Automotive Human Machine Interface Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

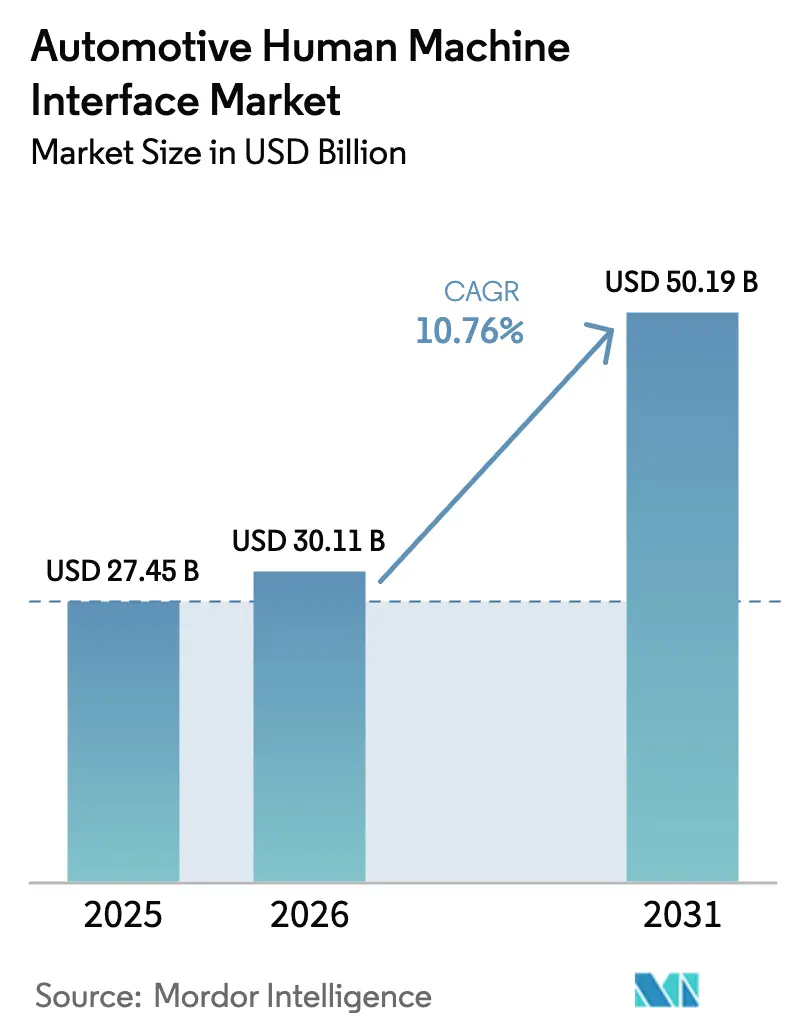

| Market Size (2026) | USD 30.11 Billion |

| Market Size (2031) | USD 50.19 Billion |

| Growth Rate (2026 - 2031) | 10.76% CAGR |

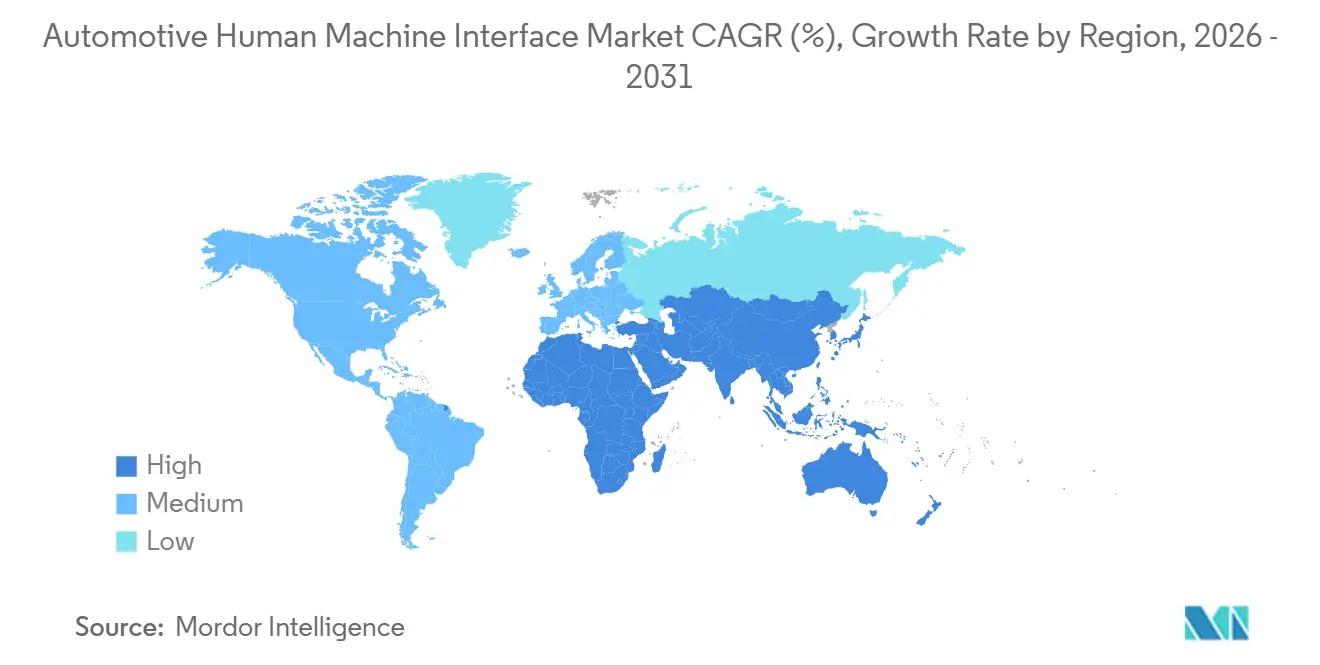

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Human Machine Interface Market Analysis by Mordor Intelligence

The automotive human machine interface market size was valued at USD 27.45 billion in 2025 and estimated to grow from USD 30.11 billion in 2026 to reach USD 50.19 billion by 2031, at a CAGR of 10.76% during the forecast period (2026-2031). This trajectory underscores how cockpit controls have shifted from physical knobs to software-defined experiences that now span voice, gesture, haptic, and visual channels. Automakers regard the interface as a revenue catalyst, using over-the-air pathways to refine features after delivery and to sell upgrades on demand. Regulatory mandates that curb distraction, notably United Nations Economic Commission for Europe (UNECE) R171 and the National Highway Traffic Safety Administration (NHTSA) over-the-air guidance, press suppliers to design layouts that cut cognitive load while still feeding rich data to driver-assistance stacks.

Key Report Takeaways

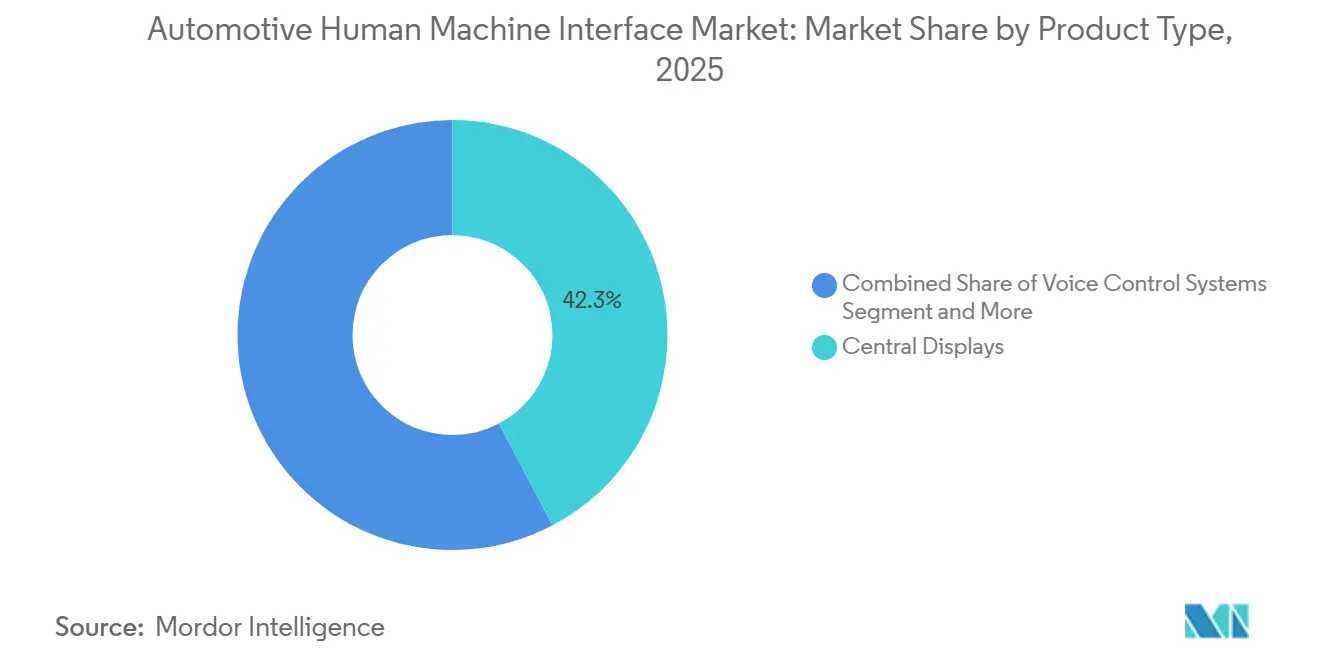

- By product type, central displays led with 42.28% of the human machine interface market share in 2025, while augmented-reality head-up displays are set to progress at a 17.06% CAGR through 2031.

- By access type, multimodal systems accounted for 51.62% of revenue in 2025 and are advancing at a 14.93% CAGR through 2031.

- By interaction modality, visual channels held a 67.14% share in 2025 and are growing fastest at 15.18% CAGR.

- By vehicle type, mid-price passenger cars captured a 35.68% share in 2025, whereas luxury passenger cars are poised to exhibit the quickest 12.34% CAGR toward 2031.

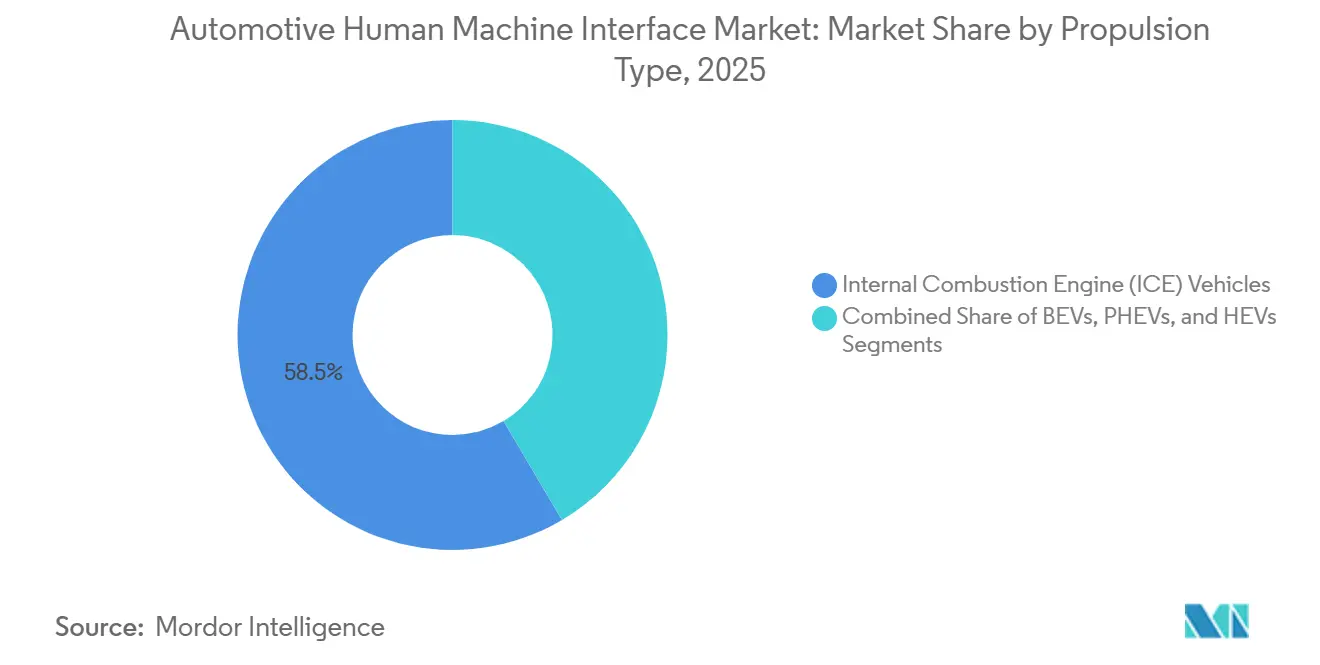

- By propulsion, internal-combustion models represented 58.47% in 2025; however, battery-electric vehicles are poised to grow at a 15.36% CAGR over the forecast period.

- By sales channel, OEM-installed systems claimed 81.12% share in 2025, but aftermarket retrofits are climbing at a 14.39% CAGR through 2031.

- By geography, Asia-Pacific dominated with 47.88% in 2025, whereas the Middle East and Africa region is set to accelerate at a 13.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Human Machine Interface Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Connected-Infotainment | +2.1% | Global, with Asia-Pacific leadership | Medium term (2-4 years) |

| ADAS and Autonomous-Driving Dependency on Intuitive HMI | +1.8% | North America and Europe regulatory focus | Long term (≥ 4 years) |

| Regulatory Focus | +1.7% | Europe, North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Shift Toward Software-Defined Vehicles | +1.5% | Global, led by premium segments | Medium term (2-4 years) |

| In-Cabin Health and Wellness Interface Innovations | +0.7% | Premium markets, North America and Europe | Long term (≥ 4 years) |

| Generative-AI Copilots | +0.6% | Global, early adoption in premium vehicles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Connected-Infotainment Ecosystems

Consumers treat the vehicle as a node in a wider digital mesh, expecting seamless handoffs among phone, home assistant, and car. TomTom and Microsoft introduced a conversational navigation platform in 2025 that employs Azure OpenAI Service to deliver real-time traffic storytelling. Voice platforms such as SoundHound, which doubled original equipment manufacturer wins to 18 brands in 2024, allow multi-turn dialogue for climate, media, and smart-home control. Always-on connectivity unlocks usage-based insurance and predictive-maintenance alerts, producing post-sale revenue that offsets hardware cost. As edge computing migrates to cockpit domain controllers, software updates can deliver new features without hardware swaps, shrinking the gap between consumer-electronics refresh cycles and automotive development. The human machine interface market, therefore, benefits from a virtuous loop in which richer cloud services justify connectivity subscriptions that in turn demand more capable interfaces.

ADAS and Autonomous-Driving Dependency on Intuitive HMI

Level 2+ assistance keeps hands loosely on the wheel while transferring lateral and longitudinal control for extended stretches. United Nations Economic Commission for Europe (UNECE) R171[1]"UN Regulation on uniform provisions concerning the approval of vehicles with regard to Driver Control Assistance Systems," UNECE, unece.org., enforced from 2024, obliges systems to communicate status and takeover prompts by escalating audio-visual cues. Mercedes-Benz Drive Pilot uses tri-color light strips and steering-wheel light-emitting diodes to signal role changes, minimizing ambiguity. Suppliers embed geo-fencing and weather limits into AR head-up displays that overlay safe-operation bounds directly on the road, trimming eyes-off-road time. Driver-monitor cameras ensure gaze compliance and can suspend assisted mode when attention drifts. As autonomous functions inch toward Level 3, the human machine interface market must visualize vehicle intent clearly enough to sustain driver trust, or regulators could throttle roll-outs.

Regulatory Focus on Driver-Distraction Mitigation

National Highway Traffic Safety Administration (NHTSA) guidelines cap any nondriving task at 12 seconds total glance time, with every single look under 2 seconds[2]"Visual-Manual NHTSA Driver Distraction Guidelines for Portable and Aftermarket Electronic Devices," National Highway Traffic Safety Administration, Federal Register, federalregister.gov.. Volkswagen backtracked on touch-only layouts, restoring rotary dials in the 2025 ID.4 facelift after user complaints and regulatory attention. China’s GB 15084-2024[3]"TC11-2023-02 Revision of GB Standards for Motor Vehicles and Parts in China," CNCA Automotive and Parts Technical Expert Group, china-certification.com. bars forward-facing video unless the vehicle is stationary, compelling original equipment manufacturers to geofence entertainment apps. Driver-monitor cameras enforce compliance by disabling features when attention strays, and ISO 21434 embeds cyber requirements that block spoofing. These measures accelerate the adoption of head-up displays and physical shortcuts that present essential information with minimal visual load, boosting the human-machine interface market.

Shift Toward Software-Defined Vehicles and OTA UI Upgrades

Tesla normalized over-the-air feature drops, prompting legacy original equipment manufacturers to adopt rolling software releases. General Motors’ Ultifi platform commits to quarterly interface refreshes, enabling A/B tests of menu hierarchies across Chevrolet, GMC, and Cadillac fleets. The eSync Alliance published a 2025 framework that covers delta compression and fail-safe boots, cutting data bills and bricking risk. ISO 24089, finalized in 2024, now treats software updates that affect safety functions with the same rigor as recalls. Consequently, the human machine interface market earns recurring revenue from feature unlocks while guarding against version rollbacks that could breach compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced HMI Hardware Stacks | -1.4% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Cyber-Security and Data-Privacy Vulnerabilities | -0.9% | Global, stricter in Europe and North America | Medium term (2-4 years) |

| Micro-LED and AR-HUD Component Supply Bottlenecks | -0.8% | Global supply chain constraints | Short term (≤ 2 years) |

| Cognitive Overload From Multimodal UI Complexity | -0.6% | Developed markets with complex regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced HMI Hardware Stacks

Curved organic light-emitting diode panels, ultrasonic haptics, and AR-HUD optics add USD 800–1,500 to the bill of materials, pricing them out of entry models. Chinese panel makers such as BOE have yet to bring curved automotive organic light-emitting diode (OLED) yields above 70%, sustaining premiums. Micro-LED wafers, still semi-manual in die transfer, sit at thrice the organic light-emitting diode (OLED) cost, confining adoption to ultra-luxury trims. Original equipment manufacturers tier features by trim to soften sticker shock, but fragmented hardware complicates software consistency and raises test overhead, an impediment to scale within the human machine interface market.

Cyber-Security and Data-Privacy Vulnerabilities

A compromised infotainment unit can pivot into critical ECUs. The United States Bureau of Industry and Security banned certain foreign code bases in connected vehicles in 2024, forcing supplier audits and redesigns. ISO 21434 now mandates threat analysis and cryptographic key management across the development life cycle. Region-specific privacy laws, from Europe’s GDPR to China’s Personal Information Protection Law, oblige localized data storage and consent flows, raising compliance costs. Silicon-level secure enclaves from Renesas and NXP embed intrusion detection, yet widespread rollout remains uneven. These factors shave growth off the human machine interface market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Central Displays Consolidate Control Architecture

Central displays held a commanding 42.28% human-machine interface market share in 2025, as 10- to 15-inch touchscreens became the default portal for navigation, media, and climate control. The augmented-reality head-up display category is scaling at a 17.06% CAGR, propelled by windshield-level navigation arrows that align with United Nations Economic Commission for Europe (UNECE) distraction caps and keep glance durations low. Voice control systems are migrating down-market to cloud natural-language processing that lowers silicon demands, expanding total addressable units. Rotary knobs are disappearing in mainstream models but linger in select luxury brands for tactile reassurance.

Augmented-reality units from Panasonic project a 13-degree field of view 10 meters ahead, overlaying object detection on the driving scene. Gesture modules from Ultraleap give mid-air call-accept motions, yet struggle with unintentional triggers in bumpy conditions. Wearable extensions, phone unlock, smartwatch battery checks, form a nascent but rising slice. As premium screens filter into mid-price cars, the human machine interface market size for displays alone is positioned to expand faster than overall revenue.

By Access Type: Multimodal Integration Drives User Adoption

Multimodal systems controlled 51.62% of the 2025 revenue and will grow at 14.93%, because Level 2+ ADAS and infotainment depth exceed any single channel’s bandwidth. Mercedes’ 56-inch Hyperscreen marries touch, gesture, and voice, dynamically prioritizing the least distracting channel per context. Single-modality layouts persist in economy tiers where cost gates experimentation, yet even these cars adopt wireless phone mirroring that injects external voice assistants.

Haptic feedback joins touch, voice, and gesture as a fourth lane; Bosch piezo touchscreens fake mechanical clicks to confirm selections without visual verification. Adaptive systems observe driver preference and highlight the dominant modality, aiming to meet NHTSA’s 2-second glance rule. However, gesture misreads and voice latency risk frustrating users, proving that multimodal value depends on orchestration quality within the human machine interface market.

By Interaction Modality: Visual Channels Capture the Lion’s Share

Visual interfaces such as LCD, OLED, and emerging micro-LED displays accounted for 67.14% of revenue in 2025 and are advancing at 15.18%, the fastest modality growth rate. Curved pillar-to-pillar screens elevate perceived cabin tech and create unified canvases for navigation and ADAS visualization. Acoustic channels rise on the back of AI voice copilots but remain complementary because drivers demand visual confirmation.

Micro-LED promises 5,000-nit brightness with a 15-year lifespan, solving OLED burn-in worries. Transparent OLED embedded in sun visors eliminates A-pillar blind spots. Regulators now restrict video on forward-facing displays unless parked, nudging OEMs to implement immobilizer triggers. Overall, modality mix evolution keeps visual hardware central to the human machine interface market size, even as voice gains mindshare.

By Vehicle Type: Mid-Price Segments Balance Features and Costs

Mid-price passenger cars retained 35.68% revenue in 2025, yet luxury models grew fastest at 12.34% CAGR, introducing micro-LED clusters and AI assistants that later migrate down-segment. Economy cars lean on smartphone mirroring for competitiveness and may omit built-in navigation entirely. Commercial trucks require interface-as-a-tool designs for route compliance and driver coaching rather than entertainment.

Subscription-based heated seats and hands-free-assist upgrades live mainly in luxury vehicles, justifying complex account-management screens. Electric vans, such as Mercedes eSprinter, borrow passenger-car display tech to attract younger drivers. This tiered rollout model creates trickle-down demand that widens the human machine interface market over the forecast horizon.

By Propulsion Type: Electric Vehicles Reshape Interface Requirements

Internal-combustion models still represented 58.47% of 2025 shipments, yet battery electric vehicles are surging at 15.36% CAGR through 2031, catapulting the human machine interface market size for large curved panels and charge-route visuals. Flat-floor skateboard chassis allows 56-inch Hyperscreens, impossible with transmission tunnels. Range anxiety forces persistent state-of-charge graphics and charger routing overlays, lifting screen time per mile.

Plug-in hybrid electric vehicles (PHEVs) complicate UI logic by needing dual fuel and battery readouts, while fuel-cell vehicles copy BEV interfaces but add stack-temperature dials. Chinese battery electric vehicle brands democratize 17-inch screens and AI helpers at sub-USD 40,000 prices, accelerating global adoption. Propulsion shifts, therefore, re-allocate R&D spend toward electric-centric interfaces across the human machine interface market.

By Sales Channel: OEM Integration Dominates Market Strategy

Original equipment manufacturer (OEM) systems owned 81.12% of 2025 shipments, but their share edges down as retrofit demand climbs 14.39% CAGR; drivers of 2020-2023 cars swap outdated head units for wireless CarPlay or vertical Android screens. Low-cost 12-inch floating displays emulate factory aesthetics for under USD 600 installed. However, original equipment manufacturers encrypt CAN data, limiting deep vehicle integration and preserving their subscription revenue.

Regulators in some states restrict safety-system modification, chilling the retrofit of driver-monitor cameras or steering haptics. Insurance exclusions further temper aftermarket penetration. Despite growth, original equipment manufacturer lock-in will keep them the dominant gatekeepers of the human machine interface market.

Geography Analysis

Asia-Pacific owned 47.88% of 2025 revenue, anchored by China’s battery electric vehicle surge and mandates that cockpit data be stored locally, forcing global suppliers to spin up Mandarin voice models and in-country cloud nodes. Japanese brands favor minimalist tactile buttons, fitting cultural preferences for low distraction, while South Korea positions itself as a second source for AR-HUD optics through Hyundai Mobis and Zeiss collaboration. India’s sub-USD 15,000 cars now feature Hindi voice assistance on 9-inch displays, enlarging unit volume.

The Middle East and Africa books a 13.74% CAGR, the fastest geography. Saudi Arabia’s USD 5.6 billion investment in Lucid includes Arabic-local HMI and region-specific maps. Dubai’s multilingual autonomous-taxi pilots demand real-time translation across Arabic, English, Hindi, and Urdu. South African assembly lines adapt interfaces to Afrikaans and Zulu, indicating original equipment manufacturer willingness to localize for sub-Saharan growth.

North America and Europe mature more slowly yet pioneer standards. United Nations Economic Commission for Europe (UNECE) R171 and GDPR shape global cockpit design and data pipelines, and premium German cars typically debut new interface tech before exporting it. Brazil and Argentina adopt Euro-style approval frameworks that favor incumbents, while Russian brands rely on Chinese Android head units amid sanctions. These regional dynamics keep the human machine interface market dispersed, with design centers clustered in Germany, the United States, China, and Japan, but growth pockets emerging in the Gulf and India.

Competitive Landscape

Continental, Bosch, Visteon, DENSO, and Harman jointly held a significant share of 2025 revenue, signaling moderate concentration and room for niche entrants. Continental acquired a stake in Leia to lock up holographic-display IP, aiming to ship 3D dashboards by 2027. Bosch pivoted to cloud middleware through a 2024 Microsoft Azure alliance that lets automakers push HMI updates independent of hardware swaps. Visteon won a multiyear Stellantis deal to supply domain controllers that mash cluster, infotainment, and driver-monitor functions on a single SoC, trimming weight and cost.

Disruptors thrive in gesture sensing, voice AI, and health monitoring. Ultraleap licenses mid-air haptics to Jaguar Land Rover, Tanvas renders texture on flat glass, and Cerence bets on large-language assistants. Chinese vendors such as Huawei bundle 5G modules with displays at a 30% discount to Western peers, squeezing margins. Silicon players, Qualcomm, Renesas, and NXP embed secure boot and AI acceleration, hijacking value from traditional Tier-1s.

Market entry barriers rise with ISO 21434 and ISO 24089 compliance. Suppliers offering baked-in security win sockets in safety domains where software-only fixes lack pedigree. At the same time, cloud hyperscalers can now supply language models directly, threatening incumbent voice giants. Patent filings by Synaptics around ultrasonic haptic overlays broaden competitive fronts, while Aptiv’s zonal architecture promises wiring-harness weight cuts that free budget for richer displays. The human machine interface market remains competitive yet rewards IP differentiation and secure pipelines.

Automotive Human Machine Interface Industry Leaders

-

Continental AG

-

Visteon Corporation

-

Valeo S.A.

-

DENSO Corporation

-

Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Toyota partnered with Unity to co-create real-time 3D in-car interfaces that boost graphical fidelity without taxing embedded GPUs.

- January 2025: Himax Technologies and AUO unveiled an AmLED cockpit display platform at CES 2025. The platform features a 16-inch panel that saves 50% of power and dual 23-inch curved screens boasting 4,800 dimming zones.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive human-machine interface market as revenue generated from factory-installed and approved aftermarket systems that let drivers or passengers interact with vehicle functions through visual, haptic, or acoustic inputs. Covered modules include central and instrument displays, head-up displays, steering-mounted controls, gesture sensors, and voice-control software across all passenger and commercial vehicles.

Scope exclusion: Generic industrial control panels, independent smartphone apps not linked through OEM APIs, and standalone ADAS electronic control units are omitted.

Segmentation Overview

-

By Product Type

- Central Displays

- Voice Control Systems

- Head-Up Displays (Conventional and AR)

- Touch-Sensitive Steering Controls

- Gesture-Control Modules

- Rotary/Knob Controllers

- Wearable and Bring-Your-Own-Device Interfaces

-

By Access Type

- Single-Modal

- Multimodal (Voice+Gesture+Touch)

-

By Interaction Modality

- Visual (LCD/OLED/micro-LED)

- Acoustic (Voice, Sound-Haptics)

- Haptic (Force-feedback, Ultrasonic)

-

By Vehicle Type

- Economy Passenger Cars

- Mid-Price Passenger Cars

- Luxury Passenger Cars

- Commercial Vehicles

-

By Propulsion Type

- Internal Combustion Engine (ICE)

- Battery-Electric Vehicles (BEVs)

- Plug-in Hybrid Vehicles (PHEVs)

- Fuel-Cell Vehicles (FCEVs)

-

By Sales Channel

- OEM-Installed Systems

- Aftermarket Retro-fits

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct structured interviews with HMI engineers at automakers, UI designers, procurement managers, and regional dealer groups across North America, Europe, China, India, and Japan. These conversations test penetration curves, discount structures, and retrofit appetite before final triangulation.

Desk Research

We begin with production and parc datasets from OICA, registration files from the Federal Motor Transport Authority, UN Comtrade trade codes for cockpit displays and input devices, and Eurostat price indices to anchor historical value and volume baselines. Complementary insights flow from bodies such as the Japan Electronics and IT Industries Association, SAE technical papers that map HMI ergonomics, and Questel patent analytics that track emerging AR-HUD filings.

To refine pricing, analysts screen tier-one supplier 10-Ks, investor decks, and OEM part catalogues, compare shipment values on Volza, consult tender notices via Tenders Info, and cross-verify firm-level splits on D&B Hoovers. The sources noted are illustrative; numerous additional references support data capture and validation.

Market-Sizing & Forecasting

A top-down build starts with global light-vehicle and truck output, which is then multiplied by interface penetration rates, average system counts, and blended ASPs. Selective bottom-up supplier roll-ups validate totals. Key model variables include digital cockpit share in mid-priced cars, AR-HUD adoption in EVs, regulatory distraction limits, and semiconductor content per display. Multivariate regression with scenario analysis projects these drivers to 2030.

Data Validation & Update Cycle

Outputs face variance checks against historic corridors, quarterly HMI chip shipments, and currency movements. Senior reviewers sign off, and reports refresh every twelve months, with interim updates triggered by major model launches or regulation shifts.

Why Our Automotive Human Machine Interface Baseline Commands Reliability

Published estimates often diverge because firms choose different scope elements, pricing logic, and refresh cadences.

Key gap drivers center on whether retrofit kits are counted, how voice-software subscriptions are annualized, ASP escalation paths, and the currency conversion date chosen.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.21 B (2025) | Mordor Intelligence | |

| USD 23.50 B (2024) | Global Consultancy A | Excludes retrofit sales; regional ASP averages only |

| USD 26.28 B (2024) | Regional Consultancy B | Blends industrial HMI revenue with automotive figures |

| USD 23.00 B (2023) | Trade Journal C | Shipment value without inflation or FX normalization |

The comparison shows that Mordor Intelligence, through disciplined scope selection, dual research funnels, and an annual refresh cycle, delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the automotive human machine interface sector today and where is it headed?

It generated USD 30.11 billion in 2026 and is projected to reach USD 50.06 billion by 2031, advancing at a 10.76% CAGR.

Which region currently shows the highest adoption of advanced cockpit interfaces?

Asia-Pacific held 47.88% of global revenue in 2025, driven by China’s connected-vehicle mandates and rapid BEV rollout.

What growth rate is expected for battery-electric vehicle cockpit systems?

BEV-focused interfaces are forecast to expand at a 15.36% CAGR between 2026 and 2031, the fastest among propulsion categories.

Which cockpit component commands the biggest revenue share?

Central displays led with 42.28% share in 2025, reflecting their role as the primary hub for navigation, media, and vehicle settings.

How quickly are augmented-reality head-up displays scaling?

AR-HUD shipments are projected to rise at a 17.06% CAGR through 2031 as automakers migrate navigation and safety cues onto the windshield.

Page last updated on: