Automotive Night Vision System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

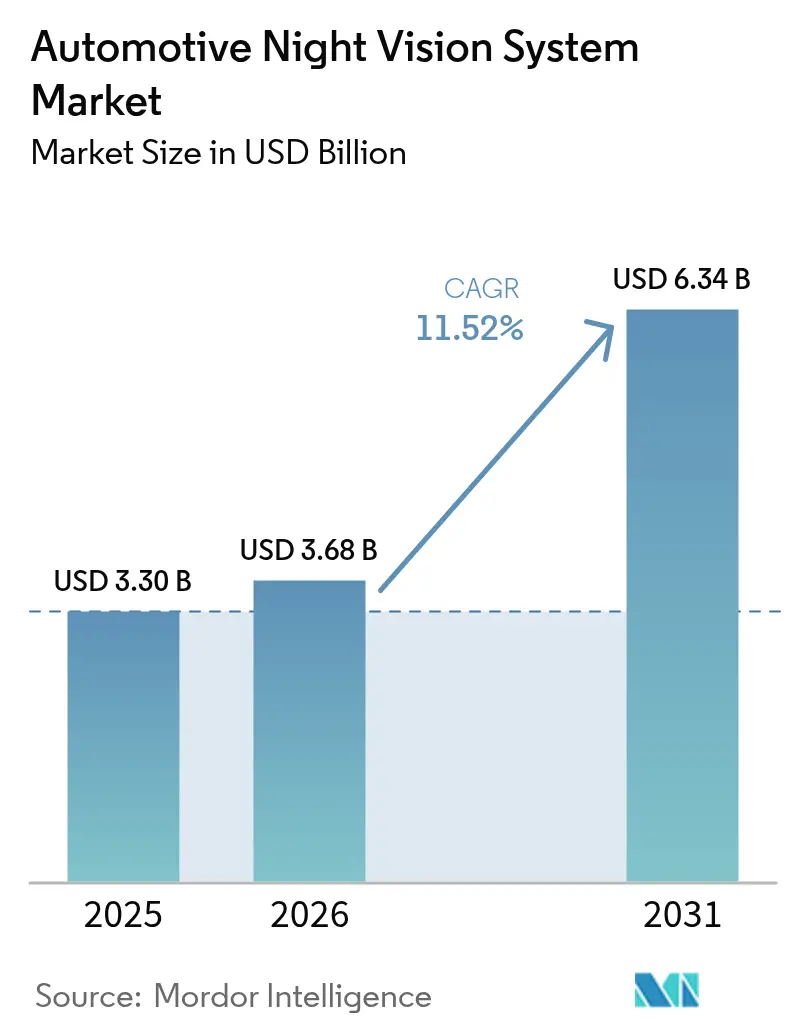

| Market Size (2026) | USD 3.68 Billion |

| Market Size (2031) | USD 6.34 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

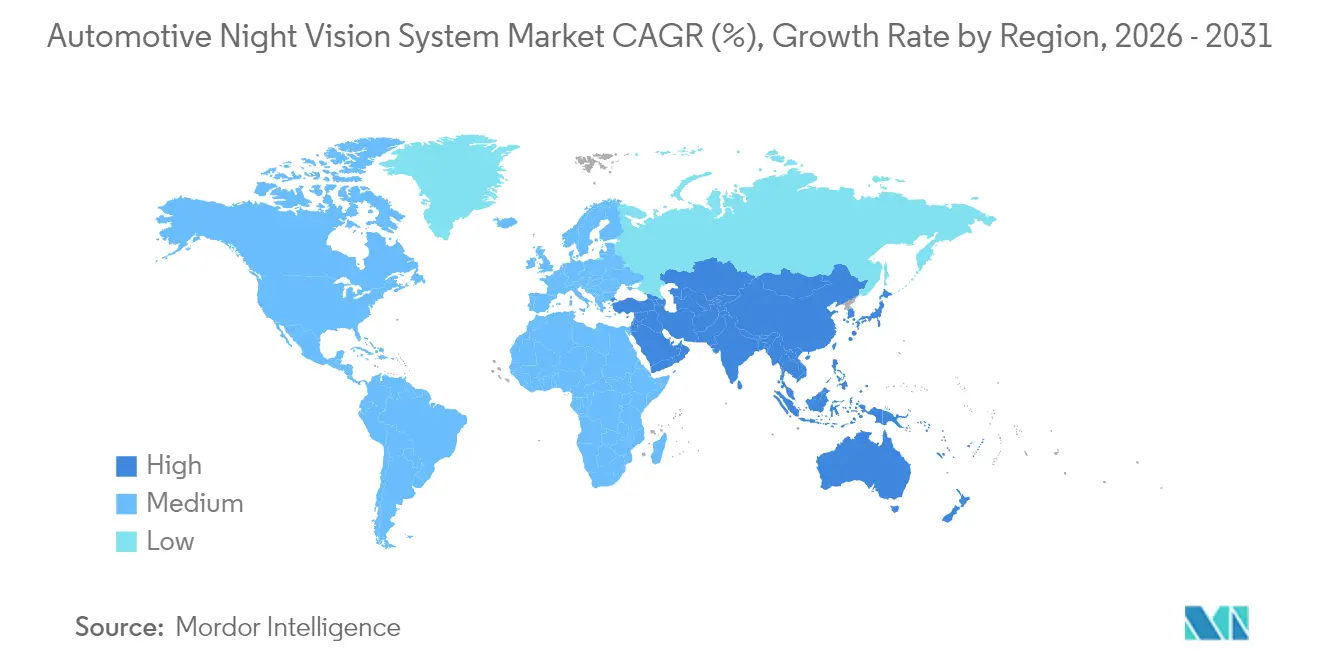

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

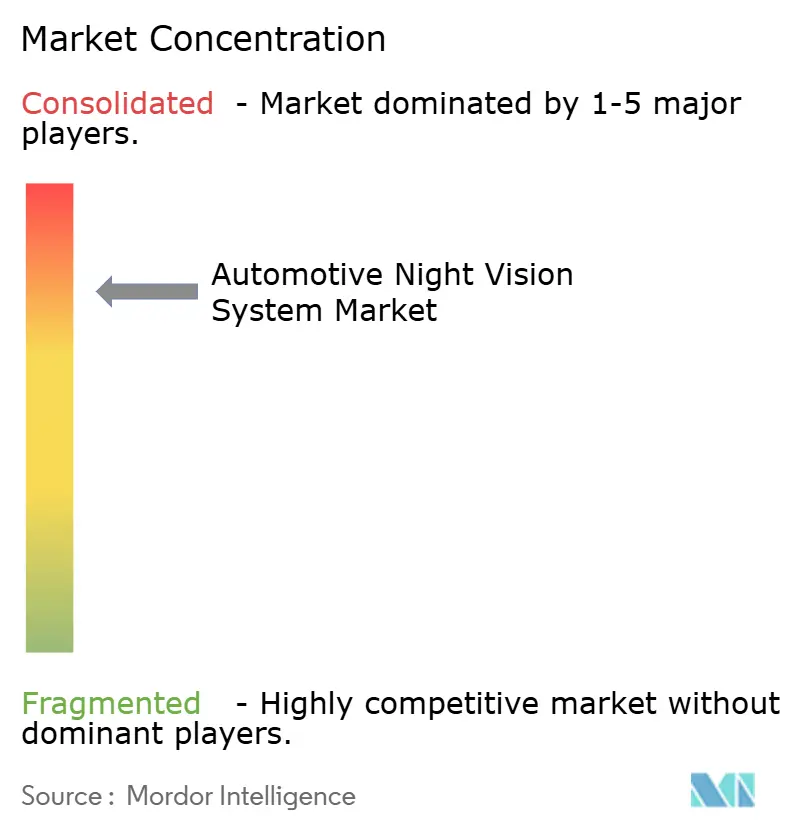

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Night Vision System Market Analysis by Mordor Intelligence

The automotive night vision systems market size was valued at USD 3.30 billion in 2025 and estimated to grow from USD 3.68 billion in 2026 to reach USD 6.34 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031). Mandatory pedestrian-protection rules in the United States and the European Union, expanding premium battery-electric portfolios, and steady cost reductions in thermal imaging components underpin this outlook. For instance, the National Highway Traffic Safety Administration's Federal Motor Vehicle Safety Standard No. 127, requires pedestrian automatic emergency braking systems by September 2029[1]"Federal Motor Vehicle Safety Standards; Automatic Emergency Braking Systems for Light Vehicles", Federal Register, www.federalregister.gov.. Automakers respond by embedding thermal sensors into advanced driver assistance systems (ADAS) stacks, while suppliers exploit wafer-le vel optics to ease price pressures. Competitive momentum intensifies as traditional Tier-1 suppliers ally with infrared specialists to defend dashboards from disruptive entrants. Over the forecast window, the automotive night vision systems market is set to move from a luxury differentiator to a broadly adopted compliance feature, especially in North America, Europe, and high-tier Chinese platforms.

Key Report Takeaways

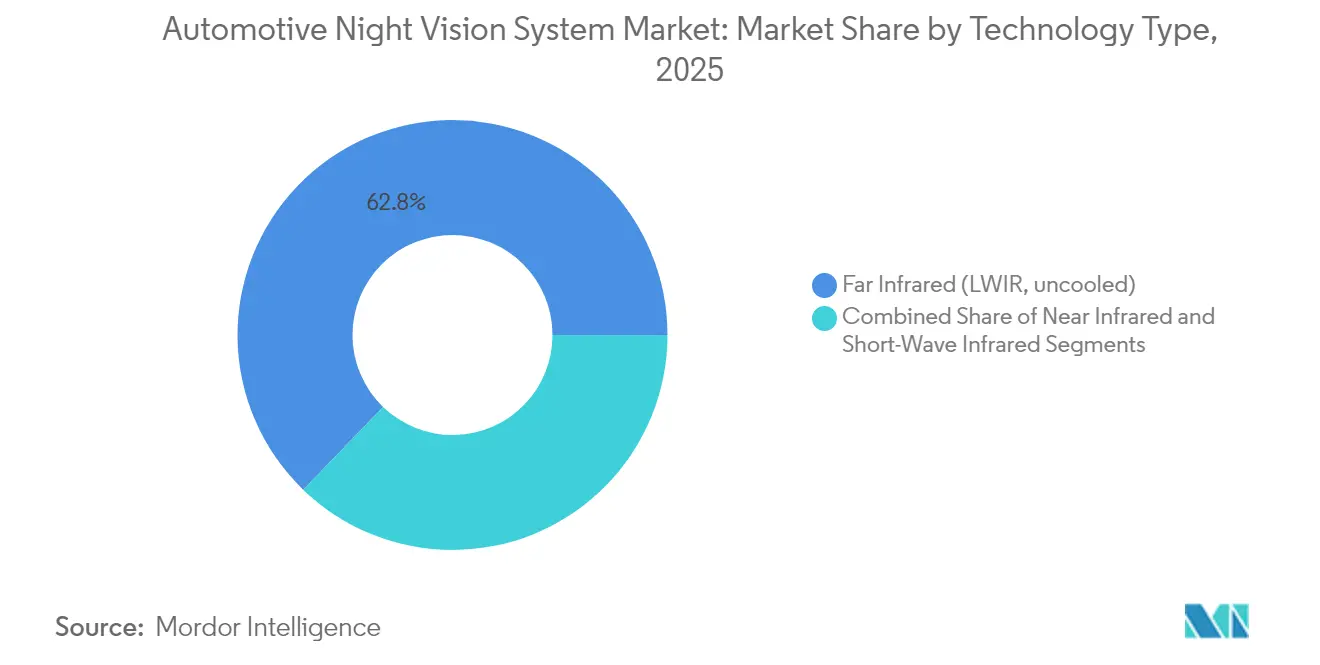

- By technology type, Far Infrared (LWIR) held 62.78% of the automotive night vision systems market share in 2025, whereas Short-Wave Infrared (SWIR) is poised to expand at a 15.88% CAGR through 2031.

- By display type, Head-Up Displays accounted for 43.10% of the automotive night vision systems revenue share in 2025; Central Infotainment Screens are forecast to advance at an 18.05% CAGR to 2031.

- By component, Night Vision Cameras commanded 54.72% of the automotive night vision systems revenue share in 2025, while IR Illumination Sources are progressing at a 15.65% CAGR.

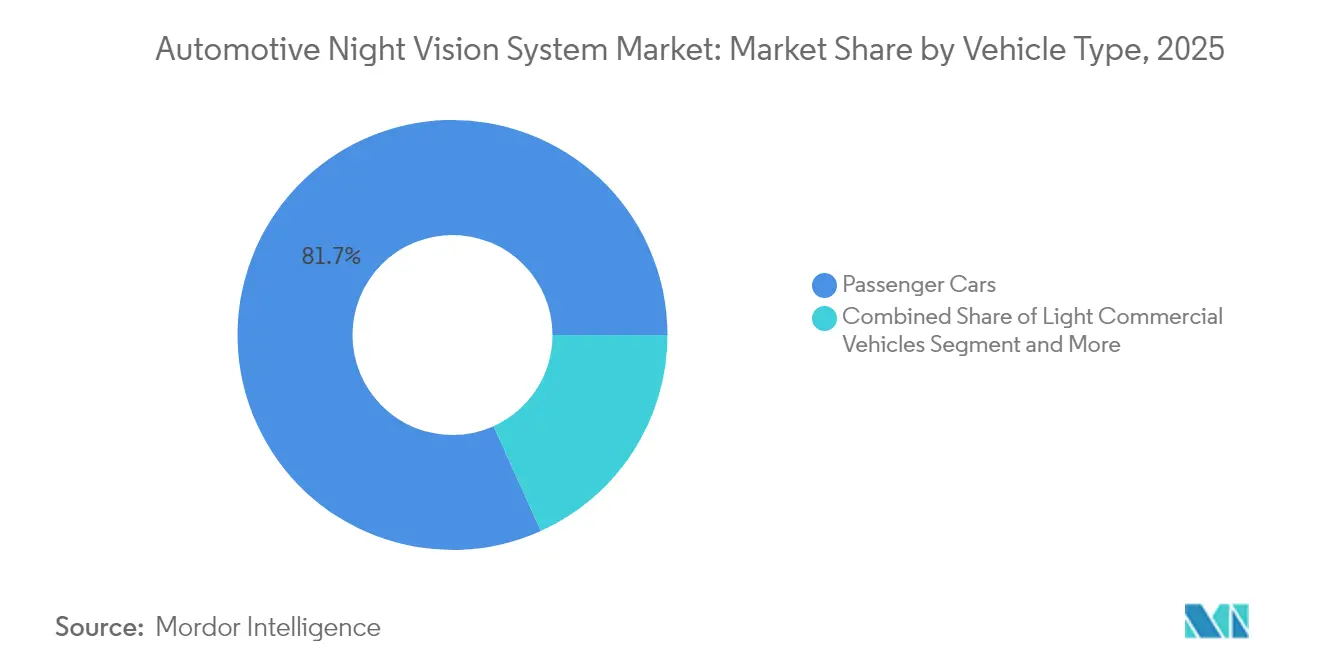

- By vehicle category, Passenger Cars led 81.74% of the automotive night vision systems market share in 2025, whereas Light Commercial Vehicles will grow at a 14.52% CAGR through 2031.

- By sales channel, OEM factory-fit installations represented 83.90% of the automotive night vision systems revenue share in 2025 and continue to rise at 15.02% CAGR.

- By geography, North America contributed 41.20% of the automotive night vision systems revenue share in 2025 and Asia-Pacific is on track for a 14.33% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Night Vision System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS Mandates in US-FMVSS 111 and EU GSR 2029 | +3.2% | North America and EU | Medium term (2-4 years) |

| Premium-Segment Penetration in BEVs and Luxury ICE Models | +2.8% | Global, concentrated in North America and EU | Short term (≤ 2 years) |

| Cost Downshift via Wafer-Level Optics and AI-Only Solutions | +2.1% | Global, manufacturing concentrated in Asia-Pacific | Long term (≥ 4 years) |

| Thermal/Visible Sensor Fusion Enabling L3 Autonomy at Night | +1.9% | Global, early adoption in North America and EU | Long term (≥ 4 years) |

| Insurance Telematics Discounts for Infrared-Equipped Fleets | +1.2% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Military-Grade LWIR Sensors Entering Civilian Supply Chains | +0.5% | Global, subject to export controls | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ADAS Mandates in US-FMVSS 111 and EU GSR 2029

Regulatory convergence between US Federal Motor Vehicle Safety Standard No. 127 and EU General Safety Regulation 2029 creates a synchronized compliance deadline that fundamentally reshapes automotive night vision adoption economics in the Automotive Night Vision System Market. The NHTSA mandate requiring pedestrian automatic emergency braking systems by September 2029 exposes a critical performance gap, as testing by Teledyne FLIR and VSI Labs demonstrated that thermal-fused PAEB systems passed all nighttime scenarios while three major 2024 vehicle models failed multiple tests. This regulatory pressure transforms night vision from luxury feature to compliance necessity, with 77.7% of pedestrian fatalities occurring at night in 2022 providing the safety justification. The EU's parallel timeline ensures global automakers cannot regionalize their approach, creating economies of scale that accelerate cost reduction across thermal imaging supply chains. Small-volume manufacturers receive a one-year extension until September 2030, creating a two-tier market dynamic that may advantage established players with existing thermal sensing capabilities.

Premium-segment Penetration in BEVs and Luxury ICE Models

High-end EVs now integrate thermal cameras to justify price premiums and differentiate against conventional rivals. Mercedes-Benz Night View Assist Plus identifies pedestrians and wildlife up to 160 m ahead and applies a spotlight beam without dazzling on-coming traffic. BMW’s far-infrared solution reaches 300 m and remains effective without external illumination. Luxury ICE models such as the Audi A6 and Q7 mirror this practice, each offering a USD 2,500 option. Because premium buyers accept equipment lists that push the USD 2,300–2,500 threshold, they provide the seed volumes necessary for supply-chain learning curves, thereby paving the way for cost-optimized trims in volume segments.

Cost Downshift via Wafer-Level Optics and AI-Only Solutions

Manufacturing innovation in wafer-level optics fundamentally alters night vision system economics by enabling semiconductor-compatible production processes that achieve automotive-grade volumes. Meridian Innovation's USD 12.5 million funding for silicon CMOS-compatible thermal sensors demonstrates venture capital confidence in cost reduction potential, with their patented wafer-level vacuum packaging targeting higher volume production at lower costs compared to traditional long-wave infrared sensors. EV Group's wafer-level optics solutions enable step-and-repeat mastering and UV microlens molding for automotive infrared sensing applications, supporting the integration of innovative photonic structures that enhance night vision capabilities. Flinders University researchers developed low-cost polymer materials from sulfur and cyclopentadiene for infrared lenses, offering cheaper alternatives to expensive germanium and toxic chalcogenide glasses while enabling rapid production and molding flexibility. AI-only solutions eliminate mechanical shutter requirements in uncooled detectors, reducing system complexity while improving reliability through software-based non-uniformity correction algorithms.

Thermal/visible Sensor Fusion Enabling L3 Autonomy at Night

Sensor fusion architectures combining thermal imaging with visible spectrum cameras unlock Level 3 autonomous driving capabilities during nighttime operations, addressing the 90% of machine vision failures that occur in difficult visibility conditions in the Automotive Night Vision System Market. Visionary.ai's partnership with Innoviz integrates True Night Vision technology with high-performance LiDAR sensors to enhance 3D machine vision performance in low-light and adverse weather, and a windshield-integrated thermal camera system from Lynred and Saint-Gobain Sekurit achieves a 140-meter pedestrian detection range while maintaining transparency through crystal-based technology, thereby enhancing automatic emergency braking reliability. Plus's evaluation of thermal cameras for Level 4 autonomous trucks, supplied by Teledyne FLIR, targets 250-meter pedestrian detection capability that surpasses typical headlight reach for heavy vehicle maneuvering safety. The fusion approach addresses individual sensor limitations while creating redundancy essential for autonomous system validation and regulatory approval.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ASP of Uncooled LWIR Modules and HUD Integration | -2.1% | Global, most acute in price-sensitive segments | Medium term (2-4 years) |

| US ITAR / Wassenaar Export Controls on More Than 9 Hz Thermal Cores | -1.8% | Global, affecting technology transfer to Asia-Pacific | Long term (≥ 4 years) |

| Consumer Data-Privacy Pushback on Cabin IR Imaging | -1.3% | EU and North America, regulatory uncertainty | Short term (≤ 2 years) |

| Reliability Drift of MEMS Shutters in Uncooled Detectors | -0.9% | Global, affecting mass-market deployment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High ASP of Uncooled LWIR Modules and HUD Integration

Thermal cores and associated optics remain expensive relative to camera and radar units. Integrating head-up projections adds further expense because each display demands optical combiners and elaborate calibration. OEM cost-engineering teams must choose between full LWIR coverage or radar-camera fusion pathways that promise compliance at lower bill-of-material counts. Emerging shutter-free algorithms and wafer-level manufacturing can relieve pressure, but the transition period keeps mainstream segments price-sensitive

US ITAR / Wassenaar Export Controls on More Than 9 Hz Thermal Cores

Thermal imagers that refresh above 9 Hz are classified as dual-use goods, which affects sourcing strategies in the Automotive Night Vision System Market. Export licenses govern shipments to large portions of Asia, compelling carmakers to juggle multiple sourcing routes. Infrared specialist Xenics lists controlled harmonized codes that trigger license reviews. Recent sanctions on selected Chinese vendors for military ties spotlight enforcement risks. Such hurdles lengthen qualification schedules, inflate inventory buffers, and sometimes oblige regional design splits. Materials innovation, such as LightPath Technologies’ BDNL-4 chalcogenide glass that skirts germanium dependency, aims to limit exposure but cannot fully neutralize compliance delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: LWIR Dominance Faces SWIR Disruption

The automotive night vision systems for LWIR solutions contributed 62.78% of the global value. Strong thermal contrast enables reliable pedestrian recognition beyond headlight beams, explaining sustained uptake in regulatory test cycles. SWIR sensors are scaling at a high CAGR of 15.88% as wafer-level photodiodes have crossed the USD 100-per-unit threshold. Semiconductor processes familiar to camera fabs supply attractive cost curves, and SWIR’s ability to see through snow spray and light fog is compelling for autonomous highway duty. The automotive night vision systems market share held by LWIR is expected to erode gradually, though it remains the benchmark for compliance certification. Active Near-Infrared occupies a middle path, supplying monochrome imagery at 600 ft ranges when paired with discreet LED emitters.

R&D pipelines continue to broaden spectral reach. Aalto University delivered germanium photodiodes with 35% higher responsivity at 1.55 µm, ideal for SWIR automotive bands. At the extreme, quantum-dot detectors have logged detectivity up to 18 µm wavelengths, demonstrating the future ceiling for sensor designers. For the next five years, dual-band arrays that blend LWIR and SWIR on common logic will likely headline premium packages, assuring redundancy while tempering total cost of ownership.

By Display Type: HUD Leadership Challenged by Infotainment Integration

Head-up displays secured 43.10% of the market share in 2025, contributing to the market size of automotive night vision systems. Drivers value forward-view retention and reduced glance time. Even so, center-stack displays capture budget placements because automakers already embed 12-inch or larger touchscreens for navigation and streaming. A CAGR of 18.05% sets infotainment-based feeds on course to meet HUD installations by the decade's end. Therefore, the automotive night vision systems market share of HUD modules is forecast to slip to the mid-30% band by 2031.

Future cockpits will reinforce augmented-reality overlays. Continental, Bosch, and HARMAN previewed display controllers that highlight warm-body silhouettes in color-coded boundaries. In lower trims, instrument-cluster views or split-screen widgets may suffice. Because windshield-projected data demands stringent optical alignment, some mass-volume badges bypass HUD architecture until component prices fall. Dual-mode strategies allow premium marques to sustain HUD as a headline feature while mid-range nameplates repurpose center panels, preserving functional consistency across line-ups.

By Component: Camera Dominance with Illumination Growth

Cameras represented 54.72% of the automotive night vision systems market share in 2025. The camera assembly integrates the focal-plane array, vacuum package, and primary lens stack, hence its outsized weight in the bill. IR illumination sources accounted for a smaller base but are estimated to rise at 15.65% CAGR as active systems proliferate. In mass-market crossovers, combination NIR camera-LED units balance cost and performance, especially for urban-density driving, where street furniture can confuse passive thermal edge detection.

Processing units remain essential for frame differencing, object classification, and driver alert logic. Many are migrating to domain controllers that service multiple ADAS functions, aiding board consolidation. Display modules, though technically simple, still dictate user acceptance. Panel brightness, contrast ratio, and ambient-light adaptation decide whether drivers trust thermal cues. Suppliers respond with automotive-grade OLEDs rated for –40 °C to +105 °C, ensuring lifespan parity with core electronics.

By Vehicle Type: Passenger Car Base Enables Commercial Growth

Passenger cars constituted 81.74% of the automotive night vision systems market share in 2025, yet the light commercial vehicle sub-segment generates the strongest momentum. At a 14.52% CAGR, fleets exploit thermal overlays to secure insurance rebates while protecting pedestrians in depot zones. Long-haul trucks and intercity buses follow suit, where night-time highway risk is concentrated. The automotive night vision systems market size for heavy vehicles expands from a low base. It attracts partnerships between chassis makers and specialist Tier-1s who guarantee functional safety ratings up to ASIL D.

In parallel, premium crossovers and sedans keep pilots for next-generation perception stacks. Their larger electrical budgets accommodate dual-thermal arrays and hybrid sensor fusion that migrate to cargo vans once cost targets align. As regulators finalize commercial vehicle AEB protocols, the technology jump from premium passenger to fleet LCV is expected to compress from five years today to less than three.

By Sales Channel: OEM Integration Dominates Aftermarket

OEM factory-fit installations accounted for 83.90% of the automotive night vision systems market in 2025 and are projected to record the highest CAGR of 15.02% over the forecast period. Direct integration during assembly guarantees correct sensor positioning, heating elements, and secure over-the-air software updates. Warranty frameworks also simplify liability in the event of false positives or detection failures. Aftermarket solutions retain niche popularity among driving enthusiasts and classic-car owners, but complex alignment procedures and limited ecosystem support curb mass adoption.

Tier-1 suppliers emphasize standardized camera modules that fit multiple vehicle platforms. Magna, for instance, surpassed the one-million-unit milestone and still owns 98% of cumulative deployments. New entrants face exhaustive PPAP qualification cycles, yet partnership announcements between Valeo and Teledyne FLIR indicate that competitive pressure is rising. While retrofit kits should persist for specialty vehicles, the primary battleground will remain the OEM procurement cycle ruled by rigorous ASIL targets.

Geography Analysis

North America controlled 41.20% of the 2025 automotive night vision systems market turnover. Legislative clarity is the decisive edge. The NHTSA stipulation that pedestrian AEB operate in darkness by September 2029 forces automakers to lock in sourcing roadmaps now. Domestic suppliers such as Teledyne FLIR and L3Harris furnish mature thermal cores, keeping value added onshore. Premium-SUV demand in the United States compounds volume, while Canadian assembly plants mirror U.S. specifications thanks to shared vehicle architectures.Teledyne FLIR's collaboration with VSI Labs in FMVSS No. 127 compliance testing positions North American suppliers advantageously for global market expansion.

Asia-Pacific is projected to record a 14.33% CAGR. China leads the regional charge as it scales level-2+ ADAS for domestic brands. GAC, NIO, and BYD incorporate AI-powered image enhancement that elevates standard CMOS sensors toward pseudo-thermal output, yet true LWIR adoption is accelerating in flagship trims. Local fabrication of chalcogenide lenses and low-cost wafers is underway to reduce exposure to export controls. Japan and South Korea add premium penetration via Toyota, Lexus, Hyundai, and Genesis nameplates, each pairing night vision with surround-view camera suites.

Europe exhibits balanced growth built on its own General Safety Regulation 2029. German marques led with early-2000s deployment and now refine sensor fusion for conditional autonomy. Valeo’s supply agreement with Teledyne FLIR covers series production thermal cameras that meet ASIL B objectives. France’s Lynred is doubling clean-room area under an EUR 85 million program to secure detector capacity against geopolitical shocks. Scandinavian markets display above-average uptake because of prolonged winter darkness, while southern European volume hinges on upscale imports. Although the region trails North America in share, synchronous regulation and supplier investments lock in dependable growth.

Competitive Landscape

Market concentration remains elevated but is trending lower. Magna’s pioneering thermal solution first appeared on the 2005 BMW 7-Series and has since delivered over one million modules, capturing a cumulative 98% share of deployed automotive night vision cameras. However, stakeholders sense an inflection point as compliance deadlines expand the addressable market from luxury sedans to high-volume crossovers.

Teledyne FLIR and Valeo signed a production contract to co-develop ASIL-grade thermal imagers that integrate with radar and LiDAR. This aligns Valeo’s extensive ADAS distribution with Teledyne’s infrared heritage, challenging Magna’s dominance. Bosch, DENSO, and Continental are exploring build-or-buy pathways, occasionally taking minority stakes in photonics start-ups to access intellectual property without lengthy licensing. Meridian Innovation uses CMOS tooling to target sub-USD 100 camera costs, aiming squarely at mid-segment trims that previously relied on visible-light cameras alone.

Patenting activity underscores a race for cost-optimized integration. Mercedes-Benz recently filed a method for thermal object detection that compensates for ambient temperature variance, signaling OEM intent to own critical algorithms. Meanwhile, software-centric players such as Deepthink and Visionary.ai insert AI pipelines that convert noisy nighttime frames into high-contrast overlays without dedicated thermal hardware. Although these solutions still require validation, they illustrate the competitive tension between hardware-heavy and software-defined approaches.

Automotive Night Vision System Industry Leaders

-

FLIR Systems Inc.

-

DENSO Corporation

-

Autoliv Inc.

-

Magna International Inc.

-

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Imagry announced a partnership with ADASKY to incorporate advanced thermal imaging technology into Imagry's AI-driven autonomous vehicle platform, enabling operation in complete darkness and extreme weather conditions while enhancing navigation safety capabilities.

- January 2024: Valeo and Teledyne FLIR announced collaboration and first contract for thermal imaging automotive safety systems, delivering ASIL B thermal imaging for night vision ADAS integration with existing sensor technologies.

Global Automotive Night Vision System Market Report Scope

An automotive night vision system uses a thermographic camera to increase a driver's perception and see the distance in darkness or poor weather beyond the reach of the vehicle's headlights. The report also covers the market size and forecast for the automotive night vision system market across the regions mentioned.

The Automotive night vision system market has been segmented by technology, display, component, and geography. The market has been segmented by technology type into far infrared (FIR) and near-infrared (NIR). The market has been segmented by display type into navigation systems, instrument clusters, and HUD.

The market has been segmented by component type into night vision cameras, a controlling units, display units, sensors, and other components. By geography, the market has been segmented into North America, Europe, Asia-pacific, and the rest of the world. For each segment, the market sizing and forecast have been done on the basis of value (USD billion).

| Far Infrared (LWIR, uncooled) |

| Near Infrared (NIR) |

| Short-Wave Infrared (SWIR) |

| Navigation System |

| Instrument Cluster |

| Head-Up Display (HUD) |

| Central Infotainment/IVI Screen |

| Night Vision Cameras (Thermal, NIR) |

| Control/Processing Units |

| Display Modules |

| IR Illumination Sources (LED/VCSEL) |

| Sensors and Other Components |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| OEM Factory-fit |

| Aftermarket Retrofit |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology Type | Far Infrared (LWIR, uncooled) | |

| Near Infrared (NIR) | ||

| Short-Wave Infrared (SWIR) | ||

| By Display Type | Navigation System | |

| Instrument Cluster | ||

| Head-Up Display (HUD) | ||

| Central Infotainment/IVI Screen | ||

| By Component Type | Night Vision Cameras (Thermal, NIR) | |

| Control/Processing Units | ||

| Display Modules | ||

| IR Illumination Sources (LED/VCSEL) | ||

| Sensors and Other Components | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Sales Channel | OEM Factory-fit | |

| Aftermarket Retrofit | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive night vision systems market?

The market stands at USD 3.68 billion in 2026 and is forecast to hit USD 6.34 billion by 2031 with an 11.52% CAGR.

Which technology holds the largest automotive night vision systems market share?

Far Infrared (LWIR) solutions hold 62.78% share in 2025, supported by superior thermal contrast useful for pedestrian detection at night.

Why are automakers shifting toward sensor fusion that combines thermal and visible cameras?

Fusion reduces perception blind spots in low-light conditions, enabling Level 3 autonomy while meeting impending safety mandates.

What segments beyond luxury cars are expected to drive future growth?

Light Commercial Vehicles are projected to grow at a 14.52% CAGR as fleet owners seek insurance incentives tied to reduced nighttime accident rates.

Page last updated on: