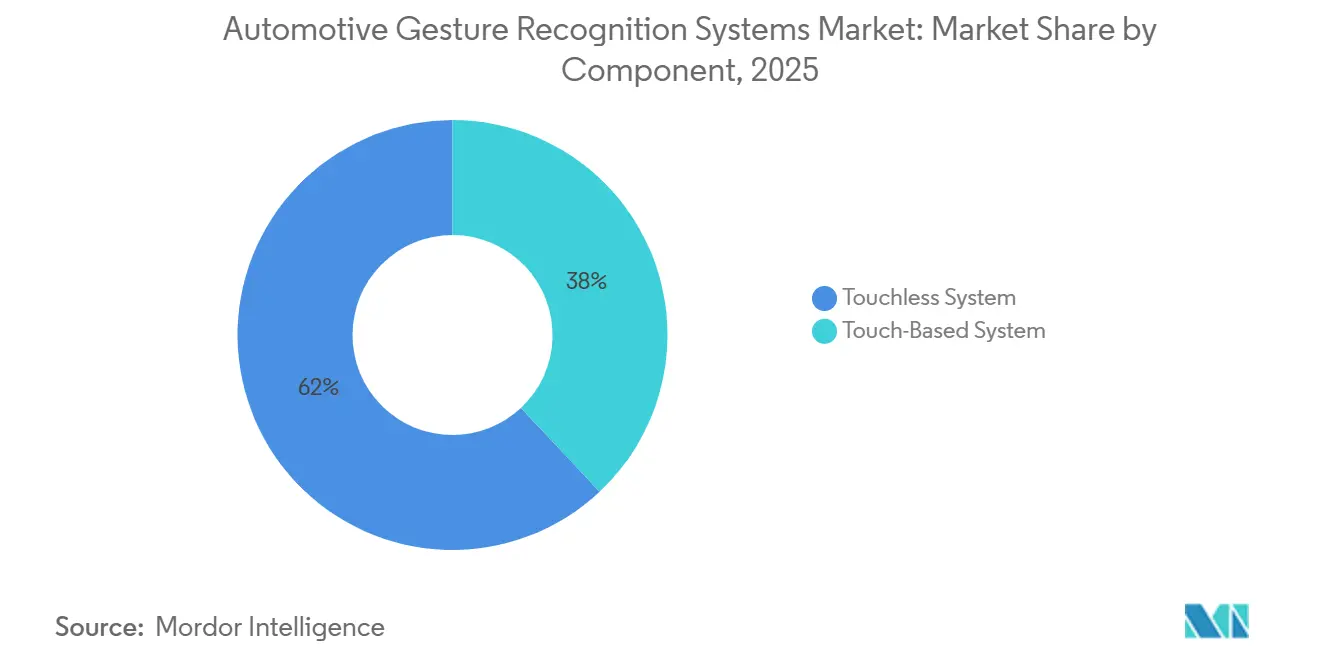

- By component, touchless systems led with 62.01% revenue share in 2025; touchless is forecasted to grow at a 17.23% CAGR through 2031.

- By authentication type, hand/fingerprint held 48.47% of the automotive gesture recognition systems market share in 2025, while vision/iris authentication posts the highest projected 19.38% CAGR to 2031.

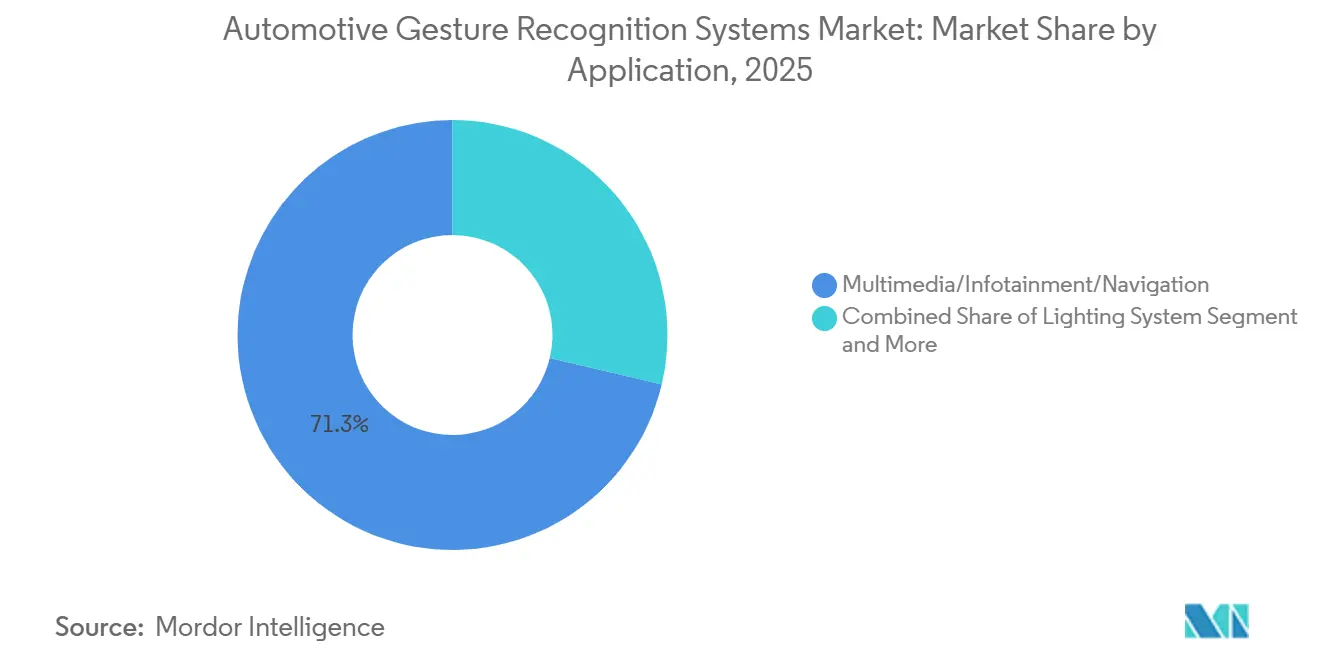

- By application, multimedia/infotainment captured 71.29% share of the automotive gesture recognition systems market size in 2025; lighting systems are advancing at a 20.14% CAGR through 2031.

- By technology, camera-based platforms held 54.63% of the automotive gesture recognition systems market share in 2025; AI software platforms are set to record the quickest 22.49% CAGR from 2026-2031.

- By geography, Europe accounted for 34.18% of 2025 revenue, whereas Asia-Pacific exhibits the fastest 18.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Gesture Recognition Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Enabled Multimodal Monitoring | +4.3% | Asia-Pacific Core, Spillover Worldwide | Long Term (≥ 4 Years) |

| Advanced HMI Demand for Premium Experience | +3.2% | Global, Premium Segments | Medium Term (2-4 Years) |

| Regulatory Focus on Driver-Distraction | +2.8% | Europe and North America; Emerging Asia-Pacific | Short Term (≤ 2 Years) |

| OEM Differentiation via Gesture Infotainment | +2.1% | Global, Led by German and Japanese OEMs | Medium Term (2-4 Years) |

| Commercial-Vehicle Hygiene and Efficiency | +1.9% | North America and Europe Commercial Fleets | Short Term (≤ 2 Years) |

| Post-Pandemic Touch-Free Preference | +1.7% | Global Consumer Shift | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Advanced HMI Demand Drives Premium Vehicle Differentiation

Premium vehicle manufacturers are deploying gesture recognition as a core differentiator in increasingly competitive luxury segments, with BMW's Panoramic iDrive and Mercedes MBUX Interior Assist systems demonstrating how touchless controls create perceived technological superiority. Continental's CES 2025 biometric demonstration car showcased integrated gesture and biometric authentication, enabling personalized vehicle settings through simple hand movements while maintaining driver attention on the road. The integration extends beyond infotainment to climate control, seat adjustment, and ambient lighting, with Jaguar Land Rover's contactless touchscreen technology eliminating physical contact while preserving tactile feedback through ultrasonic haptics. This trend reflects OEMs' recognition that gesture control creates emotional engagement and perceived innovation value that justifies premium pricing, particularly as traditional mechanical differentiation becomes commoditized across vehicle segments.

Regulatory Frameworks Accelerate Driver Monitoring Integration

European Union Advanced Driver Distraction Warning (ADDW) regulations mandating real-time driver monitoring in new heavy commercial vehicles by July 2024 have catalyzed gesture recognition adoption as part of comprehensive driver state assessment systems[1]"Truck driver monitoring — how it works, and why it’s important," Visage Technologies, visagetechnologies.com.. NHTSA driver distraction guidelines and Euro NCAP protocols increasingly recognize gesture-based controls as safer alternatives to touchscreen interaction, provided they meet specific attention-demand thresholds and incorporate fail-safe mechanisms. The regulatory influence extends beyond safety compliance to data privacy requirements, with GDPR and emerging Chinese data security laws requiring on-device processing for gesture recognition to minimize personal data transmission[2]"Automotive Industry Global Updates – Asia," Morgan Lewis, morganlewis.com.. Commercial vehicle operators report a 37% reduction in speeding violations and a 56% decrease in seatbelt non-compliance when gesture-enabled driver monitoring systems provide real-time feedback, demonstrating measurable safety improvements that support regulatory adoption[3]"Federal Motor Carrier Safety Administration’s Advanced System Testing Utilizing a Data Acquisition System on the Highways (FAST DASH) Safety Technology Evaluation Project #2: Driver Monitoring Final Report," U.S. Department of Transportation, Virginia Tech Transportation Institute, osap.ntl.bts.gov..

AI Software Platforms Enable Context-Aware Recognition

Synaptics' Astra AI-Native platform and Visteon's cognitoAI framework represent the industry's evolution toward intelligent gesture recognition that adapts to individual users, lighting conditions, and driving contexts through machine learning algorithms. NVIDIA DRIVE IX and BlackBerry IVY platforms demonstrate multimodal fusion capabilities that combine gesture inputs with voice commands, eye tracking, and vehicle sensor data to create contextually appropriate responses. Infineon's DEEPCRAFT edge AI processing enables real-time gesture classification with sub-10ms latency while consuming less than 2W power, addressing the dual challenges of responsiveness and energy efficiency in battery-electric vehicles. The competitive advantage lies in algorithms that distinguish intentional gestures from incidental hand movements, with Continental's systems achieving over 99% accuracy in controlled environments while maintaining 91.56% performance in real-world driving conditions.

Commercial Vehicle Efficiency Drives Contactless Adoption

Fleet operators are implementing gesture recognition systems to address dual challenges of driver hygiene and operational efficiency, with Netradyne's Driveri platform demonstrating up to 67% reduction in distracted driving through AI-powered gesture and gaze monitoring. Queensland Trucking Association's "Eyes on Fatigue" pilot program across 50 commercial drivers validates the effectiveness of gesture-based fatigue detection, with Seeing Machines' Guardian system using face and gaze tracking to trigger preventive interventions before critical drowsiness events. Commercial vehicle manufacturers are integrating gesture recognition into broader telematics platforms, enabling remote fleet monitoring and predictive maintenance alerts through analysis of driver behavior patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Incremental System Cost | -2.4% | Global, Price-Sensitive Segments | Short Term (≤ 2 Years) |

| Performance Limits Under Extreme Factors | -1.8% | Climate-Diverse Regions Worldwide | Medium Term (2-4 Years) |

| Data-Privacy Concerns With Camera Monitoring | -1.5% | Europe, North America, Increasingly Global | Short Term (≤ 2 Years) |

| Absence of Standardized Gesture Vocabulary | -1.1% | Global OEM Ecosystem, Led by Emerging Asia-Pacific | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Cost Constraints Limit Mass Market Penetration

Advanced AI-enabled platforms add incremental system costs that can slow adoption in price-sensitive market segments, especially in emerging markets where buyers remain highly cost-conscious. These costs come from several components, including specialized cameras, infrared sensors, dedicated processing units, and software licensing fees. Camera-based systems also need high-resolution sensors that can perform reliably across varying lighting conditions. Integration adds another layer of cost because OEMs must test and validate gesture recognition systems across thousands of use cases and environmental conditions to comply with automotive safety standards. These validation cycles can take 18-24 months longer than traditional HMI development timelines. The cost challenge becomes more pronounced in commercial vehicle segments, where fleet operators expect a rapid return on investment. Therefore, gesture systems need to show measurable productivity gains or regulatory compliance benefits to justify the additional costs.

Environmental Performance Limitations Challenge Reliability

Automotive gesture recognition systems face significant performance degradation under extreme lighting conditions and vehicle vibration, with camera-based systems experiencing up to 40% accuracy reduction in direct sunlight or complete darkness scenarios. Ultrasonic and radar-based alternatives offer improved environmental robustness but struggle with false activation rates during highway driving, where engine vibration and road noise create interference patterns that can trigger unintended gesture recognition events. Temperature extremes present additional challenges, with infrared sensors requiring thermal compensation algorithms to maintain accuracy across -40°C to +85°C automotive operating ranges, adding computational overhead and system complexity. The reliability constraints become critical in safety-related applications where false positives could distract drivers or false negatives could prevent emergency interventions, requiring redundant sensing modalities and fail-safe mechanisms that increase system cost and complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Touchless Systems Accelerate Market Transformation

Touchless systems dominated the automotive gesture recognition market with 62.01% share in 2025 and are projected to expand at 17.23% CAGR through 2031, significantly outpacing touch-based alternatives as hygiene concerns and advanced AI capabilities drive adoption across premium and commercial vehicle segments. The touchless segment benefits from post-pandemic behavioral shifts toward contactless interaction and regulatory pressure for driver distraction reduction, with systems like Mercedes MBUX Interior Assist and BMW Panoramic iDrive demonstrating consumer acceptance of air gesture controls for infotainment and climate functions.

Aptiv's AI-based Advanced Occupancy Classification platform identifies occupants by height, weight, and body position, suggesting convergence toward comprehensive contactless vehicle interaction ecosystems that extend beyond gesture recognition to include biometric access and personalized settings. The segment's growth trajectory reflects OEMs' strategic positioning of touchless interfaces as premium differentiators while addressing practical concerns about driver distraction and operational hygiene in shared mobility applications.

By Authentication Type: Vision Systems Drive Biometric Evolution

Hand/fingerprint recognition maintained 48.47% market share in 2025, reflecting established reliability and user familiarity, while vision/iris authentication emerges as the fastest-growing segment at 19.38% CAGR through 2031, supported by breakthrough partnerships like Smart Eye's USD 4.5 million iris recognition licensing deal with Fingerprint Cards.

The authentication landscape reflects broader automotive trends toward personalization and security, with vision-based systems offering advantages in shared mobility scenarios where multiple users require rapid, hygienic authentication without physical contact. Mercedes-Benz patents for biometric vehicle access demonstrate OEM commitment to seamless authentication experiences that eliminate traditional key-based systems while enhancing security through multi-factor biometric verification.

By Application: Lighting Systems Emerge as High-Growth Opportunity

Multimedia/infotainment applications commanded 71.29% market share in 2025, reflecting initial gesture recognition deployment in non-critical entertainment and navigation functions where user acceptance and system reliability could be validated without safety implications. However, lighting systems represent the fastest-growing application segment at 20.14% CAGR through 2031, driven by gesture-controlled ambient lighting, automatic headlight adjustment, and emergency lighting activation that enhance both comfort and safety without requiring complex integration with critical vehicle systems. Other applications, including climate control, seat adjustment, and window operation, demonstrate steady adoption as OEMs expand gesture recognition beyond initial infotainment deployments.

The application evolution reflects OEMs' strategic approach to gesture recognition deployment, beginning with non-critical entertainment functions to build user confidence before expanding to comfort and safety-related controls. Lighting applications offer particular advantages for gesture recognition as they provide immediate visual feedback to confirm command recognition, helping users develop trust in the technology while avoiding safety-critical failure modes. The segment's growth potential extends to autonomous vehicle applications where passengers require intuitive control over cabin environment without traditional driver-focused interfaces, with Sony Honda Mobility's AFEELA 1 demonstrating comprehensive gesture-controlled lighting and entertainment systems designed for autonomous operation.

By Technology: AI Software Platforms Lead Innovation Wave

Camera-based systems held 54.63% market share in 2025, leveraging established computer vision algorithms and benefiting from declining sensor costs and improving low-light performance. AI software platforms emerge as the fastest-growing technology segment at 22.49% CAGR through 2031. Capacitive/infrared proximity sensors and ultrasonic/radar gesture sensors provide complementary capabilities for specific applications requiring environmental robustness or privacy protection.

The technology landscape reflects the automotive industry's evolution toward software-defined vehicles, where gesture recognition algorithms can be updated over-the-air to improve performance and add new capabilities throughout the vehicle lifecycle. AI software platforms enable personalization features that adapt to individual user preferences and driving contexts. The segment's growth trajectory aligns with broader automotive AI adoption, where gesture recognition becomes one component of comprehensive in-cabin monitoring systems that assess driver attention, passenger comfort, and vehicle security through integrated sensor fusion and edge computing platforms.

Geography Analysis

Europe commanded 34.18% of 2025 revenue, driven by strict distraction regulations and early premium-segment deployments. Germany anchors regional leadership with Continental, Bosch, and Infineon providing vertically integrated solutions. BMW’s 2025 7-Series offers air-swipe seat massage activation, a feature now migrating to mid-range 5-Series trims, signaling trickle-down diffusion. French supplier Valeo embeds dual-camera mirror modules that retrofit older fleets, broadening Europe’s aftermarket potential.

Asia-Pacific posts the fastest 18.72% CAGR, fueled by China’s intelligent connected vehicle mandate and Japan’s sensor innovation pipeline. Government incentives in Beijing and Shanghai grant tax credits for driver-monitoring features, jump-starting gesture system adoption in domestic brands aiming for export compliance. Sony targets 43% global share of automotive image sensors by fiscal 2026, banking on gesture and monitoring demand. Korean OEMs integrate gesture with 5G infotainment to capitalize on high streaming uptake, while Indian two-wheeler startups trial helmet-mounted gesture modules for e-scooters, hinting at untapped niches.

North America progresses steadily as commercial fleets prioritize safety telematics. Lytx and Netradyne packages that knit hand signals with AI event detection enjoy strong uptake among last-mile operators, offsetting slower passenger-car rollout due to liability concerns. Canada funds R&D tax credits for gesture-based assistive tech, supporting suppliers’ north-of-border software labs. Latin America, the Middle East, and Africa yield modest volumes today but represent long-range expansion as 4G connectivity and ride-hailing mature, creating fertile ground for cloud-linked gesture analytics.

Competitive Landscape

The automotive gesture recognition systems market shows moderate fragmentation: the top five players together hold the majority of the share, leaving room for innovative entrants. Continental leverages deep vehicle-domain expertise to ship turnkey biometric cockpits. Its latest offerings showcase time-to-market leadership by integrating iris, mood, and gesture layers on a single zonal ECU. Synaptics differentiates with an AI-native stack that customers can skin via software, reducing hardware lock-in risk. Visteon rides the software-defined cockpit wave, partnering with Qualcomm to bundle gesture into high-compute digital cluster domains.

Specialists such as Ultraleap and Cipia Vision focus on algorithm edge cases like accurate mid-air pinch and fatigue micro-gestures, often licensing IP to Tier-1s hungry to fill performance gaps. Camera sensor giants Sony and onsemi drive hardware evolution, releasing stacked-pixel CMOS parts optimized for flicker-free LED detection, crucial for outdoor gestures. NVIDIA, Qualcomm, and Renesas vie for cockpit SoC design wins, adding dedicated NPU blocks that streamline gesture inference at single-digit watt budgets.

Smart Eye and Fingerprint Cards are bringing together eye-tracking and iris-recognition capabilities to address the premium biometric niche, where accuracy, security, and seamless user experience matter most. Seeing Machines, meanwhile, is working with truck OEMs to integrate Guardian directly into factory-built cockpits, reducing the need for aftermarket retrofit kits. This shift suggests that the competitive landscape is moving toward more connected ecosystems rather than standalone modules, favoring companies that can combine hardware, software, and compliance consulting into a single, easier-to-adopt offering.

Automotive Gesture Recognition Systems Industry Leaders

-

Continental AG

-

Sony Corporation

-

Synaptics Incorporated

-

Visteon Corporation

-

NXP Semiconductors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Aptiv launched the industry’s first camera-only occupant detection system. Its AI-based Advanced Occupancy Classification platform identifies occupants by height, weight, and body position, distinguishing adults, children, infants in carriers, and objects without in-seat pressure hardware.

- April 2026: Ford filed a patent application for software that uses in-vehicle cameras, sensors, and acoustic signals to read occupants’ lips. The system could emit inaudible sound waves and use machine learning to analyze echoes from the user’s lips and mouth.

- December 2025: LG Electronics (LG) unveiled an immersive experiential space at CES 2026 that will bring its future mobility vision to life through Affectionate Intelligence, showing how AI will make the cabin more intuitive and human-centered for every ride.

Global Automotive Gesture Recognition Systems Market Report Scope

The Automotive Gesture Recognition Systems market is segmented by component, authentication type, application, technology, and geography.

By Component, the market is segmented into Touch-Based System and Touchless System. By Authentication Type, the market is segmented into Hand/Fingerprint, Face, Vision/Iris, and Others. By Application, the market is segmented into Multimedia/Infotainment/Navigation, Lighting System, and Others. By Technology, the market is segmented into Camera-Based Systems, Capacitive/Infra-red Proximity Sensors, Ultrasonic/Radar Gesture Sensors, and AI Software Platforms. By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (United Kingdom, Germany, Spain, Italy, France, Russia, and Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, Egypt, South Africa, and Rest of Middle East and Africa).

Market forecasts are provided in terms of Value (USD).

| Touch-Based System |

| Touchless System |

| Hand/Fingerprint |

| Face |

| Vision/Iris |

| Others |

| Multimedia/Infotainment/Navigation |

| Lighting System |

| Others |

| Camera-Based Systems |

| Capacitive/Infra-red Proximity Sensors |

| Ultrasonic/Radar Gesture Sensors |

| AI Software Platforms |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Component | Touch-Based System | |

| Touchless System | ||

| By Authentication Type | Hand/Fingerprint | |

| Face | ||

| Vision/Iris | ||

| Others | ||

| By Application | Multimedia/Infotainment/Navigation | |

| Lighting System | ||

| Others | ||

| By Technology | Camera-Based Systems | |

| Capacitive/Infra-red Proximity Sensors | ||

| Ultrasonic/Radar Gesture Sensors | ||

| AI Software Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Question

Answer

How big is the automotive gesture recognition systems market today?

The market stands at USD 2.98 billion in 2026 and is projected to reach USD 6.49 billion by 2031.

Which component leads adoption of gesture control?

Touchless systems account for 62.01% of 2025 revenue and are scaling at a 17.23% CAGR.

What region is growing the fastest for gesture recognition in vehicles?

Asia-Pacific shows the quickest 18.72% CAGR, propelled by China’s intelligent connected vehicle policies and Japanese sensor innovation.

Which application segment is expected to outpace others through 2031?

Gesture-controlled lighting systems are forecast to expand at a 20.14% CAGR, the fastest among all applications.

Who are the key players shaping market innovation?

Continental, Synaptics, Visteon, Sony Semiconductor Solutions, and Ultraleap lead by offering integrated hardware-software platforms and strategic partnerships.

What is the main barrier to widespread deployment in mass-market cars?

Added hardware and validation costs of USD 150-400 per vehicle create price pressure, especially in cost-sensitive segments.

Page last updated on: