Automotive Autonomous Emergency Braking System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

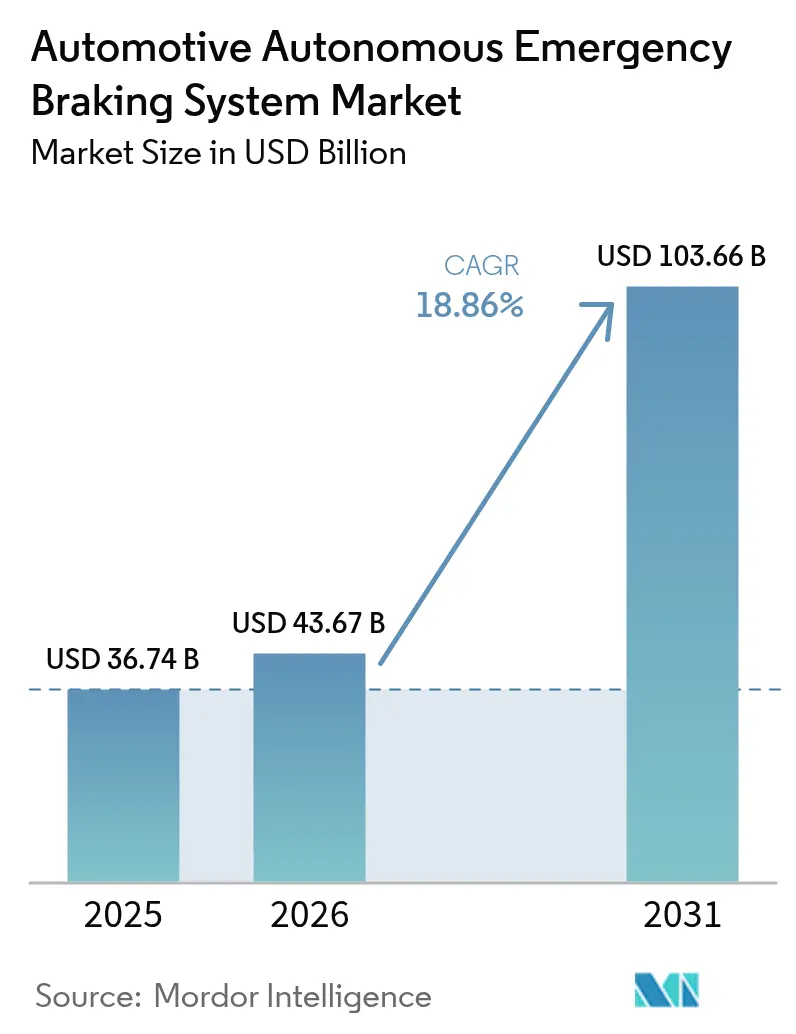

| Market Size (2026) | USD 43.67 Billion |

| Market Size (2031) | USD 103.66 Billion |

| Growth Rate (2026 - 2031) | 18.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Autonomous Emergency Braking System Market Analysis by Mordor Intelligence

The automotive autonomous emergency braking system market size in 2026 is estimated at USD 43.67 billion, growing from 2025 value of USD 36.74 billion with 2031 projections showing USD 103.66 billion, growing at 18.86% CAGR over 2026-2031. The growth trajectory is anchored in compulsory fitment rules now embedded in the United States, European Union, and China regulations. These regulations eliminate optional‐equipment cycles and drive full-range system integration across every price segment. Mandatory performance thresholds tighten around high-speed collision avoidance, night-time pedestrian detection, and junction safety, forcing automakers to standardize multi-sensor fusion architectures. Sub-USD 50 radar modules, falling LiDAR costs, and on-chip AI processing further compress system bills of material, allowing mass-market vehicles to close the technology gap with premium models. Insurance carriers, meanwhile, offer usage-based discounts on AEB-equipped fleets, catalyzing retrofit demand in commercial transport and reinforcing the autonomous emergency braking market’s momentum. Divergent regional compliance deadlines create staggered revenue waves that reward suppliers with scalable platforms capable of rapidly calibrating local protocols.

Key Report Takeaways

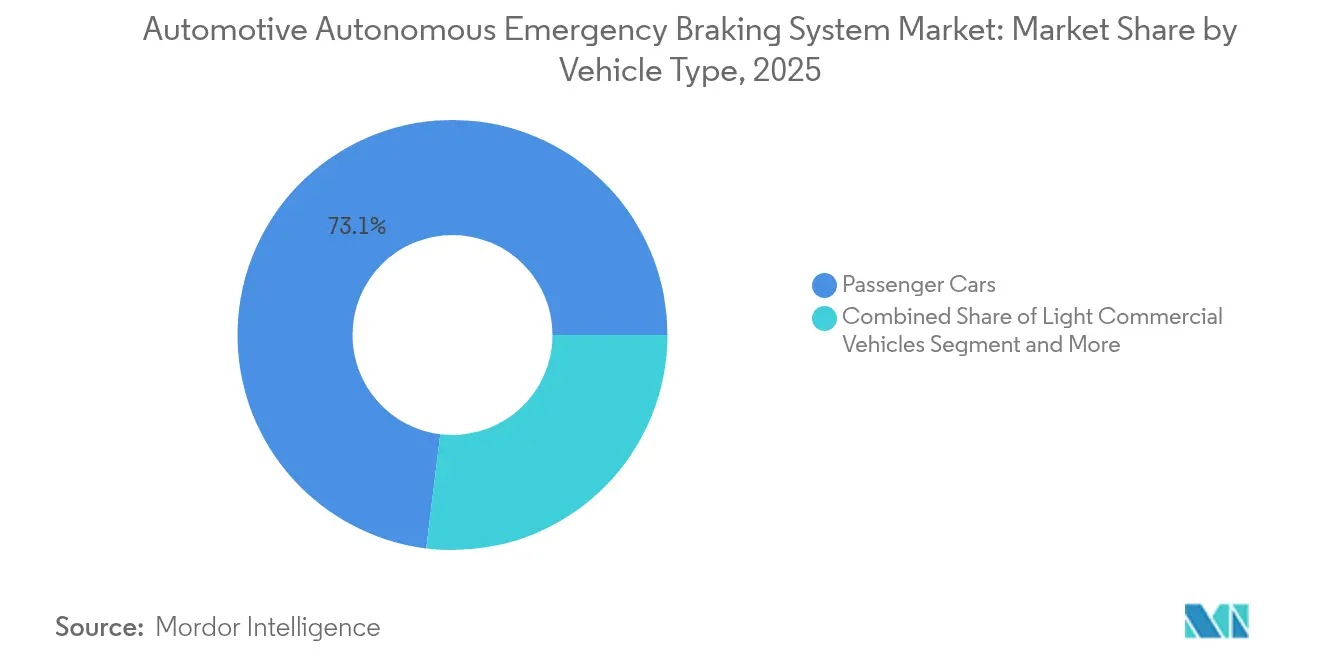

- By vehicle type, passenger cars held 73.05% of the autonomous emergency braking market share in 2025, while heavy commercial vehicles are advancing at a 13.65% CAGR through 2031.

- By component technology, radar had a 45.75% share of the autonomous emergency braking market in 2025; LiDAR is expanding at a 30.55% CAGR.

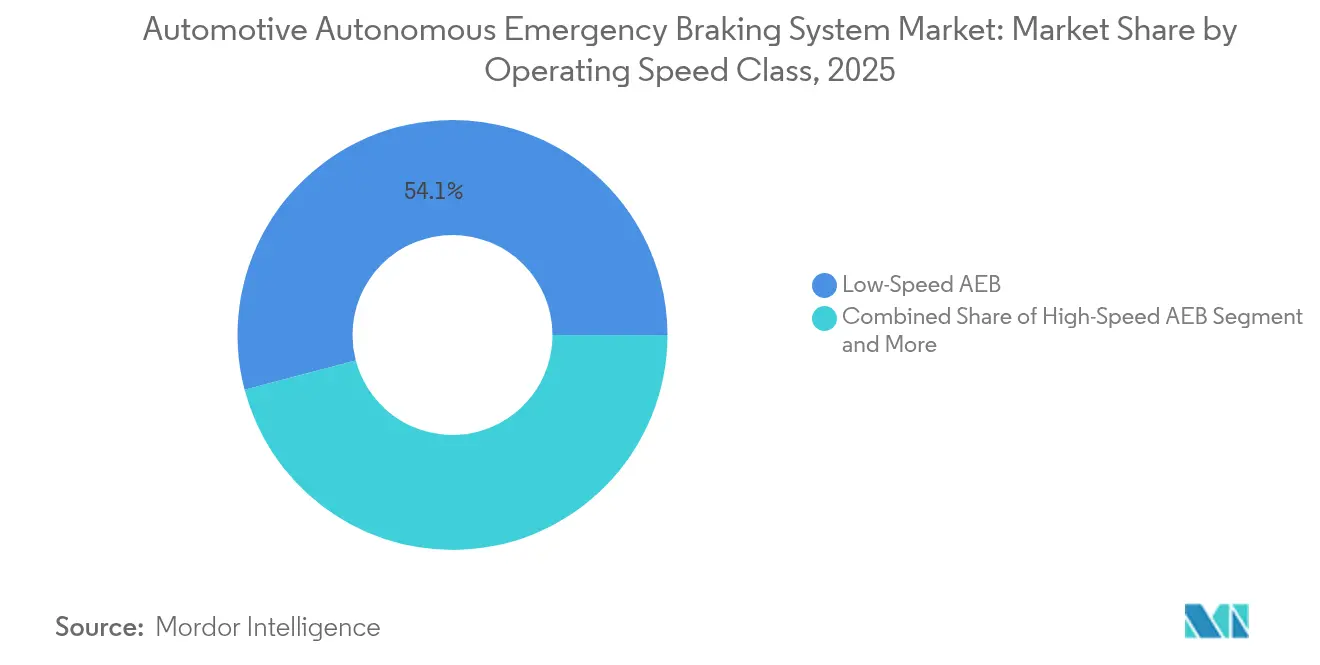

- By operating speed class, low-speed systems led the autonomous emergency braking market, with 54.10% of the size in 2025; junction AEB is projected to rise at a 27.40% CAGR to 2031.

- By sales channel, OEM installations commanded 91.10% revenue in 2025, whereas fleet retrofits are growing at an 17.45% CAGR.

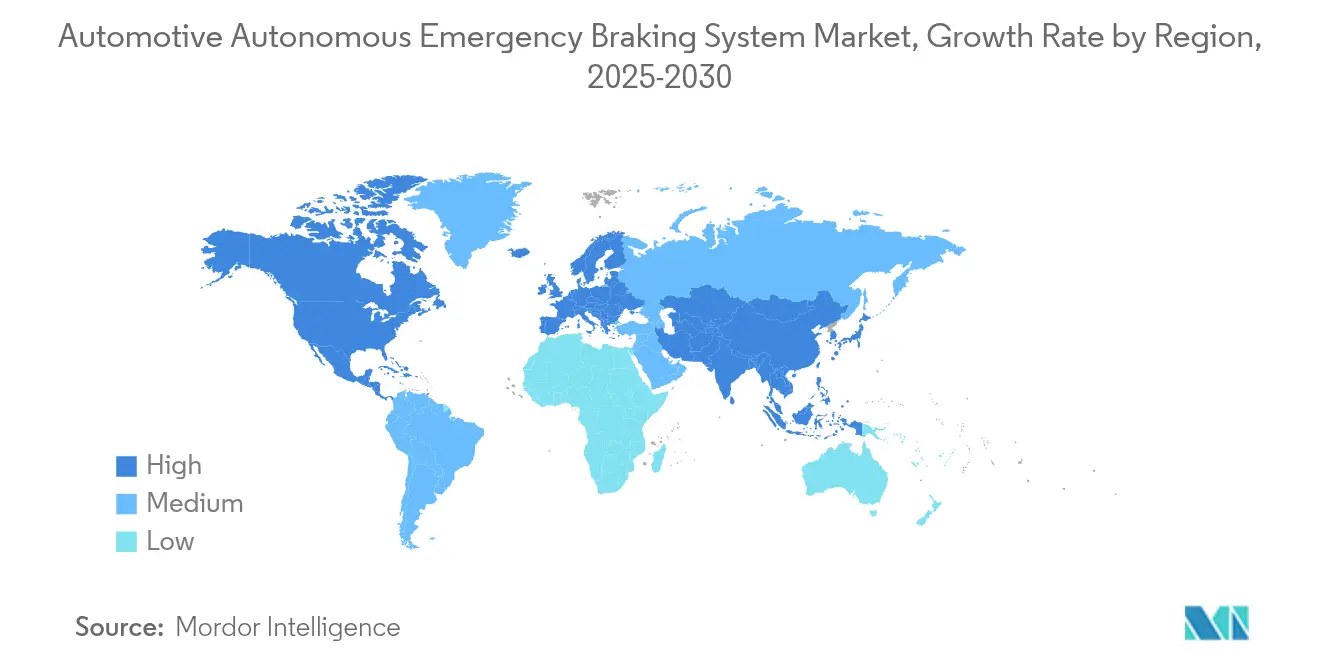

- By geography, North America led with 34.05% revenue in 2025, but Asia-Pacific is posting the fastest 12.15% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Autonomous Emergency Braking System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AEB Installation Mandates | +6.2% | Global, with US and EU leading implementation | Short term (≤ 2 years) |

| Rising Demand for NCAP 5-Star Ratings | +4.1% | Global, with Asia-Pacific cost advantages | Medium term (2-4 years) |

| Cheaper Sensors With 4D Fusion | +3.8% | Europe, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| AI Radar Enables Low-Cost High-Res Perception | +2.9% | Global, with technology leaders in US and Europe | Long term (≥ 4 years) |

| Insurance Discounts for AEB Vehicles | +2.3% | China, US, expanding globally | Short term (≤ 2 years) |

| Pedestrian AEB Rules in China & US | +1.7% | North America and Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for Mandatory AEB Installation

Government-imposed AEB requirements create non-negotiable market expansion that transcends traditional automotive adoption cycles. NHTSA's final rule mandates that AEB systems be capable of automatic braking at speeds up to 90 mph. That pedestrian detection functionality should operate effectively in darkness, with full compliance required by September 2029.[1]"Federal Motor Vehicle Safety Standards; Automatic Emergency Braking Systems for Light Vehicles", Federal Register, www.federalregister.gov.The regulation's performance-based approach, rather than technology-specific requirements, enables manufacturers to choose optimal sensor combinations while meeting stringent effectiveness thresholds. Preliminary testing reveals that only the 2023 Toyota Corolla meets these comprehensive standards, indicating substantial technology upgrades required across the industry. This regulatory framework fundamentally alters competitive dynamics by establishing minimum performance baselines that favor technologically sophisticated suppliers capable of delivering integrated sensor fusion solutions. The estimated USD 82 per vehicle implementation cost represents a minimal barrier relative to the projected USD 5.24 to USD 6.52 billion lifetime net benefits, creating compelling economic justification for accelerated adoption.

Rising Consumer Demand for NCAP 5-Star Safety Ratings

Consumer safety consciousness drives purchasing decisions beyond regulatory minimums, creating market premiums for vehicles achieving top-tier safety ratings. Euro NCAP's updated 2026 protocols introduce enhanced AEB testing scenarios, including junction collision avoidance and cyclist detection capabilities, with manufacturers requiring advanced sensor integration to achieve maximum ratings. The Insurance Institute for Highway Safety's advocacy for stringent AEB regulations reflects consumer awareness that current systems significantly underperform in darkness, creating differentiation opportunities for manufacturers deploying infrared cameras and advanced sensor fusion. This consumer-driven demand particularly influences premium vehicle segments where safety technology is a key differentiator, with manufacturers like Volvo leveraging City Safety technology to demonstrate measurable crash reduction benefits. The NCAP roadmap extending through 2033 ensures continuous technology evolution requirements, preventing market stagnation and rewarding ongoing innovation investments. Liberty Mutual's TechSafety program, offering discounts to Volvo owners with advanced safety features, demonstrates how consumer demand intersects with the insurance industry's recognition of AEB effectiveness.

Declining Radar & Camera Sensor Cost with Scalable 4D Fusion

Sensor cost reduction enables AEB democratization across vehicle price segments while enhancing system performance through advanced fusion architectures. The transition to 77GHz radar systems provides improved range resolution and detection capabilities essential for AEB functionality, with regulatory bodies intensifying requirements that push OEMs toward these advanced technologies. Texas Instruments' introduction of the AWRL6844 60GHz mmWave radar sensor with integrated edge AI capabilities demonstrates how semiconductor innovation reduces system complexity while improving detection accuracy. Magna's development of thermal-radar fusion technology extends detection range significantly while reducing false positives, positioning these solutions for mass-market adoption due to cost advantages over LiDAR systems. The emergence of 4D imaging radar with up to 2,304 virtual channels enhances autonomous vehicle perception capabilities while maintaining cost structures suitable for volume production. Automotive semiconductor market projections exceeding USD 88 billion by 2027 reflect the substantial investment in next-generation radar and processing technologies that enable sophisticated AEB implementations.

AI-Enhanced Imaging Radar Unlocking Low-Cost High-Resolution Perception

Artificial intelligence integration transforms radar sensor capabilities from basic object detection to sophisticated scene understanding that rivals LiDAR performance at significantly lower costs. Motional's imaging radar architecture processes low-level radar data using machine learning to achieve high-fidelity imagery and improved object detection, particularly in adverse weather conditions where traditional sensors struggle. Arbe Robotics' collaboration with NVIDIA demonstrates how AI-driven radar processing enables ultra-high-definition perception suitable for L2+ autonomy applications, with their technology showcased at CES 2025, highlighting real-world deployment readiness. The development of 140GHz radar technology promises even higher resolution sensing capabilities, though commercialization faces spectrum regulation challenges that vary by country and could impact global adoption timelines. Bosch's partnership with Microsoft to explore generative AI applications in automated driving functions indicates how software-defined approaches enhance radar interpretation capabilities without requiring hardware upgrades. This AI-radar convergence enables sophisticated emergency braking decisions based on predictive scene analysis rather than reactive object detection, fundamentally improving system effectiveness while maintaining cost competitiveness.

Restraints Impact Analysis*

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of LiDAR & Sensor Stacks | -2.8% | Global, particularly affecting premium vehicle segments | Medium term (2-4 years) |

| Weather & False-Positive Sensor Limits | -1.9% | Northern climates and regions with extreme weather | Long term (≥ 4 years) |

| Radar Chipset Shortages | -1.4% | Global supply chain, with Asia-Pacific manufacturing concentration | Short term (≤ 2 years) |

| mmWave Radar IP Disputes | -0.7% | US and Europe primarily, affecting technology development | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of LiDAR & Multi-Sensor Stacks for Premium AEB

LiDAR integration costs constrain widespread adoption despite superior detection capabilities, creating market segmentation between premium and volume vehicle categories. While companies like Hesai plan to reduce LiDAR prices by 50% in 2025, current costs still exceed radar-camera combinations by substantial margins, limiting deployment to higher-end vehicle segments. Oliver Wyman's analysis indicates that LiDAR provides superior accuracy for safety-critical applications like emergency braking but faces competitive pressure due to improved radar resolution and cost-effectiveness. The challenge intensifies multi-sensor fusion architectures that combine LiDAR, radar, and cameras to achieve redundancy and enhanced performance, as system complexity increases, integration costs, and validation requirements. Aeva Technologies' selection as a Tier 1 LiDAR supplier for series production vehicles demonstrates market confidence in FMCW technology. However, the transition timeline extending to mid-decade reflects the substantial engineering and cost optimization required. This cost constraint particularly affects commercial vehicle adoption, where fleet operators prioritize total cost of ownership over premium safety features, potentially delaying LiDAR-based AEB penetration in high-volume segments.

Sensor Performance Limits in Adverse Weather & False Positives

Environmental conditions expose fundamental limitations in current AEB sensor technologies, creating reliability concerns that impact consumer confidence and regulatory compliance. NHTSA's emphasis on night-time pedestrian detection capabilities highlights persistent challenges with camera-based systems in low-light conditions, while radar sensors face interference in heavy precipitation and snow.[2]"How are OEMs upgrading their Automated Emergency Braking systems to meet tougher NHTSA guidelines?", ADAS and Autonomous Vehicle International, www.autonomousvehicleinternational.com. The Insurance Institute for Highway Safety notes that while many vehicles meet daytime AEB requirements, performance drops significantly in darkness, necessitating advanced sensor combinations or infrared camera integration to maintain effectiveness. False positive activations create driver frustration and potential safety risks when systems inappropriately engage braking, leading to consumer resistance and regulatory scrutiny of system calibration. Chinese patent CN117970255A describes interference suppression methods for automotive millimeter-wave radar, indicating ongoing technical challenges in managing cross-interference between multiple radar systems. These performance limitations particularly affect system deployment in regions with challenging weather conditions, potentially creating geographic adoption disparities and requiring region-specific sensor calibration approaches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial acceleration reshapes demand curves

Passenger cars hold the largest autonomous emergency braking market share at 73.05%, benefiting from rising consumer safety expectations that align with regulation. Heavy commercial vehicles represented only 6.20% of the market share in 2025, yet are climbing at the highest CAGR of 13.65% on the back of FMCSA rules covering trucks above 10,001 lb GVW. This high-growth base positions fleets as a strategic beachhead, with retrofit kits priced from USD 1,500 achieving payback through collision-related downtime reduction and insurance rebates. Light commercial vans retain a 20.75% share as e-commerce logistics multiply delivery miles. The heavy commercial vehicles' autonomous emergency braking market size is projected to more than triple between 2026 and 2031 as fleet purchasing cycles compress around compliance deadlines.

Fleets are also influencing technology paths. ZF’s brake-by-wire program covering 5 million units demonstrates commercial platforms’ power to set scale economies that later cascade into passenger segments. Tier 1 suppliers now design modular sensor suites that clip onto tractor cabs or trailer noses, minimizing downtime and standardizing service parts. This cross-segment technology flow ensures the autonomous emergency braking industry retains a virtuous cycle of volume and innovation.

By Component Technology: Radar retains core role while LiDAR gains pace

Radar dominated the autonomous emergency braking market with a 45.75% share in 2025, prized for all-weather robustness and steadily falling cost curves. Camera-only systems cover 22.40% but struggle in lowlight, driving uptake of radar-camera fusion that occupies a 19.90% share. LiDAR, though nascent, is surging at 30.55% CAGR as vertical cavity surface-emitting lasers and FMCW architectures slash BOM and deliver sub-10 cm range accuracy. Ultrasonic units remain parked at 3.85% for low-speed maneuvers. The autonomous emergency braking market share of LiDAR-centric systems is expected to approach 15.80% by 2031, supported by global OEM order books exceeding USD 6 billion for solid-state sensors.

Convergence is increasingly likely. Hybrid modules integrate a narrow-field LiDAR for high-resolution mid-range mapping with wide-field radar to secure adverse-weather reliability, yielding cost-balanced coverage. Semiconductor roadmaps embedding radar DSP, AI accelerators, and LiDAR control on a single die promise further consolidation, amplifying competitive tension inside the autonomous emergency braking industry.

By Operating Speed Class: Junction scenarios drive next performance leap

Low-speed AEBs delivered 54.10% of 2025 revenue, having matured as a standard feature for urban driving. Interaction-rich junction environments represent only a 7.30% share today, yet bear a 27.40% CAGR, bolstered by Euro NCAP’s intersection test that forces OEMs to address multi-object trajectories and lateral impact risk. High-speed highway systems hold a 20.20% share, benefitting from NHTSA’s 90 mph stopping rule that amplifies sensor range requirements, while pedestrian-focused algorithms occupy 18.40%, buoyed by night-time test protocols. The autonomous emergency braking market size for junction systems is forecast to reach USD 10.46 billion by 2031, pulling AI software vendors into deeper collaboration with Tier 1 sensor suppliers.

Algorithm complexity rises sharply in intersections; predictive path planning and occlusion handling demand training sets that span millions of scenarios. Cloud-based synthetic data generation accelerates validation, shrinks development cycles, and sustains the autonomous emergency braking market’s technology cadence.

By Sales Channel: Retrofit momentum complements factory fitment

OEM installations controlled 91.10% of 2025 revenue as regulatory statutes lock AEB into every new‐build configuration. Though only 3.45% of sales, fleet retrofit solutions are scaling at 17.45% CAGR, propelled by insurance incentives that can lower premiums by 10% when systems meet defined performance metrics. Aftermarket consumer retrofits hold 5.45% share but grow modestly due to certification hurdles.

Tier 1s now publishes validated retrofit reference designs covering multi-brand platforms, opening a secondary revenue stream that smooths production ramp risks. Autonomous emergency braking market stakeholders increasingly view retrofit kits as a laboratory to iterate sensor firmware, which is later ported into OEM programs, reinforcing continuous improvement across the market.

Geography Analysis

North America commanded 34.05% of 2025 revenue, a position underpinned by rigorous federal safety standards and a familiar litigation landscape that encourages proactive adoption. The region’s high-average-vehicle age also underwrites robust retrofit demand as fleets accelerate compliance to capture insurance benefits. The autonomous emergency braking market size in North America is set to reach USD 35.28 billion by 2031, paralleling the staged FMVSS 127 compliance window.

Europe followed with 29.85% market share, supported by the General Safety Regulation II that synchronizes safety requirements across 27 member states and embeds AEB within a wider umbrella of Advanced Driver Assistance Systems. Euro-centric OEMs favour centralized E/E architectures that host AEB, lane-keep and adaptive cruise on a shared sensor array, improving scale effects for suppliers and boosting profitability within the autonomous emergency braking market.

Asia-Pacific posted 28.35% share in 2025 yet registers the highest 12.15% CAGR as Chinese OEMs like BYD inject AEB into budget EVs retailing below USD 15,000. Domestic chipsets and vertically integrated sensor supply chains compress cost structures, unlocking mass-volume deployments that dwarf European build counts. Australia’s mandate for AEB on all new passenger cars from February 2025 widens regulatory coverage in the region, sustaining regional momentum. The autonomous emergency braking market size in Asia-Pacific could surpass North America before 2030 if current trajectories hold.

Regulatory Landscape

Autonomous emergency braking (AEB) requirements are shifting from feature-level encouragement to enforceable, performance-based obligations across key auto markets. In the United States, NHTSA issued FMVSS No. 127 for light vehicles (GVWR 4,536 kg or less), requiring AEB and pedestrian AEB (PAEB). The compliance dates are September 1, 2029 for most manufacturers and September 1, 2030 for small-volume, final-stage manufacturers and alterers, and the rule traces back to the Bipartisan Infrastructure Law requirement to promulgate an AEB standard.

UN Regulation No. 152 establishes a harmonized framework for Advanced Emergency Braking Systems in M1 and N1 categories, including a minimum braking demand of 5.0 m/s squared upon detection of an imminent collision. In April 2026, UNECE GRVA discussed proposed amendments to UN R152 to expand scope toward bicycle impact avoidance and add special provisions for vehicles equipped with automated driving systems, indicating tighter test scenarios and additional system obligations that will feed into global platform engineering and validation strategies.

Value Chain Analysis

The AEB value chain begins with sensor and compute components (radar transceivers and antennas, camera modules, LiDAR where applied, ECUs/domain controllers, and software stacks for perception and braking decision logic). It then moves through Tier suppliers that integrate sensing, actuation, and validation, before ending with OEM integration and downstream calibration, homologation support, and service and aftermarket channels, including fleet retrofit kits. Radar remains a core subsystem in many AEB configurations, so semiconductor capacity, packaging and RF performance, plus antenna design and testing infrastructure, act as key supply-side levers.

Recent supplier actions also point to tighter vertical collaboration between chip, antenna, and system integrators to scale mandate-driven deployments and meet performance thresholds. In October 2024, Gapwaves signed a multi-year development and supply agreement with Valeo for waveguide radar antennas, with serial production scheduled to start in 2025, supporting antenna availability for volume radar programs. In March 2025, indie Semiconductor and GlobalFoundries announced a collaboration to develop high-performance radar SoCs on the 22FDX platform targeting 77 GHz and 120 GHz automotive radar applications, reflecting how foundry partnerships are used to de-risk radar SoC supply and improve performance-per-watt for multi-sensor AEB suites.

Competitive Landscape

Four global Tier 1 suppliers Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG and Denso Corporation collectively supply integrated radar, camera and braking controllers to a majority of 2025 vehicle programs, anchoring mid-market concentration. Bosch secured multi-year contracts to deliver imaging radar modules for European compact cars launching in 2027, while Continental’s Aumovio spin-off targets cost-optimized sensor stacks for Chinese joint ventures. ZF funnels brake-by-wire know-how from heavy trucks into passenger platforms, capturing long-term platform awards.

Technology specialists such as Mobileye tilt the landscape. Its SuperVision perception suite, already booked into 233 future vehicle programs, bundles 360-degree cameras with domain controllers, reducing OEM software overhead. Semiconductor innovators like Texas Instruments and NXP deliver radar SOCs with embedded neural-net accelerators, lowering latency and power consumption. Patent disputes remain intense; Magna and Panasonic concluded a cross-license on mm Wave radar in 2024 that averts supply disruptions but signals growing IP protectionism.

Start-ups target white space. For instance, Arbe Robotics commercializes 4D imaging radar ICs, Bit Sensing focuses on short-range high-resolution sensors for blind-spot mitigation, and Hesai sells low-cost hybrid solid-state LiDAR. Collectively, these entrants push incumbent Tier 1s toward software-defined value propositions, ensuring the autonomous emergency braking market sustains competitive dynamism.

Automotive Autonomous Emergency Braking System Industry Leaders

-

Robert Bosch GmbH

-

Continental AG

-

ZF Friendrichafen AG

-

Aisin Corporation

-

Hyundai Mobis Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Mandate-driven performance tightening is creating opportunity beyond baseline forward AEB, particularly in architectures and scenarios that improve night and cross-traffic outcomes while reducing false positives. In the US, FMVSS No. 127 provides a defined compliance horizon (2029-2030) that pushes OEMs and Tier suppliers to standardize AEB and PAEB capability across light-vehicle lines. UN Regulation No. 152 also continues to evolve at WP.29, including the April 2026 discussions to add bicycle impact avoidance provisions. Together, these changes support demand for higher-resolution radar, radar-camera fusion, and validation toolchains that can cover an expanding set of test cases.

Commercial-vehicle platforms and safety-suite packaging are expanding the addressable content per vehicle for AEB-related functions. In April 2026, Daimler Truck North America announced new Detroit Assurance Suite capabilities under Active Brake Assist 6, adding functions such as Cross Traffic Assist and Active Side Guard Assist 2, illustrating how braking integration is being bundled into heavy-duty safety features. Separately, data governance is becoming part of productization for assisted-driving and AEB stacks; China MIIT actions cited for July 2026 emphasize requirements including logging takeover and disengagement events and retaining data, for example 90-day retention. That drives demand for compliant software architectures, in-vehicle data handling, and driver-monitoring integration alongside core AEB sensing and braking performance.

Recent Industry Developments

- April 2026: Robert Bosch GmbH confirmed public road testing for its advanced intelligent driving solution in Yokohama, Japan, following earlier Level 3 testing activity in China. The validation work extends Bosch into another major market and supports broader tuning of perception and emergency intervention functions in dense urban environments.

- March 2026: ZF Commercial Vehicle Control Systems India (ZF Friedrichshafen AG) secured a business nomination from an Indian commercial vehicle OEM to supply its OnGuardMAX platform for bus applications, including AEB among the safety functions, with SOP targeted for Q1 2027. The nomination strengthens ZF positioning in higher-content commercial ADAS stacks and ties AEB demand to platform-level awards ahead of upcoming safety compliance cycles.

- June 2024: Bitsensing raised USD 25 million to advance high-resolution radar technology for autonomous driving use cases. Additional funding for radar R&D supports imaging-capability improvements that AEB programs can use to extend detection robustness in poor weather and complex scenes while holding cost targets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from autonomous emergency braking systems used in vehicles, where sensors detect an obstacle and the braking action is applied automatically to reduce or avoid a crash.

Scope exclusions: We exclude broader ADAS features that do not trigger automatic braking as a core function (for example, warning-only safety features).

Segmentation Overview

-

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

-

By Component Technology

- Radar-based AEB

- Camera-based AEB

- LiDAR-based AEB

- Sensor-Fusion AEB (Radar + Camera)

- Ultrasonic-based AEB

-

By Operating Speed Class

- Low-Speed AEB (Less Than 40 Kmph)

- High-Speed AEB (More Than 40 Kmph)

- Pedestrian AEB

- Junction or Intersection AEB

-

By Sales Channel

- OEM-Installed

- Aftermarket Retrofit

- Fleet Retrofit Service

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

To set the groundwork, we map the AEB demand pool through vehicle production, sales, and parc signals, then connect those volumes to safety regulation timelines and fitment trends. Public sources we typically reference include National Highway Traffic Safety Administration updates, Euro NCAP documentation, UNECE vehicle safety regulations, OICA production statistics, and road safety datasets published by the WHO.

After that, desk work is used to shape pricing and technology assumptions, including sensor mix shifts (camera, radar, LiDAR) and AEB capability ranges (low-speed, high-speed, and pedestrian-oriented functions). We also review company filings, investor presentations, association releases, and reputable press for launch timing and standard-fit announcements, then cross-check select data points with paid subscriptions for company financials, patent activity, and shipment-level trade signals where available. These desk research sources are illustrative only, and many additional public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what is actually being installed and billed, not only what is technically possible. We speak with OEM-facing stakeholders, component and subsystem participants, and channel-side experts across APAC, EMEA, and the Americas, so gaps from desk findings can be narrowed and key assumptions can be stress-tested before the model is finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 40% |

| Mid tier: 51% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 14% | Managers: 55% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where vehicle production and sales by region are translated into an installable base, then filtered by AEB penetration and the mix of speed classes that are commonly mandated or offered. To keep totals realistic, we corroborate the results using selective bottom-up approximations, such as sampled system pricing multiplied by fitted volumes, and a cross-check against supplier revenue exposure. Where the two views do not align, we adjust the assumptions and rerun the bridge.

Key inputs for this market include new vehicle production by vehicle class, the share of models offering AEB as standard versus optional, the shift toward camera-radar fusion, the take rate of pedestrian-focused functions, and average system value progression as hardware content changes. For forecasting, scenario analysis is used to represent regulatory step-ups, OEM standard-fit roadmaps, and expected cost-down curves. Scenario weights are reviewed with primary experts so the growth path does not depend on a single assumption. When direct price points are hard to confirm, gaps are handled with bounded ranges and then tightened using interview feedback and observed pricing direction in comparable safety systems.

Data Validation & Update Cycle

Before sign-off, the model is validated through multiple checks, including variance testing across regions, year-on-year adoption sanity checks, and comparisons against independent signals such as vehicle safety mandate timing and announced standard-fit programs. If a number moves outside a reasonable band, the assumptions are reopened, and targeted follow-ups are conducted with respondents to confirm what changed and why.

Reports are refreshed annually, and interim updates are made when material events occur, such as a regulation shift or a sharp technology pricing reset. Right before delivery, a final pass is completed so the published results reflect the latest information available at that point in time.

Mordor Intelligence's Automotive Autonomous Emergency Braking System Market Sizing Compared With Other Published Estimates

It is common to see different published market sizes for AEB systems because the boundaries can shift in small but meaningful ways, and those shifts change the total. Differences usually come from the year used for currency conversion, how fast average system prices are assumed to decline, and whether the analysis links adoption to vehicle output and regulatory timing, or uses broad growth multipliers.

In this study, frequent refresh checks are applied to pricing and mix assumptions, and currency timing is kept consistent to avoid inflating results during volatile exchange-rate periods, which helps keep Mordor Intelligence aligned to what OEM fitment and sensor-content signals indicate for 2026.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 43.67 B (2026) | |

| Industry Publisher A | USD 53.98 B (2026) | Often uses a broader AEB definition that can lean on higher assumed system values and a wider inclusion of function variants, and it may apply a different base-year currency timing when converting regional revenues into USD. |

| Global Publisher B | USD 26.53 B (2024) | Uses factory-gate valuation and a component-heavy scope that can understate installed system revenue when compared to end-system pricing, and the earlier base year can miss recent standard-fit adoption and ASP resets seen in newer vehicle platforms. |

The spread across these numbers is mainly explained by scope boundaries and timing choices, not by disagreement that AEB adoption is rising. By anchoring demand to vehicle volumes and then updating ASP and mix inputs in step with observed fitment shifts, the final estimate stays traceable to clear variables that can be rechecked and repeated.

Key Questions Answered in the Report

What is the projected value of the autonomous emergency braking market by 2031?

It is expected to reach USD 103.66 billion by 2031, up from USD 43.67 billion in 2026.

Which vehicle segment is growing fastest for AEB adoption?

Heavy commercial vehicles are expanding at a 13.65% CAGR as forthcoming US trucking regulations accelerate fleet retrofits.

Which region shows the highest growth rate?

Asia-Pacific posts the strongest 12.15% CAGR, led by Chinese EV makers integrating low-cost sensor fusion.

What technological trend most enhances AEB performance in poor weather?

AI-enabled imaging radar converts raw radar data into high-resolution scenes, maintaining detection accuracy in rain, fog and darkness.

Page last updated on: