Automotive Solenoid Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.61 Billion |

| Market Size (2030) | USD 7.78 Billion |

| Growth Rate (2025 - 2030) | 6.74% CAGR |

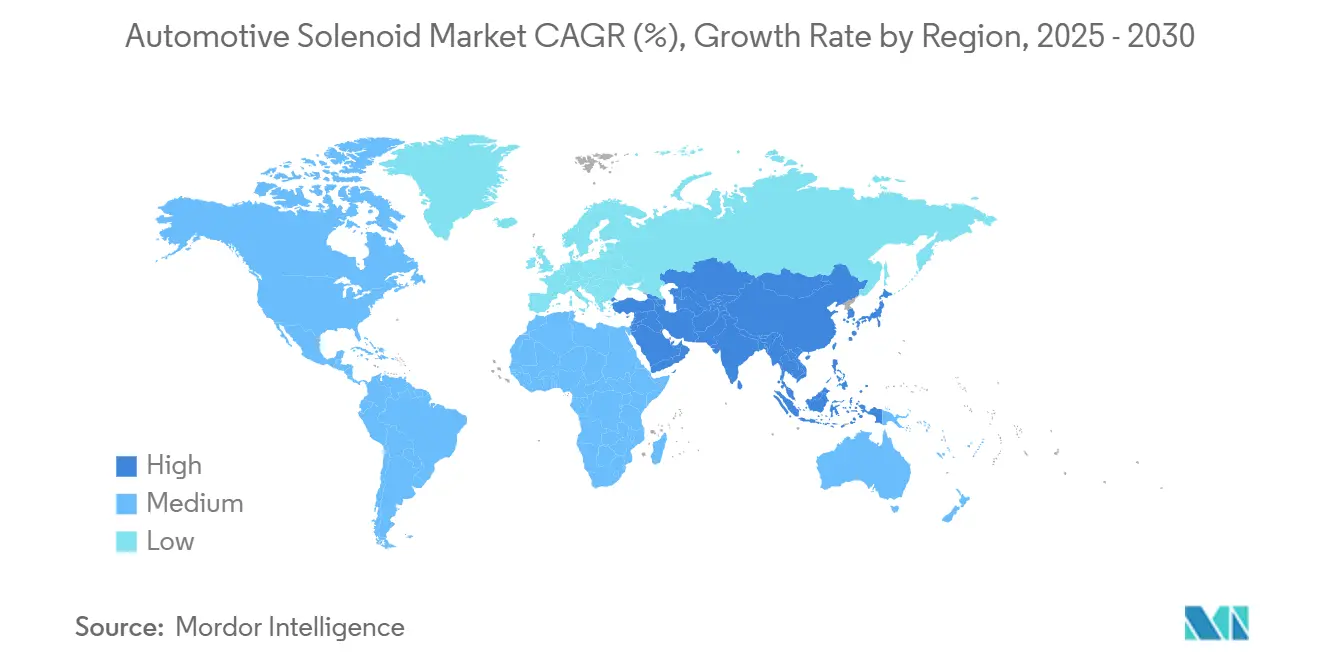

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Solenoid Market Analysis by Mordor Intelligence

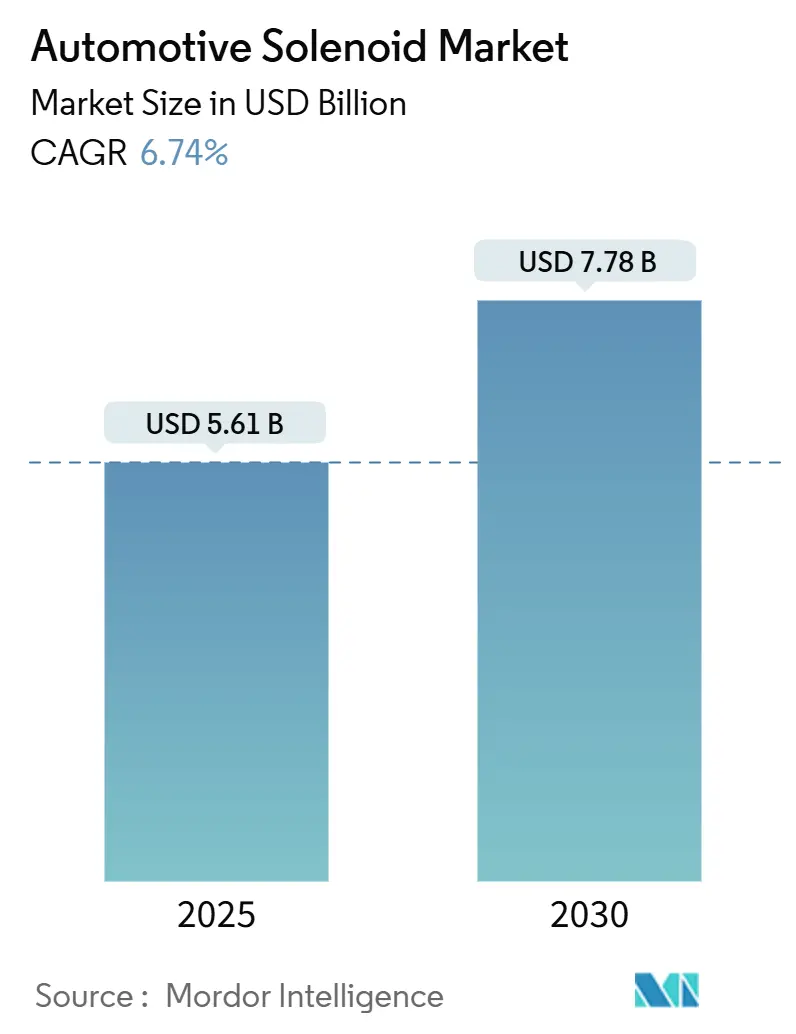

The automotive solenoid market size stands at USD 5.61 billion in 2025 and is projected to reach USD 7.78 billion by 2030, reflecting a 6.74% CAGR. Strong demand follows the rapid electrification of powertrains, the migration toward eight-speed and higher automatic transmissions, and the rollout of Euro 7 emission limits that tighten particulate thresholds. Greater use of 8–12 valve hydraulic blocks in AT, CVT, and DCT gearboxes, combined with the shift from belt-driven accessories to distributed electro-hydraulic circuits in battery-electric vehicles, increases the average valve content per vehicle. OEM efforts to lower CO₂ emissions accelerate adoption of variable valve timing (VVT) and high-pressure gasoline direct injection (GDI), each reliant on fast-switching solenoids for precise fluid metering.

Key Report Takeaways

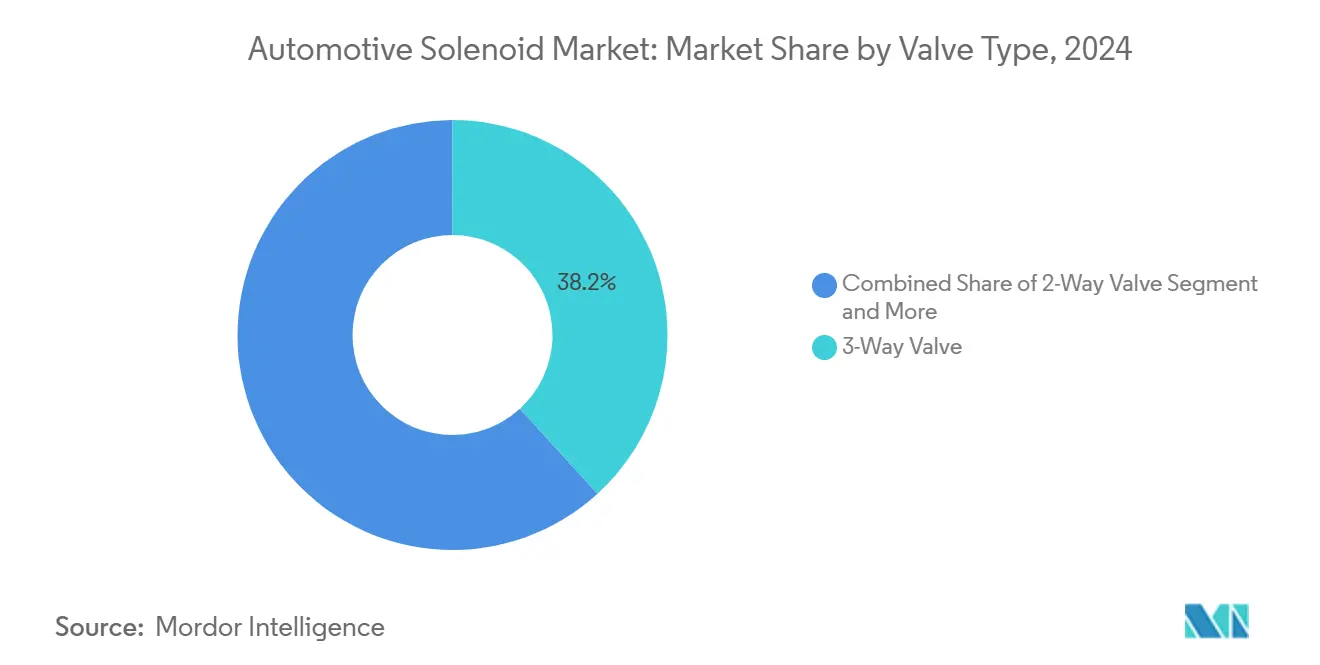

- By valve type, 3-way units led with 38.22% of the automotive solenoid market share in 2024, while 5-way configurations are projected to advance at an 8.61% CAGR through 2030.

- By application, Body Control and Interiors accounted for 29.11% of the automotive solenoid market share in 2024, whereas Safety and Security is forecast to post the highest growth at an 8.23% CAGR to 2030.

- By operation mode, Direct-Acting designs dominated, with a 63.29% of the automotive solenoid market share in 2024; Pilot-Operated systems are poised for an 8.35% CAGR over the same period.

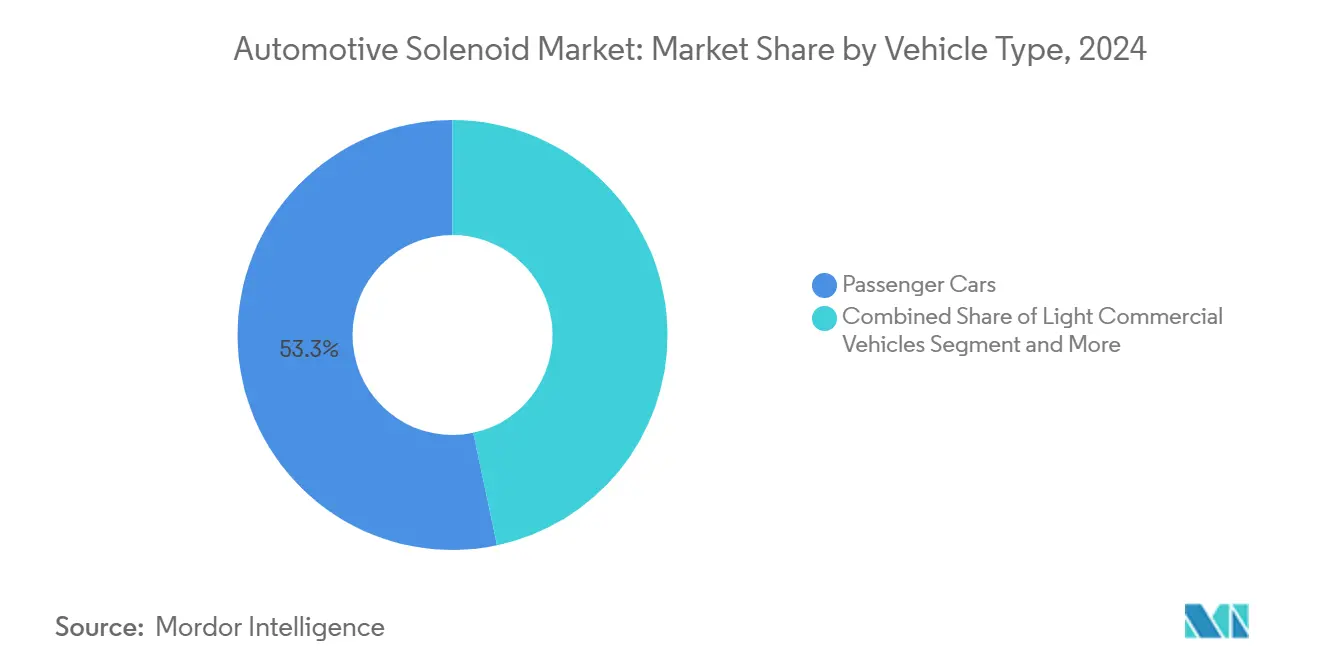

- By vehicle type, Passenger Cars captured 53.31% of the automotive solenoid market share in 2024 demand and are expected to grow at a 9.42% CAGR through 2030.

- By sales channel, OEM distribution commanded a 73.21% of the automotive solenoid market share in 2024, and this channel is set to expand at a 9.28% CAGR to 2030.

- By geography, Asia-Pacific held 48.62% of the automotive solenoid market share in 2024 and is anticipated to register an 8.35% CAGR during the forecast window.

Global Automotive Solenoid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AT/CVT/DCT Gearbox Penetration Rising | +1.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| Emission Norms Drive VVT and GDI Adoption | +1.5% | Europe, North America, expanding Asia-Pacific | Long term (≥ 4 years) |

| Vehicle Output Accelerating in China and India | +1.2% | Asia-Pacific | Short term (≤ 2 years) |

| Low-Leakage Solenoids Boost EV Efficiency | +0.9% | China, Europe, California | Medium term (2-4 years) |

| Smart Actuator Growth in Cabin Comfort and NVH | +0.7% | Global premium segments | Medium term (2-4 years) |

| Redundant Brake/Steer-by-Wire in AD Vehicles | +0.6% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of AT/CVT/DCT Gearboxes

The evolution of automotive transmission systems—from manual to automatic, continuously variable (CVT), and dual-clutch transmissions (DCT)—reflects a broader industry shift toward more sophisticated, electronically controlled drivetrains. This transition is driven by consumer demand for smoother driving experiences, improved fuel efficiency, and compatibility with hybrid and electric powertrains[1]“Automatic Transmission Control Systems,”, Robert Bosch GmbH, bosch.com.

Tighter Emission and Fuel-Economy Norms Spurring VVT/GDI Adoption

Euro 7 regulations push automakers to adopt advanced engine technologies like Variable Valve Timing (VVT) and Gasoline Direct Injection (GDI) to meet stricter emission and durability standards. These systems rely heavily on precision solenoids for fast, accurate fuel and valve timing control. As compliance deadlines approach (2026–2027), demand is rising for high-performance solenoids with features like oil-tight sealing and stroke sensing, making 2025–2027 a key supplier sourcing period [2]“Euro 7 Vehicle Emission Standards,”, European Commission, ec.europa.eu.

Cabin Smart-Actuator Boom (Active NVH and Comfort)

Based on accelerometer feedback, luxury automakers integrate active damping valves that adjust hydraulic orifices in milliseconds. Solenoids in these assemblies must deliver a microsecond response and low hysteresis to keep ride comfort metrics within +/-5 % of the target. Beyond suspension, smart actuators manage active engine mounts, zonal climate dampers, and haptic seat bolsters. The proliferation of comfort features lifts per-vehicle solenoid count and pushes suppliers to develop quieter, temperature-stable designs certified down to -40 °C.

Redundant Brake- & Steer-By-Wire Safety Circuits in AD Vehicles

Brake-by-wire systems replace mechanical components like the master cylinder with electronic boosters and pressure-modulating solenoids. Bosch is preparing to launch such a system that incorporates redundant safety features to meet stringent automotive safety standards.

Steer-by-wire technology follows a similar approach, using dual hydraulic assist mechanisms to ensure continued operation even in a failure. These innovations are part of a broader shift toward autonomous driving, which is increasing demand for highly reliable, diagnostics-enabled solenoids in the automotive sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solid-State Pumps Replace Valves in EV Platforms | -1.4% | Global EV markets, concentrated in premium segments | Long term (≥ 4 years) |

| OEMs Shift to Long-Life Piezo and Voice-Coil Actuators | -0.9% | Premium vehicle segments in developed markets | Medium term (2-4 years) |

| Copper Price Volatility Inflates Coil Costs | -0.8% | Global manufacturing, acute in Asia-Pacific production hubs | Short term (≤ 2 years) |

| High ASIL-D Compliance Costs for Small Suppliers | -0.6% | Europe and North America regulatory markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Solid-State Pumps Replacing Valves in Next-Gen EV Platforms

Research prototypes using electroactive polymers can modulate coolant flow with no moving parts, removing coil-wear failure modes intrinsic to solenoids. While today limited to bench tests, solid-state pumps appeal to high-end EV brands targeting minimal maintenance architectures. The technology could displace up to three valves per battery pack once volume maturity and cost parity arrive. For the foreseeable future, manufacturability constraints and the need for higher flow rates temper the immediate impact on the automotive solenoid valves market.

OEM Shift to Long-Life Piezo / Voice-Coil Actuators

Piezo stacks switch in under 1 ms, ten times faster than iron-core solenoids, offering pinpoint metering in fuel injection, while voice-coil designs give linear stroke without magnetic hysteresis. As cost curves drop, premium brands adopt piezo for high-pressure injection and adaptive ride systems. Voice-coil units are gaining traction in precision hydraulic circuits where proportional control is mandatory. The necessity for dedicated drive electronics and the entrenched tooling base for stamped solenoid cores slows widespread conversion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Type: Complexity Drives Multi-Port Demand

3-way valves captured 38.22% share in 2024, thanks to their ability to handle mixing and diverting tasks in engine cooling loops and HVAC mode doors. The 5-way category, although smaller, is forecast for an 8.61% CAGR as integrated thermal blocks combine charge-air, battery, and inverter cooling into a single housing. This evolution helps OEMs cut hose runs by 30% and save up to 2 kg per vehicle. Meanwhile, 2-way on-off valves persist in low-cost circuits such as windshield wash and evaporative purge, safeguarding basic unit volumes in the automotive solenoid valves market.

Multi-port integration also surfaces in fuel-system suction control modules where DENSO uses a single solenoid to orchestrate dual pumping stages. Suppliers capable of tight-tolerance zinc-die casting of valve bodies gain an edge because port misalignments over 30 µm can trigger NVH complaints. Lifecycle validation now stretches to 10 million cycles, twice the legacy requirement, reinforcing the need for proprietary coil insulation and wear-resistant seat materials.

By Application Type: Safety Systems Outpace Legacy Engine Uses

Body Control and Interiors remained the single largest application in 2024 with 29.11% share, fueled by luxury seating, zonal climate, and smart-lock uptake. Yet Safety and Security will grow fastest at 8.23% CAGR as autonomous-ready chassis migrate to brake-, steer-, and clutch-by-wire. A single brake control module incorporates up to seven shut-off and pressure-building solenoids, most with redundant winding and stroke sensor pickups.

Engine Control holds meaningful volume through VVT and exhaust-gas recirculation, but gradual ICE phase-out in Europe shifts emphasis to thermal management solenoids in battery packs and power electronics. High-pressure fuel and emission control applications remain valuable in North America and emerging markets where conversion to EVs lags. HVAC and Transmission round out demand, each mirroring global vehicle-production trends and a growing preference for electronically governed comfort systems.

By Operation Type: Pilot Designs Gain in Heavy-Duty Circuits

Direct-acting solenoids delivered 63.29% of 2024 revenue due to their low cost and sub-20 ms response. Pilot-operated versions, however, will climb at 8.35% CAGR to 2030 as heavy commercial vehicles adopt higher hydraulic pressures. A pilot valve uses a low-power coil to unblock a diaphragm, multiplying flow by up to 15× and enabling 75 l/min passage in power-steering or air-drier circuits. Advanced sensor-less feedback algorithms published by IEEE now allow pressure modulation with standard direct-acting coils, but OEMs still gravitate toward pilot solutions for durability margins.

The medium-term trajectory, therefore, calls for hybrid modules combining direct-acting vent valves with pilot-controlled main stages, especially in e-axle oil circuits where packaging space remains tight. Thermal-rise mitigation becomes critical as engine-bay ambient reaches 150 °C in turbocharged layouts, prompting PEEK bobbin adoption for 180 °C continuous-temperature ratings

By Vehicle Type: Passenger Cars Remain Volume King

Passenger Cars supplied 53.31% of 2024 demand and will expand at 9.42% CAGR, fueled by Chinese and Indian production growth and richer content per vehicle. Eight-speed automatics now appear in B-segment hatchbacks, instantly raising hydraulic solenoid count. Light Commercial Vehicles benefit from the e-commerce boom; last-mile vans employ four-zone HVAC requiring added mode valves, pushing LCV content toward 25 valves per unit. Heavy Commercial Vehicles and Buses follow regulatory timelines on diesel after-treatment; each Euro VI SCR system uses multiple dosing valves alongside DEF level sensors, maintaining a resilient baseline within the automotive solenoid valves market.

By Sales Channel: OEMs Dominate but Aftermarket Stakes Rise

OEM purchasing captured a 73.21% share in 2024 and should post a 9.28% CAGR because platform design locks in solenoids for 5–7 years. Component traceability, ISO 26262 documentation, and software calibration cement Tier-1 relationships. Continental’s plan to launch 700 new aftermarket SKUs by 2025 underscores efforts to tap replacement demand once warranty periods lapse. Aftermarket growth also stems from rising fleet awareness of preventive valve replacement to avoid EV coolant leaks that could trigger thermal runaways. However, fitment complexity limits independent workshops’ capability, keeping OEM service networks central for advanced latching products.

Geography Analysis

Asia-Pacific retained a 48.62% share in 2024 and is forecast to have an 8.35% CAGR to 2030. China’s 31.28 million-unit light-vehicle output, plus 12.87 million NEV registrations, drives colossal demand for battery-loop valves, proportional expanders, and air-damping actuators. India’s 4 million-unit production benefits from tax incentives on AT gearboxes that double solenoid counts versus manuals. Thailand and Vietnam contribute with export-oriented ICE trucks needing EGR and SCR dosing valves, broadening the regional scope for the automotive solenoid valves market.

Europe commands leading technology adoption because Euro 7 compels sophisticated VVT oil-control valves and high-pressure GDI injectors. German OEMs spearhead brake-by-wire deployment, each car containing eight safety-rated solenoids with dual windings. Eastern European plants are adding local coil-winding lines to mitigate supply-chain risk, supported by EU funding for critical components.

North America focuses on pickup, SUV, and Class 8 truck platforms. United States and Canadian fleets adopt variable-displacement oil pumps managed by solenoid valves to meet Corporate Average Fuel Economy targets. The new Mexico–United States–Canada Agreement encourages nearshoring, prompting tier-1s to expand coil-molding capacity in Monterrey.

South America, the Middle East, and Africa collectively provide a smaller but accelerating base. Brazil mandates PROCONVE L8 emissions in 2025, raising demand for canister purge and injector metering solenoids. Gulf Cooperation Council states show uptake of active comfort features in luxury imports, lifting body-control valve demand.

Competitive Landscape

The market remains moderately fragmented. Bosch has broad system knowledge from powertrain to chassis, enabling cross-functional packages such as combined brake-by-wire actuators. Continental leverages ADAS integration to supply solenoids calibrated for sensor-fusion brake controllers. DENSO capitalizes on Japanese OEM alliances, fielding fuel-pump integrated suction valves that shorten rail fill times.

Mid-tier competitors like BorgWarner and HITACHI Astemo pursue niche leadership in high-speed gearbox shift valves, whereas Chinese specialists, including Zhejiang Sanhua Electronics, focus on price-competitive HVAC diverters. Start-ups develop MEMS feedback for stroke monitoring, offering predictive maintenance hooks into OEM cloud platforms. Patent filings increasingly target coil geometry that cuts inductance while keeping force, or magnetic-flux rings that hold armatures without auxiliary springs.

Strategically, suppliers move up the value chain. Bosch’s brake-by-wire module incorporates all eight solenoids, control logic, and safety firmware, billed as a single SKU to OEMs, locking out stand-alone valve vendors. Continental’s aftermarket expansion diversifies revenue to hedge ICE wind-down. Cooperative ventures arise: Cebi licenses residual-magnet latching to Asian coil-molders, while TDK supplies piezo stacks for hybrid fuel systems, positioning to capture share if electromagnetic demand tapers.

Automotive Solenoid Industry Leaders

Robert Bosch GmbH

Continental AG

DENSO Corporation

BorgWarner Inc.

Mitsubishi Electric Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zavolzhsky Motor Plant began producing improved cylinder heads with redesigned valve covers for next-generation UAZ models.

- February 2025: Bosch launched its brake-by-wire system for passenger cars, removing hydraulic links and relying on dual-redundant solenoid actuators for fail-safe pressure control.

Global Automotive Solenoid Market Report Scope

| 2-Way Valve |

| 3-Way Valve |

| 4-Way Valve |

| 5-Way Valve |

| Others |

| Engine Control & Cooling System |

| Fuel & Emission Control |

| Body Control & Interiors |

| Safety & Security |

| HVAC Systems |

| Transmission Systems |

| Direct Acting |

| Pilot Operated |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Heavy Commercial Vehicles (HCVs) |

| Buses & Coaches |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Valve Type | 2-Way Valve | |

| 3-Way Valve | ||

| 4-Way Valve | ||

| 5-Way Valve | ||

| Others | ||

| By Application Type | Engine Control & Cooling System | |

| Fuel & Emission Control | ||

| Body Control & Interiors | ||

| Safety & Security | ||

| HVAC Systems | ||

| Transmission Systems | ||

| By Operation Type | Direct Acting | |

| Pilot Operated | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Heavy Commercial Vehicles (HCVs) | ||

| Buses & Coaches | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the automotive solenoid valves market expected to grow through 2030?

It is projected to expand from USD 5.61 billion in 2025 to USD 7.78 billion by 2030, translating into a 6.74% CAGR.

Which region contributes nearly half of global demand?

Asia-Pacific delivers 48.62% of 2024 revenue, led by China’s 31.28 million-unit vehicle output and India’s accelerating passenger-car production.

What is driving safety-related valve adoption?

The shift to brake- and steer-by-wire architectures in autonomous-ready vehicles elevates demand for ISO 26262 ASIL-D-rated solenoid valves.

Why are latching solenoids gaining traction in EVs?

They draw power only during switching, cutting thermal-management energy losses by up to 80% and adding measurable driving range.

Which valve type shows the highest growth rate?

5-way multi-port valves are forecast for an 8.61% CAGR due to their role in integrated thermal management and advanced transmission circuits.

Page last updated on: