Automotive Aftermarket Glass Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

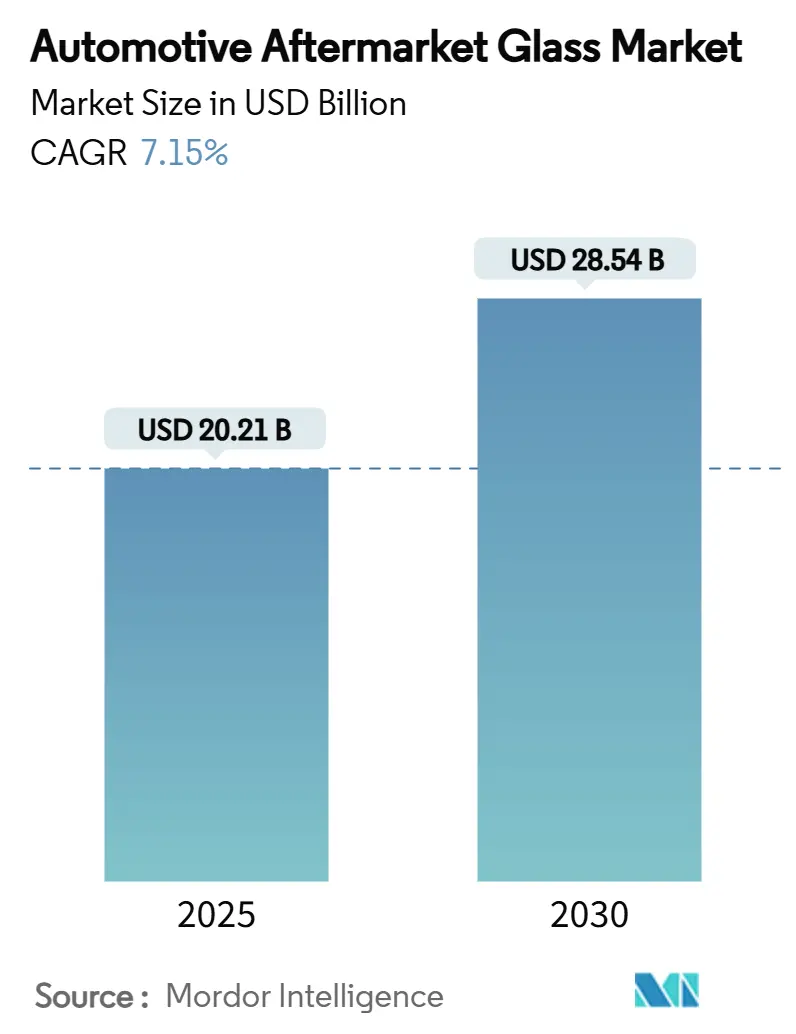

| Market Size (2025) | USD 20.21 Billion |

| Market Size (2030) | USD 28.54 Billion |

| Growth Rate (2025 - 2030) | 7.15% CAGR |

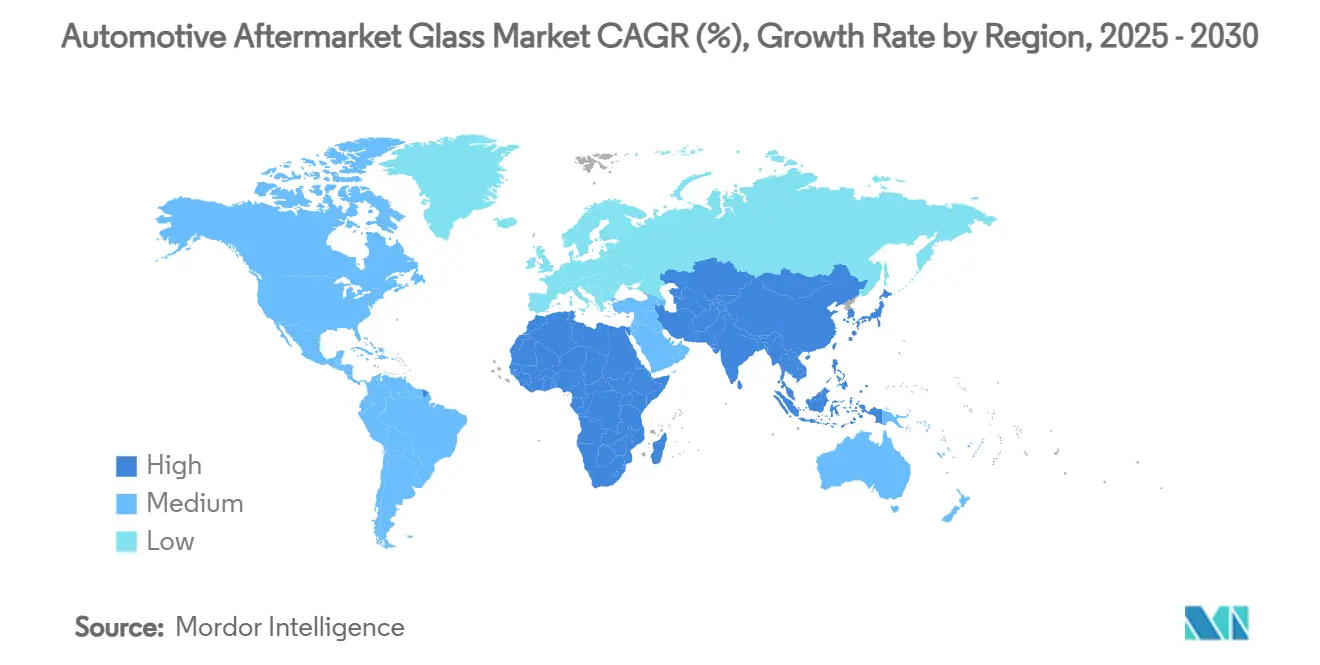

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Aftermarket Glass Market Analysis by Mordor Intelligence

The automotive aftermarket glass market size stood at USD 20.21 billion in 2025 and is forecast to expand to USD 28.54 billion in 2030, advancing at a 7.15% CAGR. Demand remains resilient because glass replacement is essential for road-worthiness, insurance compliance, and driver visibility. Technology now plays a pivotal role as calibration services for Advanced Driver Assistance Systems (ADAS) add significantly to a typical windshield job, shifting revenue toward higher-value labor. Aging vehicle populations, wider glass areas on sport-utility vehicles, and insurer support for zero-deductible “glass-only” claims further strengthen replacement volumes. At the same time, premium laminated, acoustic, and solar-control products open new profit pools for installers able to source and fit complex substrates.

Key Report Takeaways

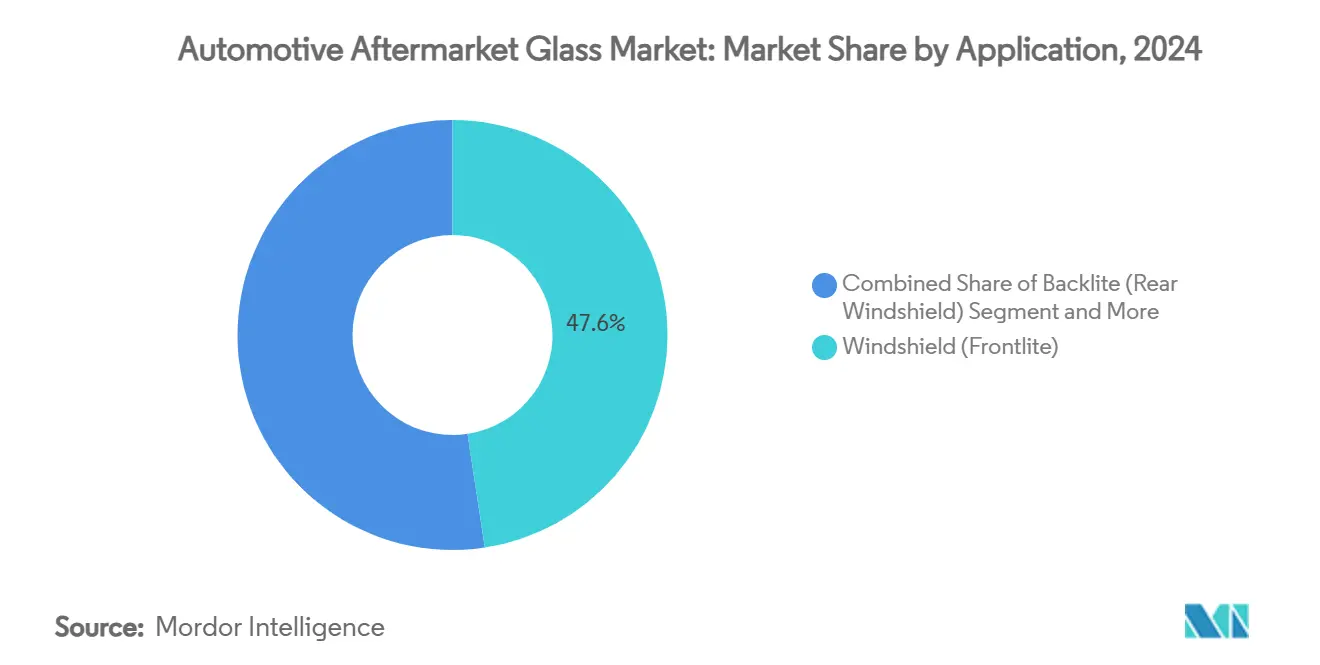

- By application windshields led with 47.61% revenue share in 2024; roof and sunroof glazing is projected to grow the fastest at 10.03% CAGR to 2030.

- By vehicle type, passenger cars accounted for 69.08% of the automotive aftermarket glass market share in 2024, and are set to climb at 8.91% CAGR through 2030.

- By material and construction, tempered products captured 61.56% share of the automotive aftermarket glass market size in 2024, whereas laminated constructions are on track for 10.44% CAGR to 2030.

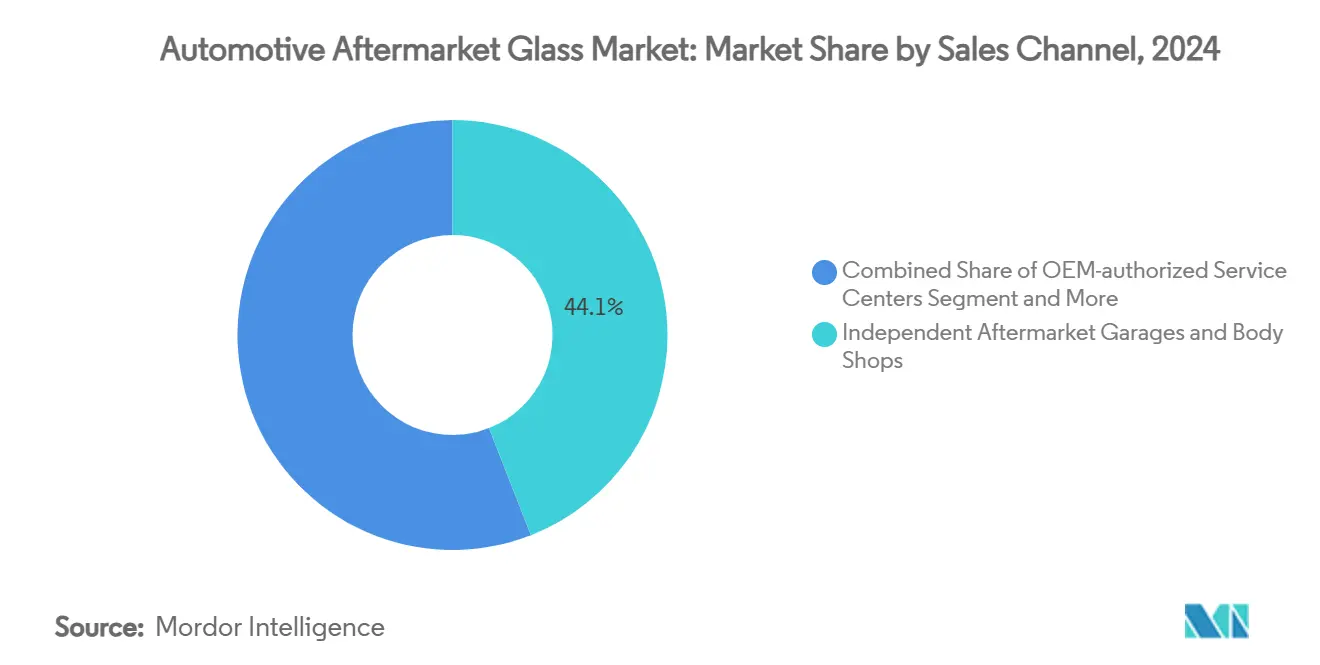

- By sales channel, independent garages held 44.05% share in 2024; online platforms represent the fastest expansion at 14.74% CAGR through 2030.

- By service type, replacement work represented 78.28% of segment revenue in 2024 and is expected to advance at 7.78% CAGR to 2030.

- By geography, Aisa-Pacific captured 40.73% share in 2024 and is projectyed to register the fastest CAGR of 8.08% through 2030.

Global Automotive Aftermarket Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory ADAS Sensor Recalibration | +1.4% | Global, with highest impact in North America and EU | Medium term (2-4 years) |

| Rising Vehicle Parc and Ageing Fleet | +1.2% | Global, particularly strong in Asia-Pacific and North America | Long term (≥ 4 years) |

| Expanding "Glass-Only" Claims Coverage | +1.1% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Increasing Accident‐Related Windshield Damage | +0.8% | Global, with regional variations based on road infrastructure | Medium term (2-4 years) |

| Retro-Fit Demand for Solar-Control | +0.6% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Subscription-Based "Windshield-As-A-Service" | +0.5% | Urban centers in North America, EU, and select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory ADAS Sensor Recalibration After Glass Replacement

Calibration now represents 30–50% of total windshield-replacement bills. Static procedures require controlled indoor targets, while dynamic calibration occurs during test drives, each demanding certified equipment and technicians[1]“Hyundai Mobis Partners with ZEISS”, Hyundai Mobis, mobis.com. Insurers increasingly reimburse these steps, embedding them in standard policies and lifting average invoice values. Forward-facing cameras, radar units, and emerging head-up display (HUD) modules are all mounted on or viewed through the windshield, so every technology upgrade binds service demand to glass integrity. Partnerships such as Hyundai Mobis and ZEISS aim to commercialise windshield-wide augmented reality displays by 2027, underscoring the glass panel’s future role as computational real estate. Shops unable to invest in recalibration rigs face competitive barriers, whereas networks offering “one-stop” replacement plus calibration see rising referrals from fleets and insurers.

Rising Global Vehicle Parc and Ageing Fleet

The average light-vehicle age in the United States reached 12.7 years in 2025 and continues to climb. Global manufacturing shortfalls since 2020 removed more than 40 million planned units from the market, extending the usable life of existing cars and light trucks. Older vehicles experience higher glass failure rates as weathering, vibration, and road debris accumulate. Economic headwinds and elevated new-car prices push consumers to retain vehicles longer, further enlarging the serviceable fleet. In emerging Asia, vehicle ownership keeps rising, so total glass exposure expands on two fronts: ageing inventory in developed economies and fleet growth in developing ones. Installers therefore enjoy steady baseline volumes regardless of light-vehicle sales volatility.

Insurance Carriers Expanding “Glass-Only” Claims Coverage

Several U.S. states mandate zero-deductible windshield replacement, and more insurers voluntarily extend similar terms nationwide. Consumers accept repairs sooner when no out-of-pocket payment is required, shortening replacement intervals and lifting claim counts. Preferred-provider agreements steer work toward networks able to meet service-level agreements, creating competitive pressure for smaller independents. The regulatory climate also raises compliance costs because carriers demand digital documentation of calibration and fitment quality. Nevertheless, predictable claim flows help glass specialists plan capacity investment and cement insurer relationships.

Increasing Road-Accident-Related Windshield Damage

Construction booms, deteriorating pavements, and extreme weather events generate more airborne debris. Large utility vehicles dominate new-car sales, and their expansive windshields are struck more frequently by stones or road junk. When damage coincides with other body repairs, multi-service centres win bundled work, whereas pure-play glass shops still benefit from higher part prices on panoramic and acoustic variants. Advanced glazing with heating, antenna, and sensor layers often cannot be safely repaired, tilting jobs toward full replacement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Durability and Longer Replacement Cycles | -1.2% | Global, with strongest impact in developed markets | Long term (≥ 4 years) |

| Expensive ADAS Windshield Replacement | -0.9% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Volatile Specialty Interlayers and Coatings Supply | -0.6% | Global, with regional supply concentration risks | Short term (≤ 2 years) |

| Restrictions on Windshield Tint / Coatings | -0.5% | Primarily North America, with varying state regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Improved OEM Glass Durability and Longer Replacement Cycles

Corning’s Fusion5 substrate delivers four-times better impact endurance while trimming weight by 12%, allowing automakers to extend recommended replacement intervals[2]“Corning® Fusion5® Glass”, Corning, corning.com. Laminated interlayers, hydrophobic coatings, and stronger frit designs resist chipping and spider-cracking. Protective films applied at the dealership further shield windshields, especially on premium vehicles where ADAS components drive repair bills higher. As durability rises, annual replacement frequency drops, forcing service chains to rely on higher transaction values rather than volume growth. Glass makers respond by emphasising recycle-ready chemistries and thinner gauges to align with electrification weight targets.

High Cost of ADAS Windshield Replacement and Calibration

A full ADAS-equipped windshield can cost USD 450–1,400, including calibration labour. Where insurance deductibles remain, some owners delay or forgo replacement, risking camera misalignment and safety failures. Calibration complexity varies across brands, discouraging price competition because equipment, software licenses, and technician training form substantial fixed costs. Although manufacturers publish position statements clarifying safe-fit procedures, reimbursement standards lag in parts of Asia and Latin America, dampening immediate uptake of premium laminated solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Windshield Dominance Drives ADAS Integration

Windshields generated the largest share in 2024, reflecting 47.61% of total value because every forward-camera or radar module depends on clear, properly curved glazing. The automotive aftermarket glass market size attributable to windshields is set to compound as calibration fees become inseparable from the job. Roof and sunroof panels form the fastest sub-segment at 10.03% CAGR thanks to the surge of panoramic designs on crossovers. These parts use larger areas of tempered or laminated lite, raising per-unit ticket prices. Backlites and sidelites remain price-competitive and follow lighting trends, while HUD-ready surfaces unlock new premium niches by integrating dual-curve optics[3]“AGC to Exhibit at CES 2025”, AGC, agc.com.

Installation complexity scales with feature integration. Rain sensors, light sensors, and head-up display projectors sit within frit bands, requiring tight spec tolerances. Service chains invest in digital clamps and contamination-free prep bays to avoid bond-line failures. Roof glass replacements often demand recalibration of interior camera systems monitoring driver attention. As connectivity grows, every panel serves multiple functions, accelerating parts diversity and logistic challenges.

By Vehicle Type: SUVs Narrow the Gap

Passenger cars retained 69.08% share in 2024, and are projected to grow at 8.91% CAGR through 2030, sustained by the global inventory of small and midsize sedans. Nevertheless, SUVs and crossovers are advancing, narrowing the difference in unit opportunity within the automotive aftermarket glass market. Larger windscreen areas and thicker side glazing elevate material costs, and premium trims frequently specify acoustic laminated glass for cabin refinement. That combination pushes average invoice values higher for SUVs than for compact cars.

Commercial fleets, including vans and medium-duty trucks, present steady, policy-driven demand because delivery sectors cannot afford downtime. Fleet managers adopt preventive maintenance schedules that pre-book glass replacements at set mileage intervals. Electric variants such as last-mile vans use expansive windshield-to-roof panels for aerodynamic flow, further boosting square-meter consumption. While sedans decline as a new-car segment, their legacy parc ensures long-tail service work until beyond 2030.

By Material and Construction: Laminated Momentum

Tempered glass commanded 61.56% revenue in 2024, underpinned by mass-market affordability and robust supply chains. Laminated alternatives, though pricier, are accelerating at 10.44% CAGR because they better retain structural integrity after impact and enable acoustic or solar-control layers. The automotive aftermarket glass market share will therefore rebalance toward laminates as regulation and comfort expectations converge.

Self-cleaning photocatalytic coatings, humidity-responsive tint, and embedded antenna circuitry are more readily implemented in laminated builds. Suppliers experiment with hybrid composites that sandwich polycarbonate between glass plies to shave weight yet keep scratch resistance. Luxury nameplates adopt these solutions first, but cost curves continue to improve, signalling broader diffusion toward mid-tier vehicles.

By Sales Channel: Digital Platforms Surge

Independent garages held 44.05% share in 2024 by leveraging lower overheads and community presence. Online aggregators, though still niche, are expanding at 14.74% CAGR and reshaping customer acquisition. They consolidate scheduling, price quotes, and inventory visibility into mobile apps, letting consumers book same-day windshield swaps at home or work. For the automotive aftermarket glass market, this raises service reach without costly retail frontage.

Original-equipment service centres secure insurer steering on late-model vehicles where calibration complexity is highest. Yet price sensitivity among owners of older cars keeps independents competitive. Glass-specialist chains continue to roll up regional operators, deploying shared call-centres and procurement platforms to secure discounts and unify customer-experience standards.

By Service Type: Replacement Predominates

Replacement generated 78.28% of spend in 2024 and is forecast to grow at 7.78% CAGR through 2030. Laminated windshields carrying embedded electronics seldom qualify for repair because optical or structural tolerances cannot be restored by resin injection. The automotive aftermarket glass market size linked to replacement jobs will therefore outpace repair even as part counts stabilise.

Chip repairs persist for small, peripheral damage on tempered sidelites, but their share progressively contracts. Equipment makers innovate injection tools that cure in under ten minutes, seeking to keep repair relevant against replacement’s rising value proposition. Nonetheless, regulatory scrutiny of ADAS alignment compels insurers to back full-panel replacement where critical sensors sit behind the glass.

Geography Analysis

Asia-Pacific contributed 40.73% of global revenue in 2024 and delivers the fastest 8.08% CAGR outlook. China’s capacity expansions, including a new 2,610 million-square-metre plant in Hefei, illustrate supplier confidence in sustained regional demand[4]"China's Fuyao Glass Unveils Second Automotive Glass Capacity Expansion Plan in a Month", Yicai Global, yicaiglobal.com. India’s youthful fleet and infrastructure build-out add momentum, while Japan and South Korea push technology boundaries that ripple into the service ecosystem.

North America grows on the back of widespread ADAS installation and favourable insurance legislation. Expansive pickups and SUVs dominate the vehicle mix, translating into large glass panels and higher per-unit values. Fuyao's ongoing USD 400 million float line additions in Illinois will localise supply and trim logistics costs, underlining suppliers’ long-term view on regional consumption.

Europe, though mature, remains the innovation hub for safety glazing. Its slower growth rate reflects long replacement cycles and tougher economic conditions, yet stringent repair-quality mandates favour service firms with certified calibration bays. Africa and Western Asia growth underpinned by rising vehicle ownership and road-building programmes that expose windscreens to debris. South America buoyed by economic recovery and the proliferation of ride-hailing fleets that maintain tight uptime targets.

Mordor Intelligence provides coverage of the automotive aftermarket glass market across other key regional markets, including Middle East and Africa, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Market concentration remains moderate with the top 5 players controlling a significant portion of the global aftermarket share, creating opportunities for regional specialists and emerging disruptors while maintaining barriers to entry through scale economies and distribution network requirements. Fuyao leverages vertical integration and geographic spread, Saint-Gobain exploits advanced simulation and OEM ties, while AGC capitalises on next-generation HUD-ready substrates. Medium-sized regional laminators thrive by specialising in short-run custom cuts and fleet contracts.

Consolidation accelerated over 2024–2025 as network operators bought local installers to expand calibration coverage. Simultaneously, technology alliances emerged: collaborations on holographic windshields, ultra-thin composites, and sensor-ready frits position suppliers as system integrators rather than commodity sheet makers. Raw-material inflation has forced all players to focus on energy efficiency and cullet recycling to defend margins.

Disruptive entrants from the broader electronics field experiment with chemically strengthened glass recipes that promise extended service life yet carry premium list prices. Should durability gains extend replacement intervals significantly, incumbents may pivot toward subscription and maintenance packages to stabilise revenue.

Automotive Aftermarket Glass Industry Leaders

-

Fuyao Glass Industry Group

-

Saint-Gobain Sekurit

-

AGC Inc.

-

Guardian Industries

-

Nippon Sheet Glass

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fuyao announced a USD 400 million expansion of its Decatur, Illinois float-glass facility to boost domestic supply for ADAS-ready windshields.

- September 2024: PGW Auto Glass acquired PH Vitres d’Autos, enlarging distribution reach across Québec.

- July 2024: Safelite Group purchased City Auto Glass, extending its North-American retail footprint.

- January 2024: Fuyao committed CNY 5.8 billion (USD 804 million) for a new Hefei automotive glass plant with 2,610 million m² annual capacity.

Global Automotive Aftermarket Glass Market Report Scope

| Windshield (Frontlite) | |

| Backlite (Rear Windshield) | |

| Sidelite | Door Glass |

| Quarter Glass | |

| Roof Glass / Sunroof / Moon-roof | |

| Rear-view Mirror Glass (interior and exterior) | |

| Others (HUD-ready, acoustic laminated, etc.) |

| Passenger Cars | Hatchbacks |

| Sedans | |

| Sport Utility Vehicles (SUVs) | |

| Multi-Utility Vehicles (MUVs) | |

| Commercial Vehicle | Light Commercial Vehicles (LCV) |

| Medium and Heavy-Duty Trucks | |

| Buses and Coaches |

| Laminated Glass |

| Tempered Glass |

| Others (Polycarbonate / Hybrid Glazing, solar-control) |

| OEM-authorized Service Centers |

| Independent Aftermarket Garages and Body Shops |

| Glass-Specialist Chains |

| Online Platforms |

| Repair |

| Replacement |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Application | Windshield (Frontlite) | |

| Backlite (Rear Windshield) | ||

| Sidelite | Door Glass | |

| Quarter Glass | ||

| Roof Glass / Sunroof / Moon-roof | ||

| Rear-view Mirror Glass (interior and exterior) | ||

| Others (HUD-ready, acoustic laminated, etc.) | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| Sport Utility Vehicles (SUVs) | ||

| Multi-Utility Vehicles (MUVs) | ||

| Commercial Vehicle | Light Commercial Vehicles (LCV) | |

| Medium and Heavy-Duty Trucks | ||

| Buses and Coaches | ||

| By Material and Construction | Laminated Glass | |

| Tempered Glass | ||

| Others (Polycarbonate / Hybrid Glazing, solar-control) | ||

| By Sales Channel | OEM-authorized Service Centers | |

| Independent Aftermarket Garages and Body Shops | ||

| Glass-Specialist Chains | ||

| Online Platforms | ||

| By Service Type | Repair | |

| Replacement | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the automotive aftermarket glass market?

The market is valued at USD 20.21 billion in 2025 and is projected to reach USD 28.54 billion by 2030, posting a 7.15% CAGR.

Why are windshields the dominant revenue generator?

Windshields account for 47.6% of revenue because they host ADAS sensors and require post-fit calibration, adding significant labour value.

Which material segment is expanding the fastest?

Laminated glass leads growth at 10.44% CAGR as safety, acoustic comfort, and smart-glass functions gain traction.

How are online channels reshaping service delivery?

Digital platforms growing at 14.74% CAGR let consumers schedule mobile replacements, compress booking times, and widen installer reach.

What factors could restrain market expansion?

Improved OEM glass durability, high ADAS replacement costs, and supply-chain volatility for specialty interlayers may temper volume growth.

Which region offers the highest growth potential?

Asia-Pacific combines the largest vehicle base with rapid ADAS adoption, generating an 8.08% CAGR outlook through 2030.

Page last updated on: