Automotive Ignition System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

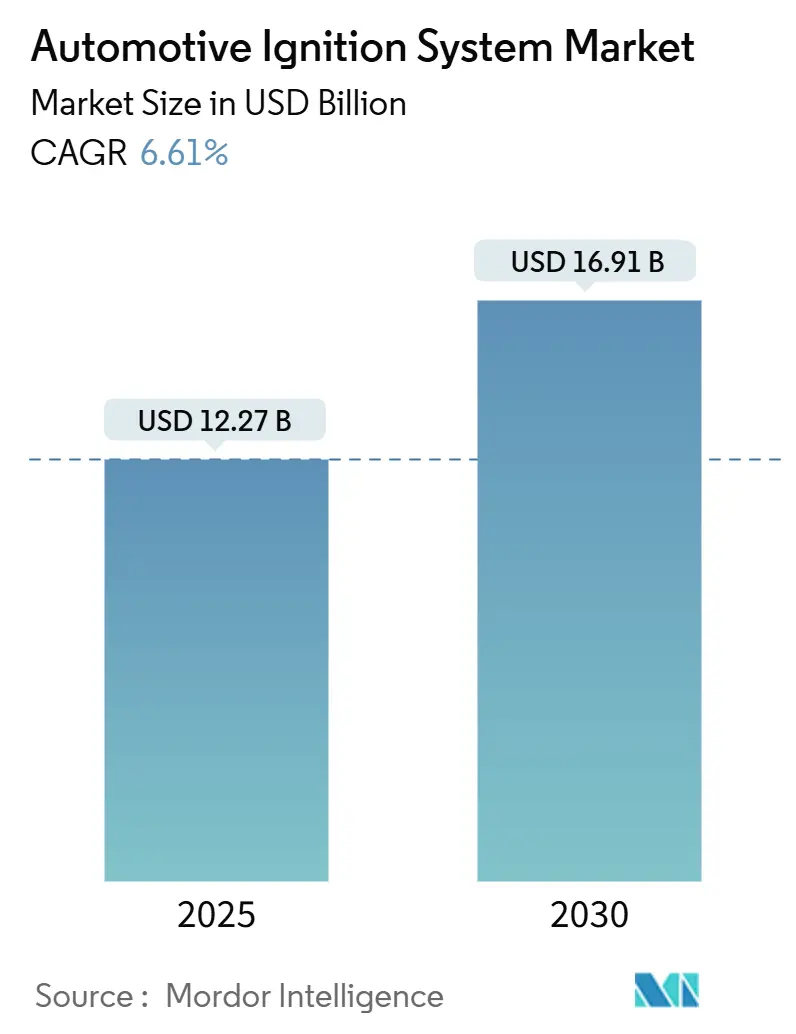

| Market Size (2025) | USD 12.27 Billion |

| Market Size (2030) | USD 16.91 Billion |

| Growth Rate (2025 - 2030) | 6.61% CAGR |

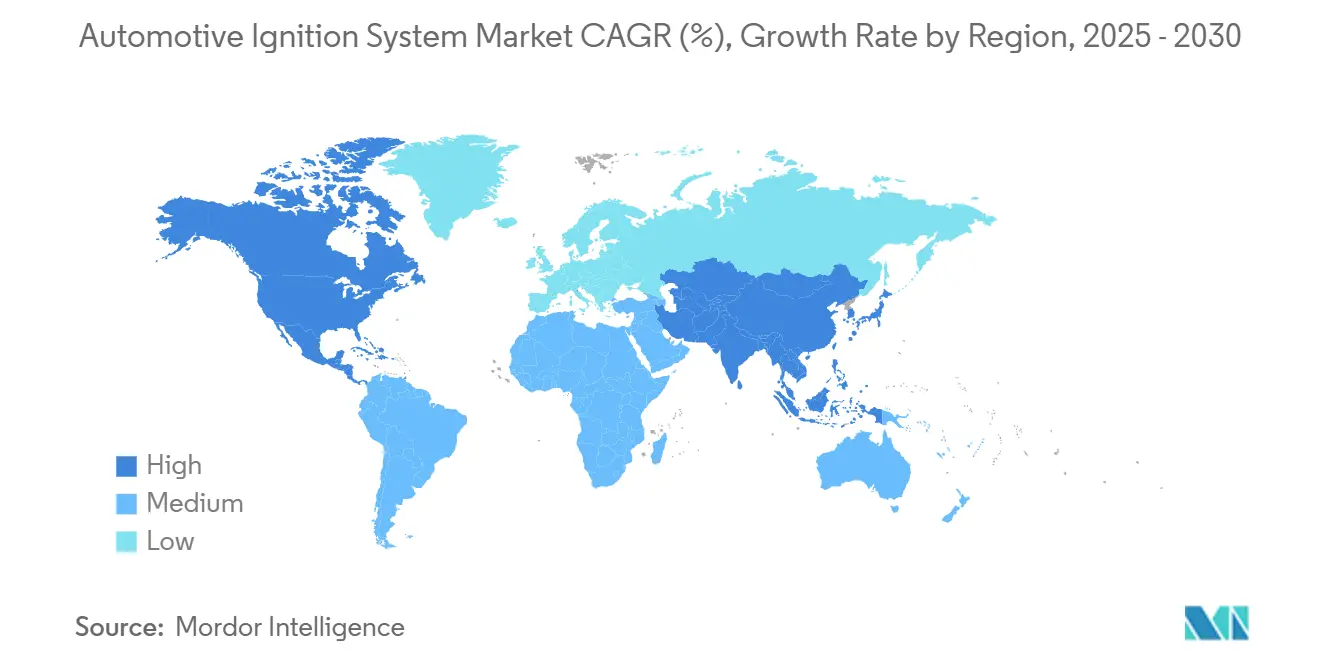

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Ignition System Market Analysis by Mordor Intelligence

The Automotive Ignition System Market size is estimated at USD 12.27 billion in 2025, and is expected to reach USD 16.91 billion by 2030, at a CAGR of 6.61% during the forecast period (2025-2030). Market expansion is sustained by stricter global emission norms that compel high-efficiency ignition upgrades, rising penetration of direct-injection and turbocharged powertrains that require higher-energy sparks, and a steady internal-combustion presence in commercial fleets despite the electric transition. Asia-Pacific holds leadership owing to scale advantages in China and India, while North America is registering the fastest growth on the back of replacement demand and commercial-vehicle investments. Component innovation, particularly in iridium spark plugs and coil-on-plug (COP) architectures, remains decisive as OEMs push efficiency gains during the ICE-to-EV bridge period. Competitive intensity is moderate; established suppliers leverage scale and R&D depth while pivoting toward plasma ignition and AI-enabled timing optimization for hydrogen and ammonia engines to secure long-term relevance in the automotive ignition system market.

Key Report Takeaways

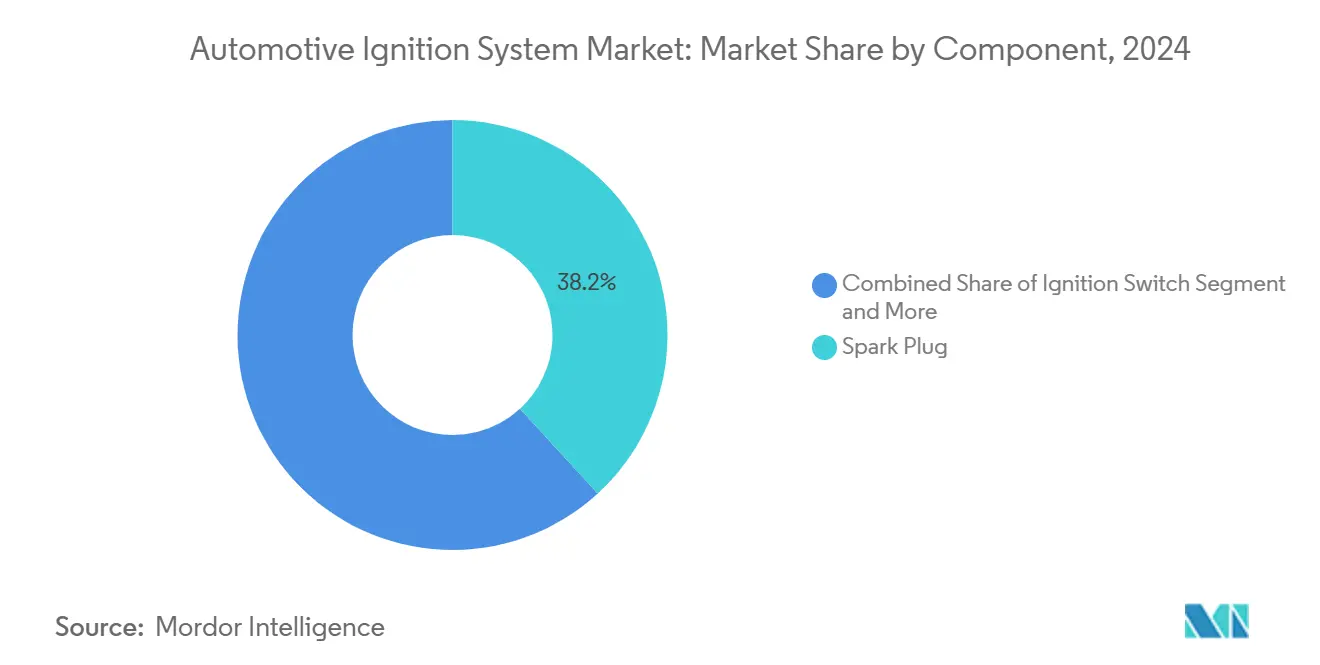

- By component, spark plugs led with 38.17% of the automotive ignition system market share in 2024, while ignition coils are projected to grow at a 6.63% CAGR through 2030.

- By ignition type, coil-on-plug systems accounted for 47.61% of the automotive ignition system market share in 2024 and are advancing at a 6.74% CAGR to 2030.

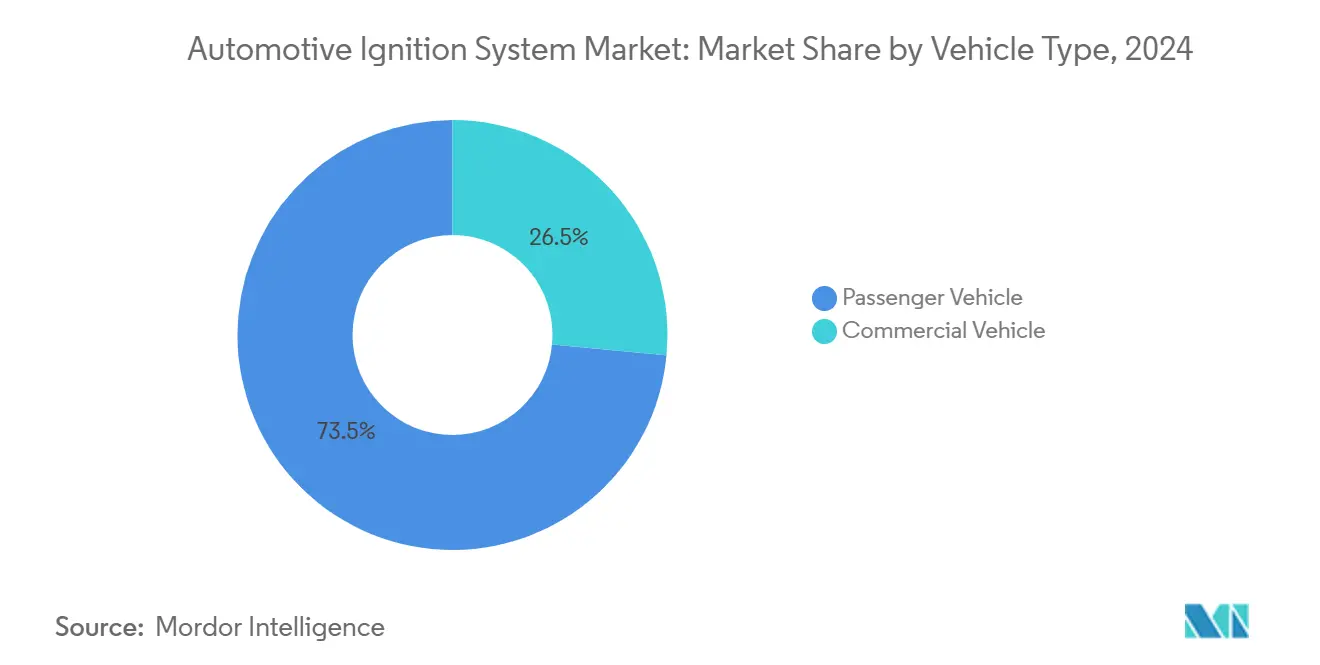

- By vehicle type, passenger vehicles held 73.47% of the automotive ignition system market in 2024; commercial vehicles record the highest forecast CAGR at 6.67% during 2025-2030.

- By sales channel, OEM channels contributed 61.22% of the automotive ignition system market share in 2024, whereas the aftermarket is expanding at a 6.68% CAGR through 2030.

- By region, Asia-Pacific captured 38.48% of the automotive ignition system market share in 2024; North America is the fastest-growing geography at a 6.71% CAGR through 2030.

Global Automotive Ignition System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Emission Norms | +1.8% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| Global Vehicle Production Growth | +1.5% | Asia Pacific core, spill-over to other regions | Short term (≤ 2 years) |

| Rise Of DI/Turbo Engines | +1.2% | Global, concentrated in premium segments | Medium term (2-4 years) |

| Expanding Vehicle PARC & Longer Ownership | +0.9% | North America and Europe primarily | Long term (≥ 4 years) |

| AI-Enabled Real-Time Spark-Timing Optimisation | +0.7% | Advanced markets with hybrid penetration | Long term (≥ 4 years) |

| Early Investments In Plasma Ignition | +0.5% | Japan, Germany, select pilot markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Emission Norms Mandating High-Efficiency Ignition Upgrades

Euro 7 regulations scheduled for 2027 create immediate pull-through for iridium-electrode spark plugs and precision coil-on-plug modules capable of constant NOx feedback correction, as demonstrated by NGK Insulators’ new sensor technology. Automakers standardize premium ignition parts once reserved for high-performance trims to meet particulate limits without expensive engine redesigns. Similar frameworks in China, the United States, and India synchronize a global upgrade cycle that cushions the automotive ignition system market against near-term EV volume losses. Suppliers investing in high-entropy alloys and advanced ceramics gain margin advantages as OEMs pay for durability and thermal stability. Regulatory certainty through 2030 underpins predictable demand curves that help ignition suppliers maintain capacity utilization even as powertrain portfolios diversify.

Global Vehicle Production Growth, Especially in Asia-Pacific

Rising assembly footprints in China, India, and ASEAN markets drive volume for complete ignition modules, harnesses, and sensors. Suzuki’s Kadkhoda plant and Honda’s fourth motorcycle facility in India exemplify capacity additions that amplify local tier-1 procurement [1]“Kharkhoda Plant Commences Operations,” Suzuki Motor Corporation, global. Suzuki . Production clustering allows shared logistics and shortens lead times for multi-spark coils delivered just-in-sequence, supporting lean OEM inventories. Export-oriented ASEAN sites maintain conventional ICE lines for African and Latin American demand, extending product life cycles for spark-plug and coil families. The scale effect lowers per-unit costs, enabling price-sensitive buyers to adopt higher-energy systems, thereby widening the addressable base of the automotive ignition system market.

Rise of DI/Turbo Engines Demanding Higher-Energy Sparks

Direct injection and forced-induction platforms run higher cylinder pressures and leaner mixtures, increasing voltage demand at the plug gap. Coil-near-plug and pencil-coil designs eliminate wire losses, allowing engineers to fire multiple sparks per cycle for complete combustion under transient loads. Toyota’s engineering data shows that per-cylinder coil control trims fuel minimal in homologation cycles, a savings OEMs favor over mechanical efficiency tweaks. Heavy-duty OEMs such as Cummins embed advanced engine control modules that modulate spark energy by cylinder temperature, illustrating cross-segment technology transfer. Vendors able to supply coils rated beyond 40 kV and spark plugs with laser-welded iridium tips secure specification wins in the automotive ignition system market.

Expanding Vehicle Parc & Longer Ownership Boosting Replacements

Average vehicle age in the United States surpassed more than a decade in 2024, swelling the service parts opportunity. Each additional year of ownership adds a cyclical sparkplug change for gasoline engines, doubling replacement occasions over a vehicle's lifetime. Standard Motor Products and PerTronix capitalize on this trend with extensive catalog coverage and electronic conversion kits that modernize legacy distributors. Fleet managers adopt predictive maintenance analytics to schedule coil replacements ahead of failure, elevating unit mix toward premium SKUs. This durable aftermarket backbone generates recurring revenue, anchoring the automotive ignition system market during OEM demand swings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated EV Shift | -2.1% | Global, led by China and Europe | Medium term (2-4 years) |

| Volatile Precious-Metal Prices | -0.8% | Global supply chain impact | Short term (≤ 2 years) |

| Counterfeit Aftermarket Parts | -0.6% | Asia Pacific core, with spillover to emerging markets | Medium term (2-4 years) |

| Cyber-Secured OTA Ignition Firmware | -0.4% | Advanced markets with connected vehicle penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated EV Shift Eroding ICE-Ignition Demand

Battery-electric share is rising fastest in Europe and China, with commercial-vehicle pilots such as Daimler’s eActros 600 proving viability for heavy haul. Each fully electric unit removes an ignition system sale, pressuring volume forecasts. Regional disparities, however, moderate the hit: infrastructure gaps keep diesel and gasoline trucks prevalent in long-distance U.S. freight and emerging Asian economies. Suppliers hedge by investing in thermal-management electronics and onboard chargers, yet must downsize capacity for conventional coils over the decade. The net effect trims but does not nullify the automotive ignition system market trajectory through 2030.

Volatile Precious-Metal Prices (Platinum, Iridium)

Iridium spot prices spiked by one-third in 2024 on mining disruptions, inflating the cost of input for premium spark electrodes. Tier-1s locked into annual OEM contracts absorb margin hits or renegotiate surcharges, causing pricing friction. Aftermarket vendors face substitution pressures from budget copper plugs, risking cannibalization unless they differentiate on lifespan. Some suppliers explore ruthenium-alloy tips and nano-structured coatings to reduce noble-metal load, but qualification cycles stretch 24 months. Material turbulence thus dents near-term profitability yet accelerates innovation toward metal-efficient designs within the automotive ignition system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Spark Plugs Maintain Scale as Coils Accelerate

Spark plugs accounted for 38.17% of the automotive ignition system market in 2024, a position reinforced by universal fitment across gasoline engines and predictable replacement cycles. The segment’s volume dominance underpins economies of scale for iridium- and ruthenium-tipped designs that prolong service life past more than a lakh miles, appealing to OEMs and fleet operators. In contrast, ignition coils deliver the sharpest growth trajectory at a 6.63% CAGR through 2030 as OEMs migrate to coil-on-plug architectures. High-energy coils tailored to direct-injection and turbo platforms command price premiums that lift revenue faster than unit shipments, making coils a profit engine inside the automotive ignition system market size for suppliers with vertical integration.

Manufacturers are retooling plants with bright pressure-supply lines and automated laser welding to meet tight tolerances on epoxy encapsulation and winding layouts. Bosch Rexroth’s digital-twin production cells illustrate this shift, improving first-pass yield and shortening time-to-market for revised coil geometries. Distributors and mechanical advance units continue to shrink due to electronic ignition retrofit kits, while glow plugs sustain a niche in light-duty diesel. Suppliers balance inventory by phasing down low-margin legacy SKUs and reallocating capital toward advanced coils, ensuring alignment with the evolving automotive ignition system market.

By Ignition Type: Coil-On-Plug Captures the Spotlight

Coil-on-plug solutions commanded 47.61% of the automotive ignition system market in 2024 and are forecast at a 6.74% CAGR, reshaping the market hierarchy. They eliminate high-tension leads, cut electromagnetic interference, and allow per-cylinder adaptive timing, all essential for stringent emission cycles. Simultaneous ignition remains in naturally aspirated small engines where cost is paramount, but its relevance wanes as direct injection proliferates. Compression ignition architectures cater to diesel powertrains and stand apart; new hydrogen ICE prototypes adopt spark-assisted compression to achieve stable burn, pointing to future hybridization of spark and compression paradigms. Suppliers able to package multi-turn high-voltage windings in compact housing without thermal soak issues gain spec advantage as engine bays become crowded.

The automotive ignition system market size for simultaneous ignition is flat, whereas coil-on-plug sees double-digit volume gains in China’s entry-SUV category and Europe’s mild-hybrid compacts. In the long term, plasma ignition and microwave-assisted spark technologies may leapfrog traditional coils, yet commercialization depends on cost-down curves and standardization efforts in Japan and Germany.

By Vehicle Type: Commercial Vehicles Anchor the Upside

Given their sheer production volume, passenger cars delivered 73.47% of the automotive ignition system market revenue in 2024. However, their growth decelerates as battery-electric adoption accelerates in urban mobility. Commercial vehicles—medium and heavy trucks, light commercial vans, and two- and three-wheel delivery fleets log a 6.67% CAGR through 2030 as e-commerce and last-mile demand stretch logistics capacity. Heavy-duty spark-ignited natural-gas trucks in North America and emerging hydrogen-ICE drivelines in Europe require robust coil packs and long-life iridium plugs rated for higher combustion pressures. Delco Remy’s 39MT starter system upgrades highlight this fleet segment's complementary nature of starting and ignition components.

Service intervals in commercial applications often follow hour-meter triggers rather than mileage, generating predictable aftermarket cycles that stabilize the automotive ignition system market size across economic swings. Passenger-car ignition designs focus on compactness and energy efficiency. At the same time, commercial applications emphasize durability, cold-start resilience, and ease of field replacement, leading suppliers to maintain segmented portfolios rather than one-size solutions.

By Sales Channel: Aftermarket Gains Momentum

OEM installations held 61.22% of the automotive ignition system market in 2024 as ignition systems are integrated at the engine-assembly stage, yet the aftermarket outpaces factory fit at a 6.68% CAGR. Extended ownership drives sparkplug and coil replacements, and rising DIY culture amplifies e-commerce turnover for trusted brands. BorgWarner’s BERU line leverages OEM heritage to combat counterfeit proliferation, offering QR-code authentication and extended warranties that encourage brand loyalty. Performance-oriented retrofits—electronic distributor-less kits, multi-spark controllers—expand the replacement basket beyond like-for-like parts.

Distributors cultivate omnichannel models: e-tailers handle long-tail SKUs, while brick-and-mortar stores serve installer networks needing immediate availability. Suppliers invest in real-time inventory APIs and small-parcel logistics to cut delivery windows. These service innovations keep the automotive ignition system market vibrant even as new-car output fluctuates.

Geography Analysis

Asia-Pacific captured 38.48% of the automotive ignition system market in 2024 by virtue of China’s regained production momentum and India’s aggressive capacity build-out that will crest 4 million annual units by decade-end. Regional manufacturers leverage abundant skilled labor and government incentives to localize coil and plug production, lowering export tariff exposure. Hybrid assembly in Thailand and Indonesia further enlarges demand because gasoline engines remain critical range extenders, each needing COP systems optimized for stop-start cycles. Diverse regulatory timelines—from China 6b to India’s Bharat Stage VII—drive tiered product offerings, enabling suppliers to upsell premium plugs in early-adoption locales while scaling copper core designs elsewhere inside the automotive ignition system market.

North America is the fastest-growing region at a 6.71% CAGR thanks to its vast and aging vehicle parc and large commercial-vehicle fleet. EPA-2027 emission standards push fleet operators to adopt high-energy ignition upgrades that ensure complete combustion of leaner mixtures, extending catalyst life. Simultaneously, tariffs on Chinese EVs prolong the sales window for domestic ICE pickups and SUVs, bolstering OEM coil demand. Mexico’s rising role as a near-shoring hub lowers lead times for U.S. distribution centers, enhancing responsiveness in the automotive ignition system market.

Europe remains technologically influential despite volume headwinds from accelerated electrification policies. The Euro 7 rules act as a short-term catalyst by mandating real-time NOx and particulate compliance, boosting uptake of advanced sensors and plasma-assisted sparks. The region’s entrenched supply chain, including Standard Motor Products’ Polish coil operation, services local and export programs. South America and the Middle East & Africa trail in volume but present upside through industrial fleet growth and used-vehicle imports, which intensify aftermarket replacement cycles. Suppliers targeting these regions prioritize robust sparkplug designs capable of low fuel quality and high dust environments, preserving reliability and reputation in the global automotive ignition system market.

Competitive Landscape

Market structure is moderately concentrated, with Bosch, Denso, and NGK (now Niterra) benefiting from decades of OEM integration, process know-how, and patent portfolios covering fine-wire electrodes and multi-spark circuitry. Mid-tier players—Standard Motor Products, BorgWarner’s BERU, and Delphi Technologies—counterbalance scale with broad catalog coverage and agile regional manufacturing. Competitive advantage increasingly hinges on dual ability: maintaining cost-competitive volumes for legacy ICE programs while incubating next-generation plasma, microwave, and AI-tuned ignition modules for hydrogen and ammonia engines. DENSO’s exploration of a semiconductor partnership with ROHM underlines the strategic necessity of in-house power-device competence as ignition modules migrate toward silicon-carbide drivers and real-time analytics [2]“Strategic Partnership Consideration with ROHM,” DENSO Corporation, denso.com .

Patent activity remains vibrant; multiple filings since 2020 center on coil heat-resistant plastics, electrode nano-coatings, and adaptive dwell algorithms. Early-stage entrants focus on compact plasma ignition for lean-burn aviation engines, signaling cross-industry technology spillovers that could reshape competitive rankings.

Nevertheless, core revenue still derives from high-volume spark plugs and coils, anchoring cash flows that fund R&D. Supply-chain resiliency—proximity to copper winding, ferrite core, and noble-metal refining capacity—emerges as a differentiator amid geopolitical disruptions. Accordingly, alliances with miners and advanced materials firms become commonplace in the automotive ignition system market.

Automotive Ignition System Industry Leaders

Robert Bosch GmbH

Denso Corporation

NGK Spark Plug

BorgWarner Inc.

Delphi Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Maruti Suzuki commenced operations at the Kharkhoda plant in India with a 250,000-unit initial output, targeting 4 million national capacity, and elevating local ignition component sourcing.

- September 2024: DENSO and ROHM began exploring a strategic semiconductor partnership for automotive power devices for ignition and engine-management electronics.

Global Automotive Ignition System Market Report Scope

| Ignition Switch |

| Spark Plug |

| Glow Plug |

| Ignition Coil |

| Others |

| Coil-on-Plug Ignition |

| Simultaneous Ignition |

| Compression Ignition |

| Passenger Vehicle |

| Commercial Vehicle |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Component | Ignition Switch | |

| Spark Plug | ||

| Glow Plug | ||

| Ignition Coil | ||

| Others | ||

| By Ignition Type | Coil-on-Plug Ignition | |

| Simultaneous Ignition | ||

| Compression Ignition | ||

| By Vehicle Type | Passenger Vehicle | |

| Commercial Vehicle | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the automotive ignition system market in 2025?

The market is valued at USD 12.27 billion in 2025 and is projected to reach USD 16.91 billion by 2030 at a 6.61% CAGR.

Which component category dominates revenues?

Due to universal fitment and predictable replacement cycles, Spark plugs lead with 38.17% revenue share in 2024.

What region is growing the fastest?

North America posts the highest CAGR at 6.71% through 2030, propelled by fleet replacements and stringent EPA 2027 rules.

Why are coil-on-plug systems gaining popularity?

COP designs eliminate spark-wire losses, enable per-cylinder timing control, and meet the higher voltage demands of turbocharged and direct-injection engines.

How does electrification impact demand?

Battery-electric growth reduces future ICE volumes, but uneven regional adoption and commercial-vehicle reliance keep ignition demand resilient through at least 2030.

Page last updated on: