Automotive Horn Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 0.75 Billion |

| Market Size (2031) | USD 0.88 Billion |

| Growth Rate (2026 - 2031) | 3.23% CAGR |

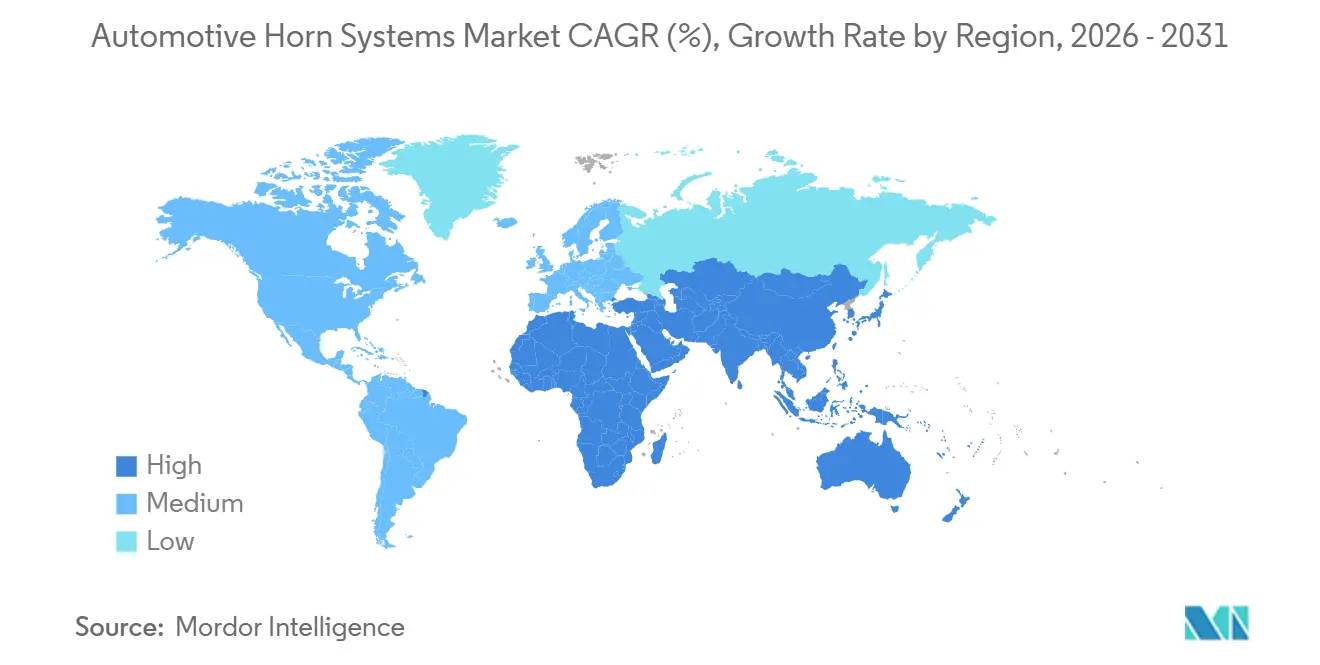

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Horn Systems Market Analysis by Mordor Intelligence

The automotive horn systems market size is expected to grow from USD 0.73 billion in 2025 to USD 0.75 billion in 2026 and is forecast to reach USD 0.88 billion by 2031 at a 3.23% CAGR over 2026-2031. Regulatory scrutiny on audible-warning devices, growth in Asia-Pacific vehicle output, and rising integration with advanced driver-assistance electronics continue to shape demand. Electronic designs that pair with body-control units dominate new installations, while pneumatic solutions maintain a niche in heavy commercial fleets for maximum sound pressure. Material inflation and localized noise cap pricing pressure, yet e-commerce channels keep aftermarket volumes resilient. Forward-looking suppliers are embedding software-defined tone libraries and CAN-bus diagnostics to align with predictive fleet-maintenance platforms.

Key Report Takeaways

- By product type, electronic horns held 45.61% of the automotive horn systems market share in 2025, while air horns are projected to register a 3.29% CAGR through 2031.

- By horn shape, flat horns led with 50.93% of the automotive horn systems market share in 2025; spiral horns are set to advance at a 3.38% CAGR through 2031.

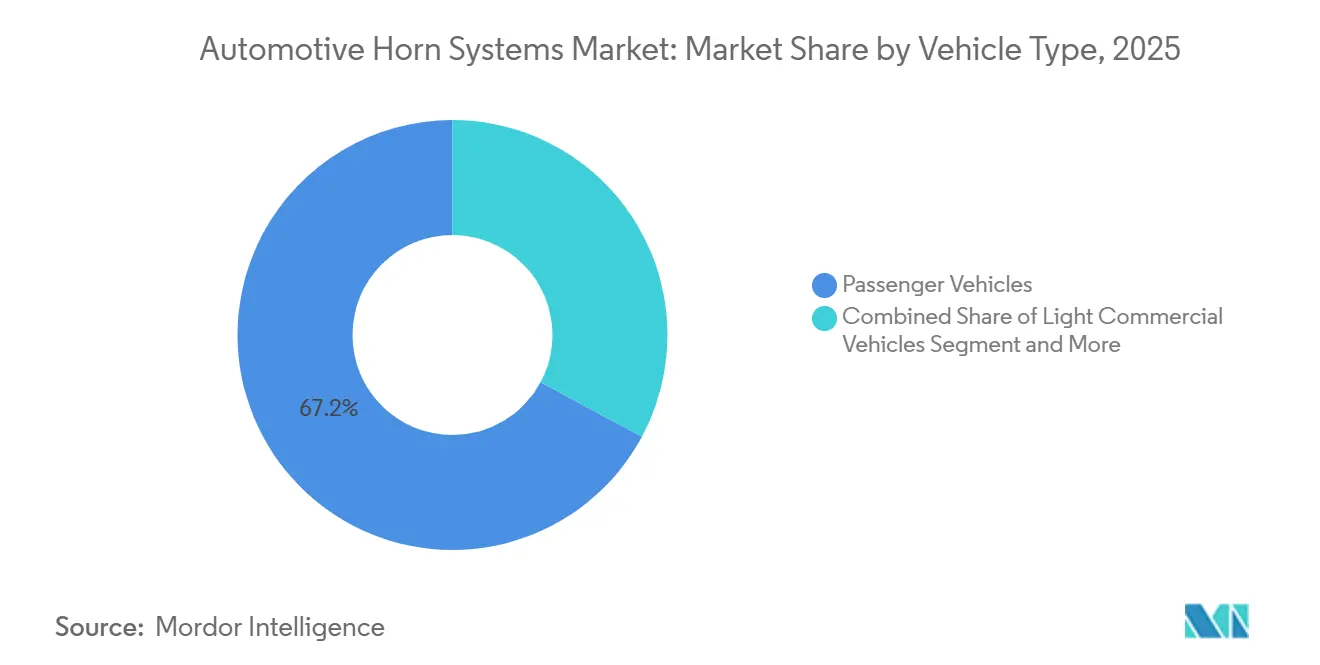

- By vehicle type, passenger cars captured 67.16% of the automotive horn systems market share in 2025, whereas medium- and heavy-duty commercial vehicles are poised for a 3.31% CAGR through 2031.

- By distribution channel, OEM installations accounted for 71.27% of the automotive horn systems market share in 2025, but aftermarket sales are expected to grow at a 3.33% CAGR through 2031.

- By geography, Asia-Pacific accounted for 39.81% of the automotive horn systems market share in 2025 and is on track to expand at a 3.35% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Horn Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vehicle Production | +0.8% | Asia-Pacific core, spillover to global OEM supply chains | Medium term (2-4 years) |

| Increasing Adoption Of Electric & Electromagnetic Horns | +0.6% | Global, with early adoption in Europe and North America | Short term (≤ 2 years) |

| Stricter Global Horn-Audibility | +0.5% | Global, led by EU, NHTSA, and emerging India regulations | Long term (≥ 4 years) |

| Rapid Expansion Of E-Commerce Channels | +0.4% | Europe and North America leading, expanding to Asia Pacific | Medium term (2-4 years) |

| Smart, ADAS-Linked Customizable Horn Tones | +0.3% | Premium segments in developed markets | Long term (≥ 4 years) |

| Predictive Maintenance Via Fleet-Telematics | +0.2% | Commercial fleet segments globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Production in Asia-Pacific Spurring OEM Horn Demand

Factory output in China and India climbed in 2025, lifting first-fit orders for electromagnetic and electronic horns. Local content rules encourage suppliers to open plants near final-assembly hubs and shorten logistics chains. OEMs favor modular horn brackets that drop directly into mixed-powertrain lines. Regional standards now align more closely with UN R28, easing transnational homologation. Suppliers that pair acoustic hardware with digital validation services secure platform nominations faster than price-only rivals.

Increasing Adoption of Electric & Electromagnetic Horns for Energy-Efficient Safety

Electromagnetic disc units that draw 3–5 amperes match electric-vehicle power budgets and integrate with acoustic vehicle-alerting systems. KEPO’s 3-in-1 module combines horn, pedestrian-alert, and welcome sounds in a single enclosure. Digital signal processing enables tone personalization without hardware swaps, appealing to ride-sharing fleets that value brand sound signatures. Over-the-air firmware allows compliance updates when jurisdictions tighten noise limits. Cost premiums continue to narrow as solenoid prices stabilize.

Stricter Global Horn-Audibility and Pedestrian-Safety Regulations

UN R28 sets a 105–118 dB(A) window measured 2 meters from the device[1]"Guide To: UNECE R28 - Audible warning devices," Dun-Bri Group, www.dun-bri.com. Automakers now verify compliance virtually using finite-element acoustics before tooling hard parts, trimming late rework. Governments in Europe and North America run roadside sound checks that fine non-compliant units. These audits spur OEMs to source horns pre-certified for multiple markets. Simulation-ready suppliers earn preferred-vendor status by reducing launch risk.

Rapid Expansion of E-Commerce Channels for Aftermarket Parts

Online storefronts list hundreds of horn SKUs with user reviews and installation guides. Fleet buyers compare CAN bus compatibility, duty cycles, and warranty terms without intermediaries. Algorithm-driven recommendations surface niche items such as wireless trigger kits, broadening category awareness. Direct-to-consumer logistics shrink lead times and support subscription models for periodic replacements. Platform policies now flag listings that exceed legal decibel thresholds, steering shoppers toward compliant units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Noise-Pollution Caps Constraining Allowable Decibel Output | -0.4% | Urban centers globally, particularly India and Europe | Short term (≤ 2 years) |

| Raw-Material Price Spikes & Supply-Chain Disruptions | -0.3% | Global, with China dependencies creating vulnerability | Medium term (2-4 years) |

| EV Acoustic Vehicle Alerting System Reducing Reliance | -0.3% | EV adoption markets, led by Europe and China | Long term (≥ 4 years) |

| Urban Anti-Honking Initiatives Dampening Replacement Demand | -0.2% | Major urban centers in India, select European cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Noise-Pollution Caps Constraining Allowable Decibel Output

City ordinances in Delhi, Mumbai, and Westminster set maximum sound-pressure levels and impose on-the-spot fines. Campaigns that restart traffic lights when ambient noise rises discourage unnecessary honking. Retailers now highlight certified decibel ratings to avoid seizure of non-compliant stock. Designers balance audibility with acceptable volume by shifting toward dual-frequency envelopes that carry further at lower pressure. Stringent zones accelerate demand for spiral chambers tuned for low-frequency reach rather than peak dB.

Raw-Material Price Spikes & Supply-Chain Disruptions for Electronic Components

Copper futures climbed sharply in late 2025, lifting costs for coil windings and relay contacts[2]"Copper price surge drives quarterly lead frame price hikes," DIGITIMES, www.digitimes.com. Aluminum price volatility raises enclosure expenses, and rare-earth magnet premiums compress margins. Suppliers hedge with long-term contracts and investigate aluminum wiring harnesses to cut copper mass. Some shift production closer to ore sources to limit freight surcharges. Others explore flat-wire designs that lower copper per unit without compromising acoustic power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electronic Advantage, Pneumatic Momentum

Electronic horns commanded 45.61% of the automotive horn systems market share in 2025, reflecting automaker trust in solid-state reliability and seamless electronics integration. Software-defined tone profiles help brands differentiate cabin experiences while keeping compliance validation simple. Their sealed architecture also meets durability targets in humid or dusty climates. Suppliers bundle diagnostics that broadcast horn health across vehicle networks, enabling predictive maintenance without additional wiring. Growth in shared-mobility fleets further favors electronic designs because usage data can be captured and analyzed at scale.

Air horns, although a smaller slice, are on course for the quickest 3.29% CAGR through 2031 as freight operators insist on unmistakable low-frequency warnings in crowded corridors. The pneumatic format pairs naturally with existing truck air systems and maintains acoustic reach even when electric drivetrains replace diesel engines. Fleet managers value the recognizably deep timbre that cuts through construction-zone noise without electronic artifacts. Aftermarket installers continue to highlight bolt-on kits that require no software updates, expediting weekend retrofits. Regulatory bodies still allow air horns when tuned within legal decibel windows, ensuring the niche remains viable for years.

By Horn Shape: Flat Footprint, Spiral Resonance

Flat horns led the segment with 50.93% of the automotive horn systems market share in 2025, benefiting from compact casings that slip behind fascias now crowded by cameras, sensors, and battery packs. Automakers appreciate the straightforward stamping and plating steps that keep supply chains lean. Engineers can position flat units close to structural rails, gaining natural amplification without extra brackets. A wide supplier base delivers interchangeable parts, reducing dual sourcing headaches when platforms stretch across regions.

Spiral horns exhibit the fastest 3.38% CAGR because their helical chambers amplify lower frequencies that remain audible under strict urban noise caps. Digital simulation accelerates chamber design, letting engineers validate sound envelopes before tooling. Automakers capitalize on the deeper pitch to project authority without exceeding limits, a balance welcomed by city regulators. Component suppliers also tout corrosion-resistant coatings that extend life when spirals sit near wheel wells and road spray.

By Vehicle Type: Passenger Dominance, Commercial Upswing

Passenger cars absorbed 67.16% of the automotive horn systems market share in 2025, as every light vehicle ships with at least one factory-fitted unit. Mass production favors cost-optimized electromagnetic discs that bolt into standardized front-end modules. Automakers weave horn switching into steering-wheel electronics, minimizing standalone cabling. Interior design teams also collaborate on signature external sounds that match welcome lighting, reinforcing brand cues when vehicles unlock. Over-the-air sound updates are emerging in premium trims, letting owners refresh tones without hardware swaps.

Medium and heavy commercial vehicles hold the fastest 3.31% CAGR because fleet telematics platforms now flag horn wear alongside brake-pad life. Managers schedule replacements during routine service stops, preventing roadside failures that could breach safety codes. Larger truck fronts offer generous mounting space, so suppliers fit dual horns tuned to complementary frequencies for long-range audibility. Regulatory agencies treat reliable horns as a core crash-avoidance feature on busy freight corridors, embedding checks into annual inspections.

By Distribution Channel: Factory Standard, Digital Shelf Rise

OEM contracts represented 71.27% of the automotive horn systems market share in 2025, underpinned by legal mandates that place horn approval squarely inside the vehicle-type-certification process. Tier-one suppliers lock multi-year deals that bundle horns with other front-end electronics, streamlining procurement for automakers. With platforms now lasting a decade or longer, validated parts remain in production to avoid costly recertification. Software-defined units add flexibility without physical redesign, strengthening the OEM channel’s hold on first-fit business. Global sourcing offices still favor vendors offering in-house acoustic testing, shortening time to market for facelifts and derivative body styles.

Aftermarket sales are set to witness a 3.33% CAGR through 2031, as e-commerce storefronts simplify comparison shopping and doorstep delivery. Do-it-yourself owners can filter by connector type, mounting tab, and decibel rating, removing the guesswork that once required counter-staff advice. Fleet technicians appreciate bulk ordering tools that align stock levels with telematics alerts, avoiding emergency purchases at roadside premiums. Influencer videos demonstrate step-by-step installs, expanding the comfort zone for novices. Marketplaces now tag listings with regional compliance notes, helping buyers steer clear of units banned in certain municipalities.

Geography Analysis

Asia-Pacific remains the epicenter of demand, holding 39.81% of the automotive horn systems market share in 2025 and maintaining a leading 3.35% CAGR into the next decade. Local governments encourage in-region sourcing, so suppliers establish coil-winding and stamping lines near final assembly plants. Harmonization with UN R28 eases cross-border homologation, letting global brands ship common designs from China, India, or Thailand. Indigenous players partner with multinational tier-ones to access digital validation software that shortens launch cycles. Training programs supported by technical institutes help raise acoustic-engineering capabilities, feeding a talent pipeline attuned to next-generation sound systems.

Europe shows stable replacement activity even as some automakers move from dual to single horns in passenger models. Premium German manufacturers invest in virtual prototyping, so suppliers with strong simulation credentials win design contests. Noise-abatement zones in cities like Paris and Amsterdam push engineers toward lower-frequency tones that travel far without breaching limits, rewarding spiral-horn innovators. Aftermarket enthusiasts still personalize their sounds, but retailers highlight certified decibel levels to comply with municipal rules.

North America blends a storied culture of customization with rising connected-fleet adoption. Pickup and recreational-vehicle owners embrace brand-licensed kits that integrate seamlessly with factory wiring and steering-wheel controls. Telematics dashboards used by logistics operators now flag horn-health metrics, nudging preventive swaps at scheduled maintenance intervals. State noise ordinances influence product marketing more than engineering, so sellers display compliance badges prominently online. Suppliers opening regional logistics hubs aim to cut delivery times for both OEM and aftermarket clients, reflecting a customer base that values rapid fulfillment. South America and the Middle East & Africa, while smaller, court investment through incentives that localize final assembly and spark ancillary parts production, including audible-warning devices.

Competitive Landscape

The automotive horn systems market is moderately concentrated. Global tier-one suppliers shape the high end of the value chain through scale, vertical integration, and access to automaker programs that last an entire platform life cycle. Uno Minda deepened its European reach after integrating a Spanish horn manufacturer and quickly redirected engineering toward pairing horns with electric-vehicle charging units. FORVIA, created when Faurecia absorbed HELLA, now pitches unified exterior-signature packages that weave lighting, radar covers, and horn tones into coherent brand identities. Bosch and Denso rely on synchronized global plants that let them deliver identical audible-warning devices on three continents without resetting validation tests.

A vigorous mid-tier of regional specialists counters the giants with niche agility and software-centric innovation. Companies rooted in India, China, and Southeast Asia exploit proximity to fast-growing assembly hubs by co-designing brackets and harnesses that match local body-in-white geometries. Several have launched contactless digital horns that drop mechanical contacts altogether, opening the door to downloadable sound libraries controlled by over-the-air updates. Simulation know-how is becoming a passport to global sourcing lists, so these firms bundle finite-element acoustic models with their quote packages even when they still outsource metal stamping. Collaboration with ride-hailing fleets gives them real-world duty-cycle data to refine durability targets that match dense urban traffic.

Distribution dynamics add another competitive layer that rewards brands able to bridge factory programs and direct-to-consumer channels. E-commerce storefronts let newcomers bypass traditional aftermarket wholesalers and market specialty items with extensive installation media, closing the knowledge gap for do-it-yourself buyers. Fleet telematics providers partner with module makers that can publish health and usage metrics, creating subscription revenue for both hardware and data services. Established suppliers respond by opening regional fulfillment centers that guarantee 24-hour delivery of replacement units and accessory kits. Compliance remains the universal gatekeeper, as city and national authorities enforce decibel caps that can ban otherwise popular products overnight.

Automotive Horn Systems Industry Leaders

-

Uno Minda

-

Robert Bosch GmbH

-

Hella GmbH & Co. KGaA

-

FIAMM Energy Technology S.p.A.

-

Mitsuba Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Uno Minda rolled out a new trumpet-horn range for the Indian aftermarket, citing demand for clearer vehicle alerts.

- September 2025: PRM Automotives India debuted its first horn line at Passenger Vehicle Expo 2.0, signaling a push into component manufacturing.

- April 2025: India’s Road Transport Minister proposed mandating horn sounds based on traditional instruments such as the flute and tabla, pointing the market toward fully programmable driver boards.

Global Automotive Horn Systems Market Report Scope

The Global Automotive Horn Systems Market is analyzed based on product type, horn shape, vehicle type, distribution channel, and geography.

By Product Type, the market includes Electric Horns, Air Horns, and Electromagnetic Horns. By Horn Shape, it is categorized into Flat Horns, Spiral Horns, and Trumpet Horns. By Vehicle Type, it covers Passenger Vehicles, Light Commercial Vehicles, and Medium & Heavy Commercial Vehicles. By Distribution Channel, the market is split between OEM and Aftermarket. By Geography, the market is segmented into North America, South America, Europe, Asia Pacific, and the Middle East & Africa.

Market forecasts are provided in terms of Value (USD).

| Electric Horn |

| Air Horn |

| Electromagnetic Horn |

| Flat Horn |

| Spiral Horn |

| Trumpet Horn |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East & Africa |

| By Product Type | Electric Horn | |

| Air Horn | ||

| Electromagnetic Horn | ||

| By Horn Shape | Flat Horn | |

| Spiral Horn | ||

| Trumpet Horn | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive horn systems market in 2031?

The automotive horn systems market size is forecasted to reach USD 0.88 billion by 2031, growing at a 3.23% CAGR over 2026-2031.

Which product type currently leads global demand?

Electronic horns held the largest share at 45.61% in 2025, favored for low current draw and software-defined tones.

Which segment is expected to grow the fastest by 2031?

Air horns are projected to post the quickest 3.29% CAGR as freight operators seek louder warnings for dense traffic.

Why is Asia-Pacific a focal region for suppliers?

The region accounts for 39.81% of revenue and continues to expand on rising vehicle assembly in China and India.

Page last updated on: