Automotive Regenerative Braking System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

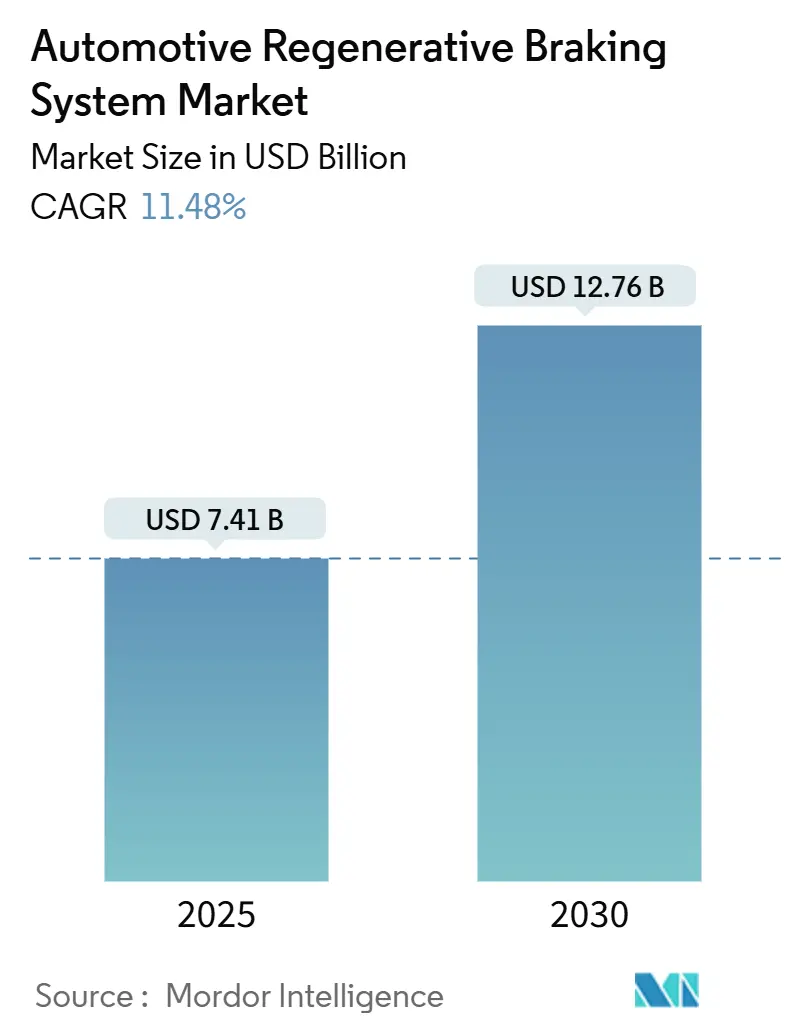

| Market Size (2025) | USD 7.41 Billion |

| Market Size (2030) | USD 12.76 Billion |

| Growth Rate (2025 - 2030) | 11.48% CAGR |

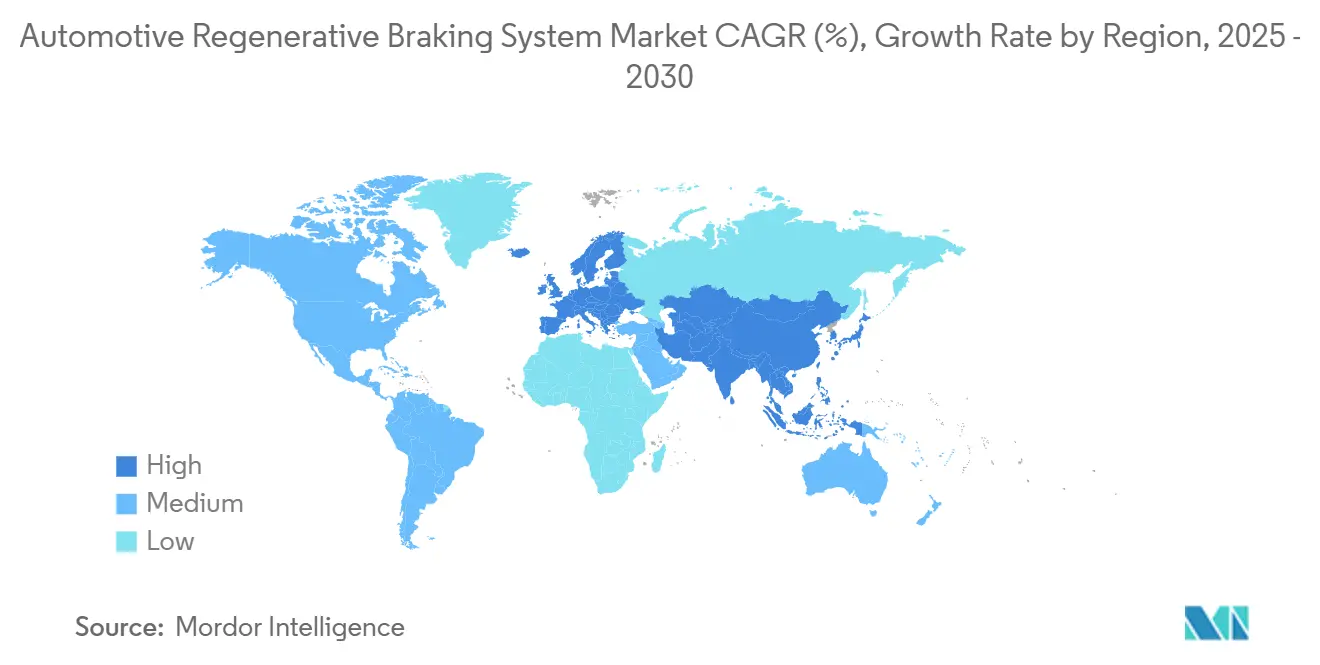

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Regenerative Braking System Market Analysis by Mordor Intelligence

The automotive regenerative braking system market reached USD 7.41 billion in 2025 and is forecast to expand to USD 12.76 billion by 2030, advancing at an 11.48% CAGR. At its core, the technology recovers kinetic energy during deceleration and channels it back to the battery, enhancing range and lowering running costs. Growth stems from a shift to electromechanical brake-by-wire designs, rising electric and hybrid vehicle sales, and regulatory frameworks that reward real-world efficiency improvements. Electromechanical systems lead, while pneumatic solutions show the fastest growth, because heavy-duty trucks harvest greater energy per stop. Supply chain tightness for rare-earth magnets and silicon-carbide chips remains a brake on momentum, prompting vertical integration by leading suppliers.

Key Report Takeaways

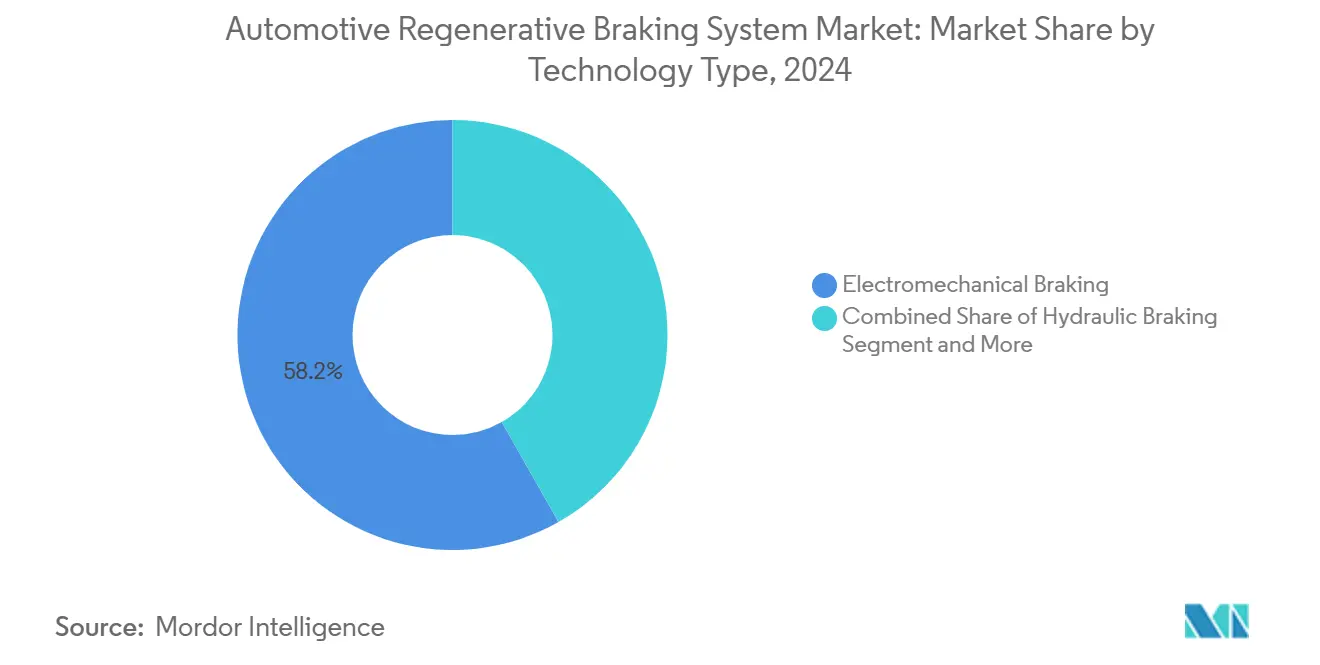

- By technology type, electromechanical systems captured 58.15% of the automotive regenerative braking system market share in 2024, while pneumatic systems are projected to grow at a 12.71% CAGR to 2030.

- By component type, electric motors accounted for a 42.11% share of the automotive regenerative braking system market size in 2024, and are forecast to post an 11.78% CAGR between 2025-2030.

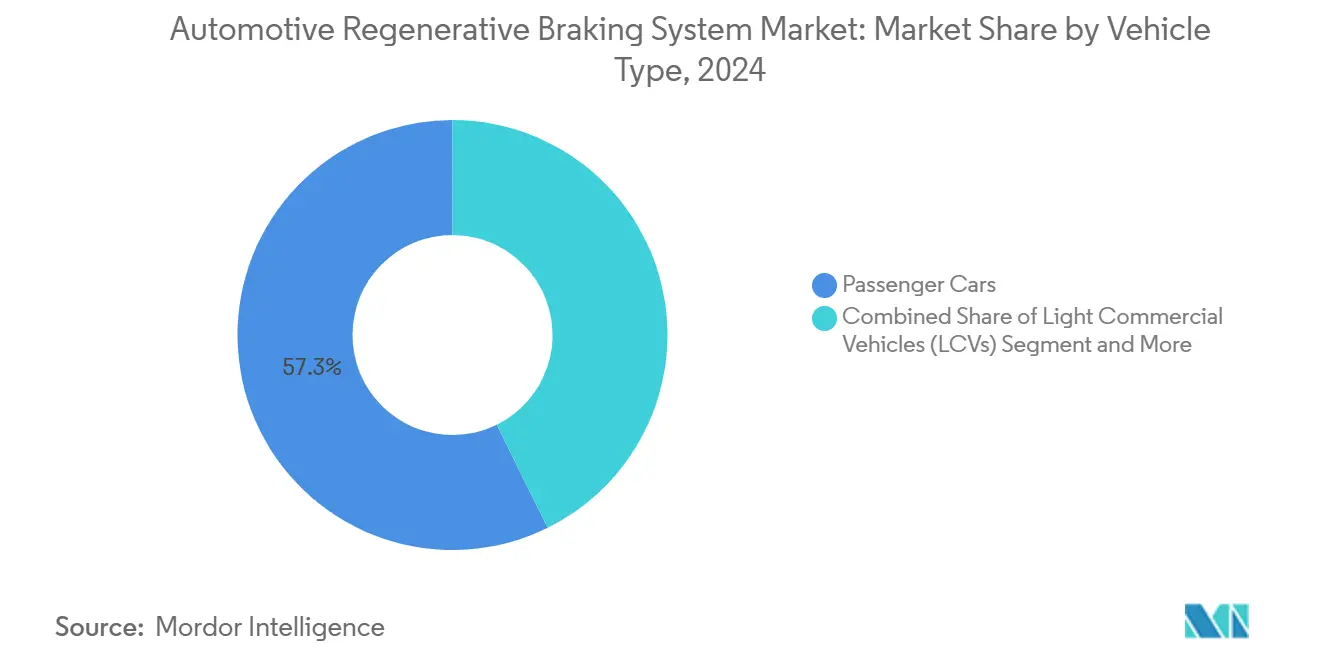

- By vehicle type, passenger cars represented 57.33% of the automotive regenerative braking system market share in 2024; medium and heavy commercial vehicles are projected to expand at a 13.66% CAGR through 2030.

- By distribution channel, the OEM segment held 79.46% of the automotive regenerative braking system market share in 2024, while the aftermarket segment is advancing at a 13.18% CAGR to 2030.

- By geography, Asia-Pacific held 47.13% share of the automotive regenerative braking system market size in 2024, while Europe is forecast to grow at a 12.24% CAGR between 2025-2030.

Global Automotive Regenerative Braking System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV and Hybrid Sales Surge | +3.2% | Global, APAC and Europe leading | Medium term (2-4 years) |

| Stricter Global Emission Norms | +2.8% | Europe and North America; APAC following | Long term (≥ 4 years) |

| OEMs Adopt Brake-By-Wire | +2.1% | Global, premium segments first | Medium term (2-4 years) |

| Battery Cost Declines Boost ROI | +1.9% | Global, with scale benefits in APAC | Short term (≤ 2 years) |

| Data-Driven Fleet Optimization | +1.3% | North America and Europe fleets | Medium term (2-4 years) |

| Carbon-Credit Trading Integration | +0.9% | Europe primary, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Electric and Hybrid Vehicle Sales

Global adoption of battery-electric and hybrid vehicles makes regenerative braking a baseline requirement rather than an option. Automakers such as Tesla integrate high-capacity motors that can recapture a significant share of brake energy, a feature now extending from premium sedans to mass-market compacts. Commercial e-trucks gain still more because higher curb weights and stop-and-go duty cycles multiply harvestable energy. As EV adoption curves steepen, suppliers scale production lines for motors, inverters, and control units tailored to regenerative duty cycles. The reinforcing loop between higher adoption, falling costs, and better range keeps the automotive regenerative braking system market on a steep climb.

Stringent Global Emission Norms and Incentives

Euro 7 rules, U.S. EPA greenhouse-gas targets, and China’s NEV credit scheme ratchet down fleet emission ceilings. Regulators explicitly count recuperated energy toward compliance metrics, elevating regenerative braking from “nice to have” to “must have.” The UN ECE R13-H and R152 regulations provide a harmonized test cycle and safety envelope, letting OEMs validate one solution for multiple markets [1]“Regulation No. 13-H on braking,” UN Economic Commission for Europe, unece.org. Several governments grant purchase subsidies only if the drivetrain includes energy-recovery capability, tipping buyer calculus in favor of regen-equipped models.

OEM Migration to Brake-by-Wire Architectures

Platform convergence on steer- and brake-by-wire enables millisecond-level torque blending between regenerative and friction brakes. Continental’s roadmap shows a phased rollout from hydraulic fallback solutions to fully dry electro-mechanical calipers that reduce weight, purge brake fluid, and sharpen response [2]“Future Brake System Roadmap,” Continental AG, continental.com. New entrants targeting autonomous robo-taxis embed brake-by-wire from day one, creating a pull for compact, high-power actuators that double as energy harvesters.

Rapid Battery-Cost Declines Boosting ROI

Lithium-ion pack costs are declining and will continue to slide, letting OEMs spec larger buffers without torpedoing vehicle list prices. Larger packs accept stronger regenerative currents, widening the share of braking events that can be fully recuperated. Silicon-carbide (SiC) MOSFETs cut inverter switching losses, further lifting round-trip efficiency. Payback cycles for fleets now compress below three years, accelerating procurement decisions in logistics, transit, and last-mile delivery segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Regen-Brakes | -2.1% | Global; price-sensitive markets hardest hit | Short term (≤ 2 years) |

| Supply Risks for Key Materials | -1.8% | Global; APAC concentration | Medium term (2-4 years) |

| Added Weight and Complexity | -1.6% | Global; sharper in small cars | Medium term (2-4 years) |

| Heavy-Duty Thermal Load Limits | -1.2% | Global commercial segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Regen Brake Hardware

Electric motors, high-voltage cabling, SiC inverters, and larger battery buffers inflate the bill of materials. In value-sensitive emerging economies, these premiums overshadow lifetime savings, delaying penetration into entry-level models. Leasing plans, component price declines, and government rebates are narrowing—but have not erased—the up-front delta.

Rare-Earth Magnet and SiC Chip Supply Risks

Permanent-magnet motors depend on dysprosium and neodymium, minerals with processing dominated by a handful of suppliers. Geopolitical twists or export quotas can spike prices, squeezing margins. SiC wafer capacity also trails demand from EVs, solar inverters, and server power supplies, forcing OEMs into long-term allocation contracts and dual-sourcing initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Electromechanical Systems Drive Market Evolution

Electromechanical solutions accounted for 58.15% of the automotive regenerative braking system market size in 2024 as OEMs favored fluid-free actuation that meshes cleanly with software-defined vehicle platforms. Their share is projected to rise as luxury automakers embrace dry calipers that eliminate hydraulic service intervals. Pneumatic systems, traditionally confined to heavy trucks, are forecast to expand at a 12.71% CAGR because energy harvest scales with gross vehicle weight. Hydraulic architectures persist in retrofit kits where cost and familiarity trump bleeding-edge performance.

Electromechanical units precisely meter clamping force, supporting smoother torque blending and quieter cabin acoustics. Remmen Brakes’ NEMB concept demonstrates pad-lift “Zero Drag” modes that trim parasitic losses and extend rotor life. Software upgrades can add new safety features without hardware swaps, aligning with the broader trend toward over-the-air updates across the automotive regenerative braking system market.

By Component Type: Electric Motors Lead Integration Complexity

Electric motors captured 42.11% of the automotive regenerative braking system market share in 2024, reflecting their dual role as propulsion and energy harvest devices. High-speed inner-rotor designs, fortified by SiC-based inverters, enable dense power in compact envelopes. Battery packs, ECUs, calipers, and flywheel modules round out the bill, each optimized for rapid bidirectional energy flow.

Between 2025-2030, motors are set to grow at an 11.78% CAGR as traction-motor recuperation extends to e-axles on trailers and auxiliary drives. ECU suppliers embed ISO 26262-compliant algorithms that arbitrate torque split, pedal feel, and anti-lock functions. In selected transit buses, flywheels offer mechanical storage where charge-discharge cycles exceed battery comfort zones, illustrating technology pluralism in the automotive regenerative braking system market.

By Vehicle Type: Commercial Vehicles Accelerate Adoption

Passenger cars still commanded 57.33% of the automotive regenerative braking system market size in 2024, but medium & heavy commercial vehicles will post the fastest 13.66% CAGR. Fleet managers measure ROI in years, not quarters, and regenerative braking slashes fuel, brake-pad spend, and downtime. Trailer axles with integrated generators from SAF-HOLLAND prove the concept that every rolling mass can harvest joules.

E-buses in densely populated cities capture ample stop-and-go energy, sometimes allowing downsized battery packs and faster overnight charging. Light commercial vans show mixed adoption, hinging on payload sensitivity to added component weight and local incentives caps.

By Distribution Channel: Aftermarket Gains Momentum

OEM programs held 79.46% of the automotive regenerative braking system market size in 2024 because system complexity favors factory integration and consolidated warranties. Still, aftermarket demand is climbing at a 13.18% CAGR as kit manufacturers tailor solutions for aging fleets transitioning to low-emission zones. Retrofitting demands re-certification of braking distances and stability control, but payback can be swift for urban delivery fleets.

Tier-1 suppliers seed authorized networks with diagnostic gear and training modules, while independent garages focus on light-duty pickups and ride-hail sedans. The trend fits a broader pivot to lifecycle revenue streams within the automotive regenerative braking system market.

Geography Analysis

Asia-Pacific held 47.13% of the automotive regenerative braking system market in 2024, buoyed by China’s New Energy Vehicle quotas, Japan’s hybrid leadership, and South Korea’s export-oriented EV pipeline. Local supply chains for magnets, SiC wafers, and battery cells compress costs, letting regional OEMs fit regen-ready drivetrains at competitive list prices. Government subsidies and dense charging networks further bolster adoption.

Europe is projected to grow at a 12.24% CAGR through 2030 as Euro 7 kicks in and carbon-credit monetization raises the financial upside. Automakers channel R&D budgets into next-gen brake-by-wire to satisfy advanced driver-assistance and autonomy requirements. Germany orchestrates pilot zones where vehicles upload verified CO₂ reductions to the EU Emissions Trading System, anchoring a reproducible business case.

North America shows steady uptake, led by state mandates on zero-emission miles and corporate fleet electrification pledges. The U.S. Infrastructure Law funds depot chargers and grants that offset retrofit costs for school buses and municipal fleets. South America, the Middle East & Africa lag but form green-field opportunities once component prices drift lower and policy clarity arrives.

Competitive Landscape

Market concentration is moderate; Bosch, Continental, and ZF leverage century-old braking know-how, global plants, and embedded OEM ties to supply integrated modules. Tesla pursues vertical integration, designing proprietary brake logic that fuses seamlessly with its traction-inverter firmware. Start-ups specialize in nano-coated rotors or pad-lift mechanisms that cut drag, while semiconductor giants court Tier-1s with SiC reference designs.

Collaborations are multiplying. BWI Group and thyssenkrupp are steering the co-engineering of electro-mechanical brakes that merge steering and stopping data for precise motion control [3]“Press Release: Electro-Mechanical Brake Partnership,” BWI Group, bwigroup.com. Magnet suppliers strike off-take agreements with miners to secure dysprosium flows. Competitive edge increasingly hinges on software stack maturity and supply-chain resilience rather than raw hardware specs alone.

M&A activity is expected as suppliers seek control over magnets, wafers, and battery-thermal IP. Firms that bridge braking, torque vectoring, and autonomous stacks stand to capture disproportionate wallet share in the automotive regenerative braking system industry.

Automotive Regenerative Braking System Industry Leaders

Robert Bosch GmbH

Continental AG

ZF Friedrichshafen AG

Hyundai Mobis Co., Ltd.

DENSO Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Kia confirmed its upcoming Carens Clavis EV, featuring i-Pedal one-pedal driving and advanced regenerative braking.

- July 2024: Resonac unveiled an NAO friction-material disc pad engineered for regen-coordinated brake systems in EVs.

- April 2024: BWI Group partnered with thyssenkrupp Steering to co-develop electro-mechanical brake technology aimed at autonomous platforms.

Global Automotive Regenerative Braking System Market Report Scope

| Electromechanical Braking |

| Hydraulic Braking |

| Pneumatic Braking |

| Battery Packs |

| Electric Motor |

| Brake Pads and Calipers |

| Electronic Control Unit (ECU) |

| Flywheel |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology Type | Electromechanical Braking | |

| Hydraulic Braking | ||

| Pneumatic Braking | ||

| By Component Type | Battery Packs | |

| Electric Motor | ||

| Brake Pads and Calipers | ||

| Electronic Control Unit (ECU) | ||

| Flywheel | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the automotive regenerative braking system market in 2025?

It is projected to reach USD 7.41 billion in 2025, on its way to USD 12.76 billion by 2030.

Which component category leads in revenue?

Electric motors contribute the largest slice at 42.11% of 2024 revenue.

What is driving fastest growth: passenger cars or commercial vehicles?

Medium & heavy commercial vehicles will expand at the highest 13.66% CAGR through 2030 due to fleet ROI priorities.

Which region grows the quickest over the forecast horizon?

Europe delivers the fastest 12.24% CAGR as Euro 7 rules and carbon credits amplify adoption.

Page last updated on: